Dental Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 681.46 Billion |

| Market Size (2031) | USD 852.84 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

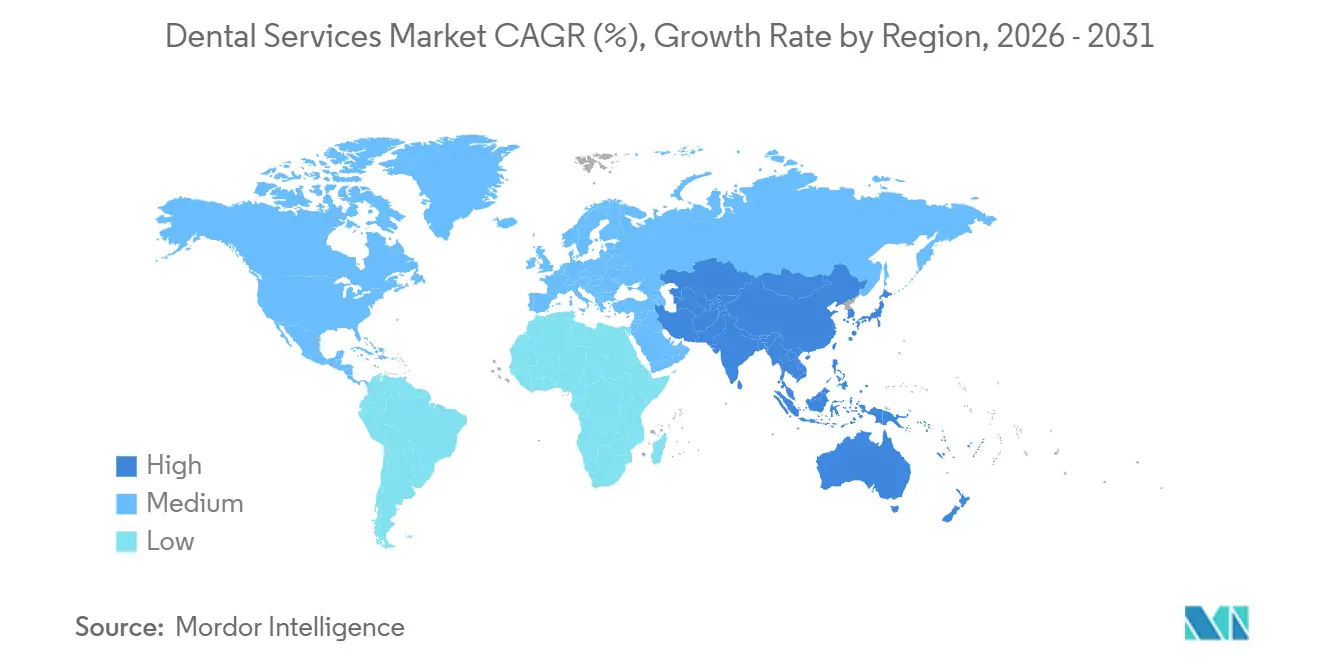

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

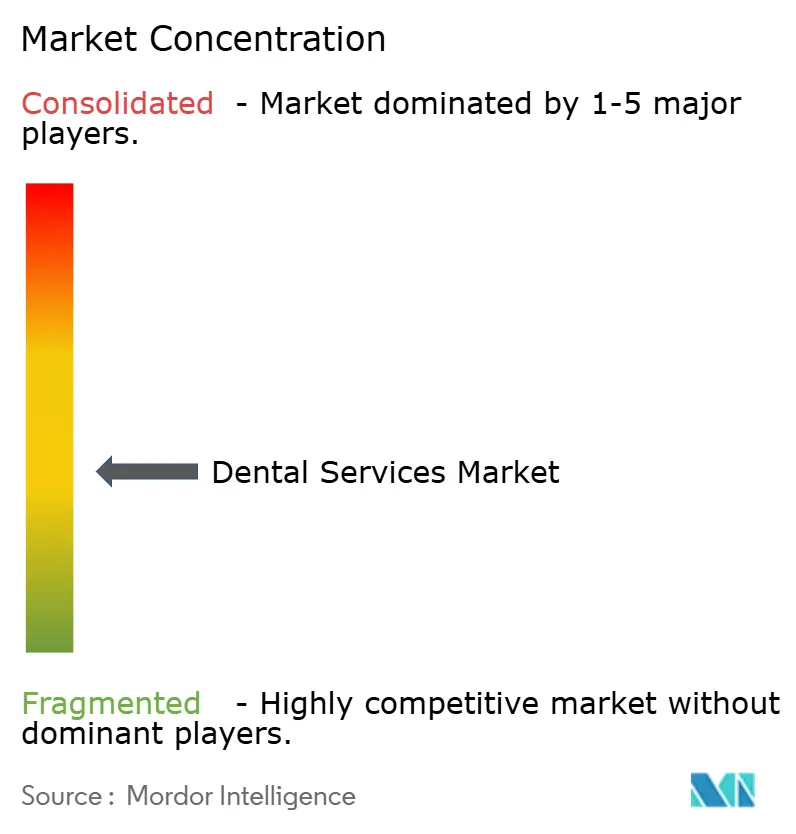

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Services Market Analysis by Mordor Intelligence

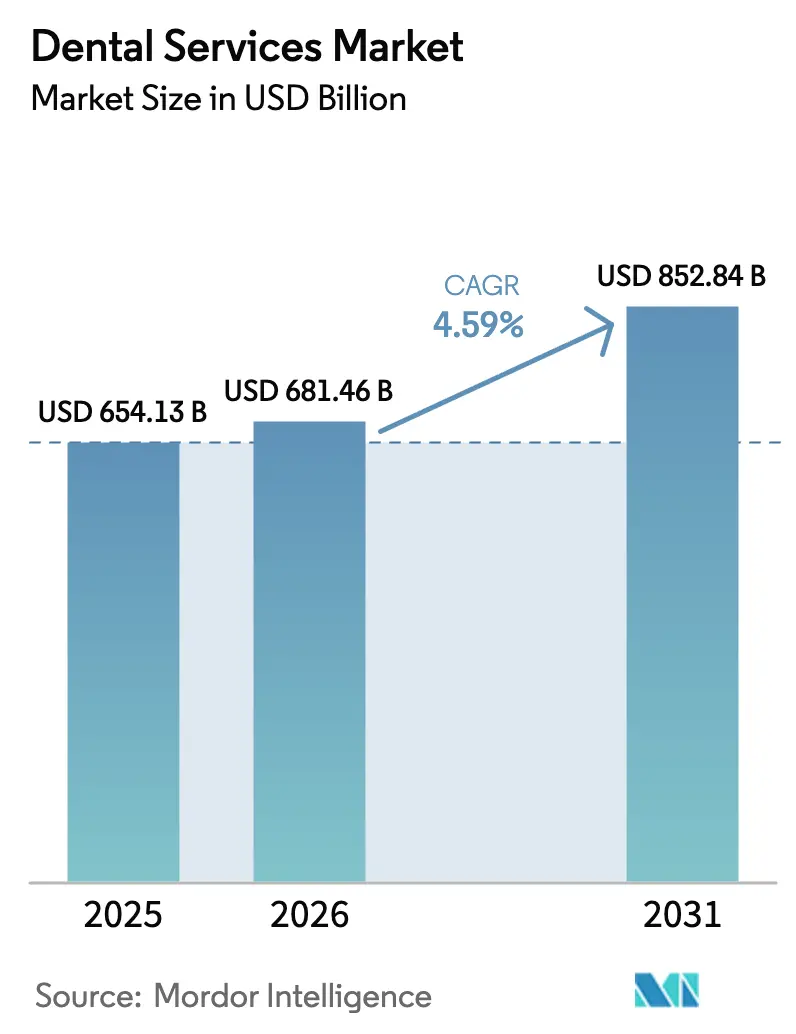

The Dental Services Market size is expected to grow from USD 654.13 billion in 2025 to USD 681.46 billion in 2026 and is forecast to reach USD 852.84 billion by 2031 at 4.59% CAGR over 2026-2031.

Persistent tooth loss among older adults, rapid adoption of fully digital workflows, and the scale advantages of dental service organizations (DSOs) are expanding the global patient base while reshaping practice economics. Aging populations in Japan, Europe, and North America continue to anchor high-value implant and denture demand, even as clear-aligner therapy attracts younger consumers seeking discreet orthodontics. DSOs leverage centralized procurement and AI-guided scheduling to increase chair utilization, but labor shortages among hygienists and assistants limit near-term capacity in many developed markets. Supply-chain volatility for titanium and zirconia, together with rising cyber-insurance premiums, compresses margins for smaller clinics yet reinforces the competitive edge of well-capitalized consolidators.

Key Report Takeaways

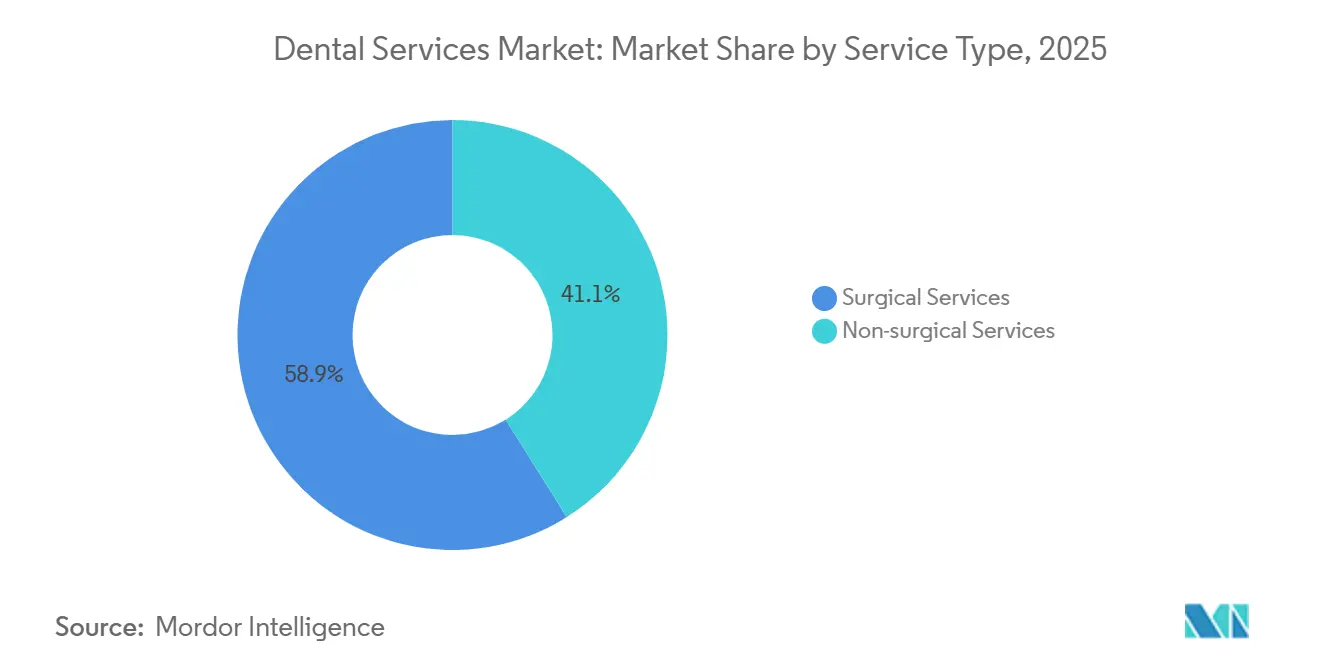

- By service type, surgical services led with 58.92% of the dental services market share in 2025. Non-surgical services are forecast to expand at a 7.06% CAGR through 2031, driven by preventive subscriptions and cosmetic whitening demand.

- By patient age, the above-17-to-60 group accounted for 54.87% of revenue in 2025, while the under-17 segment is set to grow at 9.63% annually to 2031.

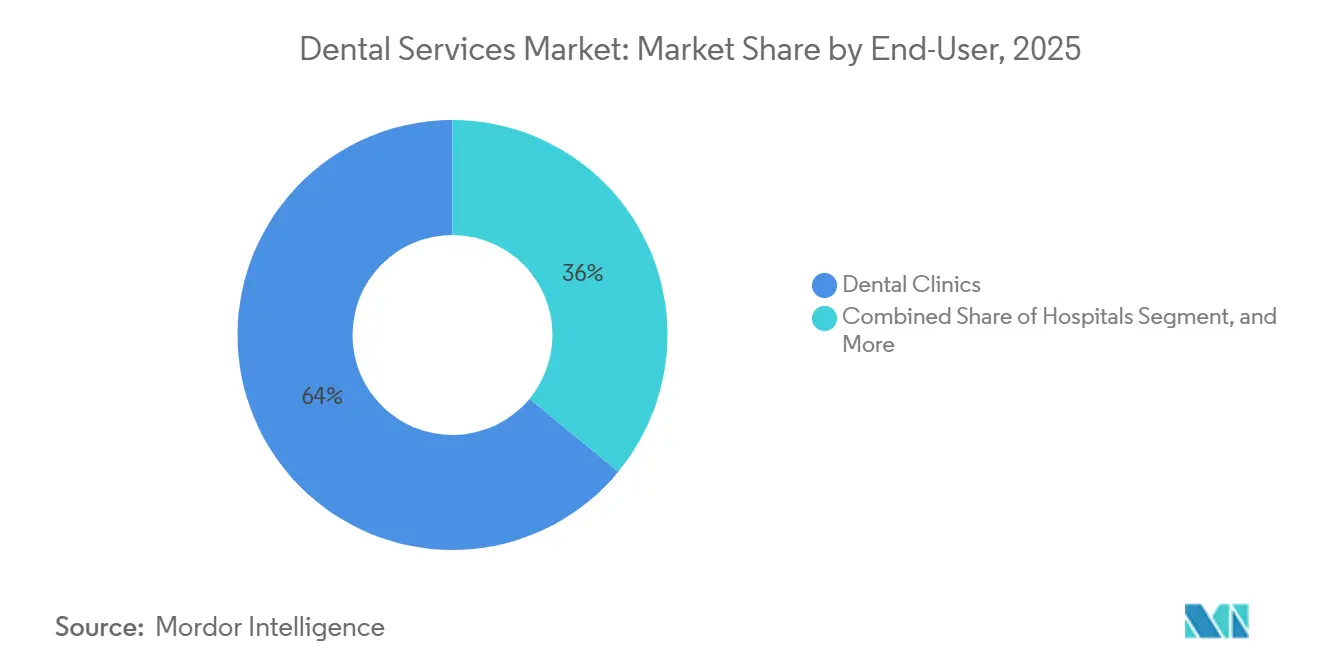

- By end user, dental clinics accounted for 64.02% of the dental services market in 2025 and are advancing at an 8.18% CAGR through 2031.

- By geography, North America held 39.28% of the dental services market share in 2025, whereas Asia-Pacific is projected to post a 10.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of Dental Disease Rate | +1.2% | Global, higher in emerging markets | Medium term (2-4 years) |

| Aging Population Driving Restorative Procedures | +1.0% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Growing Demand for Aesthetic & Cosmetic Dentistry | +0.8% | North America & Europe, rising in Asia-Pacific | Short term (≤ 2 years) |

| Increasing Awareness of Dental Health | +0.7% | Global, especially emerging markets | Medium term (2-4 years) |

| Rapid Expansion of Dental Service Organization (DSO) Model | +0.6% | North America, expanding to Europe & APAC | Medium term (2-4 years) |

| AI-Enabled Teledentistry & Preventive Analytics Adoption | +0.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Tooth-Loss Burden

Global life-expectancy gains are enlarging the pool of patients over 65, a cohort with elevated rates of periodontal disease and edentulism. In Japan, 25% of seniors lacked natural teeth in 2024, spurring steady demand for full-arch restorations. Singapore’s health ministry reported that 60% of residents aged 60-74 had fewer than 20 natural teeth, prompting expanded implant reimbursement. Manufacturers gained U.S. FDA clearance for new zirconia implants formulated for patients with metal allergies in 2024, widening clinical options. Practices integrating geriatric sedation protocols and mini-implant systems are therefore positioned to capture premium restorative revenue.

Growing Demand for Cosmetic & Aesthetic Dentistry

Social-media exposure and ubiquitous video calls heighten patients' focus on smile aesthetics, driving double-digit growth in veneers, bonding, and chairside whitening.[1]American Academy of Cosmetic Dentistry, “Cosmetic Dentistry Trends Report,” AACD.COM The teeth-whitening segment alone generated USD 6.2 billion in 2025 as consumers sought rapid, non-invasive upgrades. Align Technology disclosed that 45% of 2025 clear-aligner starts involved adults over 30, underscoring broadening acceptance of discreet orthodontics. Regulators increasingly police marketing claims; the U.K. General Dental Council mandated evidence-based before-and-after imagery in 2024. Clinics equipped with digital smile-design software and transparent consent protocols are gaining competitive traction.

Expansion of Dental Insurance Coverage & DSOs

Between 2021 and 2025, 23 U.S. states broadened Medicaid adult dental benefits, adding 8.7 million covered lives.[2]Centers for Medicare & Medicaid Services, “Medicaid Dental Benefits Expansion,” CMS.GOV DSOs negotiated higher-than-market reimbursement rates by aggregating procedure volume, with Medicaid and CHIP representing 18% of Heartland Dental’s case mix in 2025. Germany’s 2024 decision to subsidize CAD/CAM crowns trimmed patient out-of-pocket costs by EUR 150 per unit and lifted restorative case volume by 14%. Centralized billing and payer diversification, therefore, accelerate share capture for large practice networks.

Growing Adoption of Digital Dentistry

FDA approvals of 47 digital-dentistry devices in 2024, including AI-enhanced detection software and robotic implant systems, validated the technology pipeline. Sales of Dentsply Sirona’s Primescan intraoral scanner jumped 19% in 2025 as same-day crown workflows reached critical mass. 3D-printed denture bases cut production costs by roughly 40%, compressing turnaround from weeks to hours. Multi-site DSOs adopted Pearl AI and Overjet analytics to standardize diagnostics, reducing variability across hundreds of locations. ISO 13485 certification underpins global reimbursement eligibility for digital workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement in developing regions | -0.7% | Asia-Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| High cost of advanced equipment | -0.5% | Global, sharper in price-sensitive markets | Medium term (2-4 years) |

| Skilled workforce shortages | -0.4% | Global, severe in rural and underserved areas | Medium term (2-4 years) |

| Cyber-security risks in digital platforms | -0.2% | Global, most evident in digitally advanced markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages & Hygienist Burnout

The U.S. faced 16,400 vacant hygienist positions in 2025, a 9% shortfall that forces practices to cap appointment slots.[3]American Dental Association Health Policy Institute, “Dental Workforce Shortages,” ADA.ORG Burnout stems from repetitive-motion injuries and aerosol exposure, with 42% of surveyed hygienists planning to cut hours within five years. The U.K. recorded a 38% three-year attrition rate among dental nurses in 2024. Australia projects a deficit of 2,100 hygienists by 2030 unless training capacity or immigration increases. Wage inflation, U.S. hygienist pay averaged USD 42.50 per hour in 2024, squeezing smaller practices lacking DSO-level purchasing power. DSOs with in-house academies and career-ladder programs retain staff more effectively.

High Out-of-Pocket Costs in Emerging Economies

In India, patients fund roughly 80% of dental spending directly; a single implant priced at INR 25,000-50,000 (USD 300-600) equals one to two months of median urban wages. Indonesia’s BPJS plan covers only extractions and fillings, restricting full-service utilization to just 22% of residents. Long public-clinic queues in Brazil channel middle-income patients to private offices charging BRL 800-1,500 (USD 160-300) for a root canal. Cross-border dental tourism to Thailand and Mexico, where prices run 40-60% lower, drains local revenue but highlights latent demand. Microfinance and installment-payment tools help expand access yet carry elevated default risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Surgical Revenue Dominance Meets Preventive Momentum

Surgical care accounted for 58.92% of 2025 revenue, as implants, orthodontics, and oral surgery command premium fees, while non-surgical segments are slated for a 7.06% CAGR to 2031. Implant costs in North America average USD 3,000-6,000 each, propelled by demand from an aging yet increasingly active population. Clear-aligner uptake continued to swell; 1.8 million of Align Technology’s 4 million 2025 global starts involved adults over 21, reflecting expanded remote-monitoring capabilities. Endodontic and periodontal specialists retain pricing power amid limited provider supply, with urban U.S. root canals priced at USD 1,200-1,800 per tooth.

Preventive dentistry is carving out faster growth. State-mandated sealant programs under Medicaid’s EPSDT benefits lowered caries incidence by 60% in school-age children, encouraging broader payer adoption. Cosmetic demand remains resilient; 71% of elective veneer and whitening patients used third-party financing in 2024, enabling practices to capture higher discretionary spend. Same-day CAD/CAM crowns reduce lab turnaround time from 2 weeks to 2 hours, improving acceptance rates by about 18%. Consistent FDA oversight of new restorative materials sustains patient and payer confidence.

By Patient Age Group: Pediatric Surge Outpaces Adult Stability

Adults aged 18-60 contributed 54.87% of 2025 revenue, yet the pediatric under-17 segment is projected to post a 9.63% CAGR through 2031. Early-phase orthodontics gained clinical momentum after the American Association of Orthodontists' guidance in 2024, driving a 27% jump in phase-I treatments. School-based care for 4.2 million U.S. children cut emergency-room visits for dental pain by 22%. Subscription pediatric plans attracted 340,000 families by end-2025, reflecting parents’ appetite for budgeting predictability.

Seniors, though lower in volume, deliver outsized revenue via complex prosthetics. Edentulism still afflicts 17% of U.S. adults over 65, sustaining demand for overdentures and fixed restorations. Expanded Medicare Advantage coverage for mini-implants in 2025 shaved patient costs by USD 1,200-2,000 per arch. Practices in retiree hubs such as Florida report that implant-supported overdentures now represent 41% of the case mix.

By End-User: Clinic-Centric Growth Fueled by DSO Efficiency

Dental clinics accounted for 64.02% of the dental services market in 2025 and are forecast to grow at an 8.18% CAGR as DSOs optimize throughput. Heartland Dental clinics averaged 42 daily visits, 18% above the independent average, by deploying AI scheduling. Pacific Dental Services invested USD 120 million in cloud infrastructure, trimming admin overhead 14% across 860 sites. Aspen Dental opened 78 clinics across underserved communities in 2024-2025, coupling Medicaid acceptance with transparent pricing.

Hospitals concentrate on trauma and medically complex cases; only 18% of U.S. hospitals house dental units. Academic institutions enroll 26,874 dental students, yet high tuition fees impede workforce growth. DSOs secure 20-30% procurement discounts on implants and restorative materials versus independents, underpinning margin resilience.

Geography Analysis

North America retained 39.28% of global revenue in 2025 on the strength of USD 385 per-capita spending and 77% insurance coverage among non-elderly adults. Canadian provinces earmarked CAD 1.2 billion to extend adult dental subsidies, while cross-border flows saw 1.2 million U.S. residents travel to Mexico for lower-cost care.

Europe contends with tighter product rules under the EU Medical Device Regulation, which trimmed the CE-marked implant roster by 12% by 2024. Germany’s subsidy for implant-supported crowns cut co-pays by EUR 200-300, adding 9% implant volume. NHS-access challenges pushed 12 million U.K. adults toward private practices, where a single crown costs GBP 800-1,200.

Asia-Pacific is poised for a 10.27% CAGR, led by China and India. China approved 34 homegrown digital devices in 2024, cutting scanner acquisition costs by 25%. India welcomed 500,000 dental tourists in 2024, generating USD 320 million as clinics marketed ISO-certified facilities at deep discounts. The GCC reached a clinic density of 1 per 2,800 residents by 2024, driven by expatriate demand in Dubai.

Mordor Intelligence provides coverage of the dental services market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The top 10 DSOs held roughly 18% of U.S. practice locations in 2025, indicating moderate fragmentation and room for roll-ups. Heartland Dental surpassed 2,300 affiliated offices, Pacific Dental Services topped 860, and Aspen Dental continued a de novo push into underserved ZIP codes. Aspen’s 2024 acquisition of 12 regional labs signals a vertical-integration trend aimed at controlling prosthetic quality and turnaround. AI vendors Pearl AI, Overjet, and VideaHealth locked in multi-year network deals to supply diagnostic software that narrows clinician variability. Align Technology maintained a moat with more than 3,400 active or pending patents as of December 2025.

Technology remains the decisive differentiator: practices using intraoral scanning and cloud software produced 15-20% higher revenue per operatory than analog peers. Cyber risk escalates alongside digitization; HHS logged 725 healthcare breaches in 2024, prompting cyber liability premiums to jump 25% for clinics lacking multi-factor authentication. Compliance regimes such as HIPAA and GDPR impose fixed costs that larger DSOs spread across larger revenue bases. Cross-border expansion is limited; Q&M Dental Group’s 2025 purchase of an 18-clinic Malaysian chain highlights the licensing and reimbursement complexities of international moves.

Dental Services Industry Leaders

Aspen Dental Management, Inc.

Dental Care Alliance

Great Expressions Dental Centers

Pacific Dental Services

Smile Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: VideaHealth’s AI platform rolled out across GPS Dental’s 100+ practices, reinforcing mid-market DSO enthusiasm for enterprise-level diagnostics.

- April 2025: MAX secured a USD 77 million credit facility to expand partnerships in oral and maxillofacial surgery, spotlighting investor appetite for specialized high-margin segments.

- December 2024: Patterson Companies shareholders approved a USD 4.1 billion buy-out by Patient Square Capital, underscoring private-equity confidence in dental supply and services integration.

- May 2024: Progressive Dental Marketing completed a USD 100 million recapitalization with McCarthy Capital to accelerate domestic and international expansion of practice-support services.

Global Dental Services Market Report Scope

As per the scope of the report, Dental Services offered a range of treatment options to maintain oral health and manage dental disorders, including cavities, tooth loss, gum disease, and others.

The Dental Services Market Report is Segmented by Service Type (Non-surgical Services: Preventive, Restorative, Cosmetic; Surgical Services: Implants & Oral Surgery, Orthodontics, Endodontics & Periodontics), Patient Age Group (Upto 17, Above 17 to Upto 60, Above 60), End-User (Dental Clinics, Hospitals, DSOs, Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (in USD million) for the above segments.

| Non-surgical Services | Preventive Dentistry |

| Restorative Dentistry | |

| Cosmetic Dentistry | |

| Surgical Services | Implants & Oral Surgery |

| Orthodontics | |

| Endodontics & Periodontics |

| Upto 17 |

| Above 17 to Upto 60 |

| Above 60 |

| Dental Clinics |

| Hospitals |

| Dental Service Organisations (DSOs) |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Non-surgical Services | Preventive Dentistry |

| Restorative Dentistry | ||

| Cosmetic Dentistry | ||

| Surgical Services | Implants & Oral Surgery | |

| Orthodontics | ||

| Endodontics & Periodontics | ||

| By Patient Age Group | Upto 17 | |

| Above 17 to Upto 60 | ||

| Above 60 | ||

| By End-User | Dental Clinics | |

| Hospitals | ||

| Dental Service Organisations (DSOs) | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will dental-care spending be by 2031?

The dental services market size is forecast to reach USD 852.84 billion by 2031, expanding at a 4.59% CAGR from 2026 to 2031.

Which service line is growing fastest?

Non-surgical preventive and cosmetic services are projected to post a 7.06% CAGR through 2031, outpacing surgical segments that already dominate revenue.

Why are DSOs expanding so quickly?

DSOs leverage centralized procurement, AI-guided scheduling, and insurer negotiations to raise margins and acquire independent clinics efficiently.

What is fueling Asia-Pacific’s growth?

Rising middle-class incomes, universal health care rollouts, and medical tourism demand push Asia-Pacific to a forecast 10.27% CAGR through 2031.

How is digital dentistry changing care delivery?

Intraoral scanning, same-day CAD/CAM crowns, 3D printing, and AI diagnostics shorten treatment cycles and standardize outcomes, lifting revenue per operatory 15-20%.

Page last updated on: