AI In Clinical Trials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

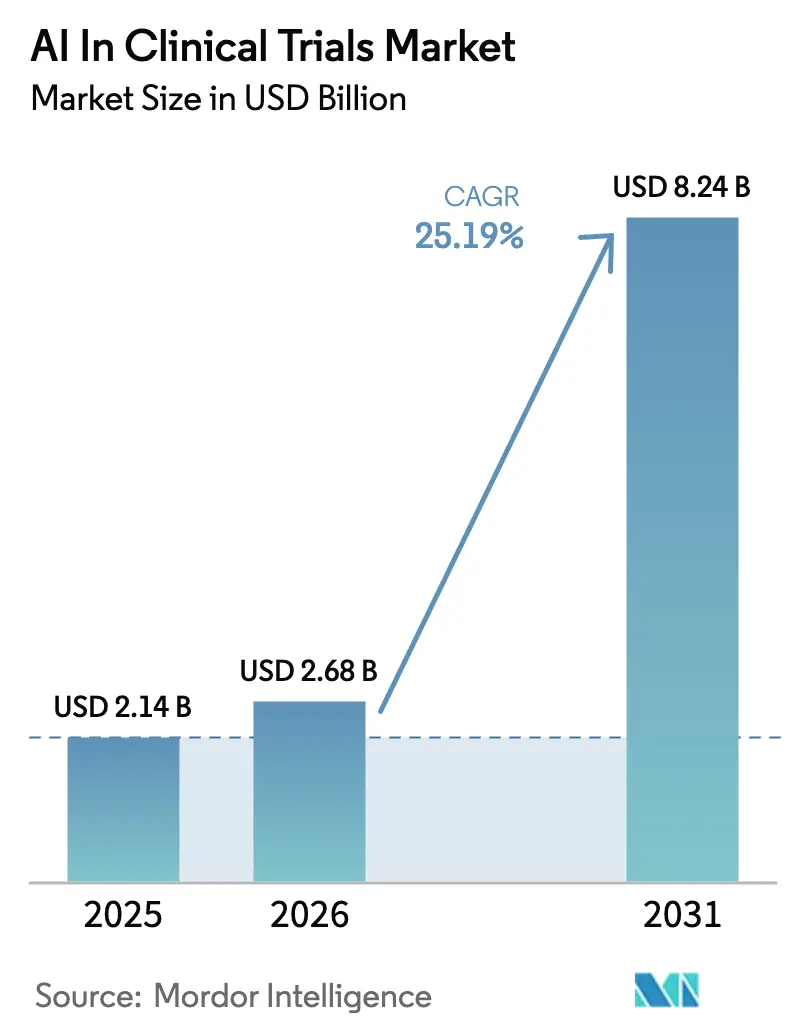

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 8.24 Billion |

| Growth Rate (2026 - 2031) | 25.19% CAGR |

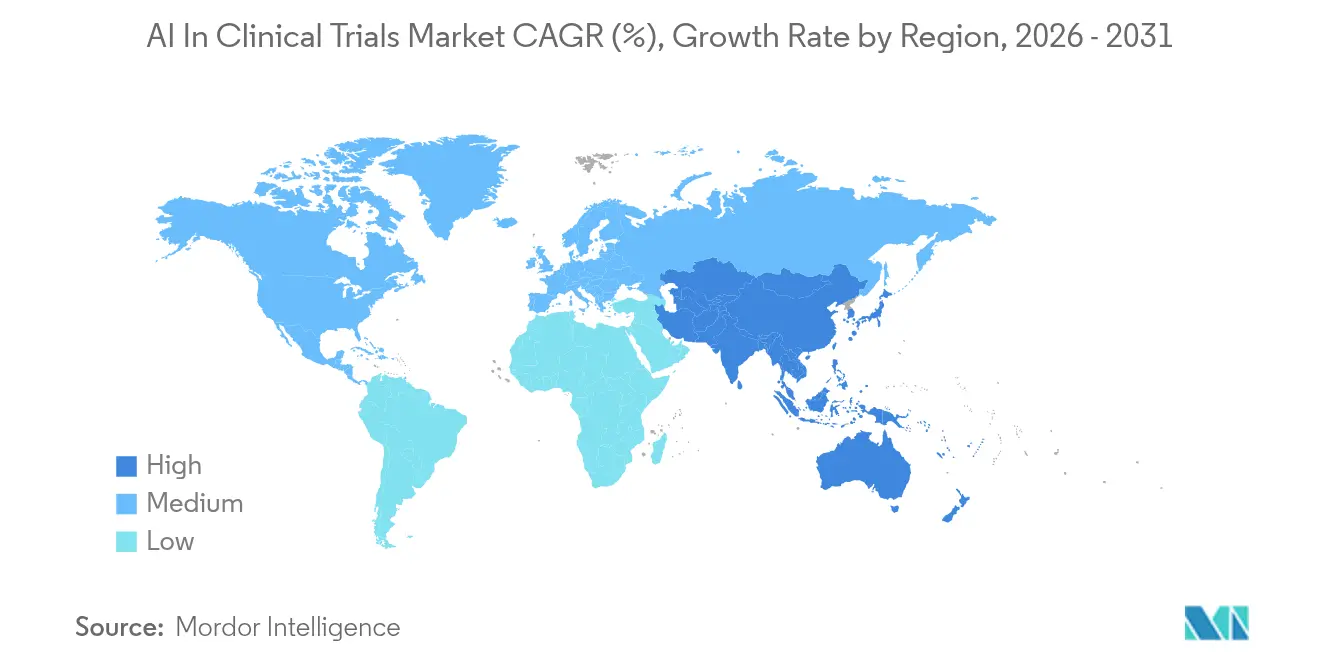

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Trials Market Analysis by Mordor Intelligence

AI in clinical trials market size in 2026 is estimated at USD 2.68 billion, growing from 2025 value of USD 2.14 billion with 2031 projections showing USD 8.24 billion, growing at 25.19% CAGR over 2026-2031. This momentum reflects the pharmaceutical sector’s shift toward data-driven drug development that compresses timelines and curbs escalating R&D expense. Broader regulatory acceptance of synthetic control arms, coupled with foundation models tailored for patient stratification and endpoint prediction, accelerates adoption. Cross-industry alliances are redrawing competitive lines as technology-first entrants challenge traditional CROs, while cloud-hosted AI platforms deliver scalability for mid-sized sponsors. Oncology remains the largest therapeutic focus, yet infectious-disease programs are expanding fastest on pandemic-forged regulatory pathways. The pace of innovation is further amplified by real-world data streams from EHRs and wearables, which enrich trial datasets and improve predictive accuracy.

Key Report Takeaways

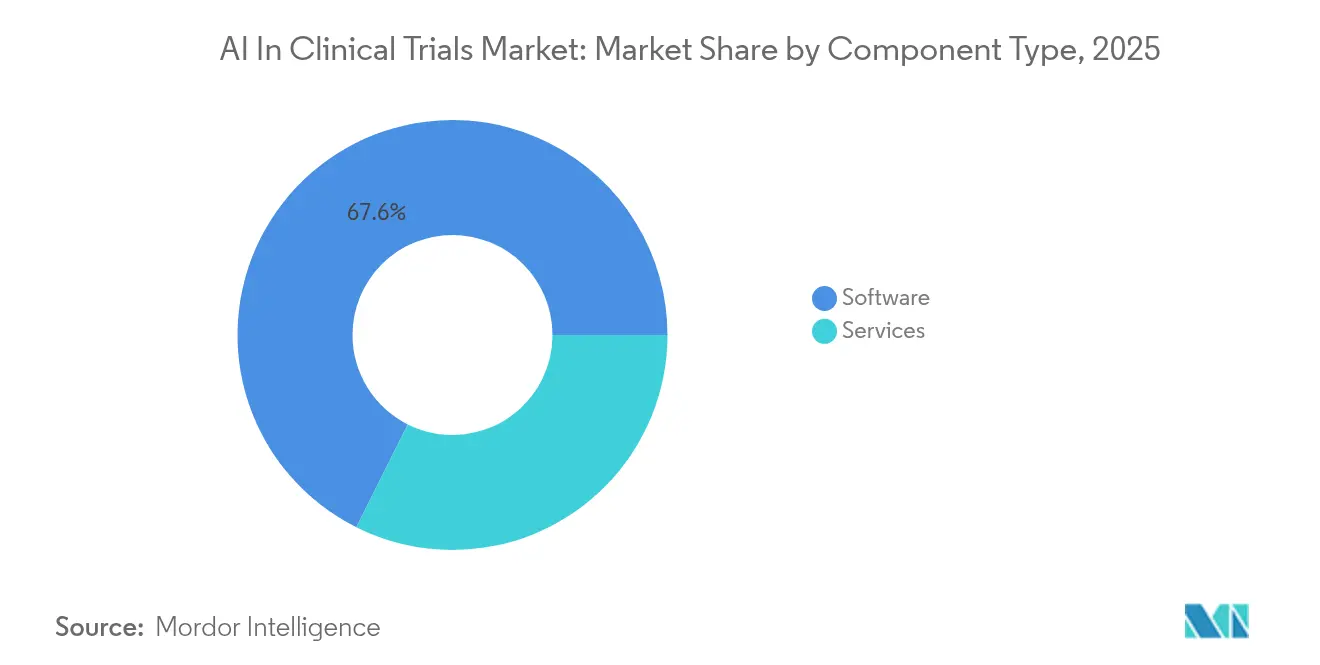

- By component type, software captured 67.62% of revenue in 2025, while services are projected to advance at a 26.61% CAGR through 2031.

- By therapeutic area, oncology led with 36.78% revenue share in 2025; infectious diseases are forecast to grow at a 26.2% CAGR to 2031.

- By clinical phase, Phase III accounted for 54.62% of revenue in 2025, whereas Phase I is expected to expand at a 25.43% CAGR through 2031.

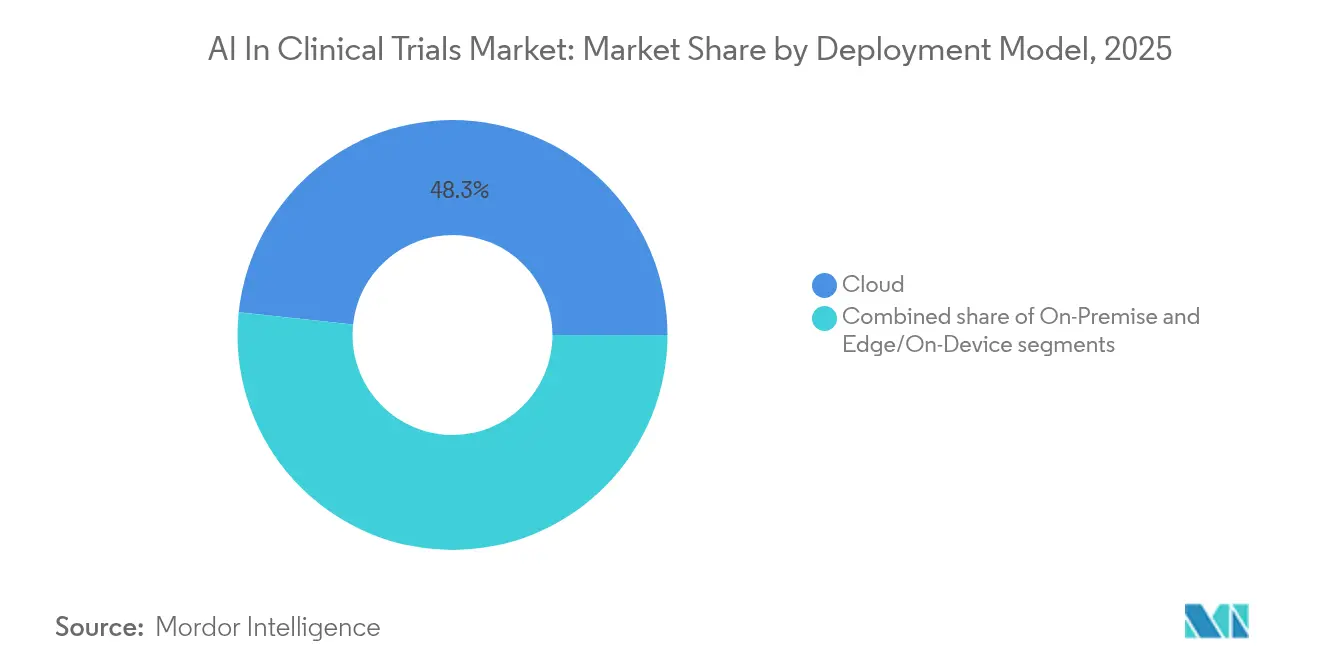

- By deployment model, cloud solutions held 48.32% revenue share in 2025, while on-premise installations are set to rise at a 25.26% CAGR to 2031.

- By end user, pharmaceutical and biotech companies represented 52.1% of revenue in 2025; contract research organizations are predicted to log a 26.05% CAGR through 2031.

- By geography, North America held 48.12% of revenue in 2025, whereas Asia-Pacific is projected to advance at a 25.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing number of cross-industry partnerships | +4.2% | North America & EU | Medium term (2-4 years) |

| Rising demand to control drug-development cost & time | +5.8% | Global | Short term (≤ 2 years) |

| Escalating EHR & wearable data volumes | +3.1% | North America & APAC | Medium term (2-4 years) |

| Regulatory acceptance of synthetic control arms | +2.9% | North America & EU | Long term (≥ 4 years) |

| Emergence of foundation models for trial analytics | +4.5% | Global | Medium term (2-4 years) |

| Increasing shift toward precision medicine | +3.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Number of Cross-Industry Partnerships

Large pharmaceutical firms and AI specialists now form joint development programs that embed analytics across design, execution, and submission workflows. Global consultancies have launched dedicated practices, and niche vendors report measurable cycle-time reductions. Sponsors treat these alliances as strategic capital investments rather than operating costs, particularly within complex oncology and rare-disease programs where traditional CROs lack adequate algorithmic depth.

Rising Demand to Control Drug-Development Cost & Time

Average out-of-pocket spend per approved drug exceeds USD 2.6 billion, intensifying the need for AI-enabled protocol optimization and automated data capture. Predictive patient-matching engines trim recruitment timelines by up to 40%, while natural-language processing converts unstructured notes into analyzable records, slashing manual data-entry labor. Infectious-disease and oncology programs adopt these tools first because of their high burn rates and complex endpoints.

Regulatory Acceptance of Synthetic Control Arms

The FDA’s evolving guidance and the EU AI Act’s high-risk-system provisions legitimize external controls created from real-world data, shrinking placebo requirements and improving patient retention. Quality-assurance frameworks such as CHECK reduce hallucination risk in medical LLMs from 31% to 0.3%, increasing regulator confidence[1]Frontiers in Oncology, “Global landscape of cancer vaccine trials,” frontiersin.org Source: arXiv, “CHECK: reducing hallucinations in medical LLMs,” arxiv.org . Oncology and orphan-disease trials gain the most, where small populations complicate randomization.

Emergence of Foundation Models for Trial Analytics

Healthcare providers are training proprietary LLMs like Me-LLaMA on 129 billion biomedical tokens to address domain-specific semantics and privacy constraints, outperforming general models in clinical reasoning tasks. NeuroSTORM leverages 28.65 million fMRI frames to refine biomarker discovery, enhancing safety-signal detection and endpoint sensitivity.

Increasing Shift Toward Precision Medicine

Multimodal fusion models integrate genomic, imaging, and pathology data to tailor eligibility and dosing. Survival-prediction networks in ovarian cancer have surpassed legacy statistical approaches, demonstrating tangible benefits in selecting high-response subpopulations. Companion-diagnostic developers collaborate closely with trial sponsors to validate biomarkers within adaptive study designs.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Standardization & stringent AI software regulation | -3.2% | EU & North America | Medium term (2-4 years) |

| Data privacy & security compliance burdens | -2.8% | Global | Short term (≤ 2 years) |

| Infrastructure gaps at sites & sponsors | -2.1% | APAC & emerging markets | Medium term (2-4 years) |

| Clinician skepticism toward AI-generated insights | -1.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Standardization & Stringent AI Software Regulation

The EU AI Act mandates pre-market conformity assessments and ongoing monitoring for high-risk clinical applications, adding cost and extending timelines[2]European Medicines Agency, “EMA perspective on AI in clinical evidence,” ema.europa.eu. Similarly, the FDA now requires transparent algorithm-change protocols under its Good Machine Learning Practice draft, challenging smaller vendors that lack regulatory affairs resources.

Data Privacy & Security Compliance Burdens

HIPAA, GDPR, and new state-level rules restrict cross-border data flows, prompting heavy investment in federated-learning architectures that keep data local yet inflates infrastructure spend. A recent US court ruling on browser-based tracking scripts has further clouded definitions of identifiable health information, forcing sponsors to revisit consent and de-identification frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Services Drive Implementation Support

Services revenue grew fastest at a 26.61% CAGR, signaling a pivot toward end-to-end transformation programs that encompass data-ingestion pipelines, algorithm customization, and continuous model tuning. While software retained 67.62% of AI in clinical trials market share in 2025, sponsors increasingly pursue managed-service contracts to mitigate internal capability gaps. Comprehensive engagements covering protocol design through regulatory submission underpin the AI in clinical trials market size for services and sustain vendor lock-in through multi-year renewals. Continuous retraining needs, driven by evolving medical-knowledge graphs, further entrench service providers.

CROs, consultancies, and boutique analytics firms bundle regulatory science, data-engineering, and domain expertise, enabling mid-tier biotechs to access sophisticated analytics without heavy capital outlay. Oncology and rare-disease programs dominate the services pipeline because of their complex eligibility schemas, while metabolic-disease trials also adopt algorithmic dosing support.

By Therapeutic Area: Infectious Diseases Accelerate Beyond Oncology

Although oncology held 36.78% revenue share in 2025, infectious-disease projects now grow at 26.2% CAGR, narrowing the gap and altering the overall AI in clinical trials market trajectory. COVID-19 fast-tracked adaptive protocols and external controls, lessons now generalized to RSV, influenza, and anti-microbial programs. Consequently, sponsors deploy AI-enabled virtual cohorts and high-resolution epidemiologic forecasting to expedite enrollment, supporting a larger AI in clinical trials market size for infectious-disease applications.

Vaccine developers integrate genomic-epitope prediction networks to personalize antigen selection. Cardiovascular and metabolic segments adopt steady but lower-velocity AI applications centered on remote monitoring devices and composite endpoint analytics, ensuring diversified downstream demand across the AI in clinical trials industry.

By Clinical Trial Phase: Early-Stage Innovation Drives Phase I Growth

Phase III protocols still command 54.62% of 2025 revenue, yet Phase I studies expand at 25.43% CAGR, reflecting heavy sponsor interest in AI for pre-proof-of-concept decisions. Biomarker-driven eligibility and adaptive dose-finding algorithms reduce cohort sizes and accelerate escalation, thereby increasing the AI in clinical trials market size among early-stage programs. Integration of omics datasets through foundation models allows real-time safety-signal detection, lowering attrition risk.

Phase II adoption centers on AI-assisted endpoint optimization, while Phase IV use cases focus on automated adverse-event detection within post-marketing surveillance pipelines, illustrating a cradle-to-grave continuum of analytics throughout the clinical lifecycle.

By Deployment Model: On-Premise Security Drives Cloud Alternative

Cloud remained the leading model with 48.32% share in 2025, yet on-premise installations rise at a 25.26% CAGR as large pharmas seek tighter governance over proprietary datasets. Hybrid architectures combine cloud elasticity for non-identifiable workloads with secure, local compute for patient-level operations, sustaining the AI in clinical trials market share balance between flexibility and sovereignty. Edge deployments on wearables facilitate low-latency inference for safety monitoring in decentralized trials.

Regulatory callouts for data-localization and audit-trail integrity drive infrastructure upgrades, especially in the EU and parts of APAC, nudging sponsors toward containerized microservices that can shift between environments.

By End User: CROs Transform Service Delivery Models

Pharmaceutical and biotech firms provided 52.1% revenue in 2025; however, CROs outpace the field at 26.05% CAGR, driven by turnkey AI platforms packaged within global site networks. These organizations amortize tool development across multiple clients, fostering economies of scale and shortening deployment cycles. Academic medical centers and device manufacturers represent smaller but stable user groups that exploit AI chiefly for investigator-initiated studies and clinical-evaluation dossiers respectively.

The CRO ascent reshapes the AI in clinical trials market as sponsors increasingly adopt a “buy” over “build” stance for analytics competency, freeing internal teams to focus on core discovery science.

Geography Analysis

North America captured 48.12% revenue in 2025, reflecting the FDA’s leadership in clarifying AI software-as-a-medical-device policy and its openness to synthetic control evidence fda.gov. Robust venture funding and deep EHR penetration create fertile ground for algorithm training, though emerging state-level privacy rules may add compliance drag.

Asia-Pacific is the fastest-growing territory at a 25.85% CAGR to 2031. Japan pilots generative-voice documentation that trims clinician workload, and China’s government-backed AI programs scale trial infrastructure rapidly. India’s vast treatment-naïve population and competitively priced sites attract global sponsors aiming to enlarge AI-augmented registries.

Europe benefits from the EU AI Act, which sets harmonized standards and incentivizes vendors that demonstrate algorithmic transparency. EMA support for real-world evidence, plus national investment in precision-medicine networks, sustains double-digit expansion. Stringent GDPR compliance, however, elevates demand for federated-learning frameworks that circumvent cross-border data transfer.

Competitive Landscape

The competitive field is moderately fragmented. Incumbent giants such as IQVIA integrate AI modules into legacy EDC and eCOA suites, leveraging longstanding sponsor ties. Medidata enhances its Rave platform with machine-learning-driven site-performance analytics. AI-native firms like Unlearn.ai specialize in digital twins for external controls, while Deep6.ai automates patient-matching from structured and unstructured hospital data.

Strategic differentiation hinges on demonstrating quantifiable improvements: reduced enrollment time, lower protocol deviations, and higher submission success. Rare-disease and pediatric trials present whitespace for niche entrants that can deliver algorithmic solutions to small-population challenges. Meanwhile, some big pharmas invest internally, partnering with hyperscale cloud vendors to develop proprietary foundation models, potentially bypassing third-party platforms yet opening co-development channels for specialized tool providers.

Acquisition activity focuses on filling data-engineering gaps and securing access to high-quality longitudinal data. Partnerships between EHR vendors and AI firms further blur category boundaries, driving ecosystem convergence around interoperable APIs that feed multi-sponsor analytics hubs.

AI In Clinical Trials Industry Leaders

Medidata (Dassault Systèmes)

IQVIA

Unlearn.ai

Owkin

Saama Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TXP Medical began trials of a generative-AI voice-input application at Japan’s National Center for Child Health and Development to auto-generate clinical records.

- June 2025: Omi Japan unveiled two-month proof-of-concept AI agent development services for healthcare institutions.

- May 2025: Recursion Pharmaceuticals gained FDA IND clearance for REC-4539, an LSD1 inhibitor for small-cell lung cancer engineered through AI-guided design.

- April 2025: BlackfinBio received FDA clearance for Phase 1/2 trials of BFB-101, an AAV gene therapy for Hereditary Spastic Paraplegia employing AI-assisted target validation.

- March 2025: Johnson & Johnson’s Tremfya secured FDA approval for active Crohn’s disease based on AI-optimized Phase 3 trial protocols.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the AI in clinical trials market as the worldwide spending on purpose-built software platforms and the related implementation or support services that apply artificial intelligence or machine learning logic from protocol design through post-marketing surveillance across Phases I-IV and real-world evidence extensions. According to Mordor Intelligence, such spend reached USD 2.14 billion in 2025.

Scope exclusion: Stand-alone discovery platforms that never interact with live clinical trial data are outside scope.

Segmentation Overview

- By Component Type

- Software

- Services

- By Therapeutic Area

- Oncology

- Cardiovascular Diseases

- Metabolic Diseases

- Infectious Diseases

- Other Therapeutic Areas

- By Clinical Trial Phase

- Phase I

- Phase II

- Phase III

- Phase IV / Real-World Evidence

- By Deployment Model

- Cloud

- On-Premise

- Edge / On-Device

- By End User

- Pharmaceutical & Biotech Companies

- Contract Research Organizations

- Research & Academic Institutes

- Medical Device Manufacturers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed clinical operations leaders at pharmaceutical sponsors, AI platform vendors, and contract research organizations across North America, Europe, and Asia-Pacific. A companion survey of investigators and data managers helped us validate price corridors, realistic adoption timelines, and perceived barriers.

Desk Research

We began with public registries: ClinicalTrials.gov, the EU Clinical Trials Register, and the WHO ICTRP to map annual starts of interventional studies by phase, giving us a demand proxy. Trade bodies such as PhRMA, EFPIA, and TransCelerate published technology budget ratios that our team converted into per-trial spending ranges. Peer-reviewed papers from the Clinical Data Interchange Standards Consortium clarified median data management costs, while D&B Hoovers revenue pulls and Dow Jones Factiva news scans highlighted vendor rollouts and price shifts. Patent clusters on Questel plus procurement notices on Tenders Info signaled emerging budgets for AI-enabled monitoring. This list is illustrative; many other sources guided cross-checks and gap filling.

Market-Sizing & Forecasting

Our top-down model starts with global R&D spend on active trials, layers typical technology outlays per phase, and applies an AI penetration curve informed by enrollment automation metrics; selective bottom-up supplier roll-ups of license volumes and average selling prices validate and refine totals. Key variables include yearly trial starts, median participants, per patient monitoring cost, software license fees, recruitment time savings, and regional cloud infrastructure prices. Five-year forecasts use multivariate regression blended with scenario analysis to capture regulatory acceleration or slowdown; expert ranges bridge sparse inputs and are stress tested against historical eClinical adoption arcs.

Data Validation & Update Cycle

Outputs pass anomaly checks before a senior reviewer signs off. We refresh the dataset annually and trigger interim updates when material events, such as major funding rounds, new guidance, or marquee platform launches, shift market momentum.

Why Mordor's AI In Clinical Trials Baseline commands reliability

Published estimates often differ because firms choose distinct functional scopes, price stacks, and refresh cadences.

Main gap drivers include whether post-approval real-world evidence spend is counted, the aggressiveness of AI uptake scenarios, exchange rate dates, and the frequency of primary research touchpoints.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.14 b (2025) | Mordor Intelligence | - |

| USD 1.35 b (2024) | Global Consultancy A | Limits scope to Phases I-III design tools; modest uptake path; older currency base |

| USD 2.40 b (2024) | Trade Journal B | Relies on vendor revenue survey only; omits cloud hosting and decentralized trial modules |

| USD 2.60 b (2025) | Regional Consultancy C | Uses single global license price and uniform 30% penetration; no primary validation |

These comparisons show that Mordor's blend of transparent variables, recurring updates, and direct industry dialogue delivers a balanced, dependable baseline for decision makers.

Key Questions Answered in the Report

What is the current size of the AI in clinical trials market?

The market stands at USD 2.68 billion in 2026 and is projected to reach USD 8.24 billion by 2031.

Which segment grows fastest within the AI in clinical trials market?

Services expand at a 26.61% CAGR as sponsors demand turnkey implementation and model-maintenance support.

Why are infectious-disease trials adopting AI so rapidly?

Pandemic-driven regulatory flexibilities, such as synthetic control accepta

How does on-premise deployment differ from cloud for AI trials?

On-premise models offer data sovereignty and regulatory compliance, driving a 25.26% CAGR, while cloud retains scalability advantages for less-sensitive workloads.

What regulatory trends influence AI adoption in clinical trials?

The FDA’s guidance on adaptive evidence and the EU AI Act’s high-risk classification both encourage transparent, validated AI, shaping global implementation standards.

Which regions lead and grow fastest in this market?

North America leads with 48.12% revenue due to advanced regulation and infrastructure, while Asia-Pacific grows fastest at a 25.85% CAGR on expanding trial capacity and supportive policy. . . . . . . .

Page last updated on: