Precision Medicine Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

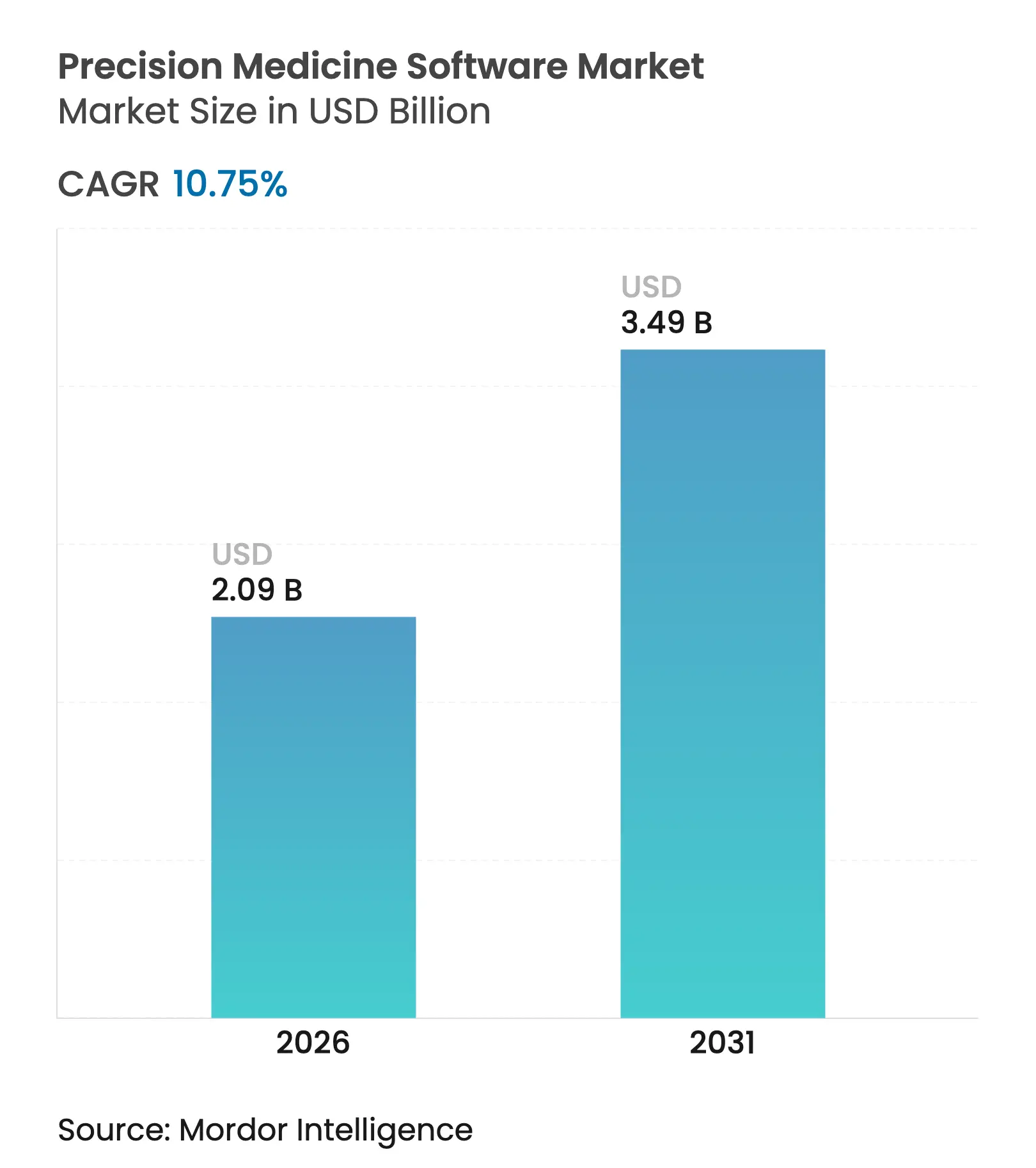

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.49 Billion |

| Growth Rate (2026 - 2031) | 10.75 % CAGR |

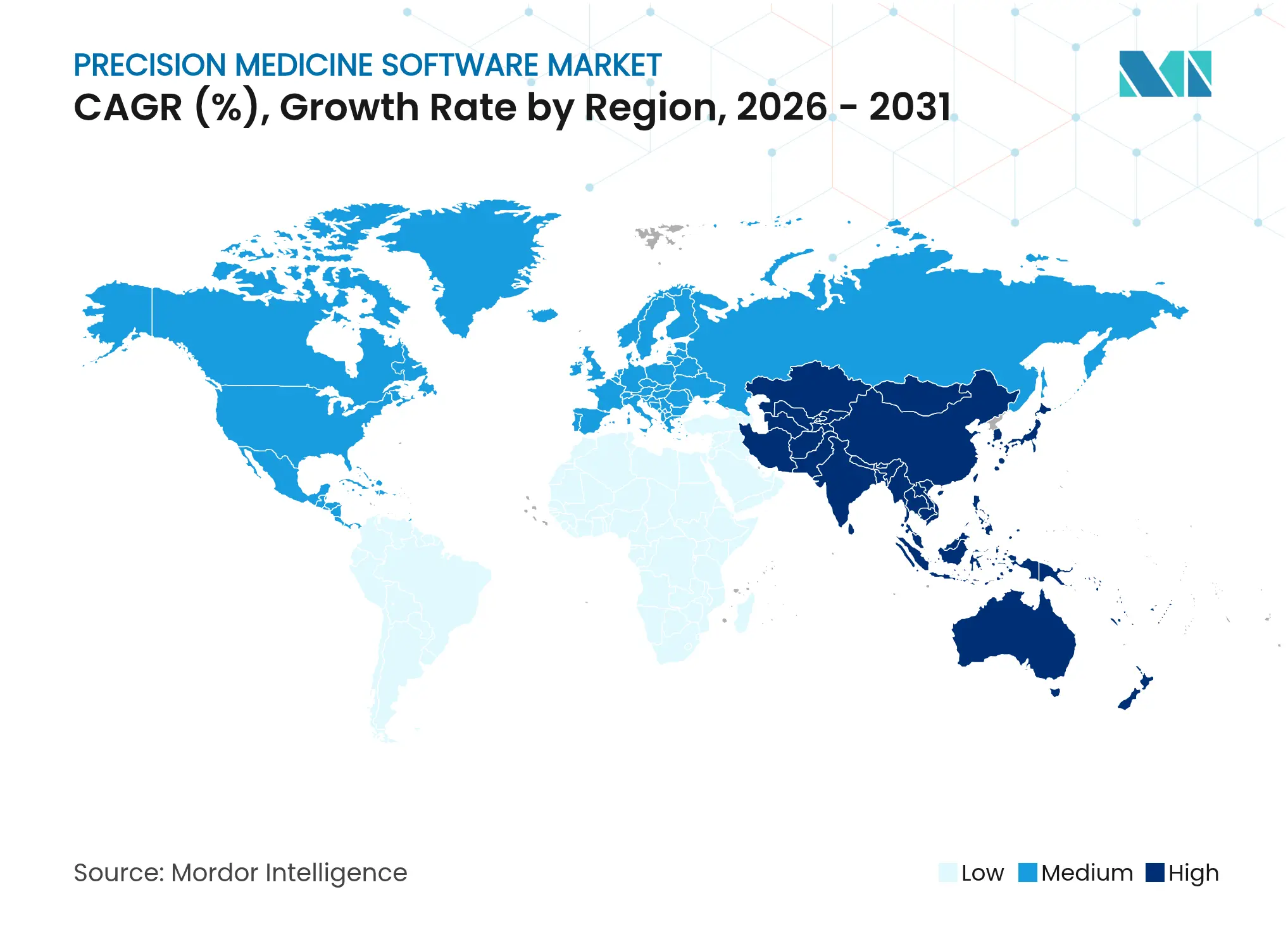

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Precision Medicine Software Market Analysis by Mordor Intelligence

The precision medicine software market size is expected to grow from USD 1.89 billion in 2025 to USD 2.09 billion in 2026 and is forecast to reach USD 3.49 billion by 2031 at 10.75% CAGR over 2026-2031. Continuous alignment of AI, genomics, and clinical workflows is transforming personalized care delivery, while sustained government genomics funding, broader reimbursement for companion diagnostics, and the rapid uptake of cloud-based deployments collectively reinforce market momentum. Oncology remains the dominant clinical application, yet rare-disease use-cases are scaling quickly on the back of AI-powered diagnostic accuracy and targeted national grants. Vendor competition is intensifying as 645 start-ups pursue novel analytics engines, digital twins, and real-world-evidence repositories, creating fertile ground for consolidation. At the same time, stringent privacy legislation and a shortage of specialized bioinformaticians keep integration costs elevated, compelling participants to balance innovation with robust compliance architectures[1]National Human Genome Research Institute, “NIH funds genomics-enabled learning health systems,” genome.gov.

Key Report Takeaways

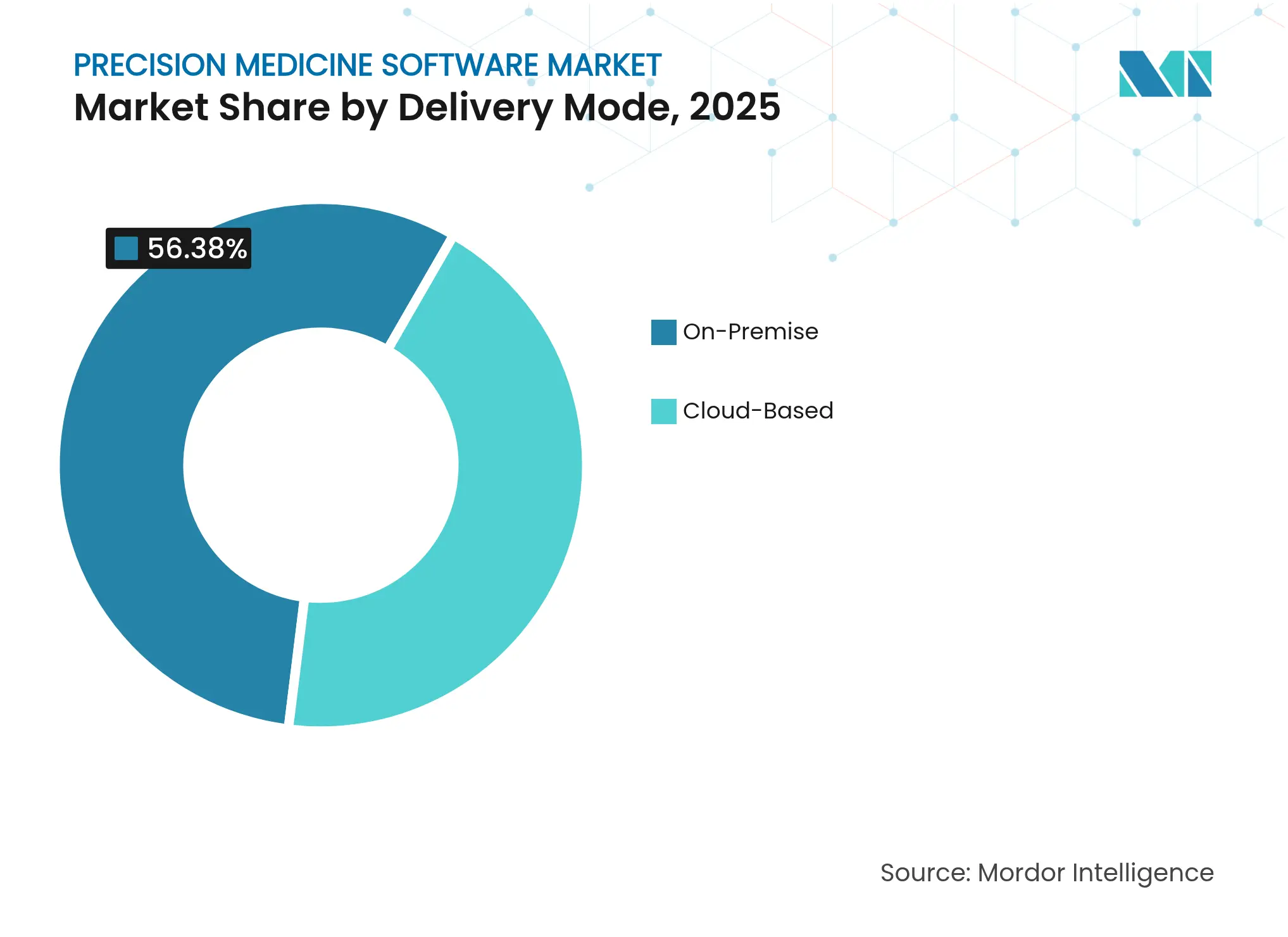

- By delivery mode, on-premise solutions held 56.38% of the precision medicine software market share in 2025, whereas cloud deployments are forecast to expand at a 12.2% CAGR through 2031.

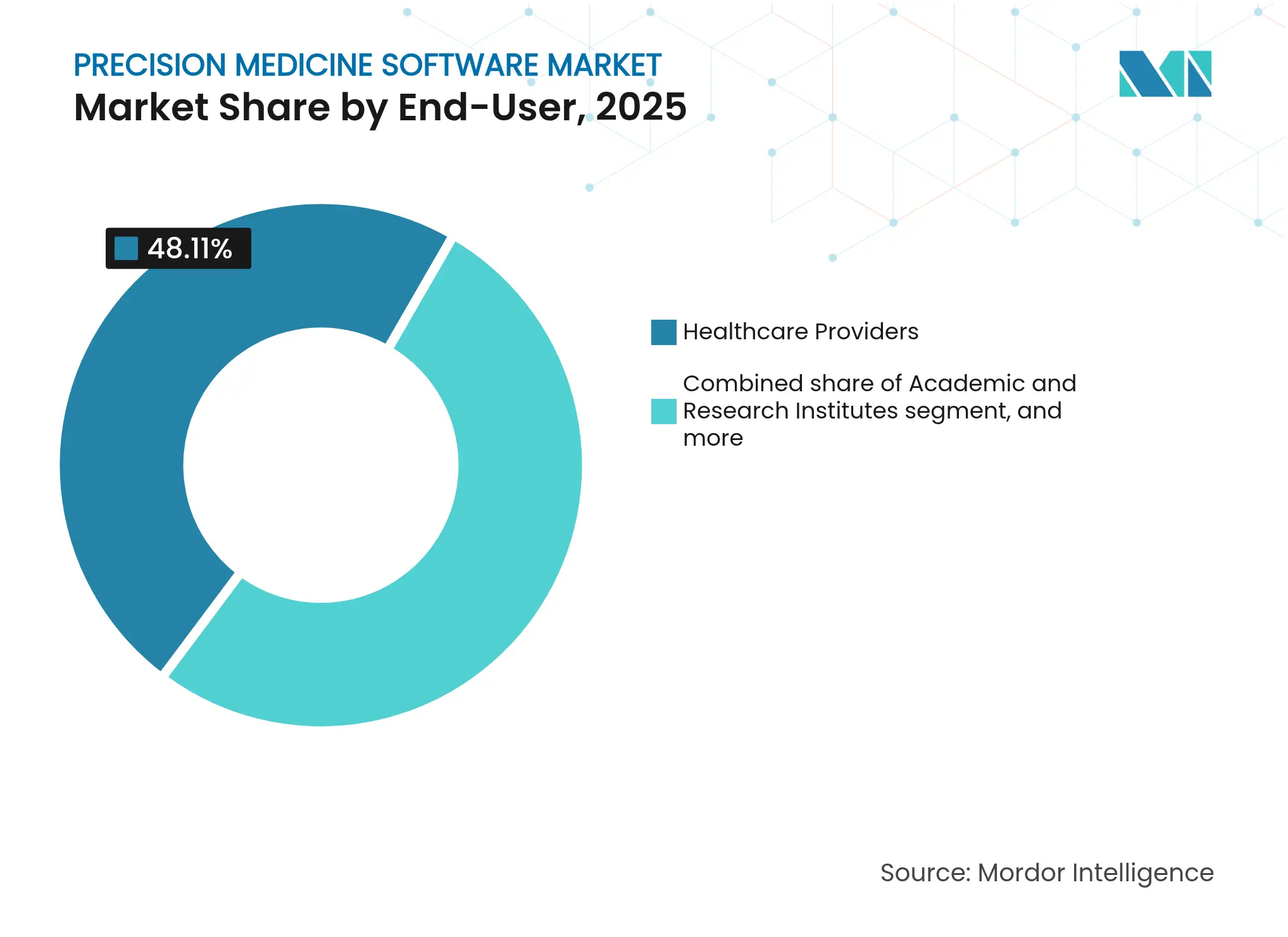

- By end-user, healthcare providers led with 48.11% share of the precision medicine software market size in 2025; pharmaceutical and biotech firms represent the fastest-growing end-user group at a 12.44% CAGR to 2031.

- By application, oncology accounted for a 51.78% share of the precision medicine software market size in 2025, while rare-disease platforms are projected to grow at 13.45% CAGR through 2031.

- By geography, North America accounted for 46.35%, whereas the Asia-Pacific is projected to grow at 11.06%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Precision Medicine Software Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising global cancer prevalence Rising global cancer prevalence | +2.8% | North America & Europe | Medium term (2-4 years) | % Impact on CAGR Forecast:+2.8% | Geographic Relevance:North America & Europe | Impact Timeline:Medium term (2-4 years) |

Accelerating government genomics funding Accelerating government genomics funding | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) | |||

Growing adoption of cloud-based clinical workflows Growing adoption of cloud-based clinical workflows | +1.9% | Global | Short term (≤ 2 years) | |||

Emergence of real-world evidence repositories Emergence of real-world evidence repositories | +1.7% | North America & Europe | Medium term (2-4 years) | |||

Expansion of companion diagnostic reimbursement codes Expansion of companion diagnostic reimbursement codes | +1.4% | North America & Europe | Medium term (2-4 years) | |||

Integration of multiomic digital twins in drug trials Integration of multiomic digital twins in drug trials | +1.2% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Global Cancer Prevalence

Rising incidence of cancer keeps oncology software investment front-of-mind for health systems. The US FDA has already cleared more than 40 companion diagnostics that direct therapy selection, and companion tests now support 43% of all oncology therapeutics authorized by the agency. Providers therefore prioritize platforms that merge tumor molecular profiles, treatment guidelines, and decision support into routine order entry. Adoption is reinforced by payer coverage expansion for next-generation sequencing, reaffirming oncology’s position as the anchor tenant of the precision medicine software market.

Accelerating Government Genomics Funding

Long-range public-sector initiatives continue to seed national data infrastructures. The NIH funds USD 1.6 million annually for genomics-enabled learning health systems, the UK’s Life Sciences Sector Plan deploys more than USD 2 billion to advance precision medicine[2]UK Government, “Life Sciences Sector Plan,” gov.uk, and Australia earmarked USD 500.1 million for its Genomics Health Futures Mission. Such allocations drive common data standards and procurement programmes that favour vendors offering secure, interoperable architectures.

Growing Adoption of Cloud-Based Clinical Workflows

Seventy-two percent of health-care executives confirm active cloud-migration roadmaps, spending USD 38 million per organisation in 2024 on hosted infrastructure. Elastic compute is indispensable for population-scale genome analytics, federated learning, and digital-twin simulations that demand petascale throughput. Partner case studies show research queries collapsing from months to minutes once genetic pipelines shift off legacy servers, and new encryption frameworks now rival or exceed on-premise defences, moderating historic security concerns.

Emergence of Real-World Evidence Repositories

Multi-institutional networks built on the OMOP common-data model accelerate hypothesis generation outside traditional trials, particularly in rare diseases where patient numbers remain small. Regulator emphasis on real-world evidence for post-market surveillance and label expansion intensifies demand for audit-ready analytics, positioning integrated data-science workbenches as indispensable.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High implementation and integration costs High implementation and integration costs | -1.8% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global | Impact Timeline:Short term (≤ 2 years) |

Data privacy and cybersecurity concerns Data privacy and cybersecurity concerns | -1.5% | Global, notably EU | Medium term (2-4 years) | |||

Limited interoperability of genomic and EHR standards Limited interoperability of genomic and EHR standards | -1.3% | Global | Medium term (2-4 years) | |||

Shortage of skilled bioinformaticians and clinical geneticists Shortage of skilled bioinformaticians and clinical geneticists | -1.1% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Implementation and Integration Costs

Entry costs span USD 100,000-500,000 for baseline deployments and surpass USD 1 million for custom builds that knit genomic analytics into electronic medical records. Beyond licences, organisations fund training, infrastructure upgrades, and interface engines, with EMR integration alone averaging USD 162,000 per multi-physician practice. These outlays postpone investment decisions for mid-tier systems but can be recouped within 2.5 years where institutions achieve throughput gains and payer reimbursement for genomic tests.

Data Privacy and Cybersecurity Concerns

Genomic datasets embed immutable patient identifiers that extend to relatives, inviting rigorous consent and encryption protocols. Europe’s GDPR drives many repositories outside EU borders, limiting cross-continental data liquidity. Meanwhile, NIST’s Genomic Data Cybersecurity Framework lays out granular controls for storage, transmission, and federated analysis[3]National Institute of Standards and Technology, “Genomic Data Cybersecurity Framework,” nist.gov. Ever-tighter FDA oversight on laboratory-developed tests heightens vendor compliance spend, favouring scale players equipped with dedicated privacy engineering teams.

Segment Analysis

By Delivery Mode: Cloud Migration Accelerates Despite Security Concerns

On-premise configurations held 56.38% precision medicine software market share in 2025 thanks to direct system control and in-house governance. Yet cloud subscriptions are scaling at a 12.2% CAGR as genomics workloads and AI pipelines exceed local compute limits. Adoption is pronounced among academic centres that must share petabyte-scale datasets in real-time. Successful migrations document lower total cost of ownership, accelerated updates, and modular add-ons for federated learning. Healthcare cloud suppliers now bundle HIPAA-compliant, genomics-optimised clusters, smoothing the transition for resource-constrained hospitals.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Pharmaceutical Companies Drive Innovation While Providers Focus on Implementation

Healthcare providers commanded 48.11% precision medicine software market size in 2025, a reflection of their central role in care delivery. Pharmaceutical and biotech firms, however, record the fastest expansion at 12.44% CAGR through 2031 as they embed AI-driven cohort selection, digital twin simulations, and real-world-evidence analytics into drug pipelines. Tempus AI alone supported nearly 1,500 research programmes in the past decade, underscoring the sector’s appetite for multimodal datasets. Providers continue to prioritise point-of-care integration, demanding intuitive modules that slot seamlessly into existing EMR screens.

Note: Segment shares of all individual segments available upon report purchase

By Application: Rare Diseases Emerge as High-Growth Frontier Beyond Oncology Dominance

Oncology software retained a 51.78% slice of the precision medicine software market size in 2025, buoyed by more than 40 FDA-cleared companion diagnostics. The rare-disease segment is expanding at 13.45% CAGR, powered by AI engines such as DeepRare that hit 100% accuracy across 1,013 disorders. Government subsidies and patient-advocacy registries underpin a data-rich environment where software platforms can pinpoint novel biomarkers and shorten the diagnostic odyssey.

Geography Analysis

North America accounted for 46.35% of 2025 revenue on the strength of mature IT infrastructure, payer coverage, and continual NIH genomics grants. The FDA has authorised over 1,000 AI-enabled medical devices, signalling a responsive but demanding regulatory climate. Implementation costs, however, still curb uptake among rural networks.

Asia-Pacific posts the fastest expansion at 11.06% CAGR, catalysed by nationwide genome programmes and digital-health roadmaps. China’s precision-health sector surpassed CNY 2 trillion (USD 296 billion) in 2022, with further upside as hospitals embed AI triage engines into routine oncology care. Japan and South Korea pilot large-scale sequencing initiatives that feed home-grown algorithm vendors, while Australia channels mission-funding toward rare-disease analytics.

Europe’s progress is shaped by GDPR and divergent IT maturity across member states. The European Health Data Space aims to harmonise access and spur innovation, yet implementation timelines vary. The UK’s GBP 2.0 billion Life Sciences Plan (USD 2.5 billion) underlines regional commitment, offering a springboard for vendors that navigate privacy constraints with interoperable designs.

Competitive Landscape

Market Concentration

More than 645 precision-medicine-software start-ups operate worldwide, with the United States hosting 355 of them, underscoring a highly fragmented market structure. Incumbent analytics vendors, sequencing platform providers, and electronic-health-record suppliers compete on algorithm accuracy, depth of proprietary multiomic datasets, and compliance toolkits that ease data-privacy audits.

Consolidation is gathering pace as scale players stitch together end-to-end stacks. Tempus AI bought Ambry Genetics for USD 600 million and GeneDx acquired Fabric Genomics for USD 33 million, moves that combine established genetic-testing laboratories with AI-powered interpretation engines. The race to aggregate high-quality genomic data and real-world-evidence repositories is reshaping competitive dynamics, creating larger platforms that can offer integrated testing, analytics, and clinical-decision support under one roof.

Partnerships remain a vital route to differentiation. Illumina and Tempus AI are jointly extending AI-enabled testing beyond oncology into cardiovascular and neurological disorders, while Owkin collaborates with Servier to co-develop AI-driven therapeutics. At the same time the US FDA continues to clarify pathways for AI/ML-enabled diagnostic devices, providing regulatory certainty that encourages new entrants yet also raises the bar on technical validation and post-market surveillance requirements.

Precision Medicine Software Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina completed the GRAIL divestiture, retaining a 14.5% stake while GRAIL began independent Nasdaq trading.

- May 2025: Tempus AI posted 75.4% Y/Y revenue growth to USD 255.7 million, locking USD 200 million in licensing with AstraZeneca and Pathos development of precision medicine.

- April 2025: Illumina and Tempus AI partnered to extend genomic testing into cardiovascular and neuro-degenerative domains.

- March 2025: GeneDx launched Multiscore, an AI-driven genetic-analysis tool enhancing diagnostic precision.

- February 2025: Tempus closed its USD 375 million cash and USD 225 million equity acquisition of Ambry Genetics, expanding hereditary cancer testing.

- January 2025: Tempus introduced generative-AI functions in Tempus One, including trial-matching and prior-authorisation automation.

Table of Contents for Precision Medicine Software Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Global Cancer Prevalence

- 4.2.2Accelerating Government Genomics Funding

- 4.2.3Growing Adoption of Cloud-Based Clinical Workflows

- 4.2.4Emergence of Real-World Evidence Repositories

- 4.2.5Expansion of Companion Diagnostic Reimbursement Codes

- 4.2.6Integration of Multiomic Digital Twins In Drug Trials

- 4.3Market Restraints

- 4.3.1High Implementation and Integration Costs

- 4.3.2Data Privacy and Cybersecurity Concerns

- 4.3.3Limited Interoperability of Genomic And EHR Standards

- 4.3.4Shortage of Skilled Bioinformaticians and Clinical Geneticists

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat Of New Entrants

- 4.5.2Bargaining Power Of Buyers

- 4.5.3Bargaining Power Of Suppliers

- 4.5.4Threat Of Substitutes

- 4.5.5Intensity Of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Delivery Mode

- 5.1.1On-Premise

- 5.1.2Cloud-Based

- 5.2By End-User

- 5.2.1Healthcare Providers

- 5.2.2Academic & Research Institutes

- 5.2.3Pharmaceutical & Biotech Companies

- 5.3By Application

- 5.3.1Oncology

- 5.3.2Pharmacogenomics

- 5.3.3Rare Diseases

- 5.3.4Other Applications

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1Syapse Holdings Inc.

- 6.3.2Foundation Medicine Inc.

- 6.3.3Sophia Genetics SA

- 6.3.4Tempus Labs Inc.

- 6.3.52bPrecise LLC

- 6.3.6Fabric Genomics Inc.

- 6.3.7Velsera Inc.

- 6.3.8Human Longevity Inc.

- 6.3.9Gene42 Inc.

- 6.3.10GenomOncology LLC

- 6.3.11PierianDx

- 6.3.12NantHealth Inc.

- 6.3.13IBM Watson Health

- 6.3.14Illumina Connected Software

- 6.3.15DNANexus Inc.

- 6.3.16Navican Genomics

- 6.3.17Sunquest Information Systems

- 6.3.18LifeOmic Holdings

- 6.3.19Philips IntelliSpace Genomics

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Precision Medicine Software Market Report Scope

Precision medicine software is a healthcare technology that aims to enhance personalized medica care by examining individual patient data to deliver customized diagnostic, therapuetic and preventive recommendations. Precision medicine is significant for the determination of the patients who are at high risk of cancer, to find out the cancers in the beginning stage, diagnosis, treatment development, and its efficacy and efficiency on the patient’s body. The precision medicine software market is segmented by delivery mode, end-users, applications and geography. By delivery mode, the market is segmented into on-premise and cloud-based. By end-users, the market is segmented into healthcare providers, academic research institutes, and pharmaceutical and biotechnological companies. By applications, the market is segmented into oncology, pharmacogenomics, rare disorders, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East, and Africa. For each segment, the market size is provided in terms of USD value.