Clinical Trials Matching Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 228.11 Million |

| Market Size (2031) | USD 413.26 Million |

| Growth Rate (2026 - 2031) | 12.62% CAGR |

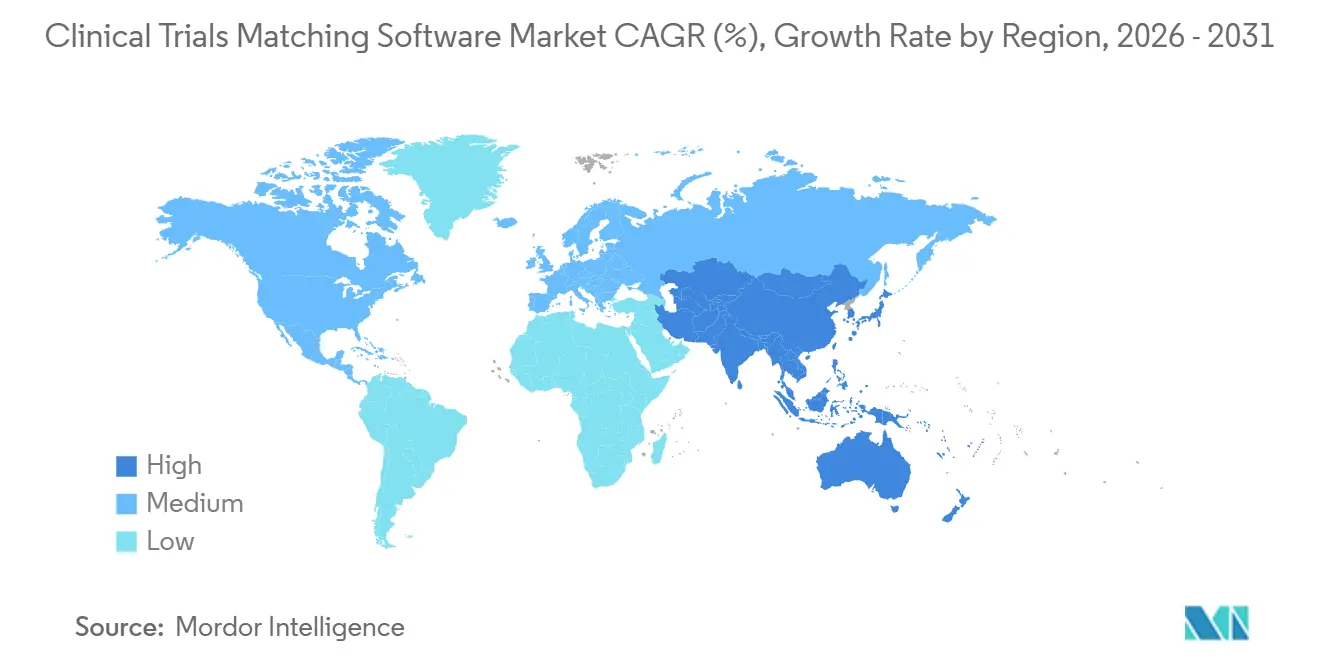

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trials Matching Software Market Analysis by Mordor Intelligence

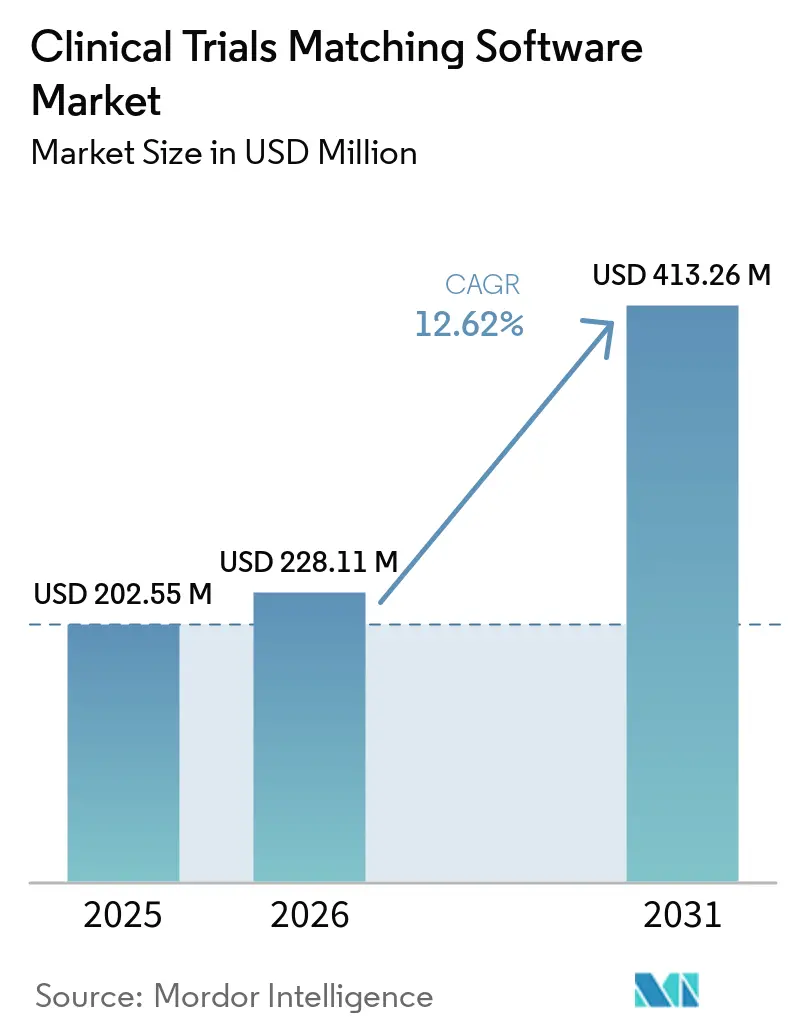

The Clinical Trials Matching Software Market size is projected to expand from USD 202.55 million in 2025 and USD 228.11 million in 2026 to USD 413.26 million by 2031, registering a CAGR of 12.62% between 2026 to 2031.

The clinical trials matching software market is growing as trial protocols, particularly in oncology and biomarker-led research, incorporate more complex eligibility criteria, making manual screening inefficient at scale. Recruitment costs remain a significant driver, with patient recruitment accounting for 32% of total clinical trial expenses and annual spending reaching USD 1.9 billion, emphasizing the need for efficient software solutions.[1]Oracle Life Sciences, “New Oracle Cloud Services Help Pharmas Accelerate Clinical Trial Site Feasibility Assessment and Patient Recruitment,” Oracle, oracle.com Regulatory support has also advanced, with the FDA’s September 2024 guidance broadening the use of remote participation, local providers, and digital tools in enrollment workflows.

Key Report Takeaways

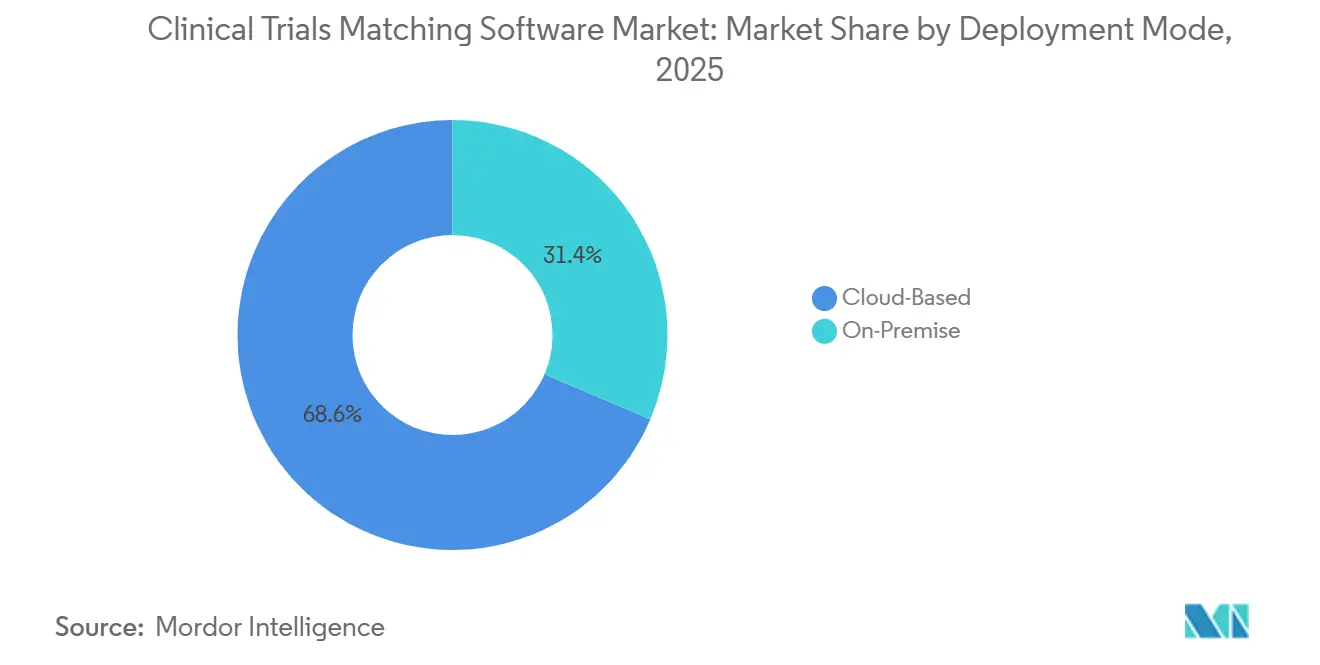

- By deployment mode, cloud-based solutions held 68.60% share in 2025, while on-premise deployment is projected to expand at a 14.24% CAGR through 2031.

- By application, patient recruitment and pre-screening accounted for 38.55% share in 2025, while site selection and activation is projected to grow at a 15.89% CAGR through 2031.

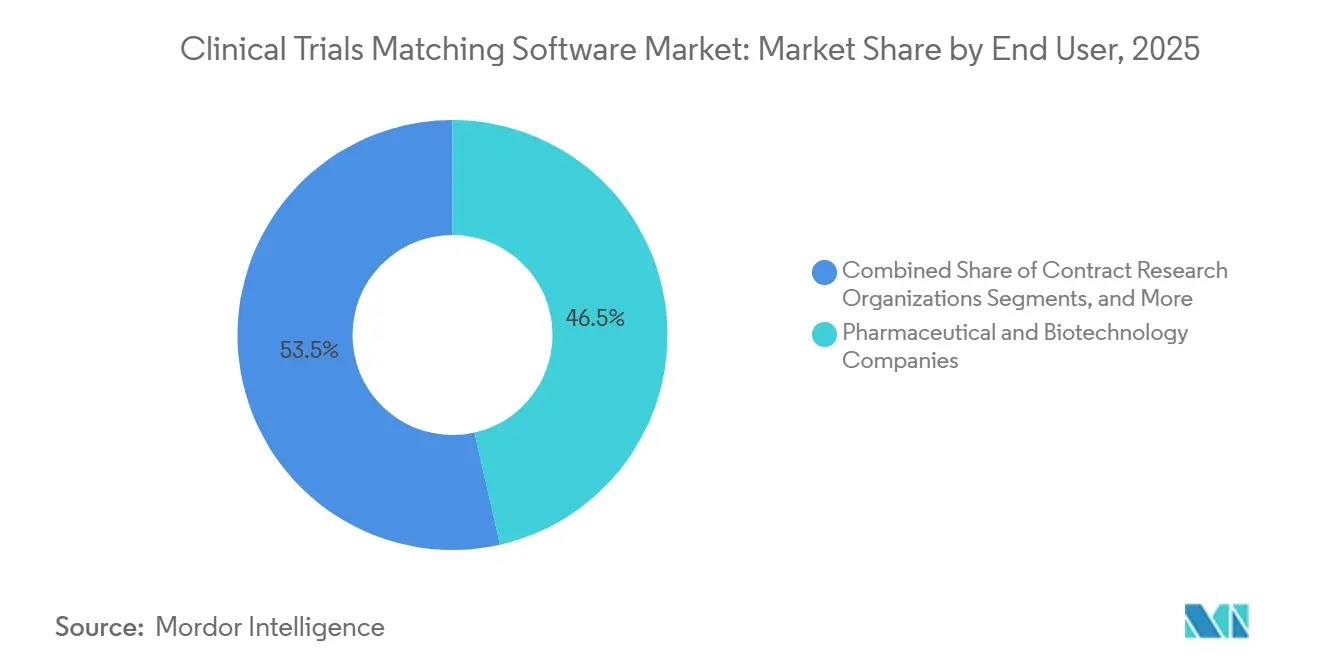

- By end user, pharmaceutical and biotechnology companies held 46.45% share in 2025, while contract research organizations recorded the highest projected CAGR at 13.77% through 2031.

- By technology, artificial intelligence captured 41.88% share in 2025, while natural language processing is expected to grow at a 14.55% CAGR through 2031.

- By geography, North America represented 42.95% share in 2025, while Asia-Pacific is projected to grow at a 15.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trials Matching Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising protocol eligibility complexity | +2.1% | Global, with strongest intensity in North America and Europe | Short term (≤ 2 years) |

| Precision oncology and biomarker trial expansion | +2.4% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Faster feasibility and site selection workflow demand | +1.8% | Global | Short term (≤ 2 years) |

| Decentralized and hybrid trial model growth | +1.7% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Ai and nlp integration for ehr matching | +2.0% | North America first, then Europe and Asia-Pacific | Medium term (2-4 years) |

| Cross-institution interoperability for pre-screening | +1.2% | North America and Europe, with early Asia-Pacific adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EHR-To-Trial AI And NLP Compressing The Patient Identification Window

AI-driven EHR mining and NLP integration are transforming clinical trial matching software by significantly reducing patient enrollment delays. Manual patient file reviews take 11 to 26 minutes, whereas AI and NLP can analyze structured and unstructured data in under 60 seconds. A 2026 study validated TrialMatchAI on 52 oncology patients and 217 molecularly defined Dutch trials, achieving a 92.3% top-20 recall rate, 88.8% inclusion accuracy, and a confabulation rate below 1% across 950 patient-criterion pairs.[2]Alvaro Briatore et al., “TrialMatchAI: an End-to-End AI-Powered Clinical Trial Recommendation System to Streamline Patient-to-Trial Matching,” Nature Communications, nature.com With more eligibility data in physician notes and pathology records than coded fields, the market focus is shifting toward patient follow-up, coordinator support, and retention workflows. Vendors integrating matching outputs with outreach tools are gaining a competitive edge in trial programs prioritizing speed and stability.

Expansion Of Precision Oncology And Biomarker-Driven Trials

The rise of precision oncology is pushing clinical trials matching software toward advanced data handling, as many oncology studies now require biomarker, genomic, proteomic, or histological filters for patient eligibility. These criteria narrow the eligible pool, reducing the utility of standard diagnosis code searches. Tempus AI's 2025 acquisition of Deep 6 AI addressed this need, with Deep 6’s platform covering over 750 provider sites and 30 million patient records, enabling complex trial matching. Vendors with genomics-linked datasets are better positioned for high-complexity oncology studies, while others lag. This gap is expected to widen as sponsors prioritize faster identification of narrowly defined patient cohorts.

Growth In Decentralized And Hybrid Trial Operating Models

The shift to decentralized trials is expanding the role of clinical trials matching software, as patient identification now extends beyond traditional research centers. The FDA's 2025 guidance supported remote participation, local healthcare provider involvement, and digital health technologies, extending compliance to distributed care settings. Platforms must now identify patients through community settings, telehealth networks, and local care pathways, reducing reliance on academic trial hubs. This evolution increases the demand for data connectors and patient engagement tools, positioning matching platforms as essential digital layers for distributed enrollment rather than narrow pre-screening tools.

Rising Complexity Of Protocol Eligibility Criteria

Rising protocol complexity is driving demand for clinical trials matching software, as sponsors require integrated screening of lab values, prior therapies, diagnosis codes, and clinical narratives. Oracle’s Patient Recruitment Cloud Service in 2025 used deidentified EHR data for AI-based eligibility scoring, identifying partially eligible patients and flagging retention risks during pre-screening. Recruitment software is now influencing feasibility testing earlier in clinical development. Citeline’s 2025 launch of Cohort SmartBuilder, leveraging over 7.4 billion tokenized real-world data points, highlighted how eligibility criteria shape patient pools at the design stage. This trend is shifting budgets from trial operations to protocol planning teams.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented data standards and incomplete HER structures | -1.2% | Global, with stronger pressure in Middle East and Africa, Latin America, and parts of Asia-Pacific | Long term (≥ 4 years) |

| Clinician trust gaps in ai eligibility matches | -0.8% | Global | Medium term (2-4 years) |

| Limited trial awareness in rare disease and niche therapy areas | -0.5% | North America and Europe | Medium term (2-4 years) |

| Workflow resistance at sites without dedicated research staff | -0.4% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Health Data Standards And Incomplete EHR Architecture

Fragmented data architecture remains a key technical limitation in the clinical trials matching software market. Even advanced health systems operate with diverse vendors, data models, and configurations. For example, Germany’s MIRACUM network developed a FHIR-based recruitment infrastructure through the Medizininformatik-Initiative but still required significant integration efforts across hospitals. In Europe, country-specific data residency rules complicate cross-border cloud processing, pushing vendors toward localized data handling. In regions like the Middle East, Africa, and parts of South America, low EHR penetration limits the data available for AI-driven matching, leading to uneven market growth despite strong sponsor demand.

Clinician Trust Gaps In AI-Generated Eligibility Screening

Clinician trust remains a critical barrier in the clinical trials matching software market, as adoption depends on coordinators and investigators understanding why a system flagged a patient. A June 2025 review in JCO Clinical Cancer Informatics found that 5 of 24 LLM-based matching studies identified explainability as a barrier, while 3 noted performance differences across patient subgroups. Sites without dedicated research staff face greater challenges in validating AI recommendations. High technical accuracy alone is insufficient; users need clear explanations of the logic behind matches. Vendors offering criterion-level explanations are more likely to drive adoption, particularly in community settings with historically low software penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Leads While On-Premise Rebounds On Data Sovereignty Pressure

In 2025, cloud-based deployment held 68.60% of the clinical trials matching software market, driven by the need for faster onboarding, multi-site visibility, and real-time enrollment management. Cloud systems reduce local infrastructure requirements and provide centralized dashboards for geographically dispersed trial teams. Sponsors and CROs prefer cloud environments for standardizing workflows across multiple sites, countries, and therapeutic programs. Despite growing privacy and sovereignty concerns, cloud remains a cornerstone of the deployment landscape.

On-premise deployments are projected to grow at a 14.24% CAGR through 2031, making them the fastest-growing segment in the clinical trials matching software market. This growth is fueled by compliance requirements in countries like Japan, Germany, and China, where strict regulations govern health data processing. Vendors are addressing this by developing containerized matching engines that operate within hospital environments, sending only anonymized or summarized data externally. The industry is increasingly adopting hybrid and federated models as a balanced approach.

By Application: Site Selection Growth Signals Protocol-Earlier Software Adoption

In 2025, patient recruitment and pre-screening accounted for 38.55% of the clinical trials matching software market, reflecting its maturity and critical role in enrollment timelines. Sponsors prioritize this function to avoid missed enrollment targets, which can impact study costs, milestones, and site productivity. Advanced matching platforms now screen using layered eligibility criteria, ensuring recruitment and pre-screening remain central to the market and justifying continued investment in tools capable of handling structured and narrative data.

Site selection and activation is projected to grow at a 15.89% CAGR through 2031, making it the fastest-growing application area in the clinical trials matching software market. AI-enhanced feasibility modeling has demonstrated significant benefits, such as reducing protocol amendments and improving site acceptance rates. Sponsors are increasingly adopting software earlier in the study cycle to enhance site selection, reduce recruitment failures, and improve protocol planning, drawing more attention from clinical development teams.

By End User: Pharma Anchors The Market As CRO Growth Signals An Outsourcing Shift

In 2025, pharmaceutical and biotechnology companies held a 46.45% share, making them the largest end-users in the clinical trials matching software market. Their dominance stems from managing large Phase II and Phase III programs, where enrollment delays have significant financial and operational implications. These organizations also handle complex eligibility frameworks, particularly in oncology, making advanced screening and patient identification essential. Their sustained budget allocations ensure their central role in driving market demand.

Contract research organizations are projected to grow at a 13.77% CAGR through 2031, making them the fastest-growing end-user segment. Sponsors are increasingly shifting recruitment responsibilities to CROs through performance-linked contracts, prompting CROs to invest in advanced matching tools. This trend highlights the growing importance of clinical trials matching software in CRO operations and economics.

By Technology: AI Dominates But NLP Represents The Fastest-Growing Value Layer

In 2025, artificial intelligence captured 41.88% of the clinical trials matching software market, reflecting its ability to process large patient populations and manage complex variables. AI has become a core operational layer, supported by its integration into broader clinical platforms and the prominence of AI-native vendors. Its widespread adoption underscores its critical role in the market.

Natural language processing is projected to grow at a 14.55% CAGR through 2031, making it the fastest-growing technology layer in the clinical trials matching software market. NLP is crucial for extracting valuable eligibility information from free-text clinical narratives like physician notes and pathology reports. Domain-specific NLP solutions are gaining traction, especially in text-heavy records with inconsistent coding quality, positioning NLP as a high-value layer in the market.

Geography Analysis

In 2025, North America dominated the clinical trials matching software market, capturing 42.95% of the share. This dominance is attributed to the region's extensive EHR penetration, a high density of clinical trial sites, and the concentration of sponsor and CRO headquarters that influence purchasing decisions. The FDA's guidance in September 2024 on decentralized clinical trial elements expanded the practical enrollment radius for individual sites and formalized pathways for remote participation. In February 2025, Inovalon introduced its AI-driven Clinical Research Patient Finder, integrating with EHRs to automate pre-screening and real-time patient identification. Canada stands out for its robust digital health adoption, while Mexico remains significant for sponsors targeting diverse oncology and cardiometabolic trial populations.

Europe ranks as the second-largest player in the clinical trials matching software market, with Germany, the UK, and France leading adoption and trial activities. Privacy regulations significantly influence software architecture and procurement decisions in the region. Vendors increasingly favor local data processing and federated models to comply with country-specific privacy boundaries. Germany's MIRACUM consortium exemplifies this trend with its FHIR-compliant recruIT infrastructure for patient recruitment across university hospitals. This model raises the bar for commercial vendors, pushing them to excel in usability, advanced analytics, and workflow value. Spain, Italy, and other European nations benefit from the EU Clinical Trials Regulation, which facilitates broader multi-country trial coordination.

Asia-Pacific is projected to grow at a 15.45% CAGR through 2031, making it the fastest-growing region in the clinical trials matching software market. Japan is accelerating trial digitization to address drug lag and expedite candidate screening. Fujitsu's collaboration with Tokai National Higher Education and Research System in May 2025 structured unstructured clinical data from 1,800 patient records with 90% accuracy, reducing patient candidate selection time by a third. China is scaling domestic platforms for global registration, while emerging markets in Africa and South America, though smaller, are gaining traction, as demonstrated by Oracle's support for the Africa Clinical Research Network trial across Zimbabwe, Rwanda, and Tanzania.

Competitive Landscape

In the clinical trials matching software market, competition is split between large integrated platforms and AI-native specialists, leading to a moderately fragmented landscape. Enterprise giants like IQVIA, Oracle, Veeva Systems, and Medidata find themselves in competition with niche players such as Tempus AI, TriNetX, Antidote Technologies, Reify Health, and Trialbee. The larger vendors leverage their extensive clinical operations coverage, established relationships with sponsors, and access to broader enterprise budgets. In contrast, specialist vendors focus on direct competition, emphasizing matching speed, the depth of data connectors, and performance metrics like time-to-first-patient. This dynamic interplay ensures the market remains vibrant, with no single platform emerging as the clear leader.

Strategically, players are expanding capabilities through acquisitions, platform enhancements, and scaling their networks. For instance, Tempus AI's acquisition of Deep 6 AI in March 2025 bolstered its precision research workflows by integrating a real-time EHR mining engine into its multimodal clinical database. Meanwhile, IQVIA, in collaboration with NVIDIA, took a different approach with the March 2026 launch of IQVIA.ai, aiming to unify AI across life sciences workflows. Further underscoring the trend, Regeneron, in April 2026, entered a strategic collaboration with TriNetX, committing up to USD 200 million to tap into a de-identified EHR network that spans 300 million patients across over 11,000 provider locations. These strategic maneuvers highlight the growing importance of scale, data depth, and workflow integration in the market.

Opportunities still exist in areas like rare disease recruitment, multilingual patient engagement, and compliance tailored to specific regions. In Europe, Japan, and China, stringent privacy regulations are favoring vendors adept at supporting federated or hybrid deployments, ensuring robust sponsor oversight. Furthermore, academic and public health networks are gaining traction. Their open-standard infrastructure poses a challenge: if commercial vendors don't elevate their offerings, basic matching functions may lose value. This shift is steering the market towards advanced analytics, enhanced engagement, and improved interoperability, moving beyond mere patient flagging. The competition, therefore, appears not only active but also on an upward trajectory.

Clinical Trials Matching Software Industry Leaders

Deep 6 AI, Inc.

Antidote Technologies, Inc.

TriNetX, LLC

Microsoft Corporation

Tempus AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Oracle collaborated with the Africa Clinical Research Network (ACRN) to launch its first clinical trial in Africa, expanding its clinical technology footprint in Sub-Saharan Africa through the PROTECT-Africa study targeting 1,106 pregnant women.

- April 2026: Regeneron Pharmaceuticals invested up to USD 200 million in TriNetX, gaining exclusive access to its global network of 300 million de-identified patient records to advance drug discovery, AI model training, and digital health solutions.

- March 2026: IQVIA, in partnership with NVIDIA, introduced IQVIA.ai, an AI platform integrating automation, analytics, and decision-making across clinical, commercial, and real-world domains, with additional features expected by Q4 2026.

- January 2026: Veeva Systems announced Veeva eSource, a SiteVault application enabling direct data capture, EHR-to-EDC transfer, and paperless processes, set for early adopter availability in the second half of 2026.

- November 2025: Citeline launched Cohort SmartBuilder in Japan, a tool leveraging 7.4 billion tokenized real-world data points to help development teams assess eligibility criteria impacts during protocol design.

Global Clinical Trials Matching Software Market Report Scope

As per the scope of the report, clinical trials matching software is a specialized technology platform that uses algorithms and data analytics to connect patients with suitable clinical research studies. It evaluates patient data against stringent study criteria to speed up recruitment and improve access to experimental treatments.

The clinical trials matching software market is segmented by deployment mode, application, end-user, and technology. By deployment mode, the market includes cloud-based and on-premise solutions. By application, the market is segmented into patient recruitment and pre-screening, trial feasibility assessment, site selection and activation, protocol matching and eligibility screening, and patient engagement and retention support. By end-user, the market is categorized into pharmaceutical and biotechnology companies, contract research organizations, medical device companies, hospitals and health systems, and others. By technology, the market is segmented into artificial intelligence, machine learning, natural language processing, big data analytics, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Cloud-Based |

| On-Premise |

| Patient Recruitment and Pre-Screening |

| Trial Feasibility Assessment |

| Site Selection and Activation |

| Protocol Matching and Eligibility Screening |

| Patient Engagement and Retention Support |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations |

| Medical Device Companies |

| Hospitals and Health Systems |

| Others |

| Artificial Intelligence |

| Machine Learning |

| Natural Language Processing |

| Big Data Analytics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Application | Patient Recruitment and Pre-Screening | |

| Trial Feasibility Assessment | ||

| Site Selection and Activation | ||

| Protocol Matching and Eligibility Screening | ||

| Patient Engagement and Retention Support | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Contract Research Organizations | ||

| Medical Device Companies | ||

| Hospitals and Health Systems | ||

| Others | ||

| By Technology | Artificial Intelligence | |

| Machine Learning | ||

| Natural Language Processing | ||

| Big Data Analytics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the clinical trials matching software space in 2026?

The clinical trials matching software market size stands at USD 288.11 million in 2026 and is projected to reach USD 413.26 million by 2031 at a 12.62% CAGR.

Which region leads global demand for trial matching platforms?

North America led with 42.95% share in 2025, supported by strong EHR infrastructure, dense trial site networks, and sponsor and CRO purchasing concentration.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected 15.45% CAGR through 2031, supported by stronger digitization efforts in Japan and expansion by domestic platforms in China.

What is the largest application area for these platforms?

Patient recruitment and pre-screening held the largest share at 38.55% in 2025, because sponsors continue to focus on reducing enrollment delays and failed screening effort.

Why is NLP becoming more important in patient-to-trial matching?

NLP is becoming more important because a large part of eligibility information remains in free-text notes and reports, and the segment is projected to grow at a 14.55% CAGR through 2031.

Which end-user group is expanding the fastest?

Contract research organizations are projected to grow the fastest at a 13.77% CAGR through 2031, as sponsors increasingly outsource recruitment and expect stronger enrollment performance from CRO partners.

Page last updated on: