Clinical Trial Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

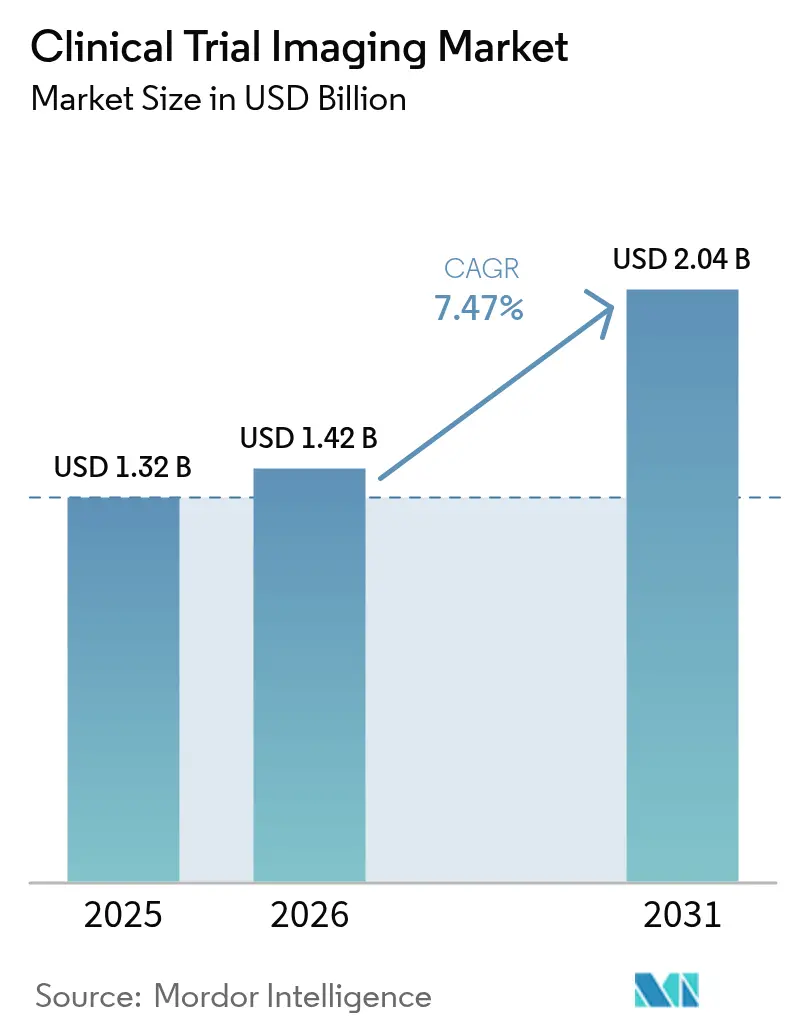

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 2.04 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Trial Imaging Market Analysis by Mordor Intelligence

The clinical trial imaging market size is expected to grow from USD 1.32 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 2.04 billion by 2031 at 7.47% CAGR over 2026-2031. This expansion mirrors the surge in global pharmaceutical R&D budgets, the growing use of imaging biomarkers in complex studies, and the steady migration toward AI-enabled data analysis. Oncology and neurology trials dominate demand because they rely on visual endpoints to prove therapeutic value, while decentralized and hybrid trial models are widening access to patient pools and accelerating enrollment timelines. AI adoption is speeding image interpretation, cutting reader variability, and improving protocol compliance across multi-site programs. Consolidation among imaging core laboratories and modality vendors is intensifying as firms bundle hardware, software, and analytics to deliver end-to-end services. Regulatory shifts—most notably the European Union Clinical Trials Regulation (EU CTR)—are harmonizing processes across borders and encouraging standardized imaging workflows.

Key Report Takeaways

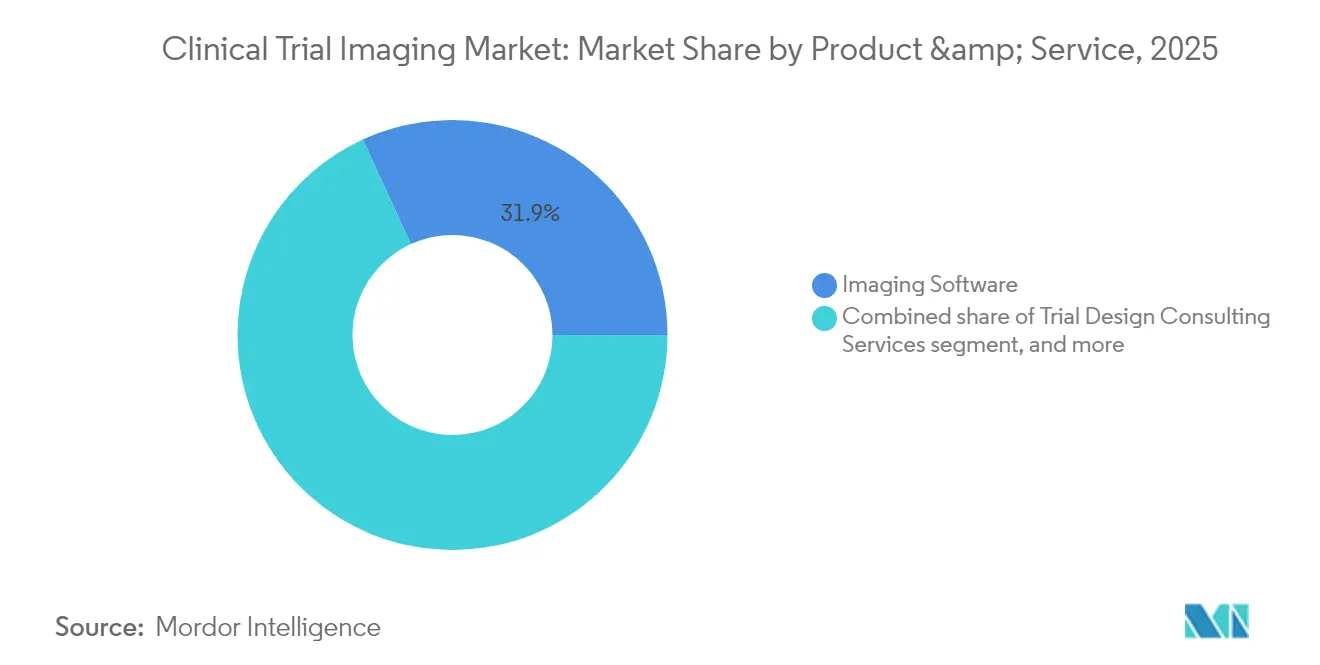

- By product & service, imaging software held 31.85% of the clinical trial imaging market size in 2025, while imaging biomarker development services are projected to climb at a 9.21% CAGR to 2031.

- By modality, computed tomography commanded 24.70% of the clinical trial imaging market size in 2025; positron emission tomography is advancing at a 9.29% CAGR between 2026-2031.

- By end-user, pharmaceutical & biotechnology companies captured 48.10% of clinical trial imaging market share in 2025, whereas contract research organizations are anticipated to grow at an 10.78% CAGR to 2031.

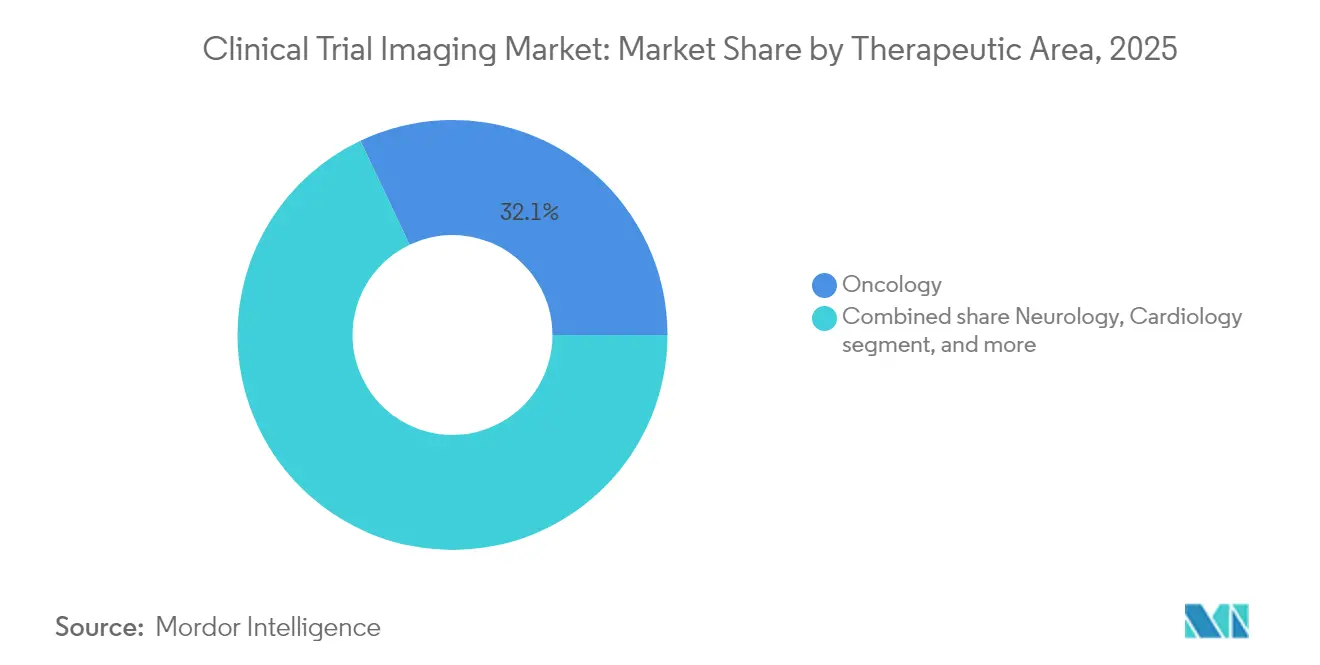

- By therapeutic area, oncology generated 32.05% of the clinical trial imaging market size in 2025, yet rare diseases are forecast to post a 9.93% CAGR through 2031.

- By trial phase, phase III studies accounted for 40.95% of the clinical trial imaging market size in 2025, while phase I studies are on track for a 10.12% CAGR during 2026-2031.

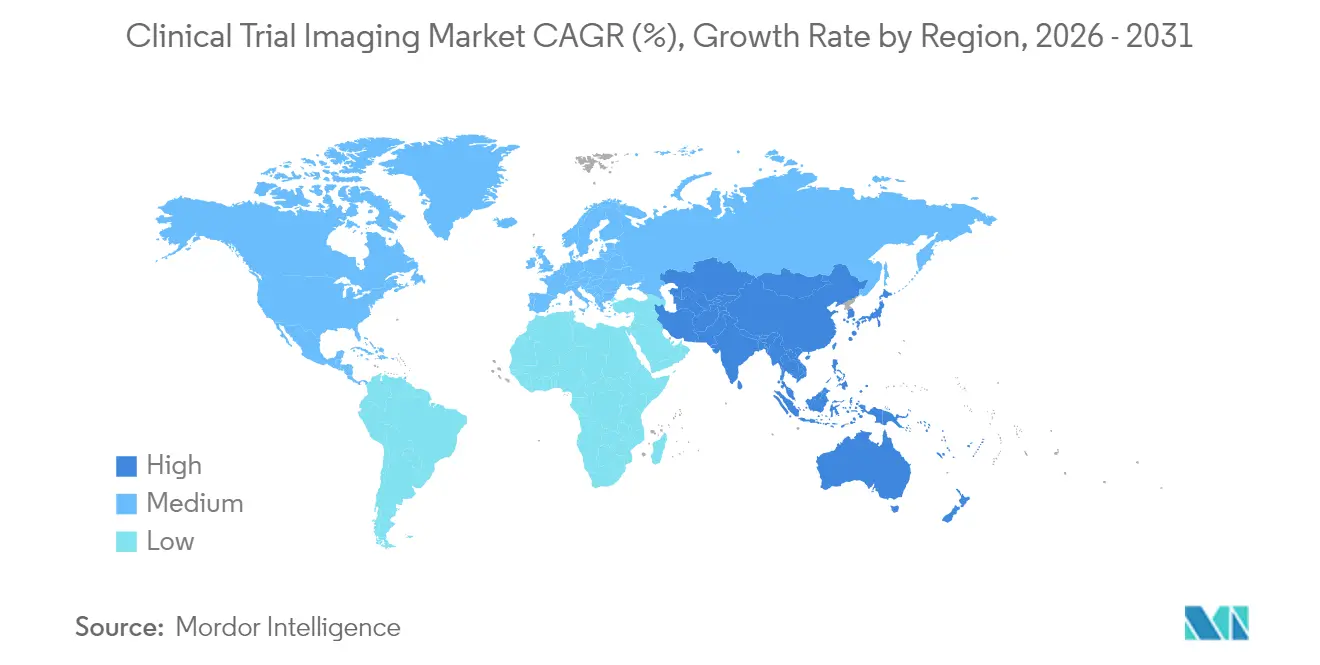

- By geography, North America led with 38.10% of clinical trial imaging market share in 2025, yet Asia-Pacific is forecast to expand at an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clinical Trial Imaging Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Pharmaceutical And Biotechnology R&D Expenditure | +2.1% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Growing Outsourcing Of Imaging Services To Contract Research Organizations | +1.8% | Global; strong in Asia-Pacific & North America | Medium term (2-4 years) |

| Technological Advancements In Medical Imaging Modalities | +1.5% | Global; innovation hubs in North America & Europe | Medium term (2-4 years) |

| Rising Adoption Of Artificial Intelligence In Clinical Trial Imaging | +1.3% | Global; early uptake in North America | Short term (≤ 2 years) |

| Growth In Oncology And Neurology Clinical Trials | +0.9% | Global; high activity in Asia-Pacific & Europe | Medium term (2-4 years) |

| Expansion Of Decentralized And Hybrid Clinical Trial Models | +0.7% | Global; accelerated in Asia-Pacific post-pandemic | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Pharmaceutical and Biotechnology R&D Expenditure

R&D budgets climbed 9.7% in 2024 among large drug makers, and pipelines now exceed 8,000 active assets, deepening demand for imaging endpoints that objectively track therapeutic impact. Biologics and gene therapies—expected to represent more than 60% of new approvals by 2030—often require molecular-level visualization, pushing sponsors to secure sophisticated imaging core lab support. Leading firms such as Eli Lilly have extended investments in GLP-1 programs, and each protocol embeds specialized MRI or PET components to monitor metabolic and cardiovascular parameters. As outsourcing grows, suppliers able to scale imaging services across continents stand out, with over 80% of R&D executives planning double-digit spending increases on external partners. This funding momentum anchors a long-term tailwind for the clinical trial imaging market.

Growing Outsourcing of Imaging Services to Contract Research Organizations

CRO revenues hit USD 52.19 billion in 2023, reflecting a strategic pivot by drug developers toward external imaging expertise to cut fixed costs and speed trial execution[1]ICON plc, “2024 Annual Report,” iconplc.com. ICON alone reported USD 9.974 billion in new business wins during 2024, underscoring sponsor appetite for integrated imaging networks capable of protocol harmonization, real-time QC, and automated AI analytics. Outsourcing can trim study timelines by up to 30% by centralizing image data and applying predefined read algorithms, advantages magnified in hybrid and decentralized models that collect scans from community sites and patients’ homes. CROs are matching demand with targeted acquisitions in teleradiology, ophthalmic imaging, and quantitative biomarker platforms to widen service breadth across therapeutic areas.

Technological Advancements in Medical Imaging Modalities

Photon-counting CT scanners cut radiation dose while boosting spatial resolution, a breakthrough for longitudinal pediatric trials where cumulative exposure is a concern. PET-MRI hybrids deliver concurrent functional and anatomic data, simplifying patient visits and enhancing endpoint correlation in neuro-oncology programs. Portable MRI and low-payload CT units are extending trial reach to rural regions, broadening recruitment and supporting decentralized designs. Novel radiotracers, including PSMA agents for prostate cancer and FAPI compounds for fibrosis mapping, enrich biomarker toolkits and enable earlier treatment-response readouts[2]Journal of Nuclear Medicine, “Total-Body PET and Emerging Radiotracers,” jnm.snmjournals.org. These innovations unlock new endpoints and improve data precision, reinforcing technology’s positive pull on the clinical trial imaging market.

Rising Adoption of Artificial Intelligence in Clinical Trial Imaging

More than half of healthcare organizations now deploy AI in at least one imaging workflow, compared with 17% in 2018. In trials, AI automates QC, flags protocol deviations, and extracts quantitative biomarkers in seconds, shrinking analysis bottlenecks and lowering inter-reader variability. ICON’s AI suite manages document routing, forecasts staffing needs, and supplies on-demand read analytics, while GE HealthCare’s acquisition of MIM Software brings deep-learning segmentation and dosimetry tools under one roof. Regulatory confidence is rising: the FDA lists more than 300 cleared AI imaging devices, and Europe has issued guidance on AI use in the product lifecycle[3]European Medicines Agency, “Clinical Trials Regulation,” ema.europa.eu. Although most sponsors remain in pilot phases, growing confidence in validation frameworks signals rapid AI scale-up over the next two years.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment And Operational Costs Of Imaging Equipment | -1.4% | Global; hardest for smaller CROs & academic centers | Long term (≥ 4 years) |

| Shortage Of Skilled Imaging Professionals | -0.8% | Global; most acute in North America & Europe | Medium term (2-4 years) |

| Stringent Regulatory And Data Privacy Requirements | -0.6% | Global; heightened in EU & North America | Medium term (2-4 years) |

| Lack Of Standardized Imaging Protocols Across Trial Sites | -0.5% | Global; multi-center studies worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Operational Costs of Imaging Equipment

State-of-the-art PET-MRI systems can cost USD 4-6 million, and photon-counting CT platforms add another USD 2-3 million burden before siting, shielding, and maintenance are factored in. Nuclear medicine programs require on-site radiopharmaceutical facilities that meet stringent cGMP standards, lifting total start-up spending far beyond many regional CROs or academic core labs. Rapid hardware cycles further complicate ROI calculations, pushing stakeholders toward mergers or strategic alliances, as seen in Affinity Equity Partners’ USD 658 million purchase of Lumus Imaging aimed at gaining scale economies.

Shortage of Skilled Imaging Professionals

Complex trial protocols depend on technologists, physicists, and image analysts versed in Good Clinical Practice, multi-modal acquisition, and regulatory submission standards. Despite growth initiatives, global supply trails demand, with vacancies highest in nuclear medicine and advanced MRI specialties. ICON employs more than 450 imaging experts, yet reports persistent recruitment strain in North America and Western Europe. Remote scanning supervision platforms and AI-guided acquisition workflows alleviate staffing gaps, but their deployment calls for regulatory approvals and secure data pathways, presenting an additional hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Software Dominance Drives Innovation

Imaging software accounted for 31.85% of the clinical trial imaging market in 2025, cementing its status as the backbone of data flow across global sites. These platforms automate QC, anonymize datasets, and integrate seamlessly with electronic data capture systems, lowering error rates and ensuring consistency. In revenue terms, the segment formed the largest slice of the clinical trial imaging market size, and its influence will grow as AI modules move from pilot to production. The rise of SaaS deployment models is shifting budgets from capex to opex, appealing to small and mid-sized sponsors seeking scalability without heavy infrastructure outlay.

Imaging biomarker development services, meanwhile, are projected to expand at a 9.21% CAGR, reflecting escalating demand for validated, quantitative endpoints capable of persuading regulators and payers. Underpinning this surge are FDA initiatives that underscore the value of imaging biomarkers in accelerated approvals, and the movement toward personalized therapies that require sensitive measures of treatment response. Vendors that fuse software, biomarker science, and regulatory consulting are capturing higher-margin projects, intensifying competition in this growth pocket of the clinical trial imaging market.

By Modality: CT Leadership Faces PET Innovation Challenge

Computed tomography held 24.70% of the clinical trial imaging market in 2025 thanks to its ubiquity, rapid acquisition times, and validated role in solid tumor trials. Its dominance also stems from reimbursement support and wide reader familiarity, factors essential to large phase III studies. Even so, the modality’s share is slowly eroding as sponsors pivot to lower-dose photon-counting systems and hybrid imaging that better resolve soft-tissue changes.

Positron emission tomography is expected to post a 9.29% CAGR through 2031, the fastest among modalities. Growth hinges on a pipeline of novel radiotracers that move beyond glucose metabolism to target cell-surface receptors, hypoxia markers, and amyloid aggregates. PET’s sensitivity in detecting molecular changes ahead of anatomical shifts makes it invaluable for early dose-response studies and adaptive trial designs. The spread of total-body PET scanners, which cut dose and bolster throughput, further sharpens its appeal and enlarges its role within the clinical trial imaging market.

By End-User: Pharma Dominance Meets CRO Acceleration

Pharmaceutical and biotechnology sponsors generated 48.10% of clinical trial imaging market revenue in 2025 by directly funding core lab contracts, technology licenses, and equipment leases tied to their R&D portfolios. Their in-house imaging groups oversee protocol development and vendor management but increasingly partner with technology suppliers to integrate AI and cloud delivery. The expansion of GLP-1 and monoclonal antibody pipelines keeps imaging budgets robust, especially for metabolic, cardiovascular, and oncology programs.

Contract research organizations are the fastest-growing constituency, projected at an 10.78% CAGR through 2031. CROs absorb imaging responsibilities for small to mid-tier biotechs that lack internal expertise, and they offer global site networks, standardized SOPs, and consolidated data hubs. Strategic acquisitions—such as Clario’s purchase of NeuroRx—broaden therapeutic specialization and strengthen neurology capabilities, allowing CROs to capture emerging rare-disease opportunities poised to reshape the clinical trial imaging market.

By Therapeutic Area: Oncology Leads While Rare Diseases Surge

Oncology contributed 32.05% of clinical trial imaging market revenue in 2025, cementing its primacy due to the modality-intensive nature of solid tumor assessments. RECIST metrics, bone lesion detection, and theranostic radiopharmaceuticals make imaging indispensable throughout oncology drug lifecycles. Immuno-oncology combinations and tissue-agnostic indications continue to propel imaging demand, with total-body PET and AI-assisted CT enabling earlier response readouts that inform mid-study dose adjustments.

Rare diseases, however, will outpace all other segments at a 9.93% CAGR because regulatory incentives and smaller patient pools magnify the utility of sensitive imaging biomarkers. NIH funding schemes encourage biomarker validation for conditions such as Friedreich’s ataxia and Huntington’s disease, prompting institutions like Biospective to develop sub-millimeter MRI protocols tailored to these populations. Precision endpoints derived from high-resolution neuroimaging reduce trial sizes and attenuate placebo effects, positioning this niche for outsized influence on the clinical trial imaging market.

By Phase of Clinical Trial: Phase III Dominance Meets Phase I Innovation

Phase III programs consumed 40.95% of clinical trial imaging market outlays in 2025 because pivotal studies require global site harmonization, blinded independent central review, and rigorous archiving to satisfy regulators. These late-stage budgets accommodate multiple modalities, repeat scanning, and data locks synchronized to interim analyses, all of which inflate imaging spend. Sponsors also commission endpoint adjudication committees and duplicate reads to shore up data integrity ahead of marketing authorization submissions.

Phase I studies are forecast to register a 10.12% CAGR through 2031 as imaging biomarkers shift upstream to guide dose selection and patient stratification. Whole-organ perfusion MRI, dynamic contrast-enhanced CT, and molecular PET enable non-invasive quantification of early pharmacodynamic signals, reducing reliance on invasive biopsies. AI-driven image analysis accelerates read turnaround, allowing real-time dose-escalation decisions in adaptive study designs. Together, these developments will enlarge the proportion of early-phase resources devoted to imaging and bolster innovation across the clinical trial imaging market.

Geography Analysis

North America retained 38.10% of global revenue in 2025 on the strength of mature reimbursement systems, a dense network of academic-industrial partnerships, and clear FDA guidance governing imaging endpoints. The United States also hosts many of the top 20 pharma sponsors, amplifying domestic demand for high-throughput core labs that can scale across therapeutic franchises. Private-equity investments and acquisitions—RadNet spent USD 54 million on targets in 2024—are consolidating imaging capacity and integrating AI platforms, deepening the region’s competitive moat.

Asia-Pacific is projected to deliver the highest regional CAGR at 8.55% through 2031, propelled by streamlined ethics approvals and attractive cost structures. Regulatory agencies in Japan, South Korea, and Singapore routinely finalize clinical trial applications within six months, shortening study start-up compared with legacy markets. Local CROs such as Wuxi AppTec have scaled imaging units that serve domestic and Western sponsors alike, leveraging broad site networks and government incentives to host multinational programs. The growing popularity of decentralized trials, tele-radiology, and bring-your-own-device imaging apps augments APAC’s role in the clinical trial imaging market.

Europe sits between these poles as it transitions to the EU CTR, which mandates full use of the Clinical Trials Information System by January 2025. The unified portal promises consistent application reviews across 30 countries and should lower administrative overhead on cross-border imaging protocols. Yet divergent rules governing radiopharmaceutical handling and data privacy remain obstacles, particularly in Germany and France. Efforts by the EMA to publish an AI reflection paper and clarify validation expectations indicate that Europe aims to retain a leadership position in governance even as operational execution evolves.

Competitive Landscape

The clinical trial imaging market features moderate fragmentation, with the top five suppliers controlling an estimated 45-50% of global revenue. Competitive intensity is rising as equipment manufacturers move upstream into software and analytics, while CROs push downstream into modality ownership to secure margin and lock in clients. Clario, ICON Medical Imaging, and IXICO are global benchmarks thanks to therapeutic breadth, proprietary platforms, and geographic reach. Their differentiation hinges on integrated AI algorithms that normalize data from disparate scanners and automate volumetric reads across oncology, neurology, and cardiology domains.

Strategic M&A is reshaping the field. GE HealthCare’s acquisition of MIM Software adds AI-powered 3D segmentation and dosimetry tools to its platform, enabling seamless workflows from scanner to analytics. RadNet’s USD 103 million iCAD deal deepens breast-imaging AI capability and illustrates a broader pattern of modality specialists acquiring algorithm developers to protect future revenue streams. Clario’s purchase of NeuroRx sharpens its focus on neurodegenerative research by absorbing advanced fMRI and PET infrastructure, while ONRAD’s takeover of Direct Radiology creates the largest independent teleradiology network in the United States, a boon for remote trial oversight.

White-space opportunities lie in blockchain-secured image repositories, which promise tamper-proof audit trails suited to regulatory audits, and in end-to-end decentralized imaging kits that pair portable scanners with cloud-native AI readers. Vendors able to wrap these capabilities into flexible, region-compliant service offerings stand to capture premium contracts as sponsors demand turnkey solutions throughout the clinical trial imaging market.

Clinical Trial Imaging Industry Leaders

Clario

Icon plc

Parexel International Corp.

Medpace Holdings, Inc.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: HOPPR secured USD 31.5 million to expand its AI medical imaging development platform, signaling investor confidence in advanced analytics for clinical trials.

- April 2025: Chipiron raised USD 17 million to commercialize a portable MRI scanner, potentially eliminating siting barriers for remote trial imaging.

- April 2025: RadNet agreed to acquire iCAD for USD 103 million in an all-stock transaction, enhancing AI-based breast-imaging services.

- March 2025: Clario purchased NeuroRx to strengthen neuro-imaging capabilities for Alzheimer’s and Parkinson’s studies.

- January 2025: ONRAD acquired Direct Radiology from Philips, forming the largest U.S. teleradiology provider and expanding remote imaging oversight capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the clinical trial imaging market as all paid services and software that plan, acquire, manage, and read medical images expressly for human interventional and observational drug or device trials. The count covers centralized imaging core labs, cloud-based workflow platforms, biomarker development services, and related analytics that translate images into trial endpoints.

Scope exclusion: Capital purchases of imaging scanners used mainly for routine diagnosis or pre-clinical animal studies are excluded.

Segmentation Overview

- By Product & Service

- Trial Design Consulting Services

- Read Analysis Services

- Operational Imaging Services

- Imaging Software

- Imaging Data-management Services

- Imaging Biomarker Development Services

- By Modality

- Magnetic Resonance Imaging

- Computed Tomography

- Positron Emission Tomography

- Ultrasound

- Echocardiography

- Other Modalities

- By End-User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Medical Device Manufacturers

- Academic & Government Research Institutes

- By Therapeutic Area

- Oncology

- Neurology

- Cardiology

- Endocrinology & Metabolic Disorders

- Rare Diseases

- Other Therapeutic Areas

- By Phase of Clinical Trial

- Phase I

- Phase II

- Phase III

- Phase IV

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed imaging scientists at global pharma sponsors, project managers within imaging core labs, CRO procurement leads, and radiology chiefs at major academic sites across North America, Europe, and Asia Pacific. The conversations clarified price dispersion, protocol complexity trends, and modality preferences, which we used to tighten model assumptions and cross-check desk findings.

Desk Research

We pulled foundation data from open statistics issued by the US National Library of Medicine's ClinicalTrials.gov, the European Clinical Trials Register, and Japan's PMDA trial database, which list trials that mandate imaging. Trade bodies such as the Medical Imaging & Technology Alliance and the Association of Clinical Research Organizations offered annual trend briefs on imaging outsourcing. Regulatory guidance notes from the US FDA and EMA, combined with peer-reviewed articles in Radiology and The Lancet Digital Health, helped our analysts map accepted imaging endpoints. Paid feeds from D&B Hoovers and Dow Jones Factiva supplied company revenue splits for leading imaging core labs. This list is illustrative; many further public and paid references informed desk validation.

Market-Sizing & Forecasting

Our bottom-up build multiplies the number of actively recruiting trials by average images per patient and contracted price per image set, which are then rolled up by phase and therapy area. A parallel top-down pass benchmarks global sponsor spending on clinical services and estimates the imaging slice by modality share. Key variables include trial starts by phase, average imaging sessions per patient, modality mix shifts toward PET and MRI, outsourcing penetration into iCROs, and prevailing image read turnaround times. We forecast with a multivariate regression that factors oncology trial growth, R&D spending, and regulatory cycle times. Where bottom-up data were thin, we back-solved values from published core-lab revenues and adjusted with price insights from primary calls.

Data Validation & Update Cycle

Outputs run through variance checks against historical spend ratios and public filings before senior review. Reports refresh annually, with mid-cycle updates if material events such as large M&A or new FDA imaging guidance alter the baseline.

Why Our Clinical Trial Imaging Baseline Inspires Confidence

Published estimates often diverge because firms vary service scope, treat scanner sales as market revenue, or apply different currency years.

Key gap drivers include Mordor's trial-level build versus others' revenue extrapolations, our exclusion of diagnostic equipment sales, and our yearly refresh cadence that captures emerging decentralized imaging workflows.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.32 B (2025) | Mordor Intelligence | - |

| USD 1.23 B (2024) | Global Consultancy A | Omits software licensing and Asia Pacific trials, leading to understated base |

| USD 1.42 B (2024) | Industry Association B | Adds imaging hardware procurement and hybrid pre-clinical work, inflating total |

The comparison shows that when scope aligns strictly with in-trial imaging services and software, our balanced bottom-up and top-down approach delivers a transparent, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the clinical trial imaging market?

The clinical trial imaging market is valued at USD 1.42 billion in 2026 and is forecast to grow to USD 2.04 billion by 2031 at a 7.47% CAGR.

Which product segment leads the market?

Imaging software holds the largest share at 31.85% because it underpins standardized data capture, QC, and AI analytics across global sites.

Why is Asia-Pacific the fastest-growing region?

Streamlined ethics approvals, lower study costs, and strong government support are driving an 8.55% CAGR in Asia-Pacific through 2031.

How is AI influencing clinical trial imaging?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which modality is expanding the fastest?

Positron emission tomography is set to grow at a 9.29% CAGR due to novel radiotracers and total-body scanner adoption that improve sensitivity and lower radiation dose.

What is the main restraint facing the market?

High capital and operational costs of advanced imaging equipment, especially PET-MRI and photon-counting CT systems, limit entry for smaller centers and raise overall trial expenses.

Page last updated on: