Clinical Trials Optimization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

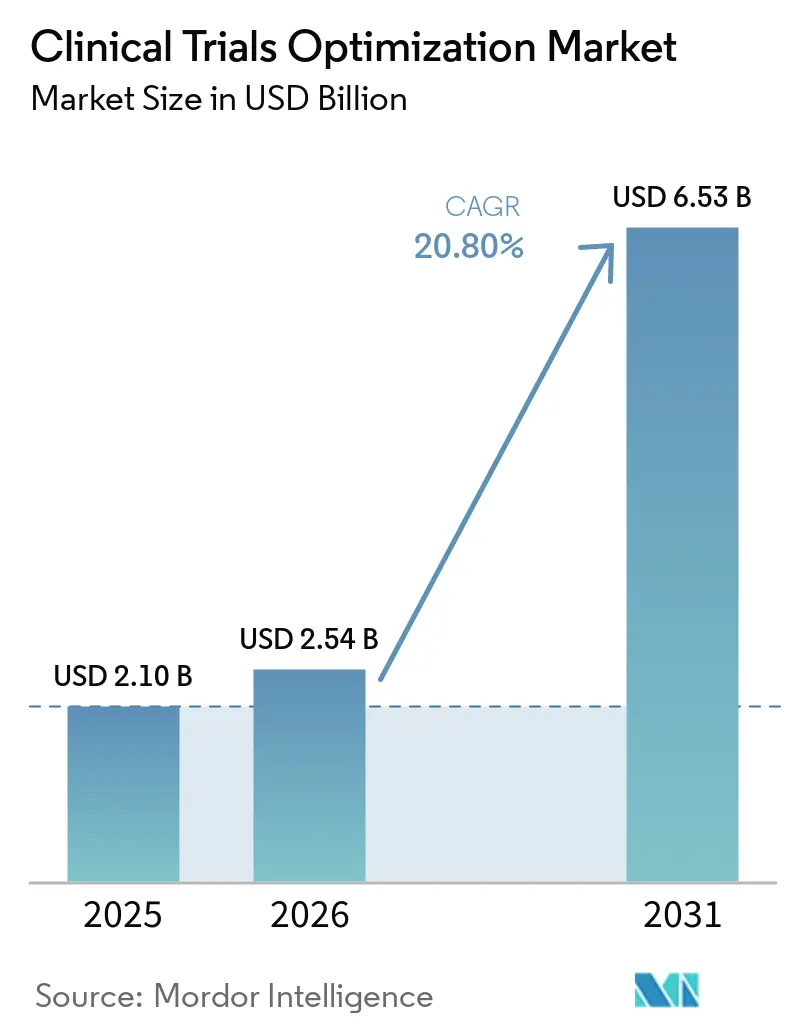

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 6.53 Billion |

| Growth Rate (2026 - 2031) | 20.80% CAGR |

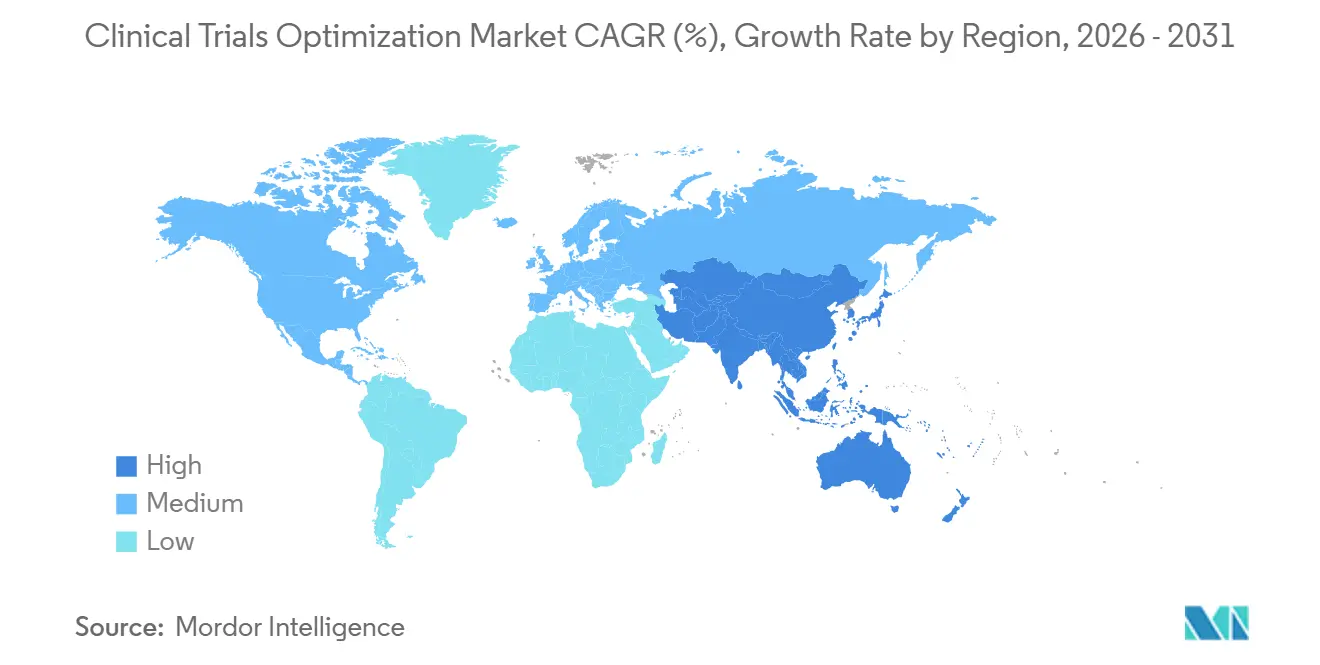

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

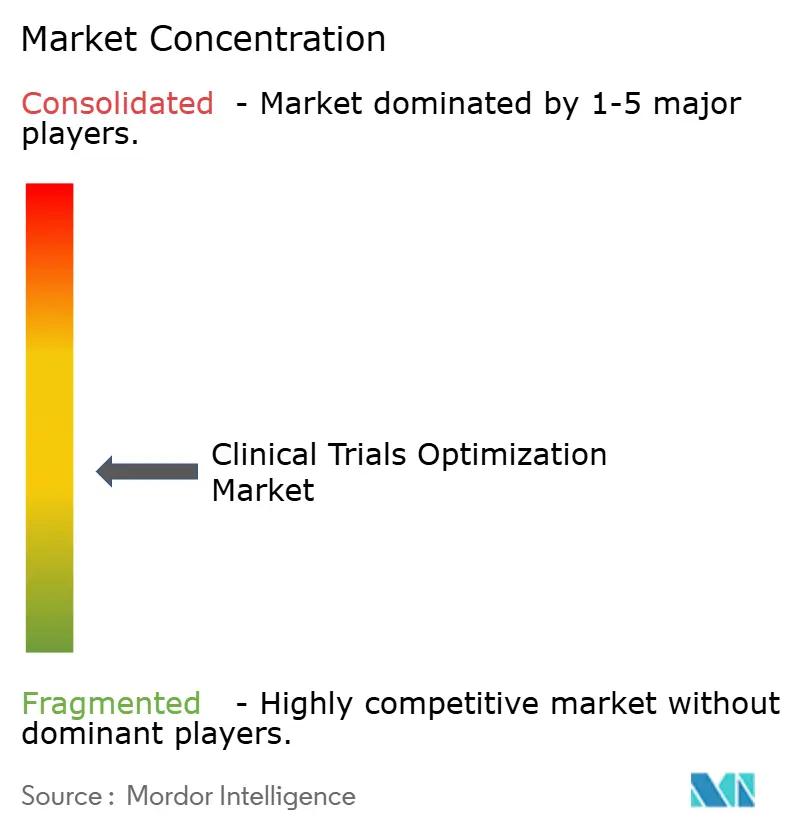

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trials Optimization Market Analysis by Mordor Intelligence

The Clinical Trials Optimization Market size is expected to increase from USD 2.10 billion in 2025 to USD 2.54 billion in 2026 and reach USD 6.53 billion by 2031, growing at a CAGR of 20.80% over 2026-2031.

Momentum stems from sponsors treating protocol design, patient recruitment, and data-science orchestration as competitive levers rather than compliance tasks. Adoption of decentralized and hybrid approaches is compressing site overhead, while artificial-intelligence (AI) analytics are lifting enrollment velocity. Outsourcing patterns are shifting toward hybrid and strategic partnerships that preserve data ownership for sponsors yet leverage contract research organization (CRO) infrastructure. The clinical trials optimization market is also benefiting from policy tailwinds Europe’s Clinical Trials Regulation (CTR) shortened cross-border approvals, the U.S. Inflation Reduction Act (IRA) incentivized larger post-marketing studies, and Asia-Pacific regulators eased decentralized-trial rules.

Key Report Takeaways

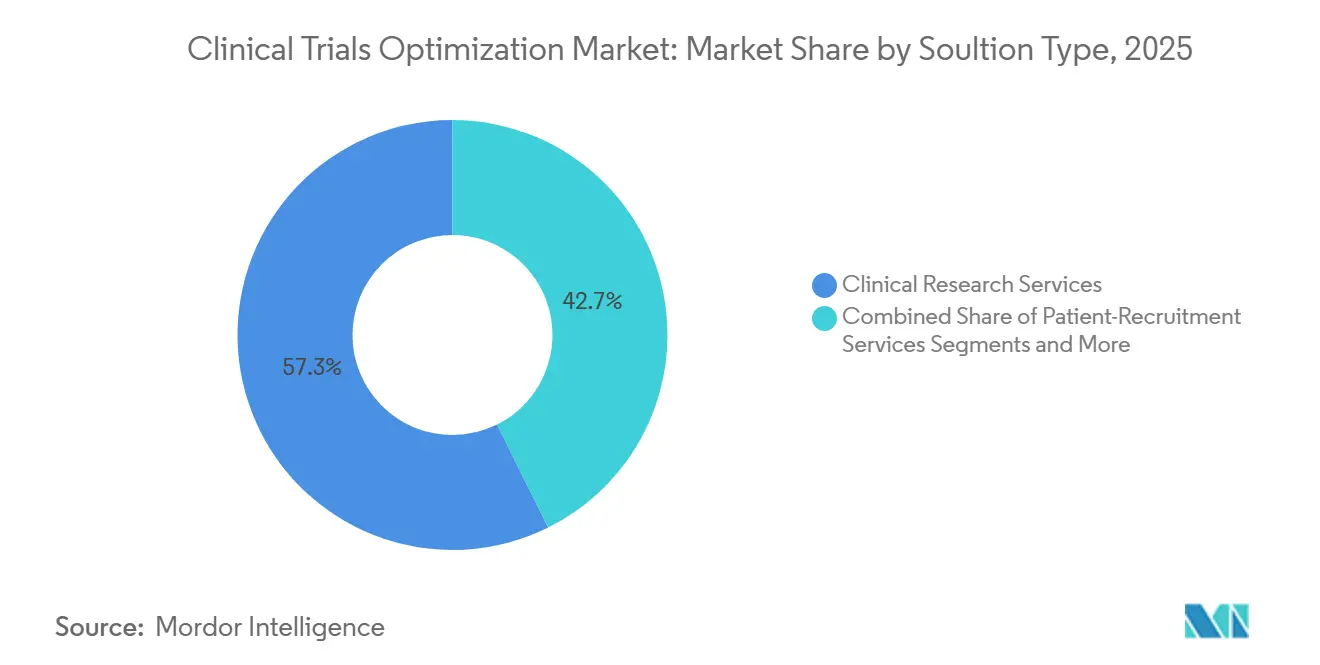

- By solution type, clinical research services commanded 57.34% revenue share of the clinical trials optimization market in 2025. Patient-recruitment services are advancing at a 21.95% CAGR to 2031, underscoring the premium sponsors attach to faster enrolment.

- By trial phase, Phase III held 48.45% of the clinical trials optimization market share in 2025, while Phase IV is forecast to grow at 22.15% through 2031 in response to IRA-mandated comparative-effectiveness evidence.

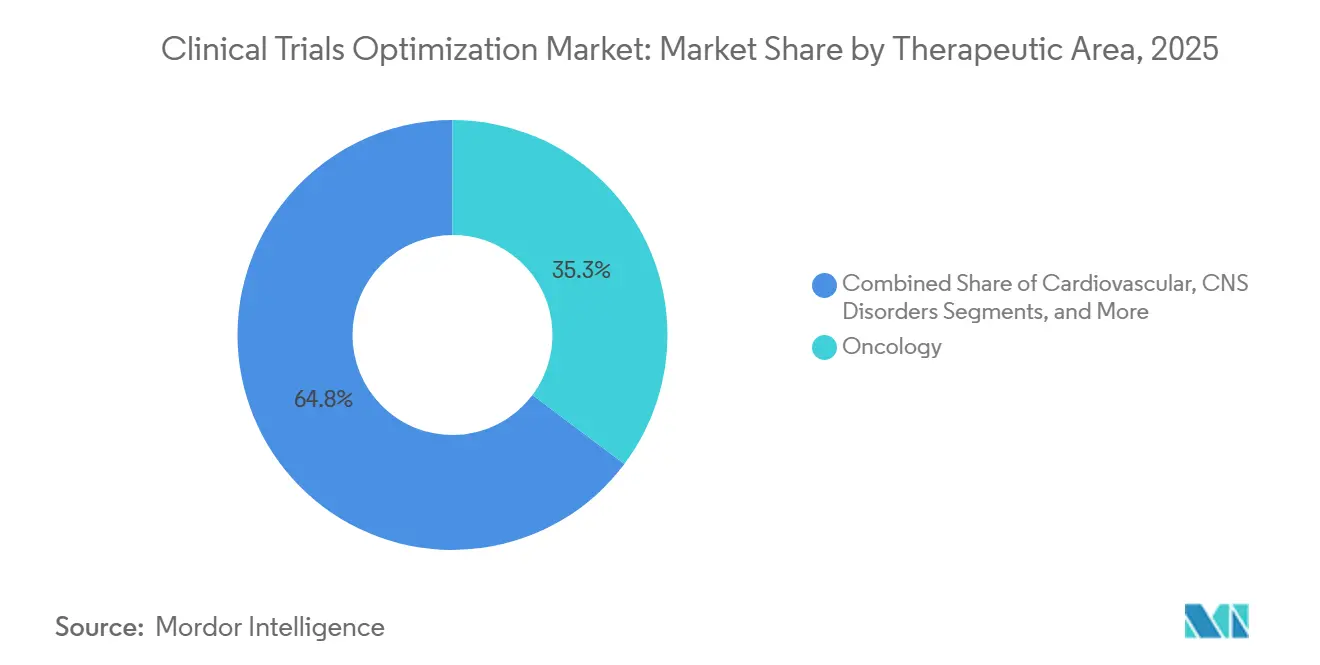

- By therapeutic area, oncology captured 35.25% of 2025 spending, whereas central-nervous-system (CNS) disorders are set to expand at a 22.45% CAGR as digital biomarkers gain regulatory clarity.

- By delivery model, full-service outsourcing accounted for 50.45% of the clinical trials optimization market size in 2025, yet hybrid and strategic partnerships are recording the highest projected CAGR at 22.76% through 2031.

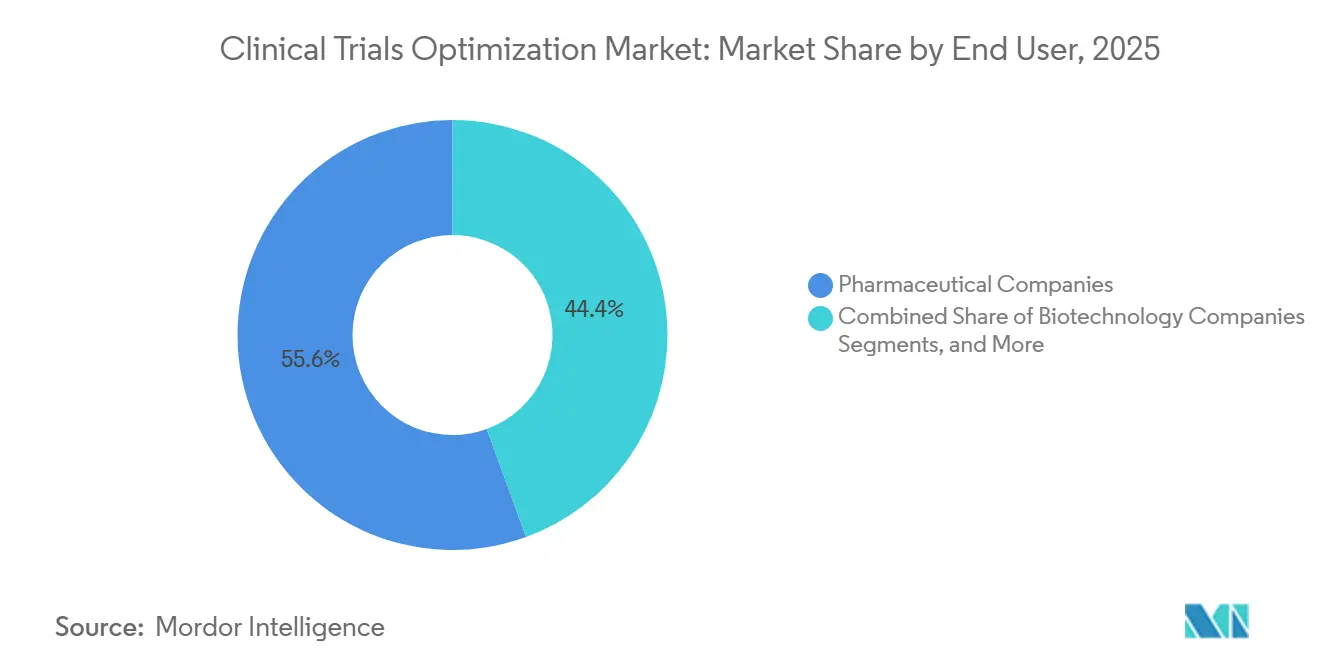

- By end user, pharmaceutical companies represented 55.56% of 2025 outlays, and biotechnology companies are forecast to rise at 22.95% through 2031 as venture capital accelerates speed-to-data-lock programs.

- By geography, North America retained 41.35% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 23.00% CAGR to 2031 on the back of Chinese and Indian regulatory reforms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trials Optimization Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Outsourcing of complex trials to full-service CROs | +4.2% | North America, Europe, global spillover | Medium term (2–4 years) |

| Adoption of decentralized and hybrid trial models | +3.8% | North America, Europe, accelerating in APAC | Short term (≤ 2 years) |

| Oncology and rare-disease pipeline expansion | +3.5% | Global; oncology in North America and China | Long term (≥ 4 years) |

| AI-driven analytics for rapid patient recruitment | +3.1% | Early adoption in North America, Europe | Medium term (2–4 years) |

| Regulatory diversity mandates boosting geo-targeted enrollment | +2.6% | Multiregional trials | Long term (≥ 4 years) |

| IRA-driven simultaneous-indication trials | +2.4% | United States only | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Outsourcing of Complex Trials to Full-Service CROs

Sponsors are increasingly outsourcing entire Phase II and Phase III programs to large CROs due to a lack of internal biometrics expertise and global site networks required for adaptive protocols. IQVIA’s 2025 partnership with Flagship Pioneering reduced time-to-first-patient-in by 30% compared to self-managed studies.[1]U.S. Food and Drug Administration, “Complex Innovative Trial Designs Pilot Program,” FDA, fda.govThe growing prevalence of oncology basket and umbrella trials has amplified the need for real-time biomarker stratification, a capability concentrated among a limited number of CROs. However, dependency risks are increasing; Eli Lilly, following a data-quality issue in 2025 with a single vendor, opted to dual-source its Alzheimer’s program between ICON and Parexel. Additionally, the FDA’s Complex Innovative Trial Designs pilot has raised technical requirements for in-house teams, further driving the outsourcing trend.

Adoption of Decentralized and Hybrid Trial Models

Decentralized trial designs, initially adopted as a pandemic workaround, have now become the standard for chronic and cardiometabolic studies. The FDA approved 127 fully remote protocols in 2025, reflecting a 3.4-fold increase from 2023. Hybrid models, which combine on-site infusions or imaging with home-based monitoring, are gaining traction in oncology.[2]IQVIA, “Flagship Pioneering Partnership Announcement,” IQVIA, iqvia.com The U.K. regulator’s approval of remote consent in January 2025 reduced enrollment timelines by 19 days across 83 studies. However, these advancements come with increased costs, as sponsors now cover patient stipends, home nursing, and device shipping, raising per-patient budgets by 15%–22% in ultra-rare trials. Regulatory acceptance remains inconsistent, with Japan’s PMDA still requiring in-person informed consent, limiting the adoption of fully decentralized trials.

Oncology and Rare-Disease Pipeline Expansion

The FDA approved 71 oncology drugs in 2025, the highest annual total, and granted rare-disease designations to 18 cancer agents.[3]Reuters, “IQVIA to Acquire Charles River Drug Discovery Assets,” Reuters, reuters.com Despite the use of AI tools, median enrollment for 300-patient Phase III solid-tumor studies extended to 26 months in 2025. In China, the NMPA approved 14 domestic oncology therapeutics, each requiring bridging trials, which increased demand for sites in the Asia-Pacific region. The IRA’s price-negotiation rules have inadvertently shifted investments toward ultra-rare indications, defined as those with fewer than 200,000 U.S. patients, due to their extended exclusivity periods.

AI-Driven Analytics for Rapid Patient Recruitment

In 2025, NIH’s TrialGPT platform demonstrated 89% accuracy in patient matching by analyzing unstructured electronic health records, reducing median screening time from 14 days to 3. IQVIA’s collaboration with Amazon Web Services in December 2025 integrated machine learning into site-selection algorithms, enabling the identification of regions based on real-time prescription patterns. However, the European Medicines Agency’s requirement for AI training dataset disclosures has slowed adoption in the EU compared to the U.S. Despite these challenges, sponsors are allocating significant budgets to external recruiters, as evidenced by the 21.95% compound annual growth rate in the patient-recruitment sub-segment, reflecting a willingness to invest in AI-enhanced enrollment solutions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented multi-country regulations | -1.8% | Europe, APAC, Latin America | Long term (≥ 4 years) |

| Shortage of experienced biometrics talent | -1.5% | North America, Europe | Medium term (2–4 years) |

| Escalating cybersecurity and privacy-compliance costs | -1.2% | Europe (GDPR), North America (HIPAA) | Short term (≤ 2 years) |

| Tariff swings on remote-monitoring hardware | -0.9% | Global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Multi-Country Regulations

Despite the guidelines set by the International Council for Harmonisation, varying evidentiary standards require sponsors to implement parallel strategies. The FDA accepts real-world evidence for label expansions, while the EMA continues to prioritize randomized data. China's requirement for 50% domestic patient enrollment has led to the creation of separate Asian arms for drugs developed in Western markets. In Japan, the restriction on remote informed consent necessitates physical site visits, even for low-risk interventions. Meanwhile, Brazil's fast-track approval process still requires translated source documents. To comply with the strictest regulatory demands, sponsors often over-enroll, increasing total trial costs by up to 25% for multiregional programs.

Shortage of Experienced Biometrics Talent

The growing adoption of adaptive design and real-world evidence integration is outpacing the available labor supply. A 2025 survey indicated that 64% of CROs are struggling to recruit senior biostatisticians, with average hiring cycles extending to 7.3 months. Rising demand has also driven a 22% increase in wages for senior biometrics staff, as reported by Medpace in 2025, which reduced operating margins by 1.4 percentage points. Limited academic programs focused on adaptive design further exacerbate the talent shortage. To address this gap, CROs are increasingly offshoring analytics to regions such as India and Eastern Europe, though this approach introduces challenges related to time-zone coordination and regulatory expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Services Retain Primacy Amid Technology Upshift

In 2025, Clinical Research Services accounted for 57.34% of total revenue, highlighting the ongoing dependence on CROs for site management, monitoring, and regulatory filings. The market for patient-recruitment services in clinical trials optimization is projected to reach USD 1.79 billion by 2031, driven by AI platforms that streamline screening timelines. Even with the rise of data platforms, sponsors continue to prioritize human judgment for protocol amendments and risk-based monitoring. The clinical trials optimization market is also responding to IQVIA’s 2026 strategy to integrate Charles River Laboratories, targeting comprehensive end-to-end demand.

Patient-Recruitment Services, set for a robust 21.95% CAGR, focus on accurately matching diverse populations, in line with regulatory diversity requirements. While decentralized-trial technology remains a niche outside North America, Japan and China's reluctance on remote consent has limited its adoption. However, the implementation of CTR in Europe has reduced administrative hurdles, encouraging sponsors to adopt tech-driven oversight. Sponsors with post-marketing commitments are increasingly turning to data-analytics platforms to integrate claims, electronic records, and patient-reported outcomes, a trend expected to gain momentum through 2031.

By Trial Phase: Post-Marketing Surveillance Rises in Strategic Importance

In 2025, Phase III trials accounted for 48.45% of expenditures, solidifying their role as the gateway to licensure. Yet, with a projected CAGR of 22.15%, Phase IV is seeing budget expansions, driven by the IRA’s price-negotiation implications on real-world evidence. By 2031, Phase IV studies are anticipated to capture over 18% of the clinical trials optimization market share, bolstering the demand for safety-signal analytics. Sponsors are embedding biomarker expansion cohorts in Phase I oncology trials, expediting proof-of-concept timelines.

While only 31% of programs advanced from Phase II to III in 2025, a decline in attrition rates is prompting sponsors to adopt larger, multi-arm Phase II designs to mitigate risks. Accelerated approval pathways, requiring confirmatory evidence, intensify pipeline pressures and heighten the urgency for post-marketing studies. Moreover, data ecosystems, integrating payer claims and digital therapeutic outputs, are reshaping trial-phase budgets, elevating Phase IV's status from a mere compliance step to a strategic extension.

By Therapeutic Area: CNS Disorders Gain Momentum on Digital Biomarker Clarity

In 2025, oncology commanded 35.25% of therapeutic expenditures, bolstered by a record 71 approvals and the routine use of companion diagnostics. The clinical trials optimization market size for oncology is set to maintain its lead through 2031, especially with the rise of basket and umbrella designs. However, CNS disorders are on a rapid ascent, projected to grow at a 22.45% CAGR, driven by the promise of smartphone-based cognitive endpoints.

Sponsors are investing in natural-history studies for rare neurologic diseases, with the NIH allocating USD 150 million in 2025 to establish foundational datasets. Cardiovascular research is experiencing a renaissance in the era of GLP-1 agonists, as multi-center obesity trials spotlight cardiometabolic outcomes. As regulators show increased receptiveness to digital-health-generated endpoints, there's a surge in investments towards sensors and at-home assessments, seamlessly integrating with decentralized trial architectures.

By Delivery Model: Hybrid Partnerships Emerge as the Middle Ground

In 2025, full-service outsourcing (FSO) captured 50.45% of the revenue, a preferred choice for midsize biopharma firms seeking comprehensive execution. Yet, the clinical trials optimization market is witnessing a shift: hybrid and strategic partnerships are on track for a 22.76% CAGR, reflecting sponsors' inclination to retain raw patient data while outsourcing site logistics. As hybrid frameworks offer both accountability and data sovereignty, functional-service-provider contracts are losing traction.

IQVIA’s partnership with Flagship Pioneering exemplifies this trend: while IQVIA manages sites and gathers data, Flagship holds the reins on algorithmic biomarker analytics. With proprietary data lakes guiding future label expansions and payer discussions, sponsors are hesitant to relinquish data assets to vendors. This shift in power dynamics is birthing new service tiers—modular analytics, oversight of decentralized operations, and cloud-centric regulatory rooms—expanding revenue avenues for tech-savvy CROs.

By End User: Biotechs Outpace Large Pharma in Growth Trajectory

In 2025, pharmaceutical companies accounted for 55.56% of expenditures, driven by robust pipelines and established master-service agreements. In contrast, venture capital-backed biotech firms are emerging as the fastest-growing segment, boasting a projected CAGR of 22.95% through 2031. Biotechs are prioritizing speed to data lock, often leaning towards hybrid partnerships to expedite their timelines.

In 2025, biotech financing hit a record USD 28 billion, predominantly channeled into oncology and rare-disease ventures, amplifying the demand for adaptive designs and a global site presence. Additionally, medical-device manufacturers are ramping up trial budgets, responding to stringent U.S. device regulations that necessitate post-market surveillance, thereby creating a spillover demand for CROs adept in real-world evidence.

Geography Analysis

In 2025, North America accounted for 41.35% of global revenue, driven by the FDA's Complex Innovative Trial Designs pilot, which accelerated 89 adaptive submissions, and the NIH's TrialGPT, which reduced oncology recruitment time by 22%. The U.S. leads the market, contributing 48% of global pharmaceutical R&D spending, supported by extensive electronic health record adoption that enhances AI-driven site-selection algorithms. The implementation of IRA price negotiations in 2026 is prompting sponsors to consolidate multiple indications into single protocols, increasing complexity while boosting contract value.

Asia-Pacific is projected to achieve a strong 23.00% CAGR through 2031. This growth is supported by China's 2025 approval of 47 decentralized protocols and the relaxation of local-trial requirements for ICH-approved drugs, which has reduced cross-border timelines by 40%. In India, fast-track processes have cut approval times for cardiovascular and diabetes treatments from 18 months to just 90 days. Japan's consultation initiative aims to address the longstanding "drug lag," although restrictions on remote consent continue to limit full decentralization. Emerging participation from Southeast Asian sites is expanding patient access and improving ethnogeographic diversity in oncology and metabolic studies.

Europe experienced a significant recovery following the 2025 enforcement of the Clinical Trials Regulation (CTR), which reduced the multistate approval process from 18 months to 106 days. Germany, the U.K., France, Italy, and Spain accounted for 68% of trial initiations, although variations in GDPR interpretations have increased per-patient compliance costs by 12% to 18% compared to U.S. studies. Eastern European countries offer cost-effective options for CNS and rare-disease research, though challenges such as language barriers and data custody regulations persist. The Middle East and Africa, while still developing, are expanding; Saudi Arabia has committed USD 1.2 billion to establish 15 trial sites under its Vision 2030 initiative, and the UAE has tripled interventional approvals. In South America, Brazil has made notable progress with fast-tracked approvals for dengue and Chagas, although Argentina's document-translation requirements continue to extend timelines.

Competitive Landscape

The clinical trials optimization market remains moderately fragmented, with the top five CROs capturing approximately 38% of the 2025 revenue. Leading players differentiate themselves through AI-powered recruitment engines, decentralized trial platforms, and global regulatory advisory services. Mid-tier CROs are focusing on specialized areas such as oncology and rare diseases.

Technology investments have become a critical competitive factor. NIH's TrialGPT demonstrated an impressive 89% matching accuracy, prompting commercial CROs to develop or license comparable models. The ISO 27001 cybersecurity certification, now mandatory in 14 countries, can cost facilities up to USD 3.5 million, favoring established players with strong financial resources. Meanwhile, emerging disruptors are driving innovation through virtual trials, reducing per-patient costs by up to 40%. However, strict on-site oversight regulations in Japan and China limit immediate scalability.

Significant opportunities remain in underexplored areas such as pediatrics, low- and middle-income countries, and post-marketing surveillance, where incumbent players have limited focus. Consolidation trends continue to shape the market: In May 2026, Parexel acquired AI pharmacovigilance firm Vitrana, and earlier in the year, Worldwide Clinical Trials acquired Catalyst Clinical Research to expand its early-phase capabilities. These strategic mergers and acquisitions aim to deliver integrated Phase I-IV services, meeting the biotech industry's demand for streamlined, single-vendor solutions.

Clinical Trials Optimization Industry Leaders

IQVIA

ICON plc

Syneos Health, LLC

WuXi AppTec Co., Ltd.

SGS SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Parexel acquired Vitrana, integrating AI-powered pharmacovigilance to automate adverse-event coding.

- February 2026: Worldwide Clinical Trials purchased Catalyst Clinical Research, adding 12 Phase I units across North America.

- February 2026: IQVIA agreed to acquire Charles River Laboratories’ discovery assets to deliver end-to-end services.

- February 2026: Duke Clinical Research Institute and IQVIA launched a collaboration to enroll 15,000 cardiometabolic patients across 200 U.S. sites.

- January 2026: WEP Clinical bought Siron Clinical, strengthening European early-phase oncology capabilities.

Global Clinical Trials Optimization Market Report Scope

As per the scope of the report, clinical trial optimization is the strategic use of data analytics, artificial intelligence (AI), and streamlined workflows to improve the efficiency, speed, cost-effectiveness, and success rates of clinical research. It involves refining trial design and execution from feasibility to data submission to reduce patient dropout, speed up recruitment, and enhance data quality.

The clinical trials optimization market is segmented by solution type, trial phase, therapeutic area, delivery model, end-user, and geography. By solution type, the market includes clinical research services, data & analytics platforms, patient recruitment services, decentralized/virtual trial technology, and regulatory & medical affairs services. By trial phase, the market is segmented into Phase I, Phase II, Phase III, and Phase IV/post-marketing. By therapeutic area, the market is categorized into oncology, cardiovascular, CNS disorders, infectious diseases, and metabolic & endocrine. By delivery model, the market is segmented into full-service outsourcing (FSO), functional service provider (FSP), and hybrid/strategic partnership. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, medical device manufacturers, and academic & research institutions. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Clinical Research Services |

| Data & Analytics Platforms |

| Patient-Recruitment Services |

| Decentralised / Virtual Trial Technology |

| Regulatory & Medical Affairs Services |

| Phase I |

| Phase II |

| Phase III |

| Phase IV / Post-Marketing |

| Oncology |

| Cardiovascular |

| CNS Disorders |

| Infectious Diseases |

| Metabolic & Endocrine |

| Full-Service Outsourcing (FSO) |

| Functional Service Provider (FSP) |

| Hybrid / Strategic Partnership |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical-Device Manufacturers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Clinical Research Services | |

| Data & Analytics Platforms | ||

| Patient-Recruitment Services | ||

| Decentralised / Virtual Trial Technology | ||

| Regulatory & Medical Affairs Services | ||

| By Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV / Post-Marketing | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular | ||

| CNS Disorders | ||

| Infectious Diseases | ||

| Metabolic & Endocrine | ||

| By Delivery Model | Full-Service Outsourcing (FSO) | |

| Functional Service Provider (FSP) | ||

| Hybrid / Strategic Partnership | ||

| End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical-Device Manufacturers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the clinical trials optimization market by 2031?

The clinical trials optimization market size is forecast to reach USD 6.53 billion by 2031, expanding at a 20.8% CAGR from 2027 to 2031.

Which service segment is growing fastest in clinical-trial operations?

Patient-Recruitment Services lead growth with a 21.95% CAGR through 2031 as sponsors pay premiums for AI-enabled enrollment acceleration.

Why are Phase IV studies gaining importance?

The U.S. Inflation Reduction Act compels comparative-effectiveness evidence post-approval, lifting Phase IV budgets and driving a 22.15% CAGR in this phase.

Which region offers the highest growth outlook?

Asia-Pacific is set to advance at a 23.00% CAGR through 2031, helped by Chinese and Indian regulatory reforms that shorten approval timelines.

How are hybrid delivery models transforming sponsor-CRO relationships?

Hybrid and strategic partnerships allow sponsors to keep control of patient data while outsourcing site management, supporting a 22.76% CAGR for these models.

What is the market concentration level among leading CROs?

The top five CROs command roughly 38% of global revenue, translating into a moderately consolidated score of 6 on a 1-10 scale.

Page last updated on: