Dental Microscope Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

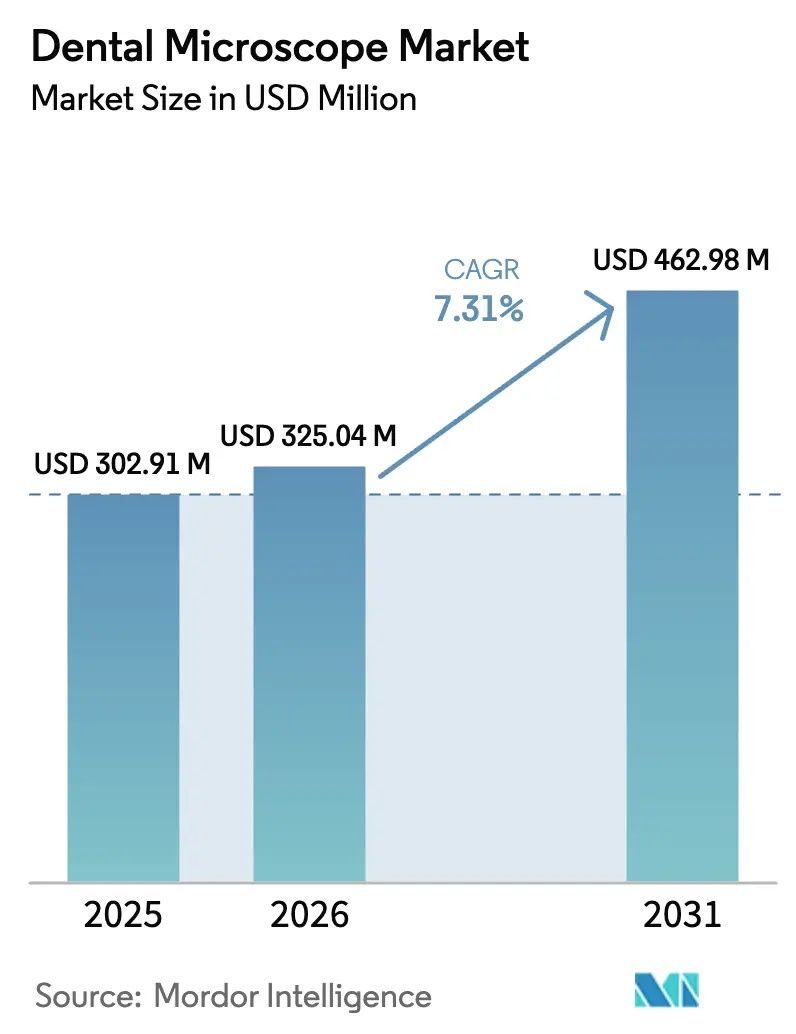

| Market Size (2026) | USD 325.04 Million |

| Market Size (2031) | USD 462.98 Million |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Microscope Market Analysis by Mordor Intelligence

The dental microscope market size was valued at USD 302.91 million in 2025 and estimated to grow from USD 325.04 million in 2026 to reach USD 462.98 million by 2031, at a CAGR of 7.31% during the forecast period (2026-2031). Strong demand for precision optics, the shift toward 4K/8K digital workflows, and rising adoption across endodontics, implantology, and cosmetic procedures underpin growth in the dental microscope market. Energy-efficient LED illumination, ergonomic form factors, and minimally invasive treatment protocols continue to accelerate equipment replacement cycles. Manufacturers position advanced optical components as foundational infrastructure for data-driven, patient-centric care, and portable designs gain traction as clinics seek flexible solutions that maximize operatory utilization. Simultaneously, developed markets confront saturation while emerging economies fuel incremental unit volumes through public and private investment in oral healthcare. Competitive dynamics hinge on optical performance, digital integration, and wrap-around training programs that help dentists navigate steep learning curves—factors that collectively shape future prospects for the dental microscope market.

Key Report Takeaways

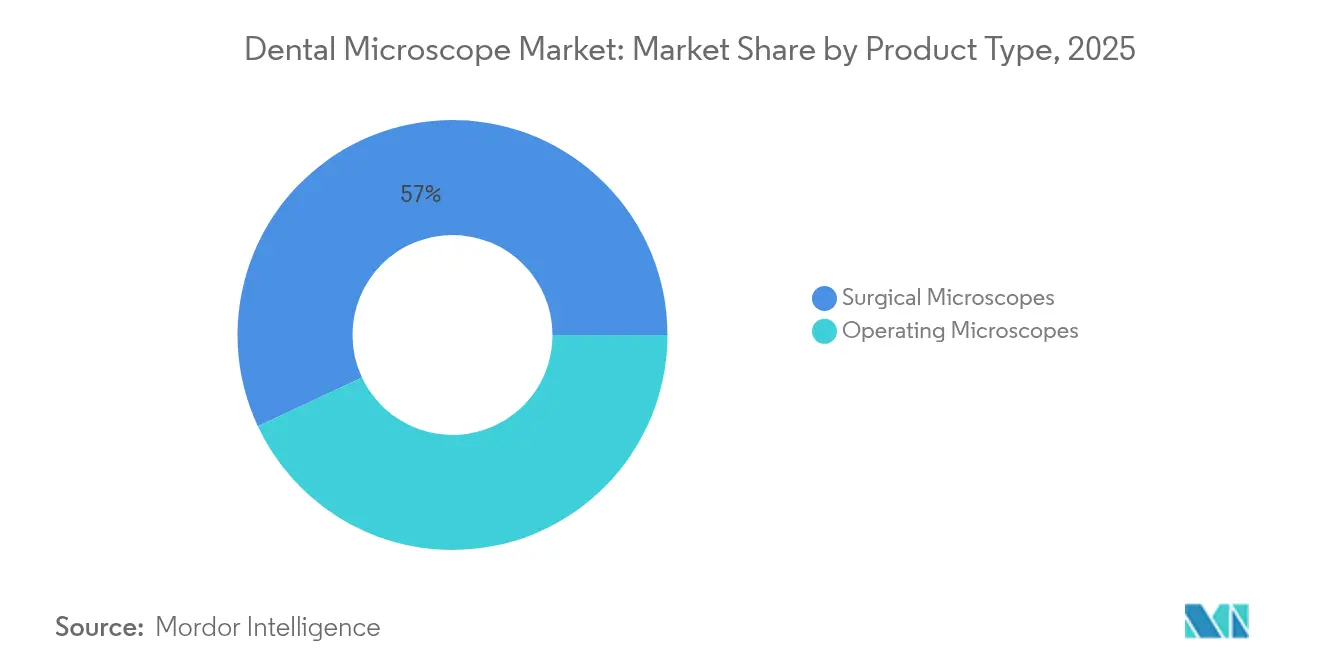

- By product type, surgical microscopes led with 56.98% of dental microscope market share in 2025, while operating microscopes post the fastest 8.12% CAGR through 2031.

- By modality, portable systems held 63.05% share of the dental microscope market in 2025; fixed installations grow at 6.18% CAGR.

- By illumination type, LED technology commanded 61.22% of the dental microscope market size in 2025 and is advancing at a 8.78% CAGR.

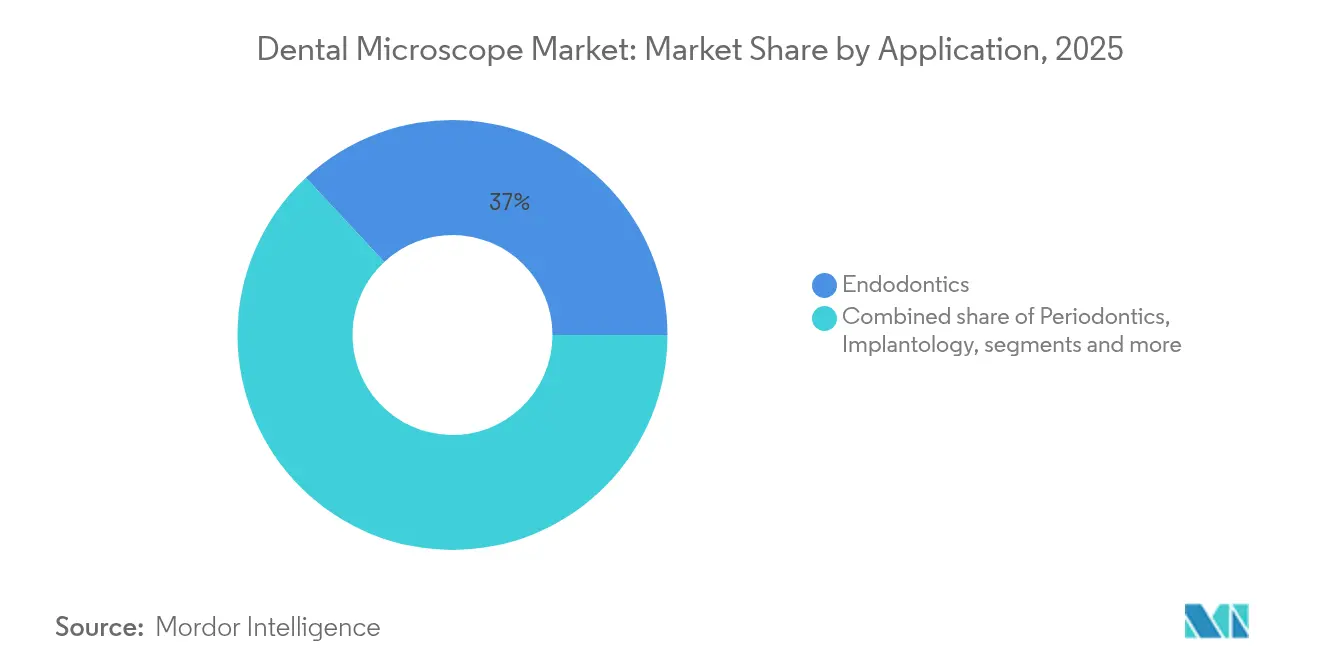

- By application, endodontics accounted for 36.95% of the dental microscope market size in 2025, whereas implantology registers an 8.34% CAGR to 2031.

- By end user, dental clinics captured 42.11% revenue share in 2025 and expand at an 8.19% CAGR through 2031.

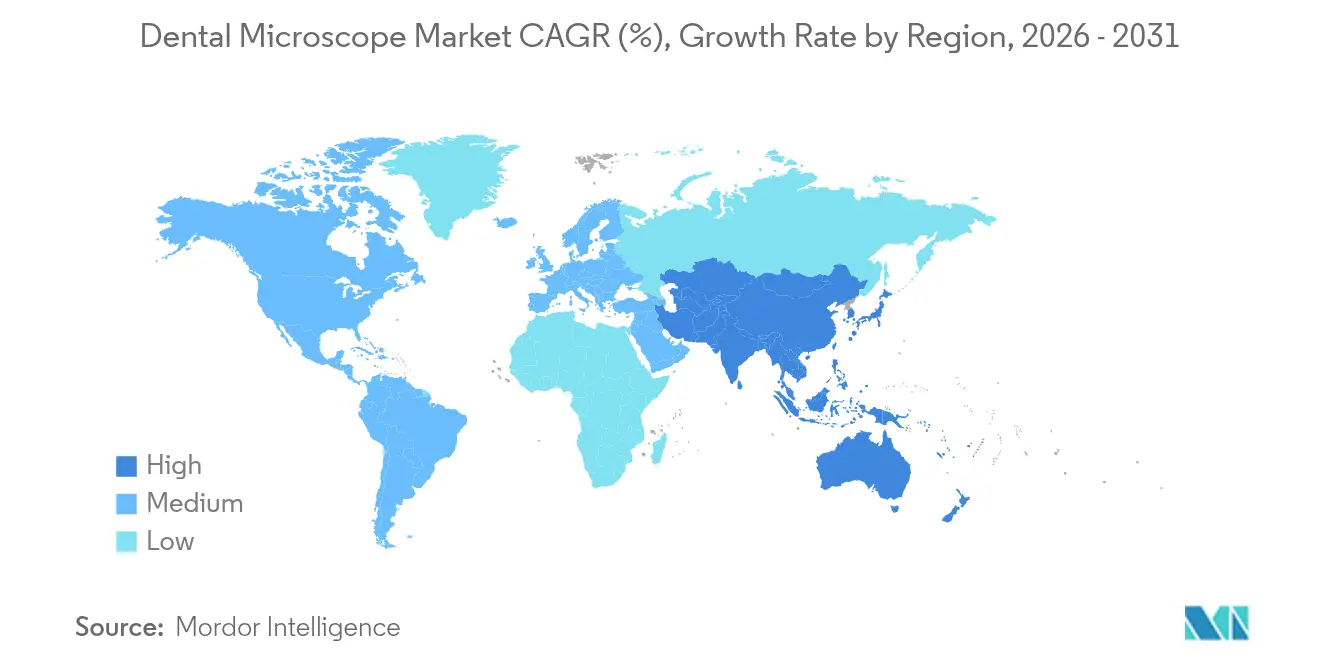

- By geography, North America represented 41.45% of the dental microscope market in 2025; Asia-Pacific is the fastest growing at 8.89% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Microscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of dental diseases | +1.8% | Global, with acute impact in low-income regions | Long term (≥ 4 years) |

| Rising demand for cosmetic & aesthetic dentistry | +1.5% | North America & EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Advancements in optical magnification & ergonomics | +1.2% | Global, led by Germany and Japan innovation hubs | Medium term (2-4 years) |

| Rising adoption of minimally-invasive endodontic procedures | +1.0% | North America & EU, selective adoption in APAC | Medium term (2-4 years) |

| Integration of 4K/8K digital workflow & chair-side education | +0.9% | High-income markets, selective adoption in emerging economies | Short term (≤ 2 years) |

| Reimbursement pilots for microscope-assisted care in EU | +0.6% | European Union, with spillover to similar healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Dental Diseases

Untreated caries and severe periodontal conditions afflict 3.5 billion people, imposing USD 387 billion in direct costs and USD 323 billion in productivity losses.[1]World Health Organization, “Global Oral Health Status Report 2024,” who.int Chronic workforce shortages—68% of member states report fewer than 5 dentists per 10,000 population—magnify reliance on technology that elevates diagnostic yield and procedure efficiency. In Japan, 126 dental clinics filed for bankruptcy across the first ten months of 2024 as practitioners aged 69 years on average struggled with digital investment needs. Microscopes mitigate this capacity crunch by enabling earlier lesion detection, precision surgery, and chair-side education that shortens appointment queues. Consequently, the dental microscope market remains pivotal for healthcare systems targeting outcome-based performance metrics and resource optimization.

Rising Demand for Cosmetic & Aesthetic Dentistry

A 7.1% annual upsurge in cosmetic dentistry stems from social media influence and post-pandemic self-care priorities. Patients now expect minimally invasive restorations, intricate implant placements, and flawless shade matching, forcing clinics to adopt high-magnification workflows that guarantee predictable aesthetic results. Microscopes bolster practice profitability because premium cosmetic procedures command higher fees, and 4K imagery boosts patient acceptance of treatment proposals. As a result, dental clinics represented 42.58% of microscope sales in 2024, underscoring how the dental microscope market penetrates general practice settings.

Advancements in Optical Magnification & Ergonomics

Component suppliers such as SCHOTT introduced Solidur LEDs that withstand sterilization and occupy minimal footprint, solving durability challenges in moist clinical environments. Ergonomic refinements—ultra-low binoculars and balanced suspension arms—alleviate neck strain for long interventions, a feature cited among the top purchase criteria by dentists surveyed in 2025. Optical comparisons reveal Carl Zeiss Extaro 300 achieving 64 lp/mm resolution versus competitor ranges near 36 lp/mm, delivering tangible clinical advantages in micro-endodontics. Such performance gains entice multidisciplinary adoption, enlarging the addressable base for the dental microscope market.

Integration of 4K/8K Digital Workflow & Chair-side Education

Modern platforms integrate UHD cameras, HDMI streaming, and cloud archiving, transforming microscopes into educational hubs that document evidence-based care. Remote consultation became standard during the COVID-19 era; clinics continue leveraging these workflows for specialist referrals and tele-mentoring. AI developers eye a USD 1.3 billion dental AI industry by 2028, with algorithms destined to embed within microscope software for real-time defect recognition. Early adopters report higher case acceptance rates once patients visualize pathology on 4K monitors, reinforcing the dental microscope market’s strategic relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced dental microscopes | -1.3% | Global, acute impact in emerging markets | Long term (≥ 4 years) |

| Limited training & learning curve for general dentists | -0.8% | Global, particularly affecting smaller practices | Medium term (2-4 years) |

| Precision-optics glass supply chain bottlenecks | -0.5% | Global, concentrated in Germany and Japan supply chains | Short term (≤ 2 years) |

| Post-COVID infection-control regulation complexity | -0.4% | Global, with varying regulatory intensity by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Dental Microscopes

Premium systems cost upwards of USD 50,000, posing hurdles for budget-constrained clinics in India, Brazil, and parts of Southeast Asia. Japanese practitioners cite equipment expense among leading factors behind 2024 clinic closures.[2]Asahi Shimbun, “Record Dental Clinic Bankruptcies in Aging Japan,” asahi.com Reimbursement gaps worsen pay-back timelines, segmenting the dental microscope market between technology-forward practices and price-sensitive operators.

Limited Training & Learning Curve for General Dentists

Microscope-guided workflows demand dexterity, altered hand-eye coordination, and auxiliary staff familiarity. The Indian Board of Micro Restorative and Endodontics introduced fellowship pathways to bridge these skill deficits, yet clinicians face multi-month adaptation periods that disrupt appointment volumes. Without structured mentorship, adoption stalls, tempering dental microscope market penetration rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surgical Microscopes Maintain Leadership

Surgical microscopes captured 56.98% of dental microscope market share in 2025, underscoring their cross-disciplinary utility. Case reports on piezo-assisted bone window techniques documented favorable hard-tissue preservation over 36 months, proof that high-resolution optics translate into clinical success. Demand escalates as complex retreatment, apicoectomy, and microsurgery protocols migrate from hospitals to office-based suites. Operating microscopes, tailored for focused indications, post an 8.12% CAGR as cost-effective entry points for niche practices. Manufacturers bundle modular attachments, enabling clinics to scale features in line with procedural mix, a model that fosters stickiness within the dental microscope market.

Broader product differentiation now aligns with workflow customization rather than mere magnification factors. Surgical systems integrate digital documentation, multi-spectral filters, and voice-activated controls that expedite transitions between endodontics and periodontics. Conversely, streamlined operating units appeal to implant-centric boutiques prioritizing compact form factors. This bifurcated roadmap illustrates how the dental microscope market responds to divergent clinical priorities without cannibalizing core revenue streams.

By Modality: Portable Units Dominate through Mobility

Portable microscopes accounted for 63.05% of the dental microscope market in 2025, thriving in group practices whose business models revolve around multi-chair utilization. Their 7.95% CAGR reflects seamless relocation across operatories, yielding higher asset productivity than fixed ceiling configurations. Folding bases, quick-lock wheels, and counter-balanced arms preserve optical stability while accommodating space-constrained urban clinics.

Fixed microscopes persist where ultimate vibration dampening and integrated cabinetry are mandatory, notably tertiary hospitals and postgraduate training centers. These installations often anchor teaching theatres with lecture capture systems that broadcast UHD feeds to remote learners. The coexistence of mobile and immobile platforms signals how the dental microscope market calibrates to architectural limitations and capital budgeting choices.

By Illumination Type: LED Takes Center Stage

LED setups controlled 61.22% of the dental microscope market size in 2025; their 8.78% CAGR dwarfs halogen alternatives because clinicians value cooler operation and superior CRI values crucial for shade-matching veneers. LEDs last up to 50,000 hours, slashing bulb replacement downtime and hazardous waste. Retrofitting kits allow legacy systems to upgrade, extending overall fleet life.

Halogen remains in budget units targeting entry-level buyers, while xenon caters to color-specific periodontal fluorescence studies. As clinics prioritize sustainable operations, LED’s energy savings dovetail with corporate ESG metrics, consolidating its dominance across the dental microscope market.

By Application: Endodontics Retains Primacy, Implantology Surges

Endodontics held 36.95% of the dental microscope market size in 2025, driven by American Association of Endodontists guidelines that advocate magnification for root canal diagnostics. Meta-analyses link higher magnification to improved instrument retrieval and canal negotiation success rates. Implantology, however, exhibits the highest 8.34% CAGR as aging populations demand functional replacements and peri-implant tissue management benefits from up to 25-fold magnification.

Restorative, periodontal, and pediatric indications follow, evidencing democratization of microscope-guided dentistry. This broadened scope pushes manufacturers to design accessories—such as variable-angle mirrors and micro-suction tips—that optimize visuals across diverse anatomies, cementing future expansion of the dental microscope market.

By End User: Clinics Spearhead Adoption

Dental clinics posted 42.11% revenue share in 2025 and expand at 8.19% CAGR as solo and group practices realize competitive leverage through differentiated technology offerings. High-definition chair-side displays bolster treatment plan acceptance, offsetting capital cost concerns.

Hospitals maintain secondary importance by virtue of oral and maxillofacial units that manage trauma and oncologic resection margins under microscopic guidance. Academic institutes play a catalytic role by embedding microscopes in curricula, graduating cohorts predisposed to maintain usage throughout professional lifecycles. This continuum reinforces sustainable demand across the dental microscope market.

Geography Analysis

North America commanded 41.45% of the dental microscope market in 2025, buoyed by insurance structures that partially reimburse microscope-assisted treatments and stringent continuing education obligations. Clinics leverage tax incentives for capital investments to refresh optical fleets every 7-10 years, yet overall unit growth tapers because penetration rates exceed 75% in major metropolitan areas.

Europe mirrors mature uptake in Germany, the United Kingdom, and Scandinavia, but Eastern European nations still present whitespace opportunities. EU reimbursement pilots that add fee modifiers for microscope use deliver a 0.6% positive CAGR impact, incentivizing upgrades in periodontal and endodontic workflows.

Asia-Pacific, led by China’s projected USD 210 billion medical device market, is the fastest-expanding region at 8.89% CAGR. Urban dental chains roll out portable units across high-footfall malls, and government-backed insurance expansion widens patient access. Japan’s aging practitioner base temporarily dampens installations, yet technology-savvy successors invest in fully digitalized operatories to tackle labor shortages. Latin America and the Middle East & Africa collectively comprise less than 10% of the dental microscope market but show double-digit unit gains as private equity funds inject capital into regional dental service organizations. Import tariff reforms in Brazil and Saudi Arabia reduce acquisition costs by up to 15%, supporting future penetration.

Competitive Landscape

The dental microscope market is moderately concentrated. Carl Zeiss Meditec recorded €512.8 million microsurgery revenue in fiscal 2023 yet saw early-2024 sales dip 1.7% after the KINEVO 900 S release disrupted existing upgrade cycles. Leica Microsystems focuses on surgeon-dentist ergonomic alignment, while Global Surgical emphasizes American-made build quality and turnkey training programs.

Competitive moats pivot on optical clarity, digital workflow integration, and after-sales education. Vendors bundle remote calibration, AI-ready firmware, and financing plans tailored to small practices. M&A chatter centers on component makers producing lenses and Solidur LEDs, as upstream consolidation promises to secure high-quality glass supply and cost synergies.

Regional entrants in China leverage government subsidies to establish vertically integrated production hubs, evident in ZEISS’s new Suzhou site supporting localization of microscope platforms for APAC customers. While patent portfolios deter outright commoditization, niche innovators can still penetrate segments by offering ultra-compact, ultraportable units priced 20% below incumbent flagships, ensuring healthy competitive tension across the dental microscope market.

Dental Microscope Industry Leaders

ARI Medical Technology Co., Ltd.

Carl Zeiss AG

Danaher Corporation (Leica Microsystems)

Karl Kaps GmbH & Co. KG

Zumax Medical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Global Surgical Corporation opened a new headquarters to expand production and on-site training capacity.

- January 2025: Global Surgical Corporation issued guidance stressing microscopes as practice-growth catalysts, citing 30 years of US manufacturing.

- July 2024: ZEISS inaugurated an R&D and manufacturing facility in Suzhou Industrial Park, China, to reinforce its APAC localization strategy.

Global Dental Microscope Market Report Scope

As per the scope of the report, dental microscopes are high-precision optical devices designed to enhance efficiency and accuracy in dental procedures by providing magnification and illumination of the treatment area. These instruments enable dental professionals to identify fine details of teeth, gums, and surrounding structures, ensuring precise diagnoses and treatments. Dental microscopes drive better patient outcomes while supporting ergonomic working conditions for clinicians. They are commonly utilized in procedures requiring high precision, such as endodontics, restorative dentistry, and periodontal treatments. The dental microscope market is segmented by product, type, application, end-user, and geography. By product, the market is segmented into surgical microscopes and operating microscopes. By type, the market is segmented into portable microscopes and fixed microscopes. By application, the market is segmented into endodontics, periodontics, restorative dentistry, and others. By end-user, the market is segmented into hospitals, dental clinics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Surgical Microscopes |

| Operating Microscopes |

| Portable |

| Fixed |

| LED |

| Halogen |

| Xenon |

| Others |

| Endodontics |

| Periodontics |

| Restorative Dentistry |

| Implantology |

| Others |

| Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Surgical Microscopes | |

| Operating Microscopes | ||

| By Modality | Portable | |

| Fixed | ||

| By Illumination Type | LED | |

| Halogen | ||

| Xenon | ||

| Others | ||

| By Application | Endodontics | |

| Periodontics | ||

| Restorative Dentistry | ||

| Implantology | ||

| Others | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the dental microscope market?

The dental microscope market stands at USD 325.04 million in 2026 and is projected to reach USD 462.98 million by 2031, supported by a 7.31% CAGR.

Which product category leads the dental microscope market?

Surgical microscopes maintain leadership with 56.98% dental microscope market share, driven by cross-specialty applicability and high-resolution optics.

Why are portable microscopes gaining popularity?

Portable units hold 63.05% share because their mobility enhances operatory utilization and supports group practice workflows without sacrificing optical quality.

Which region is growing fastest in the dental microscope market?

Asia-Pacific registers the quickest 8.89% CAGR, propelled by China’s expanding medical device sector and rising demand for technologically advanced oral care.

What restrains broader adoption of dental microscopes?

High capital expenditure, protracted training curves, and supply-chain bottlenecks in precision optics collectively temper uptake, especially in emerging markets.

Page last updated on: