Clinical Trial Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Management Systems Market Analysis by Mordor Intelligence

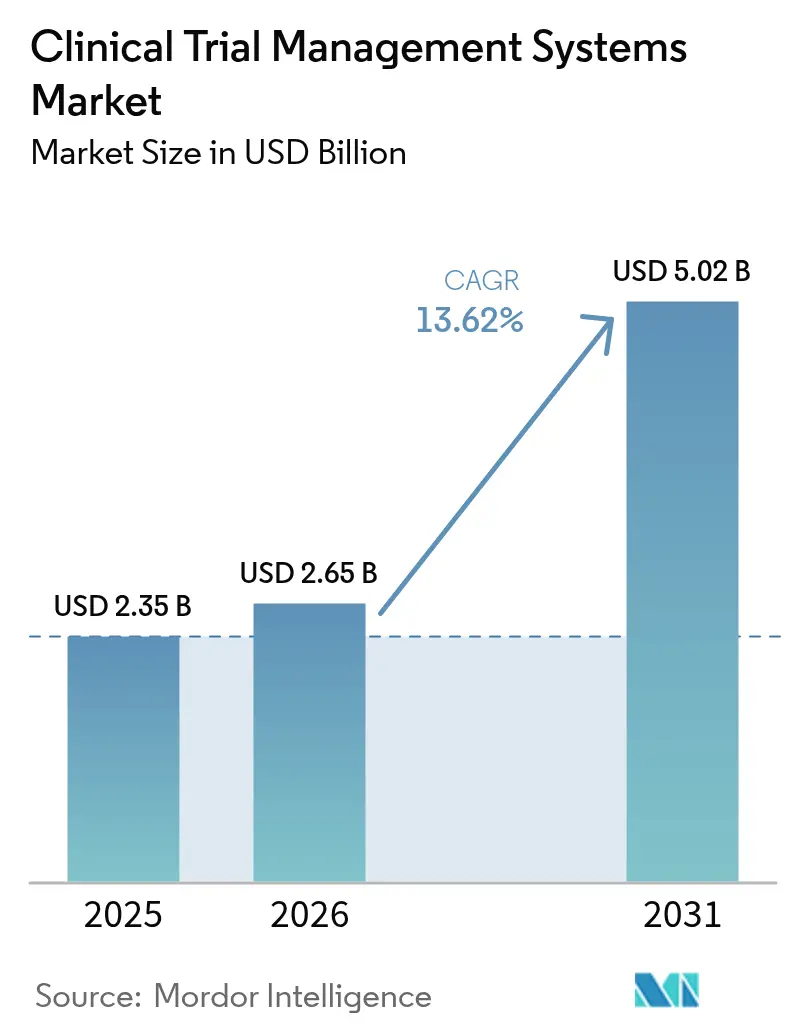

The Clinical Trial Management Systems Market size is projected to expand from USD 2.35 billion in 2025 and USD 2.65 billion in 2026 to USD 5.02 billion by 2031, registering a CAGR of 13.62% between 2026 to 2031.

Surging adoption of cloud-native platforms, expanding decentralized trial models, and new ICH-GCP E6(R3) real-time oversight mandates are accelerating investment decisions. Sponsors are consolidating disparate study tools, patient tracking, document management, and monitoring dashboards, into unified CTMS suites to cut cycle times and improve data integrity. Vendors are embedding artificial-intelligence modules that forecast enrollment risk, automate protocol-deviation alerts, and recommend corrective actions, helping sponsors protect milestone-based financing. Meanwhile, geopolitical data-sovereignty requirements are fracturing global hosting strategies, nudging multinationals toward region-specific CTMS tenants that comply with local privacy laws. Competitive intensity remains moderate as cloud newcomers challenge on-premise incumbents with usage-based pricing and rapid feature delivery cadences.

Key Report Takeaways

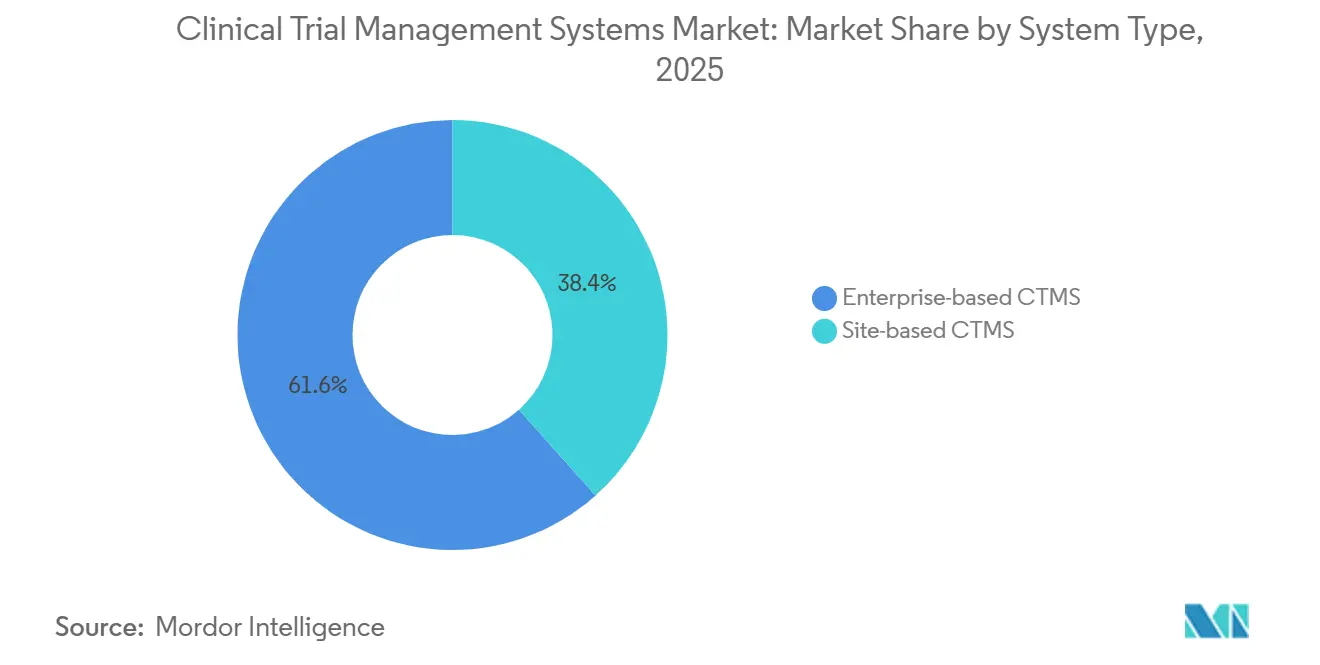

- By system type, enterprise platforms led with 61.58% of revenue in 2025, while site-based solutions are projected to expand at a 15.89% CAGR through 2031.

- By delivery mode, web-hosted deployments captured 54.66% of 2025 sales, whereas cloud SaaS is advancing at a 17.48% CAGR to 2031.

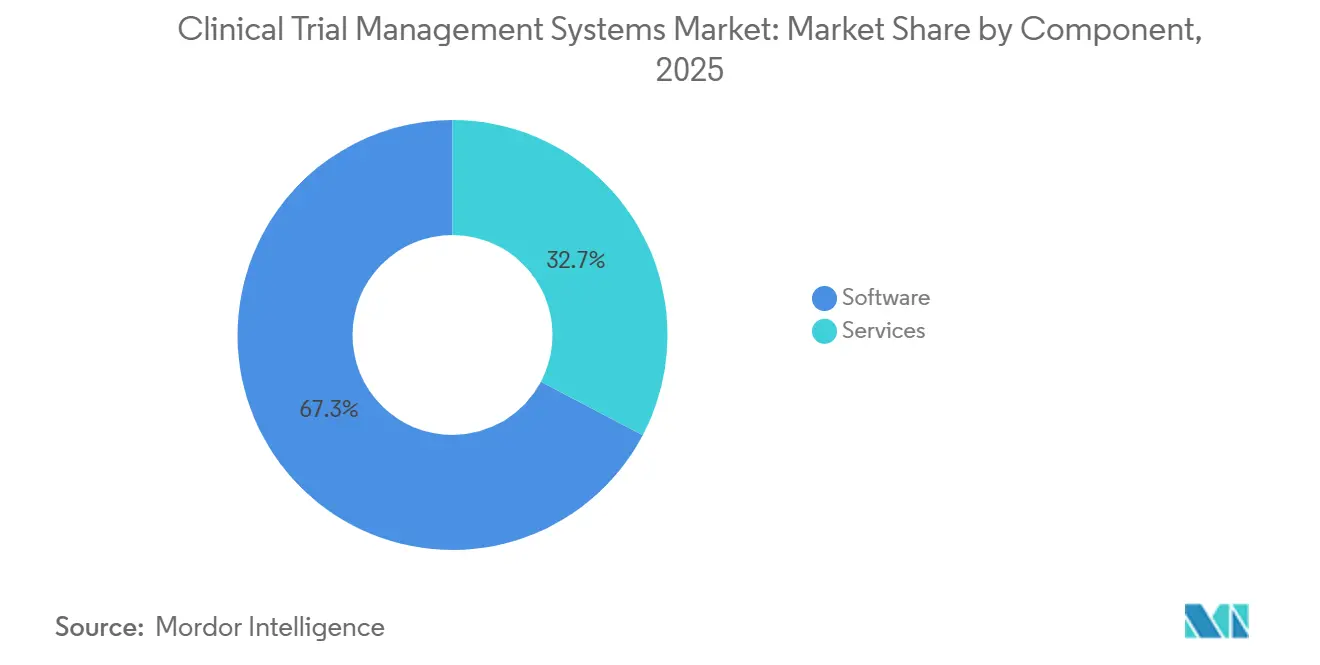

- By component, software licenses accounted for 67.27% of revenue in 2025; professional services represent the fastest-growing slice at a 16.32% CAGR over the forecast period.

- By end user, pharmaceutical and biotechnology sponsors held 39.52% of 2025 spend, while contract research organizations are on track for a 17.43% CAGR through 2031.

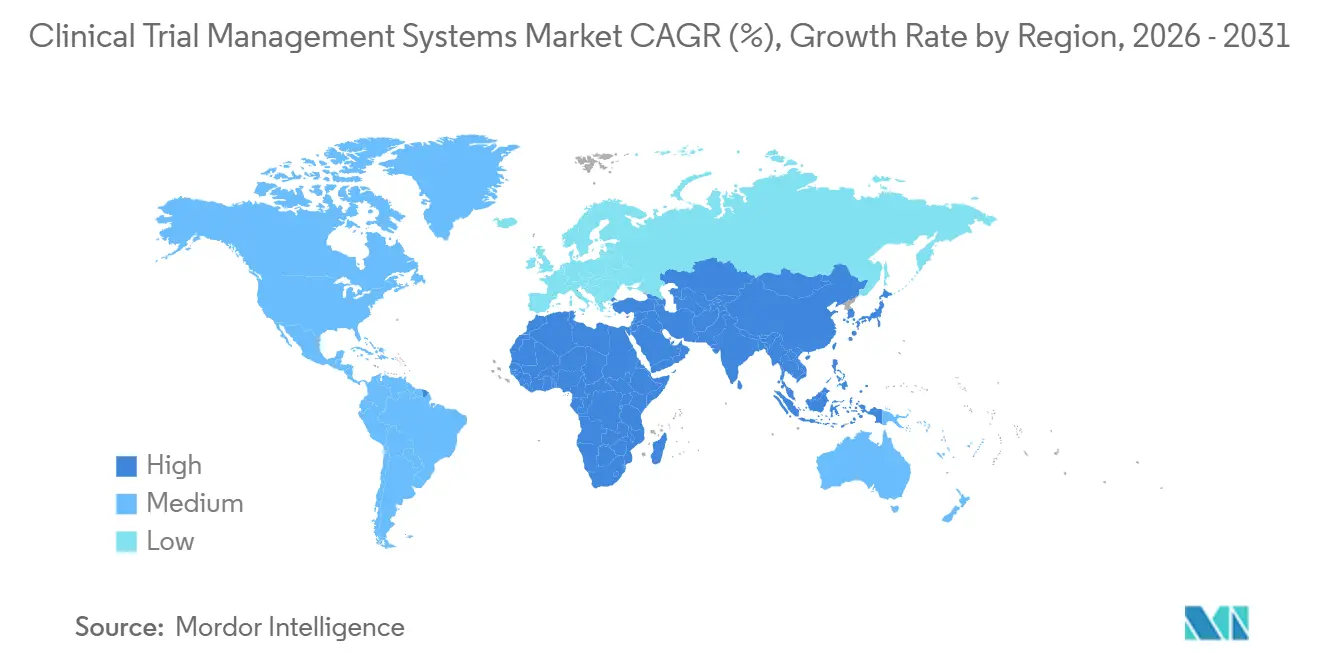

- By geography, North America commanded 49.68% of global share in 2025, yet Asia-Pacific is poised for the highest regional growth at a 15.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Clinical Trial Management Systems Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cloud-based CTMS adoption for decentralized trials | 3.2% | Global, with early traction in North America and Western Europe | Medium term (2–4 years) |

| Rising volume and complexity of global clinical trials | 2.8% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Regulatory mandates for real-time oversight (ICH-GCP E6-R3) | 2.5% | Global, led by ICH member regions (US, EU, Japan) | Short term (≤ 2 years) |

| CRO outsourcing boom among mid-size biopharma | 2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2–4 years) |

| AI-enabled predictive analytics improves enrollment velocity | 1.9% | North America and Europe, pilot deployments in Asia-Pacific | Medium term (2–4 years) |

| U.S.–China tech trade barriers pushing regional CTMS hosting | 1.1% | China, with spillover effects in APAC and select MEA markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Cloud-Based CTMS Adoption for Decentralized Trials

Decentralized designs rely on telehealth visits, home nursing, and wearable sensors, creating continuous data streams that on-premise systems cannot scale to ingest. Vendors such as Veeva report 28% year-over-year growth in Vault CTMS biotech subscriptions for fiscal 2025 as sponsors coordinate remote nursing and electronic consent workflows. FDA guidance finalized in 2024 requires auditable electronic workflows for off-site activities, a criterion best met by multi-tenant SaaS that ships version-controlled modules validated against 21 CFR Part 11.[1]Robert M. Califf, “Decentralized Clinical Trials Guidance,” U.S. Food and Drug Administration, fda.gov Oncology and rare-disease trials where eligible patients are geographically dispersed now default to cloud CTMS to curb screen-failure rates and compress enrollment timelines. These capabilities underpin the widening preference for cloud infrastructure across the clinical trial management system market.

Rising Volume and Complexity of Global Clinical Trials

Interventional registrations on ClinicalTrials.gov exceeded 480,000 by December 2025, up 9% from December 2024.[2]Rebecca J. Williams, “ClinicalTrials.gov Trends, Charts, and Maps: December 2025 Snapshot,” U.S. National Library of Medicine, clinicaltrials.gov Basket and umbrella protocols layer multiple disease cohorts into a single master protocol, driving exponential increases in task notifications, protocol amendments, and country-specific ethics workflows. Europe’s Clinical Trials Information System, fully enforced from 2024 onward, mandates structured XML uploads, a process automated by modern CTMS templates, to avoid validation errors.[3]Emer Cooke, “Clinical Trials Information System User Guide,” European Medicines Agency, ema.europa.eu As sponsors juggle 15-plus countries per phase-3 study, modular CTMS interfaces that embed multilingual informed-consent libraries and region-specific import-permit trackers have become indispensable, reinforcing demand across the clinical trial management system market.

Regulatory Mandates for Real-Time Oversight (ICH-GCP E6-R3)

The ICH issued its E6(R3) good-clinical-practice guideline in August 2024, pivoting from periodic on-site inspections toward continuous, centralized monitoring. Sponsors must now define critical-to-quality factors at study launch and surveil them in real time. CTMS suites answer this requirement by flagging protocol deviations within dashboards and auto-escalating serious adverse events to safety desks, preventing regulatory holds that can stall capital raises. Converging standards, FDA, EMA, and ISO 14155, cement CTMS as a compliance linchpin, solidifying its role inside the clinical trial management system market.

CRO Outsourcing Boom Among Mid-Size Biopharma

IQVIA’s 2025 report shows CRO revenue from biotech clients climbing 19% year-over-year, outpacing growth from large pharmaceutical companies. CROs deploy validated enterprise CTMS instances and onboard sponsor protocols via multi-tenant workspaces, spreading license and validation costs across dozens of clients. Labcorp added 1,200 new sponsor tenants during 2025, proof that variable-cost outsourcing resonates with cash-constrained biotech pipelines. This momentum places CROs among the fastest-expanding stakeholders within the clinical trial management system market.

Restraints Impact Analysis of Clinical Trial Management Systems Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and validation costs for SME sponsors | -1.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Persistent data-privacy and cross-border-transfer restrictions | -1.5% | EU (GDPR), China (PIPL), Brazil (LGPD), with global spillover | Long term (≥ 4 years) |

| Shortage of CTMS-literate clinical-ops talent in emerging regions | -1.2% | Asia-Pacific (excluding Japan), Middle East & Africa, Latin America | Medium term (2–4 years) |

| Fragmented legacy IT stacks slowing interoperability | -1.0% | Global, particularly among large pharma with decades-old EDC systems | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Validation Costs for SME Sponsors

Full-scope CTMS rollouts cost SMEs USD 0.5–2 million upfront, primarily for infrastructure, software licenses, and computer-system validation tied to 21 CFR Part 11 and EMA Annex 11. Validation commonly extends six to twelve months, during which sponsors must run duplicate paper workflows, delaying first-patient-in dates. SaaS subscriptions defer capex but escalate opex as user seats grow, limiting affordability for single-study biotechs and investigator-initiated trials. This cost drag tempers near-term penetration in the clinical trial management system market.

Persistent Data-Privacy and Cross-Border Restrictions

GDPR prohibits personal-data transfers to non-adequate jurisdictions without standardized clauses, creating carve-out CTMS instances for EU subjects. China’s PIPL compels onshore storage and security assessments before any outbound transfer. Brazil’s LGPD mirrors these requirements, and India’s Digital Personal Data Protection Act is slated to impose similar mandates once detailed rules publish. Maintaining siloed CTMS tenants inflates infrastructure complexity and slows consolidated analysis across the clinical trial management system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Clinical Trial Management Systems Market Segment Analysis

By System Type:

Enterprise Platforms Anchor Spend as Site-Based Gains MomentumEnterprise platforms accounted for 61.58% of 2025 revenue, underscoring big-pharma reliance on consolidated portfolios. These deployments integrate financial modules and quality systems to govern more than 200 concurrent trials. Conversely, site-based products are set to grow at a 15.89% CAGR through 2031 as decentralized designs hand greater autonomy to investigator sites. In oncology networks, community infusion clinics prefer lightweight CTMS that dovetail with electronic medical-record workflows, boosting vendor reach beyond the top-tier academic centers that dominated earlier procurement cycles. The clinical trial management system market size for site-based tools is projected to expand significantly as regulatory guidance now permits read-only sponsor access, lowering audit barriers. Over time, interoperability standards are likely to weave both deployment models into a single data fabric that minimizes duplicate entry.

Enterprise platforms will keep commanding budget priority for phase-3 registrational studies that involve multi-continent footprints and require uniform data visibility. Yet budget-constrained biotechs piloting first-in-human studies increasingly funnel spend toward modular, site-centric applications that go live within weeks and avoid enterprise change-control processes. As such, dual-platform coexistence will characterize the clinical trial management system market through the forecast window, with purchasing decisions hinging on trial complexity, site dispersion, and sponsor head-count scale.

By Delivery Mode:

Web-Hosted Holds the Lead, but Cloud SaaS AcceleratesWeb-hosted deployments held 54.66% of 2025 sales, a residual from early browser-based migrations. Cloud SaaS, however, is forecast to surge at 17.48% CAGR to 2031 as multitenant architectures roll out quarterly feature updates without user-side patching. The clinical trial management system market size attributed to SaaS models is expanding fastest among mid-size sponsors that lack dedicated IT staff. Regulatory guidance issued in 2024 clarified that logically segregated multitenant clouds can meet Part 11 validation if encryption, audit logging, and annual SOC 2 audits are in place, eliminating a lingering adoption barrier.

Despite the momentum, certain sponsors retain web-hosted tenants to comply with sovereign data laws that restrict cloud region choices. These hybrid patterns will persist, particularly where national regulators scrutinize foreign cloud providers. Even so, total cost-of-ownership math overwhelmingly favors SaaS, suggesting an eventual inversion in the delivery-mode revenue mix across the clinical trial management system market.

By Component:

Software Dominates, Services Outpace on GrowthLicenses captured 67.27% of revenue in 2025. Yet services, validation, integration, and training, are expanding at a 16.32% CAGR, reflecting the skills gap around risk-based monitoring and AI enrollment modules. Validation providers generate high-margin workstreams drafting traceability matrices and executing operational-qualification scripts. Sponsors also contract change-management partners to train global site staff, particularly when rolling out predictive dashboards that require statistical literacy. Consequently, the clinical trial management system market size tied to services is widening in step with platform sophistication.

Software vendors increasingly bundle consulting hours within subscription tiers, blurring traditional revenue lines. However, pure-play service firms remain pivotal when large pharma embark on multi-year migrations from legacy on-premise estates. Integration blueprints that stitch CTMS records to electronic data capture, electronic trial master file, and pharmacovigilance systems underpin the next efficiency wave inside the clinical trial management system market.

By End User:

Pharma Leads, CROs SurgePharmaceutical and biotech sponsors accounted for 39.52% of 2025 spend, reflecting their regulatory accountability and preference for direct system control. Nevertheless, contract research organizations are poised for a 17.43% CAGR through 2031 as venture-backed biotechs outsource operational heavy lifting to conserve burn rates. The clinical trial management system market size booked by CROs will therefore eclipse many single-sponsor segments over time.

Device manufacturers and academic institutes collectively supply the remainder, with digital therapeutic developers adopting CTMS to meet post-market evidence obligations. Platform trials funded by government grants are often the first adopters of adaptive-randomization features, foreshadowing broader toolchain convergence. Overall, roughly 60% of new CTMS study setups in 2026 originate from organizations that lack internal statistical programming teams, reinforcing outsourced operating models across the clinical trial management system market.

Geography Analysis

North America Clinical Trial Management Systems Market

North America retained 49.68% of 2025 revenue, anchored by dense biotech clusters in Boston, the San Francisco Bay Area, and Research Triangle Park. The FDA’s 2024 decentralized-trial guidance accelerated demand for remote-ready CTMS, and the National Institutes of Health’s USD 1.5 billion Clinical Trials Transformation Initiative funds technology modernization at academic centers, further boosting the clinical trial management system market. Canada offers 15%-plus refundable R&D tax credits, spurring cross-border study placements, while Mexico’s 2024 ethics reforms shortened site approvals, though rural broadband gaps slow site adoption.

Broader European Markets

In Europe, Germany, France, and the United Kingdom collectively host half of EU phase-3 activity. The EMA’s requirement that all submissions flow through CTIS from 2024 onward amplified CTMS auto-population features. Central and Southern European countries, including Italy and Spain, gained share by streamlining multi-site approvals, nudging wider regional uptake within the clinical trial management system market.

APAC Clinical Trial Management Systems Market

Asia-Pacific is projected to post the highest regional CAGR at 15.24% through 2031. China’s Drug Administration Law amendments and strategic goal to fulfil 50% of global innovative drug filings domestically are central catalysts. Japan expanded English-language consultation services in 2024, easing cross-border collaboration, while India’s digital trial-approval portal reaccelerated site activations post-COVID. South Korea’s cell-therapy clusters and Australia’s 43.5% refundable tax offset sustain early-phase migration into the region, positioning Asia-Pacific as the long-term volume engine of the clinical trial management system market.

Regulatory Landscape

Regulatory requirements are tightening around computerized systems validation, audit trails, and continuous oversight. This is pushing CTMS buyers toward platforms that support risk-based quality management and inspectable electronic workflows. In October 2024, the US FDA finalized guidance on Electronic Systems, Electronic Records, and Electronic Signatures in Clinical Investigations, reinforcing expectations for validation, audit trails, and trustworthy electronic records used across clinical investigations, including modern cloud and outsourced IT models.

Globally, ICH-GCP E6(R3) is reshaping operational compliance by emphasizing proactive, real-time trial oversight. The ICH Assembly adopted ICH E6(R3) Annex 2 at Step 4 in June 2026, adding updated GCP considerations for decentralized and pragmatic elements. In Canada, Health Canada began applying ICH E6(R3) in April 2026, with a six-month implementation window ending 1 October 2026. In the EU, the Clinical Trials Regulation framework and the EMA Clinical Trials Information System (CTIS) have centralized authorization workflows since 2024; sponsors still maintain their own CTMS for operational control and data handling, which increases the need for secure, compliant integration between CTIS submissions and internal study execution systems.

Value Chain Analysis

The CTMS value chain starts with infrastructure and compliance foundations, including hyperscale cloud capabilities, identity controls, encryption, audit logging, and GxP-aligned quality processes. It then moves into CTMS product development, covering core study planning, site management, budgeting, monitoring, and reporting, followed by implementation services such as computer system validation, integration, and training. Deployment and change management are typically delivered by CTMS vendors and systems integrators, while CROs act as large consolidators that operationalize CTMS across multi-sponsor portfolios. Investigative sites also increasingly become direct users through site-based and connected-site solutions.

Downstream value creation is increasingly driven by interoperability across the eClinical stack rather than standalone CTMS functionality. Integrations to EDC, eSource, eISF/eRegulatory, eTMF, and clinical supply and safety systems determine workflow automation and data quality. Partnerships reflect this shift, including the March 2026 ICON plc and Advarra collaboration to integrate CRO delivery with site technologies, including CTMS, eISF, and eSource, for a connected-site model, and the July 2025 PHARMASEAL and Viedoc integration connecting a cloud CTMS with EDC. Regulatory scrutiny on data integrity and computerized system validation, highlighted by an EMA communication in April 2026, supports service demand for validation, documentation, and inspection readiness, while data residency constraints (GDPR, PIPL, and similar regimes) increase the complexity and cost of global hosting and cross-system data transfer governance.

Competitive Landscape

The top vendors includes Veeva Systems, Oracle, IQVIA, Medidata (Dassault Systèmes), and Parexel, the market indicates moderate concentration. Cloud-native product roadmaps, seamless eClinical integrations, and therapeutic verticalization shape differentiation. Veeva cross-sells Vault CTMS into its CRM base, while Oracle leverages Clinical One’s AI patent (US11234567B2) to automate deviation detection. IQVIA exploits CRO scale to embed proprietary CTMS in turnkey outsourcing packages.

White-space opportunities exist in site-level SaaS, AI enrollment orchestration, and middleware that bridges legacy EDC schemas. Open-source entrants such as Castor EDC and OpenClinica appeal to investigator-initiated studies requiring cost sensitivity. Compliance credentials, ISO 27001, SOC 2, HITRUST, command premium pricing as regulators intensify auditing, particularly across multi-region deployments inside the clinical trial management system market.

M&A and strategic alliances continue. Medidata certified SimpleTrials as a verified partner in August 2025 to widen mid-market reach, while Veeva launched eSource in January 2026 to capture on-site data at the point of care. Partnerships between CROs and eClinical tech specialists, exemplified by Trialt and Medrio in February 2026, signal growing platform convergence trends aimed at compressing study start-up cycles and reducing total cost of ownership.

Clinical Trial Management Systems Industry Leaders

Oracle Corp.

Dassault Systmes (Medidata)

Veeva Systems

IQVIA Technologies

Parexel International

- *Disclaimer: Major Players sorted in no particular order

Clinical Trial Management Systems Market Companies Covered in this Report

- Aris Global

- Bio-Optronics (Advarra)

- Calyx

- Castor EDC

- Clario

- Dassault Systèmes

- DATATRAK International

- eClinical Solutions

- Forte Research Systems

- IBM

- IQVIA Technologies

- LabCorp

- MasterControl

- MedNet Solutions

- OpenClinica

- Oracle

- Parexel International

- RealTime Software Solutions

- Signant Health

- Veeva Systems

Read Analysis of Clinical Trial Management Systems Companies

Market Opportunities and Future Outlook

Operational automation and data unification are creating whitespace for CTMS platforms that operate as execution layers rather than only systems of record. This shows up in feasibility, site identification, and start-up orchestration needs, where sponsors look for workflow control across study start-up steps. Buyers and service providers are also pointing to measurable time compression, including Bristol Myers Squibb citing a 33% reduction in site selection to activation timelines in January 2026 after consolidating manual tracking into the Veeva Clinical Operations suite, and PSI CRO reporting in March 2026 that AI-assisted site identification shifted from weeks to minutes using an AI agent powered by the Arango Contextual Data Platform. Together, these examples support demand for CTMS-adjacent knowledge layers, governed automation, and integrations that connect historical protocol and site performance data with current study execution.

Compliance-driven modernization continues to steer procurement toward platforms that simplify validation and support traceable oversight across decentralized and multi-country trials. The FDA finalized guidance in October 2024 on electronic systems and signatures in clinical investigations, reinforcing requirements for reliable audit trails and validation practices that increase demand for packaged controls, prebuilt validation artifacts, and inspectable change management within CTMS programs. In Europe, the EU Clinical Trials Regulation requires the CTIS portal for applications, which reinforces the need for robust integration between regulatory submission workflows and sponsor or CRO operational CTMS, especially as CTIS capabilities expand, including safety-related module development. Vendors are primarily targeting configurable integration middleware, site-facing SaaS that reduces administrative load at investigative sites, and AI governance features that align automation with GCP inspection readiness.

Recent Industry Developments in Clinical Trial Management Systems Market

- July 2026: Medidata expanded its strategic partnership with CRIO to integrate site-level eSource directly with the Medidata Platform, enabling more automated data flow between research sites and sponsors. The update targets manual transcription and reconciliation work that slows decentralized and multi-site execution, strengthening the linkage between site workflows and enterprise trial oversight.

- May 2026: Veeva Systems announced Veeva Falcon, an agentic AI platform aimed at automating drug development workflows, including high-volume content intake and processing across clinical operations functions. The announcement points to a shift in CTMS ecosystems toward governed automation capabilities that complement operational tracking and compliance controls.

- October 2024: The US FDA finalized guidance on Electronic Systems, Electronic Records, and Electronic Signatures in Clinical Investigations, clarifying expectations for validation, audit trails, and reliable electronic records used in regulated clinical work. The update raised the compliance bar for CTMS and adjacent eClinical software, increasing emphasis on inspectable controls in cloud and outsourced technology environments.

Clinical Trial Management Systems Market Report Scope and Research Methodology

Market Definition and Coverage

For this report, the clinical trial management system (CTMS) market covers purpose-built software used to plan, run, track, and report clinical trial operations, along with closely linked implementation and support services, across sponsors, CROs, and trial sites worldwide.

Scope exclusions: We do not count stand-alone EDC, stand-alone eTMF, or generic project-management tools, so revenue is not double-counted across adjacent clinical-trial software categories.

Segments Covered in This Report

- By System Type

- Enterprise-based CTMS

- Site-based CTMS

- By Delivery Mode

- Web-based (Hosted) CTMS

- Cloud-based (SaaS) CTMS

- On-premise CTMS

- By Component

- Software

- Services

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Medical Device Manufacturers

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map demand and compliance needs in trial operations, and to sanity-check adoption signals across regions. We referred to public sources such as the U.S. FDA databases and guidance pages, the NIH ClinicalTrials.gov registry, EMA clinical trial regulation updates, and OECD health and R&D indicators to understand trial activity, sponsorship mix, and geographic momentum.

To translate those activity signals into a market model, we also reviewed company annual reports, investor presentations, product documentation, and credible press coverage that discussed deployments, partnerships, and contract wins. In addition, paid subscriptions focused on company financials and patent intelligence were used to connect vendor revenue exposure and feature focus back to CTMS workflows. The specific desk sources listed here are illustrative only, and we consulted many other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what counts as CTMS revenue in practice and how pricing is structured across cloud and on-premise deployments, including how services are bundled. We spoke with sponsors, CRO-side operations leaders, and site-level administrators across APAC, EMEA, and the Americas so assumptions on adoption timing, contract lengths, and module attach rates could be corrected before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 21% | Managers: 56% | Americas: 24% |

Market-Sizing & Forecasting

Sizing started with a top-down build where global trial activity and operational digitization signals were used to reconstruct the addressable CTMS demand pool by region, and then converted to revenue using typical deployment and pricing patterns reported by practitioners. After that backbone was set, totals were cross-checked with selective bottom-up approximations, including sampling vendor revenue exposure to CTMS, reviewing public contract cues, and testing sampled average contract values against estimated customer counts.

Key inputs that moved the model included clinical trial starts and active trials, sponsor versus CRO execution mix, the share of multi-country studies, cloud migration pace for trial operations, and the expected level of monitoring intensity and compliance reporting per trial. For forecasts, scenario analysis was used because adoption can shift quickly with regulatory timelines, sponsor budget cycles, and decentralized trial practices, so those levers were adjusted based on consensus ranges gathered in interviews. Where bottom-up cues were weaker for smaller markets, we used peer-region ratios and then revalidated them through follow-up calls and consistency checks.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including trial registry trends, regional R&D spending direction, and vendor commentary on pipeline and renewals. Outliers were reviewed, assumptions were re-checked, and any large variance led to re-contact with respondents to confirm whether the change came from scope, pricing, or timing.

Before sign-off, the model goes through multi-step analyst review so unit logic, currency handling, and regional splits stay consistent with the market definition. Reports are refreshed annually, with interim updates when material events occur that can change adoption or pricing, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Global Clinical Trial Management System Market Sizing Compared With Other Published Estimates

Published CTMS market estimates can look different even when the topic label is the same, because firms do not always count the same software scope, services boundary, or deal timing. Differences also show up when one model relies more on vendor-side revenue claims, and another relies more on demand-side trial activity and adoption signals.

Clinical trial registry counts and region-wise trial momentum are the evidence that anchors Mordor Intelligence s 2025 CTMS estimate to a defined user base and an explicit CTMS-only scope (excluding stand-alone EDC and eTMF), which can shift totals versus broader clinical trial software rollups. Gaps also come from how implementation services are treated, how multi-year contracts are recognized across years, and whether cloud price uplift is assumed without primary checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.35 B (2025) | |

| Global Consultancy A | USD 1.97 B (2025) | Uses a narrower counted revenue boundary that may undercount implementation and support services attached to CTMS deployments, and the scope notes on adjacent trial software exclusions are not clearly stated in the public summary. |

| Industry Publisher B | USD 2.69 B (2026) | Reports a later base year and applies a faster growth curve, which can be driven by stronger cloud uplift and broader inclusion of trial-technology elements when explicit exclusions are not published. |

Across the three figures, the spread is mainly explained by scope edges and timing choices, not by a disagreement that CTMS adoption is increasing. By keeping the definition specific and then validating price and adoption assumptions with practitioners, the estimate stays repeatable and easier to trace back to real trial activity and purchasing behavior.

Key Questions Answered in the Report

How fast is the clinical trial management system market expected to grow through 2031?

It is projected to advance at a 13.62% CAGR from 2026 to 2031, reaching USD 5.02 billion in value.

Which delivery model is gaining the most traction?

Cloud-based SaaS deployments are expanding at a 17.48% CAGR as sponsors favor elastic scalability and automated updates.

Why are contract research organizations increasing CTMS spend?

CROs consolidate multi-sponsor workloads onto enterprise CTMS platforms, spreading license costs and accelerating study start-up, resulting in a 17.43% CAGR outlook.

What regulatory shift is driving real-time monitoring features?

The ICH-GCP E6(R3) guideline finalized in 2024 mandates continuous risk-based oversight, pushing vendors to integrate real-time deviation and safety alerting.

Which region offers the fastest growth opportunity?

Asia-Pacific, led by China, India, and South Korea, is forecast to post a 15.24% CAGR due to supportive reforms and expanding trial site infrastructure.

Page last updated on: