Stereotactic Radiosurgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 77.22 Billion |

| Market Size (2031) | USD 104.04 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stereotactic Radiosurgery Market Analysis by Mordor Intelligence

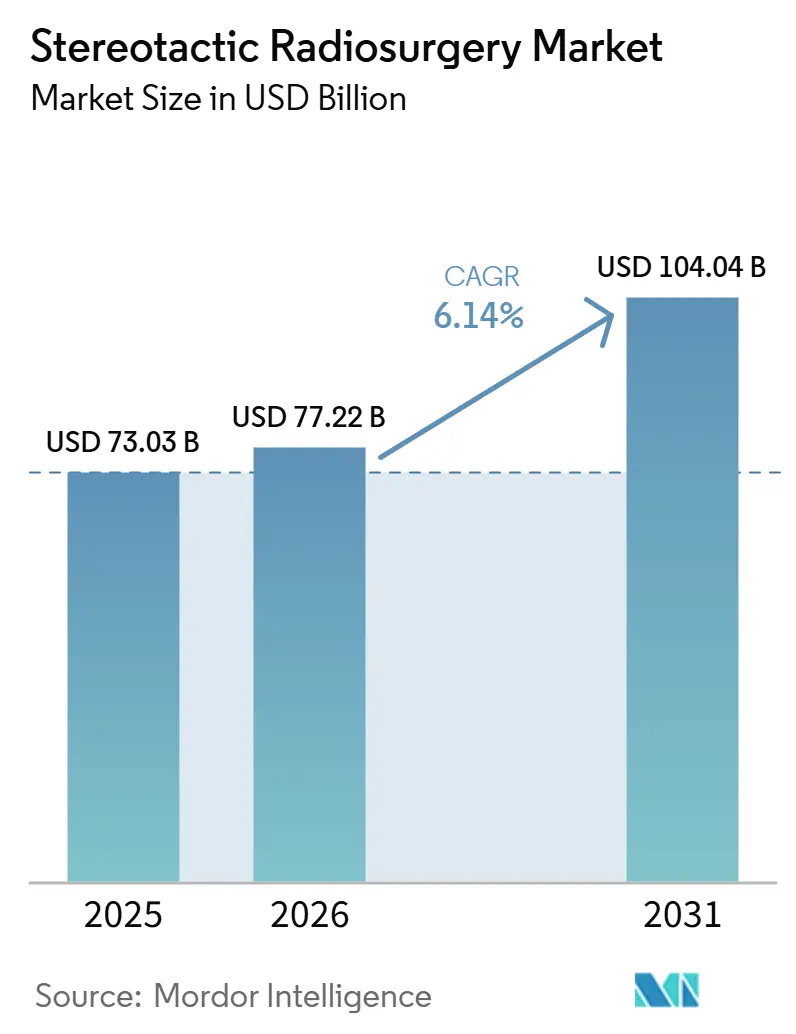

The Stereotactic Radiosurgery Market size is expected to increase from USD 73.03 billion in 2025 to USD 77.22 billion in 2026 and reach USD 104.04 billion by 2031, growing at a CAGR of 6.14% over 2026-2031.

The stereotactic radiosurgery market was valued at USD 73.03 billion in 2025 and estimated to grow from USD 77.22 billion in 2026 to reach USD 104.04 billion by 2031, at a CAGR of 6.14% during the forecast period (2026-2031). The stereotactic radiosurgery market is expanding as radiation therapy remains part of treatment for nearly 60% of cancer cases worldwide, and more than 2 million patients receive radiation therapy each year in the United States, which keeps the clinical base for high-precision treatment broad and active. The stereotactic radiosurgery market is also gaining support from a wider treatment pool in oncology and neurology, as evidence and regulatory clearances continue to move use cases beyond classic intracranial tumors. Growth in the stereotactic radiosurgery market is no longer tied only to new hardware placements, because buyers are also paying for planning software, workflow tools, and recurring service layers that improve utilization and staffing efficiency. Outpatient treatment models and frameless delivery are also changing buyer economics in the stereotactic radiosurgery market, because health systems now weigh total workflow cost and patient throughput more closely than system price alone. The main constraints on the stereotactic radiosurgery market remain concentrated cobalt-60 supply and the high capital burden of vault construction and installation, which continue to shape technology choice and access in lower-resource settings.

Key Report Takeaways

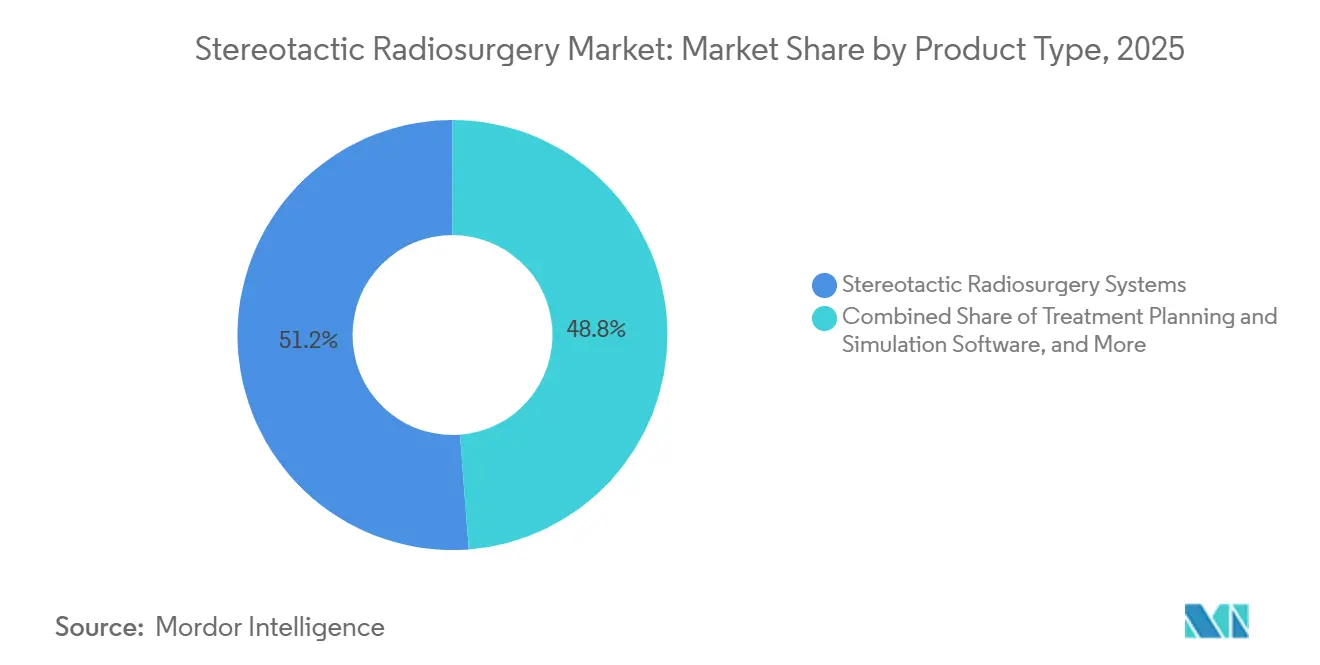

- By product type, stereotactic radiosurgery systems led with 51.24% revenue share in 2025, while treatment planning and simulation software is forecasted to expand at 6.36% CAGR through 2031.

- By technology, gamma knife technology held 41.27% revenue share in 2025, while robotic radiosurgery technology is projected to record the fastest 6.64% CAGR through 2031.

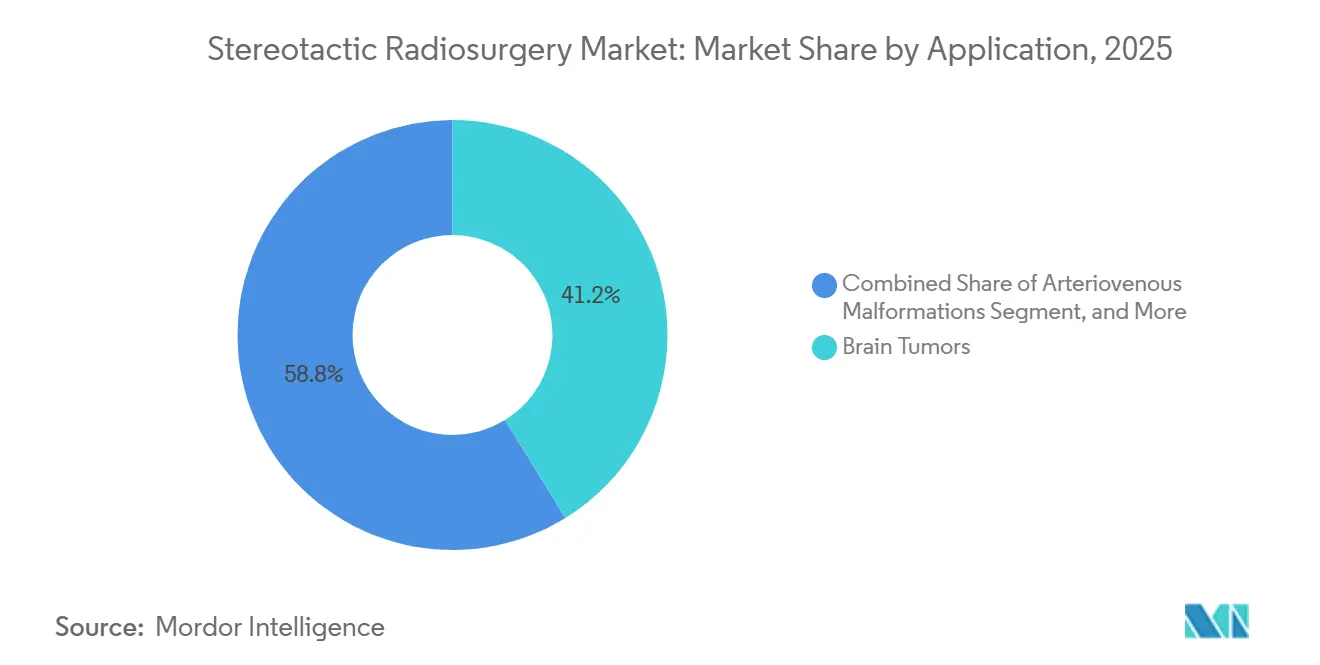

- By application, brain tumors accounted for 41.16% share in 2025, while spinal tumors and lesions are projected to advance at 7.46% CAGR through 2031.

- By end-user, hospitals held 40.53% revenue share in 2025, while specialty clinics and centers are forecasted to grow at 7.17% CAGR through 2031.

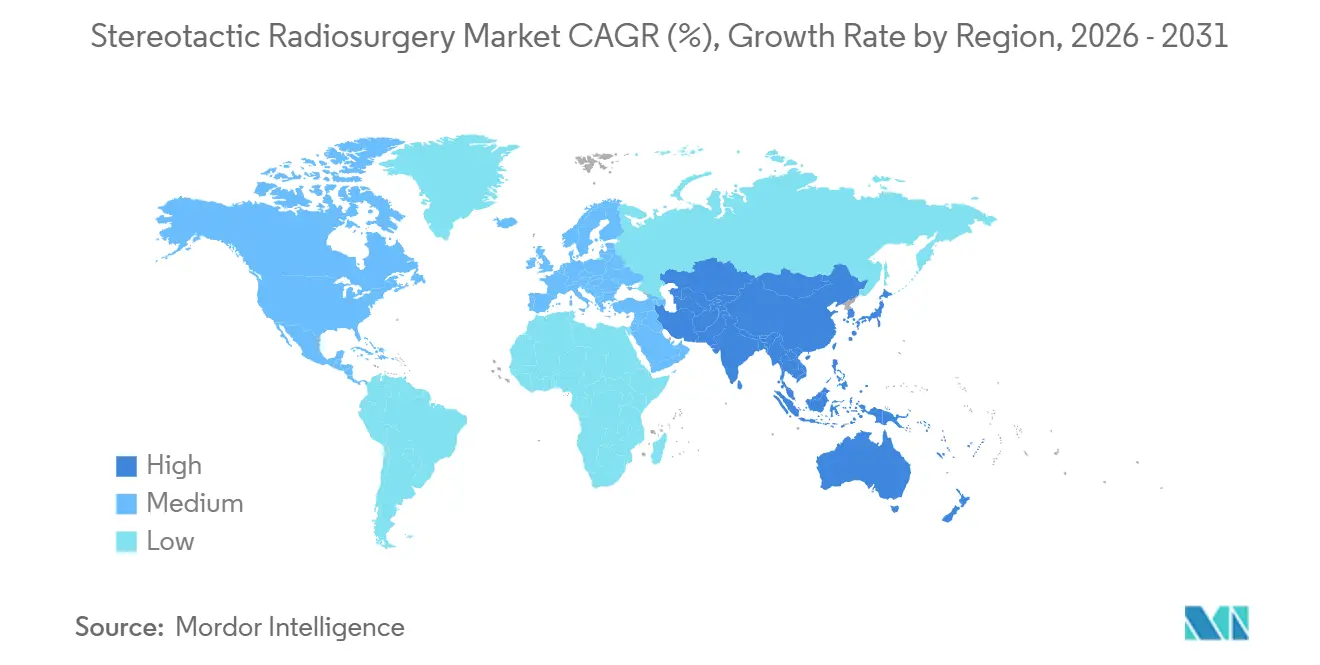

- By geography, North America captured 44.27% revenue share in 2025, while Asia-Pacific is projected to expand at 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stereotactic Radiosurgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Brain Metastases and Functional Neurological Disorders | +1.5% | Global, highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Shift Toward Non-Invasive, Outpatient Neuro-Oncology Care | +1.2% | North America, Western Europe, APAC urban centers | Short term (≤ 2 years) |

| AI-Enabled Treatment Planning and Workflow Automation | +1.0% | Global, early gains in North America and Germany | Short term (≤ 2 years) |

| Expansion of Multi-Modal Radiosurgery Platforms in Tertiary Centers | +0.7% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Reimbursement Support for High-Precision Radiation in Mature Markets | +0.5% | North America and EU | Short term (≤ 2 years) |

| Increasing Adoption of Image-Guided and Adaptive Radiation Therapy Technologies | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Brain Metastases and Functional Neurological Disorders

The stereotactic radiosurgery market is benefiting from a broader patient pool than incidence counts alone suggest, because longer survival in breast, lung, and melanoma care is creating more cases with isolated or limited central nervous system recurrence. Those patients often fit stereotactic treatment better than whole-brain radiation or open surgery, which supports repeat procedure demand over time. This means the stereotactic radiosurgery market is seeing volume growth that is not fully visible through hardware installation counts alone. The neurological side of demand also widened when Elekta received U.S. FDA 510(k) clearance in July 2025 for refractory, drug-resistant mesial temporal lobe epilepsy in adults, which added a durable non-oncology use case to the installed base.[1]Elekta, “Elekta Receives U.S. FDA 510(k) Clearance for its Gamma Knife Radiosurgery System to Treat Patients with Refractory, Drug-Resistant Mesial Temporal Lobe Epilepsy,” Elekta Investor Press Release, elekta.com That clearance matters because it opens a patient population that had been more dependent on invasive resection. It also gives the stereotactic radiosurgery market a recurring demand layer that is less exposed to oncology treatment cycles.

Shift Toward Non-Invasive, Outpatient Neuro-Oncology Care

The stereotactic radiosurgery market is moving toward same-day outpatient treatment as mask-based and frameless approaches replace older invasive workflows in many intracranial cases. This shift helps providers reduce admission burden while preserving local control, which makes radiosurgery easier to position against surgery in selected patients. The stereotactic radiosurgery market is also supported by new installations that make outpatient delivery more practical. Health Sciences Center Winnipeg deployed Elekta Esprit in January 2026 with integrated CT imaging, which removed the same-day MRI requirement and enabled fractionated treatment for larger tumors that had been harder to manage in a single session.[2]Health Sciences Centre Foundation, “New Gamma Knife for Minimally Invasive Brain Surgery Unveiled at Health Sciences Centre,” HSC Foundation Press Release, hscfoundation.mb.ca Accuray widened access in Austria in May 2025 through the country’s first CyberKnife facility, and it also supported first patient treatments in Melbourne in October 2025 through its work with Icon Group, which signaled a broader East Coast expansion path in Australia.[3]Accuray Incorporated, “Accuray Announces First SRS/SBRT Patient Treatments in Austria With the CyberKnife System,” Accuray Press Release, prnewswire.com These changes help the stereotactic radiosurgery market fit ambulatory care models that value short sessions, predictable throughput, and lower dependence on inpatient infrastructure.

AI-Enabled Treatment Planning and Workflow Automation

The stereotactic radiosurgery market is increasingly shaped by software because staffing limits at many centers now weigh more heavily than machine capacity. AI planning tools are addressing that bottleneck by reducing contouring effort, shortening planning time, and improving consistency across complex cases. At the AAPM 2026 Annual Meeting, the reasoning-based SAGE planning agent generated single-fraction SRS plans that were clinically indistinguishable from physician-approved human expert plans, and it showed statistically superior cochlear sparing in one cohort, which is relevant in lesions near the posterior fossa. These steps show that the stereotactic radiosurgery market is monetizing more of the planning layer instead of relying only on capital equipment cycles. They also support subscription and service revenue models that can expand even when new machine placements slow.

Reimbursement Support for High-Precision Radiation in Mature Markets

The stereotactic radiosurgery market remains stronger in mature healthcare systems because payment policy has moved closer to clinical practice across a defined set of indications. In the United States, CMS updated 2025 hospital outpatient payment rates by 2.9% under the Hospital Outpatient Prospective Payment System final rule, which supported equipment planning at facilities with higher Medicare exposure. Commercial payers often follow Medicare coverage patterns with a lag, so policy moves in the United States can influence the broader stereotactic radiosurgery market beyond public reimbursement alone. In Europe, national cancer plans and structural funding are widening access outside top academic hospitals, which expands the institutional buyer base. This support gives the stereotactic radiosurgery market a more stable path for replacement demand and selected new installations in mature regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Vaults, Shielding, and Platform Installation | -1.3% | Global, most acute in APAC emerging markets and MEA | Long term (≥ 4 years) |

| Shortage of Trained Radiosurgery Teams and Medical Physicists | -0.9% | Global, concentrated in South America and MEA | Medium term (2-4 years) |

| Cobalt-60 Supply Dependence for Gamma Knife Installations | -1.0% | North America and EU | Short term (≤ 2 years) |

| Lengthy Clinical Validation and Regulatory Clearance Cycles | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Vaults, Shielding, and Platform Installation

The stereotactic radiosurgery market still faces a structural access problem because total project cost extends well beyond the headline price of the treatment platform. Shielded bunker construction can add USD 1 million to USD 3 million per installation, which is a major barrier for community oncology centers and stand-alone outpatient settings. This keeps much of the stereotactic radiosurgery market concentrated in better-funded institutions that can absorb both equipment and facility costs. Even so, the stereotactic radiosurgery market still runs on a global installed base where conventional infrastructure assumptions remain common. That means cost pressure continues to slow first-time adoption in lower-resource regions even as newer architectures gain visibility.

Cobalt-60 Supply Dependence for Gamma Knife Installations

The stereotactic radiosurgery market also faces a supply chain constraint that is specific to Gamma Knife installations. In November 2025, the Source Security Working Group warned the Office of the United States Trade Representative that proposed tariffs on Canadian-origin cobalt-60 would undermine U.S. healthcare capacity because domestic supply does not currently meet medical demand. Because cobalt-60 has a short half-life, inventory buffering is limited, and that makes concentration risk harder to manage. This issue is already influencing technology selection inside the stereotactic radiosurgery market, especially for first-generation installations where buyers are weighing supply resilience more directly. As a result, cobalt-free LINAC-based and robotic systems are receiving stronger consideration when procurement teams compare long-term operating risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hardware Anchors Revenue, Software Lifts Recurring Monetization

Stereotactic radiosurgery systems held 51.24% of the stereotactic radiosurgery market share in 2025, which kept hardware at the center of revenue generation even as the business mix started to shift. The largest share still reflects the capital intensity of treatment platforms and the replacement cycle now underway at major academic centers. The stereotactic radiosurgery market is seeing this most clearly in Gamma Knife upgrades, where newer systems are replacing aging units rather than opening entirely new accounts.

Treatment planning and simulation software is expected to be the fastest-growing product type at 6.36% CAGR through 2031, and that is changing how revenue is captured over the life of an installed system. Software is moving procurement toward subscriptions, upgrades, and service contracts that continue after the initial hardware sale. The stereotactic radiosurgery industry is therefore seeing value move into workflow intelligence, contouring, optimization, and treatment planning support rather than remaining concentrated in the machine alone. Services and supporting technologies still matter, but their role increasingly depends on the size and quality of the installed base that software is helping to monetize more effectively.

By Technology: Gamma Knife Leads Installed Depth, Robotic Systems Expand the Addressable Base

Gamma knife technology accounted for 41.27% of technology-segment revenue in 2025, which shows how strongly long clinical use, intracranial specialization, and installed-base depth still shape buying patterns. That leadership remains tied to academic center demand and to recurring replacement and source-related needs in mature markets. The stereotactic radiosurgery market still treats Gamma Knife as the benchmark for intracranial precision in many hospital settings. At the same time, the stereotactic radiosurgery market is giving more weight to technologies that ease infrastructure demands and widen placement opportunities beyond large referral centers.

Robotic radiosurgery technology is projected to grow at 6.64% CAGR through 2031, which makes it the fastest-advancing technology segment in the stereotactic radiosurgery market. Growth is tied to cobalt-free and in some cases vault-light or vault-free positioning, which lowers the barrier for outpatient centers and specialty clinics. LINAC-based SRS remains the second-largest technology category because large radiation oncology departments can use shared infrastructure across conventional radiotherapy and radiosurgery. The stereotactic radiosurgery industry is therefore moving toward a technology comparison that weighs workflow, infrastructure, and resilience just as heavily as dose delivery performance.

By Application: Intracranial Demand Holds the Base, Spine and Functional Care Add the Growth Edge

Brain tumors accounted for 41.16% of the stereotactic radiosurgery market size in 2025, which kept intracranial oncology at the center of procedure demand. That leadership reflects the high volume of gliomas, meningiomas, acoustic neuromas, and especially brain metastases that remain well aligned with focused radiosurgical treatment. The stereotactic radiosurgery market still draws much of its core revenue from these established intracranial indications. The installed base, physician familiarity, and evidence history all reinforce that position across major hospital programs.

Spinal tumors and lesions are forecasted to grow at 7.46% CAGR through 2031, which reflects broader use of stereotactic body radiation therapy for oligometastatic spine disease in patients less suited to open surgery. Arteriovenous malformations continue to provide a durable non-oncologic volume stream because treatment effect unfolds over time and follow-up imaging remains predictable. Trigeminal neuralgia is also gaining attention as patient preference increasingly favors non-invasive treatment over surgery in older or higher-risk populations. The stereotactic radiosurgery market is therefore broadening application demand without losing the intracranial case mix that built the category in the first place.

By End-User: Hospitals Retain the Base, Specialty Clinics Build Faster Momentum

Hospitals retained 40.53% of end-user revenue in 2025, which reflects their continued control over the largest treatment platforms, multidisciplinary referral pathways, and specialist staffing. That share also reflects the concentration of gamma knife and proton systems inside academic and large community medical centers. The stereotactic radiosurgery market still depends on hospitals for a large part of capital procurement and complex case handling. Hospitals also remain the main setting where payer policy, tumor board coordination, and replacement budgets come together in a single site of care.

Specialty clinics and centers are projected to grow at 7.17% CAGR through 2031, which makes them the fastest-moving end-user group in the stereotactic radiosurgery market. Their rise is tied to compact robotic and advanced LINAC-based systems that fit stand-alone oncology settings more easily than traditional bunker-heavy models. Research and academic institutes remain the smallest end-user segment by revenue, yet they still shape clinical evidence, payer policy, and product design in ways that influence the entire stereotactic radiosurgery market.

Geography Analysis

North America held 44.27% of the stereotactic radiosurgery market share in 2025, which kept it as the largest regional contributor to current revenue. The United States supports that position through a dense concentration of academic cancer centers, ongoing replacement demand, and a CMS reimbursement structure that explicitly covers gamma knife, LINAC-based, and robotic stereotactic radiation therapy across defined intracranial indications. Payment clarity matters because it reduces hesitation around both utilization and capital planning in established programs. The stereotactic radiosurgery market in Canada also remains active, and Health Sciences Centre Winnipeg unveiled a USD 3.2 million Elekta Esprit system in January 2026 with integrated CT imaging and fractionation support for larger tumors. Mexico remains a smaller but advancing part of the regional stereotactic radiosurgery market, supported by private hospital expansion and medical tourism demand for advanced oncology procedures.

Europe ranks second in the stereotactic radiosurgery market, with Germany, the United Kingdom, France, Italy, and Spain accounting for the largest regional demand base. National cancer strategies and public funding support are widening access beyond top referral hospitals, which is helping secondary centers participate in precision radiotherapy adoption. France also strengthened its position as an early adopter with the late 2025 installation of the Varian Halcyon 5.0 platform with integrated real-time motion management at Institut du Cancer Avignon-Provence, while Italy continued its Esprit replacement cycle through active Gamma Knife upgrades.

Asia-Pacific is projected to post the fastest 8.33% CAGR in the stereotactic radiosurgery market size through 2031, which reflects a wider installation runway and rising investment in high-precision oncology infrastructure. China is a major part of that story after Accuray received dual NMPA approvals in January 2025, and the company stated that China may need around 2,000 radiation therapy systems over the next 5 years. India is also expanding its advanced treatment base, with IBA’s 2025 agreements with AIG Hospitals and Apollo Hospitals expected to add compact proton capacity and lift the country’s proton center count over time. Australia showed momentum in outpatient radiosurgery when Accuray and Icon Group supported first patient treatments in Melbourne in October 2025, while the Middle East, Africa, and South America remain smaller but active investment regions led by public-private oncology capacity additions.

Competitive Landscape

The stereotactic radiosurgery market is moderately concentrated, with Elekta, Varian, Accuray, Brainlab, IBA, and ZAP Surgical holding much of the global revenue base across hardware and software. Competition is no longer driven only by beam precision or treatment time because buyers are also comparing planning intelligence, workflow integration, and service economics. That shift is changing where differentiation sits inside the stereotactic radiosurgery market, especially as AI tools and adaptive planning features move closer to baseline expectations. The stereotactic radiosurgery market is also showing a split structure, where hardware remains concentrated among a limited set of platform vendors while software and planning layers are becoming more crowded. This split helps large incumbents defend installed accounts, but it also creates room for platform-agnostic planning vendors to build their own footprint.

Several strategic moves since 2025 show how competition is evolving in the stereotactic radiosurgery market. Brainlab used its 2025 Frankfurt listing process to position itself for faster software commercialization, broader ambulatory surgery center expansion, and entry into adjacent verticals, which points to a strategy that extends beyond conventional radiation oncology boundaries. Accuray also improved its position in Asia when it received China NMPA approval for the Radixact SynC and CyberKnife S7 systems in January 2025, which strengthened access to one of the largest future equipment pools in the stereotactic radiosurgery market. Elekta, meanwhile, kept its installed-base strategy active through visible Esprit replacement launches in established treatment centers, which reinforced its hold in intracranial radiosurgery accounts.

Pricing pressure is becoming more visible at the lower end of the stereotactic radiosurgery market as Chinese manufacturers expand within Asia-Pacific and selected emerging markets. Their position is supported by domestic policy incentives, local approval pathways, and lower system pricing relative to Western competitors. This pressure is beginning to matter outside China as distribution reach grows into Southeast Asia, India, and parts of the Middle East. The result is a stereotactic radiosurgery market where premium vendors still dominate high-acuity and replacement-driven accounts, while lower-cost suppliers exert growing influence in value-sensitive installations. Software capability, source independence, and infrastructure flexibility are therefore becoming as important as brand history in competitive positioning.

Stereotactic Radiosurgery Industry Leaders

Elekta AB

Siemens Healthineers AG

Accuray Incorporated

Brainlab AG

Hitachi, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Wellstar MCG Health and the Georgia Cancer Center launched the Elekta Esprit Gamma Knife in Augusta, Georgia, replacing a legacy Gamma Knife model; the system delivers sub-millimeter precision treatment for brain tumors, lesions, and vascular abnormalities without incision or general anesthesia, and has already begun active patient treatment.

- June 2026: GE HealthCare received US FDA 510(k) clearance for MIM Contour ProtégéAI+ 2.0, an AI-enabled auto-contouring platform for radiation therapy planning that introduces a new MR Brain model and an updated CT Male Pelvis model; the clearance includes a Predetermined Change Control Plan enabling ongoing AI model updates without additional premarket submissions.

- January 2026: Health Sciences Center Winnipeg unveiled a USD 3.2 million Elekta Esprit Gamma Knife unit, Manitoba's first upgraded Gamma Knife system since 2003; the platform includes integrated CT imaging that eliminates same-day MRI requirements and enables fractionated treatment of larger tumors.

Global Stereotactic Radiosurgery Market Report Scope

According to the report’s scope, the stereotactic radiosurgery market comprises advanced radiation therapy systems, software, and services used to deliver highly precise, non-invasive radiation doses for treating tumors and neurological disorders. These technologies enable targeted treatment of brain tumors, vascular abnormalities, and functional neurological conditions while minimizing damage to surrounding healthy tissue.

The stereotactic radiosurgery market is segmented into product type, technology, application, end-user, and geography. By product type, the market is segmented into stereotactic radiosurgery systems, treatment planning and simulation software, supporting technologies, and services. By technology, the market is segmented into gamma knife technology, LINAC-based SRS technology, robotic radiosurgery technology, proton beam radiosurgery technology, image-guided radiosurgery technology, and AI-assisted radiosurgery technology. By application, the market is segmented into brain tumors, arteriovenous malformations, trigeminal neuralgia, spinal tumors and lesions, and functional disorders. By end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics/centers, and research and academic institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Stereotactic Radiosurgery Systems |

| Treatment Planning and Simulation Software |

| Supporting Technologies |

| Services |

| Gamma Knife Technology |

| LINAC-Based SRS Technology |

| Robotic Radiosurgery Technology |

| Proton Beam Radiosurgery Technology |

| Image-Guided Radiosurgery Technology |

| AI-Assisted Radiosurgery Technology |

| Brain Tumors |

| Arteriovenous Malformations |

| Trigeminal Neuralgia |

| Spinal Tumors and Lesions |

| Functional Disorders |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics/Centers |

| Research and Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Stereotactic Radiosurgery Systems | |

| Treatment Planning and Simulation Software | ||

| Supporting Technologies | ||

| Services | ||

| By Technology | Gamma Knife Technology | |

| LINAC-Based SRS Technology | ||

| Robotic Radiosurgery Technology | ||

| Proton Beam Radiosurgery Technology | ||

| Image-Guided Radiosurgery Technology | ||

| AI-Assisted Radiosurgery Technology | ||

| By Application | Brain Tumors | |

| Arteriovenous Malformations | ||

| Trigeminal Neuralgia | ||

| Spinal Tumors and Lesions | ||

| Functional Disorders | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics/Centers | ||

| Research and Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in stereotactic radiosurgery through 2031?

The market growth is supported by a larger pool of brain metastasis patients, wider outpatient use, AI-based planning tools, and reimbursement support in mature markets. The market is projected to grow from USD 73.03 billion in 2025 to USD 77.22 billion in 2026 to USD 104.04 billion by 2031 at a 6.14% CAGR.

Which product category leads current revenue?

Stereotactic radiosurgery systems led revenue with 51.24% share in 2025, showing that hardware still anchors current spending even as software grows faster.

Which technology is expanding the fastest?

Robotic radiosurgery technology is projected to record the fastest 6.64% CAGR through 2031 because it lowers infrastructure barriers and supports outpatient delivery models.

Which region offers the strongest growth outlook?

Asia-Pacific is projected to expand at 8.33% CAGR through 2031, supported by equipment approvals in China, proton investments in India, and broader precision oncology buildout across the region.

Page last updated on: