Dental Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

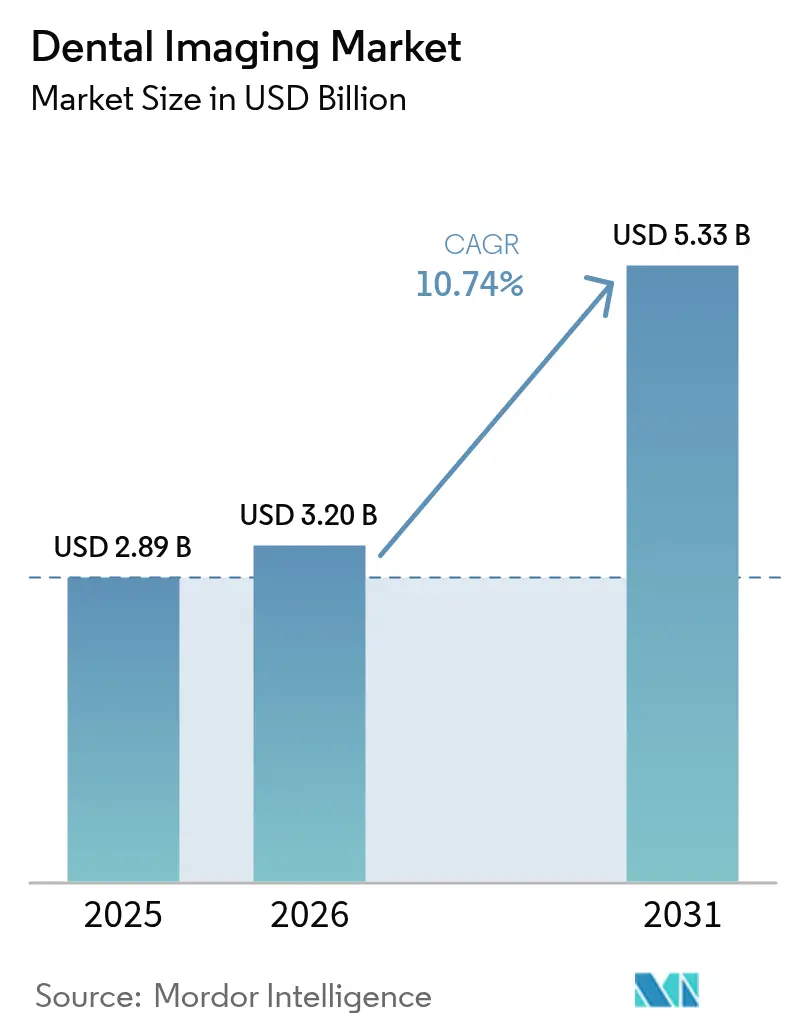

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 5.33 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Imaging Market Analysis by Mordor Intelligence

The Dental Imaging Market size is expected to increase from USD 2.89 billion in 2025 to USD 3.20 billion in 2026 and reach USD 5.33 billion by 2031, growing at a CAGR of 10.74% over 2026-2031.

This growth signals the shift from episodic care toward preventive models in which clinicians rely on data-rich images and algorithmic support to intervene earlier and plan treatments with greater certainty. AI-ready platforms now link imaging devices to practice management systems, creating a single data environment that shortens chair time, raises diagnostic confidence, and strengthens evidence-based case acceptance. Consolidation among dental service organizations (DSOs) enlarges capital budgets and encourages practices to standardize on advanced imaging suites, while regulators reduce approval cycle times for new hardware and software, which keeps the product pipeline active. An aging population frames the commercial opportunity: the 65+ cohort presents more complex clinical profiles that demand volumetric views of bone, nerve, and sinus anatomy at the moment of diagnosis, placing three-dimensional modalities at the center of practice investment strategies.

Key Report Takeaways

- By imaging technology, 2-D X-ray systems held 48.10% of the dental imaging market share in 2025, while 3-D X-ray/CBCT is advancing at a 10.76% CAGR through 2031.

- By application, Diagnostics & Detection accounted for 41.05% of the dental imaging market size in 2025; Implant Planning is expanding at an 11.08% CAGR to 2031.

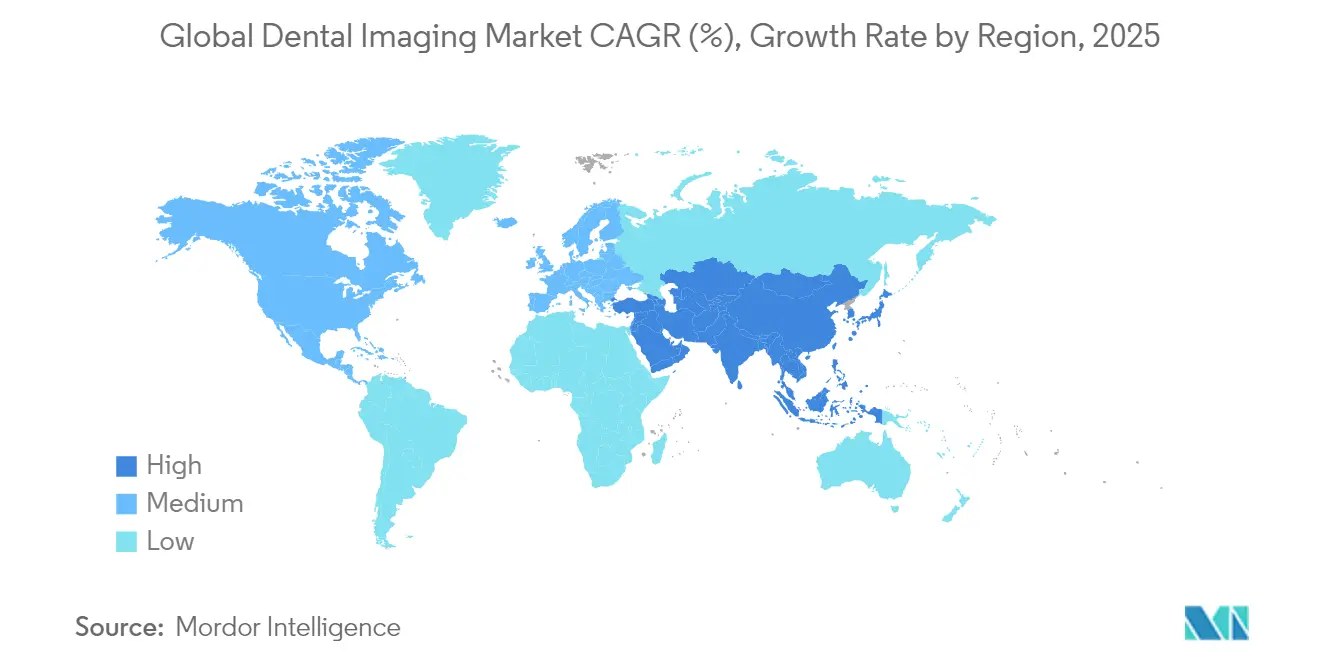

- By geography, North America led with 33.20% revenue share in 2025, whereas Asia-Pacific is forecast to grow at 11.67% CAGR, the fastest in the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Integration and Diagnostic Enhancement | +2.8% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Aging Population and Increased Dental Care Demand | +2.1% | Global, particularly pronounced in developed markets | Long term (≥ 4 years) |

| Digital Transformation of Dental Practices | +1.9% | Global, with Asia-Pacific showing rapid acceleration | Short term (≤ 2 years) |

| Growing Implant Market and Complex Procedures | +1.6% | North America & Europe primarily, expanding to Asia-Pacific | Medium term (2-4 years) |

| Regulatory Approvals and Standardization | +1.4% | North America & Europe primarily, expanding globally | Medium term (2-4 years) |

| Teledentistry and Remote Diagnostics Growth | +1.1% | Global, with higher adoption in rural and underserved areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI Integration Drives Diagnostic Precision Revolution

FDA-cleared software such as VideaHealth’s[1]Source: VideaHealth, “FDA Clearance Announcement,” videa.ai pathology detection engine raises clinically actionable findings by 26%, replacing subjective visual inspection with calibrated algorithmic review. Bigger data pools improve caries and lesion detection on panoramic radiographs where bone-loss patterns appear faint to the human eye. Consistent interpretation levels the quality gap between high-volume DSOs and small offices, creating a reliable baseline for remote consultations in teledentistry settings. Cloud hosting further scales this capability because image files, annotations, and audit trails reside in a single workspace that multiple clinicians can access without local servers. As reimbursement models favor early intervention, decision makers see AI-ready imaging as essential infrastructure rather than discretionary capital.

Aging Demographics Fuel Implant Planning Sophistication

The proportion of patients aged 65 and above is rising steadily, and with it comes multi-site edentulism, decreased bone density, and proximity of critical anatomical landmarks. CBCT offers voxel-level visualization that guides implant trajectory, reduces surgical surprises, and eliminates the 7% abort rate observed with 2-D orthopantomography. Cross-disciplinary teams—including periodontists, prosthodontists, and oral surgeons—now treat older adults in integrated care pathways in which CBCT becomes the common language. The sustained 11.31% CAGR for Implant Planning applications reflects the compound effect of demographic pressure and surgeon preference for radiation-efficient, high-resolution views that shorten chair time and healing cycles.

Digital Transformation of Dental Practices

Cloud-native scanners such as Primescan 2 remove tethering cables[2]Source: Dentsply Sirona, “Primescan 2 Product Launch,” dentsplysirona.com, automatically upload STL files, and feed data directly into AI planning modules, closing the loop between diagnosis, treatment design, and patient communication during a single visit. Practices using integrated platforms report shorter appointment sequences, higher treatment acceptance, and measurable throughput gains. Digitally prepared practices further leverage intraoral cameras, radiographs, and lab data within a common viewer so that the patient sees a single 3-D model annotated with treatment milestones. This end-to-end workflow raises competitive pressure on analogue clinics, accelerating the migration cycle already underway.

Regulatory Standardization Enables Global Market Expansion

With the FDA recognizing IEC 61223-3-7 testing protocols for dental CBCT, manufacturers can validate safety and performance once for multiple jurisdictions, cutting redundant testing expense and time. The EU-MDR pathway mirrors this clarity, as seen in DentalMonitoring’s software certification that established a repeatable method for AI algorithm validation. Consistent rule sets improve investor confidence because launch timelines become predictable, thereby easing the entry of mid-sized innovators and encouraging cross-border distribution alliances. Hospitals and group practices also gain, since purchase decisions no longer hinge on region-specific service documentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Equipment Costs and Financial Barriers | -1.8% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Training Requirements and Technology Adoption Challenges | -1.2% | Global, with higher impact in smaller practices | Medium term (2-4 years) |

| Regulatory Compliance Complexity | -0.9% | Global, with varying intensity by region | Medium term (2-4 years) |

| Data Security and Privacy Concerns | -0.7% | Global, with stricter requirements in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Barriers Limit Adoption in Price-Sensitive Segments

A new CBCT platform can exceed USD 180,000, a figure that strains cash flow in solo practices already facing inflation and reimbursement plateaus. The 10% tariff on imported imaging systems introduced in April 2025 adds further expense for buyers dependent on Asian supply chains. In emerging markets currency volatility exacerbates the hurdle because loan repayments rise unpredictably. As a result, clinics delay upgrades, rely on referral imaging centers, or opt for refurbished equipment, creating disparities in service quality between urban hubs and rural catchment areas.

Training Complexity Slows Technology Integration

Digital imaging suites require staff to master acquisition protocols, reconstruction parameters, and AI result interpretation. When turnover occurs, offices must reinvest in onboarding, stretching budgets and disrupting workflow. Evidence from German clinics shows that practices with comprehensive in-house training record higher utilization rates, whereas those without formal programs leave advanced functions untouched. Smaller offices often lack protected training hours, leading to partial adoption. The cascading effect is lower return on equipment investment, a slower learning curve for diagnostic AI, and uneven patient experiences across the same franchise network

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cone-Beam Systems Challenge Intraoral Dominance

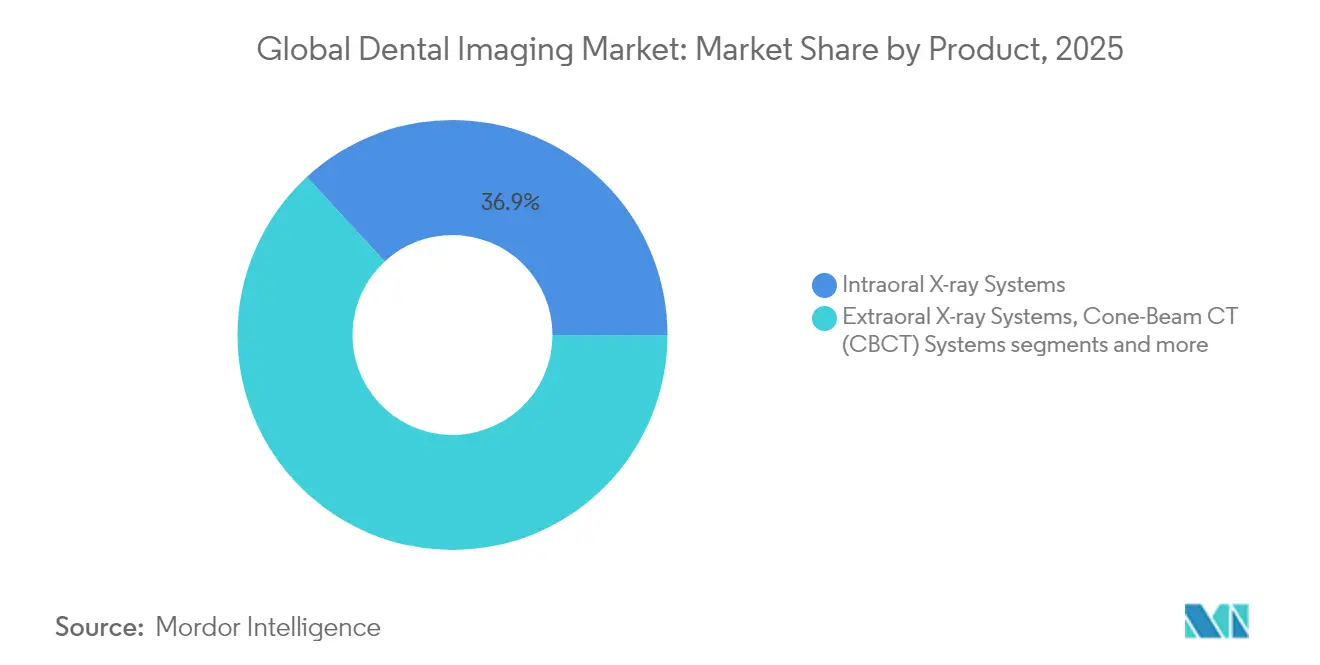

Intraoral X-ray systems captured 36.85% of the dental imaging market share in 2025, underscoring their entrenched role in routine diagnostics across general and specialty practices. Even so, cone-beam CT (CBCT) platforms represent the clear growth engine as clinicians prioritize three-dimensional visualization for implant, endodontic, and airway assessments U.S. Food and Drug Administration. Extraoral panoramic units retain relevance in orthodontic and trauma evaluations, while AI overlays on these images—such as VideaHealth’s FDA-cleared software that lifts treatment opportunity identification by 26%—extend the clinical value of legacy systems Denti.AI. The bifurcation now evident separates volume-driven intraoral screening from value-driven CBCT diagnostics, with the latter segment justifying higher capital outlays through measurably better surgical outcomes.

Competitive activity maps to this transition. Traditional intraoral platforms migrate toward direct digital sensors, cordless handpieces, and lightweight control modules that streamline workflow integration and reduce retake rates. CBCT manufacturers double down on dose-reduction algorithms, faster reconstruction times, and small-footprint designs that suit space-constrained operatories. Component suppliers such as Vieworks reported a 28.9% year-on-year jump in detector sales dedicated to cone-beam applications, signaling robust back-end demand that underpins system-level growth Vieworks. Emerging categories including intraoral scanners and optical imaging heads gain ground through CAD/CAM convergence, while early-stage MRI-based dental platforms from Dentsply Sirona and Siemens Healthineers create future pathways for radiation-free soft-tissue imaging MDPI. The product trajectory therefore points toward premiumized, all-in-one suites that connect acquisition hardware, cloud analytics, and chairside visualization inside a single diagnostic ecosystem.

By Imaging Technology: 3D Innovation Challenges 2D Dominance

2-D X-ray systems delivered 48.10% of the dental imaging market share in 2025, sustaining growth among practices that need low-cost diagnostic screening. Their familiar workflow, minimal radiation exposure, and straightforward reimbursement codes preserve relevance in routine caries detection and orthodontic progress checks. However, the 3-D X-ray/CBCT segment is expanding at 10.76% CAGR because volumetric imaging supports implant planning, pathology mapping, and airway assessments with precise spatial references. Within this shift, the dental imaging market size for 3-D devices is expected to double by 2031 as DSOs choose a single high-throughput unit capable of addressing multiple procedures, reducing the need for separate panoramic and cephalometric hardware.

Optical and digital impression systems now register the quickest unit sales growth, benefitting from chairside CAD/CAM integration and patient preference for non-invasive techniques. Because intraoral scanners feed data directly into laboratory workflows, they enhance prosthetic fit and cut remake rates, positioning them as viable substitutes for conventional impressions in crown, bridge, and clear aligner workflows. MRI and ultrasound are niche but rising modalities: the first dental-dedicated MRI from Dentsply Sirona and Siemens Healthineers introduces soft-tissue visualization without ionizing radiation, whereas point-of-care ultrasound is emerging for real-time assessment of peri-apical lesions and temporomandibular joint disorders. These modalities broaden the addressable field by reaching patients contraindicated for radiography, further diversifying the dental imaging market.

By Application: Implant Planning Drives Diagnostic Evolution

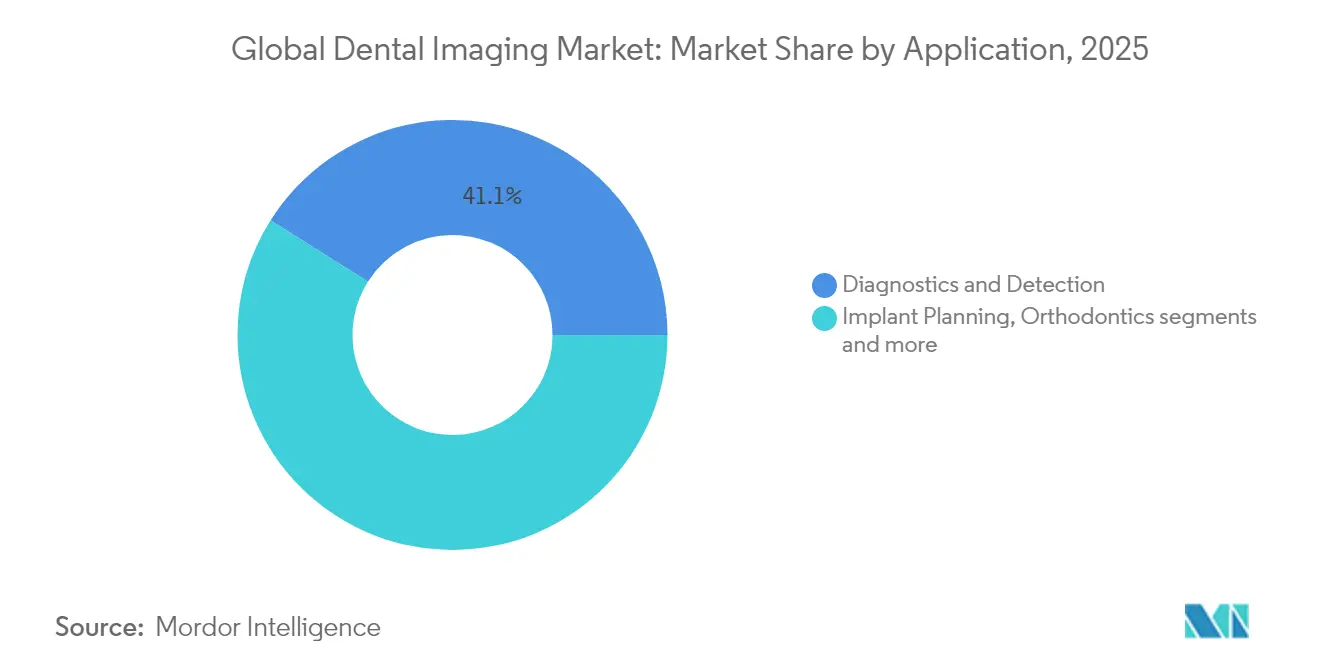

Diagnostics & Detection remained the largest application with 41.05% share of the dental imaging market size in 2025, underlining the keystone role of imaging in every patient examination. General practitioners use bitewing radiographs for caries surveillance and panoramic views to monitor eruption patterns, positioning imaging as a non-negotiable first step in the care pathway. The next phase of value creation, though, lies in Implant Planning, which is growing at 11.08% CAGR through 2031. Three-dimensional visualization informs nerve mapping, sinus lift assessment, and bone density measurement, all of which raise the predictability of surgical outcomes and reduce chairside modifications.

AI integration accelerates this adoption curve by automating nerve canal tracing and proposing implant trajectories based on cumulative data sets. Orthodontics also benefits as 3-D records enable simulation of tooth movement and airway volume assessments that guide interceptive care. Endodontics leverages high-resolution scans to locate accessory canals, while oral and maxillofacial surgery relies on CBCT for fracture planning and temporomandibular joint evaluation. Each incremental capability increases utilization frequency, broadening the revenue base and embedding imaging deeper into multi-specialty care.

Geography Analysis

North America held 33.20% of 2025 revenue, benefiting from clear insurance codes, accelerated FDA approvals, and a consolidation wave that channels capital toward advanced diagnostic suites. United States DSOs deploy AI algorithms across hundreds of sites, achieving uniform image quality and centralized analytics that inform preventive outreach programs. Canada follows a similar pattern as network operators integrate cloud-based viewers to bridge regional gaps in specialist access. Tariff-driven price hikes on imported equipment create short-term budgeting friction, yet robust reimbursement offsets the hurdle for most urban clinics. The region’s mature regulatory environment reduces uncertainty, which encourages manufacturers to debut flagship platforms in North America before global rollout.

Asia-Pacific is expanding at 11.67% CAGR through 2031 as governments invest in digital health, fiber connectivity, and AI research. China’s hospital reform plan prioritizes imaging upgrades, and public tenders now specify CBCT in maxillofacial departments. Japan’s super-aging society demands low-dose volumetric scans for implant planning and geriatric pathology review, while South Korea’s technology-savvy clinics embrace cloud workflows that sync chairside scans with in-house milling. India and Southeast Asia represent high-volume, mid-income prospects where lower equipment costs and financing programs spur first-time adoption. Regional suppliers partner with local distributors to navigate import duties and after-sales service, reinforcing the long-term trajectory of the dental imaging market in Asia-Pacific. Europe posts steady growth, supported by EU-MDR harmonization that streamlines procurement across borders. Germany, France, and the United Kingdom lead adoption through well-funded public systems and private insurance coverage for digital diagnostics. Southern and Eastern Europe catch up as economic recovery funds modernize hospital infrastructure and subsidize small-practice upgrades. Pan-European DSOs scale AI pilots region-wide, contributing to a shared evidence base that accelerates algorithm refinement. Latin America, the Middle East, and Africa remain emerging fronts where urban private clinics purchase advanced systems, while public sectors adopt gradual refurbishment strategies. As manufacturing efficiency rises and refurbished units circulate, entry-level price points drop, opening new addressable volumes in these markets.

Competitive Landscape

Global competition is balanced between diversified incumbents and AI-native entrants that specialize in software-driven diagnostics. Dentsply Sirona, Planmeca, and Carestream Dental maintain broad portfolios covering intraoral, extraoral, and chairside systems, which secures long-term service contracts and cross-selling opportunities. Their cloud platforms integrate scheduling, scanning, and laboratory workflows, embedding customers in proprietary ecosystems that lower churn. Planmeca’s partnership with myOrthos illustrates the strategy: supplying 3-D units to a national orthodontic network cements repeat consumable orders and strengthens brand loyalty.

Emerging vendors, led by Pearl, VideaHealth, and Adravision, differentiate through FDA-cleared algorithms that detect pathologies in seconds and deliver explainable outputs. Venture capital injection, exemplified by Pearl’s USD 58 million Series B, accelerates research cycles and supports global commercialization teams that co-sell software modules with hardware partners. These firms target pain points such as missed early-stage caries or inconsistent periodontal readings, demonstrating quantifiable treatment gains that resonate with evidence-driven practitioners. Hardware makers now court these software specialists to bundle AI licenses at the point of sale, creating hybrid value propositions that blur traditional boundaries between equipment and analytics.

Competitive intensity is rising yet remains moderate because switching costs, proprietary data sets, and regulatory clearances act as natural barriers. Incumbents invest in secure cloud storage and end-to-end encryption to comply with evolving data protection rules, further locking in enterprise clients. Meanwhile, disruptors exploit unserved niches such as MRI-based dental imaging, teledentistry diagnostics, and low-dose pediatric scanning. Supply chain resilience becomes a new battleground after 2025 tariff shifts, prompting manufacturers to localize assembly or dual-source key components. Strategic alliances, technology licensing, and selective acquisitions are expected to shape the next phase of consolidation in the dental imaging market.

Dental Imaging Industry Leaders

Acteon Group

Midmark Corporation

Apteryx Imaging

Flow Dental

Carestream Health (Carestream Dental LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nano-X Imaging’s Nanox.ARC Imaging System received CE mark certification, enabling low-dose 3-D tomosynthesis deployment in European clinics

- February 2025: Dentalcorp Holdings partnered with VideaHealth to roll out AI pathology detection across its practice network.

- September 2024: Dentsply Sirona launched Primescan 2, the first cloud-native wireless intraoral scanner powered by DS Core

Global Dental Imaging Market Report Scope

As per the scope of the report, dental imaging is a process in which high-quality images are created for the diagnosis of dental problems by using imaging equipment. The dental imaging market is segmented by technology (dental cone beam computed tomography (CBCT), general x-ray imaging systems, intraoral cameras, and dental optic imaging), application (cosmetic applications and diagnostic applications), method (extraoral imaging and intraoral imaging), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the market sizes and forecasts in terms of value (USD million) for the above segments.

| Intraoral X-ray Systems |

| Extraoral X-ray Systems |

| Cone-Beam CT (CBCT) Systems |

| Imaging Software |

| 2-D X-ray |

| 3-D X-ray / CBCT |

| Optical / Digital Impression |

| Others (MRI, Ultrasound) |

| Diagnostics & Detection |

| Implant Planning |

| Orthodontics |

| Endodontics |

| Oral & Maxillofacial Surgery |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Intraoral X-ray Systems | |

| Extraoral X-ray Systems | ||

| Cone-Beam CT (CBCT) Systems | ||

| Imaging Software | ||

| By Imaging Technology | 2-D X-ray | |

| 3-D X-ray / CBCT | ||

| Optical / Digital Impression | ||

| Others (MRI, Ultrasound) | ||

| By Application | Diagnostics & Detection | |

| Implant Planning | ||

| Orthodontics | ||

| Endodontics | ||

| Oral & Maxillofacial Surgery | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the dental imaging market in 2031?

The market is expected to reach USD 5.33 billion by 2031 based on a 10.74% CAGR.

Which imaging technology is growing fastest?

3-D X-ray/CBCT systems are expanding at 10.76% CAGR due to their role in implant planning and comprehensive diagnostics.

Why is Asia-Pacific the fastest-growing region?

Investment in digital health infrastructure, a rising middle class, and supportive government programs drive an 11.67% CAGR in Asia-Pacific.

How does AI improve diagnostic accuracy?

FDA-cleared AI solutions increase pathology detection rates by 26%, enabling earlier and more consistent treatment recommendations.

Page last updated on: