Advanced Dental Digital And Robotic Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

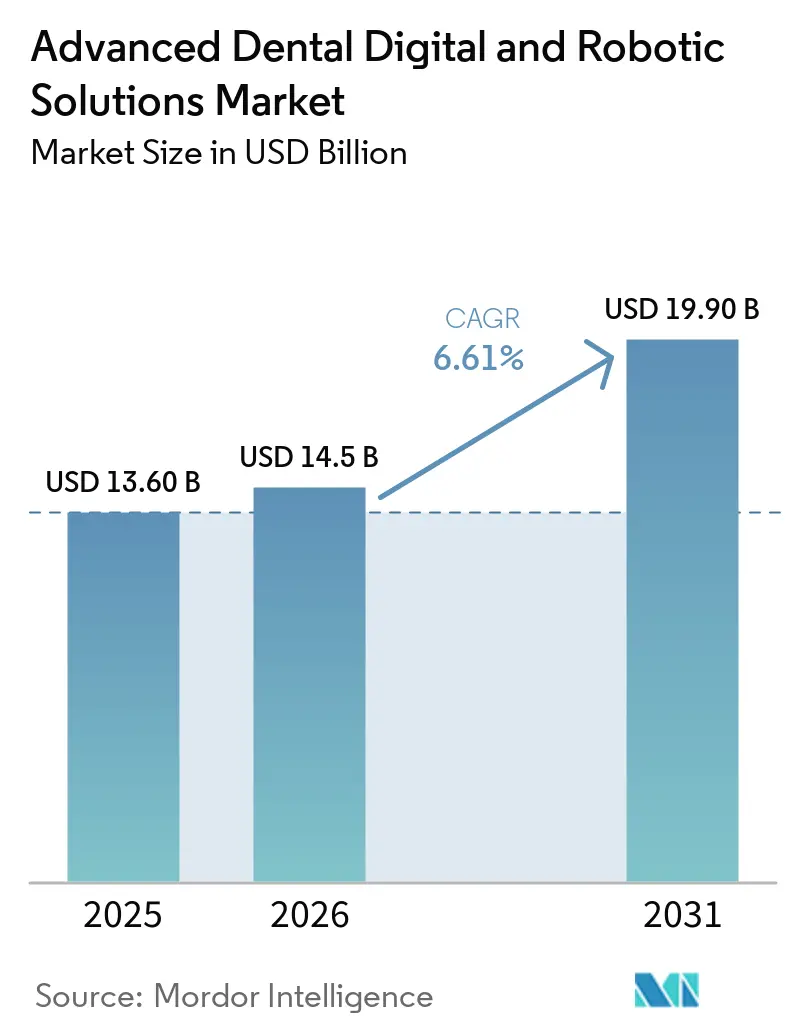

| Market Size (2026) | USD 14.5 Billion |

| Market Size (2031) | USD 19.90 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Dental Digital And Robotic Solutions Market Analysis by Mordor Intelligence

The Advanced Dental Digital And Robotic Solutions Market size is projected to expand from USD 13.60 billion in 2025 and USD 14.5 billion in 2026 to USD 19.90 billion by 2031, registering a CAGR of 6.61% between 2026 to 2031.

Demand is pivoting toward revenue-generating chairside systems as Dental Service Organizations (DSOs) accelerate bulk technology roll-outs, while independent practices confront higher financing costs that extend equipment payback horizons. Regulatory bodies are clearing artificial-intelligence (AI) platforms at an unprecedented pace 12 U.S. Food and Drug Administration (FDA) authorizations arrived in 2024 alone, yet reimbursement structures still tie digital crowns to analog fee schedules, muting short-term profit gains. Subtractive milling retains a large installed base, but additive multi-material printers are expanding fastest because they compress traditional five-visit denture protocols into two appointments, enhancing chair utilization. North America continues to command the largest regional share, whereas Asia-Pacific is scaling from a lower adoption baseline and benefits from faster National Medical Products Administration (NMPA) review times that attract first-to-market launches.

Key Report Takeaways

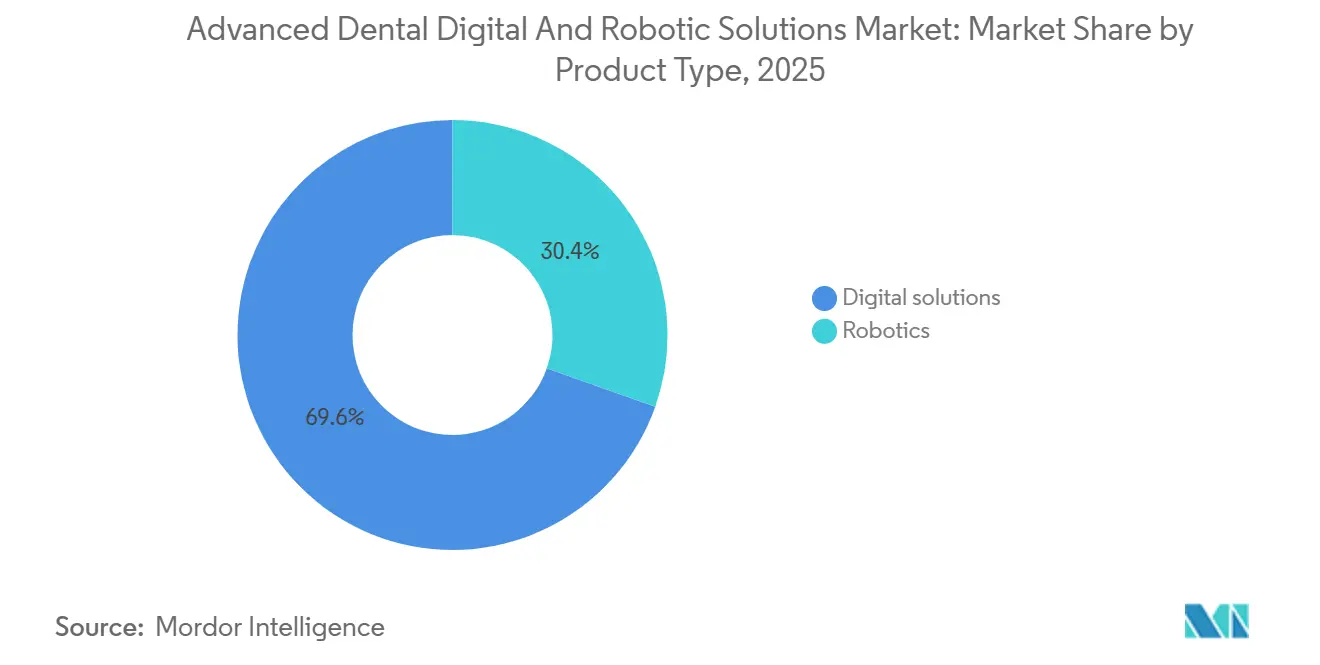

- By product type, Digital solutions led with 69.56% of the Advanced Dental Digital and Robotic Solutions market share in 2025, while robotics are forecast to grow at a 7.32% CAGR to 2031

- By technology, subtractive CAD/CAM commanded 43.10% of the Advanced Dental Digital and Robotic Solutions market size in 2025; additive 3-D printing is projected to expand at 6.90% CAGR between 2026 and 2031

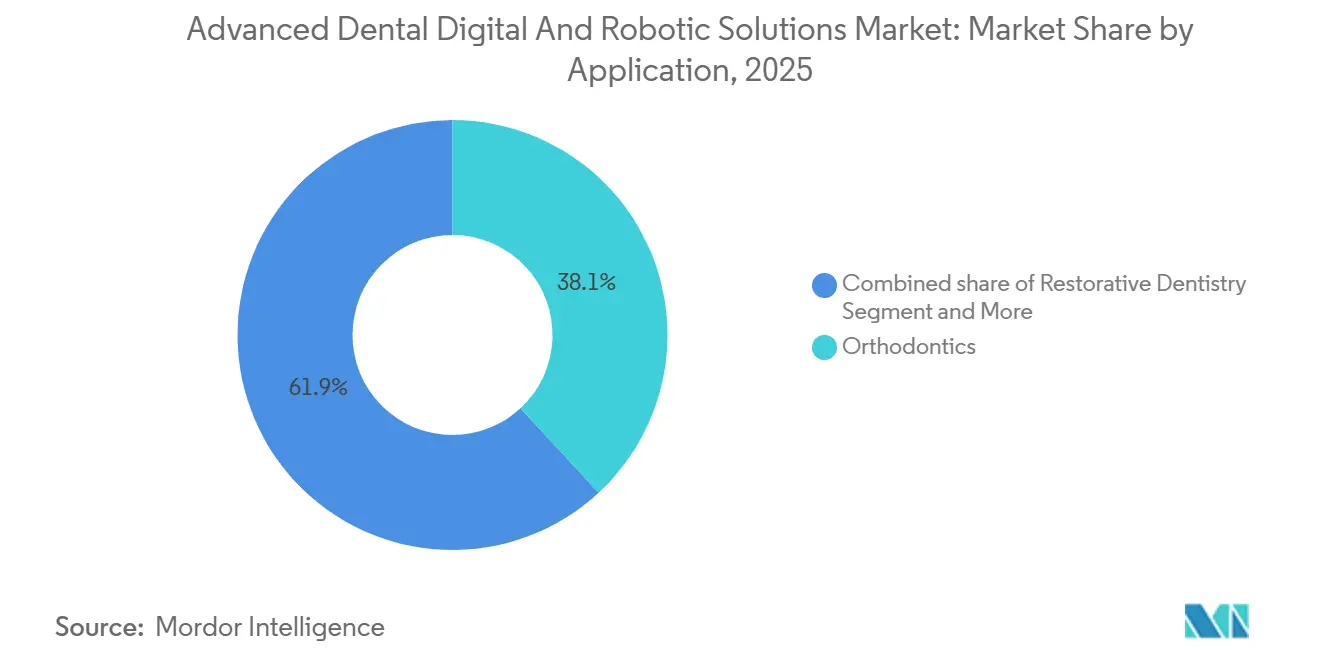

- By application, orthodontics accounted for 38.10% share of the Advanced Dental Digital and Robotic Solutions market size in 2025, whereas prosthodontics is advancing at a 6.69% CAGR through 2031

- By end user, dental clinics captured 36.40% of the Advanced Dental Digital and Robotic Solutions market share in 2025, and dental laboratories will post the highest 6.95% CAGR to 2031

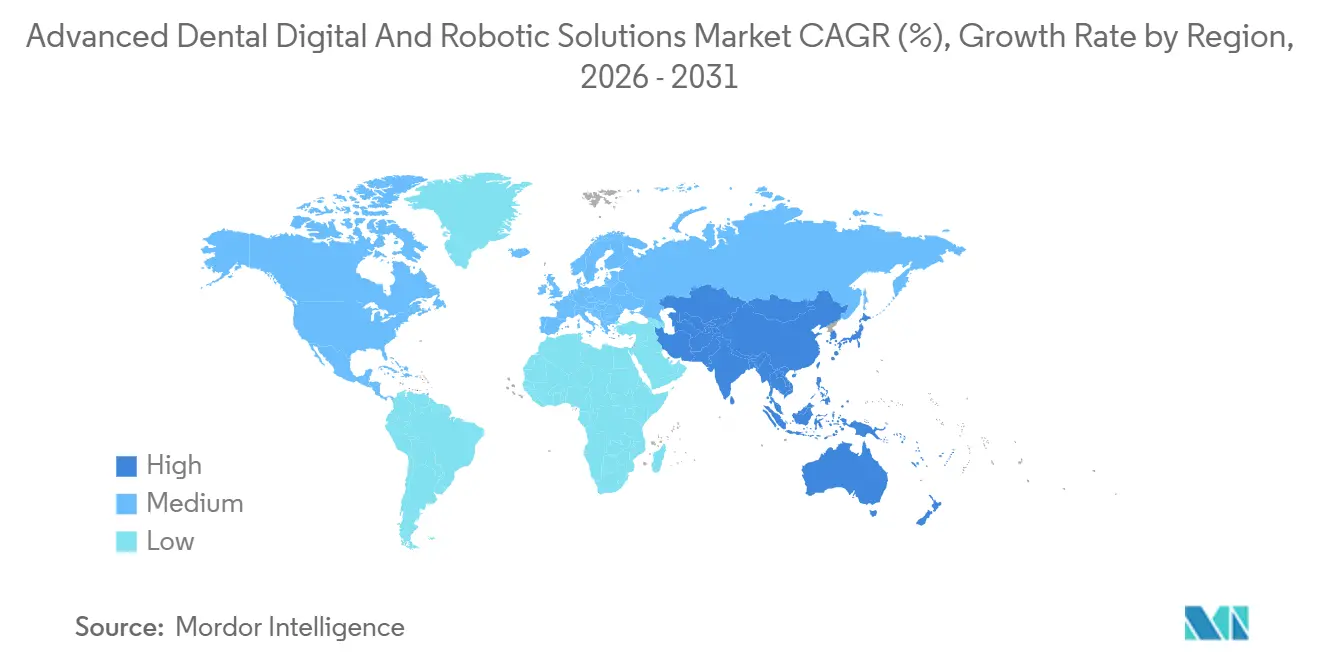

- By geography, North America commanded a 34.80% share of the revenue in 2025, while Asia-Pacific is expected to record a 6.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Dental Digital And Robotic Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid chairside workflow adoption | +1.2% | North America & Europe | Short term (≤ 2 years) |

| Cosmetic dentistry demand surge | +0.9% | Global | Medium term (2-4 years) |

| Reimbursement expansion for digital prosthetics | +0.7% | North America & EU markets | Medium term (2-4 years) |

| Cloud-integrated practice platforms | +0.8% | Global | Short term (≤ 2 years) |

| AI-driven real-time error-correction twins | +1.0% | North America & APAC | Medium term (2-4 years) |

| VC inflows into autonomous robotic systems | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Chairside Workflow Adoption

Chairside CAD/CAM cuts prosthodontic turnarounds from six visits to as few as two, allowing practices to reclaim lab margins and schedule two restorative cases in the time once reserved for one. DSOs exploit bulk discounts. Aspen Dental secured price reductions on a single-platform rollout across 1,000 offices, while assistants earning USD 18-25 per hour now handle milling tasks once outsourced at twice that labor cost [1]American Dental Association, “Economic Outlook & Practice Revenue,” ada.org. Rising lease rates stretch payback periods to roughly 30 months for sub-USD 1 million practices, but ISO 6872 materials standardization lowers switching barriers by guaranteeing cross-platform compatibility.

Cosmetic Dentistry Demand Surge

Video-centric work dynamics push smile aesthetics into mainstream expectations; 68% of 2024 iTero scans originated in cosmetic consults, up 12 points from 2022 [2]Align Technology, “Investor Presentation 2024,” aligntech.com. Digital smile-design software boosts conversion to treatment by presenting live overlays that close around half of cases compared with one-third for verbal plans. Younger clinicians fuel technology uptake, scanner penetration is increasing among dentists under 40, and chairside 3-D printers make try-in veneers while patients wait, trimming decision cycles to days instead of weeks. Conversion remains metro-centric; coastal U.S. markets derive 40% of private revenue from cosmetic procedures versus 15-20% in rural regions, signaling ample upside as urbanization proceeds.

Reimbursement Expansion for Digital Prosthetics

Six U.S. insurers introduced “digital efficiency” codes in 2024 that pay 5-10% premiums for same-day crowns, nudging midsize practices that place 300+ units annually to justify equipment buys. Medicare’s continued dental exclusion caps senior uptake, while Medicaid’s patchwork adult benefits spur state-by-state variability. Japan’s coverage of additional CAD/CAM tooth positions accelerated its digital crown share to 25-30% by 2025, though fee ceilings still inhibit multilayer zirconia upgrades. Europe remains fragmented; Germany mandates 40-50% co-pays on digital options, and France funds only analog impressions, forcing providers to upsell privately.

Cloud-Integrated Practice Platforms

Straumann’s AXS ecosystem unites scanners, management software, and lab ordering into one cloud layer, cutting implant turnaround to 14 days. Pacific Dental Services connected 850 offices in 2025, using dashboards that redirect patients from under-performing sites and optimize inventory. Yet 387 dental data breaches in 2024 drove 25-40% insurance-premium jumps for locations lacking multi-factor authentication. Proprietary application-programming interfaces (APIs) still slow multi-vendor rollouts by up to six months and add USD 20,000-50,000 in consulting fees for DSOs juggling mixed stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront equipment costs | -0.8% | Global | Short term (≤ 2 years) |

| Complex multi-jurisdiction regulatory approvals | -0.5% | Global | Medium term (2-4 years) |

| Proprietary file-format lock-ins are hindering interoperability | -0.4% | Global | Medium term (2-4 years) |

| Escalating cloud-data-breach liability premiums | -0.3% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment Costs

Fully digital workflows can require USD 150,000-250,000, equal to 15-25% of median U.S. practice revenue, and financing now runs 5.5-7% versus sub-3% pre-2022. Solos rarely meet the 30-50 extra crowns a month needed for breakeven, while DSOs amortize kits over multi-office networks, reinforcing consolidation. The gap in India is starker; a USD 30,000 scanner exceeds two years of profit for a single-chair clinic.

Complex Multi-Jurisdictional Regulatory Approvals

Europe’s Medical Device Regulation (MDR 2017/745) stretches CE-Mark timelines to 18 months, inflating costs by USD 2-5 million per product [3]European Commission, “Medical Device Regulation Implementation,” ec.europa.eu. Start-ups must earmark up to half of Series A capital for multi-region filings, delaying commercialization and dissuading investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Solutions Dominate, Robotics Niche Expands

Digital solutions accounted for 69.56% of product revenue in 2025, underscoring their central role in imaging, fabrication, software, and practice-management tasks. Practices are extending cone-beam CT replacement cycles from 7 years to nearly a decade and shifting capital toward CAD/CAM mills and 3-D printers that generate steady consumable sales, which make up 30-40% of a system's lifetime value. Global scanner installations passed 200,000 units in 2025, yet lower-priced Asian models priced at USD 15,000-20,000 are squeezing margins and nudging established brands to emphasize subscription software and AI diagnostics. Cloud-based practice software, now replacing local licenses, lifts recurring revenue but leaves offices exposed to price hikes; Dentrix Ascend raised fees 18% in 2024 and pushed 12% of users to consider open-source tools. In laboratories, multi-material printers enable single-pass dentures with rigid bases and soft liners, eliminating majority of milling and cutting material waste since the CE-marked launch of TrueDent resin in January 2025.

Robotics accounted for a modest share of 2025 sales but is on track for a 7.32% CAGR through 2031, as surgeons who place 300 or more implants each year seek higher accuracy and lower liability. The Yomi system surpassed 1,000 installs and 100,000 procedures by late 2024, delivering 0.7 mm mean linear deviation and reducing bone-graft needs compared with freehand methods. X-Guide, with 15,000 units placed by 2025, uses optical tracking to steer handpieces while letting clinicians move freely an approach some prefer to fully robotic arms. Cost remains the main hurdle: a USD 150,000-200,000 robot must support at least 200 implant cases a year to pay for itself, limiting uptake to the busiest 20% of implant dentists. Fully autonomous systems will need Class III premarket approval, a three-to-five-year process that could delay launches until near the end of the decade. Adoption is clustered in North America and Western Europe, which held majority of 2025 unit sales, while Asia-Pacific held modest share because most practices perform fewer implants and receive limited reimbursement for technology-assisted surgery.

By Technology: Additive Printing Gains, Subtractive Still Leads

Subtractive CAD/CAM held 43.10% of the Advanced Dental Digital and Robotic Solutions market size in 2025 on the strength of a 200,000-plus installed base and wide material ecosystems. Additive printers, however, are expected to grow through the forecasted period as single-print dentures combine rigid bases and soft liners, a feat milling cannot match. Laboratory adoption rose significantly in 2025, signaling a tipping point as certified permanent materials proliferate.

Cloud Software as a Service (SaaS) rides DSO consolidation, expanding 7.2% annually by linking clinical, operational, and financial data streams. AI/ML still records a modest share of revenue but scales quickly; insurers increasingly require algorithm-validated radiographs for high-cost approvals. Blockchain record-keeping has languished, serving fewer than 500 worldwide practices in 2025 due to lagging standards and regulatory clarity.

By Application: Prosthodontics Accelerates Amid Aging Demographics

Orthodontics accounted for 38.10% of 2025 revenue, but prosthodontics leads growth with a 6.69% CAGR through 2031, as aging populations in Japan and Germany demand implant-supported restorations. Digital denture workflows now account for a significant share of new U.S. cases, and robot-guided implantology broadens eligibility by reducing surgical deviations. Restorative dentistry is expanding at a rapid pace, while endodontics and periodontics are deploying printed guides that have significantly reduced healing times in recent trials.

By End User: Laboratories Automate Amid Workforce Attrition

Dental clinics retained 36.40% of 2025 revenue, though laboratories will log the most robust 6.95% CAGR thanks to lights-out milling, which slashes labor costs to USD 12-18 per crown. The top 10 U.S. labs significantly increased their share in 2025, using multi-axis mills and AI design suites that were unaffordable for smaller peers. Hospitals lag given competing capital priorities, while DSOs drive a significant portion of equipment purchases despite owning only small number of practices, underscoring their outsized influence.

Geography Analysis

North America controlled 34.80% of 2025 revenue and will grow at a notable CAGR through 2031 as hardware saturation shifts wallet share toward software, AI analytics, and security upgrades. DSOs such as Heartland Dental, Aspen Dental, and Pacific Dental Services already funnel 35-40% of equipment orders, parlaying 25-35% vendor discounts into a competitive edge. Twelve FDA AI clearances in 2024 codified algorithms into standard-of-care workflows, while dental tourism draws 1.5 million U.S. patients to Mexico for 40-60% cheaper prosthodontics annually.

Asia-Pacific will post the highest CAGR of 6.80% because China’s CNY 40 billion (USD 5.6 billion) equipment market grows each year, and NMPA approvals often conclude within 12 months, a 6-month speed advantage over FDA pathways. Local scanner vendors price units 30-40% below Western equivalents, stimulating adoption in tier-2 cities where clinics leapfrog analog workflows. India’s market stands at roughly USD 450 million and grows 12-14% annually as per-capita spend climbs toward USD 10. Japan’s expanded CAD/CAM reimbursement pushes digital crown penetration, though fee caps still sandbag premium zirconia adoption.

Europe owns significant share of revenue but have a stable CAGR because MDR backlogs extend CE approvals to 18 months and add millions in compliance costs. Germany leads at roughly USD 2.2 billion but faces a rapidly aging technician workforce that accelerates lab automation. The U.K.’s National Health Service ceiling of GBP 282 on complex treatments funnels patients into private cosmetic channels. France and Italy lag with digital uptake, held back by older practitioner demographics. South America and the Middle East & Africa both expanding as dental tourism and infrastructure projects gain momentum.

Competitive Landscape

The top five suppliers, Dentsply Sirona, Align Technology, Envista, Straumann, and 3Shape, together controlled a majority share of the Advanced Dental Digital and Robotic Solutions market in 2025, with no single brand holding major share, because the field spans imaging, CAD/CAM, software, and robotics. Platform integrators aim for seamless chairside-to-lab data flows, but point-solution specialists thrive by addressing niche pain points like AI diagnostics or navigation robotics. Dentsply Sirona’s 2024 Connected Technology revenue fell after shuttering its Byte aligner line and booking USD 1 billion in impairments, underscoring risks of consumer-facing diversification.

Asian entrants Medit and Shining 3D price scanners up to 40% cheaper than Western incumbents, eroding margins but lagging in AI toolboxes by roughly two years. Patent filings pivot from hardware to software; Align logged 42 AI treatment-planning patents in 2024, while Neocis added eight robotic navigation patents. Interoperability gaps remain the largest white-space opportunity because proprietary formats inflate user lifetime costs 15-20%, and cybersecurity platforms address the 18 million dental-record exposures tallied in 2024.

DSO standardization magnifies vendor leverage: Heartland Dental’s USD 100 million digital investment across 1,800 sites sets platform expectations for suppliers jockeying for long-term deals. Laboratories, meanwhile, replace lost technicians with automated mills and AI design suites, driving tool manufacturers to integrate robotics and multi-material printing. The resulting landscape remains moderately consolidated yet dynamic as mid-tier innovators exploit gaps in interoperability, AI ease-of-use, and cyber-risk mitigation.

Advanced Dental Digital And Robotic Solutions Industry Leaders

Dentsply Sirona

Envista Holdings Corporation

Straumann Group

3Shape

Align Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SprintRay Inc. announced the launch of the SprintRay Midas Platform, a chairside digital dentistry solution that enables clinics to produce permanent dental crowns on the same day, using a new "Midas" 3D printer and proprietary resins.

- October 2025: Straumann introduced Falcon, a compact dynamic-navigation system compatible with smart glasses for edentulous cases in EMEA markets.

- March 2025: Straumann completed the European rollout of AXS, its open cloud platform linking AI planning and 3-D printing workflows.

Global Advanced Dental Digital And Robotic Solutions Market Report Scope

As per the scope of the report, advanced dental digital and robotic solutions represent a rapidly evolving sector in healthcare that integrates cutting-edge technology to enhance diagnosis, treatment planning, and patient care.

The Advanced Dental Digital and Robotic Solutions Market is segmented by product type, technology, application, end users, and geography. By product type, it is segmented into digital solutions and robotics. By technology, the market is segmented into subtractive, CAD/CAM, additive 3-D printing, cloud SaaS, AI/machine learning, robotic automation, and blockchain data management. By application, the market is segmented into restorative, dentistry, orthodontics, implantology, prosthodontics, endodontics, periodontics, and oral surgery. By end-users, the segmentation includes dental clinics, dental laboratories, hospitals, academic & research institutes, and dental service organizations (DSOs). Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Digital solutions | Dental imaging systems |

| CAD/CAM systems | |

| 3D printing solutions | |

| Dental practice management software | |

| Other digital solutions | |

| Robotics |

| Subtractive CAD/CAM |

| Additive 3-D Printing |

| Cloud SaaS |

| AI / Machine Learning |

| Robotic Automation |

| Blockchain Data Management |

| Restorative Dentistry |

| Orthodontics |

| Implantology |

| Prosthodontics |

| Endodontics |

| Periodontics |

| Oral Surgery |

| Dental Clinics |

| Dental Laboratories |

| Hospitals |

| Academic & Research Institutes |

| Dental Service Organisations (DSOs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Digital solutions | Dental imaging systems |

| CAD/CAM systems | ||

| 3D printing solutions | ||

| Dental practice management software | ||

| Other digital solutions | ||

| Robotics | ||

| By Technology | Subtractive CAD/CAM | |

| Additive 3-D Printing | ||

| Cloud SaaS | ||

| AI / Machine Learning | ||

| Robotic Automation | ||

| Blockchain Data Management | ||

| By Application | Restorative Dentistry | |

| Orthodontics | ||

| Implantology | ||

| Prosthodontics | ||

| Endodontics | ||

| Periodontics | ||

| Oral Surgery | ||

| By End User | Dental Clinics | |

| Dental Laboratories | ||

| Hospitals | ||

| Academic & Research Institutes | ||

| Dental Service Organisations (DSOs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the shift toward same-day dentistry?

Chairside CAD/CAM cuts visits from six to two, saving 40-60% lab fees and boosting clinic throughput by adding a second restorative slot per three-hour block.

How fast is additive 3-D printing growing?

Multi-material printers for dentures and crowns are forecast to expand at 6.90% CAGR, eclipsing the growth of legacy subtractive mills.

Which region leads technology adoption?

North America holds 34.80% of revenue with penetration over 40%, while Asia-Pacific is the fastest riser at 6.80% CAGR from a lower digital baseline

Why are dental laboratories investing heavily?

Automation offsets a 9% technician shortfall and allows one employee to supervise multiple mills, lifting labs’ Advanced Dental Digital and Robotic Solutions market share growth to 6.95% CAGR.

How large will the Advanced Dental Digital And Robotic Solutions Market be by 2031

It is forecast to reach USD 19.90 billion by 2031, rising at a 6.61% CAGR from 2026-2031.

Page last updated on: