Patient Registry Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

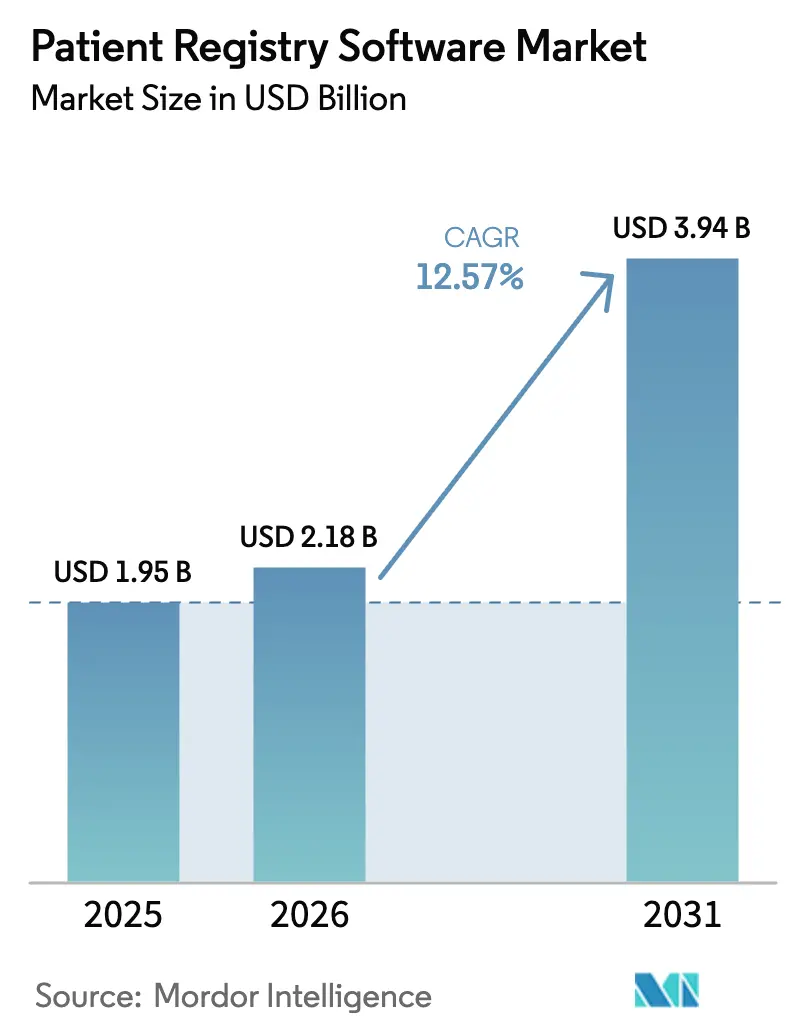

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 12.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Registry Software Market Analysis by Mordor Intelligence

The Patient Registry Software Market size is projected to expand from USD 1.95 billion in 2025 and USD 2.18 billion in 2026 to USD 3.94 billion by 2031, registering a CAGR of 12.57% between 2026 to 2031.

Robust investments in national health data programs, tighter interoperability mandates, and sponsors’ rising appetite for registry-based real-world evidence are accelerating the deployment of platforms. Cloud-deployed SaaS offerings dominate because they cut capital outlays, automate upgrades, and simplify FHIR compliance, while AI-enabled abstraction is reducing data-curation costs by as much as 40%. Pregnancy and maternal-child registries are experiencing growth following the FDA’s TEMPO pilot, which lowered surveillance costs for obstetric devices, and academic medical centers are scaling their registries to support precision-medicine grants. Competitive positioning now hinges on providing open APIs, OMOP data model support, and federated query capabilities that satisfy the emerging European Health Data Space rules.

Key Report Takeaways

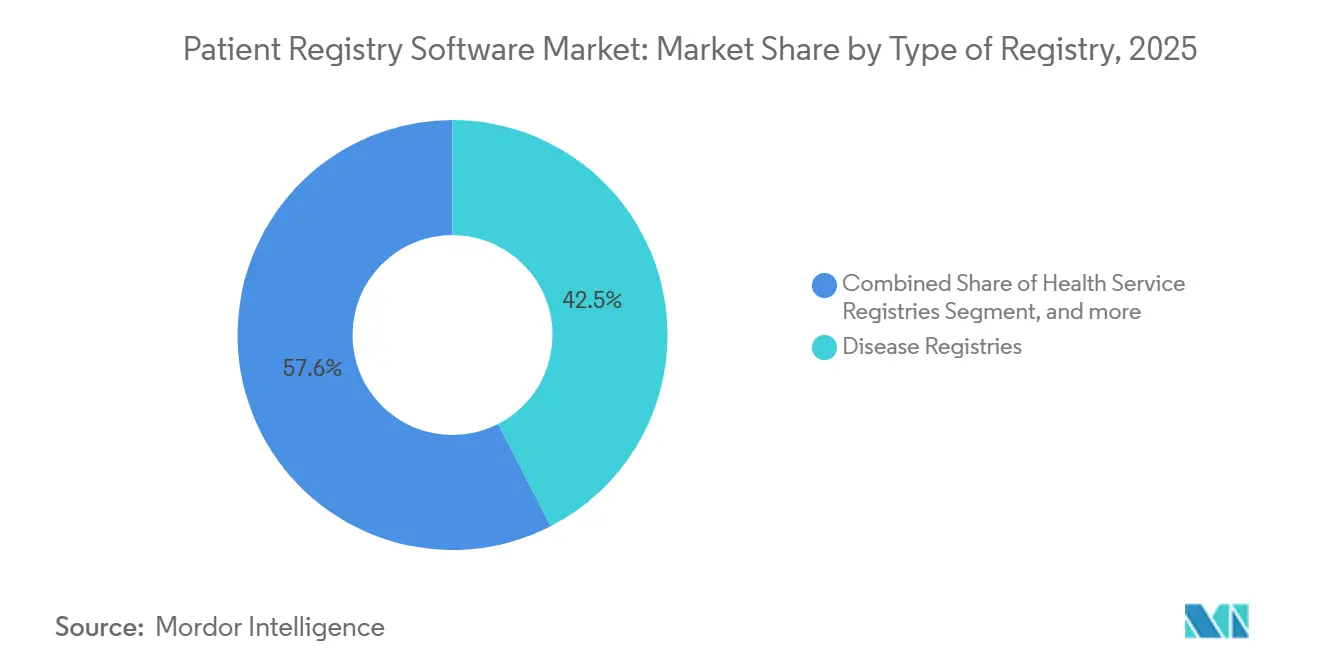

- By type of registry, disease registries led with 42.45% of 2025 revenue; pregnancy and maternal-child registries are projected to post a 14.65% CAGR through 2031.

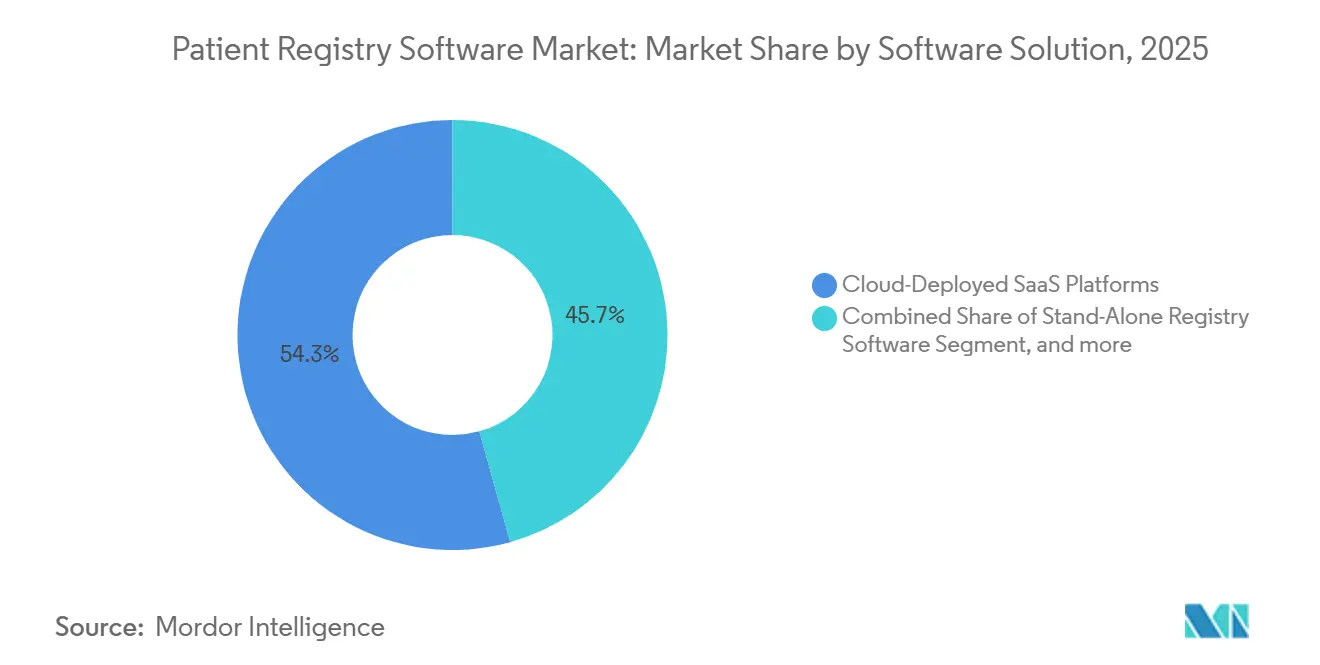

- By software solution, cloud-deployed SaaS platforms commanded 54.32% of the 2025 share and are also expected to grow fastest at a 14.78% CAGR through 2031.

- By end user, hospitals and health systems held 41.45% of the 2025 share; research institutes and academic medical centers are forecast to register a 15.65% CAGR through 2031.

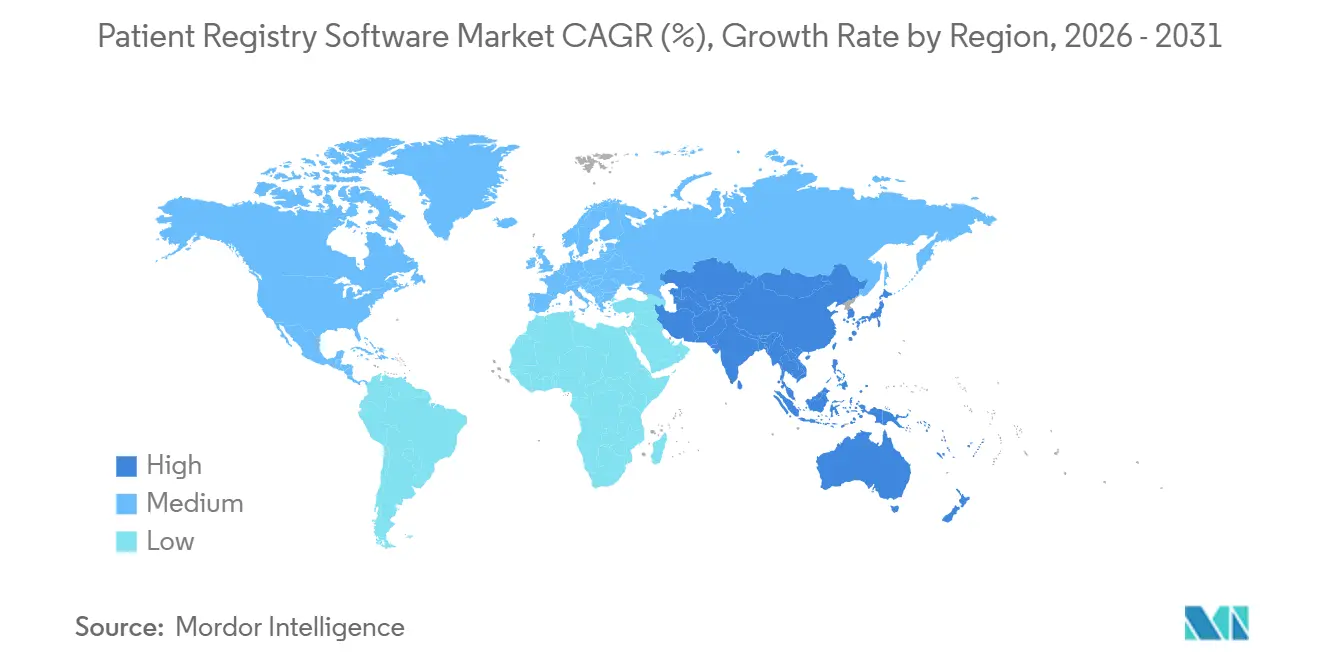

- By geography, North America accounted for 44.32% of the 2025 revenue; the Asia-Pacific region is on track to expand at a 13.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Patient Registry Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government initiatives and funding for large-scale registries | +2.1% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of EHRs and interoperability mandates | +2.5% | North America, Europe, expanding Asia-Pacific | Short term (≤2 years) |

| Registry data for post-marketing surveillance and RWE | +1.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing chronic-disease burden | +1.7% | Global aging populations | Long term (≥4 years) |

| AI-powered automated abstraction | +2.3% | North America, Europe early adopters | Short term (≤2 years) |

| Integration of patient-generated health data | +1.4% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Implementation of Government Initiatives and Funding for Large-Scale Patient Registries

Public funding is transforming registries from discretionary tools into compliance requisites. The FDA’s TEMPO pilot, launched in December 2025, enables device makers to fulfill surveillance duties through structured registry submissions, resulting in approximately 30% cost savings for sponsors. Australia’s National Cancer Data Framework earmarked grants in 2025 to test a shared oncology-registry platform and automate stage-at-diagnosis capture from radiology reports. Within the European Medicines Agency’s DARWIN EU network, 30 data partners covering 160 million lives now require registries that export OMOP-formatted datasets for multinational studies. India’s Ayushman Bharat Digital Mission has linked over 6.5 billion health records to unique identifiers, making registry enablement a prerequisite for public-sector contracts. Collectively, these programs accelerate procurement cycles and favor vendors that ship out-of-the-box FHIR and OMOP connectors.

Rising Adoption of Electronic Health Records and Interoperability Mandates

The ONC HTI-4 Final Rule, effective August 2025, expanded the USCDI to version 4 and prohibited information blocking for matching and consent APIs, providing registry vendors with real-time access to standardized data [1]Office of the National Coordinator for Health Information Technology, “HTI-4 Final Rule,” healthit.gov. TEFCA, operational since December 2024, provides a nationwide query-based exchange, enabling registries to pull longitudinal records without one-off data-use agreements. Michigan’s CHRONICLE pilot proved that HL7 ADT feeds can populate chronic-disease registries at scale, although inconsistent ICD-10 coding still hampers analytics. Faced with this momentum, EHR incumbents, such as Oracle Health, embedded registry modules to defend their installed bases and monetize incremental data flows. FHIR compatibility has therefore become a core requirement for tenders.

Increasing Utilization of Registry Data for Post-Marketing Surveillance and Real-World Evidence

Sponsors now utilize registries to generate external comparators, safety signals, and evidence for label expansion. FDA guidance clarifying the use of registries in regulatory submissions reduced uncertainty and accelerated uptake. Datavant’s July 2025 acquisition of Aetion merged a 60 million-record connectivity fabric with causal-inference analytics, demonstrating a shift toward turnkey RWE stacks. In Europe, EMA guidelines drive demand for audit-ready traceability and role-based access controls [2]European Medicines Agency, “DARWIN EU Overview,” ema.europa.eu. Partnerships, such as IQVIA-Salesforce, integrate registry data with commercial CRMs, linking clinical outcomes to physician engagement strategies.

Growth of Chronic-Disease Burden Requiring Longitudinal Outcomes Tracking

Aging populations increase the prevalence of cardiovascular, oncological, and metabolic disorders. The American College of Cardiology’s registry processes data from 2,400 hospitals, setting quality benchmarks for interventions. SEER now captures stage at diagnosis for 95% of reportable cancers, yet gaps in chemotherapy data sustain demand for integrated EHR-registry tools. Diabetes registries are increasingly incorporating continuous glucose data via FHIR, thereby easing participant burden. WHO’s DHIS2-based clinical-registry platform, launched in 2025, offers free modules that could displace commercial vendors in low-income regions. Value-based contracts underscore the importance of real-time dashboards and risk adjustment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and data-security concerns | -1.8% | Global, acute in North America and Europe | Short term (≤2 years) |

| Shortage of trained abstractors and informatics staff | -1.3% | Global, severe in North America and Europe | Medium term (2-4 years) |

| Vendor lock-in and interoperability gaps | -0.9% | Global, fragmentation highest in Europe, Asia-Pacific | Long term (≥4 years) |

| Variable data quality undermining reimbursement | -1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Privacy and Data-Security Concerns Amid Expanding Data-Sharing Ecosystems

Change Healthcare’s February 2024 ransomware breach, affecting 100 million records, heightened scrutiny of third-party processors under HIPAA and GDPR. Ascension Health’s 2024 cyberattack exposed the operational fragility of interconnected systems. Fragmented EU and U.S. rules add 3-6 months to the activation of multinational registries, as Ireland’s registry task force observed in 2025. TEFCA’s patient-access features introduce identity-proofing liabilities that smaller vendors struggle to absorb. Consequently, many sponsors demand federated architectures that keep data on hospital servers, adding 15-20% to the total cost of ownership and slowing uptake among budget-constrained societies.

Shortage of Trained Clinical Abstractors and Informatics Personnel

A 2024 HIMSS survey showed a 22% vacancy rate for documentation specialists, with hiring cycles exceeding 120 days. Certified Tumor Registrar shortages persist at 15%, compounded by retirements and competition from remote work. Q-Centrix’s expansion of outsourced services eases, but does not close, the gap because many registries still require rapid, in-house abstraction for decision support. AI tools reduce the manual load, yet accreditation rules still require human oversight to prevent the misclassification of complex cases. The lag in workforce development means constraints will continue through at least 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Registry: Pregnancy Registries Accelerate as FDA Streamlines Surveillance

Pregnancy and maternal-child registries experienced the fastest 14.65% CAGR to 2031, following the TEMPO pilot, which enabled obstetric-device sponsors to rely on registry data for post-market safety, thereby reducing compliance timelines. The Coordinated Registry Network’s FHIR guide further cut per-registry setup costs by 25% and enabled multi-sponsor collaboration. Disease registries retained 42.45% of the 2025 patient registry software market share, anchored by mature oncology and cardiovascular systems. Yet the regulatory tilt toward rare exposures favors pregnancy registries for sustained outperformance.

Oncology registries remain the largest disease sub-segment, while cardiovascular cohorts rapidly expand as structural-heart intervention data sets mature [3]American College of Cardiology, “National Cardiovascular Data Registry,” acc.org. Diabetes registries address device-data integration, and rare-disease groups collaborate across 24 European nations through ERDRI. Product registries for implants gain traction with EU conditional approvals, and quality-improvement programs evolve into real-time decision-support engines.

By Software Solution: Cloud SaaS Dominance Reflects Interoperability and Cost Pressures

Cloud-deployed platforms controlled 54.32% of 2025 patient registry software market share and are projected to grow at a 14.78% CAGR through 2031. Providers favor subscription pricing and automatic FHIR upgrades, while AI integration accelerates abstraction workflows. HEALWELL AI’s pending Orion Health acquisition unites 150 million lives on a global interoperability stack, illustrating scale advantages.

On-premise systems persist in defense and government settings where air-gapped networks are mandated; the DoD’s MHS GENESIS spans 3,600 sites worldwide. Hybrid models emerge, with edge nodes for low-latency capture and cloud analytics. Ireland’s registry roadmap recommends an OMOP-based cloud hub to end vendor lock-in and lower total cost.

By End User: Research Institutes Surge on Grant-Funded Cohorts and Precision Medicine

Hospitals accounted for 41.45% of 2025 revenue, while research institutes and academic medical centers led growth at a 15.65% CAGR, driven by NIH grants for precision-medicine cohorts. Projects such as Columbia University’s SC2K and Boston Children’s CumulusQ illustrate the convergence of registry and research data warehouses.

Pharma and device sponsors are the second-fastest segment, catalyzed by regulatory acceptance of registry-based external controls. Government agencies maintain steady use for public health surveillance, while specialty societies consolidate on multi-tenant SaaS to reduce per-registry costs. The shift highlights the rising demand for genomics integration, biospecimen tracking, and consent management that support large-scale precision medicine pipelines.

Geography Analysis

North America remained the largest region, accounting for 44.32% of the 2025 revenue, supported by CMS quality programs and the ACC’s multi-hospital cardiovascular network. HTI-4 and TEFCA sharply reduce data-exchange friction, while Canadian provinces consolidate on integrated records such as Alberta’s Netcare platform. Growth slows, however, as U.S. health systems prioritize EHR optimization over new registry rollouts amid budget pressure.

Asia-Pacific is the fastest-growing geography, advancing at a 13.54% CAGR through 2031. India’s ABDM has linked 6.5 billion health records, creating vast addressable cohorts for FHIR-enabled registries. Australia’s National Cancer Data Framework funds shared platforms, and China’s provincial-registry mandates expand demand despite localization constraints. Japan’s expansion of My Number health cards underpins registry readiness that accommodates kanji and hiragana data.

Europe accounts for approximately 25% of the patient registry software market. EHDS rules require registries to export OMOP datasets for secondary research by 2029, driving upgrades to open, cloud-native architectures. Ireland’s 2025 roadmap proposes a cloud hub across five disease areas to share costs, signaling broader regional consolidation. GDPR raises compliance expenses, yet clarity on pseudonymisation and federated queries speeds adoption. Emerging markets in the Middle East, Africa, and South America remain nascent but show proof-of-concept pilots supported by cloud infrastructure.

Regulatory Landscape

In the United States, registry platforms supporting regulated evidence generation are operating under a tightening mix of health IT and life-sciences requirements. The ONC HTI-4 Final Rule (effective August 2025) expanded USCDI to v4 and reinforced anti-information-blocking expectations around standardized access, which is pushing registry workflows toward FHIR-based ingestion and consent-aware APIs. On the life-sciences side, FDA guidance continues to formalize how real-world data from registries can support safety and regulatory decision-making. Expectations such as 21 CFR Part 11 for electronic records and signatures keep validation and audit trails central for registries used in clinical investigations.

In Europe, GDPR obligations and the European Health Data Space (EHDS) direction increase the emphasis on interoperable exchange, secure logging, and secondary-use governance. This elevates requirements for OMOP-compatible exports and federated query patterns already used in networks such as EMA DARWIN EU. Cross-border registry activation timelines remain sensitive to privacy and security expectations, and recent high-profile cyber incidents in healthcare have increased scrutiny of third-party processors, which strengthens demand for role-based access controls, traceability, and privacy-preserving linkage in registry implementations.

Value Chain Analysis

The value chain begins with data origination and capture inside hospitals, health systems, and specialty societies, where EHRs, lab systems, and imaging systems generate structured and unstructured inputs. Registry software vendors then deliver core capabilities, including cohort definition, data models such as OMOP, workflow and abstraction, analytics, and submission formats, along with integration layers such as FHIR, HL7 v2, ADT feeds, and APIs. Downstream participants include connectivity and linkage networks that enable privacy-preserving matching and enrichment, and end customers that operationalize outputs through government agencies and quality programs, academic medical centers, and life-sciences sponsors using registries for real-world evidence, post-market surveillance, and external comparators.

The main bottlenecks show up at ingestion and curation, driven by semantic variability across EHRs, inconsistent coding, and manual abstraction that remains constrained by workforce shortages and oversight requirements. This is increasing reliance on automation and partnerships across the chain, including privacy-preserving linkage collaborations (for example, Thermo Fisher Scientific with Datavant to incorporate tokenization within clinical research infrastructure) and investments to broaden de-identified research connectivity (for example, TriNetX collaborating with Regeneron on a network cited at roughly 300 million de-identified patients). Vendors are also productizing AI-enabled abstraction to reduce manual workload while keeping human-in-the-loop validation, with differentiation shifting toward interoperability accelerators, consent management, and audit-ready governance.

Competitive Landscape

The patient registry software market exhibits moderate fragmentation, with no vendor exceeding a 15% share, and strategies bifurcate between horizontal platforms and vertical, disease-specific solutions. Health Catalyst’s sequential buys of ERS and Carevive illustrate roll-up strategies that bundle abstraction labor with software. Carta Healthcare’s purchase of Realyze Intelligence pairs AI cohort matching with abstraction workflows, shortening trial recruitment cycles.

EHR giants Epic Systems and Oracle Health embed registry modules to secure installed bases, leveraging native data access while risking interoperability lock-in. Q-Centrix partners with Datavant for de-identified connectivity across 1,200 hospitals, merging services and RWE generation. Niche vendors differentiate via genomics linkage, biospecimen tracking, or consent dashboards that enhance patient engagement.

Ecosystem integration eclipses feature checklists; tenders increasingly demand FHIR Subscriptions, USCDI support, TEFCA endpoints, and OMOP compatibility. Ireland’s task force flagged prohibitive export costs from legacy systems, fueling demand for open-source alternatives. Vendors offering federated architectures gain an edge in privacy-sensitive regions such as the EU. At the same time, AI-first startups challenge incumbents by extracting structured variables directly from unstructured text and imaging.

Patient Registry Software Industry Leaders

IQVIA

Global Vision Technologies Inc.

FIGmd Inc.

Dacima Software Inc.

Image Trend Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability mandates and standards roadmaps create room for registry platforms that ship automated, standards-aligned extraction and submission rather than site-by-site custom interfaces. In the US, CMS Promoting Interoperability pathways that include active engagement with Clinical Data Registries (CDRs) tie performance reporting demand to registry connectivity, and ONC initiatives such as the 2026 Standards Version Advancement Process (SVAP) (opening voluntary adoption of updated US Core standards beginning August 29, 2026) increase the cadence of standards updates that vendors need to operationalize. These conditions favor cloud-deployed SaaS offerings and vendors that can package FHIR-based ingestion, consent-aware APIs, and submission tooling as repeatable modules.

Cross-border and multi-stakeholder programs also expand the need for interoperable registries that support OMOP export and federated governance, consistent with the EHDS framework adopted as EU Regulation 2025/327. Concrete opportunity areas include automated registry extraction and data submission using HL7 implementation guides such as the FHIR Registry Protocols and CREDS, along with embedded consent automation to reduce friction in secondary use, supported by industry guidance such as The Sequoia Project work on automated patient consent. Another near-term commercialization lane is attaching registries to expanding HIE footprints (for example, the Florida HIE transition to CRISP Shared Services beginning July 1, 2026) so registries can ingest more complete longitudinal records without one-off agreements.

Recent Industry Developments

- July 2026: FIGmd confirmed its Polaris platform status as a CMS-approved Qualified Registry (QR) for the 2026 MIPS reporting year, strengthening its position in US quality reporting workflows. The designation supports provider participation in Promoting Interoperability and performance programs that depend on registry submissions, and it can help FIGmd compete in hospital and ACO accounts that prioritize compliance-ready reporting infrastructure.

- December 2025: WellSky partnered with uMed to expand patient access to national clinical research registries through at-home participation workflows. The collaboration links WellSky's healthcare software footprint with uMed's automated registry platform, supporting direct-to-patient recruitment and data capture that aligns with decentralized research and longitudinal real-world evidence collection.

- June 2024: OM1 launched a Registries Center of Excellence (CoE) to provide specialized registry consulting and operational expertise alongside its RWE and AI capabilities. By bundling services with registry know-how, the CoE model supports faster registry stand-up, governance, and analytics adoption for sponsors and providers that face abstraction and data-quality constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid software used to build, run, and maintain patient registries that capture standardized patient data over time for clinical care improvement, research, and reporting needs. It includes registry creation, data capture, management, and reporting functions delivered through common deployment models.

Scope exclusions: We exclude general EHR or practice management licensing that is not directly tied to operating a patient registry, along with purely consulting-only programs without software revenue.

Segmentation Overview

- By Type Of Registry

- Disease Registries

- Health Service Registries

- Product Registries

- Quality Improvement Registries

- Pregnancy & Maternal-Child Registries

- By Software Solution

- Stand-Alone Registry Software

- Integrated EHR-Embedded Software

- Cloud-Deployed SaaS Platforms

- On-Premise Installed Systems

- By End User

- Hospitals & Health Systems

- Government Agencies & Third-Party Administrators

- Pharmaceutical, Biotechnology & Medical-Device Firms

- Research Institutes & Academic Medical Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first shape of the demand pool and to pin down how registry programs are being funded and adopted across health systems and life sciences. We relied on public sources such as the US Centers for Disease Control and Prevention, the US National Institutes of Health, the US Food and Drug Administration, the World Health Organization, and OECD health statistics for signals on disease burden, real world evidence needs, and data program maturity.

We also reviewed non-paywalled materials like company annual reports, investor presentations, product documentation, procurement announcements, and reputable healthcare IT press to understand typical buying cycles and deployment preferences. Where needed, subscription datasets were used only as support for company financials and intelligence, patent lookups, and tender tracking, so revenue mix and product focus could be cross-checked without overstating precision. These sources are illustrative, and many other public and paid references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with software suppliers, healthcare provider IT and informatics teams, registry program managers, and research stakeholders who use registry outputs for outcomes and reporting. Inputs were used to confirm adoption drivers, including integration needs and data governance, and to test pricing logic across stand-alone and EHR-embedded setups, with coverage balanced across the Americas, EMEA, and APAC to avoid single-region bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 45% |

| Mid tier: 54% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 16% | Managers: 53% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where healthcare digitization and registry program formation are reconstructed through demand indicators, then allocated into software spend based on observed adoption and budgeting patterns. The totals are pressure-tested with selective bottom-up approximations using sampled vendor revenue disclosure, channel checks, and a simple ASP times active-customer count logic for typical deployments, which helps adjust for over-counting.

A few inputs that mattered most included the number of active registry programs by care area, the share of registries run as cloud subscription versus on-premise installations, average contract value ranges by end user group, including providers, government and third-party administrators, and life sciences, and integration intensity with EHR workflows. We also tracked typical renewal and expansion behavior for analytics and reporting modules. When a bottom-up view is incomplete for smaller suppliers, gaps are handled through conservative expansion factors tied back to observed procurement activity and validated interview ranges.

Forecasts are produced using scenario analysis supported by light trend fitting, where macro indicators like healthcare IT spending direction, policy and reporting requirements, and real world evidence adoption are combined with primary inputs on expected pricing progression and migration to SaaS. Where a driver moves faster than expected, the scenario assumptions are revisited, and the central case is updated before final sign-off.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, then structured variance checks at the region and end user levels so the model stays aligned with realistic buying capacity. Outliers are reviewed in more than one analyst pass, and any large step changes trigger re-contact with relevant respondents to confirm whether the shift is real or model-driven.

The report is refreshed annually, and interim updates are made when material events change pricing, demand, or regulatory reporting needs. Before delivery, we run a final update sweep so clients receive the most current view available at the time of publication.

Mordor Intelligence's Patient Registry Software Market Size Measured Against Other Published Estimates

Published market sizes for patient registry software can differ by a wide margin because firms do not always count the same revenue streams, time periods, and delivery models. Differences also show up when one estimate is anchored on provider-focused deployments and another leans more toward research and population health use cases.

Some sources roll population registry and broader health information exchange functionality into the same value, which lifts the number and changes the implied adoption curve. In Mordor Intelligence, revenue is counted only when it is directly tied to patient registry software across defined registry types, deployment modes, and end users, and adjacent enterprise platforms that are not sold as registry software are not added in.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.95 B (2025) | |

| Global Consultancy A | USD 3.78 B (2025) | Uses a broader functional scope that appears to bundle population registry and adjacent health information exchange or care management functionality, which inflates spend beyond registry software contracts. |

| Industry Research Group B | USD 2.40 B (2024) | Anchors on an earlier base year and applies a faster growth path, and it is less clear how mixed software and related services revenue are separated when vendors sell combined packages. |

The spread across the table is mainly explained by what gets bundled into the definition, and by the choice of base year and growth posture. By keeping the inputs tied to observable registry program adoption, deployment mix, and contract value ranges that can be rechecked, the estimate stays easier to replicate and interpret for planning.

Key Questions Answered in the Report

How big is the patient registry software market in 2026?

The patient registry software market size is USD 2.18 billion in 2026 and is forecast to reach USD 3.94 billion by 2031.

Which registry type is growing the fastest?

Pregnancy and maternal-child registries lead growth at a 14.65% CAGR through 2031 after the FDA's TEMPO pilot reduced surveillance costs.

Why are cloud-deployed platforms so dominant?

Cloud SaaS captures 54.32% of 2025 revenue because it lowers capital costs, delivers automatic FHIR upgrades, and supports rapid scaling.

Which region offers the highest growth potential?

Asia-Pacific is projected to expand at a 13.54% CAGR to 2031, driven by India's ABDM and broader national digitization programs.

How is AI affecting registry operations?

AI-enabled abstraction cuts data-curation time by up to 40% and helps smaller hospitals launch registries despite abstractor shortages.

What are the main barriers to wider adoption?

Privacy concerns, abstractor shortages, vendor lock-in, and inconsistent data quality each exert downward pressure on growth.

Page last updated on: