Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 264.43 Billion |

| Market Size (2031) | USD 471.88 Billion |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

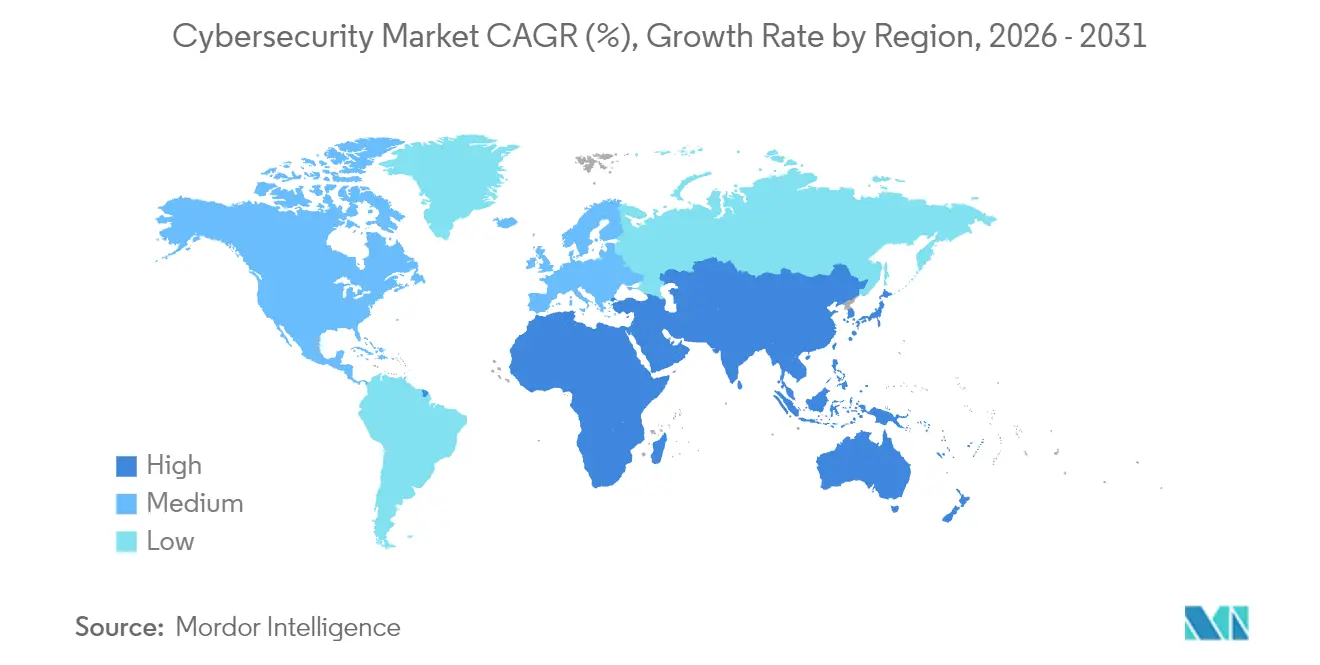

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

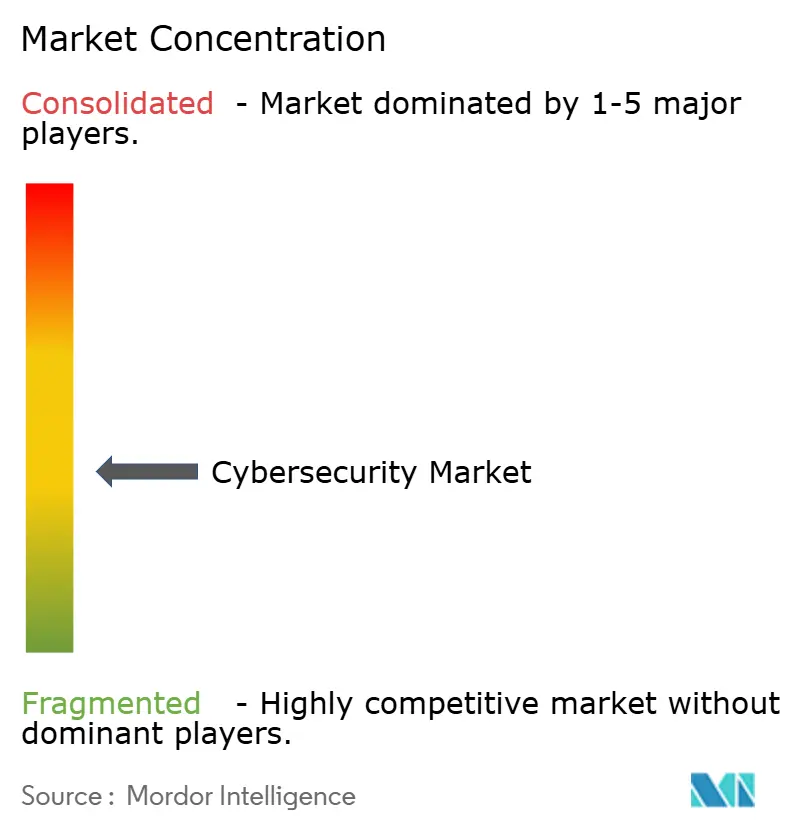

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity Market Analysis by Mordor Intelligence

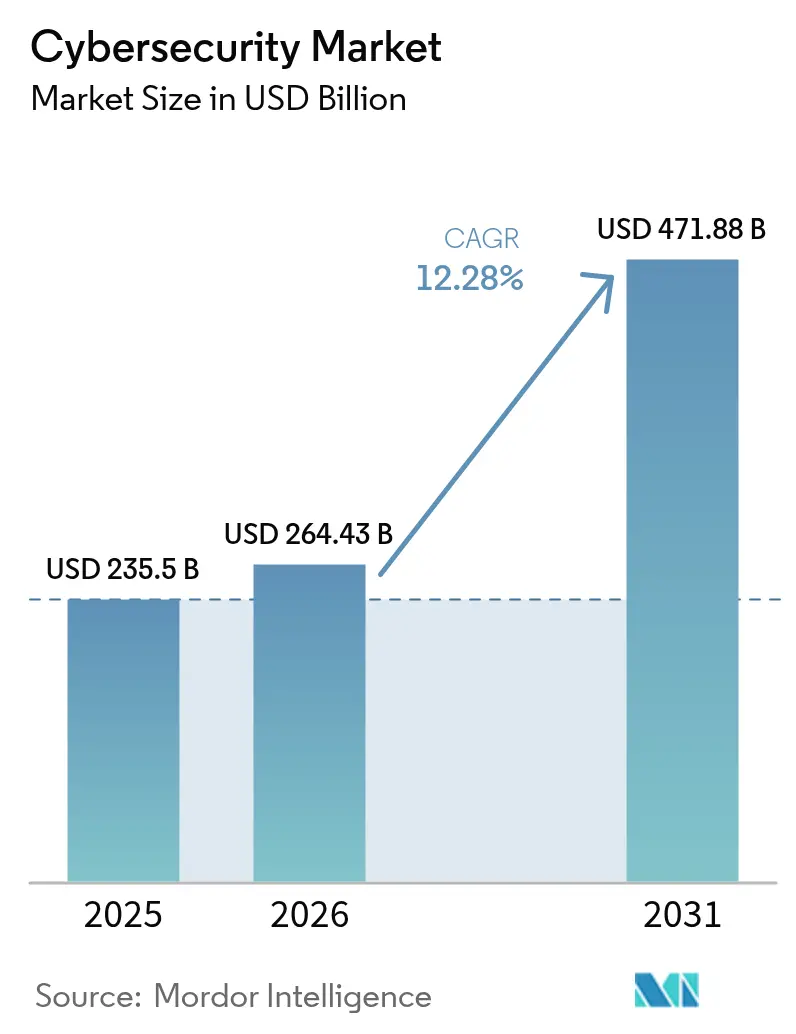

Cybersecurity Market size in 2026 is estimated at USD 264.43 billion, growing from 2025 value of USD 235.5 billion with 2031 projections showing USD 471.88 billion, growing at 12.28% CAGR over 2026-2031.

Increased spending on zero-trust architectures, the integration of IT and operational technology (OT) defenses, and preparations for quantum-ready encryption are the primary forces behind this expansion. North America retains spending leadership, while Asia-Pacific registers the most rapid gains as enterprises migrate workloads to cloud-first environments. Budget allocations are also rising as cyber-insurance underwriters demand verifiable controls, pushing organizations toward unified security platforms that simplify oversight. Simultaneously, platform consolidation through mergers and acquisitions is intensifying as vendors race to cover emerging threat vectors.

Key Report Takeaways

- By offering, solutions captured 69.55% of cybersecurity market share in 2025, while services are expanding through 2031 at 12.85% CAGR.

- By deployment mode, on-premise retained 59.40% share of the cybersecurity market size in 2025, yet cloud-based security is projected to compound at 15.95% CAGR.

- By end-user industry, BFSI led with 26.10% revenue share in 2025; retail and e-commerce is forecast to advance at 15.05% CAGR to 2031.

- By end-user enterprise size, large organizations commanded 67.55% of the cybersecurity market size in 2025, while SMEs are set to grow at 13.25% CAGR.

- By geography, North America held 43.20% cybersecurity market share in 2025; Asia-Pacific is projected to post a 16.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated cloud-first digital transformation | +2.1% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| IT-OT security convergence across critical infrastructure | +1.8% | North America, Europe, and industrial Asia | Long term (≥4 years) |

| Zero-trust architecture mandates for hybrid workforce | +1.5% | North America and EU, expanding in Asia-Pacific | Short term (≤2 years) |

| Surge in cyber-insurance underwriting requirements | +1.2% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Digital-sovereignty regulations driving localised security stacks | +0.9% | Europe, China, India | Long term (≥4 years) |

| Timelines for quantum-ready cryptography migration | +0.8% | Global; early adoption in government and finance | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud-First Digital Transformation

Cloud migration is reshaping security investment priorities as perimeter controls fail in distributed environments. Cloud deployment is growing, outpacing on-premise allocations and driving demand for cloud-native application protection platforms that integrate identity, workload, and data safeguards. Enterprises are seeking unified consoles to reduce tool sprawl, and vendors are responding with platforms that correlate telemetry across hybrid estates, improving visibility and response efficiency [1]Tenable Research Team, “State of Cloud Security 2025,” tenable.com.

IT-OT Security Convergence Across Critical Infrastructure

Industry 4.0 forces formerly air-gapped systems online, exposing legacy control networks to the same adversaries that target IT assets, driving heightened demand in the cybersecurity market. Regulatory frameworks such as ISA/IEC 62443 now require integrated defenses that span production floors and data centers, encouraging investment in specialized OT threat detection and segmentation tools. Energy utilities are leading adoption as nation-state actors probe grid vulnerabilities, and returns on OT-focused security initiatives now exceed comparable IT projects in risk-reduction value.

Zero-Trust Architecture Mandates for Hybrid Workforce

Executive Order 14028 obliges U.S. federal agencies and contractors to shift to zero-trust models by 2025, prompting private-sector emulation. Identity-centred controls, continuous authentication, and micro-segmentation replace legacy VPN-based access, mitigating credential misuse that underlies 38% of breaches. Financial institutions now allocate 12% of IT budgets to zero-trust implementation, up from 9.7% four years ago, reflecting the strategic role of identity governance.

Surge in Cyber-Insurance Underwriting Requirements

Global cyber-insurance premiums are projected to grow, and underwriters increasingly require proof of endpoint protection, multi-factor authentication, and incident response readiness. This compliance-driven purchasing influences small and medium enterprises, which adopt cloud-delivered security stacks to satisfy insurers and secure coverage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security talent deficit and wage inflation | -1.4% | Global; most acute in North America and Europe | Short term (≤2 years) |

| Integration complexity with legacy infrastructure | -0.7% | Manufacturing and finance worldwide | Medium term (2-4 years) |

| API sprawl expanding attack-surface complexity | -0.6% | Cloud-first enterprises globally | Short term (≤2 years) |

| SOC alert fatigue and false-positive overload limiting ROI | -0.5% | Organizations with mature SOCs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Talent Deficit and Wage Inflation

The shortfall of 3.4 million professionals strains budgets as salaries climb for scarce skills in cloud, OT, and AI-driven defense. This constraint is driving market consolidation toward platforms that require fewer specialized personnel to operate, while simultaneously creating opportunities for vendors offering managed security services and AI-powered automation tools. The situation is exacerbated by high turnover rates, with 64% of cybersecurity professionals considering job changes due to workload stress, creating a continuous cycle of recruitment and training costs that impact organizational security budgets [2]Bitdefender Labs, “Global Cyber-Workforce Study 2025,” bitdefender.com.

Integration Complexity with Legacy Infrastructure

Manufacturers and banks struggle to bolt advanced controls onto decades-old systems while preserving uptime. Only 31% of industrial executives believe their current IT stack is future-ready, and 70% of financial institutions admit underspending because integration disrupts operations. Vendors that offer non-intrusive asset discovery and phased migration paths are gaining traction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cybersecurity Market Segment Analysis

By Offering: Momentum Shifts Toward Platform Consolidation

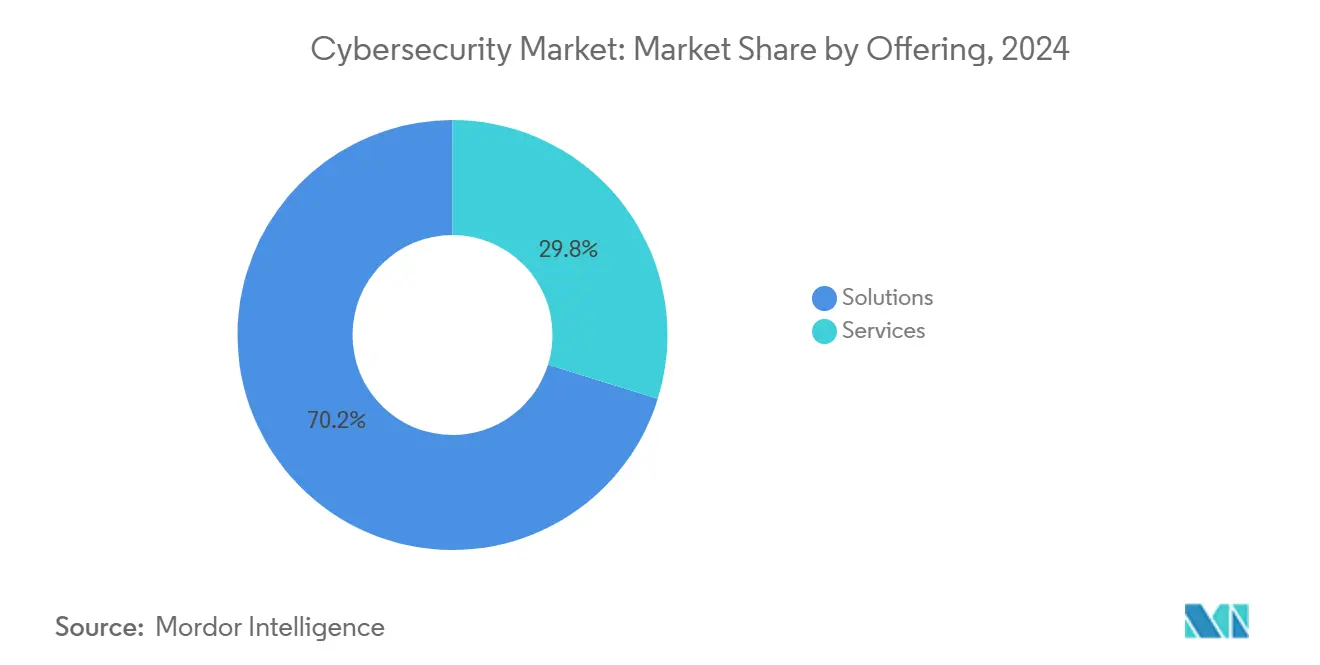

Solutions retained 70.2% cybersecurity market share in 2024 and are set to expand at 13.1% CAGR as enterprises abandon isolated tools in favor of converged suites that unify cloud, identity, and network defenses. Application, cloud, and identity safeguards post the fastest gains, while network and endpoint controls grow more modestly as XDR overlays displace standalone products. Data protection rises in prominence amid new privacy rules, and integrated risk management embeds compliance workflows directly into security dashboards.

Services generated 29.8% of 2024 revenue, with managed offerings benefitting from the talent shortfall even as automation tempers growth. Advisory engagements remain essential for regulated verticals that require bespoke implementations. Providers that pair consulting with recurring managed detection and response services lock in long-term contracts, underpinning predictable revenue streams and deeper client relationships. The cybersecurity market continues to favour vendors that fuse products and services into seamless outcomes, streamlining procurement for resource-constrained security teams while reducing integration risk.

By Deployment Mode: Cloud Uptake Outpaces On-Premise Control

On-premise deployments still accounted for 60.1% of the cybersecurity market size in 2024, reflecting continued preference for direct oversight in highly regulated sectors such as government and healthcare. Yet the centre of gravity is shifting as cloud-native security accelerates at 16.4% CAGR on promises of elastic scale, faster update cycles, and integrated threat intelligence.

Small and medium enterprises gravitate to fully hosted suites that eliminate infrastructure overhead, whereas large organizations pursue hybrid models that keep sensitive workloads in house while routing less sensitive data to regional clouds to satisfy sovereignty mandates. Providers address compliance concerns through in-region data centres and audit-ready encryption controls, removing historical barriers to adoption. Unified consoles that provide visibility across on-premise, private, and public clouds are emerging as must-have capabilities, propelling demand for platforms that correlate logs from endpoints, identities, and network flows in a single analytic engine.

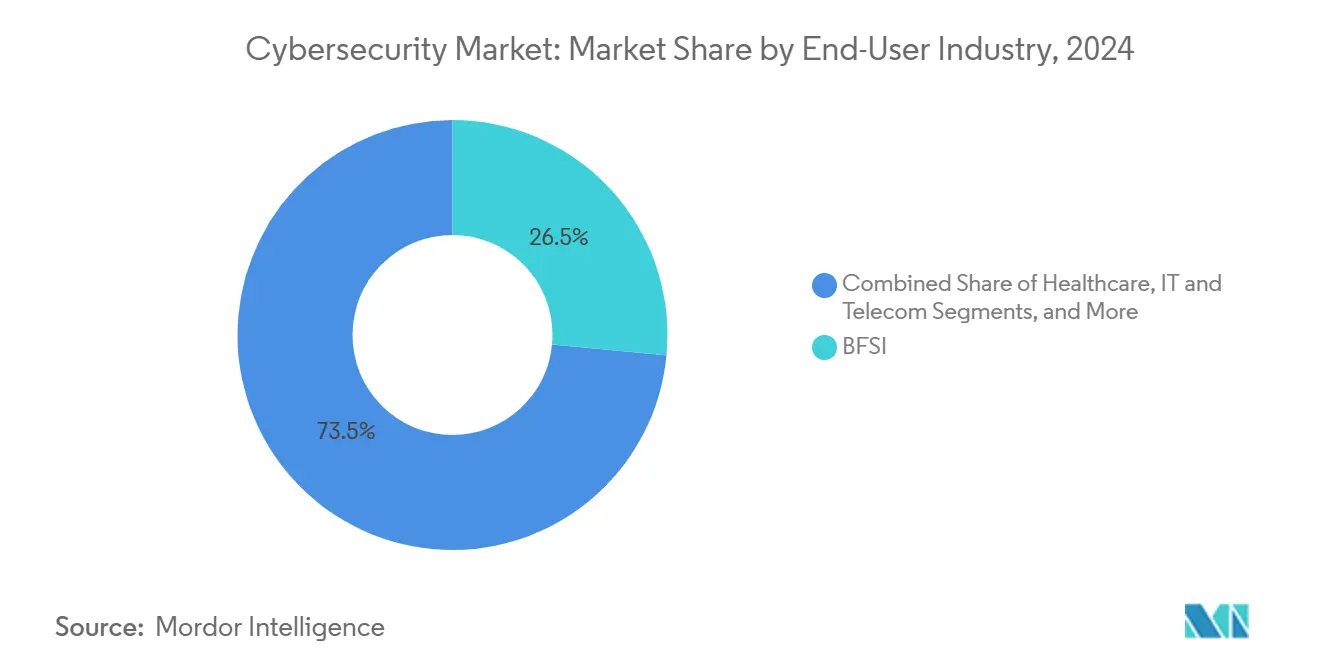

By End-User Industry: BFSI Holds Lead, Retail Surges

BFSI sustained 26.5% share of the cybersecurity market in 2024 owing to stringent regulations and the high value of financial data. Spending continues to grow as institutions implement zero-trust access, real-time fraud analytics, and quantum-ready cryptography to protect payment rails.

Retail and e-commerce is the fastest-growing vertical, advancing at 15.5% CAGR thanks to omnichannel strategies that expand digital attack surfaces. Breach costs tied to customer data exposure and payment fraud spur investment in tokenisation, application shielding, and API security. Industrial and defense entities invest heavily to secure OT environments, while IT-telecom players safeguard carrier networks that underpin national connectivity.. Manufacturers likewise escalate spending because 25.7% of 2024 cyber incidents targeted production systems, driving deployments of asset-centric anomaly detection that bridges IT and OT zones.

By End-User Enterprise Size: SMEs Lean on Cloud Simplicity

Large enterprises generated 68.3% of revenue in 2024 and continue to channel 12% of IT budgets into security, focusing on AI-driven analytics and managed extended detection and response services to counter sophisticated adversaries.

SMEs contributed 31.7% but will outpace their larger counterparts at 13.6% CAGR. Insurers now demand baseline controls before issuing cyber-policies, motivating smaller firms to adopt cloud platforms that bundle endpoint, email, and identity safeguards with simplified management portals. Lower upfront costs and subscription pricing remove capital-expenditure hurdles, while shared-responsibility models offload much of the operational burden to providers.Shared compliance dashboards that map controls to frameworks such as ISO 27001 and SOC 2 appeal to directors seeking board-level assurance without adding headcount.

Geography Analysis

North America controlled 43.20% of 2025 revenue in the cybersecurity market, underpinned by mature regulations and the presence of major vendors. Regional spending is forecast to surpass USD 137.6 billion by 2027 as Executive Order 14028 obliges extensive zero-trust migration. The United States reported 9,036 cyber incidents in 2023, dwarfing Europe’s 2,557 events and sustaining demand for advanced threat intelligence feeds and managed SOC services. Canada and Mexico contribute to growth through joint public-private programs that harmonise cross-border breach reporting and incident response.

Asia-Pacific is the fastest-growing area at 16.85% CAGR, with state-backed digital-nation plans elevating security to critical-infrastructure status. China, India, Japan, and South Korea allocate multi-year budgets to national cyber strategies, while Australia and New Zealand implement comprehensive resilience frameworks that require mandatory incident disclosure. Regional buyers often leapfrog legacy controls by adopting cloud-native security from the outset, accelerating uptake of identity-centric and AI-driven analytics.

Europe region growth is propelled by GDPR enforcement and the forthcoming NIS2 directive that expands coverage to more sectors. Germany, the United Kingdom, and France headline spending, whereas Central and Eastern European markets grow from a smaller base as they align with EU requirements. Sovereign-cloud initiatives in France and Spain stimulate demand for domestically hosted security stacks, while cross-border data-transfer restrictions accelerate adoption of privacy-enhancing encryption techniques.

Regulatory Landscape

Cybersecurity purchasing and operating models are being shaped by maturing disclosure, product-security, and critical-infrastructure requirements across major regions. In the United States, the SEC cybersecurity risk management, strategy, governance, and incident disclosure rules continue to drive board-level accountability and more structured reporting, reinforced in 2026 by updated SEC Division of Corporation Finance sample comment letters and the SEC Cybersecurity Disclosure (CYD) Taxonomy for Inline XBRL (version 2026 published on March 16, 2026). At the standards level, NIST released Cybersecurity Framework (CSF) 2.0 on February 26, 2024, extending emphasis beyond critical infrastructure and updating the reference for enterprise programs and supplier risk management.

In Europe, product and supply-chain security requirements increasingly affect vendor roadmaps and enterprise procurement. Regulation (EU) 2024/2847 (Cyber Resilience Act) introduces security-by-design obligations for products with digital elements, with key 2026 milestones including the June 11, 2026 deadline for Member States to designate notifying authorities and mandatory incident and actively exploited vulnerability reporting under Article 14 starting September 11, 2026. These timelines raise demand for vulnerability management, coordinated disclosure processes, secure update mechanisms, and audit-ready evidence across device, software, and cloud-adjacent cybersecurity stacks.

Value Chain Analysis

The cybersecurity value chain spans foundational inputs (compute infrastructure, networking, and security telemetry sources), core technology providers (identity and access management, endpoint and network controls, cloud and application security, data protection, and risk management), and delivery layers (systems integrators, MSSPs/MDR providers, cyber-insurance-aligned assessors, and incident response specialists). Hyperscalers and platform vendors increasingly act as aggregation points by embedding security controls and analytics into cloud and hybrid environments, while integrators and managed service providers operationalize these tools to offset the cybersecurity talent deficit and SOC alert fatigue.

Supply-chain assurance is now a first-order dependency across this chain as software components, third-party services, and telecom and cloud infrastructure expand the attack surface. Government and standards bodies are elevating ICT supply-chain risk management practices through programs such as CISA initiatives on ICT supply chain security and EU-level actions, including the EU ICT Supply Chain Security Toolbox and the European Commission proposal in 2026 to update the EU Cybersecurity Act framework (often referenced as a Cybersecurity Act 2 direction). These initiatives reinforce multi-vendor strategies, stronger supplier evaluation, and more formalized security documentation, pushing vendors to provide SBOM-like transparency, lifecycle vulnerability response, and certification-ready artifacts that can move with products and services across geographies.

Competitive Landscape

The cybersecurity market remains moderately fragmented, though consolidation is rising as buyers prefer integrated platforms over disconnected point solutions. Google’s USD 23 billion bid for Wiz, Palo Alto Networks’ USD 500 million purchase of IBM’s QRadar unit, and CyberArk’s USD 1.54 billion acquisition of Venafi exemplify the scramble to expand cloud and identity capabilities [3]Douglas W. Hubbard, “Platform Consolidation in Cybersecurity,” journalofcyberpolicy.com.

Emerging companies exploit white space in quantum-ready encryption, OT defense, and AI-powered orchestration. Start-ups that design controls specifically for Kubernetes, serverless workloads, or machine-learning pipelines gain traction among digital-native enterprises. Patent filings for post-quantum key-exchange protocols and reinforcement-learning-based anomaly detection rose 28% year on year, underscoring the sector’s innovation tempo.

Partnerships between cloud service providers and security vendors deepen as hyperscalers embed native threat analytics, compliance tooling, and managed response options directly into their platforms. These alliances accelerate go-to-market cycles for smaller vendors and furnish hyperscalers with differentiated security postures that appeal to regulated customers.

Cybersecurity Industry Leaders

IBM Corporation

Microsoft Corporation

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AI-agent adoption and identity expansion, including non-human identities, are creating whitespace for controls that enforce deterministic policy, monitor agent behavior, and secure machine-to-machine trust at scale. This shows up in 2026 platform moves such as Cisco strengthening identity security for AI agents via its Astrix Security acquisition, and Palo Alto Networks completing acquisitions aimed at securing AI gateways and agentic endpoints. As these capabilities fold into broader platforms, buyers have clearer paths to tool rationalization, faster deployment in hybrid estates, and managed outcomes focused on measurable reductions in tool sprawl and faster response times.

Post-quantum cryptography and machine identity security are also emerging as clearer investment lanes as organizations prepare for quantum-ready encryption migration and stronger auditability. In July 2026, Keyfactor announced over USD 1 billion in strategic growth investment led by Summit Partners to scale machine identity security and post-quantum cryptography, signaling capital flowing into certificate lifecycle, key management, and crypto-agility capabilities. Alongside this, regulatory and sovereignty pressures, including Europe-wide product-security obligations under the Cyber Resilience Act with 2026 reporting milestones, support demand for localized, compliance-mapped security stacks, security evidence automation, and vulnerability response workflows that can be demonstrated to regulators, insurers, and enterprise risk committees.

Recent Industry Developments

- June 2026: IBM, Red Hat, and Palo Alto Networks expanded Project Lightwell to connect software remediation with Palo Alto Networks virtual patching, helping organizations reduce exposure windows when vulnerabilities emerge. The effort ties vulnerability intelligence to remediation execution across hybrid environments, supporting faster, more standardized response processes for enterprises operating at scale.

- May 2026: Palo Alto Networks completed the acquisition of Portkey to add AI gateway security capabilities to its portfolio as enterprises adopt AI applications and agentic workflows. The acquisition supports platform consolidation by extending protection to AI traffic flows and governance points between models, tools, and enterprise data.

- July 2025: Accenture and Microsoft committed joint funding to build generative-AI cyber tools aimed at reducing tool sprawl and operating costs for security teams. The commitment highlights how large service providers and hyperscaler ecosystems are productizing AI-assisted security operations to improve efficiency amid ongoing workforce constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cyber security market is defined as the value of solutions and services used to prevent, detect, respond to, and recover from cyber threats across organizations and public bodies.

Scope exclusions: We exclude general IT hardware refresh, non-security IT consulting that is not tied to a security outcome, and pure telecom connectivity charges.

Segmentation Overview

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Identity and Access Management

- Infrastructure Protection

- Integrated Risk Management

- Network Security

- End-point Security

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premise

- By End-user Industry

- BFSI

- Healthcare

- IT and Telecom

- Industrial and Defense

- Retail and E-commerce

- Energy and Utilities

- Manufacturing

- Others

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, understand typical spend patterns, and collect anchors that can be measured consistently across regions and industries. We mainly referred to public sources such as NIST publications, CISA advisories, FCC and SEC disclosures where relevant, and OECD and World Bank indicators that help explain IT intensity and digital adoption.

To keep assumptions grounded, we also reviewed materials such as company annual reports and investor decks, cybersecurity incident databases, and national cyber readiness updates, along with reputable press coverage of large breaches and regulation changes. We used a paid subscription for company financials and another for patent databases selectively to cross-check vendor exposure and product activity trends. The sources listed here are illustrative, and we also used many other public references for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary discussions were completed with security buyers, channel partners, managed security providers, and product specialists to sanity-check solution adoption and services mix across major regions. We used these conversations to confirm pricing movement, contract lengths, deployment shifts toward cloud, and how budget is split across identity, endpoint, network, and security operations. Where secondary numbers were inconsistent, follow-up calls helped close gaps and align assumptions to what is being purchased in real deals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 41% |

| Mid tier: 61% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 14% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was done using a top-down approach where IT spend, cloud workload growth, and security budget share assumptions were used to reconstruct the demand pool by region, and then split across major solution and service buckets. Those totals were then corroborated using selective bottom-up approximations such as sampled average contract values times estimated buyer counts, channel checks on renewal behavior, and supplier revenue direction checks, which helped adjust any overstatement in early runs.

Key inputs used in the model included reported breach disclosure frequency and regulatory pressure signals, enterprise cloud migration pace, remote and hybrid workforce levels, managed security service penetration, and pricing movement for common subscriptions and monitoring services. For forecasting, we relied on scenario analysis supported by expert views on macro IT budgets and threat intensity, then applied adoption curves that reflect replacement cycles and contract renewal timing. If a bottom-up view could not be built for a niche category due to limited visibility, the gap was handled by using adjacent category ratios and then re-validated through interviews before finalizing.

Data Validation & Update Cycle

Results were cross-checked through triangulation across independent signals, then reviewed for outliers such as sudden regional jumps, unrealistic service shares, or price changes that did not match buyer feedback. We also compared outputs against related indicators like cloud and enterprise software spend direction, public incident reporting trends, and security hiring movement, so the totals stayed connected to a realistic demand base.

Before sign-off, the model goes through multi-step analyst review, and respondents are re-contacted when the model shows a large variance versus earlier cycles or when a major event changes buying behavior. Reports are refreshed annually, and interim updates are made when material shifts occur (for example, a new disclosure rule or a step-change in attack patterns). Right before delivery, we run a fresh pass so clients receive the most current view available at that time.

Mordor Intelligence's Cyber Security Market Size Compared Against Other Published Estimates

Published cyber security market values often differ because the scope line is drawn differently, and because each study makes its own choices on base year, currency timing, and how services are counted. Some estimates also lean more on vendor revenue samples, while others rely on demand-side budgeting signals, which can move the total up or down.

The main gap drivers in this market usually come from whether managed services, professional services, and adjacent IT risk work are bundled into the same number, and whether consumer security products are treated as part of enterprise cyber security spend. Differences also show up when aggressive cloud security growth is applied without checking renewal behavior, or when currency conversion is done using nominal rates that do not match the pricing period used in contracts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 264.43 B (2026) | |

| Trade Journal A | USD 208.10 B (2023) | Uses an earlier base year and a different forecast window, and the published excerpt does not clarify how much managed services and incident response retainers are included in the total. |

| Industry Research Group B | USD 200.10 B (2024) | Shows a lower value partly because services coverage is not clearly stated and the scope is presented mainly by security types, which can miss bundled platform and service revenue reported under broader contracts. |

The table shows a spread that is largely explained by timing and what is counted as cyber security spend, and in Mordor Intelligence's model the total includes both solutions and services across industries with a consistent 2026 value point before growth is projected. When scope is made explicit and the inputs are tied back to measurable spend and adoption signals, the final number becomes easier to interpret and reuse across planning cycles.

Key Questions Answered in the Report

What is the current size of the cybersecurity market?

The cybersecurity market size is USD 264.43 billion in 2026 and is forecast to reach USD 471.88 billion by 2031.

Which region is growing the fastest?

Asia-Pacific is projected to record a 16.85% CAGR between 2026 and 2031, the highest among all regions.

Which deployment mode is expanding most quickly?

Cloud-based security is the fastest-growing mode, expected to compound at 15.95% through 2031 as enterprises seek scalable protection.

Why is zero-trust architecture gaining momentum?

Government mandates, rising credential-based attacks, and hybrid work models are driving organizations to shift from perimeter defenses to identity-centric zero-trust frameworks.

Page last updated on: