Turkey Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

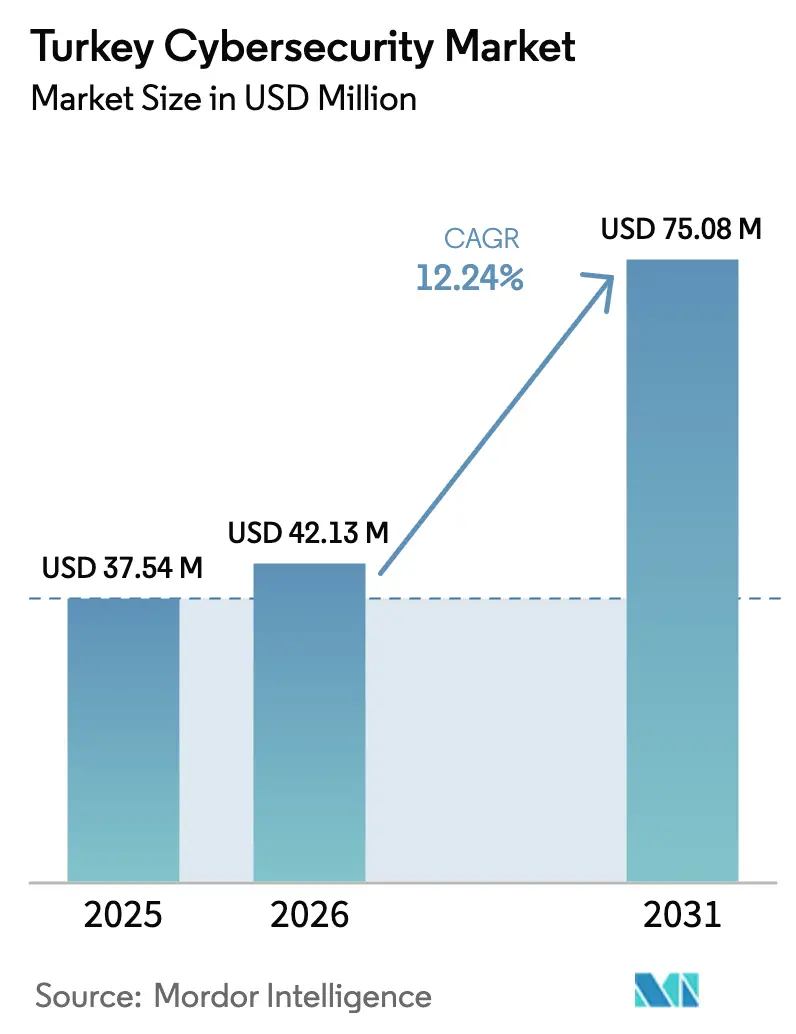

| Base Year Market Size (2025) | USD 37.54 Million |

| Market Size (2026) | USD 42.13 Million |

| Market Size (2031) | USD 75.08 Million |

| Growth Rate (2026 - 2031) | 12.24% CAGR |

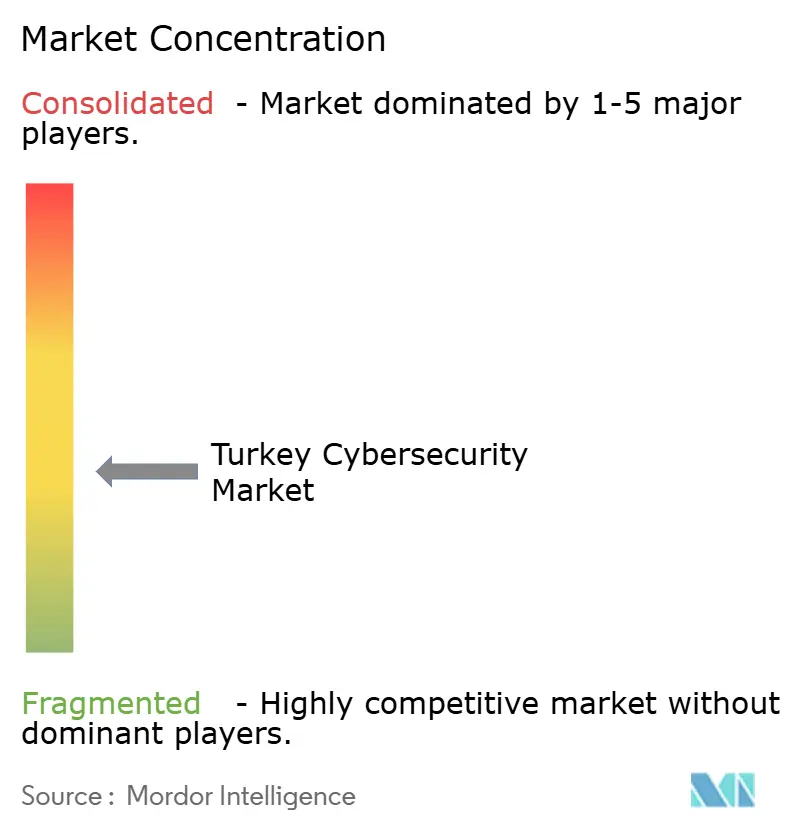

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Cybersecurity Market Analysis by Mordor Intelligence

The Turkey cybersecurity market size was valued at USD 37.54 million in 2025 and estimated to grow from USD 42.13 million in 2026 to reach USD 75.08 million by 2031, at a CAGR of 12.24% during the forecast period (2026-2031). Steady policy pressure for digital sovereignty, persistent attacks on critical infrastructure, and easier access to cloud-based protective tools keep demand on a steep upward path. The Cybersecurity Law adopted in March 2025 assigns direct supervisory power to a new Cybersecurity Authority, forcing public entities and heavily regulated sectors to upgrade controls or face penalties. Boards in finance, healthcare, and energy now treat cyber-risk as a board-level business-continuity issue rather than a discretionary IT outlay, while managed service contracts give relief from the pronounced talent gap. Defensive investments increasingly favor domestic hardware and software that meet local-content criteria, though global suppliers remain vital in high-end analytics and zero-trust frameworks. A volatile lira lifts the cost of imported licenses but also encourages multi-year subscription deals that spread payments in Turkish lira and lock in vendor support.

Key Report Takeaways

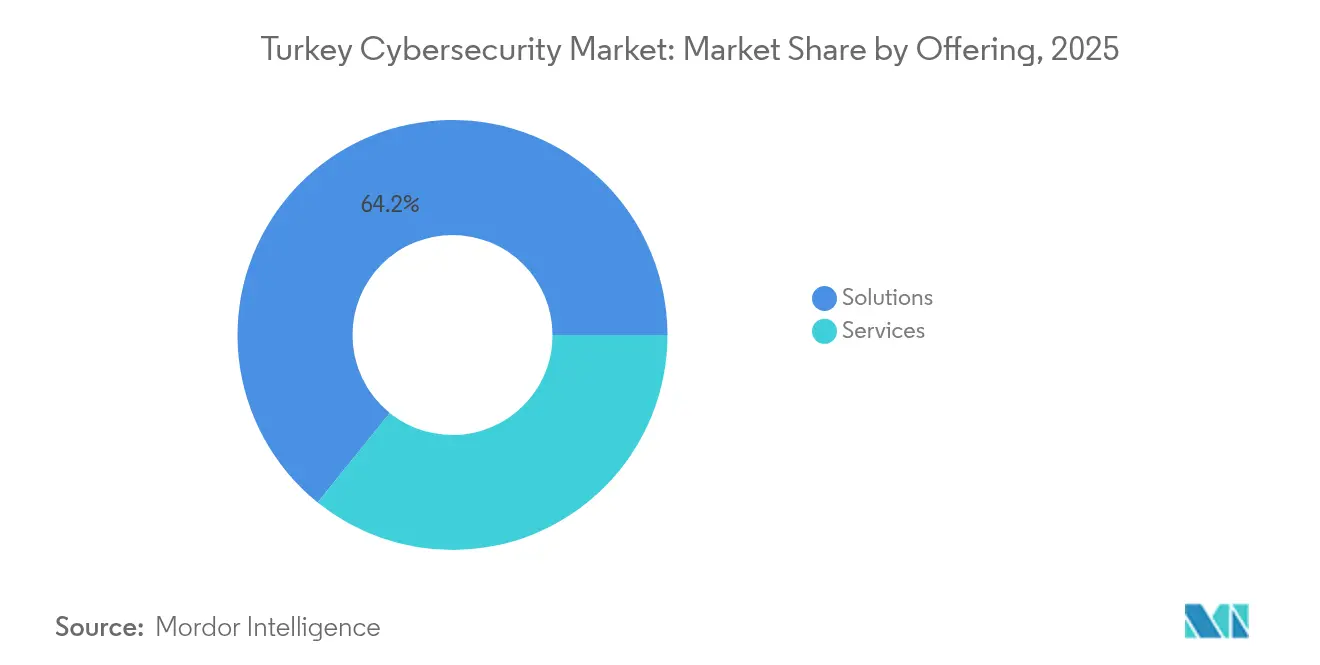

- By offering, solutions accounted for 64.21% of the Turkey cybersecurity market share in 2025, while services are forecast to register a 17.2% CAGR through 2031.

- By deployment mode, cloud captured 51.88% of the Turkey cybersecurity market size in 2025 and is predicted to advance at a 15.1% CAGR during 2026-2031.

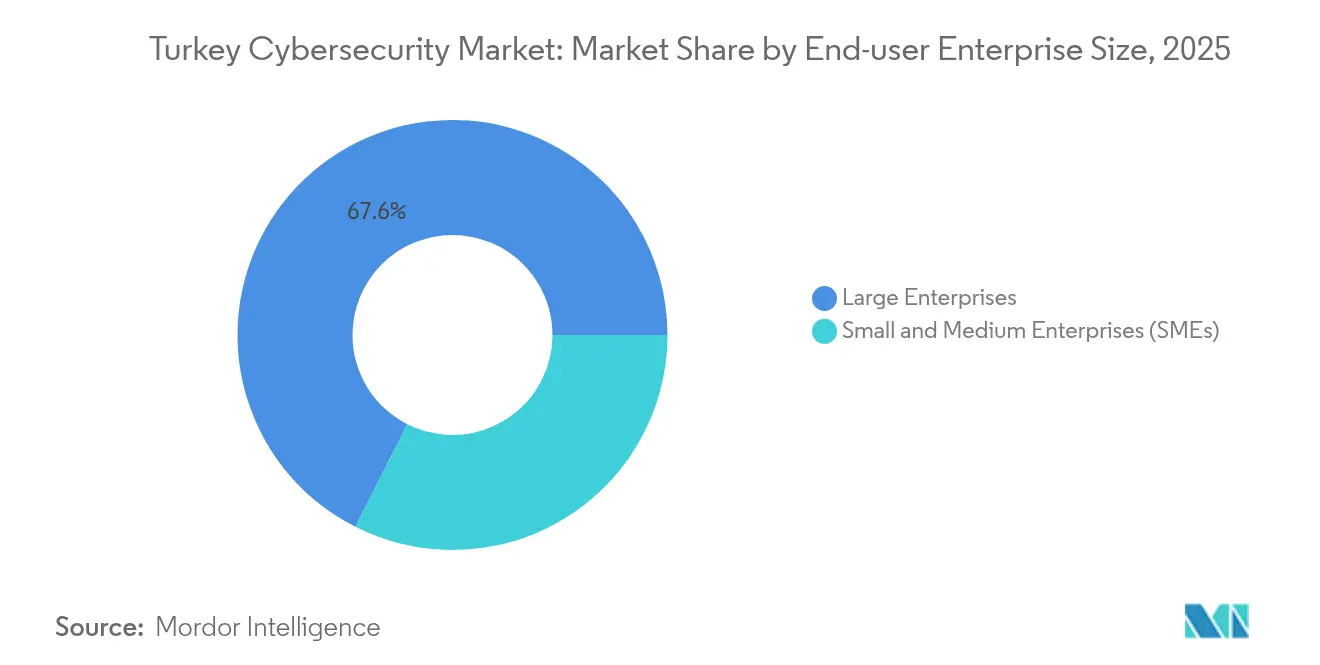

- By organization size, large enterprises held 67.55% revenue share of the Turkey cybersecurity market in 2025; small and medium enterprises (SMEs) deliver the fastest growth at a 15.6% CAGR.

- By end user, the BFSI segment led with 28.41% of the Turkey cybersecurity market share in 2025; healthcare is projected to expand at an 18.2% CAGR.

- Ankara concentrates the bulk of public-sector spending, while Istanbul dominates private-sector demand; high-growth corridors are emerging in Izmir and industrial Anatolian hubs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cyber Security Strategy and SOC roll-out | +5.2 | Ankara, Istanbul, Izmir | Short term (≤ 2 years) |

| E-invoice and e-archive mandates | +3.1 | Urban business centers | Medium term (2-4 years) |

| Geopolitical APT pressure on critical infrastructure | +4.8 | Nationwide high-value targets | Short term (≤ 2 years) |

| Fintech growth and BRSA resilience rules | +4.5 | Istanbul finance cluster | Medium term (2-4 years) |

| 5G-enabled smart-city projects | +2.8 | Major metropolitan areas | Long term (≥ 4 years) |

| NATO cyber accreditation for defense exports | +1.2 | Defense industry belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Cyber Security Strategy and SOC roll-out

Turkey’s Digital Transformation Office obliges ministries to implement round-the-clock monitoring, pushing both public entities and suppliers toward shared Security Operations Centers (SOCs). Integrated stacks combining SIEM and SOAR shorten threat dwell time and help agencies satisfy obligatory breach-report deadlines.[1]Anadolu Ajansı, “Turkey passes new Cybersecurity Law,” aa.com.tr The private sector follows suit: banks and telcos now favor cloud-hosted SOCs delivered as managed services to avoid high set-up costs. Domestic integrators bundle analytics, playbooks, and incident-response teams, capturing contracts in Ankara and Istanbul. Faster detection lowers insurance premiums, creating a secondary financial incentive that sustains spending growth.

E-invoice and e-archive mandates

Mandatory e-invoicing expanded to almost the entire SME base in 2024, forcing firms to digitize accounting data. Cloud security suites that combine encryption, multi-factor authentication, and compliance dashboards protect invoice repositories and minimize audit risk. Subscription pricing linked to issued invoices appeals to cost-sensitive owners and converts sporadic buyers into recurring clients. Vendors embed training modules that cut onboarding time, narrowing the knowledge gap that often plagues first-time technology adopters. This regulatory nudge therefore translates into structural demand for cloud-native protection.

Geopolitical APT pressure on critical infrastructure

Academic research highlights a continued rise in state-sponsored Advanced Persistent Threat (APT) activity targeting Turkey’s grids, pipelines, and transport networks arxiv.org. Utilities react by segmenting operational technology, upgrading encryption on SCADA channels, and feeding telemetry into unified monitoring platforms. Spending intensifies around coastal energy terminals and border-adjacent pipeline hubs where disruption risk is highest. Suppliers of industrial intrusion-detection systems and ruggedized firewalls report multi-year orders as operators bring legacy assets up to modern defense standards. The ripple effect cascades to OEMs that must certify cybersecurity readiness before winning service contracts.

Fintech growth and BRSA resilience rules

Fintech expansion places Turkey fourth globally for cryptocurrency transaction value, prompting the Banking Regulation and Supervision Agency to publish detailed cyber-resilience directives.[2]DEV Community, “Building Cloud-based SOCs in Turkey,” dev.to Institutions must show board-level oversight, layered controls, and tested recovery plans or risk license suspension. Payment processors and e-money issuers upgrade key-management systems and adopt real-time behavioral analytics that spot fraudulent transfers. Compliance timetables align with upcoming tax obligations on digital assets, accelerating procurement cycles. Providers offering turnkey governance frameworks gain a clear edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-talent shortage and wage inflation | –3.5 | Technology clusters nationwide | Medium term (2-4 years) |

| KVKK data-residency constraints | –2.4 | National | Short term (≤ 2 years) |

| Lira volatility and hardware price spikes | –2.1 | SME-heavy regions | Medium term (2-4 years) |

| Local-content procurement mandates | –1.5 | Public projects countrywide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-talent shortage and wage inflation

Turkey’s pool of qualified security engineers cannot satisfy employer demand, driving salary inflation above 40% year on year for senior roles.[3]HackerNoon Editorial, “Cyber-Security Talent Shortage in Emerging Markets,” hackernoon.comSMEs lose candidates to large banks that pay premium packages, prolonging vacancy durations and delaying project launches. To cope, companies outsource tier-one monitoring or deploy automation that handles routine alerts. Universities have introduced postgraduate cyber programs, but graduates will take years to offset the gap. Vendors incorporating low-code policy configuration gain traction because they lower the skill threshold required for daily operations.

KVKK data-residency constraints

Personal Data Protection Law (KVKK) rules oblige data controllers to store or mirror personal data within Turkey except under strict transfer clauses.[4]Kişisel Verileri Koruma Kurumu, “Amendments to Law 6698 on Personal Data Protection,” kvkk.gov.tr Multinational cloud providers localize regions in Istanbul and Ankara to serve regulated workloads, but cross-border threat-intelligence exchange remains constrained. Enterprises running hybrid architectures juggle dual logging stacks, adding cost and complexity that slows cloud migration. Amendments adopted in 2024 promise more flexible outbound transfer mechanisms, yet many companies await secondary guidelines before scaling multi-tenant analytics. The pause creates friction that tempers near-term cloud security uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions retain lead while services sprint ahead

Solutions captured 64.21% Turkey cybersecurity market share in 2025 on the strength of domestic spending for network firewalls, cloud-workload protection, and identity governance platforms. Government preference for locally developed intellectual property channels budget to Ankara-based labs that retrofit global reference designs with Turkish language models. Buyers increasingly demand API security and data-loss prevention to comply with verbose reporting clauses under the Cybersecurity Authority. Vendors respond with consolidated platforms that shrink integration overhead, a feature that resonates with resource-strained teams.

Services are on track for a 17.2% CAGR to 2031, reflecting urgent staff shortages. Managed detection and response converts capital expense into predictable monthly fees, helping boards justify continuous coverage. Consulting units deliver zero-trust maturity assessments for banks and telecoms, while public-sector organizations rely on professional services for SOC build-operate-transfer projects. Providers offering cyber-range training environments stand out because regulators require live-fire exercises as part of resilience audits.

By Deployment Mode: Cloud emerges as catalyst for modernization

Cloud deployments held 51.88% of the Turkey cybersecurity market size in 2025 and will grow at 15.1% CAGR as ministries, banks, and telcos lift workloads into local regions. The Armed Forces Cloud Computing System Project validates sovereign-cloud concepts and spurs parallel civilian investments. Consumption-based pricing neutralizes lira weakness by converting up-front capital into operating expenditure, preserving cash flow.

On-premise installations remain entrenched in agencies managing classified information or running legacy mainframes. These buyers favor virtualized next-generation firewalls and network-access control extensions that import common policy sets for consistency. Vendors now ship identical rule engines across hardware, virtual, and SaaS options, making gradual workload migration easier when compliance barriers subside.

By End-user Enterprise Size: SMEs catch up as compliance tightens

Large enterprises occupied 67.55% of the Turkey cybersecurity market share in 2025, buttressed by strong liquidity and dedicated security teams. They roll out zero-trust architectures across branches and subsidiaries, leveraging centralized procurement to extract volume discounts. In parallel, group-level SOCs harmonize incident handling, satisfying regulatory demand for demonstrable governance.

SMEs will post a 15.6% CAGR to 2031 as e-invoice mandates and supply-chain requirements force action. Turnkey bundles that pack endpoint security, web gateway, and automated backup into a single subscription resonate with owner-managers intimidated by complex tooling. Trade associations mediate group insurance products that reward baseline security certification, creating a carrot for lagging firms. Cloud-native platforms reduce initial investment, making cyber hygiene affordable despite currency swings.

By End User: BFSI stays dominant while healthcare accelerates

BFSI retained 28.41% of the Turkey cybersecurity market size in 2025, propelled by BRSA’s cyber-resilience directives and rising cryptocurrency adoption. Banks implement hardware security modules and real-time fraud analytics, while fintech startups embrace secure-code pipelines from day one to satisfy licensing requirements. The sector’s early adoption sets benchmarks that reverberate into payments, insurance, and wealth-management niches.

Healthcare will compound at 18.2% CAGR through 2031 as telemedicine scales and electronic health records proliferate. Hospital groups deploy micro-segmentation to isolate imaging devices and adopt zero-trust network access to protect remote consultations. Ministry of Health guidelines require encryption of all at-rest patient data, spurring uptake of key-management and secure email gateways. Vendors offering HIPAA-aligned tool sets gain quick traction with private clinics expanding into cross-border medical tourism.

Geography Analysis

Ankara anchors public spending because ministries and defense agencies centralize software procurement, giving the capital an outsized share of framework contracts. Technology parks clustered around Middle East Technical University incubate startups focused on threat analytics and vulnerability research, reinforcing a self-sustaining ecosystem. Close proximity to regulators helps local suppliers iterate platform features quickly, aligning road maps with evolving compliance checklists. International vendors often pilot localized versions of policy engines in Ankara before nationwide release.

Istanbul outspends every other city in private-sector cybersecurity thanks to its concentration of banks, telcos, media houses, and global headquarters. Managed security providers locate primary data centers along the Asian shore to serve both European and Middle Eastern clients with low latency. Competition for skilled professionals is sharpest in Istanbul, keeping wages above the national median and encouraging vendors to bundle automation into offerings. International audit firms base regional cyber-fusion centers in the city, heightening standards across supply chains.

Izmir, Bursa, Konya, and other fast-industrializing Anatolian hubs post double-digit growth as factories digitize production lines. Municipal smart-city pilots in these provinces embed secure IoT frameworks from inception, side-stepping legacy technical debt. Local chambers of commerce run cyber-awareness roadshows that funnel SMEs toward vetted solution partners, smoothing the path to adoption. Rising export orientation forces manufacturers to gain ISO 27001 certification, further expanding regional demand.

Competitive Landscape

Turkey cybersecurity market remains moderately fragmented, housing domestic specialists, defense-linked conglomerates, and global heavyweights. Local champions such as Picus Security and SOCRadar leverage state RandD incentives that reimburse up to 70% of qualifying expenditure, accelerating innovation in breach simulation and external attack-surface management. Defense electronics giant ASELSAN employs a Millileştirme (localization) program that subsidizes qualifying suppliers, ensuring a homegrown parts pipeline for critical projects. This ecosystem effect also benefits civilian verticals where localized firmware and Turkish language interfaces offer a competitive edge.

International vendors including Palo Alto Networks, Cisco, and Fortinet maintain strong positions in next-generation firewalls and secure-access service edge (SASE) platforms, but frequently form joint ventures with local integrators to navigate procurement rules. These partnerships speed up Turkish language support, regulatory alignment, and hardware maintenance turnaround times. Competitive differentiation increasingly centers on value-added services such as threat-intelligence feeds tailored to regional adversaries and flexible financing that shields buyers from currency swings.

Managed security services show signs of consolidation, with a handful of providers capturing a growing slice of recurring revenue. Clients prefer suppliers that combine liability coverage, clear service-level agreements, and on-shore data residency. Vendors that automate triage and reporting free scarce analysts to focus on high-complexity incidents, a capability that resonates across all sectors facing talent constraints. White-space opportunities still abound in IoT firmware hardening and AI-driven user-behavior analytics, areas where no single provider has yet claimed category leadership.

Turkey Cybersecurity Industry Leaders

ADEO Group

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Grand National Assembly passed the Cybersecurity Law, creating a Cybersecurity Authority tasked with safeguarding public institutions and critical infrastructure while prioritizing domestic technology adoption.

- December 2024: Turkish Armed Forces signed the Cloud Computing System Project agreement to establish sovereign cloud infrastructure that supports local data-center products.

- September 2024: Picus Security raised USD 45 million in Series C funding to scale its breach-and-attack simulation platform.

- July 2024: Draft Artificial Intelligence Law submitted to parliament outlines safe and fair AI use, affecting AI-driven security tools.

Turkey Cybersecurity Market Report Scope

The TuTurkey cybersecurity market is defined based on the revenues generated from the solutions and services used in various end-user industries across the world. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting its growth in terms of drivers and restraints.

The Turkey cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the projected Turkey cybersecurity market size by 2031?

The Turkey cybersecurity market is forecast to reach USD 75.08 million by 2031, expanding at a 12.24% CAGR.

Which segment is expected to record the fastest growth through 2031?

Services are set to register the highest growth, advancing at an estimated 17.2% CAGR as firms outsource monitoring and response to offset the talent shortage.

Why does the new Cybersecurity Authority matter for Turkish businesses?

Created under the March 2025 Cybersecurity Law, the Authority can audit critical infrastructure operators and levy fines for non-compliance, making continuous cybersecurity investment mandatory.

How do KVKK data-residency rules affect cloud adoption?

KVKK requires personal data to remain in Turkey unless strict transfer conditions are met, prompting cloud providers to open local regions and enterprises to maintain hybrid architectures.

Page last updated on: