Defense Cybersecurity Market Size and Share

Market Overview

| Study Period | 2024 - 2031 |

|---|---|

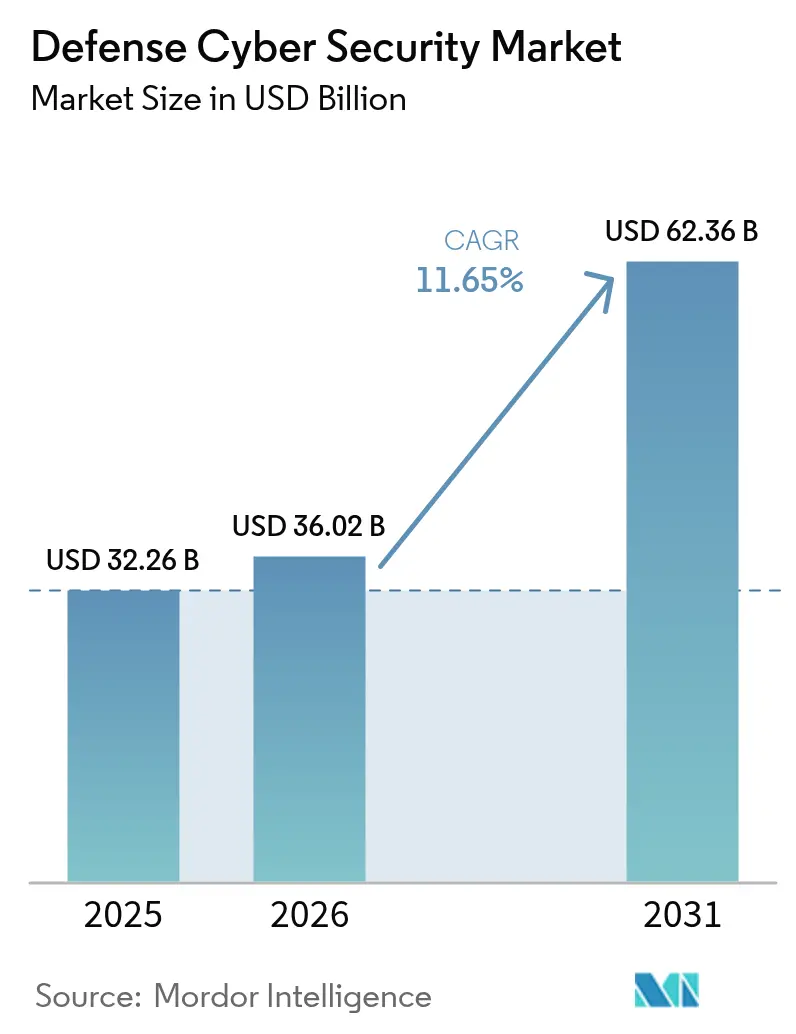

| Market Size (2026) | USD 36.02 Billion |

| Market Size (2031) | USD 62.36 Billion |

| Growth Rate (2026 - 2031) | 11.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

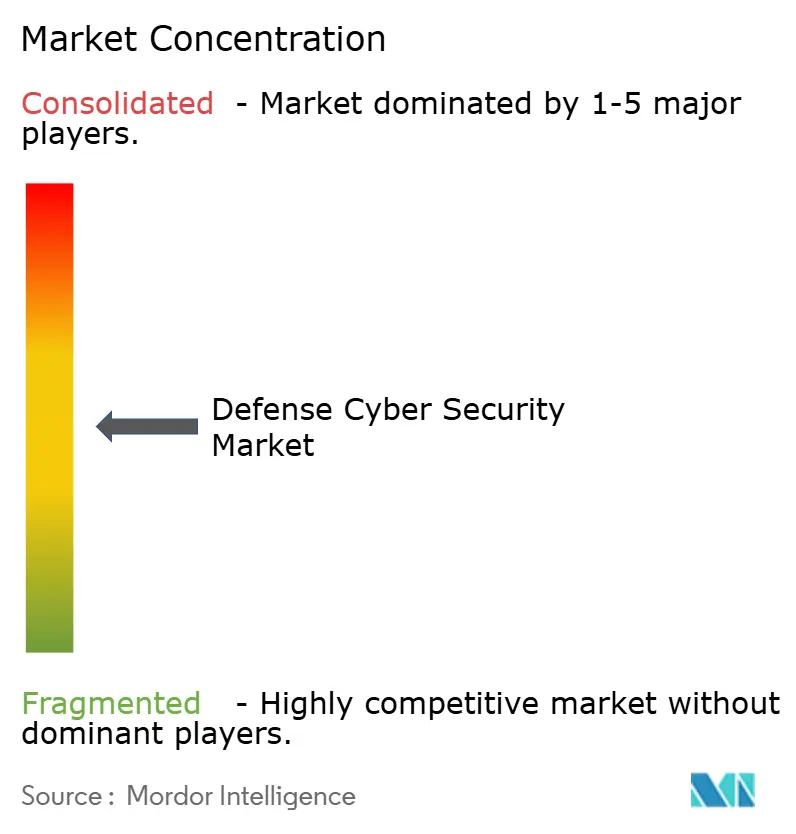

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defense Cybersecurity Market Analysis by Mordor Intelligence

The Defense Cybersecurity Market size was valued at USD 32.26 billion in 2025 and estimated to grow from USD 36.02 billion in 2026 to reach USD 62.36 billion by 2031, at a CAGR of 11.65% during the forecast period (2026-2031). Rapid institutionalization of zero-trust policies, the weaponization of operational technology, and mounting pressure to defend satellite and software-defined networks combine to elevate cyber operations to a full war-fighting domain on par with land, sea, air, and space. Mandates issued by the United States Department of Defense (DoD) to embed zero trust into every weapons platform by 2035 amplify demand for security solutions that operate at both enterprise and tactical echelons.[1]Jared Serbu, “DoD Aims to Automate Zero Trust Assessments,” federalnewsnetwork.com At the same time, the shift to joint, all-domain operations under programs such as JADC2 and GCIA is propelling investment in secure cloud-edge fabrics capable of real-time data sharing in contested theaters.

Key Report Takeaways

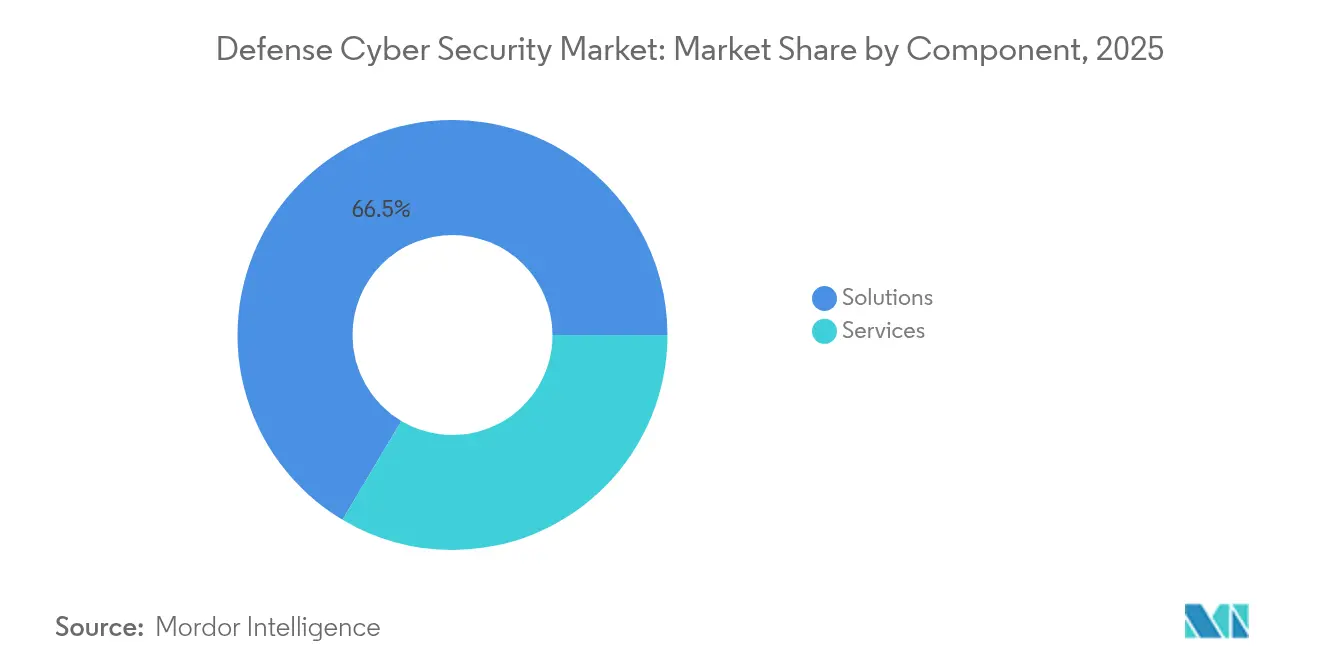

- By component, solutions continued to dominate with 66.45% revenue in 2025, while services are forecast to expand at 11.72% CAGR to 2031.

- By security type, network security led with 41.55% share of the Defense Cybersecurity Market size in 2025, yet cloud security is projected to advance at 15.43% CAGR through 2031.

- By deployment mode, on-premises models accounted for 71.20% of 2025 revenue, whereas cloud deployment is set to rise at 14.42% CAGR.

- By end user, land forces held 36.65% of the Defense Cybersecurity Market share in 2025; naval forces register the fastest growth at 12.24% CAGR.

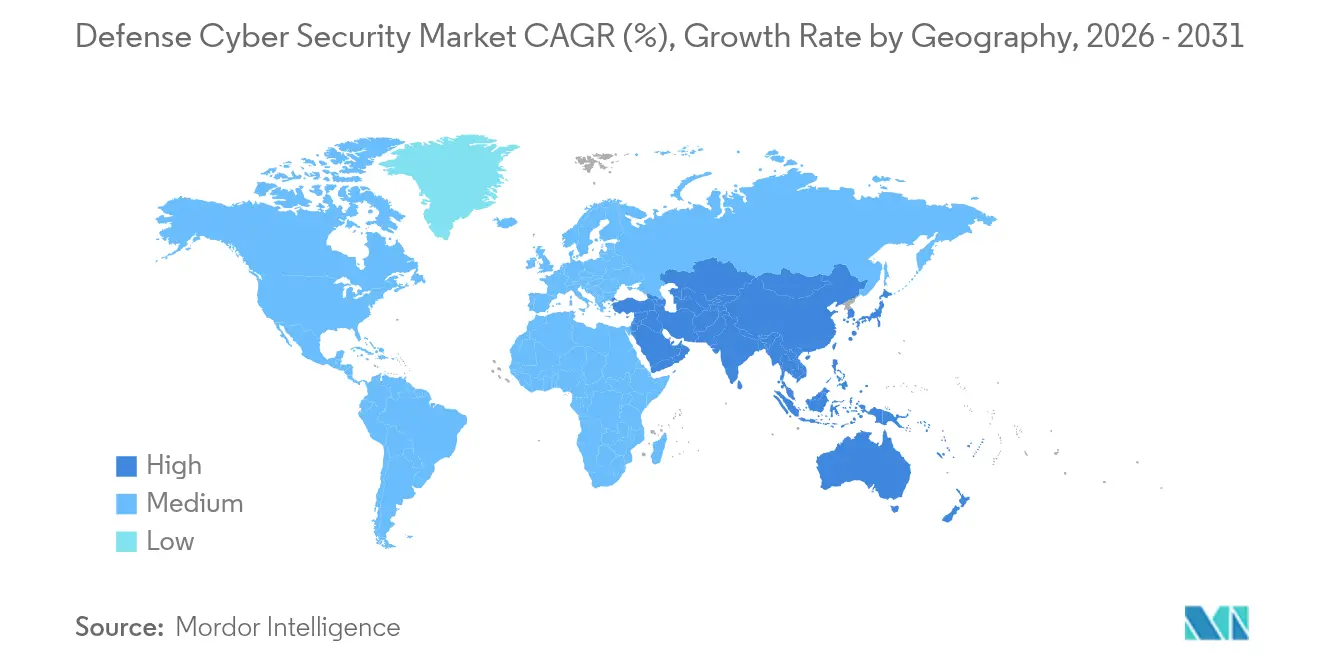

- By geography, North America secured 37.55% revenue leadership in 2025, while Asia-Pacific is pacing at 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Defense Cybersecurity Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Deployment of Software-Defined & Satellite-Based Battlefield Networks in Asia | +2.1% | Asia-Pacific, with spillover to Indo-Pacific allies | Medium term (2-4 years) |

| Mandated Zero-Trust Architectures in U.S. & Five-Eyes Defence Procurement | +2.8% | North America, Australia, UK, with NATO adoption | Long term (≥ 4 years) |

| Accelerated Digital Twin & Autonomous Platform Adoption Demanding Real-Time OT-IT Security | +1.9% | Global, with early adoption in U.S. and Europe | Medium term (2-4 years) |

| Defence Cloud-Edge Migration Programmes (JADC2, GCIA) Driving Secure Data Fabric Spend | +2.3% | North America, with allied interoperability requirements | Long term (≥ 4 years) |

| NATO DIANA & EU EDF Funding Catalysing Cross-Border Cyber Range Investments | +1.4% | Europe, with transatlantic collaboration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Deployment of Software-Defined & Satellite-Based Battlefield Networks in Asia

Asia-Pacific militaries are field-testing software-defined networks that let commanders reconfigure communications topologies in seconds, multiplying potential attack vectors that adversaries can exploit from space to shore. South Korea’s 2024 doctrine now integrates offensive cyber options alongside zero-trust secure enclaves, signaling a regional transition from purely defensive postures. Japan’s active cyber defense law takes effect by 2027 and permits government monitoring of critical infrastructure traffic to flag anomalies, a marked expansion of state oversight. Coupling satellite links with terrestrial 5G nodes improves resilience, yet exposes spacecraft telemetry to spoofing and denial tactics. Exercises such as Talisman Sabre increasingly weave cyber objectives into kinetic war-games, underscoring how the Defense Cybersecurity Market is entwined with broader force-structure decisions.[2]International Institute for Strategic Studies, “Asia-Pacific Military Exercises Data-Set,” iiss.org

Mandated Zero-Trust Architectures in U.S. & Five-Eyes Defence Procurement

Executive Order 14028 and National Security Memorandum 8 oblige every U.S. national-security system to embrace zero trust, fueling compliance-driven procurement that extends from enterprise IT to tactical weapon controls. The Pentagon’s automation of assessment workflows accelerates accreditation without diluting rigor, a prerequisite for scaling across millions of endpoints. Five Eyes interoperability clauses now appear in request-for-proposal language, rewarding vendors that can satisfy multinational security-clearance thresholds. By 2035, zero trust must permeate launch-systems, avionics, and fire-control chains, demanding cryptographic agility and continuous identity verification even in communications-denied settings.

Accelerated Digital-Twin & Autonomous Platform Adoption Demanding Real-Time OT-IT Security

Digital-twin engineering is shortening development cycles but simultaneously exposing simulation environments to espionage. The U.S. Army’s May 2024 decision to build the XM30 infantry vehicle entirely inside a virtual ecosystem illustrates how design data can become a high-value cyber target. Intelligent Acting Digital Twins already issue control commands to physical drones, obliterating the former OT-IT air gap. Protecting controlled unclassified information across these mirrored systems requires encryption at rest and in motion, plus AI-based anomaly detection tailored for real-time sensor traffic. As autonomy expands from reconnaissance drones to lethal systems, the Defense Cybersecurity Market finds new demand for deterministic response engines that cannot be jammed or spoofed.

Defense Cloud-Edge Migration Programmes (JADC2, GCIA) Driving Secure Data-Fabric Spend

JADC2 and GCIA re-architect information flows so that tactical echelons share data seamlessly with strategic commands. The Defense Information Systems Agency earmarked USD 504.9 million in FY 2025 for zero-trust and advanced cyber situational awareness, signaling firm budgetary backing. Edge nodes in denied or degraded environments must make autonomous risk decisions, prompting investment in lightweight security stacks that operate without reach-back connectivity. Cross-Domain Solutions that move intelligence among classification levels now embed automatic sanitization to preserve secrecy while enabling coalition operations. Consequently the Defense Cybersecurity Market is tilting toward adaptive access controls and high-assurance audit functions that persist even when adversaries disrupt backbone links.[3]TechUK, “Cross-Domain Solutions for Coalition Operations,” techuk.org

Restraints Impact Analysis of Defense Cybersecurity Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Platforms Hindering End-to-End Encryption Roll-Out | -1.8% | Global, with acute impact in established defense systems | Long term (≥ 4 years) |

| Prolonged Security-Cleared Talent Gap in Classified Projects | -2.1% | North America and Europe, with spillover to allied nations | Medium term (2-4 years) |

| Cost-Heavy Authority-to-Operate (ATO) & Certification Cycles for Multi-Domain Solutions | -1.3% | North America, with regulatory influence on allied procurement | Medium term (2-4 years) |

| Low Funding Priority and the Lack of Effective ROI Metric | -0.9% | Global, with varying impact based on defense budget allocation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Platforms Hindering End-to-End Encryption Roll-Out

Weapon systems built in the 1990s remain on duty, yet their processors and buses cannot handle modern cryptography without performance trade-offs. Each service branch still sustains platform-specific protocols, complicating any push for unified key-management. Commanders sometimes prefer mission uptime over exhaustive encryption, creating cultural resistance that matches the technical impasse. Because replacement cycles span decades, prime contractors must architect wrapper solutions that retrofit zero-trust principles without rewriting source code, a niche but growing slice of the Defense Cybersecurity Market.

Prolonged Security-Cleared Talent Gap in Classified Projects

DoD’s cyber workforce initiative has not filled critical billets; clearance backlogs of 12-18 months dissuade mid-career professionals. Commercial firms entice the same candidates with compensation packages that dwarf GS-scale equivalents, widening retention gaps. Reciprocal vetting across allies is uneven, limiting multinational staffing on joint programs. Regional imbalances emerge, with the U.S. South and Mountain West confronting sharper shortages because cleared professionals cluster near Washington, D.C., Huntsville, and San Antonio. Talent scarcity therefore drives sustained demand for managed services inside the Defense Cybersecurity Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Defense Cybersecurity Market Segment Analysis

By Component:

Services Growth Outpaces Solutions DominanceSolutions captured 66.45% revenue in 2025, reflecting steady refresh contracts for firewalls, secure-gateway appliances, and threat-intelligence platforms that anchor enterprise networks. That dominance translated into USD 21.44 billion of the Defense Cybersecurity Market size in the base year. Yet services are scaling faster, advancing at 11.72% CAGR, because militaries increasingly view security as a continuous practice rather than a one-off install.

Consulting teams now embed DevSecOps experts inside agile software factories to ensure code pipelines meet authority-to-operate standards from day one. Managed detection and response providers triage millions of daily alerts across the Air Force’s global infrastructure, employing AI to suppress noise and elevate actionable threats. Training regimens covering zero-trust concepts, quantum-safe encryption, and adversarial AI are being delivered by private academies under indefinite-delivery contracts. These activities grow recurring revenue and tilt spending toward services, a pattern that will likely lift the Defense Cybersecurity Market share of services to one-third by 2031.

By Security Type:

Cloud Security Disrupts Network-Centric ModelsNetwork security remained the anchor at 41.55% in 2025, equivalent to USD 13.4 billion of the Defense Cybersecurity Market size. Firewalls, intrusion-prevention systems, and secure gateways still safeguard garrison networks, but cloud security is streaking ahead at 15.43% CAGR. JADC2 mandates multi-level security architectures that stretch from classified to coalition to commercial clouds, forcing procurement of identity, configuration, and data-loss-prevention controls tailored for infrastructure-as-code.

Endpoint and application security segments gain incremental traction as every drone, radar, and combat vehicle morphs into a node on the defense network. Quantum-random-number-generation and AI-enabled threat hunting are emerging sub-segments attracting venture capital and EDF grants. Vendors capable of spanning traditional perimeter defenses and containerized micro-services in cloud environments will consolidate share in the Defense Cybersecurity Market.

By Deployment Mode:

Cloud Adoption Accelerates Despite On-Premises DominanceOn-premises installations accounted for 71.20% of spending in 2025, mainly because classified workloads cannot traverse public infrastructure without high-assurance encryption. That figure represented USD 22.97 billion of the Defense Cybersecurity Market size. Nevertheless, cloud deployment is forecast to add 14.42% annually through 2031 as ministries exploit accredited commercial-cloud zones such as AWS Secret and Azure Government. Hybrid patterns prevail: mission-planning applications may live on-premises while analytics and training simulators run in FedRAMP High clouds where elastic compute is cheaper and faster to scale.

Edge nodes aboard destroyers, aircraft, and forward operating bases now link into this hybrid mesh and rely on burstable satellite bandwidth. The outcome is a nuanced procurement thesis: invest in legacy data-center hardening today while preparing for cloud-native shift tomorrow—a dynamic that sustains growth across both segments of the Defense Cybersecurity Market.

By End-User:

Naval Forces Lead Growth Through Maritime Domain ModernizationLand forces generated 36.65% of 2025 revenue, equating to USD 11.82 billion, as armored formations and signal battalions required hardened networks for contested environments. Naval forces, however, are registering the sharpest trajectory at 12.24% CAGR. Fleet modernization involves outfitting destroyers with zero-trust enclaves, updating submarine combat systems for cyber-resilient stealth operations, and integrating unmanned surface vehicles that share sensor data via secure mesh links.

Air and space arms keep allocating budget to guardianship of satellite constellations and aircraft mission-systems, yet maritime priorities around anti-submarine warfare and choke-point navigation are driving specific investments in crypto-agile communications and autonomous incident response. The varied tempo across end users sustains balanced demand, ensuring no single service monopolizes the Defense Cybersecurity Market.

Geography Analysis

North America Defense Cybersecurity Market

North America retained the lead with 37.55% revenue in 2025 as congressional appropriations embedded cybersecurity line-items in every major acquisition program. Compliance regimes such as CMMC 2.0 obligate the entire defense industrial base—from primes to sub-tier suppliers—to implement controls before bidding, enlarging addressable demand beyond uniformed customers. Canada follows U.S. frameworks to preserve Five Eyes interoperability, while Mexico’s procurement ties gain momentum through cross-border defense technology transfers.

APAC Defense Cybersecurity Market

Asia-Pacific is expanding at 11.12% CAGR through 2031 on the strength of accelerated cyber doctrine in Japan and South Korea, India’s trilateral partnerships with Australia and the United States, and South-East Asian fleet upgrades designed to monitor contested waterways. Sovereign-cloud mandates coupled with satellite network investments make the region the most dynamic theater for vendors targeting forward-deployed, software-defined capabilities within the Defense Cybersecurity Market.

EMEA Defense Cybersecurity Market

Europe benefits from EUR 8 billion (USD 8.5 billion) in EDF funding for 2021-2027, plus the DIANA accelerator that marries NATO demand signals with venture capital. The European Investment Bank’s June 2025 tranche of EUR 8.9 billion (USD 9.4 billion) earmarked for security technologies underlines how public-finance tools are funneling capital into sovereign cyber resilience projects. Meanwhile, the Middle East and Africa register healthy but lower growth as budgets prioritize kinetic systems first; nonetheless, adoption of NATO-aligned standards creates latent demand that global integrators aim to unlock.

Competitive Landscape

The Defense Cybersecurity Market features moderate concentration. Traditional primes—including Lockheed Martin, Raytheon, BAE Systems, and Northrop Grumman—retain incumbency because they already manage classified networks and possess full-spectrum security clearances. They are vertically integrating by buying niche cybersecurity providers to accelerate zero-trust and AI offerings. Examples include CACI’s take-over of Applied Insight, which deepens cloud security and DevSecOps expertise for intelligence agencies; and KBR’s acquisition of LinQuest, adding digital-engineering capabilities for space and missile commands.

Specialist cyber vendors such as Darktrace, CrowdStrike, and BlackBerry’s Cylance division are penetrating the market via autonomous-response engines and device-embedded AI that detect lateral movement in milliseconds. These firms partner with primes in pursuit of Program Executive Office contracts that stipulate cleared personnel and high-assurance supply chains. Meanwhile, platform OEMs like L3Harris are investing USD 3 billion annually in R&D to bundle hardened communications, threat intelligence, and zero-trust gateways into radios, sensors, and tactical networks, eroding the boundary between cybersecurity and platform electronics.

Competitive advantage increasingly hinges on credentials for handling multiple classification levels, ownership of patents in AI or quantum-safe cryptography, and the ability to navigate multi-year authority-to-operate pipelines. Vendors that demonstrate mastery of DevSecOps while offering accredited cyber ranges for training are well positioned to scale market share in the next five years within the Defense Cybersecurity Market.

Defense Cybersecurity Industry Leaders

Raytheon Technologies Corporation

Lockheed Martin Corporation

CACI International Inc.

SAIC Inc.

General Dynamics Corp.

- *Disclaimer: Major Players sorted in no particular order

Defense Cybersecurity Market Companies Covered in this Report

- CACI International Inc.

- SAIC Inc.

- Raytheon Technologies Corp.

- Lockheed Martin Corp.

- General Dynamics Corp.

- L3Harris Technologies Inc.

- BAE Systems plc

- Northrop Grumman Corp.

- Booz Allen Hamilton Holding Corp.

- Leidos Holdings Inc.

- Thales Group

- Airbus Defence and Space

- Leonardo S.p.A

- QinetiQ Group plc

- Palantir Technologies Inc.

- Darktrace plc

- Viasat Inc.

- IBM Corporation

- DXC Technology

- Rohde and Schwarz Cybersecurity

Recent Industry Developments in Defense Cybersecurity Market

- June 2025: The European Investment Bank approved EUR 8.9 billion (USD 9.4 billion) to finance security and defense projects, allocating a significant tranche to encryption, threat-intelligence, and network-protection systems. The move signals stronger EU appetite for strategic autonomy and offers vendors low-cost financing to accelerate R&D.

- June 2025: Microsoft unveiled a European security program that provides governments with advanced threat-intelligence feeds and AI-powered analytics, enhancing detection of state-sponsored groups while deepening public-private collaboration in the Defense Cybersecurity Market.

- May 2025: VTT Technical Research Centre joined six EDF projects worth EUR 218 million (USD 231 million) covering electronic warfare and virtual battlefields, positioning Finland as a key contributor to pan-European cyber-defense innovation.

- March 2025: Japan’s Ministry of Defense, METI, and the Information-Technology Promotion Agency formed a cybersecurity cooperation pact to bolster national situational awareness and streamline industry advisories, creating new compliance baselines for suppliers.

Defense Cybersecurity Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, the defense cyber security market covers all software, hardware, and managed service contracts that enable military and allied defense bodies to monitor, detect, prevent, and respond to malicious cyber activity across IT networks, operational technology, weapon platforms, and classified cloud workloads. Value is captured at the point of contract award or renewal when scope is materially expanded.

Scope exclusion: Civilian-agency endpoint tools and general enterprise licenses are not included.

Segments Covered in This Report

- By Component

- Solutions

- Services

- By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Other Security Types

- By Deployment Mode

- On-Premises

- Cloud and Hybrid

- By End-User

- Land Force

- Naval Force

- Air Force

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Chile

- Colombia

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Qatar

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with cyber-command officers, system integrators running DevSecOps pipelines, and regional procurement advisers across North America, Europe, Asia-Pacific, and the Middle East clarified average contract values for zero-trust frameworks, upgrade cadences for tactical networks, and regional cloud-edge adoption rates, letting us tighten every assumption drawn from desk work.

Desk Research

Our analysts first mapped the spending universe using open sources such as U.S. DoD budget books, NATO CCDCOE threat briefs, SIPRI military expenditure tables, ENISA incident reports, and ITU cyber-readiness indexes. Supplier intelligence gleaned from D&B Hoovers, Dow Jones Factiva, defense procurement portals, and audited filings added contract-level granularity that anchored pricing and deployment timelines. The sources named here are illustrative; numerous additional government and academic references guided data checks and contextual understanding.

Market-Sizing & Forecasting

A top-down pool is built from defense ICT outlays and cyber-earmarked budget lines, then corroborated with selective bottom-up vendor roll-ups and sampled ASP × deployment counts. Key variables include force digitalization ratios, active combat platform counts, classified-cloud penetration, publicly disclosed vulnerabilities, and inflation-adjusted defense spending paths. Multivariate regression on these drivers projects 2025-2030 demand, while scenario analysis stress-tests optimistic and restrained spending cases. Gaps in bottom-up evidence are bridged through calibrated coefficients derived from primary interviews.

Data Validation & Update Cycle

Outputs run through automated variance screens, senior-analyst peer review, and a quarterly trigger that reopens the model when supplemental appropriations, major CVE spikes, or currency swings occur. Full reports refresh yearly, and clients receive interim briefs whenever material events surface.

How Mordor Intelligence's Defense Cybersecurity Market Size Compares to Other Published Estimates

Published estimates vary because firms choose dissimilar scopes, currencies, and refresh cadences. Differences also stem from whether satellite-link hardening is counted, how managed-service renewals are treated, and the timing of foreign-exchange conversion. Mordor's disciplined scope selection, variable tracking, and continual refresh create a dependable decision-making baseline.

In short, by blending verified budget data with selective vendor cross-checks and by revisiting assumptions each quarter, Mordor Intelligence delivers a transparent, balanced market view that procurement planners can replicate with confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.26 B (2025) | Mordor Intelligence | - |

| USD 30.49 B (2024) | Regional Consultancy A | Excludes sovereign-cloud hardening and holds currency at 2022 levels |

| USD 19.14 B (2024) | Global Consultancy B | Counts software only, omits managed security outsourcing |

| USD 42.60 B (2025) | Industry Association C | Rolls aerospace IT cyber spend and civilian space programs into total |

Key Questions Answered in the Report

What is the current size of the Defense Cybersecurity Market?

The Defense Cybersecurity Market size reached USD 36.02 billion in 2026 and is forecast to hit USD 62.36 billion by 2031, growing at 11.65% CAGR.

Which region is growing fastest in defense cyber security?

Asia-Pacific is expanding at 11.12% CAGR as Japan, South Korea, and India enhance cyber doctrine, invest in sovereign clouds, and integrate satellite-based networks.

Why is zero trust critical for defense organizations?

Executive mandates and Five Eyes interoperability requirements force militaries to abandon perimeter defenses, ensuring every user and device is continuously authenticated—even in weapons systems destined to remain in service past 2035.

How are services outpacing product sales?

Services are climbing at 11.72% CAGR because zero-trust roll-outs, DevSecOps pipelines, and managed detection and response demand specialized, ongoing expertise rather than one-time hardware installs.

What are the main restraints holding the market back?

A shortage of cleared cyber professionals, fragmented legacy platforms that cannot run modern encryption, and lengthy authority-to-operate cycles collectively shave more than three percentage points off the potential growth rate.

Which segment shows the highest CAGR by security type?

Cloud security, driven by JADC2 and hybrid-cloud mandates, records a 15.43% CAGR, outstripping network, endpoint, and application security segments in the Defense Cybersecurity Market.

Page last updated on: