Market Overview

| Study Period | 2020 - 2031 |

|---|---|

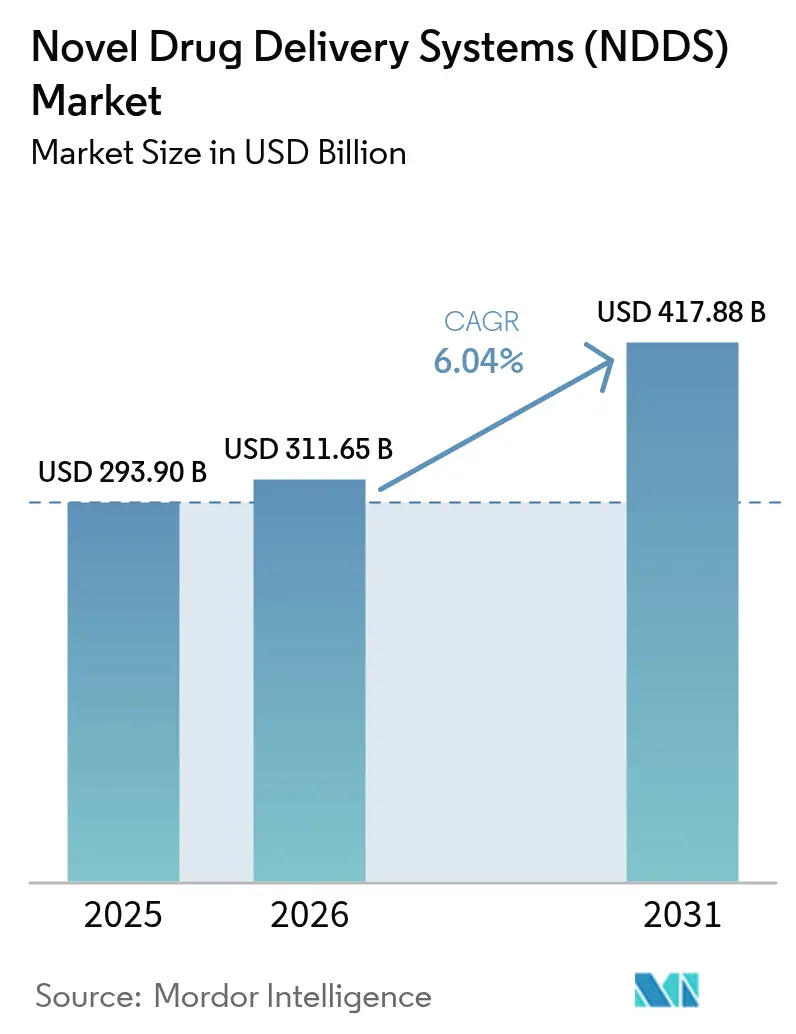

| Market Size (2026) | USD 311.65 Billion |

| Market Size (2031) | USD 417.88 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

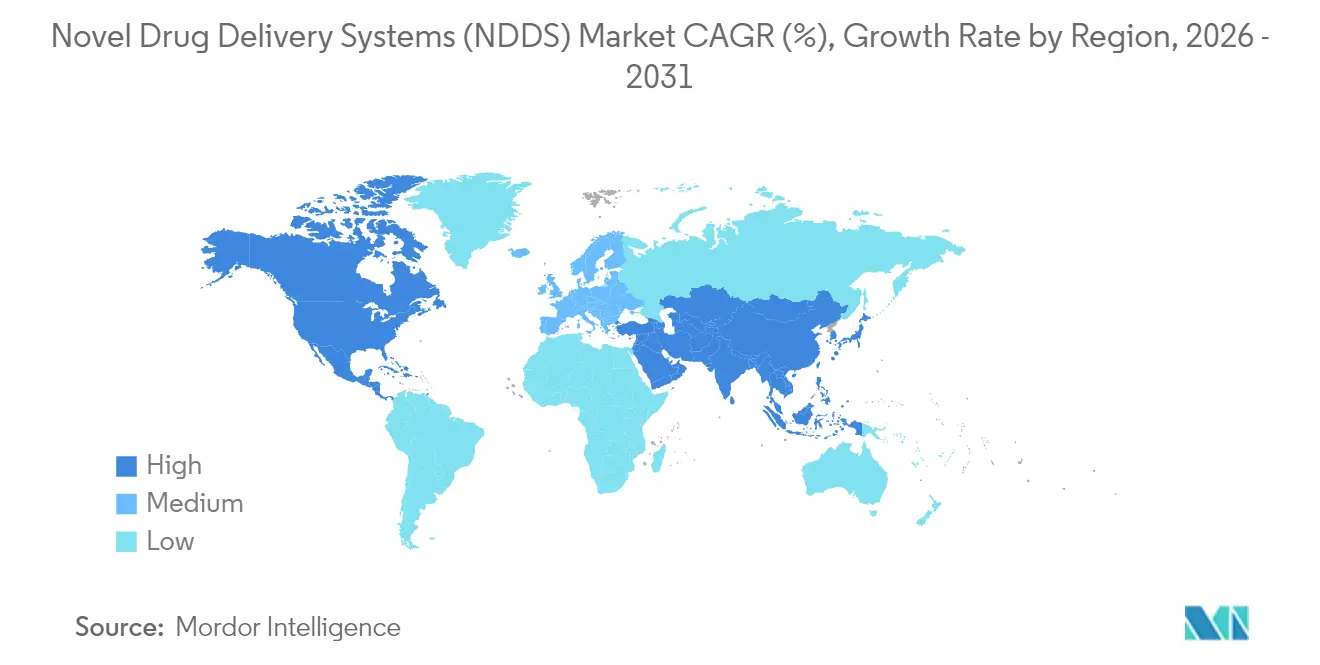

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Novel Drug Delivery Systems (NDDS) Market Analysis by Mordor Intelligence

New Drug Delivery Systems market size in 2026 is estimated at USD 311.65 billion, growing from 2025 value of USD 293.9 billion with 2031 projections showing USD 417.88 billion, growing at 6.04% CAGR over 2026-2031. An acceleration in patient-centric therapeutics, the clinical shift toward biologics and gene therapies, and the convergence of connected health technologies collectively propel this trajectory. Heightened demand for self-administration devices, ongoing regulatory support for combination products, and rising ventures in smart delivery platforms sustain competitive momentum. Strategic acquisitions—such as Novo Nordisk’s purchase of Catalent—signal intensifying competition for advanced formulation know-how. Meanwhile, sustainability requirements in Europe are nudging vendors toward recyclable packaging that maintains temperature integrity.

Key Report Takeaways

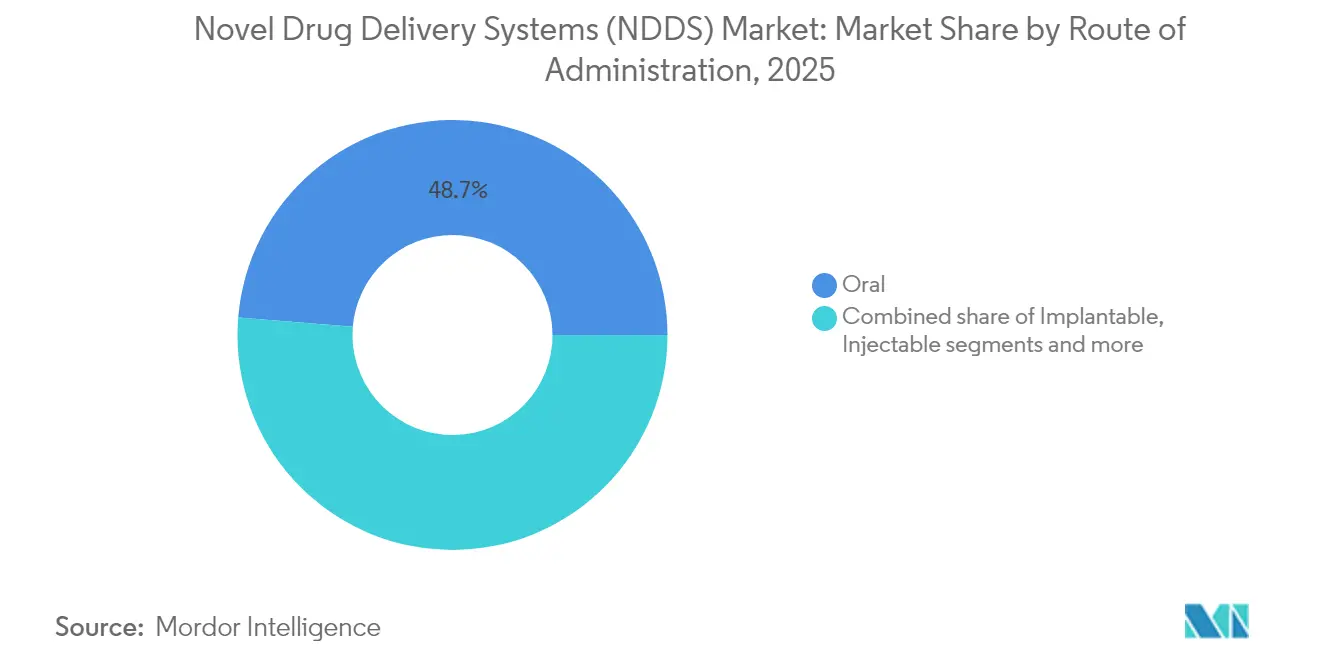

- By route of administration, oral systems led with 48.70% revenue share in 2025; implantable systems are projected to grow at a 8.72% CAGR through 2031.

- By technology, auto-injectors captured 22.05% of the New Drug Delivery Systems market size in 2025, whereas smart and connected devices are forecast to advance at 9.18% CAGR between 2026-2031.

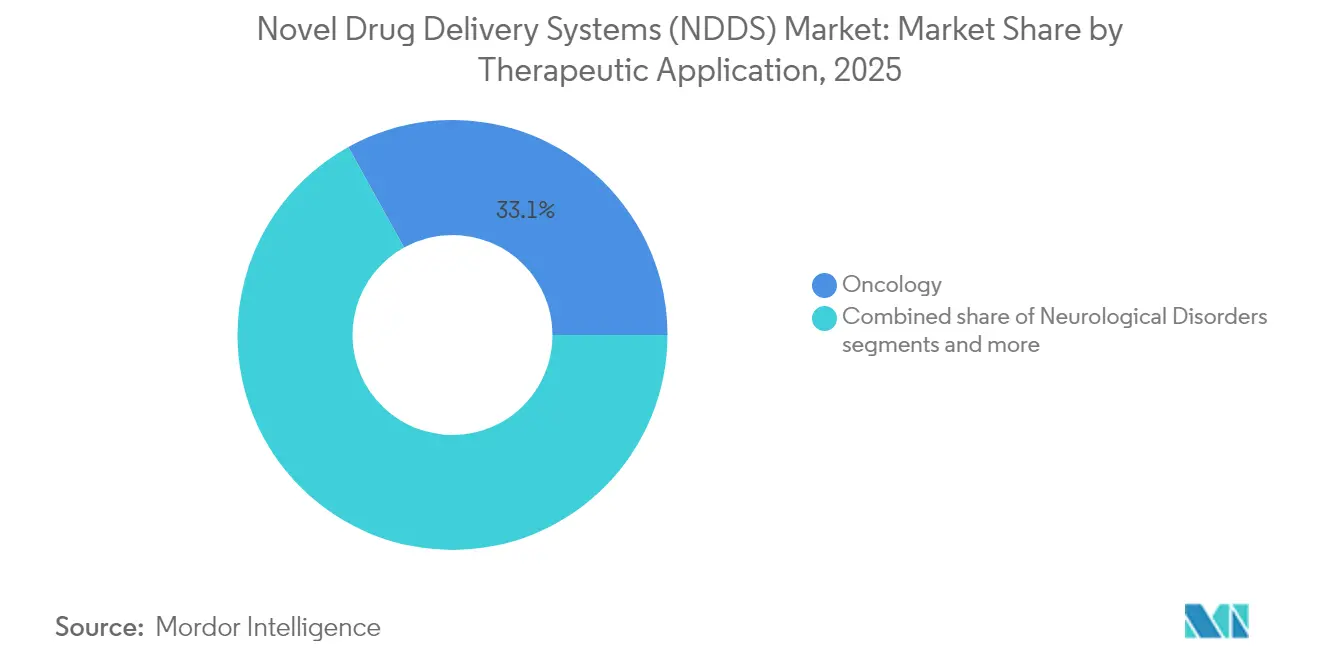

- By therapeutic application, oncology generated 33.05% share of the New Drug Delivery Systems market size in 2025, while neurological disorder applications are poised for a 9.36% CAGR through 2031.

- By end user, hospitals accounted for 53.10% of New Drug Delivery Systems market share in 2025; home-care settings are expected to expand at 10.12% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Novel Drug Delivery Systems (NDDS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.5% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growing adoption of biologics & large-molecule drugs | +2.1% | North America & EU leading, APAC accelerating | Long term (≥ 4 years) |

| Digital-therapeutic integration enabling smart delivery | +1.8% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Expansion of mRNA / gene-therapy pipelines | +1.2% | North America & EU, selective APAC markets | Long term (≥ 4 years) |

| Patient preference for self-administration & home care | +0.9% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Decarbonization push favoring long-acting formulations | +0.7% | EU leading, North America following, APAC emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Cardiovascular and diabetic conditions affected more than 1.23 billion people globally in 2024 and continue to swell clinical demand for sustained-release therapies that reduce dosing frequency[1]Source: World Health Organization, “Cardiovascular diseases (CVDs),” who.int . Long-acting platforms such as the intravesical TAR-200 device illustrate this shift, delivering gemcitabine continuously over multiple months and achieving median response duration of 25.8 months, markedly higher than intermittent regimens. Regulators respond with guidance that favors integrated drug–device products able to improve adherence, reinforcing investment in implantable and transdermal formats.

Growing Adoption of Biologics & Large-Molecule Drugs

Escalation in monoclonal antibodies and RNA-based therapeutics elevates formulation complexity and stimulates nanoparticle innovation. Pfizer’s ponsegromab trial underscores the benefit—optimized delivery improved performance in cancer cachexia patients. Vendors consequently expand lipid nanoparticle capacity; Lonza added multiple dedicated suites in 2025 to ease supply shortages. Cold-chain logistics and patient ease-of-use remain critical, widening prospects for temperature-controlled packaging and self-injecting wearables.

Digital-Therapeutic Integration Enabling Smart Delivery

Connected devices advance from passive dispensing toward continuous data capture. Global revenue for smart delivery systems approached USD 12 billion in 2024. FDA cybersecurity guidelines released in 2024 impose secure-by-design requirements, prompting early-stage redesigns but ensuring long-term patient safety[2]Source: U.S. Food and Drug Administration, “Cybersecurity in Medical Devices: Refuse to Accept policy,” fda.gov . Artificial intelligence embedded in injectors and inhalers now supports algorithm-directed dose titration.

Expansion of mRNA / Gene-Therapy Pipelines

More than 200 gene-therapy trials launched in 2024, accentuating the bottleneck in vector and LNP capacity. Cytiva, Lonza and other suppliers committed multi-million-unit plants to satisfy projected demand to 2030. Tissue-targeting challenges and immunogenicity concerns sustain R&D in novel capsids and biodegradable carriers, while regulatory agencies maintain rigorous safety thresholds for viral or non-viral vectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent combination-product regulations | -1.8% | Global, most restrictive in EU & North America | Medium term (2-4 years) |

| High device cost in LMICs | -1.1% | APAC, Latin America, MEA primarily | Long term (≥ 4 years) |

| Cyber-security risk in connected injectors | -0.9% | North America & EU core, expanding globally | Short term (≤ 2 years) |

| Limited LNP manufacturing capacity | -0.7% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Combination-Product Regulations

Revised FDA and EMA guidelines require exhaustive drug–device interaction studies, inflating budgets by as much as USD 100 million and extending timelines up to two years. J&J secured Breakthrough Therapy Designation for TAR-200 yet still navigated extensive post-market commitments, highlighting the difficulty for smaller innovators. Divergent regional rules further complicate global launches.

High Device Cost in LMICs

Connected auto-injectors and implantables cost 10-20 times more than oral generics, limiting access in resource-constrained regions. Procurement agencies in Latin America and Africa require localized manufacturing or tiered pricing; however, limited regulatory capacity delays approvals for sophisticated devices. Companies are piloting simpler, single-function variants to lower cost while preserving core therapeutic benefit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Oral Dominance Faces Digital Disruption

Oral therapies commanded 48.70% of New Drug Delivery Systems market share in 2025, yet growth moderates as digital implants and long-acting injectables demonstrate superior adherence. Implantable formats are projected to deliver a 8.72% CAGR to 2031, supported by breakthroughs such as Vivani Medical’s GLP-1 implant that filled its first human study in four weeks. Injectable routes benefit from the biologics wave, while inhaled delivery attracts neurological and respiratory pipeline investments.

Patient preference, manufacturing scalability and reimbursement convenience underpin oral system resilience through 2030. However, smart pill sensors and micro-fluidic implants that log dosing create fresh value propositions for chronic disease management. Nasal and ocular options prosper in niche neurological and ophthalmic settings. Ultimately, route selection is increasingly dictated by molecular characteristics and personalized care models rather than historical convenience.

By Technology/System Type: Smart Connectivity Reshapes Traditional Platforms

Auto-injectors retained 22.05% share of the New Drug Delivery Systems market size in 2025 on entrenched supply chains and clinician familiarity. Smart and connected devices, however, are advancing at a 9.18% CAGR as cloud-linked patches and app-integrated pens transform medication into data streams. Nanoparticle carriers, essential for mRNA therapeutics, underpin capacity expansions at Lonza and similar CDMOs.

Needle-free jet injectors reduce vaccination anxiety and speed mass-immunization programs, while microneedle patches gain traction in dermatology and vaccine delivery. Wearable infusers capable of delivering 5-50 mL biologics at home remove infusion-center bottlenecks. The technology race increasingly favors modular platforms adaptable across molecules, thereby compressing development cycles and enhancing portfolio ROI.

By Therapeutic Application: Oncology Leadership Challenged by Neurological Innovation

Oncology contributed 33.05% of New Drug Delivery Systems market revenue in 2025, supported by antibody–drug conjugates, radiopharmaceuticals and device-enabled intratumoral therapies. J&J’s pasritamig showcased early anti-tumor activity with outpatient dosing every six weeks. Neurological disorders, including Parkinson’s and Alzheimer’s, are forecast to record a 9.36% CAGR, as BBB-penetrating nanoparticles and continuous infusion pumps address unmet needs.

Diabetes maintains momentum through closed-loop insulin systems integrating real-time glucose data, while cardiovascular therapies shift toward once-quarterly depot injections. Infectious disease platforms leverage rapid-fill needle-free injectors for pandemic preparedness. Cross-application platforms permit scale economies, aligning R&D cost with expanded indication breadth.

By End User: Hospital Infrastructure Supports Home-Care Transition

Hospitals held 53.10% share of New Drug Delivery Systems market in 2025, reflecting embedded infusion suites and surgical implant capabilities. Home-care settings, anticipated to post a 10.12% CAGR, capitalize on reimbursement reforms that finance at-home biologic administration. Ambulatory centers exploit minimally invasive implants, enabling same-day discharge.

Specialty clinics partner with device makers for disease-focused programs. Remote monitoring dashboards linked to connected injectors reduce unscheduled hospital visits, further reinforcing the migration to decentralized care. Successful systems therefore must balance clinical precision with ease of patient self-use.

Geography Analysis

North America retained 41.90% of New Drug Delivery Systems market revenue in 2025, supported by fast regulatory pathways and payer acceptance of high-value devices. Breakthrough Therapy designations accelerate adoption, yet rising scrutiny of cybersecurity prolongs time-to-market for connected delivery tools. Capacity shortfalls for lipid nanoparticles prompt partnerships with Asian CDMOs.

Asia-Pacific is projected to log a 10.66% CAGR through 2031. Regional governments expand universal health coverage and incentivize domestic manufacturing. China’s policy to localize high-end medical technology has spurred joint ventures for smart auto-injectors, while India’s generics producers eye value capture in cost-effective microneedle patches.

Europe remains mature but regulation-intense. The Medical Device Regulation introduces dual compliance needs that delay launches but elevate safety standards. Sustainability imperatives accelerate interest in recyclable packaging and long-acting formulations. Brexit’s separate U.K. pathway demands parallel submissions, adding complexity but not materially eroding demand.

Competitive Landscape

The New Drug Delivery Systems market is moderately fragmented, yet recent headline acquisitions demonstrate rising concentration. Novo Nordisk’s USD 16.5 billion Catalent deal provides integrated formulation and fill-finish capacity, while Lantheus’s radiopharmaceutical buyouts build vertical expertise. Larger firms leverage scale to navigate combination-product dossiers and absorb cybersecurity compliance costs.

Start-ups differentiate via AI-directed dosing algorithms, biodegradable carriers and user-centric industrial design. Strategic alliances between Pharma and MedTech accelerate prototyping, exemplified by Enable Injections collaborating with multiple biologic sponsors on high-volume wearable infusers. Platform technologies capable of accommodating multiple APIs now command premium valuations.

Customer purchasing decisions increasingly weigh clinical outcome data, economic evidence and environmental footprint. Consequently, suppliers that bundle real-world evidence with connected dashboards enjoy stronger formulary positioning. In this landscape, rapid regulatory clearance and modular production capacity emerge as the decisive competitive levers.

Novel Drug Delivery Systems (NDDS) Industry Leaders

Abbott Laboratories

Bayer AG

F. Hoffmann-La Roche AG

GlaxoSmithKline Plc

Merck & Co., Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Johnson & Johnson's TAR-200 received FDA Breakthrough Therapy Designation for treatment of BCG-unresponsive high-risk non-muscle-invasive bladder cancer, with the intravesical system

- July 2025: Johnson & Johnson submitted New Drug Application to FDA for icotrokinra, a first-in-class oral peptide IL-23 receptor blocker for moderate to severe plaque psoriasis in patients aged 12 and older, representing a breakthrough in oral delivery of complex biologics

Global Novel Drug Delivery Systems (NDDS) Market Report Scope

As per the scope of this report, the novel drug delivery system (NDDS) is intended to increase the efficacy of drugs. NDDSs are adopted to increase the bioavailability of the drug, reduce adverse effects and side effects, and increase drug stability. The Novel Drug Delivery Systems (NDDS) Market is segmented by Route of Administration (Oral Drug Delivery Systems, Injectable Drug Delivery Systems, Pulmonary Drug Delivery Systems, Transdermal Drug Delivery Systems, and Other Routes of Administration), Mode of NDDS (Targeted Drug Delivery Systems, Controlled Drug Delivery Systems, Modulated Drug Delivery Systems), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

By Route of Administration (Value)

| Oral |

| Injectable |

| Inhalation |

| Transdermal |

| Implantable |

| Ocular |

| Nasal |

| Others |

By Technology / System Type (Value)

| Nanoparticle-based Systems |

| Wearable Injectors |

| Smart / Connected Devices |

| Needle-Free Injection Systems |

| Microneedle Patches |

| Auto-Injectors |

| Enteric-Coated Capsules |

| Others |

By Therapeutic Application (Value)

| Oncology |

| Diabetes |

| Cardiovascular Diseases |

| Infectious Diseases |

| Respiratory Diseases |

| Neurological Disorders |

| Others |

By End User (Value)

| Hospitals |

| Ambulatory Surgical Centers |

| Home-Care Settings |

| Specialty Clinics |

| Others |

By Geography (Value)

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Route of Administration (Value) | Oral | |

| Injectable | ||

| Inhalation | ||

| Transdermal | ||

| Implantable | ||

| Ocular | ||

| Nasal | ||

| Others | ||

| By Technology / System Type (Value) | Nanoparticle-based Systems | |

| Wearable Injectors | ||

| Smart / Connected Devices | ||

| Needle-Free Injection Systems | ||

| Microneedle Patches | ||

| Auto-Injectors | ||

| Enteric-Coated Capsules | ||

| Others | ||

| By Therapeutic Application (Value) | Oncology | |

| Diabetes | ||

| Cardiovascular Diseases | ||

| Infectious Diseases | ||

| Respiratory Diseases | ||

| Neurological Disorders | ||

| Others | ||

| By End User (Value) | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-Care Settings | ||

| Specialty Clinics | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What revenue level does the New Drug Delivery Systems market reach in 2026?

The sector generated USD 311.65 billion in 2026 and is projected to climb to USD 417.88 billion by 2031.

Which administration route grows fastest through 2031?

Implantable systems are projected to register a 8.72% CAGR, outpacing other routes.

How quickly will smart and connected devices advance?

This technology segment is set for a 9.18% CAGR between 2026-2031 as data-enabled platforms gain acceptance.

Which therapeutic area leads 2025 revenue?

Oncology applications held 33.05% share of sector revenue in 2025.

Which region shows the highest forecast growth?

Asia-Pacific is poised for a 10.66% CAGR through 2031 thanks to expanding healthcare access.

What driver contributes most to CAGR uplift?

Adoption of biologics and large-molecule drugs adds roughly +2.1 percentage points to the forecast CAGR.

Page last updated on: