Clinical Knowledge-Based Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 4.80 Billion |

| Growth Rate (2026 - 2031) | 14.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

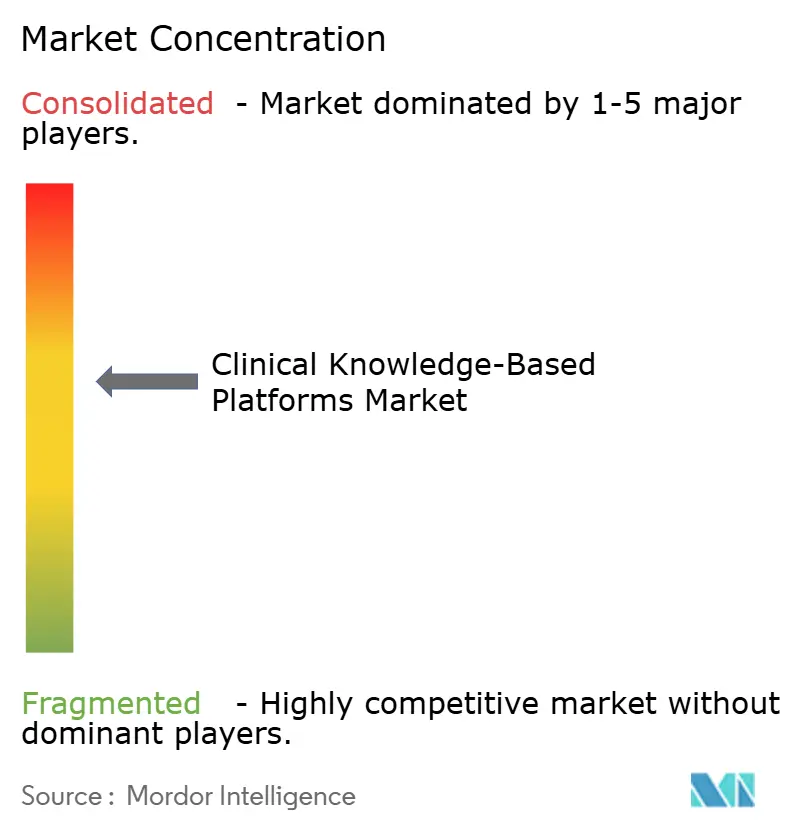

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Knowledge-Based Platforms Market Analysis by Mordor Intelligence

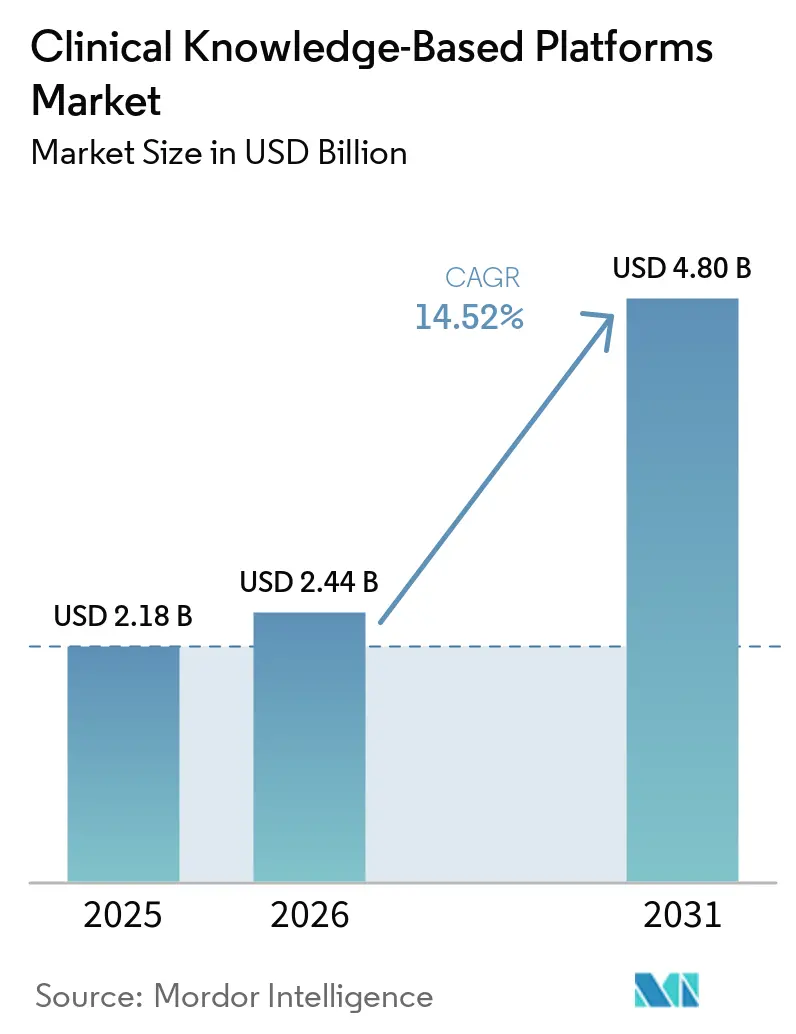

The Clinical Knowledge-Based Platforms market size is expected to be USD 2.18 billion in 2025, USD 2.44 billion in 2026, and reach USD 4.80 billion by 2031, growing at a CAGR of 14.52% from 2026 to 2031. Expanding value-based reimbursement, accelerating evidence-based medicine adoption, and rapid uptake of large language models are deepening demand across hospitals, payers, and ambulatory networks. Cloud elasticity now underpins real-time guideline updates and high-volume inference, while regulatory mandates such as the CMS Prior Authorization Final Rule are hard-coding FHIR API connectivity into daily workflows. Competitive intensity is rising as incumbent reference publishers embed generative AI layers and EHR vendors launch native decision-support modules that threaten standalone suppliers. Investment momentum is strongest in markets where patient-safety penalties and data-sharing rules already align financial rewards with guideline adherence.

Key Report Takeaways

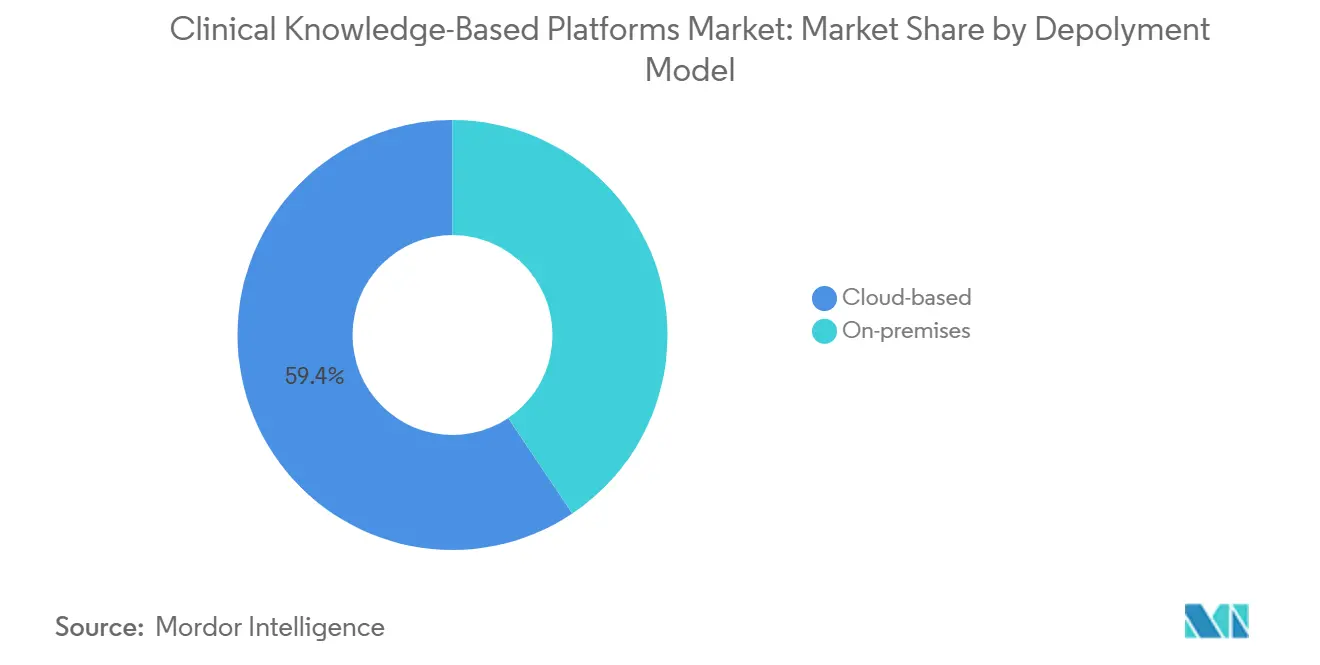

- By deployment model, cloud-based platforms captured 59.38% of the Clinical Knowledge-Based Platforms market share in 2025. Cloud-based deployments are projected to expand at a 15.54% CAGR to 2031, the fastest rate among deployment models.

- By end user, hospitals and health systems held 56.43% of the Clinical Knowledge-Based Platforms market share in 2025. Healthcare payers record the highest growth, advancing at a 15.72% CAGR through 2031.

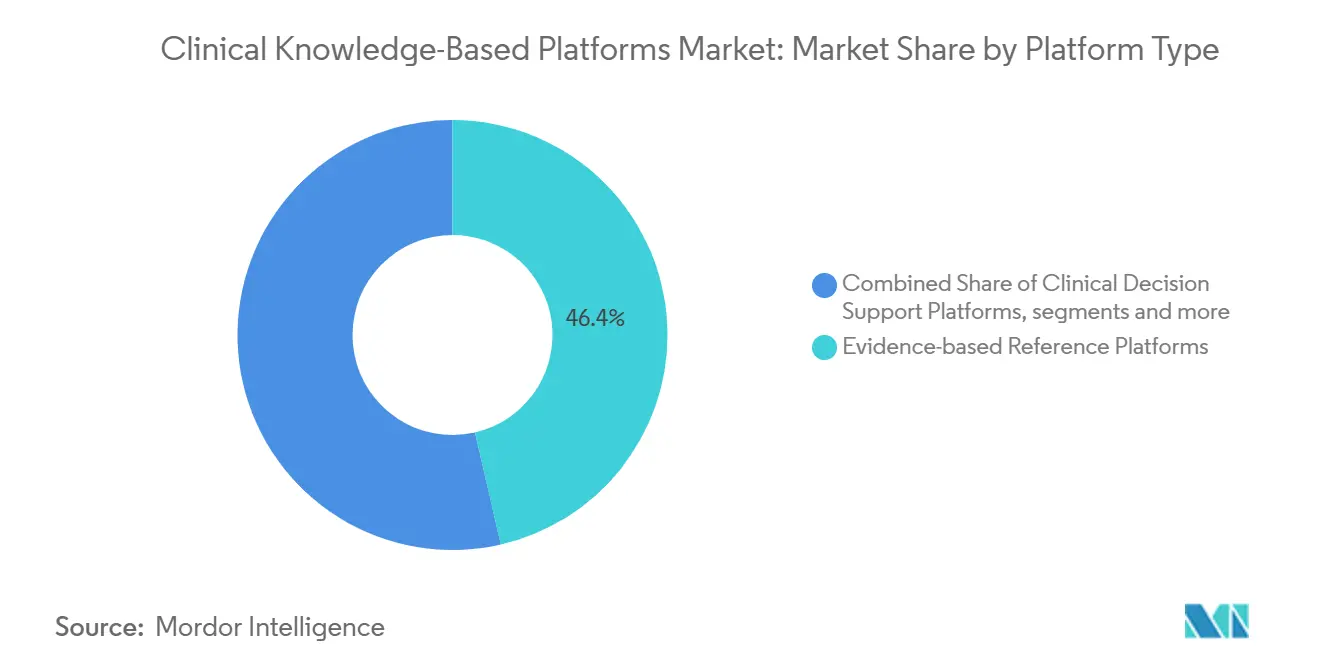

- By platform type, evidence-based reference platforms led with 46.44% revenue share in 2025. Clinical decision-support platforms are forecast to grow at a 16.61% CAGR to 2031, outpacing every other platform cohort.

- By region, North America led with 48.26% revenue share in 2025. Asia-Pacific is forecast to grow at a 16.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Knowledge-Based Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Adoption of Evidence-based Medicine | +3.2% | North America, Western Europe first movers | Medium term (2-4 years) |

| Exponential Growth of Clinical Data Volumes | +2.8% | Global, APAC core | Long term (≥ 4 years) |

| Regulatory Mandates to Reduce Medication Errors | +2.5% | North America, EU | Short term (≤ 2 years) |

| Expansion of Value-based Care Reimbursement Models | +2.4% | North America dominant | Medium term (2-4 years) |

| Integration of Large Language Models into Platforms | +2.9% | North America and China lead | Short term (≤ 2 years) |

| FHIR-based API Marketplaces Enabling Plug-and-Play Services | +2.1% | North America, EU core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Adoption of Evidence-based Medicine

Health systems are locking standardized pathways into order sets to compress variation, shorten length of stay, and safeguard reimbursement. Atropos Health’s Alexandria curated 33 million evidence artifacts by 2025, letting clinicians surface comparative-effectiveness answers in seconds. Oncology and cardiology services feel this shift most acutely because guideline volumes outpace manual review capacity. Elsevier extended ClinicalKey AI to more than 300 hospitals in February 2026, integrating with Epic and DrFirst so guideline snippets appear at prescribing time.[1]Elsevier, “ClinicalKey AI Expands Hospital Footprint,” elsevier.com Specialty societies now embed their recommendations directly into workflows, raising immediate adherence. As penalties for readmissions intensify, the Clinical Knowledge-Based Platforms market becomes an operational requirement rather than an optional upgrade.

Exponential Growth of Clinical Data Volumes

Mayo Clinic’s APOLLO AI ingested 25 billion clinical events by 2025, producing foundation models trained on decades of longitudinal records.[2]Mayo Clinic, “APOLLO AI Foundation Model Initiative,” mayoclinic.orgContinuous glucose monitors, wearable telemetry, and genomic panels pour terabytes of data that exceed human synthesis capacity. InterSystems IRIS for Health powers Stanford Health Care’s ChatEHR, retrieving context-aware notes and trends in real time. In April 2026 Nature published DxDirector-7B, showing specialist-level diagnostic accuracy across 14 disciplines. Yet fragmented coding schemes and inconsistent FHIR adoption hamper multi-site aggregation, especially in the United States where hospital consolidation remains incomplete.

Regulatory Mandates to Reduce Medication Errors

The FDA’s SAFER guides and 21st Century Cures rules oblige hospitals to deploy real-time medication verification; the agency itself rolled out an agentic AI system in December 2025.[3]U.S. FDA, “SAFER Guides and Agentic AI System,” fda.gov First Databank answered with AlertSpace 2.0, a machine-learning tier that mutes low-value notifications. CMS ties reimbursement to adverse-drug-event scores, while the European Medicines Agency urges electronic prescribing with embedded checks. Japan’s PMDA cleared AI software-as-device approvals in 2024, opening Asia-Pacific pathways. Collectively, these directives inject urgency—and budget—into Clinical Knowledge-Based Platforms market adoption.

Expansion of Value-based Care Reimbursement Models

The CMS Merit-based Incentive Payment System tracks diabetic-retinopathy screens, blood-pressure control, and cancer screenings, all measurable via clinical knowledge engines. From January 2026 payers must answer prior-authorization queries within 72 hours through FHIR APIs, accelerating utilization-management automation. UnitedHealth, Anthem, and Cigna channel investments toward AI adjudication services to trim costs and speed provider approvals. EvidenceCare’s BetterCare produced more than USD 100 million in client savings during 2025 by reducing unwarranted imaging and admissions. Similar value-based pilots in Australia and the United Kingdom foreshadow wider global uptake.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Barriers with Legacy EHRs | −1.8% | Global, acute in fragmented U.S. market | Medium term (2-4 years) |

| Alert Fatigue and Clinician Trust Concerns | −1.5% | North America, EU | Short term (≤ 2 years) |

| High Implementation Costs for Small Practices | −1.2% | North America, rural APAC | Long term (≥ 4 years) |

| IP Litigation Around Proprietary Clinical Algorithms | −0.9% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Barriers with Legacy EHRs

Many hospitals still run HL7 v2 feeds and bespoke data models. Oracle’s Cerner cloud transition announced February 2026 will unfold over years, leaving heterogeneous install bases in place. Semantic mismatches—“HbA1c” versus “glycated hemoglobin”—dilute decision-support accuracy. Middleware from Smile CDR and InterSystems can translate formats but adds latency and maintenance overhead. Facilities lacking robust IT staff struggle to keep these adapters patched, slowing Clinical Knowledge-Based Platforms market penetration in rural and community settings.

Alert Fatigue and Clinician Trust Concerns

Peer-reviewed studies show override rates from 49% to 96% for interruptive alerts. When minor interactions trigger the same warnings as life-threatening ones, clinicians dismiss pop-ups reflexively. First Databank’s AlertSpace 2.0 now ranks notices by severity, yet most legacy EHRs still lack dynamic filtering. Burnout linked to documentation time magnifies resistance, and opaque AI reasoning raises liability worries. Clear explainability and tiered severity scoring are prerequisites for broader trust inside the Clinical Knowledge-Based Platforms market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominates as Inference Workloads Scale

The cloud-based segment commanded USD 1.29 billion and 59.38% of the Clinical Knowledge-Based Platforms market in 2025, dwarfing on-premises demand. Elastic compute absorbs surges in inference calls from large language models, while single-tenant architectures satisfy HIPAA and GDPR compliance. First Databank’s MedProof server runs multi-tenant clusters that handle millions of daily API calls without local installs. Elsevier leverages Azure to deliver sub-second evidence retrieval to more than 300 hospitals. These dynamics propel a 15.54% CAGR for cloud, more than double the on-premises clip, sustaining the broader Clinical Knowledge-Based Platforms market growth narrative.

On-premises deployments persist where data-sovereignty statutes or air-gap mandates prevail, such as military and some Chinese government hospitals. Oracle’s hybrid Cerner roadmap keeps sensitive records local while shifting analytics to its cloud when policy permits. Yet patching, capacity planning, and content-update chores burden internal teams, tilting new contracts toward managed or private-cloud variants. Vendors marketing hardened appliances with bundled auto-update services will capture residual on-premises spend, but secular gravity favors cloud expansion.

By End User: Healthcare Payers Accelerate as Digital Prior Authorization Takes Hold

Hospitals and health systems generated USD 1.23 billion, or 56.43%, of 2025 revenue inside the Clinical Knowledge-Based Platforms market. These buyers lead on safety metrics and face direct CMS penalties for adverse events. Mayo Clinic’s 25 billion-event APOLLO repository exemplifies the scale advantages academic centers wield. Teaching hospitals also value research registries that leverage standardized data to speed clinical-trial enrollment and guideline updates.

Healthcare Payers post the fastest trajectory at 15.72% CAGR as CMS mandates 72-hour prior-authorization responses through FHIR APIs. UnitedHealth, Anthem, and Cigna channel AI adjudication to cut manual reviews. EvidenceCare’s BetterCare saved over USD 100 million for payer clients by eliminating low-value imaging in 2025. Ambulatory centers adopt lighter-weight cloud tools, especially when bundled with their EHR license, broadening the Clinical Knowledge-Based Platforms market footprint.

By Platform Type: Clinical Decision Support Surges on Generative AI

Evidence-based reference platforms represented 46.44% revenue in 2025, anchored by UpToDate and ClinicalKey. These static libraries still underpin physician trust. Yet clinical decision-support modules that fuse patient context with real-time labs are rapidly expanding; a 16.61% CAGR will propel them past references before 2031. Corti’s Agentic Framework drafts notes and suggests treatments live in the encounter. Predictiv AI’s multi-model reasoning patent illustrates the march toward autonomous differential diagnosis. APIs such as MedProof lower integration friction, extending reach across heterogeneous EHR estates and driving deeper Clinical Knowledge-Based Platforms market penetration.

Reference vendors respond by layering generative interfaces that surface concise updates, easing clinicians’ cognitive load. Pathway-management tools—Zynx Health partnered with Innovaccer to embed order-set pathways—tie discrete CDS alerts into longitudinal care plans. This convergence blurs category lines and fuels cross-selling as buyers seek unified knowledge stacks rather than point solutions.

Geography Analysis

North America contributed 48.26% of 2025 revenue to the Clinical Knowledge-Based Platforms market, buoyed by near-universal EHR penetration and outcome-based reimbursement penalties. The CMS Final Rule compels payers to open FHIR interfaces, stimulating API-centric vendors. Epic records 175 generative AI use cases under development, indicating how quickly innovation cycles shorten. First Databank’s MedProof launch lowers switching costs, fragmenting incumbent lock-in. Vendor heterogeneity across systems such as Epic, Oracle, and Meditech increases integration complexity and slows implementation timelines, particularly in smaller hospital settings.

Asia-Pacific is on track for a 16.44% CAGR and will nearly double its share by 2031. India’s Ayushman Bharat Digital Mission issued 680 million health IDs and registered 260,000 facilities by 2025. China’s NMPA had cleared more than 170 AI medical devices by 2024, creating local clinical-reasoning datasets. Japan’s AI SaMD pathway and South Korea’s Digital Healthcare Act expand telemedicine codes, lifting demand for cloud CDS in remote monitoring. Diverse languages and data-localization statutes, however, force vendors to build region-specific ontologies and hosting zones, adding cost.

Europe’s trajectory hinges on the EU AI Act that classifies clinical decision support as high-risk, mandating conformity assessments and post-market surveillance. GDPR rules elevate compliance overhead but reinforce buyer preference for established vendors with audited quality systems. NHS England pilots value-based contracts linked to digital triage and remote monitoring outcomes. Germany, France, and Italy seek cross-border data liquidity through the European Health Data Space by 2027, which should unlock federated CDS analytics. Middle East and Africa spend remains nascent but accelerates where Saudi Arabia and the UAE invest in cloud health infrastructure, while Latin America wrestles with macroeconomic volatility that delays large-scale rollouts, nudging providers toward subscription SaaS instead of capex.

Competitive Landscape

Market concentration is moderate; legacy publishers Wolters Kluwer, Elsevier, and BMJ leverage decades of editorial rigor, while pure-play CDS vendors such as EvidenceCare, Zynx Health, and Isabel Healthcare differentiate on live workflow integration. First Databank’s API-first MedProof strategy exemplifies architecture pivots that erode vendor lock-in.

EHR giants Epic and Oracle embed native CDS, posing vertical-integration threats but also opening app-store ecosystems that smaller suppliers can ride. Continuous evidence updates—drug approvals now weekly—create operating complexity that favors well-capitalized incumbents able to maintain editorial staffs. White-space growth sits in ambulatory and rural facilities where capital budgets are tight yet quality metrics match hospital obligations. Cloud SaaS with pre-integrated EHR connectors lowers barriers.

Direct-to-consumer symptom-checker entrants, including Infermedica and Ada Health, extend the Clinical Knowledge-Based Platforms market beyond traditional institutional buyers. Patent filings around multi-model reasoning signal future algorithm differentiation, but enforceability remains unclear. Compliance mastery—ISO 13485, EU MDR, FDA SaMD Q-submissions—continues to screen competitors, consolidating share within players that can finance global regulatory upkeep.

Clinical Knowledge-Based Platforms Industry Leaders

Wolters Kluwer Health

Elsevier (ClinicalKey)

IBM

Epic Systems Corporation

Oracle

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Predictiv AI filed a patent for a Clinical AI Reasoning Platform chaining multiple large language models to automate multi-step diagnostics.

- March 2026: First Databank released MedProof Model Context Protocol, giving AI agents universal medication-intelligence query access; Artera integrated the server into its oncology platform.

- February 2026: Corti launched the Agentic Framework for autonomous clinical-note drafting and treatment suggestions inside EHR workflows.

Global Clinical Knowledge-Based Platforms Market Report Scope

According to the report’s scope, clinical knowledge‑based platforms are software systems that deliver evidence‑based medical guidance by organizing clinical guidelines, pathways, drug information, and diagnostic logic into structured, searchable, and often algorithm‑driven tools that clinicians can use at the point of care. They function as external, third‑party knowledge engines, separate from EHRs, that help clinicians make consistent, informed decisions by surfacing validated medical content, reducing variability, and supporting safer, more standardized care.

The clinical knowledge-based platforms market is segmented into deployment model, end user, platform type, and geography. By deployment model, the market is segmented into cloud-based and on-premises. By end user, the market is segmented into hospitals and health systems, ambulatory care centers, academic and research institutes, and healthcare payers. By platform type, the market is segmented into evidence-based reference platforms, clinical decision support platforms, clinical pathway management platforms, and API-based knowledge services. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Cloud-based |

| On-premises |

| Hospitals and Health Systems |

| Ambulatory Care Centers |

| Academic and Research Institutes |

| Healthcare Payers |

| Evidence-based Reference Platforms |

| Clinical Decision Support Platforms |

| Clinical Pathway Management Platforms |

| API-based Knowledge Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Model | Cloud-based | |

| On-premises | ||

| By End User | Hospitals and Health Systems | |

| Ambulatory Care Centers | ||

| Academic and Research Institutes | ||

| Healthcare Payers | ||

| By Platform Type | Evidence-based Reference Platforms | |

| Clinical Decision Support Platforms | ||

| Clinical Pathway Management Platforms | ||

| API-based Knowledge Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Clinical Knowledge-Based Platforms market in 2026?

The Clinical Knowledge-Based Platforms market size stands at USD 2.44 billion in 2026, on track to reach USD 4.80 billion by 2031 at a 14.52% CAGR.

Which deployment model holds the biggest share?

Cloud-based platforms command 59.38% of 2025 revenue thanks to elastic compute and centralized content updates.

What segment is growing fastest?

Clinical decision-support platforms lead growth with a 16.61% CAGR forecast through 2031 as generative AI accelerates adoption.

Which region will outpace others to 2031?

Asia-Pacific is set for a 16.44% CAGR, propelled by India’s national health ID rollout and China’s AI device approvals.

Page last updated on: