Intravenous (IV) Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

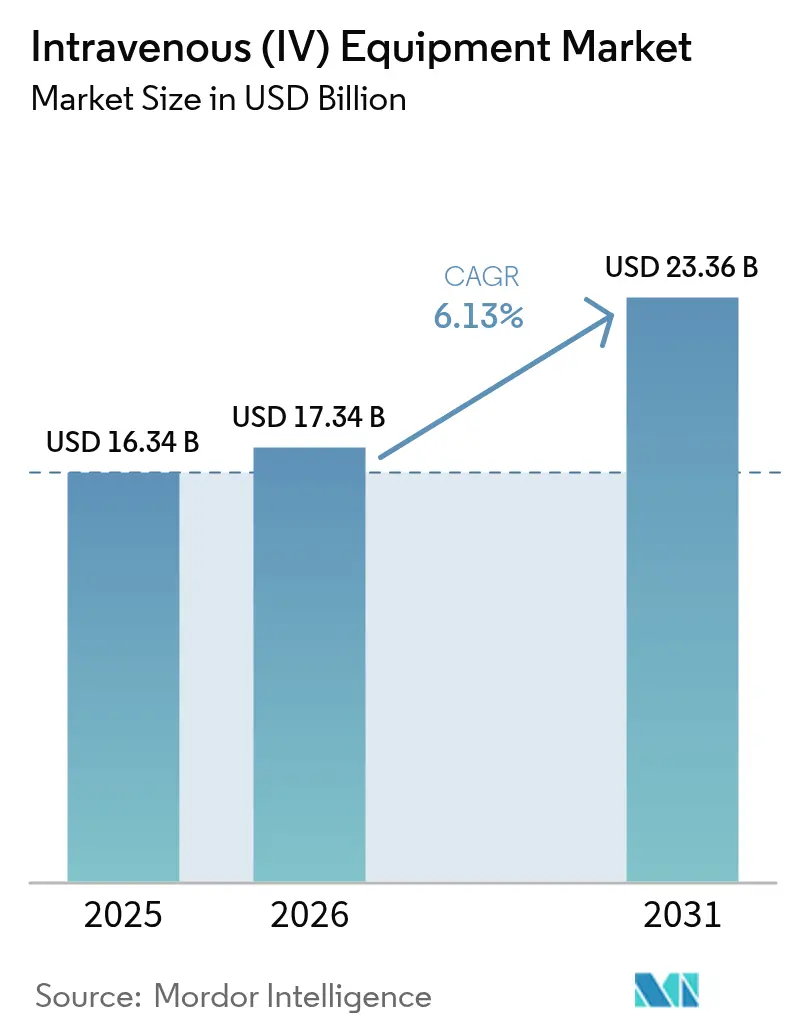

| Market Size (2026) | USD 17.34 Billion |

| Market Size (2031) | USD 23.36 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intravenous (IV) Equipment Market Analysis by Mordor Intelligence

The IV therapy devices market size is expected to grow from USD 16.34 billion in 2025 to USD 17.34 billion in 2026 and is forecast to reach USD 23.36 billion by 2031 at 6.13% CAGR over 2026-2031. Supply-chain fragility became clear when Hurricane Helene forced Baxter to shut its North Carolina plant, eliminating 60% of US IV fluid capacity and prompting hospitals to cut usage by up to 55%[1]Source: NPR Staff, “Hurricane Helene Shuts Baxter Plant And Triggers IV Fluid Shortage,” npr.org . The disruption accelerated point-of-care fluid production pilots and broadened calls for diversified sourcing. Regulatory pressure after multiple Class I recalls has pushed manufacturers toward AI-enabled safety features, driving rapid uptake of smart infusion systems. Asia-Pacific’s healthcare build-out and chronic-disease burden underpin the fastest regional expansion even as North America remains the revenue anchor. Intensifying M&A, illustrated by Stryker’s USD 4.9 billion acquisition of Inari Medical, signals a shift toward portfolio convergence that bundles pumps, catheters, and monitoring into integrated platforms.

Key Report Takeaways

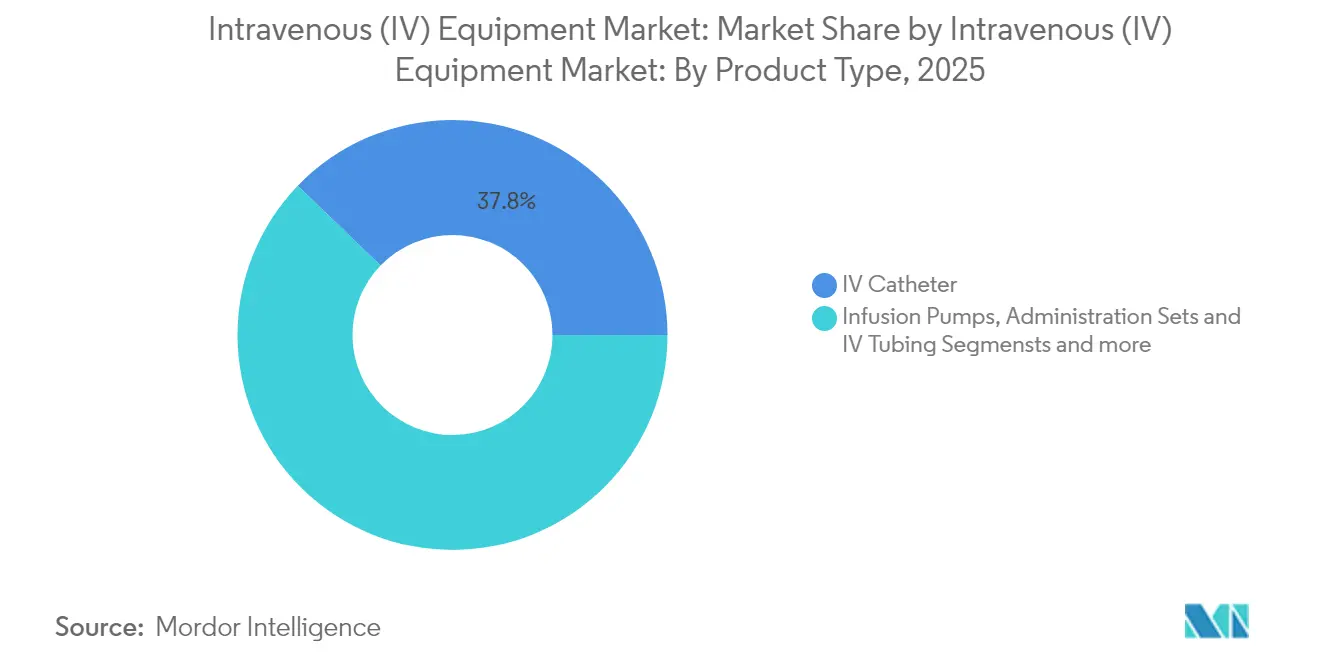

- By product type, IV catheters led with 37.78% of the IV therapy devices market share in 2025, whereas smart infusion pumps are forecast to deliver a 6.67% CAGR to 2031.

- By end user, hospitals held 48.62% revenue share in 2025; home-care settings are expected to expand at a 6.97% CAGR through 2031.

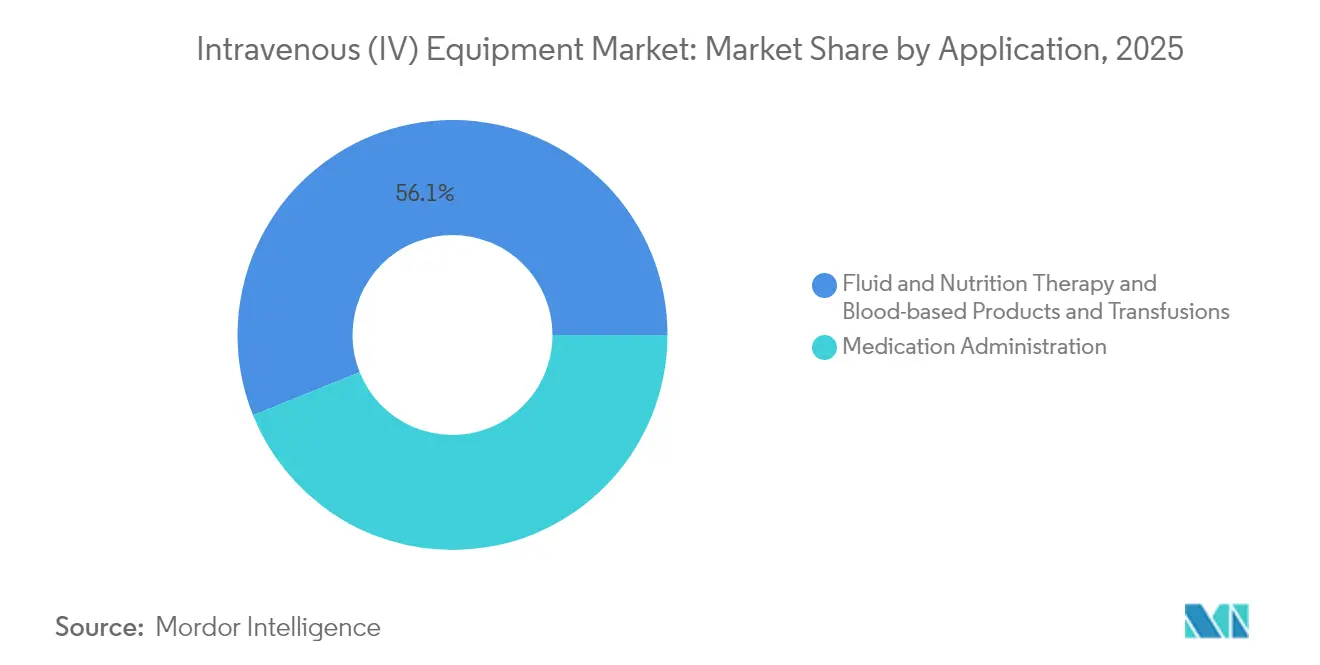

- By application, chemotherapy and oncology accounted for 7.72% CAGR growth, outpacing medication administration’s 43.92% revenue share baseline in 2025.

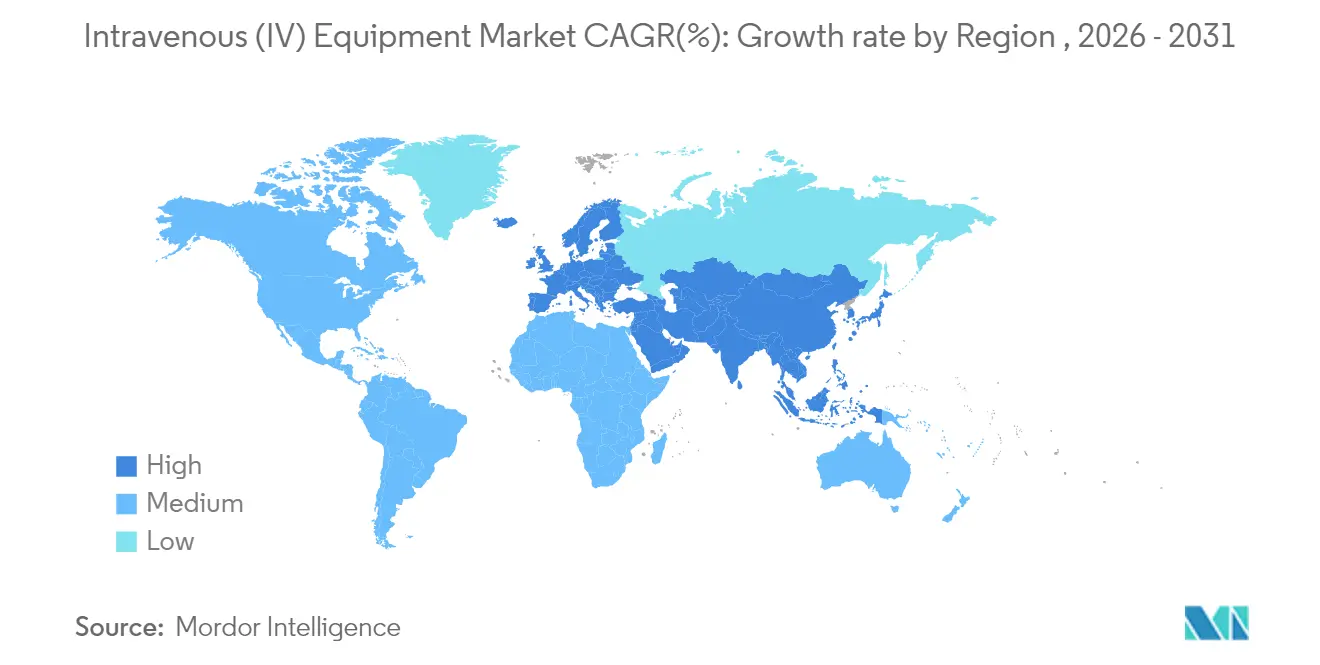

- By geography, North America captured 41.85% of total revenue in 2025, while Asia-Pacific is projected to rise at a 7.96% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intravenous (IV) Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases requiring long-term IV therapy | +1.8% | Global, with concentration in aging populations of North America, Europe, and Japan | Long term (≥ 4 years) |

| Growth in home- and ambulatory-based infusion therapy | +1.2% | North America & EU leading, APAC emerging markets following | Medium term (2-4 years) |

| Increasing surgical procedures & hospitalization rates | +0.9% | APAC core markets, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Technological advancements in smart infusion & needle-free systems | +0.8% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Emergence of closed-loop AI drug-delivery algorithms | +0.5% | North America & EU, limited APAC penetration | Long term (≥ 4 years) |

| Decentralized clinical trials driving portable IV devices | +0.3% | Global, concentrated in major pharmaceutical hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Long-Term IV Therapy

Diabetes affects 537 million adults and often necessitates intravenous intervention for complications, underpinning predictable demand across the IV therapy devices market[2]Source: MIT News, “Closed-Loop Drug-Delivery System Could Improve Chemotherapy,” news.mit.edu . Aging populations in North America, Europe, and Japan further widen the chronic-care pool that relies on multi-drug regimens unsuitable for oral delivery. MIT’s CLAUDIA system exemplifies the push toward closed-loop chemotherapy that automatically adjusts dosing every five minutes, illustrating how disease complexity spurs advanced infusion adoption. Payers support home-based IV services to curb readmissions, reinforcing a durable revenue stream for manufacturers that supply patient-centric delivery platforms. Together, these forces propel sustained growth momentum within the IV therapy devices market.

Growth in Home- and Ambulatory-Based Infusion Therapy

Veterans Affairs saved USD 10.2 million by substituting inpatient care with home infusion, validating an economic case that pressures providers to shift toward ambulatory models academic.oup.com. Portable pumps such as the Infonde unit record 95% patient-satisfaction rates, underscoring how mobility-friendly technology supports quality-of-life goals. Pending US legislation proposes stronger Medicare reimbursement, likely boosting patient volumes. During the COVID-19 pandemic, nurses operated pumps outside ICU rooms to reduce exposure risks, accelerating digital-monitoring upgrades. Oncology remains the prime home-care growth engine as patients favor familiar settings for lengthy chemotherapies, reinforcing upward momentum in the IV therapy devices market.

Increasing Surgical Procedures & Hospitalization Rates

Rising surgical volumes across Asia-Pacific require precise perioperative fluid management that smart pumps provide. BD’s HemoSphere Alta platform integrates Hypotension Prediction Index analytics, illustrating how AI-based decision support elevates pump utility during complex procedures. ERAS protocols demonstrated 50% fluid-use reductions without compromising outcomes, driving hospitals to adopt pumps capable of more granular delivery. Minimally invasive techniques and an aging population spur ongoing operating-room demand, sustaining the IV therapy devices market trajectory.

Technological Advancements in Smart Infusion & Needle-Free Systems

FDA guidance now permits software updates under predetermined change-control plans, accelerating AI innovation cycles in infusion devices. Needle-free connectors like Delta P.Valve achieve neonatal-safe flow rates while offering clear visualization to avert infection deltamed.pro. BD’s Nexiva closed catheter reduces blood-exposure risk by 98% and delivers median dwell times of 144.5 hours, boosting clinical productivity. Digital droplet infusion scales down volumes to 57 nL, demonstrating precision leaps that encourage adoption in high-value therapies. Coupled with IoT dashboards, these advancements anchor premium pricing power within the IV therapy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product recalls & medication-error related regulatory scrutiny | -1.10% | Global, with stricter enforcement in FDA and EU markets | Short term (≤ 2 years) |

| High cost of advanced infusion systems in low-resource settings | -0.80% | APAC emerging markets, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Shortage of skilled infusion nurses raising complication risks | -0.60% | North America & EU, with spillover effects globally | Medium term (2-4 years) |

| Shift toward subcutaneous/oral biologics reducing IV demand | -0.40% | Global, led by oncology and immunology therapeutic areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Recalls & Medication-Error Regulatory Scrutiny

The FDA initiated Class I recalls affecting more than 150,000 infusion devices in 2024, including ICU Medical’s Medfusion line, intensifying oversight across the IV therapy devices market. New Quality Management System Regulation, effective February 2026, aligns US rules with ISO 13485:2016 and expands post-market surveillance. Fresenius Kabi’s USD 240 million Ivenix buy-out swiftly encountered warning letters, illustrating compliance risk. Section 524B cybersecurity mandates now form part of pre-market submissions, raising barriers for smaller entrants. While these actions uplift safety, short-run cost spikes can dampen equipment turnover, tempering growth within the IV therapy devices market.

Shift Toward Subcutaneous/Oral Biologics Reducing IV Demand

Large-volume subcutaneous formulations constitute 15% of late-stage pipelines, signaling a channel shift away from intravenous delivery. Merck’s subcutaneous pembrolizumab aims to cut chair-time from hours to minutes, pending September 2025 FDA action drugs.com. Oncology biologics such as daratumumab already demonstrate patient-preference swings toward rapid injections, challenging pump utilization rates. Pharma companies are also exploring eco-friendly delivery devices that sidestep single-use IV disposables. Consequently, manufacturers must showcase superior clinical or economic value to defend share within the IV therapy devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Pumps Lead Innovation Wave

IV catheters controlled 37.78% of 2025 revenue as the foundational access tool across settings, securing the single-largest slice of the IV therapy devices market bbraunusa.com. Smart infusion pumps, however, represent the fastest growth at 6.67% CAGR thanks to AI dose-error reduction and cloud analytics. Baxter’s Spectrum IQ earned its seventh Best-in-KLAS award with 97% drug-library compliance, illustrating the performance bar now expected in the IV therapy devices market. Consumables such as tubing and administration sets benefit from steady replacement cycles, ensuring recurring revenue. Needle-free connectors, securement devices, and advanced filters collectively add infection-prevention value, making them attractive add-on sales. Mature drip-chamber components grow modestly yet remain essential, preserving backbone demand throughout the IV therapy devices market.

By End User: Home Care Disrupts Traditional Models

Hospitals retained 48.62% share in 2025, reflecting embedded procurement pathways and the scale of acute-care demand. Home-care settings, advancing at a 6.97% CAGR, illustrate how payer cost controls and patient comfort reorder priorities within the IV therapy devices market. Japanese home-care data show 21.6% of patients need intravenous therapy, yet 75% experience venous-access complications, spotlighting the safety gap that premium devices aim to close. Ambulatory surgery centers absorb spill-over cases as same-day procedures proliferate, requiring compact yet sophisticated pumps. Diagnostic and specialty clinics exploit niche oncology and immunology therapies where controlled infusion remains critical. Value-based care incentives further fuel migration outside hospitals, strengthening multi-setting demand across the IV therapy devices market.

By Application: Oncology Drives Premium Growth

Medication administration comprised 43.92% revenue in 2025, spanning antibiotics to biologics. Yet chemotherapy and oncology applications post the steepest climb at 7.72% CAGR, propelled by rising cancer incidence and regimen complexity. Closed-loop delivery prototypes like CLAUDIA monitor plasma drug levels every five minutes, foreshadowing a new standard of precision in the IV therapy devices market. Fluid and nutrition therapy retains baseline demand in critical-care units, while blood-product infusion requires strict alarm and monitoring features. AI-optimized parenteral nutrition formulations illustrate how application-specific software differentiation can unlock fresh value pools.

Geography Analysis

North America generated 41.85% of global revenue in 2025 owing to robust reimbursement and early technology adoption, reinforcing its anchor position in the IV therapy devices market. Yet Hurricane Helene exposed supply-chain risk, triggering federal initiatives to validate point-of-care fluid manufacturing and argue for broader supplier portfolios. Canada’s universal system and Mexico’s private-hospital build-out add incremental volumes, while a harmonizing regulatory backdrop facilitates cross-border trade.

Asia-Pacific is the fastest-growing region at an 7.96% CAGR, propelled by China’s healthcare-spend trajectory toward RMB 205 trillion by 2030 and incentive schemes that fast-track innovative devices . Japan’s super-aging society intensifies home-infusion uptake despite elevated complication rates, creating openings for safer vascular-access designs. India’s hospital expansion and chronic-disease surge position it as a high-potential adopter once reimbursement barriers ease. South Korea and Australia, with advanced payer systems, foster premium-device adoption that often cascades into neighboring markets, reinforcing Asia-Pacific’s strategic weight within the IV therapy devices market.

Europe delivers steady gains through stringent quality standards and sustainability mandates that spur eco-design innovation. Economic pressure in Southern markets dampens capital purchases, but Northern nations maintain high replacement cycles. Latin America and the Middle East & Africa contribute emerging-market upside: Brazil drives regional scale through public-hospital acquisitions, while GCC states channel oil revenues into specialty-care facilities requiring sophisticated IV infrastructure. South Africa acts as a distribution hub for sub-Saharan adoption. Collectively, these markets diversify revenue streams and cushion regional shocks for participants in the IV therapy devices market.

Regulatory Landscape

Intravenous (IV) equipment is primarily regulated as medical devices, with many IV administration and infusion-related products falling under US FDA Class II pathways with special controls (for example, under 21 CFR Part 880). In August 2024, the FDA issued a final order classifying an intravenous catheter force-activated separation device into Class II (special controls), reinforcing device-specific control expectations for vascular-access risk mitigation.

Quality and post-market obligations tightened in the base-year-to-current-year window. The FDA Quality Management System Regulation (QMSR) became effective on February 2, 2026, updating 21 CFR Part 820 and aligning the US quality system framework more closely with ISO 13485:2016. In the EU, the MDR (Regulation (EU) 2017/745) continues to define conformity assessment and surveillance requirements, and in April 2026 the Medical Device Coordination Group updated classification guidance (MDCG 2021-24 Rev.1), prompting manufacturers to revisit classification rationales for borderline and software-enabled IV technologies. Adoption of ISO 8536-series standards also provides a practical compliance anchor for infusion set performance, including ISO 8536-13:2024 and ISO 8536-16:2025 for gravity feed infusion sets used with volumetric infusion controllers.

Value Chain Analysis

The IV equipment value chain stretches from upstream medical-grade inputs (PVC, polypropylene, polyethylene, stainless steel needle components, and specialized elastomers) through regulated conversion and finishing. Core manufacturing steps include injection molding (connectors, clamps, drip chambers), tube extrusion (catheters and tubing), assembly in controlled environments (commonly ISO Class 8), and terminal sterilization (EtO or gamma), followed by packaging, lot release testing, and quality documentation aligned with ISO 13485 and risk management expectations. For smart infusion pumps, embedded software validation, cybersecurity documentation, and interoperability testing add additional verification burdens before distribution.

Downstream, products move through a mix of direct hospital sales, group purchasing organizations, and distributors, while recurring consumables (administration sets, tubing, connectors, securement) are frequently bundled to support pump ecosystems and standardize protocols. Supply concentration has been a key stress point: Hurricane Helene (September 2024) disrupted Baxter International operations in North Carolina and removed a major share of US IV fluid capacity, which increased the importance of dual sourcing, validated alternate manufacturing, and inventory buffers at providers. Policy and regulator actions during the shortage, including FDA shortage-list management, import facilitation, and outreach via the Office of Supply Chain Resilience, reinforced a supply-continuity lens in procurement and supplier qualification that goes beyond price-focused contracting.

Competitive Landscape

The IV therapy devices market exhibits moderate consolidation, with the top five suppliers controlling majority of 2024 revenue. Strategic acquisitions characterize recent moves: BD paid USD 4.2 billion for Edwards Lifesciences’ critical-care assets to bundle monitoring with infusion delivery. Stryker’s USD 4.9 billion bid for Inari Medical secures entry into peripheral-vascular infusion therapies, signaling portfolio expansion beyond traditional orthopedics.

Regulatory stringency raises operating thresholds; smaller firms like InfuTronix exited after recalling 52,328 Nimbus units, underlining financial exposure to quality lapses. Platform strategies that integrate pumps, disposables, and analytics create sticky ecosystems that elevate switching costs for providers. AI capabilities now act as competitive differentiators: BD’s HemoSphere Alta showcases real-time cerebral-autoregulatory insights, whereas Baxter augments its Spectrum IQ with dose-change alerts.

White-space opportunities persist in home-infusion monitoring and mid-tier emerging markets where cost-optimized systems can undercut premium incumbents. Cybersecurity compliance and software-as-a-medical-device expertise are becoming critical gating factors for market entry. Collectively, these dynamics support healthy rivalry while reinforcing the importance of scale and technical depth within the IV therapy devices market.

Intravenous (IV) Equipment Industry Leaders

Becton, Dickinson and Company

3M

Henry Schein, Inc.

B. Braun Melsungen AG

ICU Medical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Safety-driven modernization creates whitespace across IV pumps and associated disposables, particularly in software, usability, and connectivity layers. The FDA’s QMSR effective February 2, 2026 raises the operational bar for design controls and post-market surveillance by aligning more tightly with ISO 13485:2016, which increases demand for suppliers that can provide validated updates, traceable software lifecycles, and robust complaint and CAPA systems. This environment favors smart infusion platforms that integrate dose error reduction software with EHR workflows to reduce manual programming steps and support standardized drug libraries in hospitals and home-infusion networks.

Supply resiliency and materials transition are also becoming tangible investment themes. After the Hurricane Helene disruption highlighted dependence on concentrated IV supply, manufacturers and health systems are prioritizing redundancy and domestic capacity where feasible. In July 2026, the Otsuka ICU Medical joint venture announced a USD 500 million investment to expand its Austin, Texas manufacturing footprint, including a new 500,000-square-foot facility aimed at improving supply resiliency and supporting non-DEHP-related requirements. At the same time, recurring Class I recall activity tied to software and alarm integrity, including 2026 correction and recall actions involving large-volume pumps, supports demand for vendors that can demonstrate dependable alarm behavior, drop-event robustness, and rapid field update capability across installed bases.

Recent Industry Developments

- June 2026: BD was awarded a Vizient Innovative Technology contract for the BD CentroVena One Insertion System after evaluation by hospital experts. The award supports faster access to the system across Vizient member facilities and strengthens BD's pathway to scale a new central line insertion workflow in acute care.

- April 2025: BD launched the HemoSphere Alta platform with AI-driven decision support for critical-care hemodynamics. The launch extends BD's installed-base strategy by pairing monitoring analytics with infusion-adjacent workflows in operating rooms and ICUs where precise fluid and drug delivery decisions are made.

- August 2024: The US FDA issued a final order classifying an intravenous catheter force-activated separation device into Class II (special controls). This action clarified regulatory expectations for a safety-oriented catheter accessory category and raised the importance of documented performance and risk controls for vascular-access innovations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from devices and consumables used to deliver fluids and drugs through a vein in clinical and home care settings. It includes the common delivery hardware and supporting components used in routine IV therapy.

Scope exclusions: IV solutions and drugs (including parenteral nutrition) are excluded from this sizing.

Segmentation Overview

- By Product Type

- Infusion Pumps

- IV Catheters (Peripheral & Central)

- Administration Sets & IV Tubing

- Securement & Stabilization Devices

- Needle-Free/Closed IV Connectors

- Drip Chambers & Filters

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home-Care Settings

- Diagnostic & Specialty Centers

- By Application

- Medication Administration

- Fluid & Nutrition Therapy

- Blood-based Products & Transfusions

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the model and to make sure product definitions matched how healthcare providers actually buy and use IV equipment. We referenced public sources such as the US FDA device databases for product classifications and recalls, the US CDC for healthcare use patterns and infection-related context, the World Health Organization for healthcare delivery indicators, and the World Bank for macro health spending and population trends. Where relevant, we also checked sources such as the US Centers for Medicare and Medicaid Services for spending benchmarks and peer-reviewed clinical journals for adoption trends in vascular access and infusion practices.

To convert those signals into a working market model, we used company filings, investor presentations, annual reports, and reputed press coverage to understand mix shifts across disposables and capital equipment. We also used paid subscriptions that support company financials and intelligence, along with patent databases, to sanity check innovation intensity and product pipeline activity. This list is illustrative, and many other public sources were also reviewed for data collection, validation, and clarification during analysis.

Primary Interviews and Surveys

Primary work focused on validating the demand pool and pricing logic for key IV equipment categories, since procurement terms and usage rates can vary by care setting. We spoke with a mix of manufacturers, distributors, group purchasing stakeholders, and hospital and clinic users across APAC, EMEA, and the Americas, so assumptions from desk research could be checked and then tightened where gaps existed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 43% |

| Mid tier: 43% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 19% | Managers: 43% | Americas: 27% |

Market-Sizing & Forecasting

Our core sizing starts with a top-down build where procedure and patient care activity is translated into IV equipment demand, then filtered through typical usage per setting. For example, hospitalization volumes, outpatient infusion visits, vascular access utilization, and ICU and surgical case intensity help shape the addressable demand that can realistically convert into equipment consumption. When the implied volumes are set, the total market value is formed by applying representative price points and then adjusting for mix between disposable components and infusion devices.

Selective bottom-up approximations were used to corroborate totals and catch over or under statements, including supplier revenue roll-ups for sampled product groups and channel checks on average selling price movement. Inputs tracked in the model included infusion pump install base replacement cycles, catheter and administration set consumption per admission day, share of needleless connectors in protocols, and region-level shifts toward home infusion. For forecasting, we used scenario analysis supported by expert views on how utilization and pricing will move, followed by short trend smoothing on stable series to avoid sharp jumps. Where bottom-up signals were thin in smaller geographies, gaps were handled using proxy indicators like hospital bed density and spend per capita, then rechecked with interview feedback before finalizing.

Data Validation & Update Cycle

Validation is done through multiple checks so the final outputs stay consistent with real world healthcare activity. We compare modeled totals against independent signals such as device shipment commentary in public filings, utilization indicators from public health statistics, and price direction from procurement feedback. If a region shows an unusual jump, the drivers are rechecked, assumptions are revisited, and respondents may be recontacted when the variance cannot be explained from public data.

Before sign-off, the model is reviewed in steps by analysts to confirm math accuracy, consistent currency treatment, and logical share splits across regions. The report is refreshed annually, and interim updates are made when material events occur such as major regulatory changes, product recalls, or large shifts in hospital spending. Right before delivery, a fresh pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Intravenous Iv Equipment Market Size Measured Against Other Published Estimates

Published market sizes for IV equipment do not always match because the scope is not identical and because the activity signals used to build demand can vary by publisher. Differences also show up when one estimate leans more on long-range growth assumptions, while another puts more weight on near-term hospital utilization and replacement cycles.

IV solutions and drugs are excluded, and that item sits outside Mordor Intelligence's scope for this report, which is a key reason some wider numbers look higher when adjacent therapy value is bundled in. Other gaps also come from how infusion pumps are treated (installed base replacement versus unit shipments), how disposable consumption per admission day is assumed, and how currency conversion timing is handled for multi-region rollups. When update cadence differs, recent recall activity or procurement tightening can also be reflected earlier in one estimate than another.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.34 B (2026) | |

| Global Consultancy A | USD 16.84 B (2025) | Uses a different base year and time horizon, and product mapping can differ across disposable components versus capital devices, which shifts the mix and the implied average prices. |

| Industry Publisher B | USD 16.78 B (2024) | Earlier base year and a higher stated growth path can move the implied current size, and some line items like stopcocks, valves, and connectors may be grouped differently across catheter and administration set buckets. |

The table shows that most of the spread is explained by year alignment and by what gets counted as IV equipment versus adjacent therapy value. By keeping the demand build tied to clear care activity indicators and by checking totals against supplier and procurement signals, we can present a market size that is traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the IV therapy devices market?

The IV therapy devices market size is USD 17.34 billion in 2026 and is projected to reach USD 23.36 billion by 2031 under a 6.13% CAGR.

Which product segment is expanding the fastest?

Smart infusion pumps lead growth at a 6.67% CAGR due to AI-enabled safety features and connectivity upgrades.

Why is Asia-Pacific viewed as the key growth region?

Rising healthcare spending, chronic-disease prevalence, and pro-innovation policies in China, India, and Japan push Asia-Pacific toward an 7.96% CAGR, the highest worldwide.

How are recalls influencing device innovation?

Heightened FDA scrutiny after Class I recalls compels manufacturers to embed AI dose-error checks, strengthen cybersecurity, and adopt ISO-aligned quality systems.

Will subcutaneous biologics erode future IV demand?

Large-volume subcutaneous formulations and oral biologics will lower some hospital infusions, yet complex chemotherapies and critical-care needs should sustain core IV volumes, especially for precision pumps.

Page last updated on: