Commercial Helicopters Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 7.13 Billion |

| Market Size (2031) | USD 9.03 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

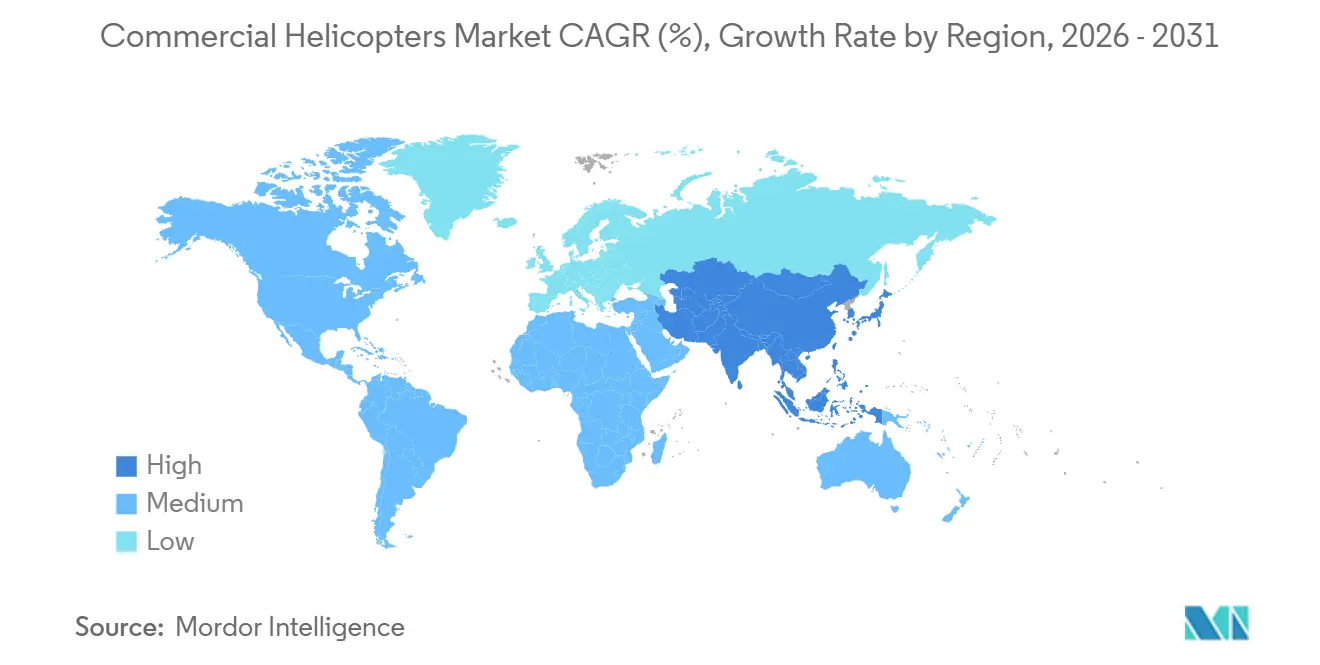

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Helicopters Market Analysis by Mordor Intelligence

The commercial helicopters market size is expected to grow from USD 6.80 billion in 2025 to USD 7.13 billion in 2026 and is forecasted to reach USD 9.03 billion by 2031 at a 4.85% CAGR over 2026-2031. The growth stems from brisk offshore wind construction, a pivot to outsourced emergency medical fleets, and stricter noise rules that favor next-generation twin-engine designs. Contract momentum is visible in CHC Helicopter’s multi-year deal with Ørsted for North Sea and Baltic crew transfer, NHV Group’s new Vestas assignments, and Global Medical Response’s January 2025 purchase of 28 Airbus H140s with single-pilot IFR capability. Heavy twin adoption also reflects record wildfire seasons that drove US federal and state agencies to award USD 180 million in exclusive-use contracts for 2025 and to accept seven Sikorsky S-70i Firehawks into CAL FIRE service during the 2024-2025 period. OEMs are positioning for sustainable fuel and hybrid-electric retrofits; Bell flew its 505 for more than 700 hours on 100% SAF in 2024, while Airbus demonstrated neat-SAF operations on an H225 in September 2024.

Key Report Takeaways

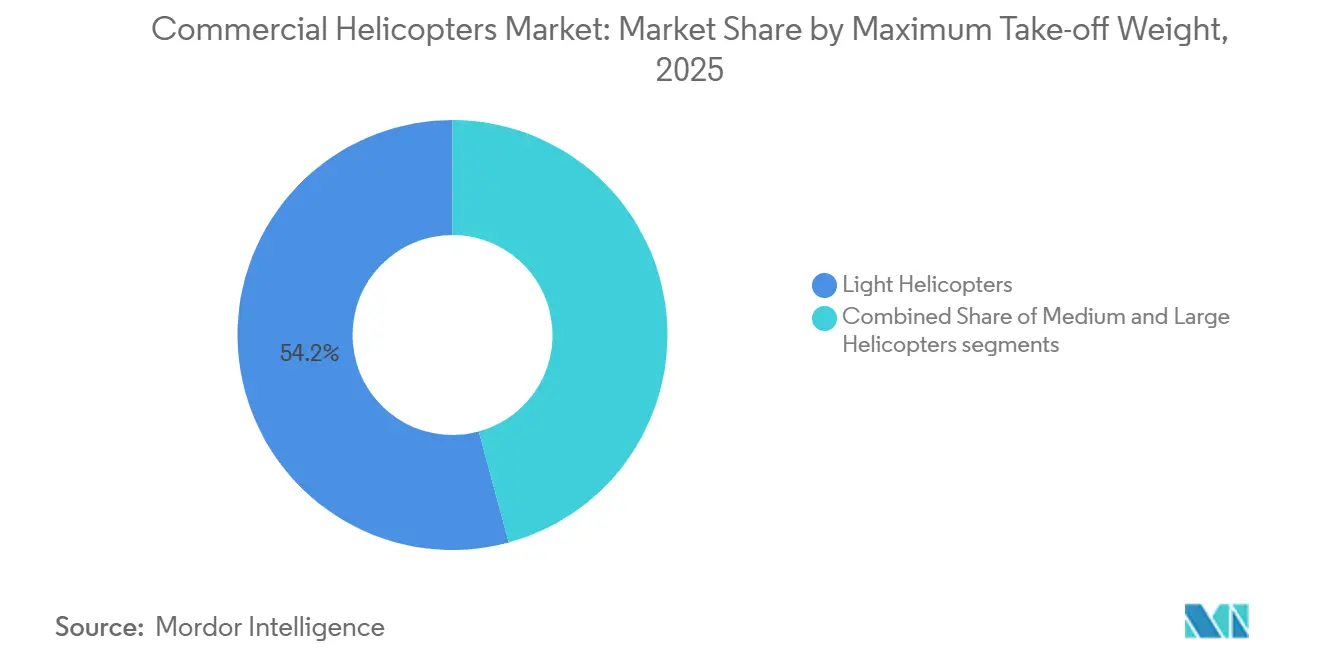

- By maximum take-off weight, light helicopters below 3.1 tons commanded 54.21% of the commercial helicopters market share in 2025; heavy platforms above 9 tons are projected to advance at a 6.92% CAGR through 2031.

- By number of engines, single-engine rotorcraft held 63.34% share of the commercial helicopters market in 2025, while twin-engine variants are expected to grow at 6.27% through 2031.

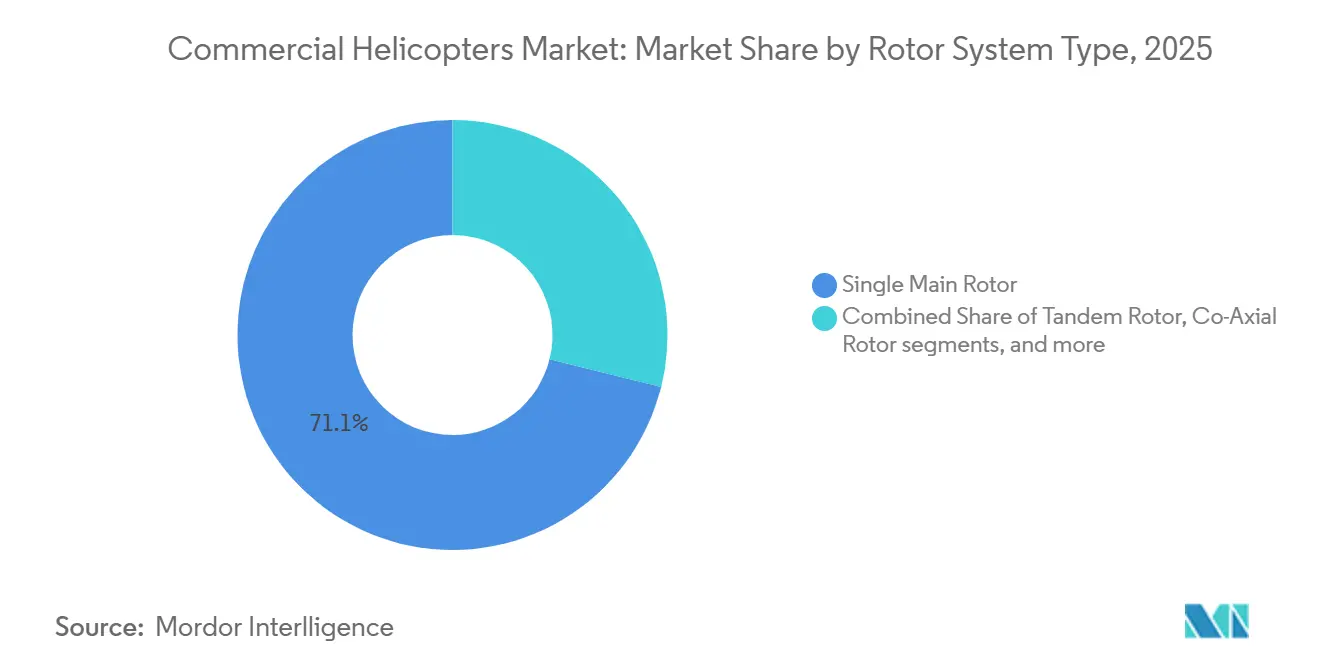

- By rotor system type, single main-rotor designs captured 71.12% of 2025 deliveries, and tilt-rotor configurations are on track for a 9.21% CAGR through 2031.

- By end-use, offshore oil and gas maintained a 35.11% share in 2025, while emergency medical services are forecast to expand at a 7.31% CAGR through 2031.

- By region, North America accounted for 39.78% of 2025 revenue, but Asia-Pacific is projected to record the fastest CAGR of 7.55% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Helicopters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid offshore wind-farm expansion widens mission scope | +0.8% | Europe (North Sea, Baltic), Asia-Pacific (Taiwan, Japan, South Korea), North America (US East Coast) | Medium term (2–4 years) |

| Outsourced HEMS shifts fleets toward purpose-built twins | +0.9% | North America, Europe (UK, Germany, France) | Short term (≤ 2 years) |

| Modernization wave tackles aging fleets | +0.7% | Global, with concentration in North America and Europe | Medium term (2–4 years) |

| VIP and charter flying gains traction in congested cities | +0.5% | Middle East (UAE, Saudi Arabia), Asia-Pacific (China, India), South America (Brazil) | Long term (≥ 4 years) |

| Climate-driven rise in wildfires supporting aerial firefighting contracts | +0.6% | North America (Western US, Canada), Europe (Mediterranean), Australia | Short term (≤ 2 years) |

| Commercialization of hybrid-electric, SAF-ready, and tilt-rotor technologies | +1.2% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Offshore Wind-Farm Expansion Widens Mission Scope

Eight US Atlantic wind projects approved in 2024–2025 will together require more than 7,000 flight hours of annual crew and technician lift once turbines reach full output, a shift that shields operators from oil-price swings.[1]Bureau of Ocean Energy Management, “Atlantic Offshore Wind Projects,” boem.gov European demand is already visible; Airtelis ordered eight Airbus H145 D3 aircraft in June 2024 for North Sea work, citing lower cabin vibration on 90-minute legs. Leonardo’s AW169 is likewise securing multiyear charters with Vestas via NHV Group, and Ørsted has extended HeliService’s Atlantic coverage through 2029. These contracts lock in five- to seven-year revenue streams and diversify mission portfolios.

Outsourced HEMS Shifts Fleets Toward Purpose-Built Twins

Hospital divestitures of helicopter assets are accelerating the renewal of helicopter fleets. Global Medical Response’s 28-unit Airbus H-140 purchase in January 2025, with options for 15 more, follows the same cost-of-capital logic that led Life Flight Houston to the H-160 platform in March 2025. IFR-certified twins reduce insurance premiums and simplify scheduling because they allow single-pilot operations under instrument conditions. Standardized avionics across an outsourced fleet also compresses training cycles, which is critical amid a pilot shortfall.

Modernization Wave Tackles Aging Fleets

Pre-2010 airframes are prone to fatigue and expensive ADS-B retrofits, making replacement a more economical option. Robinson delivered 312 units in 2024, with many R66 turbine aircraft replacing piston-powered R44s for utility and training missions. Lease-return data tell the same story: Milestone Aviation noted that 22% of its portfolio ended lease terms in 2024–2025 and rolled into newer twins rather than extending single-engine contracts. OEM production stability now relies as much on replacements as on new missions, supporting the commercial helicopters market through the decade.

VIP and Charter Flying Gains Traction in Congested Cities

Blade flew 47,000 paying passengers in 2024 on Manhattan airport routes, a 31% year-over-year increase, and has opened vertiport partnerships in Miami and Los Angeles for 2026 operations. Brazil’s ANAC recorded 2.1 million helicopter movements in São Paulo during 2024, highlighting latent demand in megacities where road commutes exceed 90 minutes. Light twins, such as the Airbus H145, combine cabin quietness with IFR capability, enabling operators to secure nighttime slots in noise-sensitive urban zones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operating-cost inflation squeezes margins | -0.6% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Pilot supply constraints limit utilization | -0.5% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Tightening global noise and emissions certification hurdles | -0.4% | Europe (EASA), North America (FAA), Asia-Pacific (CAAC) | Long term (≥ 4 years) |

| eVTOL and long-range drone substitution risk in light segments | -0.3% | North America, Europe, Asia-Pacific urban corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Operating-Cost Inflation Squeezes Margins

Jet-A averaged USD 3.20 per gallon in North America during 2024, 14% higher than 2023, and parts inflation lifted maintenance reserves by 16% over the same period. Hull-and-liability insurance for HEMS fleets increased 18% in 2024-2025 due to night-IFR claims, and smaller operators lack the scale to negotiate discounts. These pressures curb discretionary upgrades such as glass-cockpit retrofits or SAF adoption.

Pilot Supply Constraints Limit Utilization

The Bureau of Labor Statistics projects a 6% annual shortfall in US helicopter pilots through 2030, and HAI surveys suggest that 68% of operators now have vacancies.[2]Helicopter Association International, “2025 Operating Cost Survey,” rotor.org Captains with 2,000 or more flight hours receive a USD 25,000 signing bonus; however, the training pipelines produce only 3,200 new pilots annually, while demand stands at 4,500. Some North American HEMS fleets are seeing utilization rates dip below 70%, as aircraft remain grounded, awaiting crew availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Maximum Take-Off Weight: Heavy Platforms Gain Share on Offshore and Firefighting Demand

Light helicopters retained 54.21% of the commercial helicopters market share in 2025, primarily driven by deliveries of the Robinson R44 and R66 to flight schools and ranching operators.[3] Medium twins serve offshore oil, HEMS, and corporate missions, while heavy models above 9 tons are forecast to post a 6.92% CAGR to 2031 as offshore wind and firefighting contracts proliferate. The Airbus H225 Super Puma secured nine heavy-lift orders in 2024-2025 after a 2,500-hour TBO extension, and Sikorsky’s S-92 picked up a 12-unit Bristow Group order in March 2025.

Heavy helicopters hold approximately 18% of the commercial helicopters market size, a figure that is expected to rise as governments bundle multi-year aerial firefighting contracts. Erickson’s nine-aircraft backlog for the S-64 Skycrane stretches to 2027, indicating sustained demand.

By Number of Engines: Twin Redundancy Commands a Premium in HEMS and Offshore

Single-engine models accounted for 63.34% of deliveries in 2025, offering a price-point entry for training and utility roles. Yet twin-engine types are expanding at 6.27% as insurers mandate redundancy over water and at night. Airbus delivered 187 H135 and H145 units combined in 2024, many into HEMS service, while Leonardo shipped 52 AW139s and 28 AW169s across offshore wind and VIP fleets.

Twin-engine helicopters contributed 36% to the commercial helicopters market size in 2025 and are projected to surpass single-engine helicopters in revenue by 2030, as unit prices average 2.5 times higher.

By Rotor System Type: Tilt-Rotor Commercialization Reshapes Speed Expectations

Single-main-rotor airframes still dominate, with a 71.12% share, due to their mechanical simplicity and parts commonality. The arrival of the AW609 tilt-rotor, however, introduces a 275-knot cruise that halves crew-transfer time on 150-nautical-mile offshore legs. Tilt-rotor deliveries are expected to expand at 9.21% through 2031, the highest rate among rotor categories.

Tilt-rotor entrants are projected to capture USD y million of the commercial helicopters market size in 2031, though pilot-training and maintenance-complexity hurdles temper early adoption.

By End-Use: HEMS Overtakes Offshore as Fastest-Growing Mission

Offshore oil and gas maintained a 35.11% share in 2025, but growth in flight hours is flat as energy majors shift their focus toward renewables. Emergency-medical missions recorded a 7.31% CAGR forecast, benefiting from Global Medical Response’s 28-aircraft H140 order and similar procurements at STAT MedEvac and Stanford Health Care. Corporate-VIP traffic is also rising due to urban congestion. Blade’s sixth AW109 came online in April 2025, and Falcon Aviation added three AW139s in March 2025 to Abu Dhabi shuttle routes.

HEMS represents 18% of the commercial helicopters market size in 2025 and is positioned to surpass offshore oil by 2028, assuming current order books remain intact.

Geography Analysis

North America retained 39.78% of 2025 revenue, anchored by the world’s densest HEMS grid and stable Gulf of Mexico operations. CAL FIRE’s S-70i intake and the US Forest Service’s contract expansion underscore public-sector demand. FAA leadership on tilt-rotor and eVTOL certification supports early adoption of next-generation fleets.

Europe benefits from stringent noise standards that compel fleet renewal and from the rapid development of offshore wind. The region’s 76 GW offshore-wind target for 2030 under REPowerEU assures heavy-twin demand, while EASA’s Chapter 11 enforcement accelerates retirement of older Chapter 8 airframes.[4]European Commission, “REPowerEU Offshore Wind Targets,” ec.europa.eu

The Asia-Pacific region is the fastest-growing, with a 7.55% CAGR, driven by China’s low-altitude economy, India’s urban mobility schemes, and Japan's disaster response upgrades. AVIC’s AC352 deliveries and Pawan Hans’ 10-unit Bell 407GXi order illustrate indigenous and imported growth channels.

Competitive Landscape

Airbus Helicopters, Bell Textron, Leonardo S.p.A., Rostec, and Lockheed Martin Corporation together accounted for about 60% of global deliveries in 2024-2025, while Robinson Helicopter controlled roughly one-quarter of the light piston-and-turbine segment. Airbus delivered 330 civil units in 2024, supported by 31 service centers, and has enrolled 120 operators in its HCare parts-by-the-hour plan.[5]Airbus Helicopters, “2024 Orders and Deliveries,” airbus.com Bell shipped 140 units and is doubling down on hybrid-electric R&D. Leonardo’s AW609 tilt-rotor offers the only certified propeller in the commercial space, providing product differentiation as FAA approval nears.

Competition now hinges on innovation in propulsion and aftermarket capture. SAF compatibility, parts-hour programs, and predictive-maintenance analytics generate margins above 40%, versus less than 15% on new-aircraft sales. eVTOL disruptors Joby and Archer pose a medium-term threat to short-haul light singles, yet infrastructure build-outs give incumbent OEMs a window to decarbonize and retain customers.

Commercial Helicopters Industry Leaders

Bell Textron Inc.

Lockheed Martin Corporation

Leonardo S.p.A.

Airbus SE

Russian Helicopters (Rostec)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Airbus Helicopters Canada, a subsidiary of Airbus SE, inaugurated its new integrated distribution center in the Niagara region. The 21,000-square-foot facility expands the spare parts storage capacity and strengthens industrial operations.

- March 2025: Leonardo S.p.A. booked nearly 30 helicopters worth EUR 370 million (USD 423.39 million) for energy, public service, and VIP roles.

- February 2024: Lockheed Martin Corporation Sikorsky introduced the hybrid-electric HEX 2-Rotor Tiltwing demonstrator with a 575-mile range.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global commercial helicopters market as the annual value of brand-new, civil rotorcraft delivered for passenger transport, offshore logistics, emergency medical services, aerial work, tourism, law enforcement, and search and rescue missions. Values are captured at manufacturer transfer price in US dollars, net of military contracts yet before in-service support.

Scope Exclusion: Pre-owned sales, military rotorcraft, aftermarket MRO revenues, and eVTOL prototypes are excluded.

Segmentation Overview

- By Maximum Take-off Weight

- Light Helicopters

- Medium Helicopters

- Heavy Helicopters

- By Number of Engines

- Single-engine

- Twin-engine

- By Rotor System Type

- Single Main Rotor

- Tandem Rotor

- Co-Axial Rotor

- Tilt-Rotor

- By End-Use

- Offshore Oil and Gas

- Emergency Medical Services (HEMS)

- Corporate and VIP Charter

- Search and Rescue / Firefighting

- Aerial Work (Utility, Survey, Cargo)

- Tourism

- By Geography

- North America

- United States

- Canada

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed helicopter lessors, HEMS operators, offshore flight planners, and civil aviation regulators across North America, Europe, Asia-Pacific, and the Middle East. These dialogues clarified price realizations, utilization hours, and forward order intentions, which we used to validate desk findings and refine regional penetration assumptions.

Desk Research

We began by mapping publicly available fleet and production statistics from sources such as the FAA, EASA, ICAO, and the UN Comtrade database. We then supplemented these with delivery disclosures from OEM annual reports and the International Helicopter Safety Foundation. Macroeconomic context, oil and gas capital spend, EMS sortie volumes, and tourism arrival data came from the IEA, WHO, and UNWTO. Subscription files from Aviation Week and Airframer furnished model-level build rates, while Questel patent analytics helped track drivetrain and SAF-ready design pipelines. Additional insight flowed from civil aviation authority tenders, investor presentations, and reputable press releases. This list is not exhaustive; numerous other secondary sources informed data collection and cross-checks.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model underpins our numbers. Global rotorcraft production and trade data are first reconstructed to a delivery value pool, which is then corroborated with sampled ASP × volume roll-ups from OEM disclosures and operator channel checks. Key inputs include fleet age profiles, offshore rig count, EMS mission growth, tourism passenger flows, and SAF adoption timelines. Forecasts to 2030 rely on an ARIMA model blended with scenario analysis, and the coefficient set is stress tested with expert consensus to adjust for currency swings and regulatory shocks.

Data Validation & Update Cycle

Outputs pass multi-layer variance scans; anomaly flags trigger re-contact with domain experts, and every worksheet undergoes peer review before sign-off. Reports refresh annually, while interim updates follow material events such as certification of new platforms or major oil price swings.

Why Mordor's Commercial Helicopters Baseline Commands Reliability

Published estimates often diverge because firms choose different scopes, pricing anchors, and refresh cadences. We acknowledge these variations upfront, then demonstrate how disciplined variable selection and transparent assumptions keep Mordor's view dependable.

Key gap drivers stem from whether aftermarket MRO is counted, whether list prices or realized prices are used, and how aggressively future technology adoption is embedded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.80 bn (2025) | Mordor Intelligence | - |

| USD 39.51 bn (2025) | Global Consultancy A | Adds warranty MRO and parapublic fleet value; applies list prices without discounting |

| USD 7.12 bn (2025) | Industry Databook B | Uses manufacturer guidance for ASP; limited primary validation in Asia and Middle East |

In short, Mordor's model rests on clearly bounded scope, cross-verified inputs, and an annual refresh cycle, giving decision-makers a balanced baseline that traces every figure to reproducible steps.

Key Questions Answered in the Report

How large is the commercial helicopters market in 2026 and what growth is expected?

The commercial helicopters market size reached USD 7.13 billion in 2026 and is projected to reach USD 9.03 billion by 2031, reflecting a 4.85% CAGR.

Which weight class is growing the fastest?

Heavy platforms above 9 tons are forecasted to post the strongest 6.92% CAGR through 2031 as offshore wind and wildfire contracts expand.

Why are twin-engine helicopters gaining share?

Insurance requirements for IFR and over-water missions, coupled with outsourced HEMS contracts, push operators toward twin redundancy despite higher acquisition cost.

What region offers the highest growth opportunity?

Asia-Pacific is set to grow at 7.55% due to China’s low-altitude economy policy, India’s urban connectivity plans, and Japan’s disaster-response renewals.

How will sustainable aviation fuel affect fleet economics?

Trials on Bell 505 and Airbus H225 indicate up to 75% lifecycle CO₂ cuts with drop-in 100% SAF, helping operators meet ReFuelEU mandates without hardware changes.

Are eVTOL aircraft a near-term threat to light helicopters?

Certification milestones at Joby and Archer suggest commercial launches by 2026-2027, potentially displacing light single-engine helicopters on short urban routes where vertiport infrastructure is available.

Page last updated on: