Controlled Release Drug Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

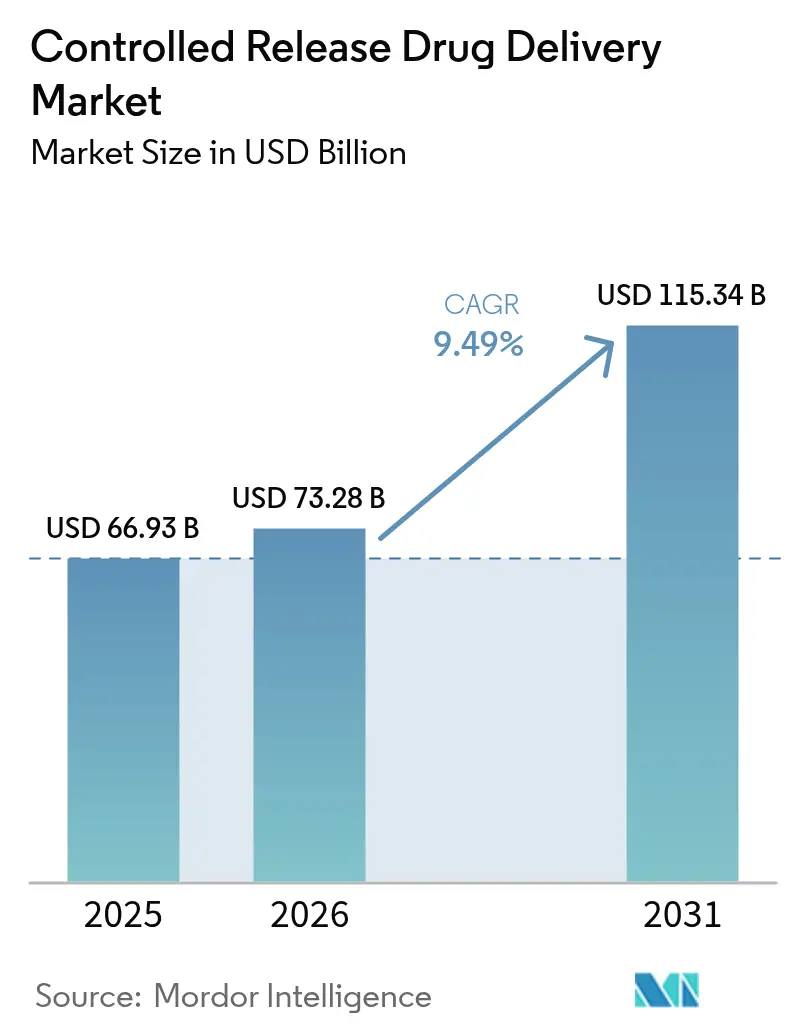

| Market Size (2026) | USD 73.28 Billion |

| Market Size (2031) | USD 115.34 Billion |

| Growth Rate (2026 - 2031) | 9.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

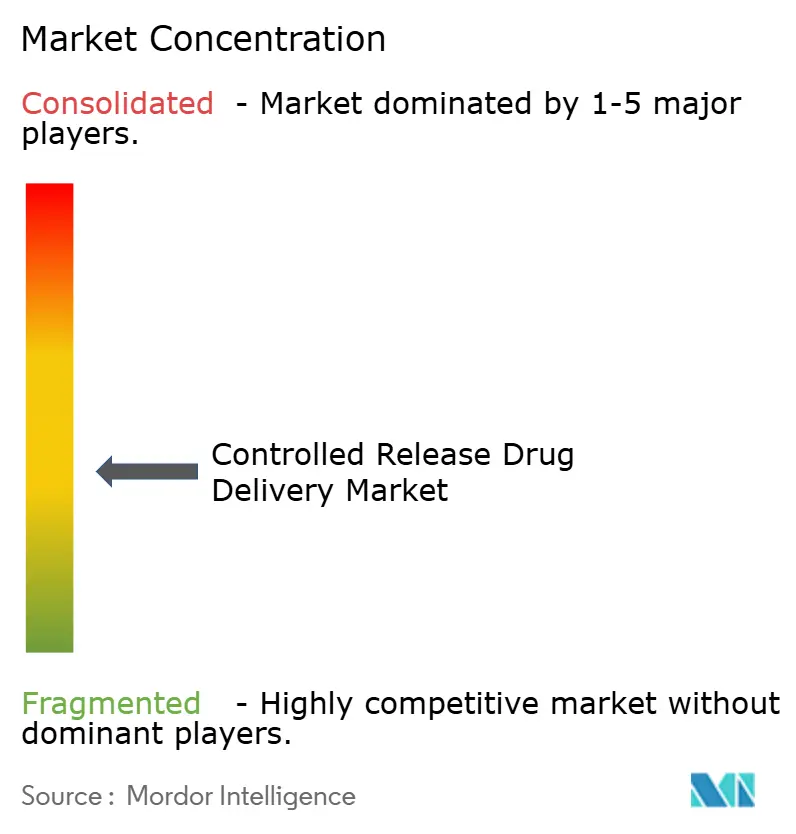

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Controlled Release Drug Delivery Market Analysis by Mordor Intelligence

The controlled release drug delivery market size was valued at USD 66.93 billion in 2025 and estimated to grow from USD 73.28 billion in 2026 to reach USD 115.34 billion by 2031, at a CAGR of 9.49% during the forecast period (2026-2031). Expanding chronic-disease prevalence, wider use of biologics, and fresh advances in polymer science together steer this growth momentum. Investors are focusing on long-acting formulations that improve drug exposure profiles, reduce systemic side effects, and lengthen product lifecycles. Active capital flows into large-molecule manufacturing, increased adoption of patient-centric dosing, and meaningful repurposing of lipid nanoparticle infrastructure further widen the therapeutic and commercial runway for the controlled release drug delivery market. Strategic advantages accrue to firms that couple in-house formulation know-how with broad commercialization networks, while nimble CDMOs carve out complex formulation niches for fast-moving specialty players.

Key Report Takeaways

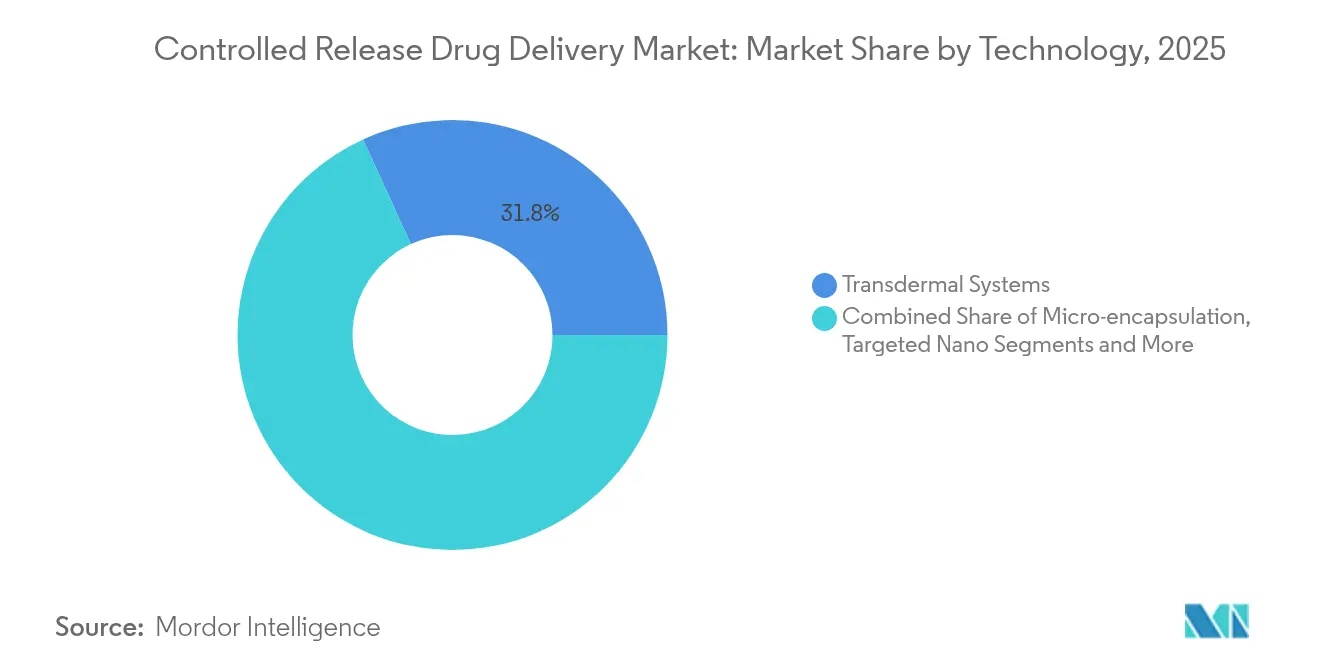

- By technology, transdermal systems held 31.83% of controlled release drug delivery market share in 2025; targeted nano/lipid carriers are projected to expand at a 12.05% CAGR through 2031.

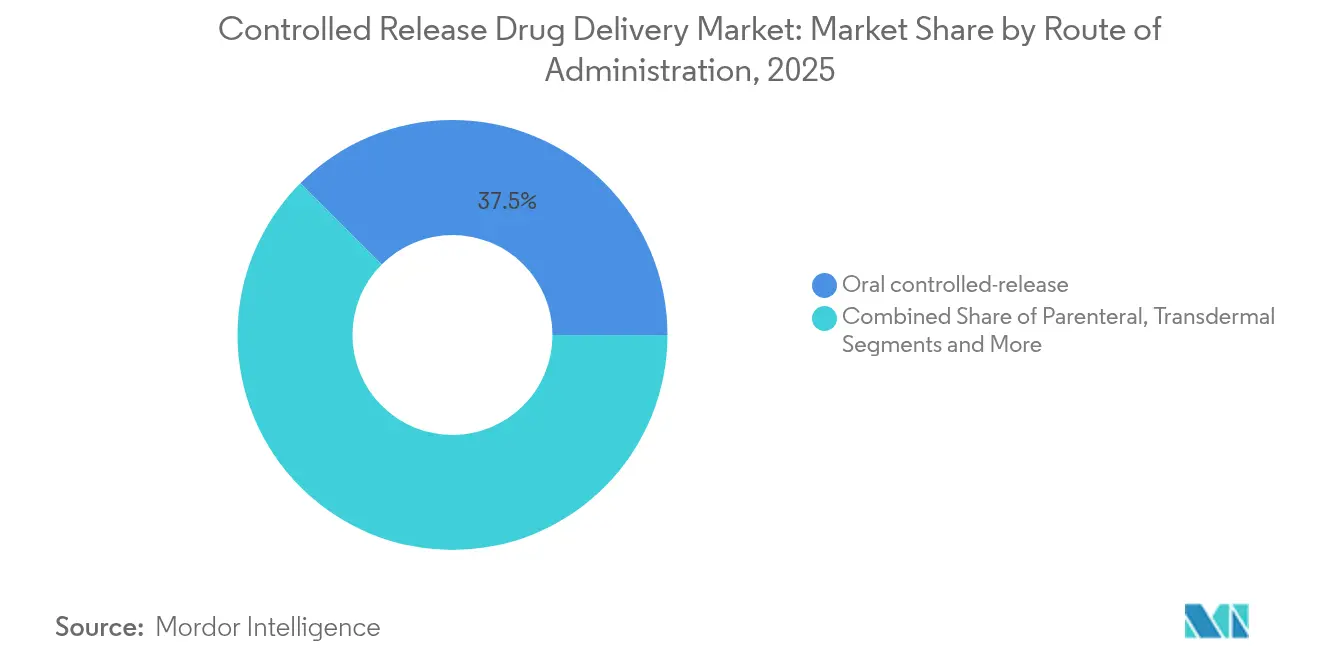

- By route, oral formulations accounted for 37.52% share of the controlled release drug delivery market size in 2025, while parenteral injectables are advancing at an 11.23% CAGR through 2031.

- By polymer, PLGA/PLA systems captured 25.94% share of the controlled release drug delivery market size in 2025; lipid nanoparticles lead growth at a 12.28% CAGR, powered by mRNA process know-how.

- By geography, North America dominated with 36.02% share in 2025, but Asia Pacific is forecast to clock an 11.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Controlled Release Drug Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating chronic-disease burden | +2.1% | Global, strong in North America & Europe | Long term (≥ 4 years) |

| Rapid growth in geriatric & pediatric cohorts | +1.8% | Global, especially APAC and North America | Medium term (2-4 years) |

| Breakthroughs in micro-/nano-encapsulation polymers | +1.5% | North America & EU, spreading to APAC | Medium term (2-4 years) |

| Shift toward once-weekly/monthly dosing | +1.2% | Global, led by developed markets | Short term (≤ 2 years) |

| mRNA-lipid infrastructure repurposed | +0.9% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| AI-driven formulation optimization platforms | +0.7% | Global, focused in innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating chronic-disease burden

Diabetes, cardiovascular disease, and cancer together affect more than 1.5 billion people and require therapies that promote adherence over many years. Controlled release tablets such as extended-release ketamine achieved a 6.1-point decline in MADRS scores versus placebo while limiting adverse reactions, demonstrating the clinical pay-off from stable plasma profiles.[1]Paul Glue, “Extended-Release Ketamine Tablets for Treatment-Resistant Depression,” Nature Medicine, nature.comHealthcare buyers under value-based payment rules favor regimens that lower readmissions, which supports ongoing expansion of the controlled release drug delivery market. Firms also rely on long-acting platforms to refresh generic molecules and defend exclusivity as biologics meet biosimilar pressure.

Rapid growth in geriatric & pediatric cohorts

Older adults often juggle five or more prescriptions each day; children need palatable options at lower strengths. Innovations such as Lonza’s Enprotect size 9 capsule allow acid-sensitive actives to release in the intestine without extra coatings, cutting formulation steps. Weekly oral risperidone maintained steady plasma levels in schizophrenia patients and raised satisfaction scores in phase 3 trials, showing that the controlled release drug delivery market can address adherence for vulnerable populations.

Breakthroughs in micro-/nano-encapsulation polymers

PLGA implants now pair with 3D printing for patient-matched shapes that release drug in tune with individual metabolism.[2]Renae L. Wilson, “PLGA Implants for Controlled Drug Delivery,” mdpi.com Wearable osmotic microneedle patches held steady drug delivery for 24 hours and caused minimal discomfort, underscoring how polymer science revitalizes mature molecules.[3]Zhen Gu, “A Wearable Osmotic Microneedle Patch Provides High-Capacity Sustained Drug Delivery in Animal Models,” Science Translational Medicine, science.org Such progress widens therapeutic windows and strengthens the competitive profile of the controlled release drug delivery market.

Shift toward once-weekly/monthly dosing

Long-acting lenacapavir cut HIV infections to zero over 5,300 subjects, illustrating demand for therapy that moves from daily pills to twice-yearly injections. Copolymer technology in Teva’s once-monthly olanzapine produced 92% patient satisfaction and shows how reduced visit load can reshape psychiatric care ir.tevapharm.com. These design shifts raise the growth ceiling for the controlled release drug delivery market by meeting payer and patient preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CMC & scale-up costs vs. conventional forms | −1.4% | Global, heavier in emerging markets | Medium term (2-4 years) |

| Complex multi-jurisdictional regulatory pathway | −1.1% | Global, varied by region | Long term (≥ 4 years) |

| API stability challenges inside long-acting matrices | −0.8% | Global, notable in biologics | Medium term (2-4 years) |

| Tight global supply of specialized GRAS excipients | −0.6% | Global, supply anchored in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CMC & scale-up costs vs. conventional forms

Sophisticated release coatings and multi-layer tablets demand analytical protocols that stretch development by up to two years relative to immediate-release pills, boosting cost and complexity. Smaller firms often outsource to CDMOs, paying a premium that narrows price competitiveness in cost-sensitive markets, tempering uptake within the controlled release drug delivery market.

Complex multi-jurisdictional regulatory pathway

Distinct bioequivalence and dissolution criteria among the FDA, EMA, and emerging-market agencies compel duplicate studies and site audits. Pending European restrictions on titanium dioxide illustrate how sudden excipient policy shifts can trigger full reformulations, delaying launches and dampening revenue visibility. Such uncertainty slows cross-border roll-outs in the controlled release drug delivery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Nano-carriers Drive Innovation Despite Transdermal Dominance

Transdermal platforms led the controlled release drug delivery market with a 31.83% revenue share in 2025, owing to ease of self-administration and proven manufacturing lines. Nano- and lipid-based systems, however, are set to post a 12.05% CAGR through 2031 as precision medicine rises. Osmotic pump tablets sustain zero-order kinetics unaffected by food intake, while implantable pumps meet oncology needs for local micro-dosing. LNPs leverage pandemic-era capacity to speed oncology and protein replacement programs, cementing their place in the controlled release drug delivery market.

Competitive focus now centers on carrier architecture. Branched-tail LNPs direct mRNA payloads to lung dendritic cells, widening respiratory applications. Push-pull osmotic tablets remove variability from gastric pH, aiding chronic disease control. Together these advances give manufacturers flexibility to match molecule, route, and patient need, helping the controlled release drug delivery market sustain robust innovation cycles.

By Route of Administration: Parenteral Growth Challenges Oral Supremacy

Oral units remained the largest route with 37.52% share of the controlled release drug delivery market size in 2025, supported by cost-efficient lines and high patient familiarity. Parenteral injectables will post an 11.23% CAGR to 2031 as biologics advance and device makers refine safety syringes. Transdermal products cater to opioid-sparing pain management and hormone care, while inhaled formats speed systemic entry for acute crises.

Direct bioavailability remains a core advantage. Teva’s generic Sandostatin LAR showed that mastering depot injections can unlock large revenue pools even when patents expire. Programmable injectors plus longer intervals ease clinic traffic, making injectables a top target for new entrants seeking differentiation within the controlled release drug delivery market.

By Polymer/Carrier Type: Lipid Systems Accelerate Past Traditional Polymers

PLGA / PLA matrices still anchor 25.94% of the controlled release drug delivery market share in 2025 for their predictable erosion and regulatory familiarity. Yet lipid nanoparticles are climbing at a 12.28% CAGR on the back of mRNA success. Ionizable lipids, phospholipids, cholesterol, and PEG lipids form a modular kit that scientists tune for organ specificity and immune avoidance, giving LNPs cross-therapy appeal.

Alternative polymers also gain ground. PEG blends raise solubility for hydrophobic APIs, while cellulose ethers lower cost for immediate global scaling. Evonik’s broad CDMO menu covers lipid nanoparticles, polymeric microparticles, and drug-loaded implants, allowing customers to transition smoothly between carriers as program needs evolve. This growing material toolkit broadens addressable indications and cements a high-growth outlook for the controlled release drug delivery market.

Geography Analysis

North America maintained leadership with 36.02% revenue in 2025, enabled by strong R&D outlays, rapid FDA breakthrough designations, and a deep skilled labor pool. Lilly’s USD 9 billion Indiana build-out for tirzepatide illustrates continuing commitment to complex production on-shore. Novo Nordisk’s USD 4.1 billion expansion in North Carolina doubles peptide capacity, securing supply for long-acting injectables. These investments strengthen local sourcing for the controlled release drug delivery market.

Asia Pacific is projected to be the fastest region with an 11.52% CAGR, powered by regulatory harmonization through the Pharmaceutical Inspection Co-operation Scheme and large-scale capital projects. China approved 40 innovative drugs in 2023 under accelerated reviews and logged 18,503 registration filings, underscoring pipeline depth. Lonza’s capsule lines in India and China and WuXi STA’s 169-acre Taixing API hub reveal supply-side commitment to support local and global demand.

Europe shows steady uptake. The region’s tight quality codes create a reputation edge that appeals to multinational sponsors. CordenPharma’s €900 million peptide platform expansion across Colorado and European sites bridges transatlantic supply for GLP-1 compounds in obesity and diabetes care. Lonza’s Innovaform Accelerator in France accelerates formulation co-development, giving EU clients fast access to controlled release expertise. Pan-regional alignment under the European Medicines Agency also helps smaller firms navigate the controlled release drug delivery market with fewer duplicative filings.

Competitive Landscape

The controlled release drug delivery market shows moderate consolidation. Top pharmaceutical firms lean on vertical integration to pair discovery with proprietary delivery, defending margins as small-molecule price pressure rises. Johnson & Johnson’s TAR-200 system earned FDA breakthrough status and posted an 82.4% complete response in high-risk NMIBC, demonstrating how device-drug combos can command premium pricing. Patent filings for branched lipids, silyl lipids, and nucleic acid carriers reinforce a steady innovation cadence across leading firms.

CDMOs gain share by offering turnkey capabilities for sponsors lacking capital or expertise. Lonza reorganized around core CDMO franchises and projects CORE EBITDA margins near 30% by 2025, revealing scale benefits in complex formulation services. Evonik positions as a preferred partner for polymeric systems, while Hovione’s joint venture with Zerion Pharma leverages Dispersome to fix drug solubility gaps. Strategic deals such as Merck’s USD 493 million license with Cyprumed for oral peptides show big-pharma appetite to buy proven platforms rather than build in-house.

Device companies broaden access with injection pens, smart pumps, and microneedle wearables. BD’s glass prefillable syringe integrated into YpsoMate delivers high-viscosity biologics, removing a barrier for subcutaneous GLP-1 drugs. Medtronic’s adaptive deep brain stimulation system ferries insights from real-time signals, hinting at future closed-loop delivery possibilities. Such devices expand the controlled release drug delivery market by linking formulation science with digital health.

Controlled Release Drug Delivery Industry Leaders

Johnson and Johnson

GlaxoSmithKline

Pfizer

Merck & Co.

Novartis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva and Alvotech won FDA interchangeability status for SELARSDI with Stelara.

- April 2025: Johnson & Johnson secured FDA approval for IMAAVY to treat generalized myasthenia gravis allowing for controlled and targeted drug release.

- March 2025: Mallinckrodt and Endo announced a merger to create a scaled diversified pharmaceutical leader.

- 2025: Johnson & Johnson initiated a New Drug Application for TAR-200 under the FDA Real-Time Oncology Review.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the controlled-release drug delivery market as the global revenues generated from prescription-grade dosage forms, oral, parenteral, transdermal, inhalation, ocular, and implantable, that are specifically engineered to dispense an active pharmaceutical ingredient at a planned rate for six hours or longer, thereby sustaining therapeutic plasma levels without repeated dosing.

Scope exclusion: Immediate-release tablets, bulk API sales, and over-the-counter nutraceutical slow-release products remain outside this assessment.

Segmentation Overview

- By Technology

- Micro-encapsulation

- Transdermal Systems

- Long-acting Injectable Depots

- Targeted Nano / Lipid Carriers

- Implantable Pumps & Stents

- Osmotic Pump Tablets

- By Route of Administration

- Oral Controlled-Release

- Parenteral (Injectable)

- Transdermal

- Inhalation

- Ocular

- By Polymer / Carrier Type

- PLGA / PLA

- PEG & PEG-blends

- Cellulose Derivatives

- Lipid Nanoparticles / SLNs

- Polyanhydrides

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews were completed with formulation scientists, contract development executives, hospital pharmacists, and reimbursement advisors across North America, Europe, and Asia Pacific. Discussions tested adoption rates of once-weekly injectables, typical price premiums over immediate-release generics, and realistic timelines for nano-carrier scale-up, allowing us to close data gaps uncovered during desk work.

Desk Research

We began by mining public domain data from tier-one bodies such as the US FDA Orange Book, European Medicines Agency authorization lists, and Japan's PMDA notifications that detail approved extended-release products and expiration of key patents. Production volumes and trade values for functional excipients were gathered from UN Comtrade and Eurostat, which hint at formulation activity by region. Industry-specific associations, for example, the Controlled Release Society, publish annual proceedings that outline pipeline technologies, while peer-reviewed articles in the International Journal of Pharmaceutics provide dissolution-profile benchmarks used to validate technical assumptions. Company 10-Ks, investor decks, and reputable press helped us map capacity additions and licensing deals. Our analysts also drew selectively on D&B Hoovers for sponsor financials and Dow Jones Factiva for transaction screening. This list is illustrative; many further sources were checked for data confirmation and nuance.

Market-Sizing & Forecasting

Our base year value pools were first estimated with a top-down construct that links national prescription spending to the share attributable to controlled-release formats, rebuilt from production and trade records of key excipients, prevalence-to-treated-cohort ratios in diabetes and pain management, and average ex-factory selling prices. Selected bottom-up checks, supplier roll-ups of major contract manufacturers and sampled ASP × unit volumes, served to challenge and refine the totals. Key variables in the model include chronic-disease incidence, patent expiry timelines, polymer cost curves, unit shift toward long-acting injectables, and regulatory approval counts. Five-year forecasts were generated through multivariate regression with lagged inputs for geriatric population growth and R&D outlay, supplemented by scenario analysis for high-price biologic launches. Data gaps in country splits were bridged using nearest-neighbor averages and validated with distributor channel feedback.

Data Validation & Update Cycle

Outputs undergo variance checks versus historical sales, excipient shipment tonnage, and hospital procurement dashboards. Any anomaly above two standard deviations triggers analyst re-contact of sources before sign-off. Mordor Intelligence refreshes the model annually and issues interim tweaks after material events such as blockbuster approvals. Right before publication, an analyst reruns the update routine so clients receive the freshest baseline.

Why Mordor's Controlled Release Drug Delivery Baseline Stands Up to Scrutiny

Published figures can vary because firms diverge on dosage-form scope, apply distinct price-mix assumptions, or freeze exchange rates at different points.

Our disciplined inclusion of only prescription-grade extended-release formats, coupled with yearly refreshes and dual-path validation, keeps our baseline firmly tethered to traceable variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 66.9 B (2025) | Mordor Intelligence | - |

| USD 54.3 B (2023) | Global Consultancy A | Older base year and static currency conversion; limited primary validation |

| USD 61.1 B (2024) | Regional Consultancy B | Excludes inhalation and ocular routes; applies uniform ASP escalation |

| USD 66.2 B (2024) | Trade Journal C | Relies on shipment weight proxies without therapy-area adjustment |

Taken together, the comparison shows that when scope breadth, refresh cadence, and cross-checks are factored in, our analysts deliver a balanced, decision-ready baseline that executives can trace back to clear drivers and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the controlled release drug delivery market?

The market is worth USD 73.28 billion in 2026 and is on track to reach USD 115.34 billion by 2031.

Which technology segment is growing fastest?

Targeted nano- and lipid-based carriers are expanding at a 12.05% CAGR, making them the technology growth leader.

Why is Asia Pacific growing quickly in this space?

Accelerated regulatory harmonization, large patient pools, and new manufacturing plants are pushing Asia Pacific to an 11.52% CAGR.

What are the main hurdles for companies entering this market?

High Chemistry, Manufacturing, and Controls (CMC) costs and multi-region regulatory complexity raise both capital and time requirements.

How does controlled release benefit patients with chronic diseases?

Longer-acting formulations cut dosing frequency, improve adherence, and often reduce side effects by smoothing plasma concentration profiles.

Which polymers dominate current controlled release products?

PLGA / PLA systems remain the most used polymers today, though lipid nanoparticles are moving up fastest thanks to mRNA vaccine infrastructure.

Page last updated on: