Clinical Trials Support Software Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

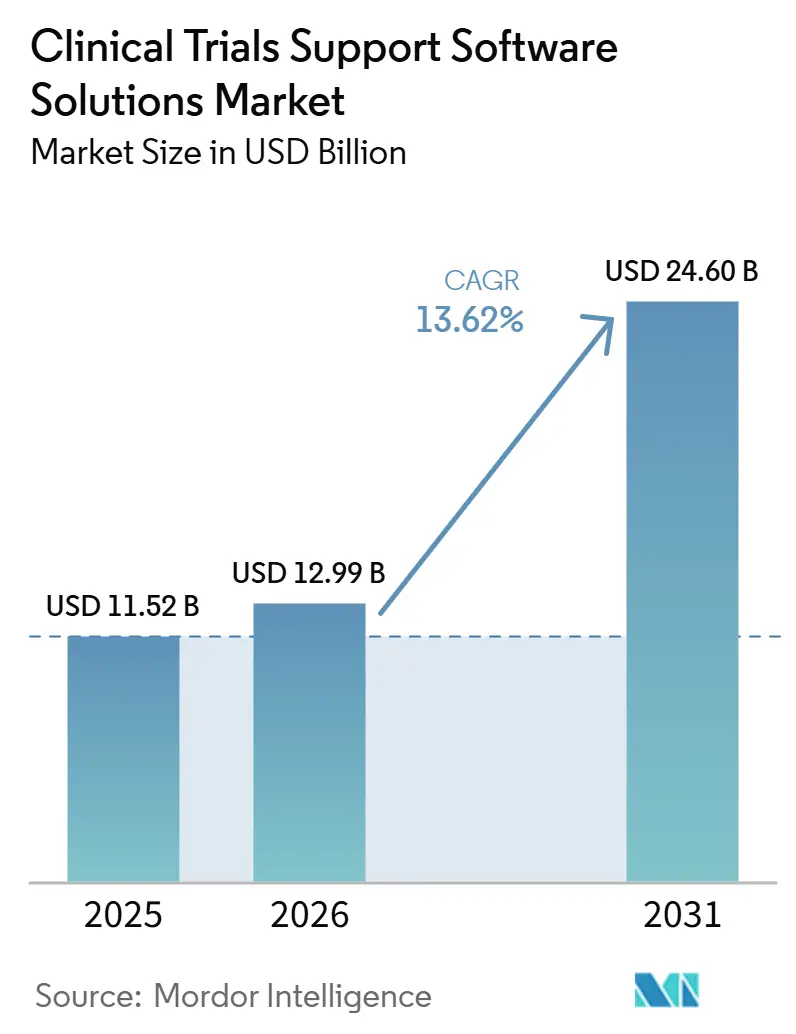

| Market Size (2026) | USD 12.99 Billion |

| Market Size (2031) | USD 24.60 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trials Support Software Solutions Market Analysis by Mordor Intelligence

The clinical trials support software solutions market was valued at USD 11.52 billion in 2025 and is projected to be valued at USD 12.99 billion in 2026. It is expected to reach USD 24.60 billion by 2031, registering a CAGR of 13.62% from 2026 to 2031. The market is advancing because sponsors, contract research organizations, and regulators are moving away from paper-heavy and stand-alone workflows toward connected digital platforms that can support trial execution across functions. The clinical trials support software solutions market is also being shaped by compliance needs, since regulators now expect standardized, traceable, and audit-ready data flows across study design, conduct, monitoring, and submission activities. The clinical trials support software solutions market is moving toward unified software environments where clinical data management, trial management, trial documentation, and decentralized trial tools work together instead of sitting in separate systems. This change is raising the value of platforms that can simplify data handling, reduce manual reconciliation, and support oversight in multinational trials. It is also creating room for vendors that can combine operational breadth with validated workflows, cloud delivery, and selective AI-enabled features that fit regulated trial settings.

Key Report Takeaways

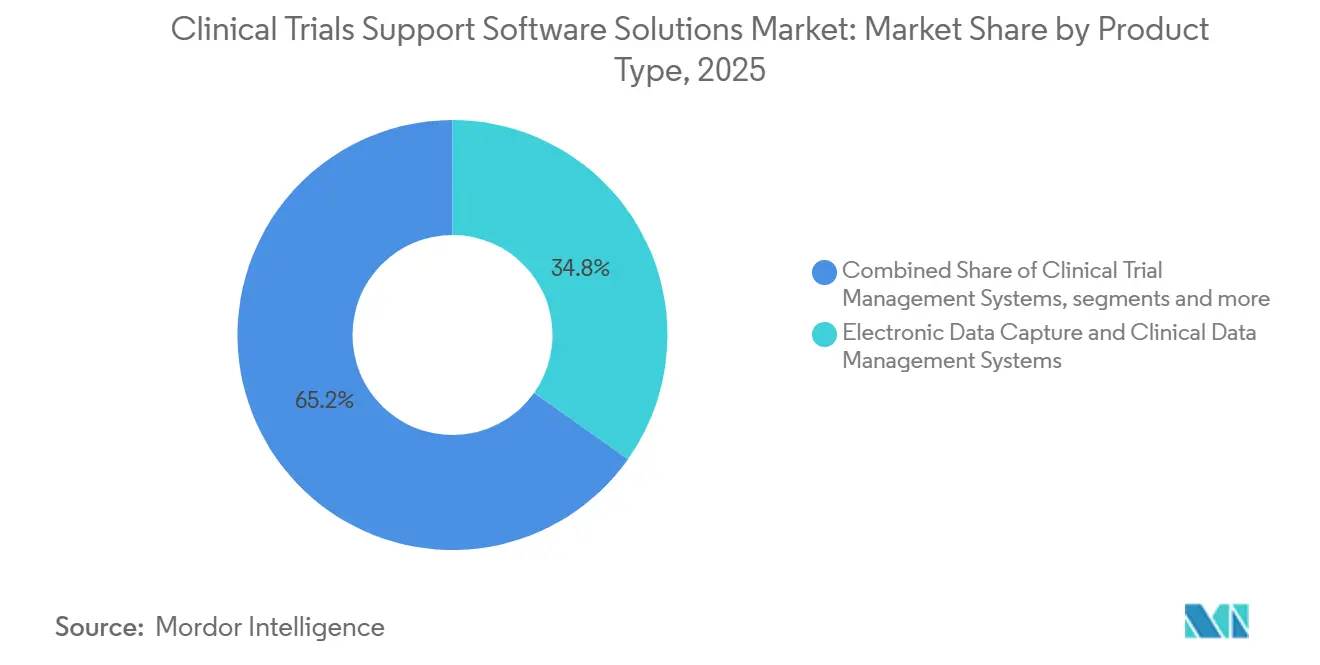

- By product type, electronic data capture (EDC) & clinical data management systems held 34.76% of the clinical trials support software solutions market share in 2025, while clinical trial management systems (CTMS) are projected to expand at a 16.84% CAGR through 2031.

- By delivery mode, cloud and web-based deployment accounted for 68.24% share of the clinical trials support software solutions market size in 2025 and is projected to grow at a 15.37% CAGR through 2031.

- By clinical trial phase, phase III accounted for 41.58% of segment demand in 2025, while phase I is forecast to grow at a 14.92% CAGR through 2031.

- By trial model, traditional site-based trial solutions held 62.41% of segment revenue in 2025, while hybrid trial solutions are forecast to record the highest CAGR at 18.46% through 2031.

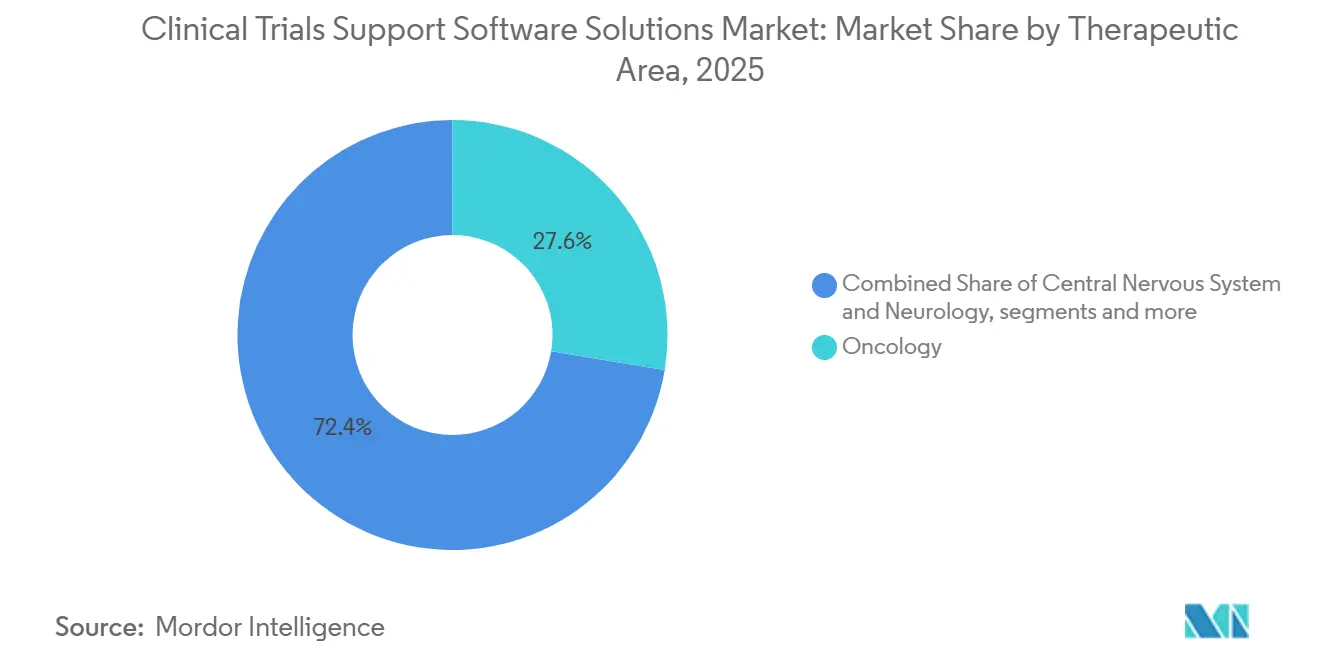

- By therapeutic area, oncology captured 27.63% of segment demand in 2025, while cardiovascular and metabolic diseases are projected to grow at a 15.28% CAGR through 2031.

- By end-user, contract research organizations (CROs) held 39.82% of the clinical trials support software solutions market share in 2025, while pharmaceutical and biotechnology companies are forecast to expand at a 15.74% CAGR through 2031.

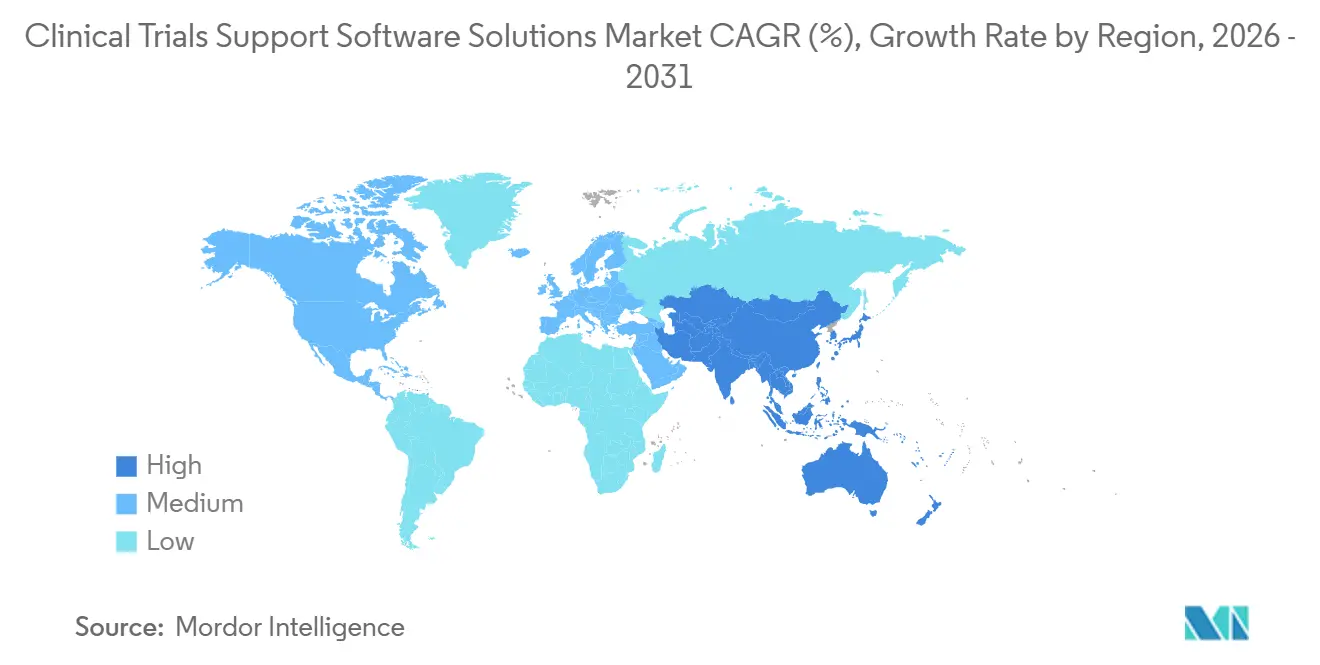

- By geography, North America captured 40.18% of segment demand in 2025, while the Asia-Pacific is projected to grow at a 17.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Trials Support Software Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Complexity of Multinational, Multi-Protocol Trial Operations | +3.1% | Global | Medium term (2-4 years) |

| Shift from Point Solutions to Unified Trial Operating Systems | +2.8% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Sponsor Demand for Real-Time Site, Patient, and Supply Visibility | +2.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Compliance-Driven Digitization of Audit Trails and Inspection Readiness | +2.2% | Global | Short term (≤ 2 years) |

| Direct Integration Pressure from Decentralized Trial Workflows | +1.5% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Clinical Finance and Payments Automation Becoming a Trial Retention Lever | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Complexity of Multinational Multi-Protocol Trial Operations

The clinical trials support software solutions market is gaining support from the rising operational complexity of multinational studies that involve more sites, more countries, and more parallel workflows. Large programs now require tight coordination across data capture, trial management, document control, safety reporting, and oversight functions, which makes fragmented system setups harder to manage. This pressure is strongest in later-stage and oncology-heavy programs where protocol changes, regional operating differences, and dense reporting requirements create repeated workflow adjustments. Unified platforms are becoming more attractive in this setting because they allow teams to manage changes inside one operating structure rather than reconciling several point tools after each update. That shift improves consistency in trial execution and makes platform standardization more valuable for sponsors with large global portfolios. It also favors vendors that can support repeatable study builds, shared metadata, and cross-study reuse in regulated environments.[1]Veeva Systems, “2026 Clinical Data Trend Report,” Veeva Systems, veeva.com

Shift from Point Solutions to Unified Trial Operating Systems

The clinical trials support software solutions market is also being pushed by a clear move away from separate tools for EDC, CTMS, eTMF, eConsent, and related functions. Sponsors want fewer system handoffs because each extra interface can add reconciliation work, validation effort, and operational delay. The move toward a unified operating model is gaining force because regulators are asking for better visibility into how oversight actions, protocol execution, and data handling are documented across the full study lifecycle. In 2025, the M11 technical specification advanced formal structured protocol expectations, which supports the broader push toward more consistent and digital study design workflows.[2]U.S. Food and Drug Administration, “Electronic Study Data Submission, Data Standards, Clinical Data Interchange Standards Consortium Dataset-JSON,” Federal Register, federalregister.gov Veeva’s 2026 report also shows that clinical data organizations are prioritizing simplification and standardization, which fits the same direction of travel in the clinical trials support software solutions market. As a result, vendors with native workflows across core modules are in a stronger position than vendors that depend mainly on stitched integrations.

Sponsor Demand for Real-Time Site, Patient, and Supply Visibility

The clinical trials support software solutions market is benefiting from sponsor demand for faster visibility into what is happening at the site, patient, and operational level. Trial teams want earlier signals on enrollment progress, data quality issues, protocol deviations, and study execution risks because slower feedback makes corrective action more costly. This need is reinforcing the value of CTMS, analytics layers, and connected data management systems that can support ongoing oversight rather than only storing records after the fact. The FDA’s broader work on AI and machine learning in regulated settings has also helped move sponsor expectations toward documented and controlled use of more advanced digital workflows. In practical terms, the market is rewarding platforms that can combine operational monitoring with defensible validation and traceability. That creates a stronger case for software suites that can support both execution and inspection readiness at the same time.

Compliance-Driven Digitization of Audit Trails and Inspection Readiness

The clinical trials support software solutions market continues to be shaped by compliance needs more than by convenience alone. In April 2025, the FDA proposed CDISC Dataset-JSON v1.1 as a data standard for electronic clinical study data submission, which reinforces the need for software systems that can produce structured and submission-ready outputs. The same pattern is visible in China, where the revised GCP framework issued in June 2026 and effective from September 1, 2026, introduced stronger data governance expectations across the trial data lifecycle. These developments make validated audit trails, metadata handling, electronic signatures, and computerized system controls more central to trial software buying decisions. They also raise the pressure on smaller sponsors and sites that still depend on manual processes or lightly connected systems. In turn, the clinical trials support software solutions market is favoring vendors that can turn compliance requirements into standard platform capabilities rather than one-off customization exercises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Data Models Across Sponsor, CRO, and Site Systems | -1.9% | Global, most acute in large pharma legacy environments | Long term (≥ 4 years) |

| Validation, Configuration, and Change-Control Burden for Regulated Deployments | -1.4% | North America and Europe, with spillover to Asia-Pacific site networks | Medium term (2-4 years) |

| Site-Level Software Overload Reducing User Adherence | -1.1% | Global | Long term (≥ 4 years) |

| Interoperability Gaps with eSource, EHR, and Safety Stacks | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Data Models Across Sponsor, CRO, and Site Systems

The clinical trials support software solutions market still faces resistance from legacy data structures that have been built over long development histories. Large sponsors often run a mix of old validated systems and newer cloud tools, and that makes full migration slower than the demand story alone would suggest. Every change to a regulated system can trigger validation work, documentation reviews, and operational retraining, which raises the cost of moving too quickly. This is especially difficult when multiple systems feed one trial program and each one handles study logic, reporting, or document control in a slightly different way. As a result, many organizations are choosing phased modernization instead of broad replacement programs. That slows adoption speed in the clinical trials support software solutions market even when the strategic case for consolidation is already clear.

Site-Level Software Overload Reducing User Adherence

The clinical trials support software solutions market also has to deal with friction at the research site level, where staff are often asked to use several sponsor-specific systems at once. Sites may need separate logins and workflows for EDC, eConsent, ePRO, telehealth tools, and trial management activities, and that can create practical fatigue rather than smoother execution. This issue matters because even strong sponsor-side technology can underperform if site teams do not have the time, staffing, or training support needed for consistent use. The burden is even greater for smaller community sites and academic centers that have thin internal IT support but still play an important role in specialized patient recruitment. Vendors that simplify user experience and reduce duplicate steps can lower this barrier, but software design alone will not solve it. The restraint stays relevant because adoption quality depends not only on what sponsors buy, but also on how easily sites can operate the resulting tool stack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: EDC and CDMS Anchor Demand While CTMS Scales Faster

Electronic data capture (EDC) & clinical data management systems held 34.76% of product type demand in 2025, which kept them at the center of the clinical trials support software solutions market because data capture and clinical data handling remain essential in every study. These systems sit close to the core record of trial activity, so they are often the first software decision in a new program. Their position is strengthened by the fact that later functions such as monitoring, documentation, and analytics still depend on clean and timely source data flow from the capture layer. In practical terms, sponsors and CROs continue to treat EDC and CDMS as foundational even when they are broadening spend into adjacent modules. That is why the leading share stayed with this category despite the growth of more specialized functions across the clinical trial software market.

The fastest-growing product type is clinical trial management systems (CTMS), which is projected to expand at a 16.84% CAGR through 2031. That pace reflects a shift in how trial teams use CTMS, from a passive record-keeping tool toward a live coordination system for milestones, oversight, and operational visibility. RTSM still retains a distinct position because adaptive and multi-arm studies require specialized allocation and supply logic. Analytics and data integration layers are also becoming more valuable because they connect operational systems with external feeds, including wearables and health record inputs, into one decision environment. That means product competition is now shaped as much by integration depth as by module-specific features.

By Delivery Mode: Cloud Becomes the Default Operating Model

Cloud and web-based deployment represented 68.24% of delivery mode demand in 2025, and that leads to this being the clearest structural choice inside the clinical trial software market. It is also expected to be the fastest-growing delivery mode, with a projected 15.37% CAGR through 2031, so the largest segment is still widening its lead. Cloud delivery fits the needs of multinational trials because it supports easier scaling, faster software updates, and broader access across sponsor, CRO, and site teams. It also supports more consistent rollout of new workflows across countries without the same infrastructure burden associated with local installations. For many buyers, deployment is no longer a simple IT preference. It now affects how quickly a platform can support compliance changes, global study expansion, and connected oversight.

On-premises models still exist, especially in large legacy environments or places with strict data residency expectations. Even so, these deployments are increasingly moving toward hybrid or private cloud structures instead of full stand-alone systems. That suggests the real question is not whether cloud will lead, but how fast holdout environments can transition without disrupting validated operations. The delivery pattern also changes the vendor landscape because cloud-native design can make deployment simpler for mid-sized sponsors and growth-stage biopharma companies.

By Clinical Trial Phase: Phase III Remains the Revenue Core While Phase I Builds Momentum

Phase III accounted for 41.58% of segment demand in 2025, which reflects where the clinical trials support software solutions market sees the greatest concentration of operational complexity and spend. These studies usually involve many sites, multiple countries, larger patient groups, and close coordination across data, documentation, monitoring, and safety functions. Because the cost of delay is high at this stage, sponsors are more willing to invest in software that can support controlled execution and fewer operational breaks. Phase II continued to contribute meaningful demand because it often serves as the bridge between early validation and late-stage scale, and that still requires strong data and trial management capabilities.

Phase I is projected to grow at a 14.92% CAGR through 2031, making it the fastest-expanding phase segment in the clinical trial software market. This growth points to rising early-stage activity in oncology, rare disease, and advanced therapy programs where close safety tracking and flexible workflows are essential. Early-phase studies are also becoming more data-rich, with greater interest in device-linked monitoring, continuous observation, and streamlined process control. That increases the value of specialized software support even before studies reach the high-volume Phase III stage. Phase IV is also becoming more relevant as post-approval evidence needs continue to widen. Adaptive and seamless study designs require systems that can carry forward consistent data structures rather than forcing a new build at each transition. This makes phase-agnostic architecture more attractive to buyers that want continuity across the development path. It also means growth is no longer limited to late-stage trial volume alone, because earlier phases are becoming more software-intensive in their own right.

By Trial Model: Hybrid Designs Gain Ground Without Displacing the Site Base

Traditional site-based trial solutions held 62.41% of the segment in 2025, which shows that the clinical trials support software solutions market still depends on physical research sites as the main setting for evidence generation. This remains true even as remote tools, telehealth visits, and patient-facing digital workflows gain wider use. The large installed base of site-led workflows also means sponsors are looking for extension rather than total replacement in how they modernize studies.

Hybrid trial solutions are forecasted to grow at an 18.46% CAGR through 2031, which makes them the fastest-moving model in the clinical trial software market. The FDA’s final guidance on decentralized elements, published in September 2024, helped reduce uncertainty around telehealth use, eConsent, and digital health technologies in trial conduct.[3]U.S. Food and Drug Administration, “Conducting Clinical Trials With Decentralized Elements,” U.S. Food and Drug Administration, fda.gov That guidance supports the pattern already seen in practice, where sponsors combine site-based and remote elements instead of moving fully to all-virtual designs. In purchasing terms, hybrid readiness is becoming a baseline expectation. That is why the clinical trials support software solutions market is rewarding vendors that can connect remote data capture and patient-facing tools without weakening the operational discipline of site-led trials.

By Therapeutic Area: Oncology Leads Current Demand While Cardiovascular and Metabolic Programs Accelerate

Oncology held 27.63% of therapeutic area demand in 2025, which kept it as the largest clinical area within the clinical trial software market. Oncology pipelines remain dense, and many oncology studies use adaptive designs, multi-arm structures, and real-time decision points that place heavy demands on software systems. These studies often need rapid data visibility and strong coordination across sites and geographies, which raises software intensity per study. Central nervous system and neurology studies also stand out for their complexity, especially where patient-reported outcomes, longer follow-up, and digital measurements matter.

Cardiovascular and metabolic diseases are projected to grow at a 15.28% CAGR through 2031, making them the fastest-growing therapeutic area in the clinical trial software market. This acceleration to expanding GLP-1 programs, cardiovascular outcomes studies, and obesity-related metabolic trials that bring together digital monitoring, ePRO, and broader data integration needs. Rare diseases and infectious diseases also continue to expand, especially where remote data collection can support access to dispersed patient groups. Vendors that can align with those therapy-specific data needs are likely to strengthen their position as study design complexity grows.

By End-User: CROs Lead Current Spending While Pharma and Biotech Build Internal Capability

Contract research organizations (CROs) held 39.82% of end-user demand in 2025, which made them the largest buyer group in the clinical trial software market. Their lead reflects the fact that CROs operate trials for many sponsors and therefore maintain licenses, workflows, and service teams across several eClinical functions. Because they manage activity across multiple programs and clients, CRO purchasing decisions can influence which platforms scale most widely. It also means software providers often treat CRO relationships as a route to broader market reach rather than only a direct revenue stream.

Pharmaceutical and biotechnological companies are projected to grow at a 15.74% CAGR through 2031, making them the fastest-growing end-user group in the clinical trial software market. The shift to emerging biopharma companies that are building more internal digital infrastructure to reduce dependence on CRO-led operating models. Hospitals and healthcare providers also remain an important secondary group, especially in investigator-led settings and academic environments that participate in broader sponsor networks. Taken together, the end-user pattern shows that the clinical trials support software solutions market is broadening from outsourced execution support toward a more mixed model of external delivery and internal platform ownership.

Geography Analysis

North America held 40.18% of the clinical trials support software solutions market size in 2025, which made it the leading regional segment. The United States remains the main anchor because it has a high concentration of industry-sponsored Phase II and Phase III studies and a regulatory environment that is actively shaping digital trial practice. The FDA’s 2024 decentralized trial guidance and its 2025 Dataset-JSON proposal have given sponsors and vendors a clearer operating path for digital workflows and submission-ready data handling. Canada and Mexico support regional trial activity as well, with Mexico retaining a role in cost-sensitive late-stage enrollment programs.

Europe remained the second-largest region in the clinical trials support software solutions market and is moving through an important regulatory transition. The EU Clinical Trials Regulation framework and CTIS standardization have pushed sponsors and CROs toward more consistent submission and workflow practices across member states. FAST-EU, which moved forward in late 2025 and early 2026, adds to that direction by aiming to streamline multinational approvals within the region. The European Health Data Space also adds a longer-term driver because wider cross-border health data access for research can increase the need for stronger integration and data governance tools.

Asia-Pacific is forecasted to grow at a 17.82% CAGR through 2031, making it the fastest-growing regional segment in the clinical trial software market. China and Japan are the main anchor markets, while India and South Korea are expanding as clinical hubs in the regional mix. China’s revised GCP framework, issued in June 2026 and effective from September 2026, strengthens the region’s data governance direction and raises the value of validated software controls in ongoing and future studies. That change supports stronger demand for electronic audit trails, metadata handling, and broader computerized system discipline. South America and the Middle East and Africa remain smaller in absolute size, but they continue to gain attention as sponsors seek wider patient diversity and faster enrollment across more geographies. Within those regions, Brazil, South Africa, and GCC countries remain the most visible activity centers. Taken together, the regional picture shows a clinical trials support software solutions market led by North America in current scale, supported by Europe’s regulatory alignment, and accelerated by Asia-Pacific’s faster expansion.

Competitive Landscape

The clinical trials support software solutions market is moderately consolidated at the enterprise level and more fragmented across mid-market and specialist layers. Veeva Systems, Dassault Systèmes through Medidata, Oracle, and IQVIA remain the leading large-platform names because they offer broad suites across data capture, trial management, document workflows, and analytics. Their scale matters because sponsors want fewer integration points and stronger validation discipline in regulated trial settings. Even so, competition is not defined only by broad suites. Specialist vendors continue to hold space in areas such as endpoint data, digital outcomes, trial supply, and AI-enabled planning tools. This creates a market structure where top-tier platforms anchor core workflows while niche players compete where technical depth or speed of innovation is more important.

Mergers and acquisitions remain the strongest visible strategy in the clinical trial software market. Signant Health’s May 2026 acquisition of Ametris shows a similar logic at the digital measurement layer, where software vendors want stronger control of both patient-reported and wearable-derived outcome data. Parexel’s April 2026 acquisition of Vitrana extends this pattern into pharmacovigilance technology and supports a broader integrated service and software proposition.

A second line of competition is forming around AI-enabled workflow support rather than only module breadth. Newer companies are also targeting trial simulation, feasibility, site selection, and recruitment preparation, which can shift value earlier in the study lifecycle. That does not replace core eClinical platforms, but it can reduce amendment risk and tighten study design before execution begins. As a result, incumbents may face slower growth in configuration-heavy work if sponsors move more planning logic upstream. The clinical trials support software solutions market therefore remains competitive not because demand is weak, but because the next layer of value is moving toward connected intelligence, operational fit, and evidence-ready data flows rather than stand-alone functionality alone.

Clinical Trials Support Software Solutions Industry Leaders

Veeva Systems

IQVIA

Dassault Systèmes

Oracle

Signant Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Signant Health acquired Ametris (formerly ActiGraph), creating an end-to-end eCOA platform integrating patient-reported outcomes with wearable-derived digital measurements. The combined entity targets CNS and cardiovascular trials where multimodal evidence packages are increasingly required for regulatory submissions.

- April 2026: Parexel acquired Vitrana, an AI-enabled end-to-end pharmacovigilance (PV) technology platform. The acquisition aligns Vitrana's automated safety signal processing with Parexel's Patient Safety Services, deepening its integrated CRO-plus-technology proposition for pharma clients.

- April 2026: WCG announced the acquisition of The Contract Network to extend its ClinSphere AI platform into study start-up and contract workflow intelligence. The deal strengthens WCG's end-to-end trial activation capabilities, from predictive site feasibility to contract and budget alignment.

Global Clinical Trials Support Software Solutions Market Report Scope

According to the report’s scope, the clinical trials support software solutions market refers to the ecosystem of digital platforms and software tools that enable the planning, execution, monitoring, and management of clinical trials. It includes solutions for data capture, trial oversight, patient engagement, regulatory documentation, supply management, and analytics, supporting sponsors, CROs, and research sites in running trials more efficiently, compliantly, and at scale.

The clinical trials support software solutions market is segmented into product type, delivery mode, clinical trial phase, trial model, therapeutic area, end-user, and geography. By product type, the market is segmented into electronic data capture and clinical data management systems, clinical trial management systems, clinical analytics platforms, randomization and trial supply management solutions, electronic clinical outcome assessment solutions, electronic trial master file solutions, regulatory information management solutions, clinical data integration platforms, risk based quality management solutions, payments and investigator payments solutions, and other product types. By delivery mode, the market is segmented into cloud and web-based and on-premises. By clinical trial phase, the market is segmented into phase I, phase II, phase III, and phase IV. By trial model, the market is segmented into traditional site-based trial solutions, hybrid trial solutions, and decentralized clinical trial solutions. By therapeutic area, the market is segmented into oncology, central nervous system and neurology, cardiovascular and metabolic diseases, rare diseases, infectious diseases, and other therapeutic diseases. By end-user, the market is segmented into contract research organizations (CROs), pharmaceutical and biotechnological companies, hospitals and healthcare providers, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Electronic Data Capture and Clinical Data Management Systems |

| Clinical Trial Management Systems |

| Clinical Analytics Platforms |

| Randomization and Trial Supply Management Solutions |

| Electronic Clinical Outcome Assessment Solutions |

| Electronic Trial Master File Solutions |

| Regulatory Information Management Solutions |

| Clinical Data Integration Platforms |

| Risk Based Quality Management Solutions |

| Payments and Investigator Payments Solutions |

| Other Product Types |

| Cloud and Web-Based |

| On-Premises |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Traditional Site-Based Trial Solutions |

| Hybrid Trial Solutions |

| Decentralized Clinical Trial Solutions |

| Oncology |

| Central Nervous System and Neurology |

| Cardiovascular and Metabolic Diseases |

| Rare Diseases |

| Infectious Diseases |

| Other Therapeutic Diseases |

| Contract Research Organizations (CROs) |

| Pharmaceutical and Biotechnological Companies |

| Hospitals and Healthcare Providers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Electronic Data Capture and Clinical Data Management Systems | |

| Clinical Trial Management Systems | ||

| Clinical Analytics Platforms | ||

| Randomization and Trial Supply Management Solutions | ||

| Electronic Clinical Outcome Assessment Solutions | ||

| Electronic Trial Master File Solutions | ||

| Regulatory Information Management Solutions | ||

| Clinical Data Integration Platforms | ||

| Risk Based Quality Management Solutions | ||

| Payments and Investigator Payments Solutions | ||

| Other Product Types | ||

| By Delivery Mode | Cloud and Web-Based | |

| On-Premises | ||

| By Clinical Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Trial Model | Traditional Site-Based Trial Solutions | |

| Hybrid Trial Solutions | ||

| Decentralized Clinical Trial Solutions | ||

| By Therapeutic Area | Oncology | |

| Central Nervous System and Neurology | ||

| Cardiovascular and Metabolic Diseases | ||

| Rare Diseases | ||

| Infectious Diseases | ||

| Other Therapeutic Diseases | ||

| By End-User | Contract Research Organizations (CROs) | |

| Pharmaceutical and Biotechnological Companies | ||

| Hospitals and Healthcare Providers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the clinical trials support software solutions market?

The clinical trials support software solutions market stands at USD 11.52 billion in 2025 to USD 12.99 billion in 2026 and is forecasted to reach USD 24.60 billion by 2031 at a 13.62% CAGR.

Which product type segment leads current demand?

Electronic data capture (EDC) & clinical data management systems led product demand with 34.76% share in 2025 because data capture and clinical data handling remain core to every study.

Which delivery mode is gaining the most traction?

Cloud and web-based delivery leads with 68.24% share in 2025 and is also expected to be the fastest-growing delivery mode at a 15.37% CAGR through 2031.

Which region offers the fastest growth outlook through 2031?

Asia-Pacific is forecasted to expand at a 17.82% CAGR through 2031, supported by regulatory change, growing trial activity, and wider software adoption across key regional hubs.

Page last updated on: