Dental Panoramic Radiography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

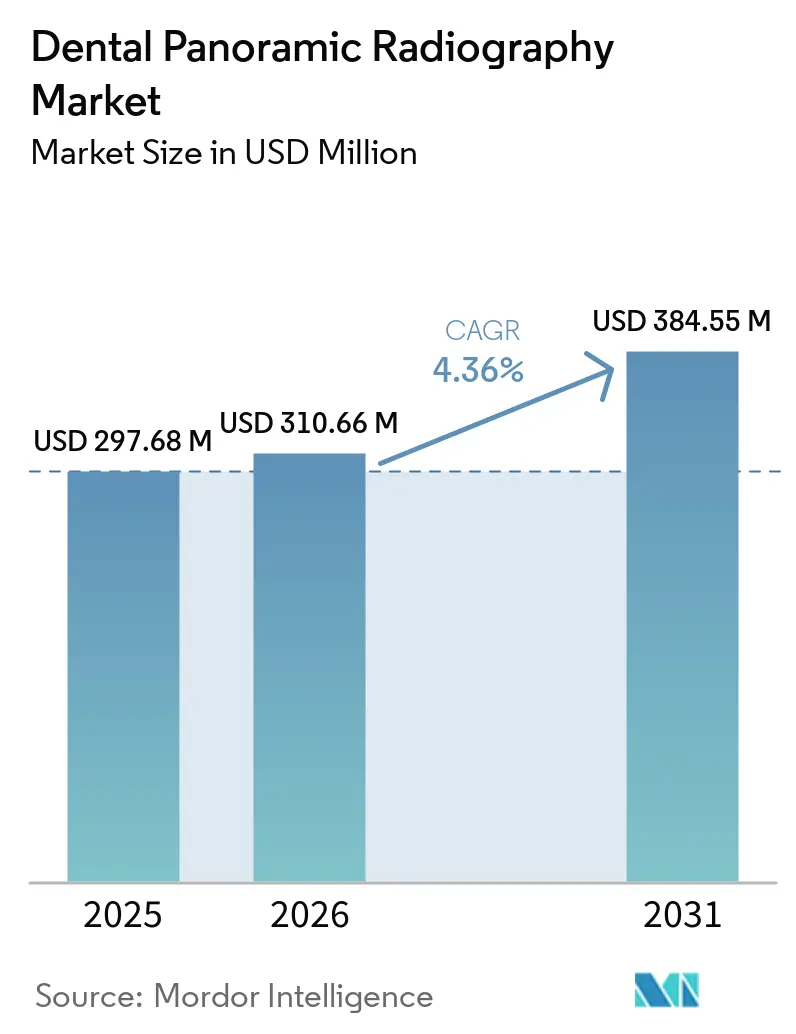

| Market Size (2026) | USD 310.66 Million |

| Market Size (2031) | USD 384.55 Million |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Panoramic Radiography Market Analysis by Mordor Intelligence

The Dental Panoramic Radiography Market size is projected to expand from USD 297.68 million in 2025 and USD 310.66 million in 2026 to USD 384.55 million by 2031, registering a CAGR of 4.36% between 2026 to 2031.

Oral diseases, affecting 3.5 billion people globally, highlight the ongoing importance of diagnostic imaging in routine dental care workflows. A 2025 study based on Global Burden of Disease 2021 data reported 1.07 billion cases of periodontal disease worldwide, driving consistent demand for full-arch imaging in primary dental settings.[1]World Health Organization, “Oral Health,” WHO Fact Sheet, who.int Source: Amaechi C. Chukwuemeka et al., “Global, Regional, and National Burden of Periodontal Diseases From 1990 to 2021 and Predictions to 2040,” BMC Oral Health, pmc.ncbi.nlm.nih.gov The dental panoramic radiography market is further supported by the shift toward digital workflows, as providers increasingly prefer software-linked systems that integrate imaging, diagnosis, and patient communication. Suppliers are focusing on AI-enabled reading tools, cloud platforms, and integrated viewers rather than solely upgrading hardware. However, the market faces challenges from CBCT substitution in complex cases and compliance costs, which favor larger manufacturers with stronger regulatory and service capabilities.

Key Report Takeaways

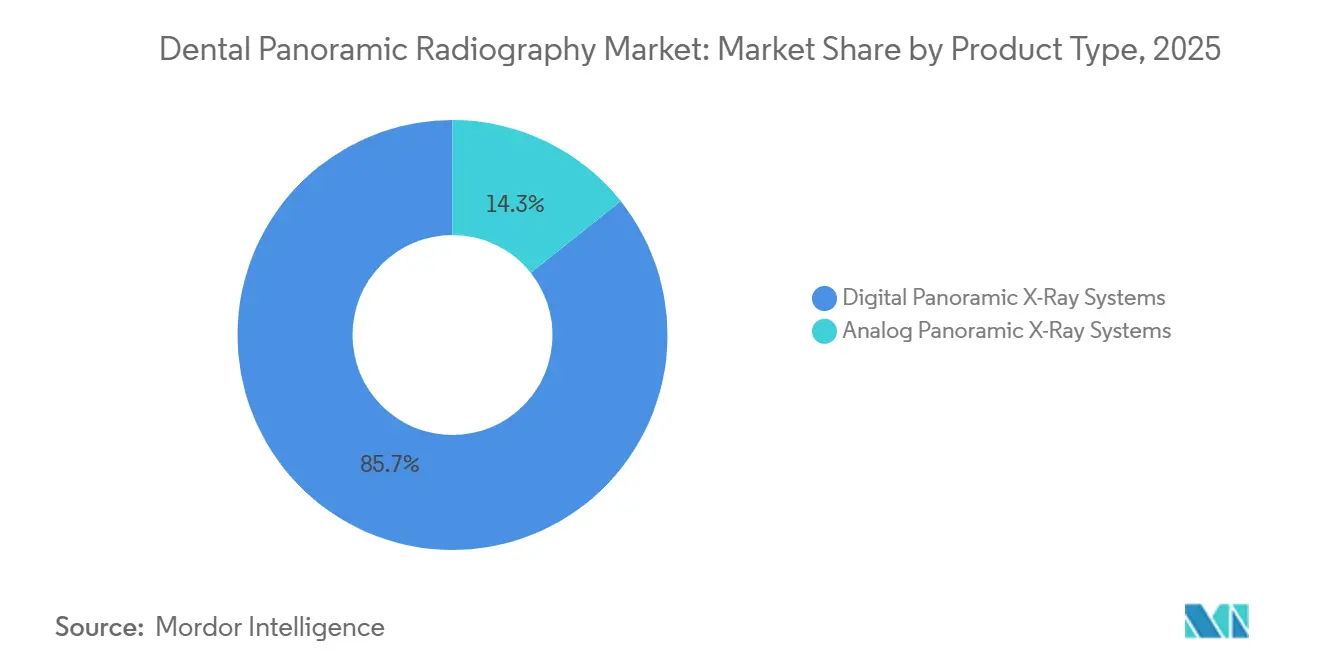

- By product type, digital panoramic X-ray systems held 85.68% of revenue in 2025, and this segment is projected to grow at a 4.66% CAGR through 2031.

- By technology, 2D panoramic X-ray systems held 68.55% of revenue in 2025, while 3D panoramic X-ray systems are projected to record the fastest CAGR at 5.89% through 2031.

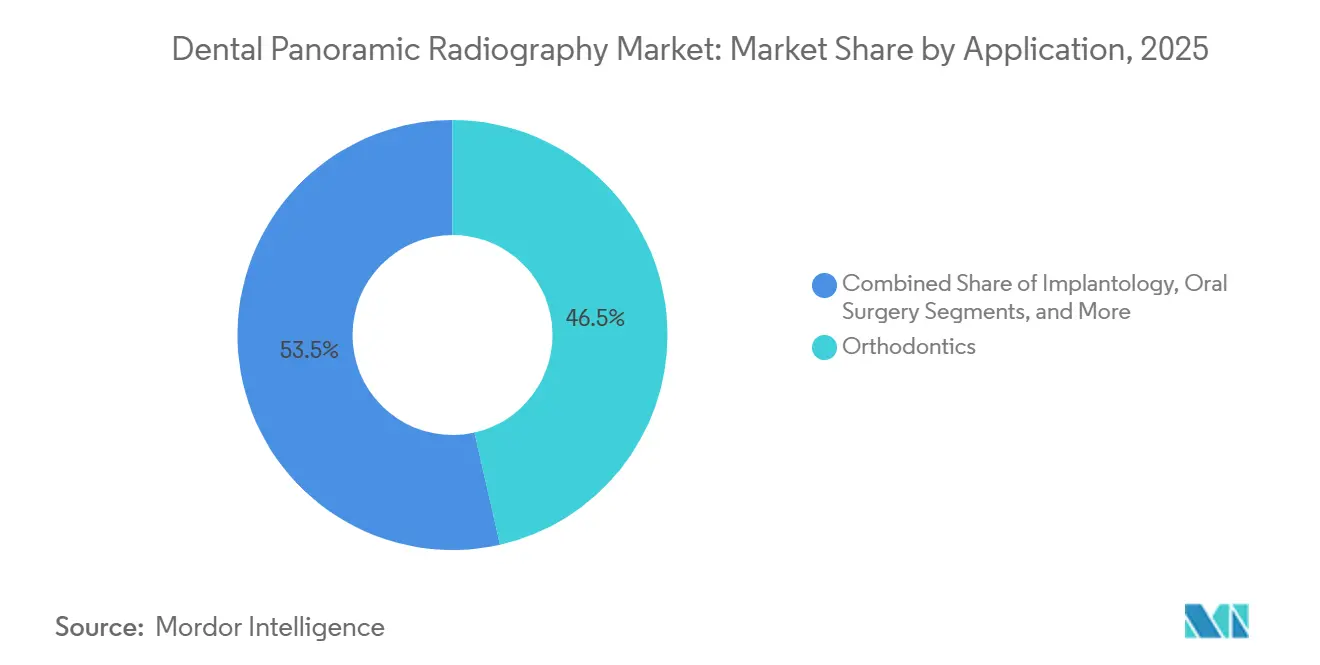

- By application, orthodontics held 46.45% of revenue in 2025, while implantology is projected to grow at the fastest CAGR of 6.54% through 2031.

- By end user, DSOs and group practices held 35.45% of revenue in 2025, while dental clinics are projected to expand at the fastest CAGR of 5.77% through 2031.

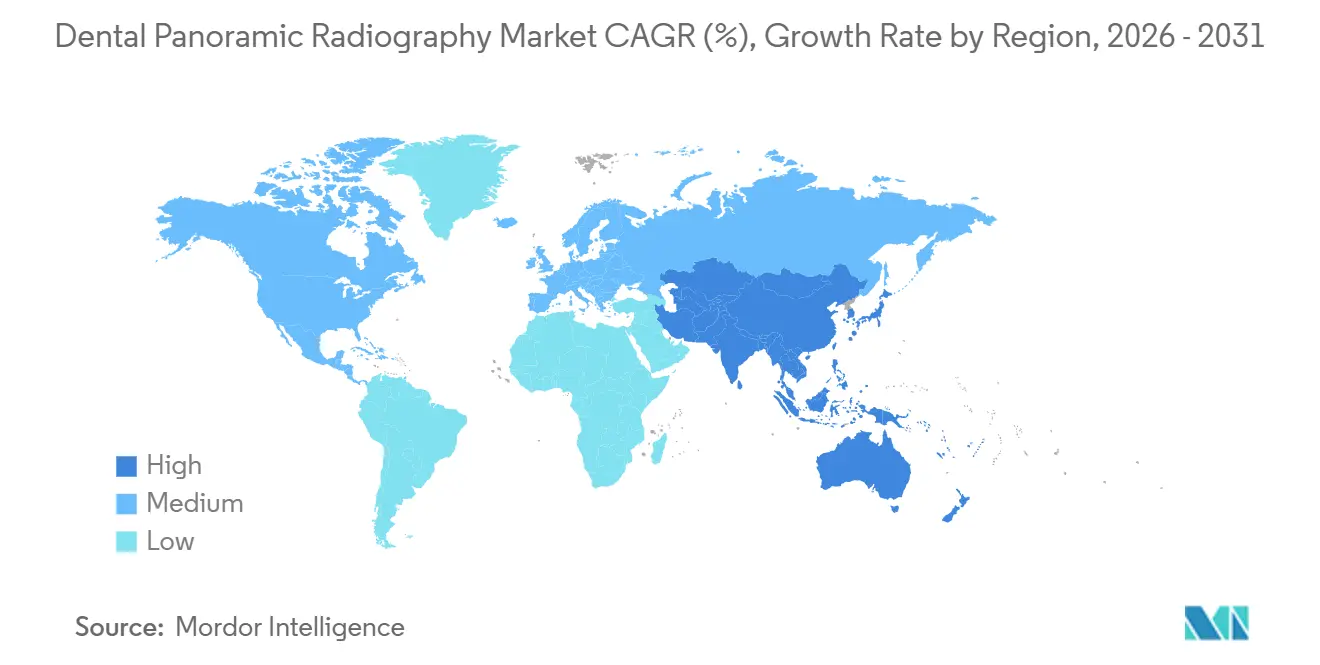

- By geography, North America held 38.95% of the dental panoramic radiography market share in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 5.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Panoramic Radiography Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising periodontal and caries case load | +1.2% | Global | Short term (≤ 2 years) |

| Digital workflow replacement in solo and group practices | +1.0% | North America, Europe, APAC core | Short term (≤ 2 years) to Medium term (2-4 years) |

| Ai-assisted image interpretation | +0.8% | North America, Europe, with spill-over to APAC | Medium term (2-4 years) |

| Chairside implant and orthodontic planning demand | +0.7% | North America, Europe, APAC | Medium term (2-4 years) |

| Preventive oral screening expansion | +0.5% | Global, early gains in emerging Asia and GCC | Long term (≥ 4 years) |

| Film-to-digital retrofit demand in emerging markets | +0.4% | Latin America, MEA, South and Southeast Asia | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Periodontal and Caries Case Load

Periodontal diseases and dental caries continue to drive demand in the dental panoramic radiography market. A 2025 study highlighted 1.07 billion global cases of periodontal disease, with a 76.32% rise in incidence from 1990 to 2024, reaching 89.6 million new cases annually. Another study reported 2.37 billion caries incidence cases in 2024, with further growth expected through 2035.[2]Dentsply Sirona, “Dentsply Sirona Launches Smart View – Detect, World’s First FDA-Cleared AI-Enabled Diagnostic Aid for Detecting Teeth With Periapical Radiolucencies in CBCTs,” Dentsply Sirona, dentsplysirona.com Many patients present with multiple untreated conditions, making panoramic imaging essential, especially in middle-income regions where it often serves as the foundation for structured dental reviews. This trend supports high utilization rates per patient, even in areas with limited routine recall visits.

Digital Workflow Replacement in Solo and Group Practices

The shift from analog and outdated digital systems to modern solutions is driving growth in the dental panoramic radiography market. In 2025, PDS Health and DEXIS implemented AI-driven 3D imaging across over 1,000 dental practices, showcasing the move toward cohesive diagnostic environments. Smaller practices face competitive pressure as patients increasingly compare clinics based on speed, image quality, and treatment clarity. A study revealed that 52% of surveyed dentists in Brazil still use analog systems, indicating significant upgrade potential in non-core markets. This replacement cycle benefits the market through renewals in established regions and digital adoption in emerging economies.

AI-Assisted Image Interpretation

AI-driven image interpretation is becoming a necessity in the dental panoramic radiography market. In 2025, Pearl's Second Opinion platform received FDA clearance for detecting caries, periapical radiolucencies, and impacted third molars. Similarly, Dentsply Sirona launched Smart View Detect in 2026, reporting a 46% increase in detection sensitivity compared to unaided reviews. A review identified 13 companies with 29 FDA-cleared AI solutions for dental imaging. As AI tools expand, older panoramic units with limited compatibility face obsolescence, creating a clear upgrade path for the market where software value aligns with image quality.

Chairside Implant And Orthodontic Planning Demand

Chairside planning links the dental panoramic radiography market to orthodontics and implant workflows. By 2025, orthodontics was the largest application segment, highlighting the importance of full-arch imaging in case initiation. Implantology, the fastest-growing segment through 2031, relies on panoramic imaging for baseline reviews, referrals, and patient communication. Orthodontic providers prefer systems combining panoramic and cephalometric capabilities, simplifying planning and reducing the need for separate devices. Panoramic imaging remains a practical first step before advanced imaging, ensuring its relevance in routine treatment planning.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| CBCT substitution in implantology and complex cases | -0.9% | North America, Europe, advanced APAC | Short term (≤ 2 years) to Medium term (2-4 years) |

| High capital cost and service dependence | -0.6% | Global, concentrated in MEA, South Asia, Latin America | Short term (≤ 2 years) |

| Radiation compliance and procurement friction | -0.3% | Europe, North America | Medium term (2-4 years) |

| Interoperability and IT integration gaps | -0.3% | Global, concentrated in solo and small-group practices | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CBCT Substitution in Implantology And Complex Cases

CBCT technology is significantly impacting the dental panoramic radiography market, particularly in implantology, the fastest-growing application segment. The American Academy of Oral and Maxillofacial Radiology recommends 3D imaging for pre-surgical implant evaluations in complex cases. In July 2025, PDS Health and DEXIS introduced CBCT and AI-supported imaging across over 1,000 practices, showcasing the integration of 3D capabilities into routine operations. Panoramic systems are expected to remain in use but may shift toward screening and communication roles, reducing the demand for premium upgrades and narrowing the application of high-end units in advanced diagnostics.

High Capital Cost and Service Dependence

High capital costs continue to challenge the dental panoramic radiography market, especially in cost-sensitive clinics and emerging economies. Advanced 3D-capable or AI-integrated systems are priced significantly higher than basic 2D units, and financing options are not universally available. A 2025 study in Brazil indicated that 52% of dentists still use analog systems, reflecting cost barriers, infrastructure limitations, and uneven digital adoption. Additionally, ongoing expenses such as software licenses, service contracts, and sensor replacements add to ownership costs. In regions with limited technical support, downtime risks further hinder market growth, emphasizing the need for affordable and easily maintainable equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Dominance Narrows Analog's Viable Geographies

In 2025, digital panoramic X-ray systems captured 85.68% of the revenue, highlighting the dental panoramic radiography market's shift toward digital imaging. Analog systems, with a 14.32% share, are increasingly limited to cost-sensitive clinics in sub-Saharan Africa, rural South Asia, and lower-income Latin American markets. The digital segment is projected to grow at a 4.66% CAGR through 2031, driven by replacement demand in mature markets and first-time digital adoption in clinics transitioning from film-based workflows. Digital systems have become the standard for new acquisitions, replacing their earlier premium positioning.

Digital platforms dominate due to their compatibility with software-based recordkeeping, image sharing, and treatment communication. Analog systems face challenges from declining detector costs, reduced film economics, and rising expectations for instant image access. AI-driven workflows and regulatory changes further accelerate the shift, creating opportunities for cost-competitive Asian suppliers and expanding the reach of digital platforms in the market.

By Technology: 3D Platforms Redefine the Diagnostic Baseline for Complex Cases

In 2025, 2D panoramic X-ray systems accounted for 68.55% of the technology segment revenue, driven by their suitability for general dentistry, orthodontic screenings, and full-arch reviews. However, 3D panoramic X-ray systems, growing at a 5.89% CAGR through 2031, are the fastest-growing segment, fueled by demand for precise implant planning, third molar evaluations, and temporomandibular joint assessments. Buyers increasingly prefer 3D systems as a middle ground between basic 2D imaging and standalone CBCT investments.

Hybrid panoramic and cephalometric systems remain vital in orthodontics, offering craniofacial imaging and panoramic captures in one setup. Vatech's 2025 launch of Clever One in the U.S., featuring AI-based lesion detection, reflects the market's shift toward integrated workflows. While 2D systems continue to improve in image quality, innovation is advancing faster in systems that integrate multiple imaging modes for streamlined planning.

By Application: Orthodontics Anchors Revenue as Implantology Drives Growth Asymmetry

In 2025, orthodontics contributed 46.45% of the application segment revenue, making it the largest application area. Panoramic imaging is essential in orthodontic planning, offering a comprehensive view of the dental arch for patient assessments, tooth positioning, and treatment planning. This segment provides a stable revenue base, independent of advanced surgical procedures, as panoramic imaging remains integral to orthodontic workflows.

Implantology, growing at a 6.54% CAGR through 2031, is the fastest-growing application segment. Panoramic imaging supports baseline evaluations, referrals, and patient consultations before advanced imaging. AI tools enhance the clinical utility of panoramic systems by assisting with caries and periodontal condition detection, improving equipment ROI and appealing to first-time buyers. Oral surgery, periodontics, and general dentistry continue to rely on panoramic imaging for routine documentation and assessments.

By End User: DSO Consolidation Sets the Procurement Agenda

In 2025, DSO and group practices accounted for 35.45% of the revenue, making them the largest end-user segment. These organizations influence vendor selection, software integration, and training by standardizing imaging protocols across multiple locations. Their bulk purchasing power can rapidly shift market dynamics compared to smaller independent clinics.

In October 2025, The Aspen Group partnered with Planmeca to deploy advanced digital imaging across over 1,100 Aspen Dental locations, supported by Henry Schein. Smaller dental clinics, growing at a 5.77% CAGR through 2031, are the fastest-growing segment as they align with network-led standards. Hospitals remain stable due to public budgets and licensing processes, while academic and research institutions, though smaller in revenue share, shape long-term brand preferences and training familiarity in the market.

Geography Analysis

In 2025, North America accounted for 38.95% of global revenue, establishing itself as the leading contributor to the dental panoramic radiography market. The region benefits from strong DSO-led procurement, widespread private dental insurance adoption, and rapid integration of connected imaging workflows. Large-scale deployments, such as the 2025 rollouts by PDS Health and DEXIS across over 1,000 practices, have further driven demand. Canada supports steady replacement demand, while Mexico contributes through urban clinic modernization and private dental care growth. Regulatory clarity from the FDA and Health Canada enhances buyer confidence in adopting new platforms and software tools.

Europe remains the second-largest regional market for dental panoramic radiography, with key activity in Germany, France, the UK, Italy, and Spain. Regulatory compliance has become a critical market factor, with Vatech achieving full EU MDR certification for its dental imaging portfolio in June 2026. Over 50% of EU medical device companies have reduced product offerings due to MDR compliance costs, giving larger suppliers a competitive edge. Germany maintains strong demand through its developed private dental sector, while the UK relies on private practice investments for premium imaging purchases.

Asia-Pacific is projected to grow at a 5.45% CAGR through 2031, making it the fastest-growing region in the dental panoramic radiography market. Growth drivers include private clinic expansion, rising demand for digital workflows, and significant opportunities to transition from analog systems. South Korea stands out with its domestic demand and manufacturing strength, supporting exports to Southeast Asia, the Middle East, and parts of Europe. South America, still in the early stages of digital adoption, shows potential, with 52% of Brazil's practices using analog systems in 2025.

Competitive Landscape

In the dental panoramic radiography market, a handful of global players dominate the premium and mid-range segments. Companies like Dentsply Sirona, Planmeca, Vatech, Carestream Dental, Envista Holdings, and J. Morita stand out, seamlessly integrating hardware, software, and robust distribution channels. Today's buyers prioritize not just detector quality and field of view, but also platform connectivity, AI enhancements, and the long-term suitability of workflows. This evolution favors larger players, as those with expansive software ecosystems can tie equipment sales to ongoing service and cloud revenues.

In May 2026, Dentsply Sirona exemplified this trend by unveiling its Smart View Detect via the DS Core cloud platform. Vatech strengthened its position by aligning its Clever One debut in the U.S. (August 2025) with comprehensive EU MDR certification for its 2026 lineup, enhancing both integration and regulatory outreach. Planmeca, through its October 2025 alliance with The Aspen Group, amplified its presence across a vast multi-site practice network, reaping the benefits of systemwide deployment momentum. These instances underscore that vendors are vying for dominance not just through the imaging unit, but also through the depth of their installed ecosystem. Thus, the market favors entities that can seamlessly merge image capture, data management, and clinical support into a singular, compelling offering.

While major players lead, smaller and regional entities still find opportunities in the dental panoramic radiography arena, particularly where cost-sensitive buyers or those seeking specialized service support are concerned. The transition from film to digital in emerging markets remains a viable avenue, as not all global frontrunners have crafted cost-effective platforms suited for service in areas beyond major urban hubs. Furthermore, AI-driven software providers are reshaping the competitive landscape; their open-platform integrations enhance the value of compatible systems, diminishing the allure of hardware-only distinctions.

Dental Panoramic Radiography Industry Leaders

Dentsply Sirona Inc.

Planmeca Oy

Carestream Dental LLC

Vatech Co., Ltd.

J. MORITA CORP.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Vatech completed EU Medical Device Regulation (MDR) certification for its entire dental imaging portfolio, including all existing and newly launched 2026 models, enabling immediate European distribution and gaining a competitive edge as rivals faced certification delays.

- May 2026: Dentsply Sirona launched Smart View - Detect, an FDA-cleared and CE-approved AI diagnostic tool for detecting periapical radiolucencies in CBCTs, showing a 46% increase in detection sensitivity and available via DS Core cloud subscription.

- March 2026: Cefla Medical Equipment introduced the MyRay Hyperion X9 Pro FullView panoramic X-ray imager, featuring high-resolution sensors and radiation-free facial positioning technology, supporting comprehensive diagnostic requirements.

- December 2025: Pearl received FDA clearance for its Second Opinion AI platform, which identifies caries, periapical radiolucencies, and impacted third molars, making it the most comprehensive FDA-cleared radiologic AI in dentistry with global regulatory approval.

Global Dental Panoramic Radiography Market Report Scope

As per the scope of the report, panoramic radiography, often called an OPG (Orthopantomogram), is an extraoral technique that produces a single continuous 2D image of the entire maxillofacial region, including the upper and lower jaws, teeth, and temporomandibular joints (TMJs).

The dental panoramic radiography market is segmented by product type, technology, application, end-user, and geography. By product type, the market includes digital panoramic X-ray systems and analog panoramic X-ray systems. By technology, the market is segmented into 2D panoramic X-ray systems, 3D panoramic X-ray systems, and hybrid panoramic and cephalometric systems. By application, the market is categorized into orthodontics, implantology, oral surgery, periodontics, general dentistry, and other dental applications. By end-user, the market is segmented into DSO and group practices, hospitals, dental clinics, academic and research institutes, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Digital Panoramic X-Ray Systems |

| Analog Panoramic X-Ray Systems |

| 2D Panoramic X-Ray Systems |

| 3D Panoramic X-Ray Systems |

| Hybrid Panoramic and Cephalometric Systems |

| Orthodontics |

| Implantology |

| Oral Surgery |

| Periodontics |

| General Dentistry |

| Other Dental Applications |

| DSO and Group Practices |

| Hospitals |

| Dental Clinics |

| Academic and Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Digital Panoramic X-Ray Systems | |

| Analog Panoramic X-Ray Systems | ||

| By Technology | 2D Panoramic X-Ray Systems | |

| 3D Panoramic X-Ray Systems | ||

| Hybrid Panoramic and Cephalometric Systems | ||

| By Application | Orthodontics | |

| Implantology | ||

| Oral Surgery | ||

| Periodontics | ||

| General Dentistry | ||

| Other Dental Applications | ||

| By End User | DSO and Group Practices | |

| Hospitals | ||

| Dental Clinics | ||

| Academic and Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the dental panoramic radiography space by 2031?

The dental panoramic radiography market is forecast to reach USD 384.55 million by 2031, up from USD 310.66 million in 2026, at a CAGR of 4.36%.

Which product type leads dental panoramic radiography revenue?

Digital panoramic X-ray systems led with 85.68% of revenue in 2025, reflecting the broad shift away from analog imaging.

Which application area is growing the fastest in dental panoramic radiography?

Implantology is projected to record the fastest CAGR at 6.54% through 2031, although orthodontics remained the largest application segment in 2025 at 46.45%.

Why does North America lead this space?

North America held 38.95% of revenue in 2025 because of strong DSO procurement, broad private dental coverage, and faster adoption of connected imaging workflows.

What is the main risk to panoramic imaging demand?

The biggest pressure comes from CBCT substitution in implantology and other complex cases, where 3D imaging can offer more detailed planning support.

What is changing competition among imaging vendors?

Competition is moving toward software depth, AI support, cloud connectivity, and enterprise deployments rather than only hardware specifications.

Page last updated on: