Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 77.59 Billion |

| Market Size (2031) | USD 92.56 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

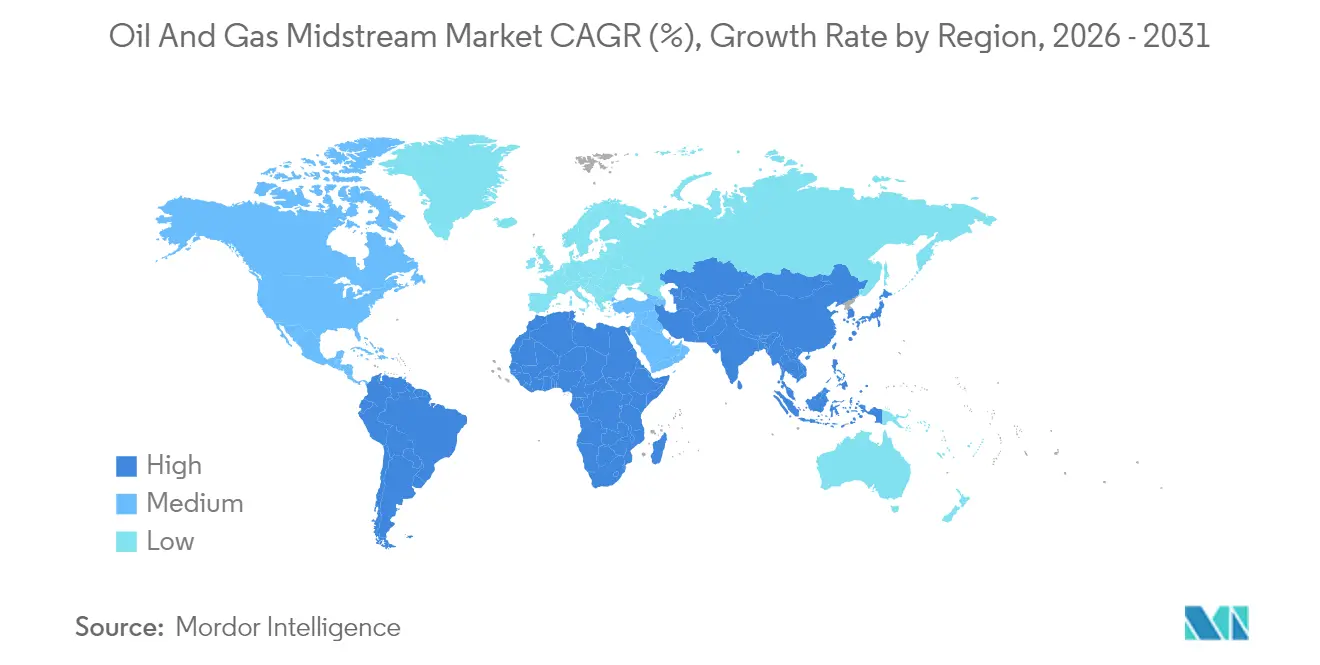

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas Midstream Market Analysis by Mordor Intelligence

The Oil And Gas Midstream Market size was valued at USD 74.90 billion in 2025 and estimated to grow from USD 77.59 billion in 2026 to reach USD 92.56 billion by 2031, at a CAGR of 3.59% during the forecast period (2026-2031).

Rising U.S. liquefied natural gas (LNG) export capacity, a rapid shift in Asian fuel‐mix preferences, and improving pipeline replacement economics collectively boost project backlogs and lift tariff revenues. Consolidation among master limited partnerships (MLPs) enlarges infrastructure footprints, widens basin optionality, and unlocks operating synergies. Supply-demand volatility tied to renewable energy integration continues to drive up storage values, while cybersecurity and environmental, social, and governance (ESG) considerations influence capital allocation and funding costs.

Key Report Takeaways

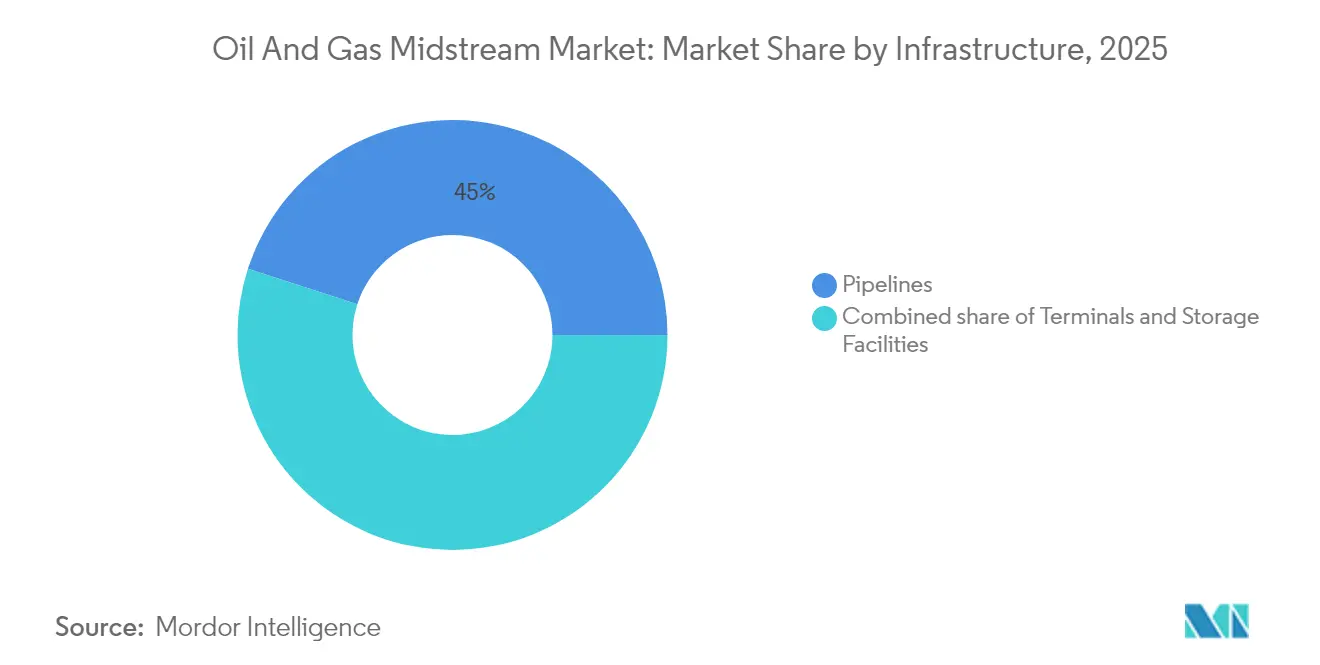

- By infrastructure, pipelines commanded 45.02% of the oil and gas midstream market share in 2025, and storage facilities are projected to post the fastest growth rate of 5.14% CAGR through 2031.

- By product type, natural gas accounted for 39.47% of the market in 2025, while LNG is projected to register the highest segmental CAGR of 6.41% over 2026-2031.

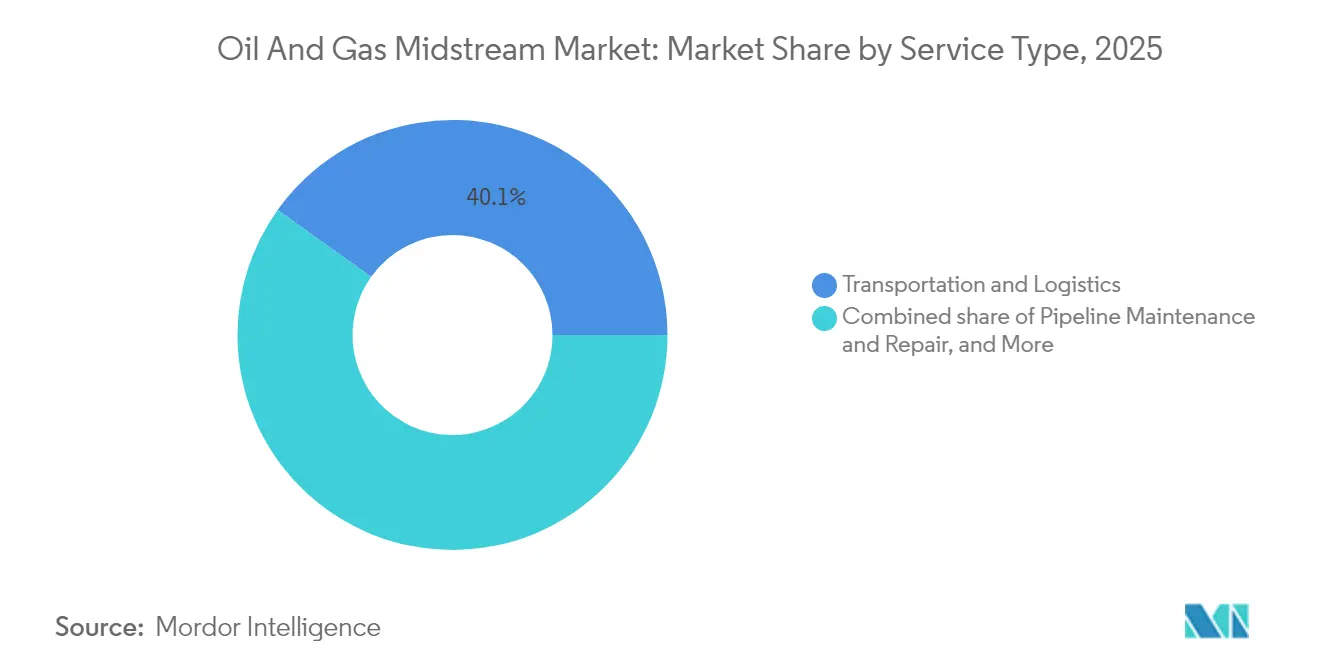

- By service type, transportation and logistics led with a 40.12% share of the oil and gas midstream market in 2025 and is likely to grow the fastest, at a 4.44% CAGR over 2026-2031.

- By geography, North America accounted for 30.22% of the market in 2025, and the Asia-Pacific region is set to record the strongest 4.74% regional CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oil And Gas Midstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging U.S. LNG export capacity build-out | +1.20% | North America with spillover to global shipping routes | Medium term (2-4 years) |

| Rising Asian gas demand shifting global flow patterns | +0.90% | Asia-Pacific core, extending to Middle-East supply corridors | Long term (≥ 4 years) |

| North American crude-by-rail replacement with pipelines | +0.50% | North America, concentrated in Permian and Canadian oil-sands regions | Medium term (2-4 years) |

| Aging onshore pipelines requiring replacement CAPEX | +0.70% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Modular FLNG deployment for stranded gas assets | +0.60% | Southeast Asia and West Africa | Medium term (2-4 years) |

| Growing gas-storage demand to manage renewable intermittency | +0.60% | Global, especially Asia-Pacific and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging U.S. LNG export capacity build-out

U.S. LNG export capacity is on track to rise 80% by 2028 as new Gulf Coast terminals come online. The projects enable the country to supply nearly one-third of global LNG by 2030, spurring investments in upstream gathering, processing, and trunkline infrastructure.(1)CME Group, “LNG Outlook 2025,” cmegroup.com Cheniere Energy reported USD 4.6 billion Q2 2025 revenue alongside USD 1.6 billion net income, highlighting robust earnings visibility under long-term take-or-pay agreements. Federal Energy Regulatory Commission approvals dictate construction pacing, yet favorable contract coverage and rising Asian demand keep final investment decisions on track. Liquefaction developers are increasingly partnering with midstream MLPs to secure feed gas and reduce balance-sheet strain.

Rising Asian gas demand shifting global flow patterns

Morgan Stanley projects 5% annual Asian gas consumption growth through 2030, dwarfing 1% in Europe.(2)Morgan Stanley, “Global Gas Demand Outlook,” morganstanley.com China imported 79 million tonnes of LNG in 2024 and plans to connect 150 million more residents to pipelines by 2030. India’s 27 million-tonne LNG tally in 2024, up 20% from 2023, aligns with a five-year plan to serve 30 million new consumers. Rising imports stimulate the construction of regasification terminals, storage caverns, and last-mile distribution grids. The demand wave reshapes shipping routes, drives longer-tenor offtake agreements, and underpins LNG-linked midstream tariffs. It also encourages U.S. exporters to secure destination-flexible contracts that capitalize on arbitrage.

Crude-by-rail replacement with pipelines

North American crude-by-rail movements continue to cede share to pipelines as new takeaway capacity cuts transport costs and spill risks. The Matterhorn Express Pipeline commenced operations in November 2024 with a 2.5 Bcf/d gas capacity, indicative of cross-commodity infrastructure development. Permian and Canadian oil sands producers secure multi-year transport contracts to lock in egress and eliminate rail discounts. States tighten rail safety rules, pushing shippers toward safer pipelines, while carbon reduction goals favor lower-emission transport modes. Midstream developers utilize brownfield corridors to expedite permitting and reduce capital intensity.

Aging onshore pipelines requiring replacement CAPEX

Many North American pipelines have surpassed 40 years of operation, coinciding with stricter regulations from the Pipeline and Hazardous Materials Safety Administration. Enterprise Products Partners advanced the Athena gas processing plant, which has a 300 MMcf/d capacity, to integrate with replacement lines and increase recoveries. New materials and fiber-optic monitoring reduce spill frequencies and lower long-term maintenance costs. Utilities accelerate parallel-loop projects to eliminate integrity digs and boost throughput. Replacement CAPEX sustains construction backlogs, lifts service revenues, and supports fee escalators tied to inflation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened ESG-driven capital scarcity | −0.8% | Global, most pronounced in Europe and North America | Medium term (2-4 years) |

| Volatile oil-price outlook dampening long-term contracts | −0.6% | Global, with particular impact on crude midstream | Short term (≤ 2 years) |

| Cybersecurity threat premium on midstream assets | −0.5% | Global, concentrated in North American pipeline systems | Short term (≤ 2 years) |

| Renewable-energy growth creating execution risks for LNG jobs | −0.4% | Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened ESG-driven capital scarcity

Large banks continue to tighten their lending to fossil fuels, prompting mid-tier lenders and private equity firms to bridge the resulting funding gaps. Sustainability-linked bonds are gaining traction as operators tie coupon step-ups to methane intensity targets. Mission Secure reports that cyber-hardened facilities cut insurance costs by USD 50,000 per site each year, partially offsetting higher financing spreads.(3)Mission Secure, “Case Study: Midstream Cyber Resilience,” missionsecure.com Project developers also explore public-private partnerships to align energy-security goals with environmental mandates. Delays in capital formation lead to contingency budgets and extend payback periods.

Volatile oil price outlook dampening long-term contracts

Spot-market crude swings deter shippers from locking into 10-year transportation deals, constraining pipeline earnings visibility. Counterparties favor volume-based over acreage-dedicated commitments, shifting volume risk back to operators. MLPs respond by diversifying into gas and NGL corridors that enjoy firmer demand. Hedging strategies grow more sophisticated as marketers blend physical storage with futures to manage volatility. While short-term pain suppresses tariff escalations, diversified asset portfolios cushion cash flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Storage Facilities Drive Capacity Expansion

The oil and gas midstream market size for pipelines stood at USD 33.72 billion in 2025, equal to 45.02% share, confirming the segment’s backbone status. Storage, however, is projected to expand at a 5.14% CAGR, the fastest among infrastructure categories, as power grids need flexible gas withdrawal to balance renewable intermittency. Enstor’s Mississippi Hub expansion is expected to increase working gas to 56.3 Bcf by 2028, a 2.5-fold increase that highlights investor interest in cavern assets. EnLink’s Jefferson Island Storage will add 8 Bcf capacity under long-term take-or-pay agreements, highlighting how utility customers value seasonal balancing. Cavern projects benefit from favorable geology, low operating cost, and revenue uplift from arbitrage trading between summer injection and winter withdrawal spreads.

Terminals play a critical role in supporting LNG imports, exports, and coastal refined product distribution. Bulgaria’s Chiren facility completed a 20% capacity step-up in 2024 to fortify regional supply resilience. Dubai awarded Baker Hughes its largest integrated compressor contract for the Margham expansion to manage solar-driven demand swings. Terminal operators integrate automation and advanced metering to trim boil-off gas losses and comply with International Maritime Organization regulations. Combined, these investments expand the oil and gas midstream market by raising fee-based revenue streams and enhancing network reliability.

By Product Type: LNG Acceleration Reshapes Traditional Gas Flows

Natural gas held a 39.47% slice of the oil and gas midstream market share in 2025, reflecting its dominant throughput volume. LNG outpaces all segments with a 6.41% CAGR through 2031 as Shell projects global demand to rise 60% by 2040. China’s 79 million-tonne import volume and India’s 27 million-tonne surge in 2024 strain regasification and storage capacity, accelerating the need for pipeline tie-ins. Marine LNG demand is projected to exceed 16 million tonnes annually by 2030, driving the development of new bunkering infrastructure along major shipping lanes. U.S. Gulf Coast liquefaction terminals anchor upstream gathering systems that transport shale gas from the Permian, Eagle Ford, and Haynesville plays under fixed-margin agreements.

Crude oil volumes face contract headwinds linked to price volatility; however, pipeline optimizations and blending services help mitigate margin erosion. Refined-product corridors innovate with drag-reducing agents and real-time batch tracking to optimize line pack. NGLs benefit from petrochemical growth and propane export arbitrage. Altogether, product diversification shields the oil and gas midstream industry from cyclical exposure, maintaining growth trajectories intact.

By Service Type: Transportation and Logistics Consolidate Market Position

Transportation and logistics services captured 40.12% of the oil and gas midstream market size in 2025 and led growth at a 4.44% CAGR. Complexity in global trade flows lifts demand for end-to-end scheduling, tariff optimization, and capacity marketing. Howard Energy Partners' Nueva Era Pipeline connects Eagle Ford gas to Monterrey's industrial demand, highlighting the value of cross-border logistics. Vaquero Midstream's 70-mile extension near Waha Hub pairs with a 200 MMcf/d plant to elevate system utilization to 800 MMcf/d. Service providers layer software-defined networking and predictive maintenance to minimize downtime and monetize uncommitted capacity.

Pipeline construction and repair services secure steady workloads from replacement and expansion projects. Storage handling services leverage cavern pressure management know-how and multi-cycle withdrawal rights to extract incremental revenue. Taken together, integrated offerings reinforce customer stickiness, extend contract tenors, and deepen barriers to entry across the oil and gas midstream market.

Geography Analysis

North America's oil and gas midstream market size reached USD 22.64 billion in 2025, accounting for a 30.22% share, driven by established networks, regulatory clarity, and robust LNG export pipelines. Permian Basin gathering buildouts, such as Matterhorn Express, and Enterprise's Midland Basin acquisitions, highlight a pivot from greenfield to optimization projects. Replacement CAPEX and brownfield loopings dominate spend, while cybersecurity mandates from the Transportation Security Administration widen compliance budgets.

The Asia-Pacific region advances at a 4.74% CAGR through 2031, the swiftest among all regions, as coal-to-gas switching accelerates. Countries target household pipeline penetration and peak-shaving storage, driving demand for steel pipes and the rollout of compressive stations. LNG import share eclipses indigenous supply growth, prompting flexible contract structures indexed to Henry Hub rather than oil-linked Japan Korea Marker prices. Geopolitical diversification strategies favor U.S. and Qatari cargoes, reducing the risk of single-supplier dependence and increasing voyage-charter activity.

Europe moderates as energy-security upgrades converge with decarbonization imperatives that prioritize hydrogen networks. South America channels investment to offshore pre-salt gas monetization, notably in Brazil. The Middle East and Africa rely on modular floating LNG to monetize remote fields, while regional storage expansions act as a buffer against seasonal demand spikes. Collectively, these geographically diverse investments sustain a balanced growth profile for the oil and gas midstream market.

Competitive Landscape

Midstream consolidation continues as operators seek to achieve scale, basin optionality, and cost synergies. DT Midstream’s USD 1.2 billion purchase of three ONEOK gas lines added 3.7 Bcf/d capacity across seven U.S. states and deepened contracted cash flow coverage. Enterprise Products Partners acquired Occidental’s Midland Basin affiliate for USD 580 million, securing 200 miles of pipe and long-term acreage agreements. MPLX spent USD 715 million to acquire BANGL and co-fund major Permian takeaway projects, underscoring the capital requirements for corridor dominance.

Technology adoption emphasizes incremental efficiency rather than disruptive change. Mission Secure’s cyber platform helped a North American operator reduce insurance premiums by USD 50,000 per location annually and enhance real-time monitoring. Baker Hughes secured its largest integrated compressor order for Dubai’s Margham storage project, showcasing the benefits of vendor consolidation in mega-tenders. Operators deploy fiber sensing, drone surveillance, and automated pigging to minimize leak‐related downtime and improve regulatory compliance.

Regulatory frameworks shape competitive dynamics. FERC permitting timelines influence asset valuations, while TSA directives require cyber-incident reporting and minimum protections. Companies with strong balance sheets and diversified business models are best positioned to navigate capital scarcity, ESG scrutiny, and insurance premium inflation. Overall competition centers on securing fee-based contracts, optimizing asset bases, and delivering predictable distributions that attract yield-oriented investors to the oil and gas midstream industry.

Oil And Gas Midstream Industry Leaders

APA Group

Chevron Corporation

BP PLC

Enbridge Pipelines Inc.

Shell PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DT Midstream completed a USD 1.2 billion acquisition of three natural gas pipelines from ONEOK, adding over 3.7 Bcf/d of combined capacity across seven Midwestern states and strengthening regional market position.

- January 2025: Keyera Corp announced a significant expansion of its storage facility at Fort Saskatchewan, Alberta, enhancing regional hydrocarbon storage capacity and supply chain flexibility in an established Canadian midstream hub.

- December 2024: MPLX announced pricing of USD 2.0 billion senior notes offering in two tranches (USD 1.0 billion 5.400% due 2035; USD 1.0 billion 5.950% due 2055) to refinance near-term maturities and support general partnership purposes.

- November 2024: The Matterhorn Express Pipeline began operations with a 2.5 Bcf/d capacity, connecting Permian Basin production to Texas demand centers and Gulf Coast LNG export terminals, fully contracted upon startup.

- October 2024: Summit Midstream Holdings acquired Moonrise Midstream assets in Colorado's Denver-Julesburg Basin for USD 90 million total (USD 70 million cash, USD 20 million equity), adding 80 miles of gas gathering pipeline and 65 MMcf/d processing capacity.

Global Oil And Gas Midstream Market Report Scope

The oil and gas midstream market report includes:

By Infrastructure

| Pipelines |

| Terminals |

| Storage Facilities (Underground and Above-ground) |

By Product Type

| Crude Oil |

| Natural Gas |

| Refined Products |

| LNG |

By Service Type

| Pipeline Construction |

| Pipeline Maintenance and Repair |

| Storage and Handling Services |

| Transportation and Logistics |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Norway |

| United Kingdom | |

| Russia | |

| Netherlands | |

| Germany | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Infrastructure | Pipelines | |

| Terminals | ||

| Storage Facilities (Underground and Above-ground) | ||

| By Product Type | Crude Oil | |

| Natural Gas | ||

| Refined Products | ||

| LNG | ||

| By Service Type | Pipeline Construction | |

| Pipeline Maintenance and Repair | ||

| Storage and Handling Services | ||

| Transportation and Logistics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Norway | |

| United Kingdom | ||

| Russia | ||

| Netherlands | ||

| Germany | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the oil and gas midstream market?

It was USD 77.59 billion in 2026.

How fast will global midstream revenue grow through 2031?

The sector is forecast to expand at a 3.59% CAGR between 2026 and 2031.

Which infrastructure type will see the fastest growth?

Gas storage facilities lead with a 5.14% CAGR through 2031.

Which region is poised for the quickest expansion?

Asia-Pacific is projected to grow at 4.74% CAGR over the forecast period.

What drives consolidation among midstream operators?

Scale benefits, geographic diversification, and the push for predictable fee-based cash flows motivate recent mergers and acquisitions.

How does cybersecurity affect midstream financials?

Operators with advanced cyber defenses can lower insurance premiums by approximately USD 50,000 per facility each year.

Page last updated on: