AI-Augmented Security Analyst Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

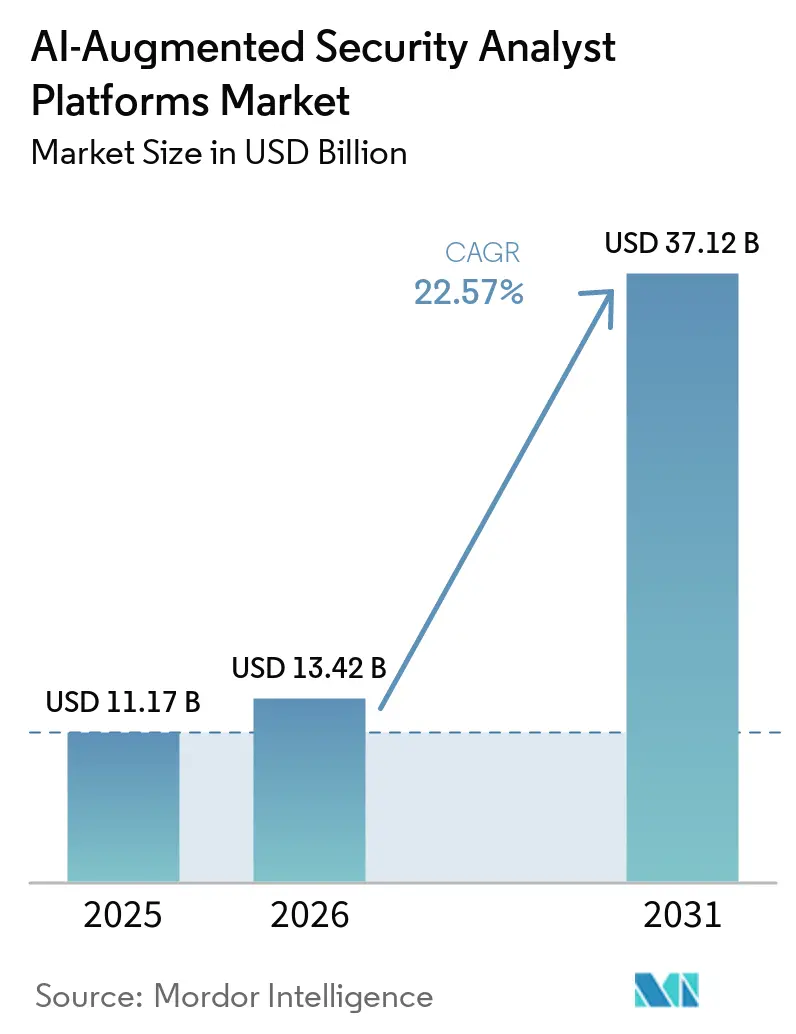

| Market Size (2026) | USD 13.42 Billion |

| Market Size (2031) | USD 37.12 Billion |

| Growth Rate (2026 - 2031) | 22.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Augmented Security Analyst Platforms Market Analysis by Mordor Intelligence

The AI-augmented security analyst platforms market size is expected to grow from USD 11.2 billion in 2025 to USD 13.4 billion in 2026 and is forecast to reach USD 37.1 billion by 2031 at 22.6% CAGR over 2026-2031. The expansion of the AI-augmented security analyst platforms market reflects a simple operating reality: enterprises now run large security stacks, yet analyst teams still struggle to connect signals across cloud, endpoint, network, identity, and operational environments in time. Buying behavior in the AI-augmented security analyst platforms market is also shifting toward broader platforms, as vendor consolidation has become a direct response to tool sprawl, the rising integration burden, and the cost of moving analysts across too many consoles. 45% of organizations actively consolidated cybersecurity vendors in 2025 and 2026. Regulation is adding another layer of demand in the AI-augmented security analyst platforms market because DORA has been applied since January 17, 2025, NIS2 enforcement has widened the compliance gap, and the EU AI Act is pushing buyers to prioritize auditability, sovereignty, and evidence generation in regulated environments. The competitive direction of the AI-augmented security analyst platforms market is moving from simple automation toward agentic investigation, where vendors are competing on reasoning speed, workflow depth, integration breadth, and their ability to reduce manual effort without raising headcount. Opportunities in the AI-augmented security analyst platforms market remain strongest where buyers need sovereign deployment models, compliance-led proof of control, and practical ways to bring advanced security operations to smaller teams that cannot staff a full analyst bench.

Key Report Takeaways

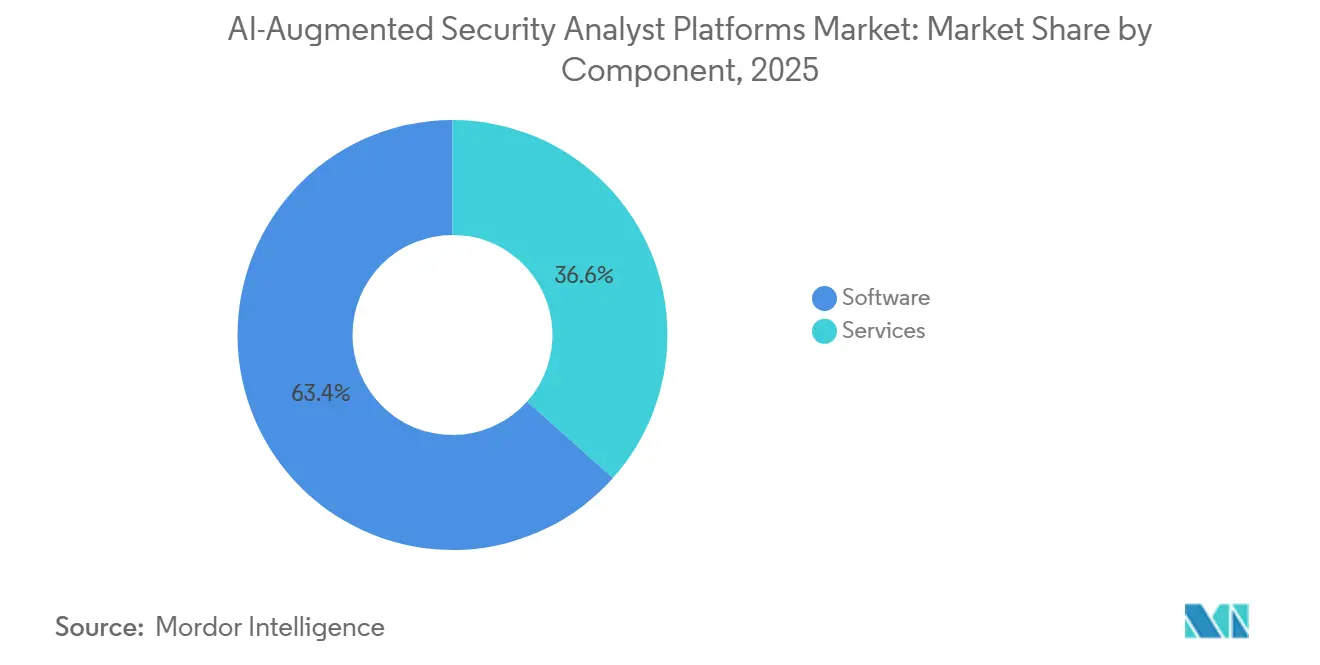

- By component, software led with a 63.4% share of the AI-augmented security analyst platforms market in 2025, while services are forecast to expand at a 23.7% CAGR through 2031.

- By application, Threat Detection and Alert Management held 21.2% share in 2025, while Exposure Management and Security Posture Analysis is projected to grow at 23.9% CAGR through 2031.

- By deployment, cloud accounted for 56.1% share in 2025, while hybrid is expected to record the highest CAGR at 24.0% through 2031.

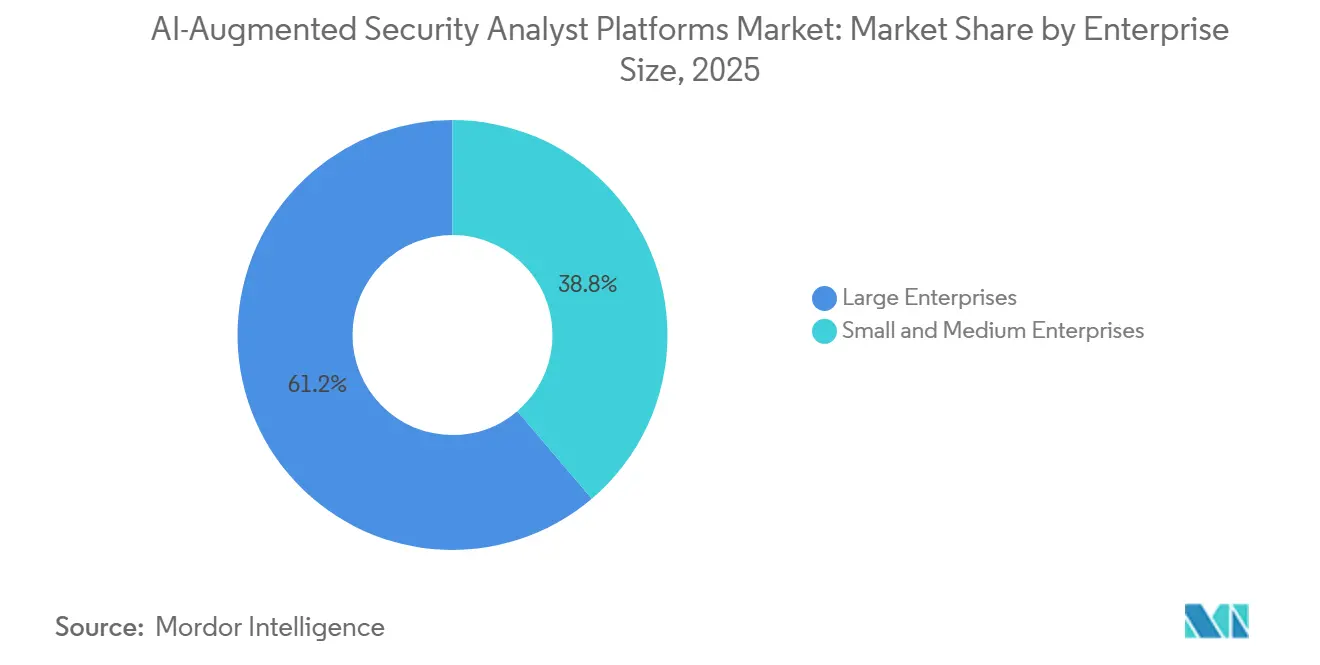

- By enterprise size, large enterprises held 61.2% share in 2025, while SMEs are projected to grow at 24.1% CAGR through 2031.

- By end-user industry, BFSI led with 17.1% share in 2025, while healthcare and life sciences are forecast to expand at 24.2% CAGR through 2031.

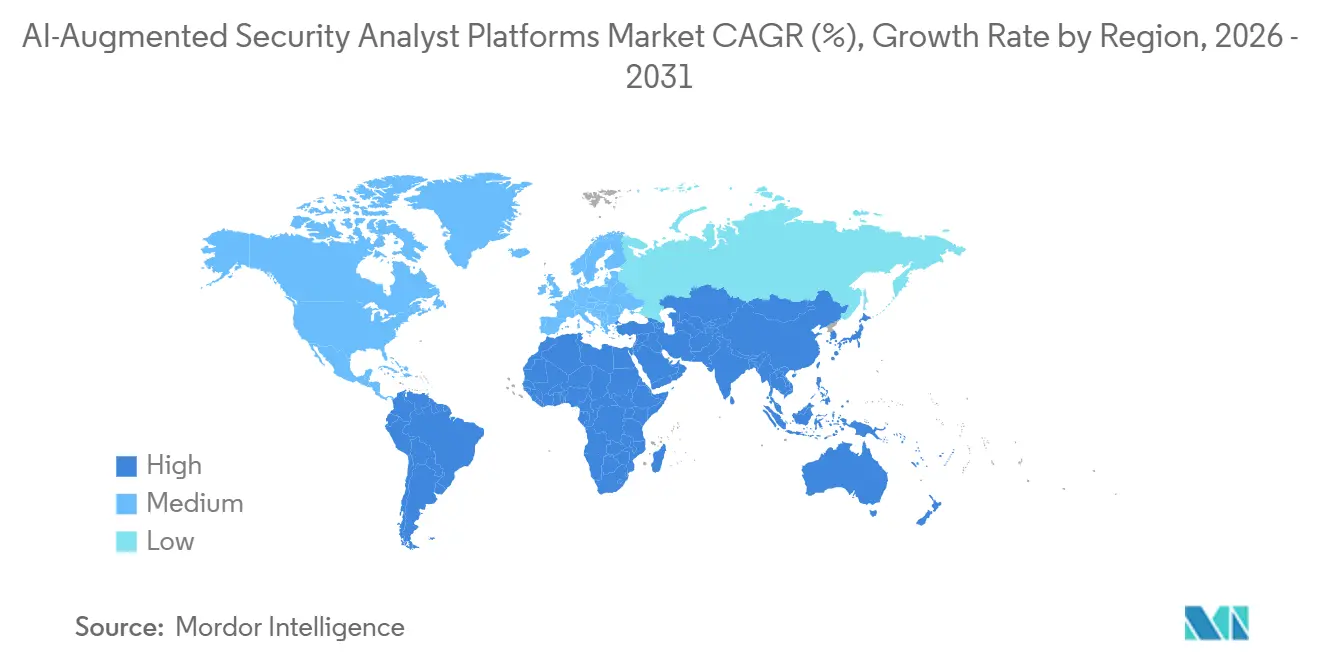

- By geography, North America held a 33.1% share in 2025, while Asia-Pacific is expected to grow at a 24.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Augmented Security Analyst Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Alert Volumes Across Hybrid Security Stacks | +4.8% | Global | Short term (≤ 2 years) |

| Persistent Shortage of Experienced Security Analysts | +4.2% | Global | Medium term (2-4 years) |

| Rising Enterprise Demand for AI-Assisted Triage and Investigation | +3.6% | North America and Europe | Short term (≤ 2 years) |

| Consolidation of SIEM, SOAR, XDR, and UEBA Workflows | +3.1% | North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Higher Spend on Autonomous Response in Regulated Industries | +2.4% | North America and EU | Medium term (2-4 years) |

| Growing Need for Continuous 24/7 Threat Hunting at Lower Unit Cost | +1.9% | Global, with early gains in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Alert Volumes Across Hybrid Security Stacks

The AI-augmented security analyst platforms market is benefiting from a direct mismatch between the growth in alerts and analysts' capacity in hybrid environments. Security teams now work across cloud, on-premises, and operational technology estates, where telemetry is spread across too many systems for manual review to remain effective. This problem is more serious when attacks leave weak signals at each layer, because those signals often become useful only after correlation across endpoint, network, identity, and workload data. Vendors are responding by bringing SIEM and XDR functions together within unified operating layers, reducing the delays caused by siloed products and separate investigation paths. Organizations that use AI and security automation identify and contain breaches 98 days faster than those using manual methods, while average breach savings reach USD 2.2 million per incident, providing the AI-augmented security analyst platforms market with a clear cost-based demand trigger.[1]Fortinet, “Cybersecurity Trends 2026, Defending Against Agentic and AI Threats,” Fortinet, fortinet.com

Persistent Shortage of Experienced Security Analysts

The AI-augmented security analyst platforms market is also being lifted by a shortage that is no longer limited to headcount alone. The problem now centers on skill depth: many organizations can hire staff but still cannot find enough experienced people to investigate incidents at the required level. In 2026, research showed that 27% of organizations had experienced breaches tied directly to workforce capability gaps, and that regulatory compliance was a strong hiring driver. The shortage is especially visible in senior roles, where long experience requirements slow hiring and raise the cost of building a mature internal security operations team. That is why the AI-augmented security analyst platforms market is attracting buyers who want junior analysts to work with greater depth, consistency, and less dependence on scarce senior staff.

Rising Enterprise Demand for AI-Assisted Triage and Investigation

The AI-augmented security analyst platforms market is moving beyond basic automation, as legacy alerting models no longer keep pace with the speed and volume of modern security operations. Buyers increasingly want triage and investigation layers that can classify, prioritize, and assemble evidence before an analyst enters the workflow. The draft indicates that in fully operational configurations, fewer than 2% of alerts may need escalation to a senior analyst, which materially changes staffing assumptions for enterprise security teams. A major vendor reinforced this direction in June 2026, launching Purple AI Agentic Investigation for all customers, bringing zero-click investigations that detect, investigate, verify, and respond without manual initiation. Another leading vendor added native support for frontier AI models across its platform in June 2026, showing that the AI-augmented security analyst platforms market is now competing on reasoning capability as much as on detection depth.[2]SentinelOne, “SentinelOne Opens Purple AI Agentic Investigation to All Customers,” SentinelOne, sentinelone.com

Consolidation of SIEM, SOAR, XDR, and UEBA Workflows

The collapse of old product boundaries across SIEM, SOAR, XDR, and UEBA is reshaping the market for AI-augmented security analyst platforms. Enterprises increasingly view separate tools as a source of cost, operational delay, and data fragmentation rather than as a sign of a best-of-breed strategy. One leading vendor cited data showing that 45% of organizations are actively consolidating cybersecurity vendors, which supports the shift toward integrated platforms.[3]CrowdStrike, “CrowdStrike Unveils Falcon Next-Gen SIEM Support for Microsoft Defender for Endpoint,” CrowdStrike, crowdstrike.com Another major vendor strengthened this trend in March 2026 by adding Next-Gen SIEM support for Microsoft Defender for Endpoint, allowing customers to modernize operations without adding another endpoint sensor. As a result, the AI-augmented security analyst platforms market is seeing procurement shift toward platform economics, where total ownership cost and analyst efficiency now matter as much as product feature depth.[4]Palo Alto Networks, “The Frontier AI SOC Has Arrived,” Palo Alto Networks, paloaltonetworks.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Model Explainability Gaps in High-Risk Security Decisions | -1.9% | Global, with heightened concern in EU-regulated sectors | Medium term (2-4 years) |

| Integration Complexity With Legacy Security Tooling | -1.6% | Global, pronounced in large enterprises with legacy infrastructure | Short term (≤ 2 years) |

| Data Sovereignty and Privacy Constraints on Training Data | -1.3% | EU, Southeast Asia, and Asia-Pacific markets with data localization laws | Medium term (2-4 years) |

| Trust Deficit Around AI-Driven False Positives and Autonomous Action | -1.0% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Model Explainability Gaps in High-Risk Security Decisions

The AI-augmented security analyst platforms market faces a real limit when AI recommendations affect business-critical systems or user access. Regulated organizations need decisions that can be explained, reviewed, and defended in accordance with rules that require clear accountability for security actions. That makes it harder to adopt fully autonomous responses in areas where a wrong isolation action or access block could disrupt production, compliance, or customer service. The EU AI Act raises this bar further by requiring high-risk systems processing personal data to preserve logs and ensure traceability under Article 12, thereby increasing documentation expectations for vendors and buyers. Vendors are trying to narrow the gap with agentic workflows that show investigation steps and evidence chains, but the AI-augmented security analyst platforms market will still see slower adoption of full autonomy until explainability standards become more settled.

Integration Complexity With Legacy Security Tooling

The AI-augmented security analyst platforms market also slows where buyers carry a large base of older SIEM, rules, and workflow investments. Many enterprise environments still use tools bought across several technology cycles, and those products were not built to share schemas, formats, or APIs with AI-native operating layers. Migration is therefore not only a data move; it often requires recreating detection content, response playbooks, and analyst workflows before the new platform can carry the operational load. One vendor addressed part of this issue in March 2026 with a Query Translation Agent in its Next-Gen SIEM, but the feature primarily reduces syntax friction rather than the broader schema and process burden. This keeps the AI-augmented security analyst platforms market from moving at the same pace for all buyers, especially in mid-sized enterprises and public-sector environments with tighter budgets and leaner IT teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Extends Value Beyond Initial Software Purchase

Software held 63.4% of the AI-augmented security analyst platforms market share in 2025, which confirms that the first buying motion still centers on platform subscriptions and core product licenses. AI-assisted SIEM, XDR, and threat intelligence tools remain the primary commercial entry points because enterprises still prefer buying a platform before committing to deeper process redesign. The software lead also reflects how buyers frame the category, since platform coverage, telemetry integration, and investigation capability are usually evaluated before operational support layers. Even so, the AI-augmented security analyst platforms market is no longer defined solely by software, as services are gaining weight, with deployment maturity as the main challenge.

Services are projected to expand at a 23.7% CAGR through 2031, making it the fastest-growing component of the AI-augmented security analyst platforms market. That pace reflects the practical work needed after purchase, including tuning, playbook development, model calibration, process alignment, and ongoing optimization. The draft also ties this pattern to skills depth because many organizations can buy advanced platforms more easily than they can operationalize them internally. Research reported in March 2026 found that 60% of organizations identified skills gaps, rather than simple headcount shortages, as their main cybersecurity challenge, supporting demand for external implementation and managed support. The result is a component mix where the AI-augmented security analyst platforms market is moving from first-stage adoption toward a more service-led operating model.

By Application: Exposure Management Gains Ground as Detection Becomes More Mature

Threat Detection and Alert Management accounted for 21.2% of the AI-augmented security analyst platforms market size in 2025, showing that detection remains the most established application area. This lead stems from installed-base maturity, as enterprises have funded AI-assisted detection workflows longer than any other application group in the category. The segment still matters because alert triage and event correlation are the daily operating core of many security teams. At the same time, the AI-augmented security analyst platforms market is showing a clear shift in marginal spending toward prevention-focused workflows rather than only faster reaction.

Exposure Management and Security Posture Analysis is projected to grow at 23.9% CAGR through 2031, making it the fastest-growing application in the AI-augmented security analyst platforms market. That shift shows that mature buyers now want to reduce the attack surface and identify exploitable gaps before they become active incidents. One vendor moved in this direction in April 2026 with Wayfinder Frontier AI Services, which paired Anthropic's Claude Opus 4.7 with senior security experts for continuous attack surface discovery and guided remediation. The same demand pattern supports incident investigation, response assistance, orchestration, and threat hunting, especially where smaller teams need deeper coverage without adding more senior analysts. Overall, application demand in the AI-augmented security analyst platforms market is broadening from alert handling into posture, exposure, and guided action.

By Deployment: Hybrid Growth Reflects Sovereignty and Control Demands

Cloud captured a 56.1% share in 2025, keeping it the leading deployment model in the AI-augmented security analyst platforms market. SaaS economics, native cloud telemetry access, and consumption-based pricing all support the continued strength of cloud delivery. Cloud also remains attractive because many buyers want faster rollout, simpler upgrade cycles, and easier integration with multi-cloud workloads. Even so, deployment choices in the AI-augmented security analyst platforms market are becoming increasingly segmented as regulatory and data-location requirements grow.

Hybrid deployment is forecast to expand at a 24.0% CAGR through 2031, making it the fastest-growing option in the AI-augmented security analyst platforms market. This pattern appears to run counter to the broader move toward cloud-native architectures, yet it meets the needs of regulated buyers, where some log classes cannot leave local jurisdictions. On-premises deployment, therefore, remains important for government agencies, defense contractors, and financial institutions that need tighter control over where sensitive data resides. Two major vendors responded to this need in June 2026 with Sovereign Cortex with T Security, a model built for regulated European sectors and designed around sovereignty controls. The likely outcome is that the AI-augmented security analyst platforms market will continue to favor architectures in which sensitive logs remain local while AI inference and broader workflow coordination run in managed environments.

By Enterprise Size: SME Adoption Rises as Delivery Models Become Easier to Use

Large enterprises held a 61.2% share in 2025, making them the primary revenue base in the AI-augmented security analyst platforms market. They have the budget scale, operational complexity, and compliance exposure that justify broad platform purchases and long deployment programs. They also gain the most from consolidation because large environments carry the highest penalty from tool overlap, context switching, and workflow duplication. This explains why the AI-augmented security analyst platforms market still derives most current value from enterprise buyers with mature security operations.

SMEs are projected to grow at a 24.1% CAGR through 2031, making them the fastest-growing segment in the AI-augmented security analyst platforms market. Managed delivery models, lower entry friction, cyber insurance expectations, and the rising use of smaller firms as supply-chain entry points into larger organizations are supporting growth here. One vendor widened its SME reach in September 2025 through Amazon Business Prime by offering Falcon Go as a member benefit, which lowered adoption barriers for smaller organizations. The draft also links SME momentum to ISO and CMMC-related compliance expectations, which are pushing buyers to show more formal control coverage without building large internal teams. As a result, the AI-augmented security analyst platforms market is becoming easier for organizations to enter, as they previously lacked the staffing depth to run advanced security operations on their own.

By End-User Industry: Healthcare Growth Outpaces a Still-Strong BFSI Base

BFSI held a 17.1% share in 2025, making it the largest end-user group in the AI-augmented security analyst platforms market. The sector's lead reflects high compliance density, high-value data, and a long record of security spending across banks, insurers, and financial infrastructure providers. Buyers in this segment also face strong pressure to demonstrate resilience, preserve audit trails, and respond more quickly to incidents that could affect customer trust or regulatory standing. For those reasons, the AI-augmented security analyst platforms market remains closely tied to BFSI demand even as other verticals accelerate.

Healthcare and life sciences are expected to expand at a 24.2% CAGR through 2031, making it the fastest-growing vertical in the AI-augmented security analyst platforms market. The draft connects that growth to the spread of AI-assisted clinical systems, which widen behavioral attack surfaces while increasing the need for traceable access and activity records. Government, public administration, energy, utilities, and IT and telecommunication remain meaningful established verticals, while manufacturing, retail, logistics, oil and gas, media, and education continue to move through earlier adoption stages. The European Banking Authority also warned in June 2026 that large language models, particularly frontier ones, had increased cyber risk for European banks by making vulnerability discovery and exploitation more efficient, keeping financial services demand structurally high even as healthcare grows faster. The Reserve Bank of India added to the vertical demand case in June 2026 by requiring board-approved AI risk gap assessments, showing that regulated spending pressure is spreading beyond Europe into Asia-Pacific.

Geography Analysis

North America held 33.1% of the AI-augmented security analyst platforms market share in 2025, which made it the largest regional contributor. The region benefits from deep enterprise security spending, a dense presence of platform vendors, and a policy environment in which the cost of weak cybersecurity controls is rising. The United States remains the main demand center because regulatory disclosure rules, supply chain security expectations, and defense-oriented compliance programs all increase the need for stronger operating platforms. The region also has a high concentration of hybrid multi-cloud environments, and that operating context closely matches the core problem the AI-augmented security analyst platforms market is built to solve. In practical terms, North America remains the most mature buying environment because security teams are already far enough along to justify platform consolidation, AI-assisted triage, and automation at scale.

Europe remains the second-largest regional market for AI-augmented security analyst platforms, with Germany, the United Kingdom, and France as the main demand centers. The region stands out because security purchases are now strongly shaped by the combined effect of NIS2, DORA, and the EU AI Act, which together make explainability, auditability, and sovereignty central to vendor selection. This produces a compliance-first buying pattern that differs from markets where detection performance alone remains the lead criterion. The June 2026 Sovereign Cortex with T Security announcement shows how the AI-augmented security analyst platforms market is adapting with regionalized deployment models for healthcare, financial services, public sector, and critical infrastructure buyers. South America is still earlier in adoption, with Brazil and Argentina showing interest as regulatory ideas begin to move closer to European models, though budgets and IT maturity still limit speed.

Asia-Pacific is forecast to grow at a 24.3% CAGR through 2031, making it the fastest-growing regional band in the AI-augmented security analyst platforms market. Growth is being driven by cloud infrastructure expansion, a rising base of digitally active enterprises, and stronger government-backed cybersecurity mandates across several markets. India is an important trigger point because the Digital Personal Data Protection framework and the Reserve Bank of India's June 2026 advisory are increasing scrutiny of AI-related cyber risk in the financial sector. South Korea and Japan are moving through more advanced adoption paths where large companies are building AI-enabled security operations capabilities at scale. Australia supports steady upgrade demand through public sector and critical infrastructure programs linked to the Essential Eight maturity model. The Middle East and Africa are growing from a smaller base, though Saudi Arabia and the UAE are creating greenfield demand as AI security capabilities become part of broader digital transformation and national cybersecurity agendas.

Competitive Landscape

The AI-augmented security analyst platforms market is moderately fragmented at the broad platform level, but it remains visibly fragmented when specialist vendors are included. Microsoft, Palo Alto Networks, and CrowdStrike remain central to the competitive structure because they combine broad product reach with large customer bases, deep telemetry access, and the ability to build or integrate advanced AI features. At the same time, vendors such as Darktrace, Exabeam, and Vectra AI continue to compete by focusing on narrower operating strengths, including self-learning AI models, cloud-native SIEM positioning, and network-led detection. This means the AI-augmented security analyst platforms market does not behave like a winner-take-all category, since broad incumbents and focused challengers can still win under different buying priorities. Buyers are therefore comparing not only platform breadth but also integration quality, AI workflow design, deployment flexibility, and the operational effort required after purchase.

Strategic moves in 2025 and 2026 show that competition in the AI-augmented security analyst platforms market is shifting toward agentic ecosystems and open workflow design. One vendor launched the Charlotte AI AgentWorks Ecosystem in March 2026, with partners including Amazon Web Services, Anthropic, NVIDIA, and OpenAI, providing customers with a path to build and orchestrate custom security agents within its platform. Another vendor expanded the category in April 2026 through Wayfinder Frontier AI Services, which combined frontier model capability with managed exposure operations and practical remediation support. A third vendor moved at the reasoning layer in June 2026 by adding native support for frontier AI models across its platform, which signaled that model access itself has become part of competitive positioning. These moves show that the AI-augmented security analyst platforms market is being shaped as much by ecosystem partnerships and workflow design as by traditional detection features.

Open architecture is becoming another clear line of differentiation in the AI-augmented security analyst platforms market, as buyers want to modernize without replacing every existing control at once. One vendor's June 2026 extension of its AI Detection and Response across AI gateway partners such as Databricks, Google Cloud, and Microsoft Azure illustrates this push toward broader interoperability. Another vendor also signaled its intent to stay close to frontier model development through its participation in the OpenAI Daybreak Cyber Partner Program, which reflects the importance of external model partnerships to category credibility. White space remains strongest in sovereign deployments, SME-focused platforms, and exposure management use cases that map AI-driven risk paths. The competitive outlook, therefore, points to continued share movement, though not to a collapse around a single vendor set, because the market still rewards different architectures across different security operating models. In that setting, the AI-augmented security analyst platforms market is likely to keep balancing platform consolidation with specialist innovation rather than moving fully to one structure.

AI-Augmented Security Analyst Platforms Industry Leaders

Microsoft Corporation

Palo Alto Networks, Inc.

CrowdStrike, Inc.

SentinelOne, Inc.

Darktrace plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: CrowdStrike extended Falcon AI Detection and Response across leading AI gateway partners including Databricks, Google Cloud, JetStream Security, Kong, LiteLLM, Microsoft Azure, and TrueFoundry, establishing the Falcon platform as an AI security control plane with cross-domain detection across endpoint, identity, cloud, SaaS, and third-party data sources. The move positions CrowdStrike as the security layer for enterprise AI deployments rather than solely a cybersecurity tool.

- June 2026: Palo Alto Networks announced native support for frontier AI models, including Claude Sonnet 4.6, Claude Opus 4.8, and Gemini 3.5 Flash, across the Cortex platform covering XSIAM, AgentiX, XDR, and Cloud, advancing AI reasoning speed and intelligence across security operations workflows. The capability entered private preview with general availability targeted for Q4 FY26

- June 2026: SentinelOne launched Purple AI Agentic Investigation to all customers, introducing Singularity Credits as a unified AI currency across the Singularity Platform and enabling zero-click autonomous investigations that detect, investigate, verify, and respond to threats at machine speed without human dependencies.

- April 2026: SentinelOne unveiled Wayfinder Frontier AI Services, pairing Anthropic's Claude Opus 4.7 with SentinelOne's senior offensive and defensive security experts for continuous, intelligence-led attack surface discovery, prioritization, and guided remediation across the full customer attack surface, extending the Wayfinder portfolio into proactive, AI-accelerated exposure operations.

Global AI-Augmented Security Analyst Platforms Market Report Scope

The AI-Augmented Security Analyst Platforms market comprises software and services that integrate artificial intelligence into security operations to enhance human analysts' capabilities. These platforms include AI-assisted SIEM (Security Information and Event Management), XDR (Extended Detection and Response), and threat intelligence solutions that provide automated detection, investigation, and response support. They are designed to reduce alert fatigue, accelerate incident resolution, and improve overall security posture by augmenting human expertise with machine-driven insights.

The AI-Augmented Security Analyst Platforms market report is segmented by Component (Software,[AI-Assisted SIEM Platforms, AI-Assisted XDR Platforms, AI Threat Intelligence Platforms, Others] and Services), Application (Threat Detection and Alert Management, Incident Investigation and Root Cause Analysis, Response Assistance and Orchestration, Threat Hunting, Exposure Management and Security Posture Analysis), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Government and Public Administration, Industrial Manufacturing, Retail and E-Commerce, Transportation and Logistics, Energy and Utilities, Oil and Gas, IT and Telecommunication, Media and Entertainment, Education and Research Institutions, Healthcare and Life Sciences, Banking, Financial Services, and Insurance (BFSI), and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | AI-Assisted SIEM Platforms |

| AI-Assisted XDR Platforms | |

| AI Threat Intelligence Platforms | |

| Others | |

| Services |

| Threat Detection and Alert Management |

| Incident Investigation and Root Cause Analysis |

| Response Assistance and Orchestration |

| Threat Hunting |

| Exposure Management and Security Posture Analysis |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Government and Public Administration |

| Industrial Manufacturing |

| Retail and E-Commerce |

| Transportation and Logistics |

| Energy and Utilities |

| Oil and Gas |

| IT and Telecommunication |

| Media and Entertainment |

| Education and Research Institutions |

| Healthcare and Life Sciences |

| Banking, Financial Services, and Insurance (BFSI) |

| Other End User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | AI-Assisted SIEM Platforms | |

| AI-Assisted XDR Platforms | |||

| AI Threat Intelligence Platforms | |||

| Others | |||

| Services | |||

| By Application | Threat Detection and Alert Management | ||

| Incident Investigation and Root Cause Analysis | |||

| Response Assistance and Orchestration | |||

| Threat Hunting | |||

| Exposure Management and Security Posture Analysis | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | Government and Public Administration | ||

| Industrial Manufacturing | |||

| Retail and E-Commerce | |||

| Transportation and Logistics | |||

| Energy and Utilities | |||

| Oil and Gas | |||

| IT and Telecommunication | |||

| Media and Entertainment | |||

| Education and Research Institutions | |||

| Healthcare and Life Sciences | |||

| Banking, Financial Services, and Insurance (BFSI) | |||

| Other End User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of AI-augmented security analyst platforms by 2031?

The category is forecast to reach USD 37.1 billion by 2031, rising from USD 13.4 billion in 2026 at a 22.6% CAGR.

Why are enterprises consolidating security tools into broader platforms?

Tool sprawl has increased cost, analyst switching time, and integration burden, and 45% of organizations were actively consolidating cybersecurity vendors in 2025 and 2026.

Which application area is growing the fastest through 2031?

Exposure Management and Security Posture Analysis is projected to grow at 23.9% CAGR, ahead of the more mature Threat Detection and Alert Management segment.

Which buyers are expanding fastest, large enterprises or SMEs?

Large enterprises still lead current revenue with 61.2% share in 2025, but SMEs are growing faster at 24.1% CAGR through 2031.

Which region is expected to expand the fastest over the forecast period?

Asia-Pacific is projected to grow at 24.3% CAGR, supported by cloud expansion, a larger digital enterprise base, and government-backed cybersecurity mandates.

Which end-user vertical currently leads adoption, and which one is growing the fastest?

BFSI led with 17.1% share in 2025, while healthcare and life sciences is expected to post the highest growth at 24.2% CAGR through 2031.

Page last updated on: