Clinical Trial Investigative Site Network Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

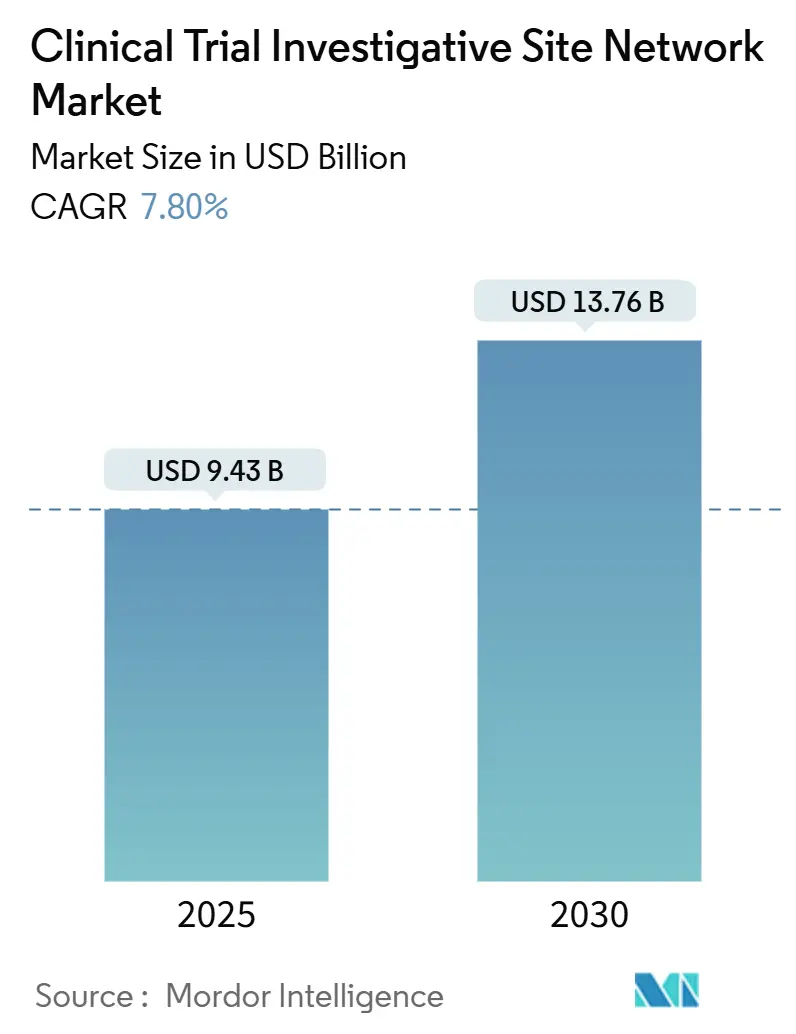

| Market Size (2025) | USD 9.43 Billion |

| Market Size (2030) | USD 13.76 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

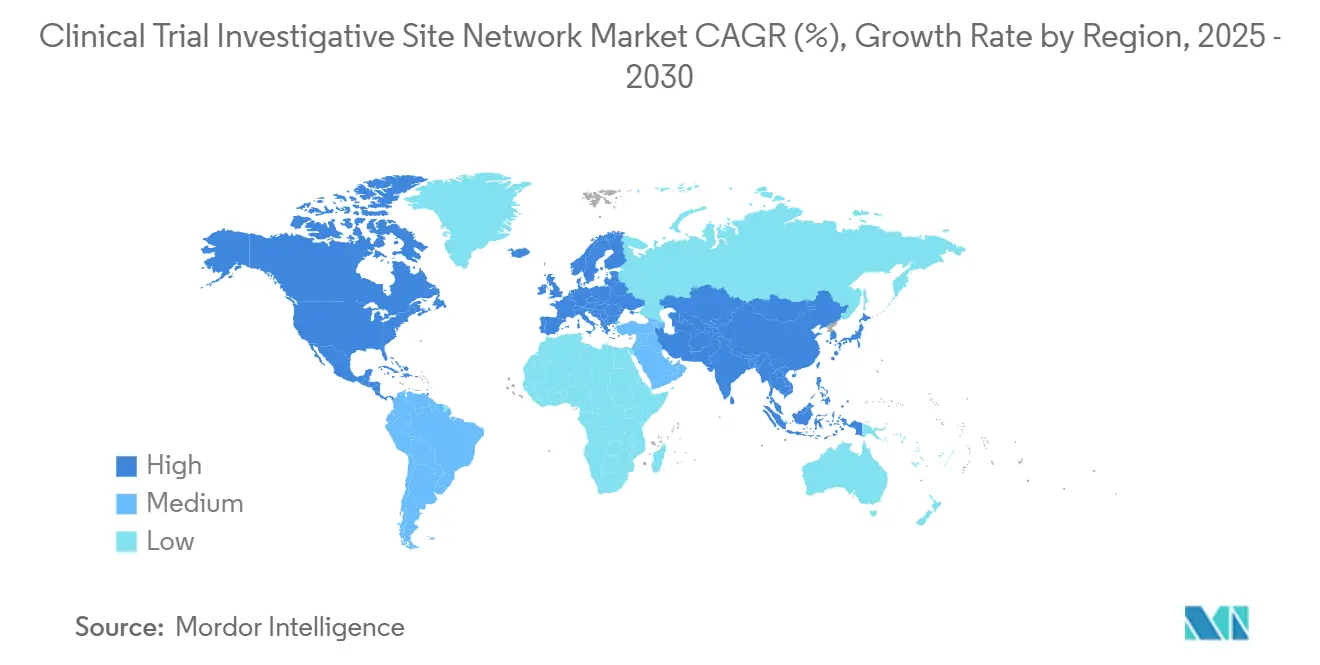

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Investigative Site Network Market Analysis by Mordor Intelligence

The clinical trial site networks market size reached USD 9.43 billion in 2025 and is projected to grow to USD 13.76 billion by 2030, registering a 7.8% CAGR during the forecast period. Sponsors are consolidating study execution within large, multi-site platforms to manage protocol designs that now routinely exceed 1 million data points, a two-fold increase over the past decade. Escalating biotech R&D expenditure of USD 161 billion in 2023 sustains steady early-phase study flow and favors networks with intensive safety-monitoring infrastructure. Retail pharmacies are entering the landscape to boost enrollment diversity, while Asia Pacific accelerates on the back of 30-40% cost savings and maturing regulatory pathways. Preferred-provider agreements between site networks and CROs are tightening capacity and driving investment in AI-driven CTMS platforms that alleviate multisystem fatigue for investigators.

Key Report Takeaways

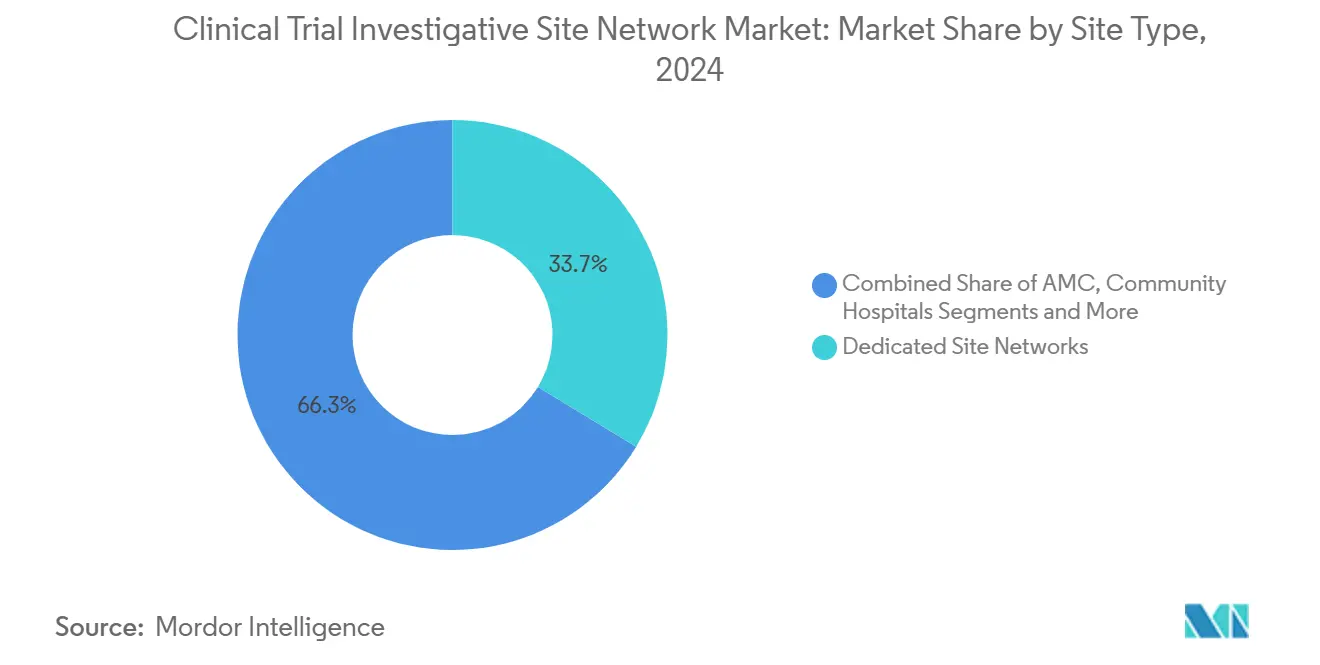

- By site type, dedicated networks captured 33.7% of the clinical trial site networks market share in 2024, while retail-health clinics are forecast to advance at a 6.8% CAGR through 2030.

- By therapeutic area, oncology retained 42.5% revenue leadership in 2024; rare and orphan diseases are expected to expand at an 8.2% CAGR to 2030.

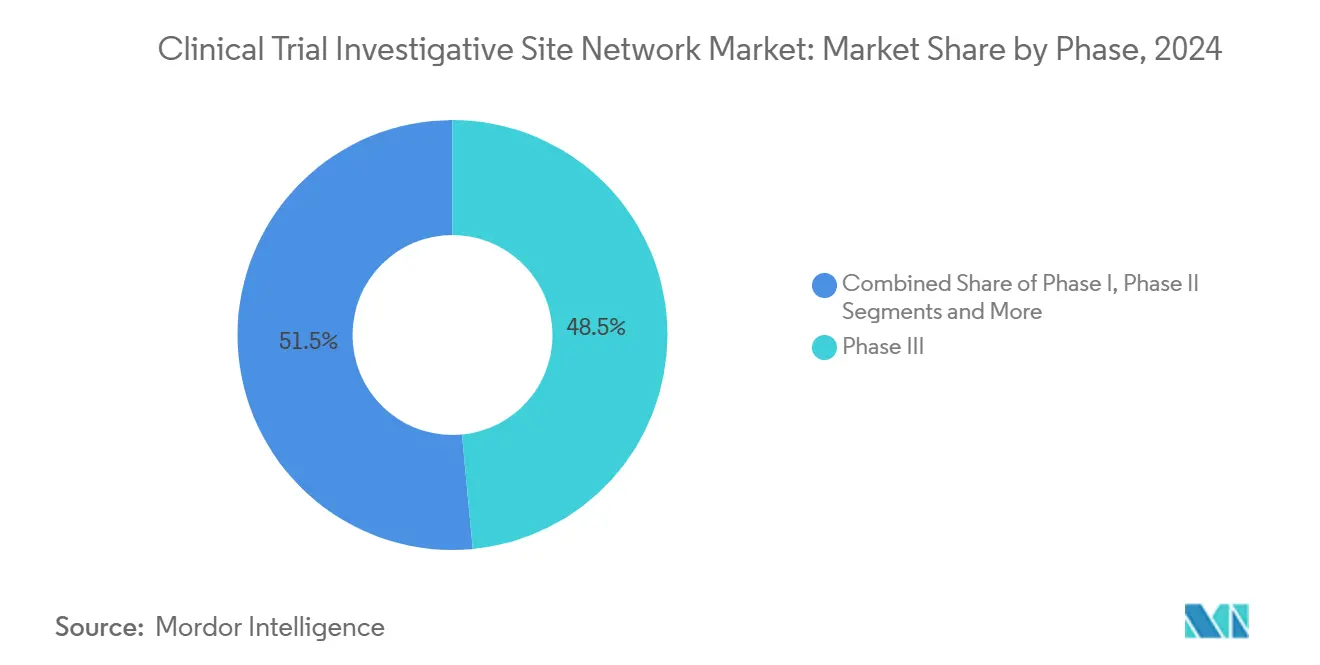

- By phase, Phase III accounted for 48.5% of the clinical trial site networks market size in 2024, whereas early- and expanded-access programs are projected to grow at 7.5% CAGR through 2030.

- By geography, North America held 42.8% revenue share in 2024, yet Asia Pacific is expected to post the fastest 8.3% CAGR to 2030.

Global Clinical Trial Investigative Site Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing protocol complexity drives demand for multi-site networks | +1.80% | North America & EU | Medium term (2-4 years) |

| Decentralized & hybrid trial models boost site-network partnerships | +1.50% | Global | Short term (≤ 2 years) |

| Rising biotech funding for early-phase studies | +1.20% | North America expanding to APAC | Medium term (2-4 years) |

| CRO consolidation prompting preferred-provider site agreements | +0.90% | North America & EU | Long term (≥ 4 years) |

| Under-served rare-disease communities seeking purpose-built networks | +0.70% | Developed markets | Long term (≥ 4 years) |

| Retail-health entrants expanding patient access | +0.60% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Protocol Complexity Drives Demand for Multi-Site Networks

Phase III protocols now require an average of 170 procedures, up from 106 in 2002. This 67% workload increase slows recruitment and lengthens cycle times, prompting sponsors to divert studies to networks with standardized procedures across multiple geographies.[1]Kenneth A. Getz, “The Impact of Bad Protocols,” ScienceDirect, sciencedirect.com Consolidated platforms spread procedural burden, curbing the USD 4-6 billion spent annually on non-core tasks. Robust quality-management systems embedded in networks also align with ICH E6(R3) traceability mandates, giving multi-site operators a compliance edge. As a result, investigative burden continues to climb 10.5% annually, reinforcing network demand.

Decentralized & Hybrid Trial Models Boost Site-Network Partnerships

Hybrid designs combining tele-visits with on-site assessments are moving from experiment to norm, with 77% of sponsors planning adoption by 2025. Digital platform usage has grown 239%, cutting dependence on fragmented tech vendors by 62%.[2]Deborah Borfitz, “Future Looks Bright for Decentralized Clinical Trials,” Clinical Research News Online, clinicalresearchnewsonline.comSite networks that integrate ePRO, remote monitoring, and community clinics report 10% faster recruitment and 400% improvement in demographic diversity. ICON’s Accellacare now connects 112 sites that serve 9 million patients, highlighting the scale benefits. Patients still prefer travel times under 1 hour for complex visits, making coordinated hybrid models attractive.

Rising Biotech Funding for Early-Phase Studies

Biotech IPOs raised USD 3 billion in 2024, channeling capital into proof-of-concept pipelines that rely on first-in-human expertise. Dedicated early-phase networks command premium fees thanks to intensive safety monitoring and biomarker analytics that mitigate the 31% protocol-uncertainty hurdle cited by sponsors. Asia Pacific’s expedited pathways in South Korea and Taiwan trim approval timelines 20-30%, encouraging geographic expansion. Phase I and II specialists increasingly pair on-site telemetry with virtual follow-ups, boosting retention in oncology and rare-disease cohorts.

CRO Consolidation Prompting Preferred-Provider Site Agreements

ICON’s USD 12 billion purchase of PRA Health Sciences exemplifies a merger wave that positions CROs to negotiate long-term capacity blocks with leading site networks. Master service agreements streamline governance, lower per-patient costs, and standardize SOPs. Networks gain steady revenue while CROs shave overhead through functional resourcing models. Technology is integral: IQVIA’s One Home for Sites consolidates credentials and training records to reduce log-in fatigue for personnel. Barriers rise for stand-alone sites lacking integrated digital infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Investigator burnout & high staff turnover | -1.40% | North America & EU | Short term (≤ 2 years) |

| Stringent data-privacy regulations | -0.80% | EU & North America | Medium term (2-4 years) |

| Rising insurance & liability costs for sites | -0.60% | Developed markets | Medium term (2-4 years) |

| Sponsor hesitancy toward non-validated virtual-first networks | -0.40% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Investigator Burnout & High Staff Turnover

Ninety-five percent of cancer centers report workforce shortages that delay trials and impair data quality. Pandemic pressures pushed CRA turnover to 30%, and 46% of sites now decline new studies.[3]WCG Clinical, “WCG’s 2024 Clinical Research Site Challenges Report,” WCGClinical.com, wcgclinical.comCompensation gaps and limited career paths impede hiring. Networks are adopting eSource and eConsent to cut manual tasks and launching global training curricula, but these investments strain margins in the near term.

Stringent Data-Privacy Regulations (GDPR, HIPAA Updates)

GDPR fines have exceeded EUR 1.6 billion since 2018, underscoring compliance risk. Multi-jurisdiction networks juggle divergent retention rules, encryption standards, and localization mandates. HIPAA modernization and U.S. state laws add layers of complexity, demanding costly upgrades to audit trails and consent workflows. Larger networks can absorb these costs; smaller operators often struggle to maintain regulatory parity, limiting their competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Site Type: Dedicated Networks Lead Consolidation

Dedicated networks controlled 33.7% of revenue in 2024, reflecting sponsor confidence in centralized SOPs and uniform quality controls that accelerate start-up timelines. Retail-health clinics are advancing at a 6.8% CAGR as chains leverage loyalty programs to pre-screen diverse patients and reduce site-activation costs. Community hospitals and academic medical centers remain essential for high-acuity therapeutic areas, yet they feel margin pressure from private-equity roll-ups that deliver faster contracting cycles.

Retail entrants such as CVS Health channel USD 100 million of infrastructure funding toward community-based research models, expanding hybrid deployment for chronic-disease trials. Dedicated platforms answer with advanced analytics that forecast screen-fail rates and adjust outreach in real time. Resulting competition spurs a service arms race: virtual nursing, at-home phlebotomy, and concierge travel emerge as standard offerings. The clinical trial site networks market consequently gravitates toward full-service operators that blend brick-and-mortar capacity with decentralized extensions.

By Therapeutic Area: Oncology Dominance Faces Rare-Disease Growth

Oncology maintained a 42.5% revenue share in 2024, supported by established investigator communities and the complexity of biomarker-rich protocols that necessitate central lab integration. Yet the rare-disease segment is pacing fastest at 8.2% CAGR to 2030, boosted by regulatory incentives and a rising inventory of gene and cell therapies. Purpose-built rare-disease networks use national patient registries to locate sparse populations, improving enrollment velocity.

Cardiometabolic studies leverage retail pharmacy partnerships to mine electronic prescription data and identify eligible candidates, while infectious-disease programs integrate home-health nursing to curtail hospital-based visits. CNS disorders call for specialized imaging and neurologic assessment tools, driving site selection to networks possessing dedicated EEG suites and trained raters. As sponsors pivot toward antibody-drug conjugates and radiopharmaceuticals, demand intensifies for radiation-qualified sites that pass stringent handling audits.

By Phase: Late-Stage Dominance Shifts Toward Early-Access

Phase III accounted for 48.5% of the clinical trial site networks market size in 2024, reflecting large patient counts and strict regulatory scrutiny. Early-access and compassionate-use programs, however, are climbing at 7.5% CAGR as patient-advocacy groups lobby for accelerated treatment. Networks that master expedited IRB review and real-time safety reporting secure competitive advantage in these programs.

Phase I operators differentiate through in-house bioanalytical laboratories and telemetry units that allow rapid dose-escalation decisions. In Phase II, adaptive designs and platform trials multiply sub-study logistics; networks respond with integrated data hubs that maintain blinding integrity while sharing interim results with steering committees. Such capabilities shorten development timelines and attract biotech sponsors seeking proof-of-concept validation before Series C fundraising.

Geography Analysis

North America contributed 42.8% of 2024 revenue, anchored by dense sponsor headquarters and mature CRO ecosystems. Investigator burnout and rising malpractice premiums push networks to automate scheduling, remote monitoring, and eConsent in order to sustain throughput. Retail pharmacies disrupt conventional models by embedding trial kiosks inside primary-care settings, enhancing reach among underrepresented minorities. Private-equity interest remains strong, as illustrated by GHO Capital’s expansion of Velocity Clinical Research across 37 U.S. sites.

Asia Pacific is the fastest-growing geography with an 8.3% CAGR outlook, owing to 30-40% cost efficiencies and regulatory harmonization initiatives. South Korea and Taiwan cut approval timelines through expedited pathways, and Japan’s PMDA improves parallel scientific-advice programs that reduce protocol amendments. China prioritizes oncology and orphan drugs via breakthrough-therapy fast tracks, leveraging a pool of 17,000 certified investigators, regional networks partner with local hospitals to navigate language needs and cultural variance in informed consent.

Europe grows steadily, benefiting from the implementation of the EU Clinical Trial Regulation, which centralizes submissions and accelerates start-ups. However, divergent GDPR interpretations and post-Brexit customs formalities raise logistics costs, prompting networks to establish dual hubs in mainland Europe and the United Kingdom. Emerging regions in Latin America, the Middle East, and Africa offer recruitment advantages in infectious-disease and vaccine trials but face infrastructure gaps. Networks with telehealth and mobile-nursing assets bridge facility shortfalls while adhering to varying import license rules for investigational products.

Competitive Landscape

The market remains moderately fragmented: the top five networks control well below 30% of global revenue, yet consolidation is accelerating. Velocity Clinical Research grew via GHO Capital-backed acquisitions, while Centricity Research integrates 40 sites under unified SOPs. ICON’s Accellacare expansion to 112 sites across eight countries demonstrates scale advantages in unified contracting and patient outreach.

Technology is a critical differentiator. IQVIA’s Orchestrated Clinical Trials aggregates EHR, eSource, and wearables to cut site-level data entry by 60%. Verily’s Viewpoint CTMS centralizes calendar management and finance, reducing investigator log-ins from nine systems to one. Retail entrants leverage prescription databases to pre-screen high-volume chronic-disease patients, challenging traditional networks on speed and diversity metrics.

White-space opportunities persist in underserved geographies and rare-disease cohorts. Life-science sponsors seek networks able to launch studies quickly in healthcare deserts where 80% of U.S. counties lack active trial sites. Networks that embed mobile clinics and tele-neurology expand access while preserving data integrity. Capital inflows from private equity underpin continued M&A, driving standardization of eSource, remote monitoring, and centralized budgeting tools across acquired assets.

Clinical Trial Investigative Site Network Industry Leaders

Velocity Clinical Research

Accellacare (ICON plc)

Centricity Research

Synexus

WCG Site Network

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Headlands Research acquired a Puerto Rico site, expanding patient diversity for multi-regional studies.

- May 2025: Tempus chose the TIME Network to run Phase I oncology trials, emphasizing molecular-profiling capabilities.

- March 2025: ICON plc consolidated PMG and MeDiNova under the Accellacare network, creating 112 sites with integrated decentralized functions.

- January 2025: Suvoda agreed to merge with Greenphire to form an end-to-end randomization, supply, and patient-payment platform.

Global Clinical Trial Investigative Site Network Market Report Scope

| Academic Medical Centers |

| Community Hospitals |

| Dedicated Site Networks / SMOs |

| Retail-Health Clinics |

| Private Physician Sites |

| Oncology |

| Cardiometabolic |

| Infectious Diseases |

| CNS Disorders |

| Rare & Orphan Diseases |

| Phase I |

| Phase II |

| Phase III |

| Phase IV / Observational |

| Early-Access / Expanded-Access |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Site Type | Academic Medical Centers | |

| Community Hospitals | ||

| Dedicated Site Networks / SMOs | ||

| Retail-Health Clinics | ||

| Private Physician Sites | ||

| By Therapeutic Area Focus | Oncology | |

| Cardiometabolic | ||

| Infectious Diseases | ||

| CNS Disorders | ||

| Rare & Orphan Diseases | ||

| By Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV / Observational | ||

| Early-Access / Expanded-Access | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the clinical trial site networks market in 2030?

The market is forecast to reach USD 13.76 billion by 2030, reflecting a 7.85% CAGR from 2025.

Which region is expected to grow fastest through 2030?

Asia Pacific is projected to register the highest 8.3% CAGR, supported by cost advantages and regulatory harmonization.

Which site type segment shows the quickest growth?

Retail-health clinics are advancing at a 6.8% CAGR as companies like CVS and Walgreens leverage community presence for trial recruitment.

How large is oncologys share within the market?

Oncology accounted for 42.5% of total 2024 revenue, underscoring its dominance in complex trial demand.

What technological capabilities are differentiating leading networks?

AI-enabled CTMS platforms that consolidate eSource, wearables, and remote monitoring are reducing data-entry workload and improving investigator satisfaction.

Why are early-access programs gaining traction?

Patient-advocacy efforts and supportive regulatory frameworks are accelerating early-access study volumes, leading to a 7.5% CAGR in this sub-segment.

Page last updated on: