Dental Syringes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

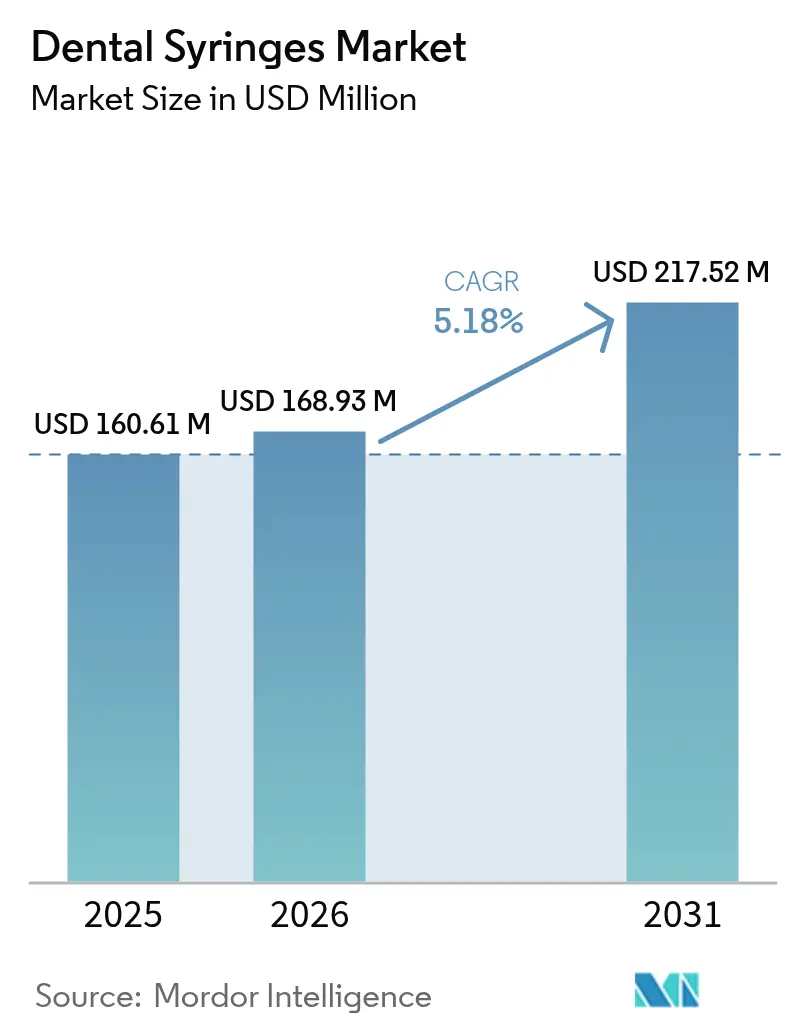

| Market Size (2026) | USD 168.93 Million |

| Market Size (2031) | USD 217.52 Million |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dental Syringes Market Analysis by Mordor Intelligence

The dental syringes market size is expected to grow from USD 160.61 million in 2025 to USD 168.93 million in 2026 and is forecast to reach USD 217.52 million by 2031 at 5.18% CAGR over 2026-2031. Growth reflects tighter infection-control requirements, a wider older-adult population needing prosthodontic care, and the steady roll-out of computer-controlled local anesthetic delivery systems. Heightened awareness after recent global health events has moved dentists toward single-use devices and RFID-tracked instruments that simplify compliance with CDC sterilization rules. Insurers are also influencing demand: 65% of U.S. adults held dental coverage in 2024 and 91% now view dental check-ups as essential preventive care. On the supply side, manufacturers are redesigning products around biodegradable plastics and lightweight metals to meet the upcoming EU Packaging and Packaging Waste Regulation. Tariffs introduced in April 2025 and volatile stainless-steel supply chains are prompting practices to diversify sourcing and accelerate group purchasing.

Key Report Takeaways

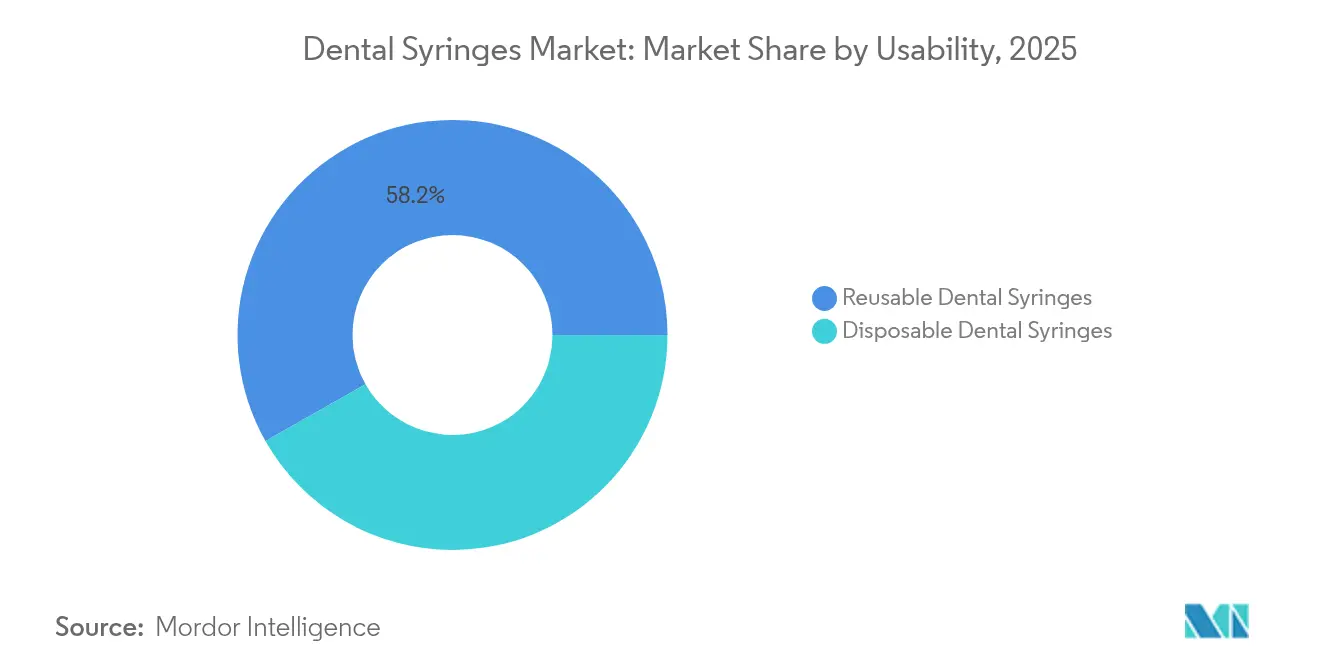

- By usability, reusable devices held 58.20% of dental syringes market share in 2025 while disposables are projected to expand at a 6.28% CAGR through 2031.

- By product type, aspirating models led with 61.55% revenue share in 2025 while non-aspirating units are forecast to grow at 6.12% CAGR.

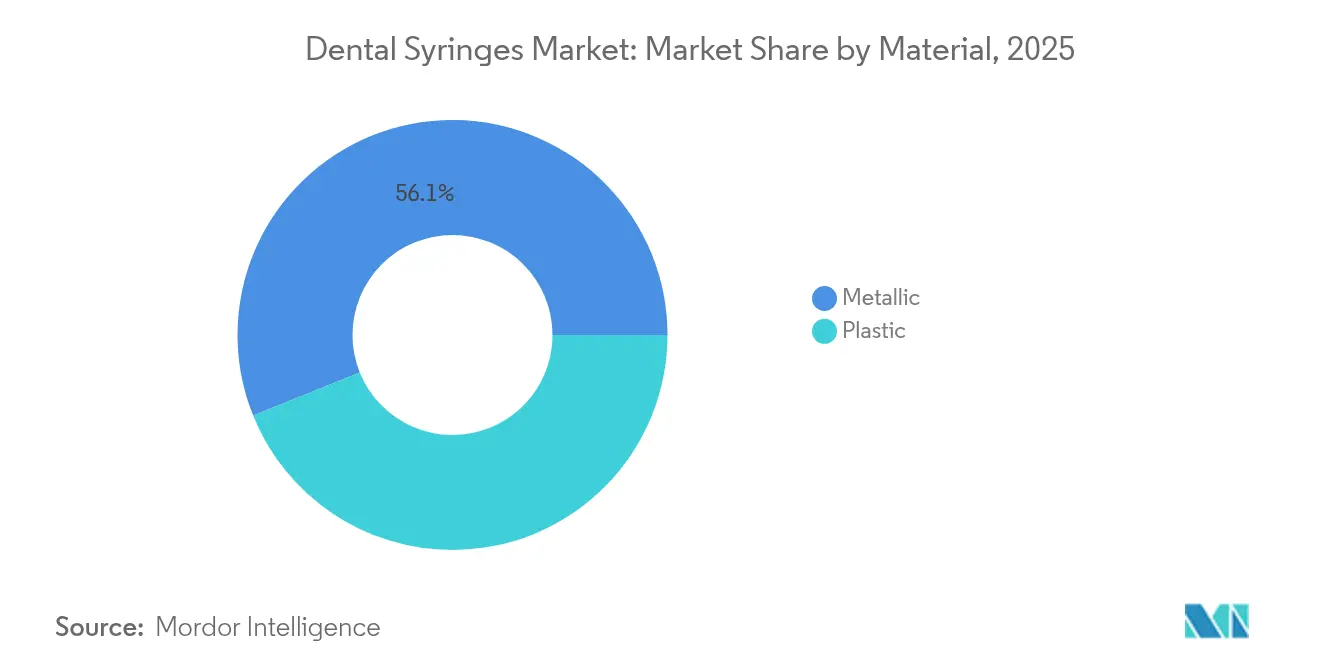

- By material, metallic formats accounted for 56.10% of the dental syringes market size in 2025 and plastics are advancing at a 6.05% CAGR to 2031.

- By end-user, hospitals and clinics commanded 49.10% of the 2025 revenue while laboratories are poised for the fastest 6.01% CAGR.

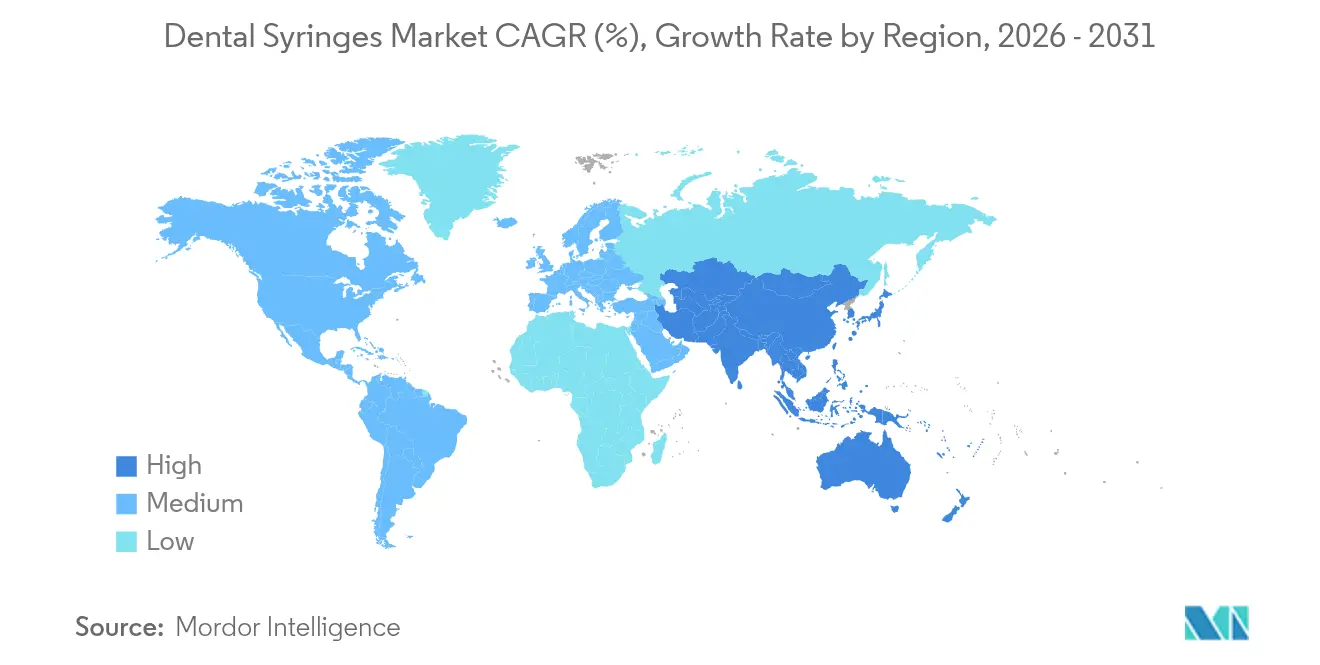

- By geography, North America contributed 43.10% revenue in 2025 while Asia-Pacific is projected to post the highest 6.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Syringes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population expanding prosthodontic workload | +1.2% | North America and Europe core, global spill-over | Long term (≥ 4 years) |

| Rising prevalence of caries & periodontal disease | +0.9% | Higher impact across Asia-Pacific and MEA | Medium term (2-4 years) |

| Rapid shift to single-use safety syringes | +1.4% | Led by North America and EU | Short term (≤ 2 years) |

| Growth in dental tourism across APAC & CEE | +0.7% | Asia-Pacific core, Central and Eastern Europe spill-over | Medium term (2-4 years) |

| Chair-side digital anesthesia delivery | +0.8% | North America and EU early adopters, APAC emerging | Medium term (2-4 years) |

| RFID-enabled instrument tracking mandates | +0.3% | High-income clinics in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Expanding Prosthodontic Workload

Adults aged 60 and older already number 1.0 billion and will pass 1.4 billion by 2030. Prosthodontic interventions that dominate this cohort demand precise anesthetic delivery, pushing clinics to adopt advanced dental syringes market solutions such as computer-controlled local anesthetic devices [1]Rakhee Patel, "Healthy ageing and oral health: priority, policy and public health," BDJ Open, nature.com. In Malaysia, adults aged 25-54 form the largest patient group, further straining chair capacity. Dental insurers highlight the link between oral and systemic health, driving preventive visits and reinforcing demand for premium syringes. Practices consequently prefer ergonomic designs that perform multiple injections without user fatigue. As full-arch restorations rise, syringe designs featuring high barrel clarity and controlled aspiration are becoming standard [2]Delta Dental Plans Association, “State of America’s Oral Health and Wellness Report 2024,” deltadental.com .

Rising Prevalence of Caries & Periodontal Disease

More than 280 million older adults face untreated caries or gum disease worldwide. Updated CDC guidelines stipulate that cartridge syringes must be sterilized between patients and that needles as well as anesthetic cartridges remain single use [3]Centers for Disease Control and Prevention, “CDC Summary of Infection Prevention Practices in Dental Settings,” cdc.gov . Emerging economies report faster disease incidence due to sugary diets and limited prophylaxis, opening space for cost-effective yet compliant syringes. Teledentistry is enabling earlier diagnosis among younger adults, creating more occasions for minimally invasive restorations that still need local anesthesia. Early-stage interventions such as drill-free cavity repair delivered by products like Curodont Repair Fluoride Plus lower chair time, but complex cases continue to rely on aspirating devices that confirm safe deposition.

Rapid Shift to Single-Use Safety Syringes for Infection Control

The CDC states that single-use instruments “should not be reprocessed” which is accelerating the switch to disposables. Pac-Dent’s TruTip Plus Colors and NeoTip lines illustrate how manufacturers integrate stainless-steel interiors with color-coded plastic exteriors to maintain stiffness while easing disposal. Studies demonstrate that reusable tips retain bacterial load despite sterilization, reinforcing the move to disposables. The EU regulation that all healthcare packaging must be recyclable by 2030 is catalyzing R&D into PLA and PHA syringes that biodegrade without compromising performance. Dental syringes market suppliers are balancing shelf-life, cost, and sustainability as clinics weigh infection control against waste targets.

Growth in Dental Tourism Across APAC & CEE

Malaysia’s oral-care blueprint positions the country as a dental tourism hub by 2027 and prioritizes premium anesthesia delivery to reassure visiting patients. Romanian clinics partner with travel agencies to extend peak seasons and attract complex restorative cases that rely on high-precision syringes. International clients expect U.S. or EU-level infection protocols, prompting facilities to use single-use aspirating devices packaged in tamper-evident pouches. Clinics also integrate chair-side CAD/CAM workflows, so syringe suppliers bundle disposables with scanners and implant kits to capture downstream revenue within the dental syringes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled dentists in low-income regions | -0.8% | Asia-Pacific, MEA, rural zones worldwide | Long term (≥ 4 years) |

| Up-front cost of electronic & smart syringes | -0.6% | Higher pressure in price-sensitive markets | Medium term (2-4 years) |

| Regulatory crackdown on single-use plastics | -0.4% | EU first movers and eco-focused markets | Medium term (2-4 years) |

| Volatile supply of medical-grade stainless steel | -0.3% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Dentists in Low-Income Regions

Many emerging economies record fewer than one dentist per 10,000 residents. The WHO notes that geographic and economic barriers keep older adults from timely care. Limited training capacity delays the uptake of advanced computer-controlled devices that require instruction on aspiration and flow-rate settings. Governments respond by funding mobile clinics but focus spending on basic instruments. In turn, syringe makers supply simplified metallic formats that tolerate rugged reprocessing and align with thin operating budgets inside the dental syringes industry.

Up-Front Cost of Electronic & Smart Syringes

Systems such as the STA or Wand can cost several thousand dollars, which smaller practices may not recoup quickly. The 10% tariff applied to U.S. imports in April 2025 further inflates equipment price tags. Some clinics arrange vendor financing or group-buy schemes, though rising interest rates raise total ownership costs. Suppliers have introduced modular upgrades so dentists can start with manual aspirating handles and later add digital control boxes without discarding prior investment. These tiered packages shape adoption trajectories in the dental syringes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usability: Disposables Gain Infection Control Momentum

Reusable devices retained 58.20% revenue in 2025, benefiting from well-established autoclave infrastructures. In the same year disposables grew swiftly as the dental syringes market size for single-use formats recorded a 6.28% CAGR, reflecting heightened infection control vigilance. Practices with patient loads exceeding 30 daily injections cite sterilizer bottlenecks, thus preferring color-coded disposable barrels that cut turnaround time.

Disposable adoption faces environmental scrutiny; the EU framework compels recyclable packaging by 2030, prompting suppliers to launch PLA and PHA barrels that meet compostability targets. Large group practices lock in multi-year contracts to stabilize pricing and guarantee supply. Reusables still dominate where capital budgets cover advanced washer-disinfectors and where unit cost savings outweigh staffing constraints. Hybrid strategies emerge, with clinics using metallic aspirating handles paired with single-use needles and cartridges to balance safety and sustainability.

By Product Type: Aspirating Dominance Faces Digital Disruption

Aspirating models captured 61.55% of dental syringes market share in 2025 because they allow clinicians to verify they are not in a blood vessel before injecting. Non-aspirating designs appeal to younger practitioners seeking simpler handling during routine composites and prophylaxis.

Digital CCLAD platforms incorporate pressure sensors that can identify tissue differences without manual aspiration. When paired with narrow-gauge needles, these systems deliver near-painless infiltration which is expanding patient acceptance in elective cosmetic work. Needle-free devices such as LED-based Nuralyte promise further disruption; however, indications remain limited to shallow treatments and adoption hinges on upcoming FDA clearance. Traditional aspirating syringes now integrate silicone coating and reduced plunger friction to maintain relevance within an evolving dental syringes market.

By Material: Metallic Strength Versus Plastic Innovation

Metallic barrels secured 56.10% revenue in 2025 thanks to their durability and autoclave compatibility. Supply challenges for specialty stainless steel have triggered a switch to hardened aluminum and titanium blends that shave grip weight by 25% without sacrificing rigidity.

Plastics advance at a 6.05% CAGR, lifted by cost advantages and growth in single-use protocols. Bioplastics win regulatory favor yet face output limitations, leading manufacturers to blend PLA with recycled PET for wider availability. Future designs may feature composite interiors lined with thin steel sleeves to deliver metal-like aspiration while reducing raw steel content. Material innovation enables competitive pricing and differentiates brands in the dental syringes market.

By End-User: Laboratories Emerge as Growth Catalyst

Hospitals and clinics held 49.10% revenue in 2025 due to their direct patient interface. Dental laboratories post the highest 6.01% CAGR because chair-side milling and immediate prosthetic services now demand on-site anesthesia capability.

Lab-integrated digital workflows rely on fast setting times, so staff prefer syringes with pre-threaded needles and calibrated cartridges that minimize interruptions. Academic programs adopt premium aspirating handles for student instruction, fueling baseline demand. The rise of dental service organizations centralizes purchasing which favors vendors able to bundle syringes with burs, imaging sensors, and CAD/CAM blocks leading to consolidated volume within the dental syringes market size for multi-disciplinary institutions.

Geography Analysis

North America generated 43.10% of 2025 revenue as stringent CDC protocols and widespread insurance coverage sustained premium device uptake. Computer-controlled systems are common in large group practices, and 91% of adults equate dental visits with annual physicals which underpins procedure volumes. Tariffs imposed in April 2025 raise equipment costs so distributors diversify toward Mexico and Vietnam sources to maintain catalog breadth. Solventum, spun off from 3M, posted USD 335 million in Q1-2024 dental solutions sales in spite of a 1.8% revenue dip, demonstrating resilience in the regional dental syringes market.

Asia-Pacific is the fastest-growing territory with a 6.22% CAGR to 2031. Malaysia illustrates the trend: a USD 2.8 billion dental services sector by 2027 with private clinics holding 70% share. Rising middle-class incomes boost demand for cosmetic orthodontics and implantology, both reliant on accurate local anesthesia. Dental tourism blends hotel-style recovery suites with EU-compliant infection protocols, leading facilities to favor single-use aspirating syringes packaged in bar-coded peel pouches. Domestic manufacturers supply cost-efficient polystyrene barrels while importers market premium CCLAD units, creating tiered opportunities inside the dental syringes market.

Europe maintains consistent growth as the circular-economy agenda reshapes material selection. The EU Packaging and Packaging Waste Regulation forces producers to redesign components for recyclability by 2030. Germany pilots municipal collection of clinical-grade bioplastics, giving early movers brand advantage. Clinics in France and Scandinavia advertise carbon-neutral restorations which in turn favor PLA or PHA syringe bodies. Eastern Europe gains momentum from inbound dental tourists seeking affordable full-arch implants, driving mid-range aspirating device sales. The Middle East and Africa record accelerating demand, especially in GCC countries that pair medical tourism with luxury hospitality. South America exhibits incremental gains, with Brazil and Argentina leveraging local plastics production to stabilize supply chains within the dental syringes market.

Competitive Landscape

The dental syringes market is moderately fragmented. Global multinationals compete with specialist brands, each vying to differentiate through infection-control features, ergonomic enhancements, and digital integration. Solventum re-entered the segment as an independent healthcare company in April 2024 and now allocates more capital to R&D for biodegradable disposables. Dentsply Sirona leverages its imaging and milling portfolio to cross-sell syringes bundled with CAD/CAM kits, reinforcing ecosystem lock-in.

Manufacturers invest 3–5% of revenue on supply-chain resilience after stainless-steel and resin shortages highlighted vulnerabilities. Additive manufacturing is used to prototype low-friction plungers and lightweight grips that cut material use by 15%. Companies also integrate generative AI to optimize demand forecasts and shrink inventory buffers. Niche firms develop needle-free solutions such as LED or TENS-based anesthesia devices which could cannibalize simple infiltration uses but still coexist with aspirating syringes for surgical work. Regulatory clarity improved after the ADA proposed ANSI/ADA Standard No. 34 aligning cartridge syringes with ISO 9997:2020; conforming early gives suppliers marketing leverage.

Strategic alliances rise as vendors collaborate with packaging converters to co-design recyclable blister packs that pass accelerated aging tests. Some brands pilot pay-per-use contracts where practices pay on injection count rather than upfront equipment purchase. The practice offers predictable cash flow for clinics and deeper user data for suppliers, reinforcing stickiness within the dental syringes market.

Dental Syringes Industry Leaders

-

Dentsply Sirona

-

A. Titan Instrument Inc

-

Septodont

-

Solventum

-

Ultradent Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: American Dental Association released the draft ANSI/ADA Standard No. 34 that harmonizes with

- June 2024: Pac-Dent launched TruTip Plus Colors and NeoTip disposable air/water syringe tips with stainless-steel interiors to improve rigidity.

- April 2024: 3M completed the spin-off of Solventum which now manages the Dental Solutions portfolio as an independent entity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global dental syringes market as revenues generated from handheld instruments used by dentists to deliver local anesthetics or irrigants during diagnostic, restorative, or surgical procedures, covering aspirating, non-aspirating, computer-controlled, reusable, and single-use formats sold through dental supply channels.

Scope Exclusions: Veterinary injectors, oral-medicine training dummies, and general medical or oral-dosing syringes sit outside this assessment.

Segmentation Overview

-

By Usability

- Reusable Dental Syringes

- Disposable Dental Syringes

-

By Product Type

- Aspirating

- Non-aspirating

-

By Material

- Metallic

- Plastic

-

By End-User

- Dental Hospitals & Clinics

- Dental Laboratories

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed practicing endodontists, procurement leads at multi-site clinics across North America, Europe, Asia-Pacific, and Latin America, plus product managers at syringe manufacturers. Short distributor surveys clarified inventory turns, safety-syringe adoption, and current-year average selling prices, helping us confirm and fine-tune model inputs.

Desk Research

We screened open datasets from the WHO oral-health unit, UN Comtrade trade code HS-960810, and U.S. FDA 510(k) clearances, then matched them with OECD health accounts and statistics released by the American Dental Association and FDI World Dental Federation. Mordor analysts next mined company 10-Ks, investor decks, and distributor catalogs to map price ladders and mix shifts. Subscription resources such as D&B Hoovers and Dow Jones Factiva filled gaps on financial footprints and shipment news. This list illustrates the backbone; many further sources informed validation and context.

A second pass aligned epidemiological baselines with regional procedure volumes, ensuring demand signals tied back to observable data rather than generic healthcare spending.

Market-Sizing & Forecasting

A blended top-down reconstruction of production and trade flows is corroborated with selective bottom-up supplier roll-ups and clinic volume × ASP checks. Key variables feeding the multivariate regression model include active dentist headcount, anesthetic cartridge consumption per procedure, shift toward safety designs, regional price ladders, and currency movements. Scenario analysis adjusts projections when regulations or technology adoption accelerate beyond trend.

Data Validation & Update Cycle

Outputs undergo variance checks against independent procedure tallies before a second Mordor analyst reviews formulas. We refresh every twelve months and trigger interim updates when recalls, guideline shifts, or foreign-exchange swings breach preset thresholds.

Why Mordor's Dental Syringes Baseline Commands Confidence

Published estimates often diverge because research firms pick different product baskets, price anchors, and refresh moments.

Key gap drivers include bundling of general medical injectors, reliance on list prices without volume weighting, exclusion of emerging economies, or focusing solely on computer-controlled units. These choices can inflate or deflate totals relative to Mordor's transparent, procedure-level build-up.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 160.61 Mn (2025) | Mordor Intelligence | - |

| USD 11.21 Bn (2025) | Global Consultancy A | Combines dental, medical, and veterinary injectors; limited price validation |

| USD 652.7 Mn (2024) | Regional Consultancy B | Uses catalog prices and omits several emerging markets |

| USD 12.55 Mn (2025) | Industry Journal C | Counts only computer-controlled units, ignores clinic reuse |

These contrasts show how our disciplined variable selection and yearly refresh give decision-makers a grounded, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the dental syringes market?

The dental syringes market was valued at USD 168.93 million in 2026 and is projected to reach USD 217.52 million by 2031 at a 5.18% CAGR.

Which region leads the dental syringes market?

North America leads with 43.10% revenue thanks to strict CDC protocols and widespread insurance coverage.

Why are disposable dental syringes gaining popularity?

Disease-control guidelines from the CDC mandate that single-use devices should not be reprocessed, prompting clinics to adopt disposable syringes that reduce cross-contamination risk.

What share do aspirating syringes hold?

Aspirating models captured 61.55% of dental syringes market share in 2025 because they allow clinicians to verify safe injection sites.

How will environmental regulations influence product design?

EU rules requiring recyclable packaging by 2030 are accelerating the shift toward PLA and PHA bioplastics and motivating manufacturers to redesign components for circularity.

What is the fastest-growing end-user segment?

Dental laboratories are the fastest-growing end-user, expanding at a 6.01% CAGR as chair-side digital workflows integrate anesthesia delivery into lab services.

Page last updated on: