Ostomy Drainage Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 3.82 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

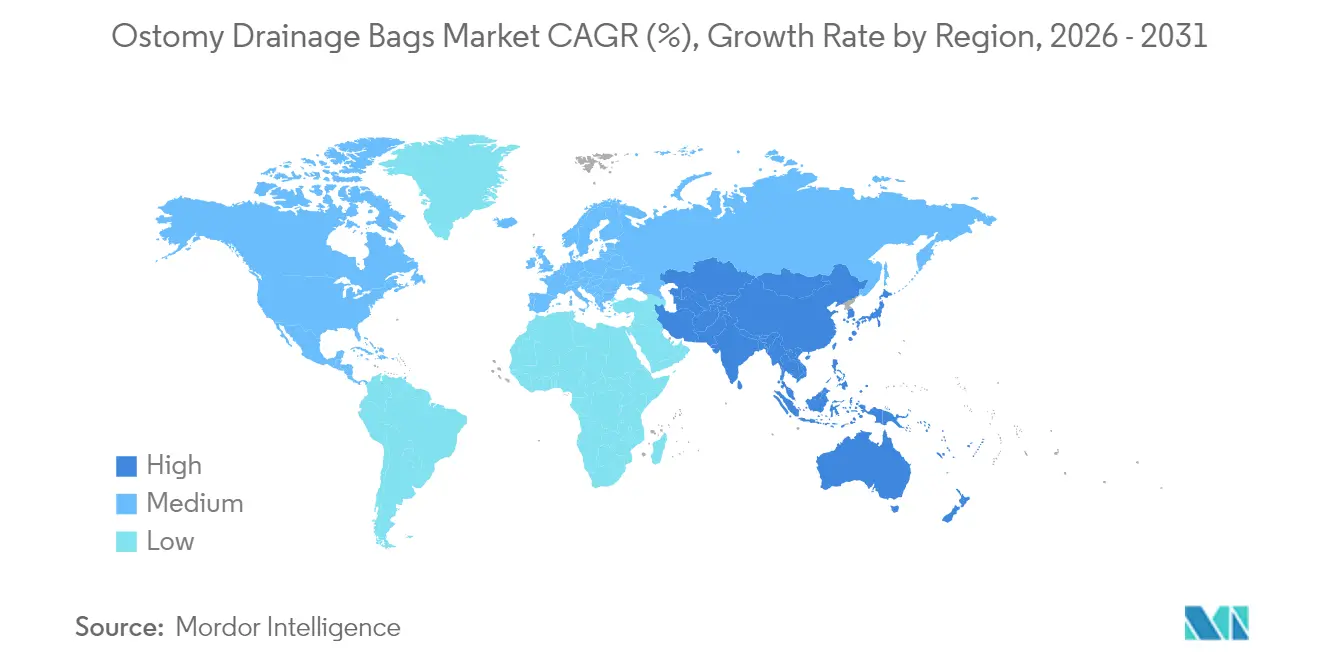

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

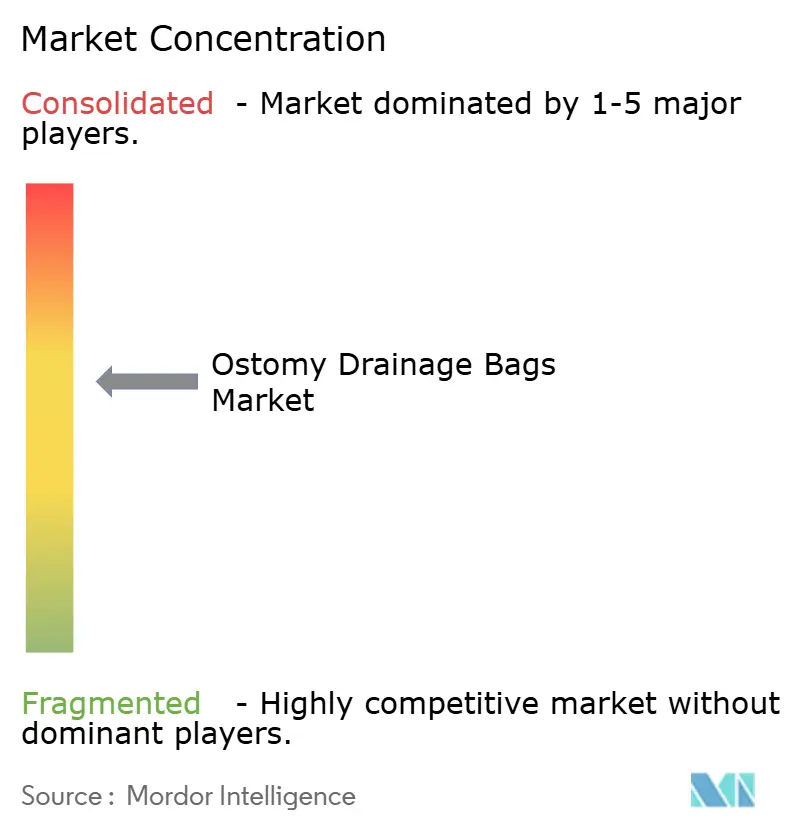

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ostomy Drainage Bags Market Analysis by Mordor Intelligence

The Ostomy drainage bags market size is expected to grow from USD 2.94 billion in 2025 to USD 3.07 billion in 2026 and is forecast to reach USD 3.82 billion by 2031 at 4.44% CAGR over 2026-2031. Demographic momentum is the core catalyst, as an expanding pool of older surgical candidates carries higher comorbidity levels that lengthen postoperative ostomy usage. Converging with age trends, the global rise in inflammatory bowel disease and cancer surgeries keeps procedural volumes on an upward path, while smart-sensor pouches reposition the category as part of digital health rather than a commodity appliance. Subscription-based home-delivery services improve adherence and cut stock-out risk, and healthcare sustainability rules encourage fresh research into recyclable films and hydrocolloid blends. Together, these forces shape a predictable but opportunity-rich environment for both incumbents and new entrants in the Ostomy drainage bags market.

Key Report Takeaways

- By type, colostomy bags held 45.32% of the Ostomy drainage bags market share in 2025; ileostomy bags are projected to post the fastest 4.78% CAGR to 2031.

- By system configuration, one-piece products controlled 59.46% revenue in 2025, whereas two-piece systems are forecast to expand at a 5.02% CAGR through 2031.

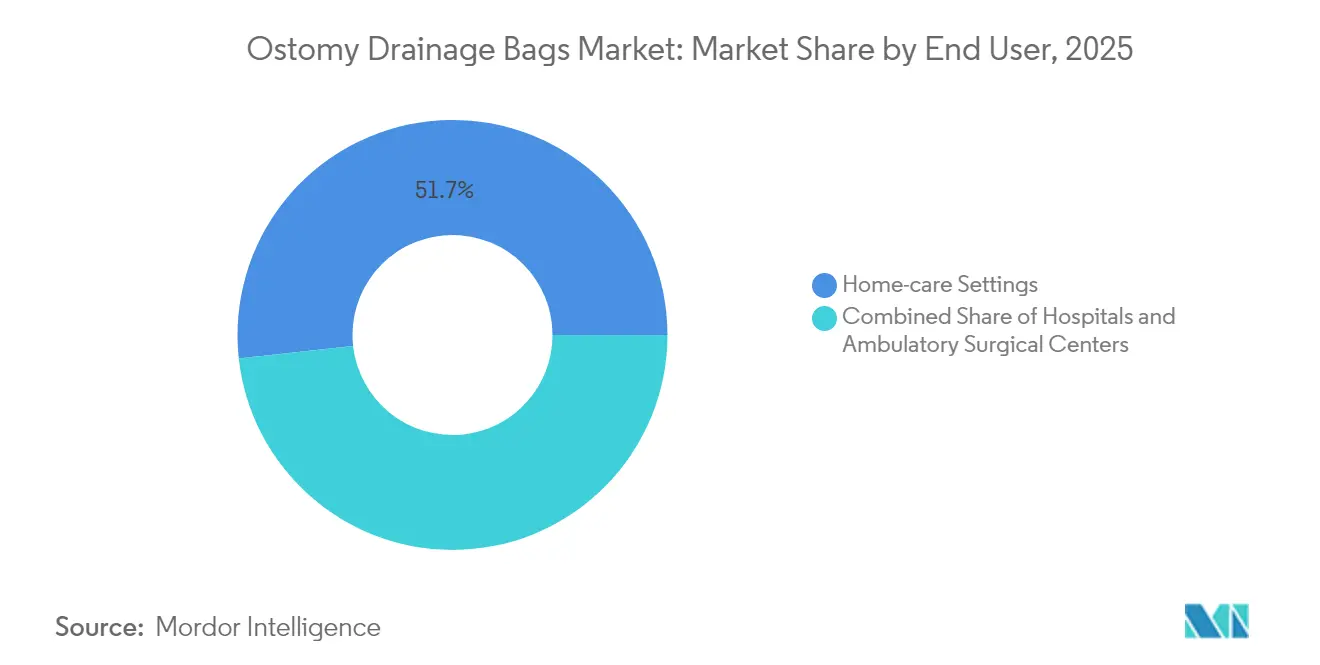

- By usability setting, home-care accounted for 51.74% of the Ostomy drainage bags market size in 2025 and hospitals represent the highest 5.07% growth outlook to 2031.

- By distribution channel, direct tender procurement held 55.10% of revenue in 2025, while retail and e-commerce are advancing at a 5.18% CAGR on the back of subscription models.

- By geography, North America commanded 41.42% of the Ostomy drainage bags market in 2025, yet Asia-Pacific shows the quickest 5.65% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Ostomy Drainage Bags Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic wounds & diabetic ulcers | +1.4% | Global, with highest impact in North America & Europe, accelerating in APAC | Long term (≥ 4 years) |

| Escalating volume of surgical procedures worldwide | +1.2% | Global, with emerging markets showing fastest growth | Medium term (2-4 years) |

| Technological shift toward moist-active & NPWT‐integrated dressings | +0.9% | North America & Europe leading, expanding to developed APAC markets | Medium term (2-4 years) |

| Sustainability mandates spurring adoption of bio-derived collagen, chitosan, and alginate dressings | +0.8% | Europe & North America primarily, selective APAC adoption | Long term (≥ 4 years) |

| Expanding reimbursement for home-based wound care in OECD nations | +0.7% | OECD countries, with spillover to upper-middle-income markets | Short term (≤ 2 years) |

| Adoption of smart/connected dressings with real-time monitoring | +0.6% | North America & Europe initially, gradual APAC expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Inflammatory Bowel Disease

New epidemiological updates confirm that ulcerative colitis and Crohn’s disease continue to affect a wider segment of adults and seniors, prompting earlier and more frequent ostomy interventions. Specialist centers in North America already treat well over 2.5 million residents living with IBD, and clinicians expect the present caseload to tilt further toward patients aged over 60. Payer databases show that direct IBD care costs now exceed USD 27 billion annually in the United States, much of which relates to surgical diversion episodes that necessitate advanced pouching systems. Emerging economies such as India and China register rapid year-over-year jumps in newly diagnosed IBD yet have limited stoma-care infrastructure, creating a high-growth frontier for the Ostomy drainage bags market. Device developers therefore tailor portfolio extensions that address both the high-volume basic segment and specialist lines for hard-to-seal peristomal skin. Heightened clinical attention on quality-of-life metrics further elevates demand for products with secure adhesives, thin profiles and user-friendly closures.

Rapidly Growing Aging Population

Hospital discharge records for 2024 show a noticeable shift toward older and heavier surgical candidates, with four in every five elective colorectal operations now involving a patient who presents above normal BMI levels [1]International Journal of Surgery, “Changing Surgical Demographics and Comorbidity Profiles,” ijsurgery.com. Higher age correlates with greater ostomy-related complications such as skin irritation, herniation and leakage anxiety, expanding the requirement for premium hydrocolloid barriers that flex with abdominal contour changes. Diabetes prevalence among surgical patients is climbing past 15%, adding wound-healing challenges that push clinicians toward longer-wear pouches incorporating antibacterial layers. Home-based tele-monitoring garners acceptance among geriatric users, with recent studies showing 95% concordance between remote and bedside stoma assessments, a finding that strengthens reimbursement arguments for connected devices. Collectively, these dynamics add meaningful incremental volume to the Ostomy drainage bags market while also raising the average selling price through technology-rich features.

Rising Colorectal and Bladder Cancer Cases

The American Cancer Society projects more than 2 million new cancer diagnoses in the United States during 2025, keeping resection-related stoma creation at a consistently high level [2]American Cancer Society, “Cancer Facts & Figures 2025,” cancer.org. Techniques such as temporary ileostomy after low-anterior resection aim to protect anastomotic sites yet still require months of dependable pouching. In bladder cancer care, average direct treatment expenses almost double in the year following cystectomy, with over 85% of patients reporting at least one post-operative complication that extends pouch dependency. Surgical teams in high-volume centers increasingly select cutaneous ureterostomy for frail individuals to shorten theater time, which sustains separate demand for urine-specific drainage bags with anti-reflux valves. Oncology guidelines also promote trimodal organ-preservation therapies, creating cyclic demand spikes for temporary stoma supplies during chemoradiation. These patterns reinforce a resilient volume baseline throughout the Ostomy drainage bags market.

Emergence of Smart-Sensor Ostomy Bags

Coloplast brought the first leakage notification system to market in mid-2024, pioneering real-time stoma-output tracking for consumer and clinician dashboards. Early usability trials reveal a strong preference for connected pouches, with 65% of surveyed users favoring sensor-enabled products over legacy models when both are available. Academic teams at Stanford University demonstrate that a wearable ostomy monitor can provide flow-rate data with an R² above 0.90, validating the technical feasibility of predictive alarms [3]ClinicalTrials.gov, “Stanford Smart Ostomy Sensor Study,” clinicaltrials.gov. Regulatory agencies have begun to clear predicate devices under the 510(k) pathway, smoothing the route for successive launches that overlay machine-learning analytics on drainage patterns. Device makers expect premium pricing and recurring app-subscription revenue to lift the overall value captured per user inside the Ostomy drainage bags market, particularly in North America and Western Europe during the next three years.

Restraints Impact Analysis of Ostomy Drainage Bags Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unstructured or shrinking reimbursement coverage | -0.7% | North America & Europe primarily | Short term (≤ 2 years) |

| High cost of advanced multi-layer barrier materials | -0.5% | Global, with higher impact in price-sensitive markets | Medium term (2-4 years) |

| Environmental disposal restrictions on single-use plastics | -0.4% | Europe & developed markets, expanding globally | Long term (≥ 4 years) |

| Supply-chain vulnerability for medical-grade resins | -0.3% | Global, with acute impact in specialized markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unstructured or Shrinking Reimbursement Coverage

Medicare caps on monthly pouch quantities and recent HCPCS code adjustments increase provider paperwork and may delay beneficiary access to upgraded appliances. Private insurers in the United States impose variable prior-authorization thresholds or coinsurance levels, prompting some patients to stretch wear-time at the expense of skin health. Policy divergence across European payers magnifies disparity; for example, a regional Medicaid program in the southern United States now requires explicit medical-necessity proof for accessories such as barrier rings, whereas a neighboring state imposes no copayment but limits closed-end pouches. In Japan, toughened cost-containment rules cut reimbursement lists for imported devices, urging suppliers to justify incremental performance benefits with real-world evidence. Such hurdles temper short-term uptake of premium two-piece systems in the Ostomy drainage bags market until coverage clarity improves.

High Cost of Advanced Multi-Layer Barrier Materials

Hydrocolloid-based skin barriers that feature rebound memory or moldable edges rely on specialized resins manufactured in comparatively small industrial batches, keeping input costs high. ConvaTec’s proprietary Moldable Technology™ depends on advanced compounding steps that raise unit margins yet also require tight supplier control. When a film producer exited the healthcare segment in 2024, several pouch makers faced temporary shortages that underlined raw-material concentration risk. Even as polymer firms such as Syensqo announce capacity additions, medical-grade adhesive sheets still command premium pricing due to traceability and purity mandates. Environmental compliance adds another layer: upcoming European recycling targets demand redesigned laminates that meet both barrier integrity and circular-economy goals, a shift that will likely raise cost of goods in the Ostomy drainage bags market during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ostomy Drainage Bags Market Segment Analysis

By Type:

Colostomy Leadership While Ileostomy AcceleratesColostomy bags maintained 45.32% revenue leadership in 2025 due to steady colorectal cancer volumes and high prevalence of diverticular disease. This dominant position supplies a reliable baseline for the Ostomy drainage bags market, especially in North America and Western Europe where permanent stomas remain common. Temporary diversion patterns from low-anterior resection continue to shape product roadmaps toward softer plates and low-profile flanges that improve discretion during social activity. In parallel, ileostomy bags register the briskest 4.78% CAGR through 2031, supported by the climbing burden of inflammatory bowel disease among adults under 50. Surgeons favor loop ileostomy to protect anastomoses, a choice that drives higher pouch change frequency and thus raises per-patient consumption inside the Ostomy drainage bags market size.

The short fluidic output of ileostomies spurs demand for high-capacity drainable options with lockable tap valves, while colostomy users prioritize odor barriers and filter reliability. R&D teams now integrate gas-selective membranes into both segments, aiming to curb ballooning without compromising discretion. On the urinary side, cutaneous ureterostomy gains traction for frail patients, and this procedure raises the need for specialized anti-reflux urostomy pouches. Continent diversions such as K-pouch present a niche but clinically significant area where internal reservoirs still require external night drainage, opening another micro-specialty for innovators within the Ostomy drainage bags market.

By System Type:

Modularity Boosts Two-Piece AdoptionOne-piece appliances captured 59.46% revenue in 2025 as their all-in-one design appeals to elderly or dexterity-limited users. These systems reduce handling steps and minimize potential misalignment between barrier and pouch. Yet two-piece systems are advancing at a 5.02% CAGR because modularity resonates with active users who value the freedom to replace either component without disturbing the other. Clinical audits reveal that more than 90% of moldable two-piece users report easier application after structured nurse training, translating into lower peristomal skin complications and longer wear-time. Lock-and-roll closures as well as audible coupling clicks further elevate user confidence and fuel brand loyalty across the Ostomy drainage bags market.

Manufacturing investments in injection-molded coupling rings bring down cost differentials, narrowing the historic price gap between formats. This shift, combined with payers’ growing focus on total-care cost rather than unit price, underpins the two-piece momentum. In the premium tier, connected sensor wafers currently launch only for flat plates, yet roadmaps indicate curved and convex versions will follow, allowing two-piece configurations to capture the earliest volumes in the smart-device niche of the Ostomy drainage bags market size.

By Usability:

Drainable Dominance With Closed-End MomentumDrainable pouches accounted for 63.05% of 2025 shipments because their empty-and-reuse design aligns with ileostomy and urostomy needs. Recent drainable models embed transparent viewing windows that assist stoma nurses during remote coaching sessions, a key benefit for telehealth deployment. Closed-end pouches, however, deliver a 5.09% CAGR through 2031 on the back of colostomy demand for odor containment and one-handed disposal simplicity. Manufacturers differentiate via charcoal or zeolite filters that manage flatus without compromising water barrier performance, keeping closed-end products competitive in urban consumer channels.

Innovation merging the two lines is emerging in the form of hybrid pouches that allow drainable functionality for daytime use and closed-end seals for social events, supporting lifestyle versatility. Smart-sensor pilots predominantly focus on drainable platforms because of easier flow-rate measurement, yet firmware updates under evaluation aim to adapt leakage algorithms to closed-end formats as well. These technical pathways ensure that both sub-segments sustain recurrent upgrades, continuously expanding overall value extraction from the Ostomy drainage bags market.

By End User:

Hospitals Regain Share Amid Rising Surgical ComplexityHome-care environments represented 51.74% of end-user demand in 2025, reflecting strong adoption of outpatient care models and aging-in-place preferences. Tele-consultation adoption accelerated during recent public-health emergencies, propelling ostomy supply firms to bundle virtual nurse sessions with starter kits. Hospitals nonetheless show a faster 5.07% CAGR, driven by complex cancer surgeries that extend inpatient stays and necessitate on-site stoma management training. Institutions are standardizing formularies around high-wear products with advanced leak barriers to curb readmission risk, thereby lifting average revenue per procedure in the Ostomy drainage bags market.

Ambulatory surgical centers act as an efficiency bridge, handling uncomplicated closures and reversals yet still stocking an optimised pouch line to support immediate discharge. In both inpatient and outpatient settings, value-based care contracts reward suppliers who can prove reduced skin breakdown episodes, making clinical outcome data an increasingly important tender determinant. Home-care operators collaborate with subscription portals to automate restocking, maintaining continuity of care for frail or mobility-limited patients and reinforcing retention in the Ostomy drainage bags market.

By Distribution Channel:

Digital Commerce Redefines EngagementDirect tender procurement secured 55.10% of 2025 revenue as hospitals and group purchasing organizations consolidate volume under multiyear contracts for predictability and price discipline. Retail pharmacies and e-commerce are expanding at a 5.18% CAGR, however, reflecting the consumerization of chronic-care supplies. Leading web platforms now embed secure chat with certified ostomy nurses, step-by-step video tutorials, and lifestyle forums, turning a transactional reorder into a holistic support interaction. Automated subscription shipments match Medicare-allowed monthly pouch quantities, eliminating last-minute shortages that can trigger emergency visits.

Vendors are deploying AI recommendation tools that analyze leakage incidents, body-shape changes, and mobility to personalize product selection across the Ostomy drainage bags market. Regulators already remind online sellers to retain prescription evidence for restricted accessories; yet, compliance audits indicate that mature e-commerce pharmacies meet these criteria through electronic health record integration. Market watchers anticipate that transparent pricing, combined with doorstep convenience, will continue to erode the market share of legacy distributors unless those incumbents raise their service levels beyond simple fulfillment.

Geography Analysis

North America Ostomy Drainage Bags Market

North America owned 41.42% of global revenue in 2025 because of its advanced surgical infrastructure, broad insurance coverage and early adoption of sensor-enabled devices. The United States remains the region’s anchor, supported by more than 2 million projected new cancer cases during 2025 and strong physician loyalty to premium moldable wafers. Canada contributes steady volume growth through nationwide stoma-nurse networks that help keep complication rates low and justify higher average selling prices. In Mexico, expanding private hospital chains now mirror U.S. formularies, fostering fresh demand for two-piece appliances with lock-in coupling systems and filter upgrades.

Europe Ostomy Drainage Bags Market

Europe generates balanced growth as universal health schemes favor cost-effectiveness while still endorsing products that demonstrate tangible skin-health benefits. Germany and France promote specialist stoma clinics that encourage best-practice adoption, while Italy and Spain remain price-focused but increasingly receptive to connected leak-alert add-ons. Environmental legislation is a prominent agenda item; the upcoming EU Packaging and Packaging Waste Regulation requires full pouch packaging recyclability by 2035 for healthcare, urging suppliers to expedite thinner multilayer film research. Such regulation shapes product design decisions and could expand the Ostomy drainage bags market share of companies with early compliant portfolios.

APAC Ostomy Drainage Bags Market

Asia-Pacific is the most dynamic territory, clocking a 5.65% CAGR to 2031 as healthcare infrastructure investment accelerates. China’s ongoing hospital construction boom and widening social-insurance coverage allow international brands to distribute premium two-piece and smart-sensor models beyond top-tier cities. ConvaTec reported double-digit ostomy sales growth in China during 2024, underscoring local appetite for higher-performance solutions. India shows fast-rising IBD incidence that stretches stoma nursing resources, but the private-hospital segment is increasingly sourcing high-capacity drainable pouches to limit peristomal dermatitis. Japan’s reimbursement cuts temper near-term price escalation, yet local clinicians maintain a preference for high-quality skin barriers, sustaining stable unit value. Australia, South Korea and select Southeast Asian economies extend regional momentum through aging populations and rising colorectal screening programs, together ensuring that the Ostomy drainage bags market remains on a multi-year growth trajectory.

Regulatory Landscape

In the United States, ostomy pouches and accessories are regulated by the US Food and Drug Administration (FDA) under 21 CFR 876.5900 as Class I (general controls) devices and are generally exempt from 510(k) premarket notification, subject to the regulation's limitations. Even with this exemption, manufacturers still work under general controls, including establishment registration, device listing, labeling, and quality system expectations appropriate to the device. In practice, this affects change-control discipline for materials, filters, and closure designs used in ostomy drainage bags.

In the European Union, market access is governed by the Medical Devices Regulation (EU) 2017/745 (MDR), which continues to shape technical documentation and conformity assessment requirements across ostomy portfolios. MDCG 2021-24 Rev.1 provides classification guidance that indicates ostomy bags are typically Class I, while intended uses involving certain breached-skin conditions can move classification higher. That shift tightens evidence and assessment requirements, increasing the need for accurate intended-use statements and claims for advanced pouching and skin-contact material variants.

Value Chain Analysis

The value chain for ostomy drainage bags begins with upstream suppliers of medical-grade polymers and films (including polyethylene-based structures and multi-layer barrier constructions) and adhesive chemistry inputs for hydrocolloid-based skin-contact materials. Converters then co-extrude or laminate films and prepare backing layers and filter media. Finished-device manufacturers complete pouch converting and assembly steps, including die-cutting, sealing, integration of closures, coupling rings for two-piece systems, and the addition of filters or valves. These steps are typically supported by packaging and, where applicable, sterilization and release testing under regulated quality systems.

Downstream, demand is fulfilled through institutional channels, including direct tender and group purchasing in hospitals and health systems, as well as home-care distribution models that use pharmacy, retail, and e-commerce subscription replenishment. Bottlenecks and risk points tend to cluster around medical-grade film availability, consistency of specialized adhesive formulations, and change-management burdens when material substitutions become necessary. This is especially sensitive where compliance expectations under FDA general controls (21 CFR 876.5900) and EU MDR documentation can slow reformulation and supplier switching.

Competitive Landscape

The Ostomy drainage bags market displays moderate concentration, with a handful of multinationals leveraging proprietary adhesives and widening geographic footprints to defend share. Coloplast differentiates via the first commercial leakage notification pouch, securing an early-mover position in connected stoma management and building a data-analytics platform that could evolve into subscription revenue. B. Braun and Hollister emphasize convexity options and wafer thickness diversity to address niche body profiles, whereas Salts Healthcare and Welland Medical exploit localized relationships with stoma nurses in the United Kingdom and Ireland.

Sustainability and supply-chain resilience dominate strategic planning. Several suppliers enter forward contracts for medical-grade polyethylene to avoid sudden shortages, and more firms vertically integrate adhesive coating to insulate against vendor withdrawals. Research consortia involving material science companies and universities investigate polyhydroxyalkanoate film that meets both biodegradability and moisture-vapor-transmission needs, a capability likely to serve as a future point of differentiation. At the same time, software developers are partnering with ostomy leaders to create algorithmic leak predictors, indicating a convergence between medtech and digital-health ecosystems within the Ostomy drainage bags market.

Competitive pressure also arises from service innovation. Direct-to-patient portals capture reorder data that historically belonged to wholesalers, reducing channel opacity and enabling dynamic pricing models. Manufacturers accelerate investment in multilingual tele-nursing teams that can be bundled with premium pouches, offering hospitals assurance of post-discharge support. The resulting landscape balances technological prowess, channel strength and end-user experience, making it difficult for low-cost entrants to erode incumbents without matching at least two of those dimensions.

Ostomy Drainage Bags Industry Leaders

Alcare Co. Ltd

B Braun Melsungen AG

Coloplast AS

ConvaTec Inc.

Flexicare Medical Ltd

- *Disclaimer: Major Players sorted in no particular order

Ostomy Drainage Bags Market Companies Covered in this Report

- Alcare

- B. Braun

- Coloplast

- Convatec

- Hollister

- Flexicare Medical

- Marlen Manufacturing

- Pelcin Healthcare

- Salts Healthcare

- Torbot Group

- Welland Medical

- Prowess Care

- Goodhealth

- Oakmed Healthcare

- 3M

- Genairex Inc.

- Cymed Ostomy Co.

- Nu-Hope Laboratories

- Jiangsu Steadlive Medical

Market Opportunities and Future Outlook

Smart and predictive leakage-notification capability remains a clear area for differentiation beyond passive collection, backed by continued technical work on monitoring moisture propagation and adhesive performance. A January 2026 published patent application describing an ostomy appliance using electrode multiplexing for predictive leakage notification points to ongoing R&D that can support premium tiers through sensor-enabled pouches and companion analytics, consistent with the report's shift toward connected ostomy systems.

At the same time, purchasing and reimbursement mechanics create near-term execution opportunities for suppliers that can secure standardized access while sustaining clinical performance. In the United States, group purchasing agreements remain a primary route to scaled uptake for core ostomy portfolios, and policy attention around CMS competitive bidding for ostomy supplies in 2026 has increased stakeholder focus on access, product categorization, and contractor coverage structure, reflecting updated trade association guidance. These conditions favor manufacturers that pair strong GPO reach with home-delivery fulfillment and patient-support services, while still leaving room for portfolios designed to fit tighter price corridors without compromising wear-time, leak protection, or skin-health outcomes.

Recent Industry Developments in Ostomy Drainage Bags Market

- July 2026: Coloplast entered into a renewed two-year national group purchasing agreement with Vizient, effective July 1, 2026. The renewal supports continuity of access for Coloplast ostomy care offerings in large US health systems and reinforces the role of GPO contracting in standardizing hospital procurement for pouching systems.

- May 2026: Coloplast reported progress in its Ostomy Care business in its interim financial reporting for H1 2025/26, with performance linked to the SenSura Mio portfolio, including Convex variants. The update points to continued product mix and portfolio strength in premium segments that underpin differentiation in ostomy drainage bags.

- July 2024: Coloplast introduced a digital leakage notification system for ostomy users, enabling mobile alerts and clinician dashboard integration. The launch helped reposition parts of ostomy drainage bags from commodity consumables toward connected care, supporting premium pricing and service-led engagement models.

Ostomy Drainage Bags Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers ostomy drainage bags used to collect stool or urine after colostomy, ileostomy, or urostomy procedures, across hospital discharge use and home care use. Values are captured in USD for the defined geography set and time period.

Scope exclusions: Accessories used with ostomy care, such as skin barriers, belts, deodorizers, and irrigation kits, are not counted.

Segments Covered in This Report

- By Type

- Colostomy Bags

- Ileostomy Bags

- Urostomy Bags

- Continent Ileostomy & Urostomy Bags

- By System Type

- One-piece Bags

- Two-piece Bags

- By Usability

- Drainable

- Closed-end

- By End User

- Home-care Settings

- Hospitals

- Ambulatory Surgical Centers

- By Distribution Channel

- Direct Tender

- Retail & E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the starting demand pool and pricing context, we relied on public clinical and health statistics and then aligned them with device usage patterns. Sources included CDC cancer statistics, WHO health datasets, OECD health spending series, and PubMed-indexed publications that report ostomy incidence and post-surgery care needs.

We also reviewed regulatory and trade signals to understand product availability and adoption, such as FDA device databases and national customs and trade statistics where relevant, plus company filings, investor presentations, and reputable medical-association websites. A paid subscription for company financials and another for patents were used selectively to sanity-check revenue exposure and material or technology shifts, especially around pouch materials and odor-control features. The sources listed here are illustrative, and additional public references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to pressure-test the desk assumptions, especially around one-piece versus two-piece usage, drainable versus closed-end preference, and typical replacement frequency in home care. We spoke with a mix of manufacturers, distributors, clinicians involved in stoma care, and procurement or category managers, then checked how those inputs differed across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 42% |

| Mid tier: 55% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 17% | Managers: 48% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach, where procedure volumes and treated ostomy population indicators were reconstructed by region and converted into annual pouch consumption using replacement frequency assumptions. Once that demand base was established, it was valued using average selling prices that differ by system type (one-piece versus two-piece), usability (drainable versus closed-end), and setting of care.

To keep the totals realistic, we corroborated the model with selective bottom-up checks, such as sampled channel price points, distributor mark-up ranges, and supplier revenue exposure for the relevant product families, then adjusted where reporting is not consistent across countries. Key inputs used as fingerprints included ostomy procedure mix (colostomy, ileostomy, urostomy), aging population trends that influence surgery volumes, reimbursement and tender behavior in large markets, and the pace of home care adoption that shifts replacement patterns.

Forecasts were generated using scenario analysis supported by short series smoothing, varying procedure growth, reimbursement stability, and price progression assumptions, then aligning the outputs with what interviewees considered plausible. ASP progression used a simple logic that separates mix shift toward premium products from inflation and currency effects, keeping the forecast explainable and repeatable.

Data Validation & Update Cycle

Outputs were validated through cross-checks against independent signals, including procedure and patient pool ranges from public health statistics, plus pricing sanity checks from channel observations and interview feedback. If the model showed step-changes that could not be explained by procedure trends, reimbursement, or mix, we revisited the underlying inputs and triggered follow-up questions with relevant respondents.

Before sign-off, the full model went through multi-step analyst review, where assumptions, unit conversions, and currency handling were checked for consistency across regions. Reports are refreshed annually, and interim updates are made when a material change affects pricing, reimbursement, or procedure volumes. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Ostomy Drainage Bags Market Sizing Compared With Other Published Estimates

It is normal to see different market sizes published for ostomy drainage bags, even when the topic name looks the same. The gaps usually come from what is included in the product boundary, which year is treated as the base, and how pricing is translated into USD when currencies have moved.

When refresh cadence is tighter, currency conversion timing is consistent, and ASP logic is re-checked against current channel signals, the total tends to stay closer to the real purchasing pattern. This is the approach used in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.07 B (2026) | |

| Trade Publisher A | USD 3.10 B (2024) | Uses an earlier base year and does not clearly separate drainage bags from adjacent ostomy accessories, which can shift the counted revenue and the implied price level. |

| Industry Research Group B | USD 1.84 B (2024) | Appears to apply a narrower priced demand pool and may undercount home care replacement frequency, which reduces the implied annual unit consumption per patient. |

The table shows that the spread is mostly explained by what gets counted as a bag-only market and how volumes and prices are refreshed into a single USD year. By keeping the model tied to procedure mix, replacement frequency, and observable price points, the final number stays traceable to simple inputs that can be rechecked over time.

Key Questions Answered in the Report

What is the current Global Ostomy Drainage Bags Market size?

The Ostomy drainage bags market size is valued at USD 3.07 billion in 2026 and is projected to reach USD 3.82 billion by 2031

Who are the key players in Global Ostomy Drainage Bags Market?

Alcare Co. Ltd, B Braun Melsungen AG, Coloplast AS, ConvaTec Inc. and Flexicare Medical Ltd are the major companies operating in the Global Ostomy Drainage Bags Market.

Which is the fastest growing region in Global Ostomy Drainage Bags Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Ostomy Drainage Bags Market?

In 2025, the North America accounts for the largest market share in Global Ostomy Drainage Bags Market.

How fast is the Asia-Pacific market for ostomy drainage bags growing?

Asia-Pacific shows the strongest regional outlook with a 5.65% CAGR forecast through 2031, driven by expanding healthcare access and higher IBD incidence.

Page last updated on: