Pharmaceutical Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 6.38 Billion |

| Growth Rate (2026 - 2031) | 11.67% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Management Software Market Analysis by Mordor Intelligence

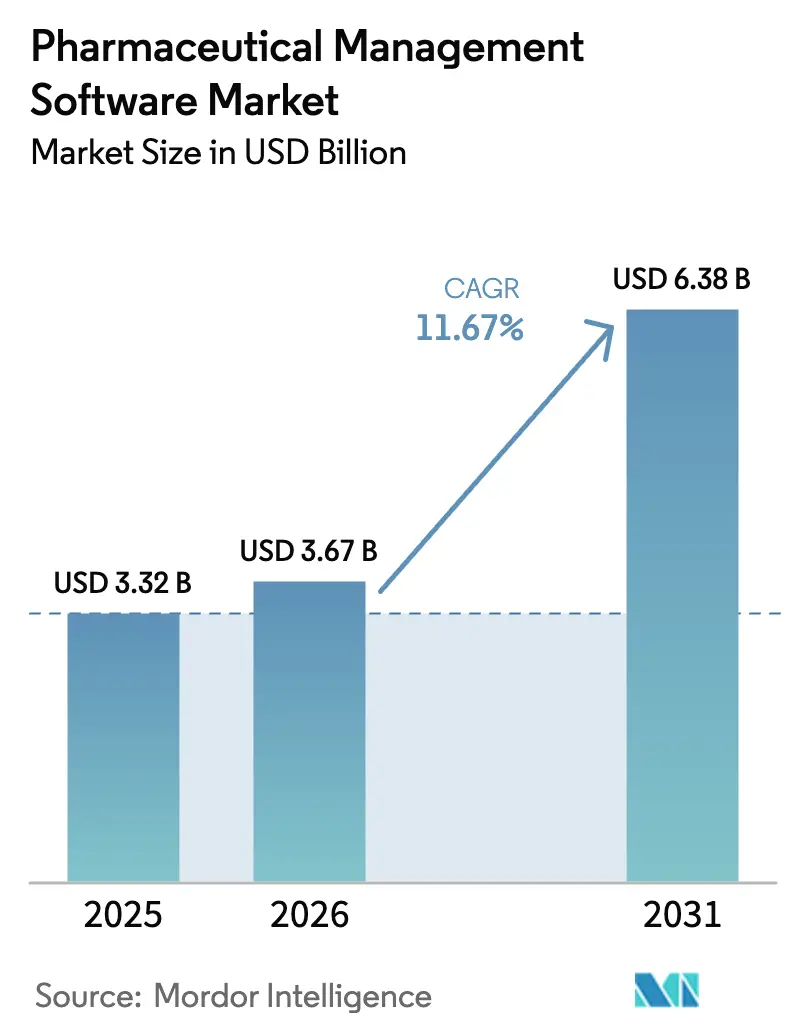

The Pharmaceutical Management Software Market size is projected to be USD 3.32 billion in 2025, USD 3.67 billion in 2026, and reach USD 6.38 billion by 2031, growing at a CAGR of 11.67% from 2026 to 2031.

Heightened global compliance mandates, the rapid migration toward validated cloud services, and the growing complexity of biologics are accelerating spending on platform integrations that unify quality, manufacturing, and regulatory data. Vendors that can embed immutable audit trails, role-based access controls, and e-signature workflows into configurable solutions are capturing early-mover advantages as companies revalidate legacy systems to meet the European Medicines Agency’s expanded Annex 11 draft. Demand is further strengthened by the expansion of decentralized clinical trials that require remote patient monitoring, e-consent, and real-time submission workflows. Cybersecurity incidents such as the Change Healthcare breach underscore the need for ISO 27001-aligned architectures, pushing buyers toward providers that pair software with zero-trust security toolkits. In parallel, sovereign-AI regulations in Europe and China are steering the pharmaceutical management software market toward hybrid deployments in which sensitive batch-genealogy data remain on-premise while analytics layers run in regional clouds.

Key Report Takeaways

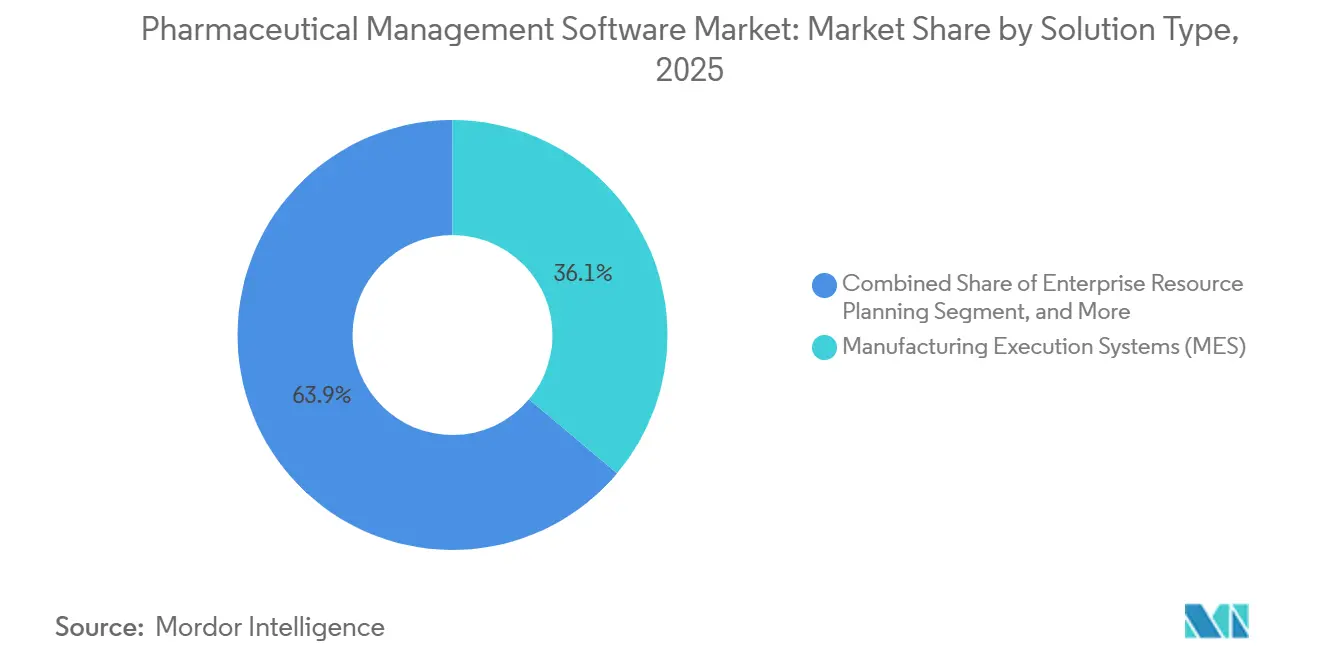

- By solution type, manufacturing execution systems led the pharmaceutical management software market with 36.12% market share in 2025. Quality and compliance management solutions are projected to expand at a 13.06% CAGR through 2031, the fastest among all categories.

- By deployment model, on-premises systems accounted for 55.87% of the pharmaceutical management software market in 2025, whereas cloud-based systems are forecast to grow at a 12.63% CAGR through 203.1

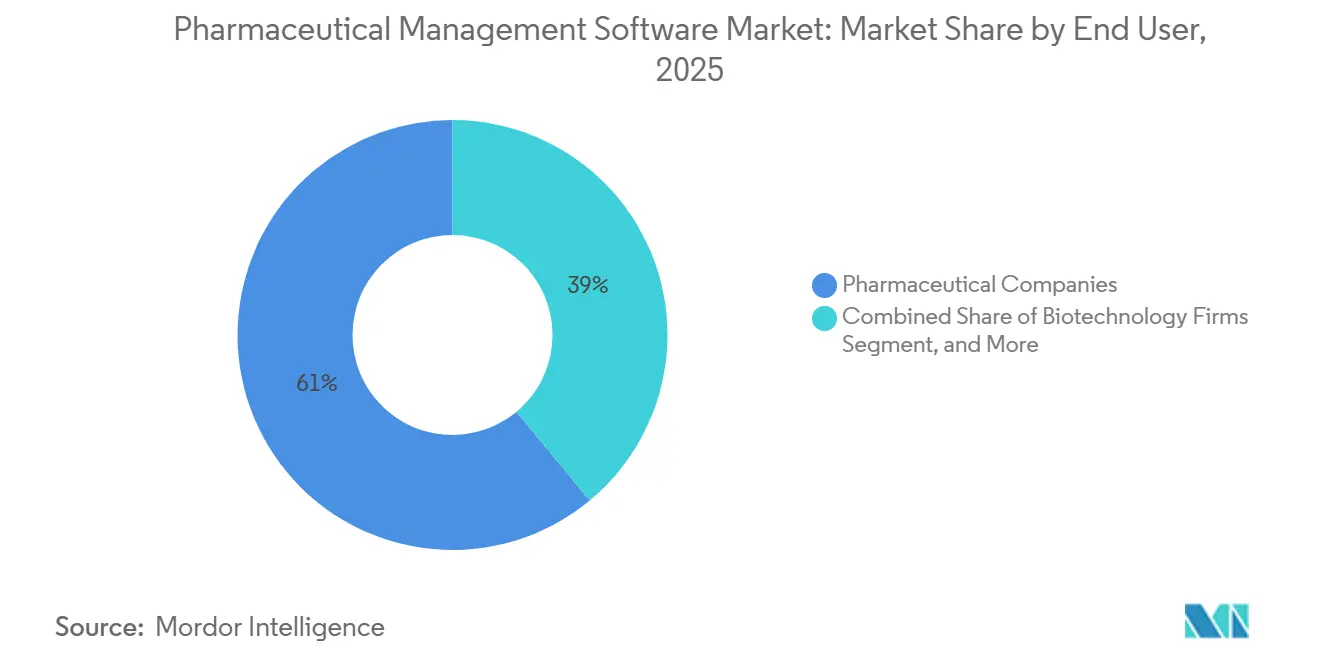

- By end user, pharmaceutical companies held a 61.03% share of the pharmaceutical management software market in 2025; biotechnology firms recorded the highest projected CAGR at 12.18% through 2031.

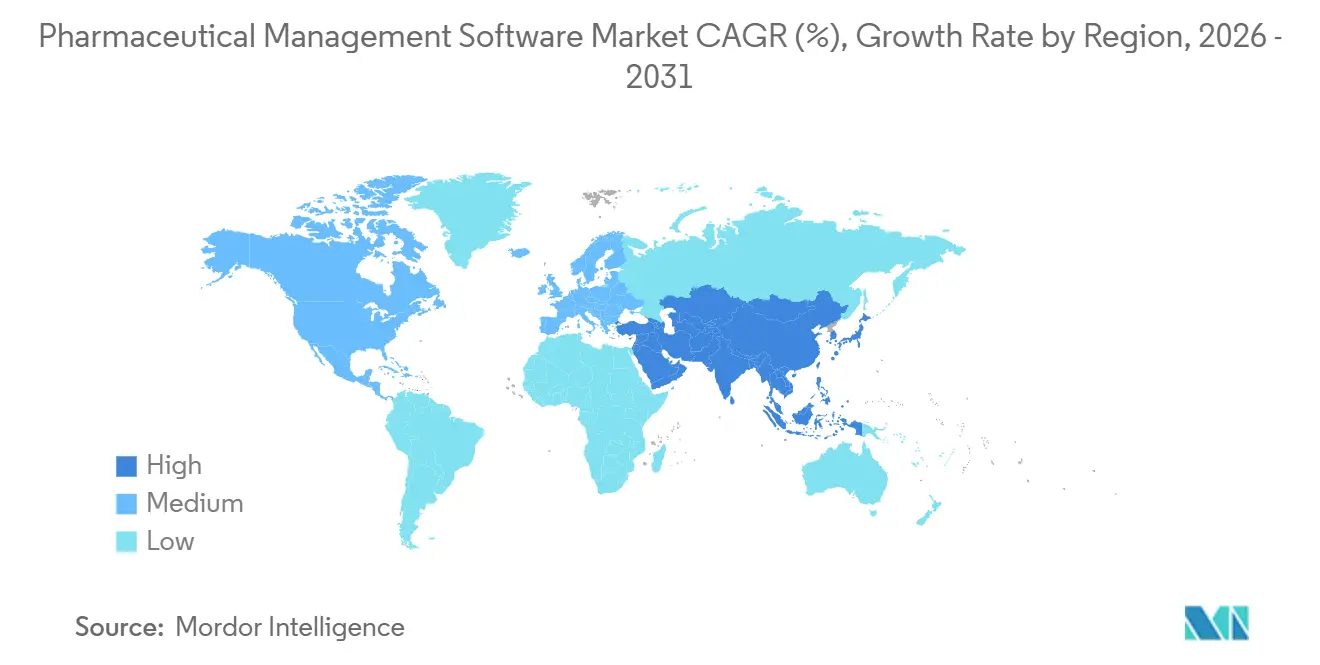

- By geography, North America led with 41.18% revenue share in 2025, while Asia-Pacific is advancing at a 14.71% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Management Software Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven predictive quality analytics reduces batch-failure costs | +3.2% | Global, concentrated in advanced manufacturing hubs | Medium term (2-4 years) |

| Cloud-first ERP migration across Big Pharma | +2.8% | Global, with North America & EU leading adoption | Medium term (2-4 years) |

| Mandatory serialization/track-&-trace enforcement in low- and middle-income countries | +2.4% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Cyber-resilience mandates from regulators (FDA, EMA) | +2.1% | Global, with stricter enforcement in developed markets | Short term (≤ 2 years) |

| Biologics manufacturing complexity driving MES–ERP convergence | +1.8% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Shift toward decentralized & virtual clinical trials | +1.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Compliance Mandates Accelerate Software Validation Investments

The European Medicines Agency draft released in 2025 stretched Annex 11 from five to nineteen pages, forcing manufacturers to upgrade audit-trail logic, supplier-qualification protocols, and data-integrity testing.[1]Pharmaceutical Technology Staff, “EU Annex 11 Draft Update Expands Computerized System Requirements,” pharmaceutical-technology.com The United States continues to strictly enforce 21 CFR Part 11, with 2024 warning letters citing validation gaps in 23% of inspections. WHO Technical Report Series 1033 codifies ALCOA+ principles, effectively prohibiting post-hoc edits to batch data. China’s National Medical Products Administration now demands local hosting or live regulatory access for foreign software, tightening oversight on multinational platforms. Together, these mandates are expanding validation budgets and pushing the pharmaceutical management software market toward configurable, compliance-ready suites.

Rapid Migration to Cloud / SaaS Platforms Balances Agility With Data Sovereignty

Cloud uptake is rising, yet patterns diverge by workload. North American firms push commercial analytics into public cloud environments while retaining batch records on-premises for tighter control.[2]Oracle Corporation, “Life Sciences Cloud Adoption Trends 2025,” oracle.com Veeva reported that 78% of new Vault QMS clients chose multi-tenant SaaS in 2025, though 64% deployed Vault Manufacturing on private instances to comply with residency clauses. The European Union’s GDPR and pending AI Act trigger a 15-20% cost premium as organizations add sovereign-cloud controls. SAP’s S/4HANA Life Sciences sovereign-cloud launch in October 2025 demonstrates the vendor's pivot toward regional compliance. SaaS inflation, averaging 8-12% per annum, is prompting mid-tier buyers to revisit lifetime economics, slowing pure-cloud migrations in inflationary economies.

Growth of Biologics & Personalized Medicine Fragments Batch Architectures

Personalized medicine is fragmenting batches into single-patient lots that still need full validation. Siemens noted that 42% of new cell-therapy customers required electronic health-record links in 2025, a feature absent from small-molecule lines. Contract manufacturers such as Lonza are investing in modular suites like Siemens Opcenter Execution Pharma to orchestrate parallel autologous campaigns at scale.

Mandatory Electronic Batch-Record Adoption Eliminates Paper Deviations

The eBR segment is projected to expand from USD 734.85 million in 2026 to USD 1.92 billion by 2035 as regulators reject paper workflows. FDA data-integrity guidance states that manual logs cannot supply the same contemporaneous evidence as validated digital records. MasterControl’s 2025 survey shows eBR users reduced average deviation investigation time from 28 days to 11 days, freeing quality resources for proactive analytics. Implementation costs of USD 500,000–2 million still deter some mid-size firms, but CDMOs offer pre-validated platforms to lower CapEx barriers.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation & Validation Cost | -1.4% | Global, acute in emerging markets & mid-tier firms | Short term (≤ 2 years) |

| Cyber-Security & Data-Sovereignty Concerns | -1.1% | EU & APAC data-residency mandates, US breach exposure | Medium term (2-4 years) |

| Regulatory Patchwork Triggers Frequent Re-Validation Cycles | -0.9% | Multinational deployments across FDA, EMA, NMPA jurisdictions | Long term (≥ 4 years) |

| Rising SaaS Subscription TCO In Inflationary Markets | -0.7% | North America & Europe SaaS-heavy deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation & Validation Cost Constrains Mid-Tier Adoption

Total project budgets range from USD 1.5 million for single-site QMS to more than USD 10 million for enterprise MES-ERP roll-outs, driven by installation, operational, and performance qualifications.[3]Pharmaceutical Executive Editors, “Pharma Software Implementation Costs Range USD 1.5M to USD 10M,” pharmexec.com European Annex 11 supplier audits can add 25% to baseline costs relative to non-regulated roll-outs. External validation consultants bill USD 1,200-2,500 per day, prolonging timelines for firms with limited in-house expertise. Although CDMOs supply turn-key, pre-validated environments, clients trade configurability for speed, heightening vendor lock-in concerns.

Cyber-Security & Data-Sovereignty Concerns Fragment Deployment Topologies

The February 2024 Change Healthcare ransomware event compromised more than 100 million records and cost USD 872 million in remediation, amplifying scrutiny on third-party software chains. EU GDPR fines top 4% of global revenue, while China’s Data Security Law forces domestic hosting of sensitive health data, splintering global architectures into regional silos. Companies now demand ISO 27001 and annual penetration tests as part of software contracts, raising operating budgets by about 10-15%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Compliance Suites Drive Uptake Beyond Traditional ERP

Manufacturing execution systems accounted for 36.12% of pharmaceutical management software market share in 2025, underpinned by their ability to orchestrate real-time batch execution, equipment integration, and lot genealogy across sterile suites. Quality and Compliance Management platforms, including eBR, are projected to post a 13.06% CAGR through 2031, reflecting regulatory emphasis on immutable audit trails and supplier qualification. Pharmaceutical management software market size allocations continue shifting as companies favor modular, compliance-ready layers over sprawling transactional ERP refreshes, evidenced by enterprise resource planning growth lagging newer quality modules.

Demand is also increasing for supply-chain and inventory suites that embed serialization rules from the US Drug Supply Chain Security Act and the EU Falsified Medicines Directive, enabling full chain-of-custody from API procurement through retail dispense. Customer and Commercial applications capture early traction among firms piloting direct-to-patient programs and value-based contracts. Knowledge and Data Management hubs are emerging as strategic assets, providing unified repositories that support AI-driven signal detection and real-world evidence snapshots, with 64% of top-20 companies adopting Veeva Vault RIM by 2025.

By Deployment Model: Hybrid Architectures Balance Compliance and Agility

On-premise systems accounted for 55.87% in 2025, as risk-averse manufacturers retain validated workloads behind facility firewalls to comply with 21 CFR Part 11 and Annex 11 rules. Nonetheless, cloud instances represent the fastest-growing segment of the pharmaceutical management software market, advancing at a 12.63% CAGR to 2031, as multi-tenant SaaS accelerates upgrades and eases audit preparation. Firms are widely opting for hybrid topologies in which manufacturing and quality cores remain on-premises or in sovereign cloud zones, while analytics, collaboration, and supplier portals reside in hyperscale public clouds.

GDPR and China’s data-localization statutes force regional data centers, adding up to 20% in infrastructure overhead and further complicating multi-cloud deployments. SAP’s 2025 release of S/4HANA Life Sciences sovereign clouds in Germany, France, and the United Arab Emirates reflects vendor recognition that localization is non-negotiable for regulated records. Persistent SaaS price inflation of 8-12% per year pressures buyers to compare subscription models with perpetual licensing in total-cost analyses, which can occasionally slow migrations among mid-cap firms.

By End User: Biotechnology Firms Accelerate Digital Adoption

Pharmaceutical companies accounted for 61.03% of 2025 revenue, yet biotechnology firms are forecast to exhibit a 12.18% CAGR, outpacing all other segments, because cell and gene therapies require highly configurable workflows that legacy MES systems cannot support. CDMOs and CMOs are scaling software investments to shorten batch release times and differentiate capacity offerings, as illustrated by Lonza’s USD 580 million Visp expansion, which uses Siemens Opcenter to orchestrate parallel autologous runs.

CROs deepen investments in trial-management stacks as decentralized studies displace site-based models. Hospitals and clinics remain an emerging buyer group but show rising interest in pharmacy automation tools that integrate with electronic health records systems, especially for personalized therapies requiring bedside chain-of-identity validation. Together, these evolving buyer patterns are expanding the addressable market for pharmaceutical management software.

Geography Analysis

North America retained a 41.18% share in 2025, propelled by robust biologics pipelines, strict Part 11 enforcement, and the early adoption of SaaS quality suites that shorten validation cycles. The United States hosts most of the world’s commercial-scale cell and gene therapy plants, fueling demand for real-time equipment integration and cold-chain genealogy tracking. Canada’s CDMO sector is growing due to near-shoring trends, though expertise shortages are extending validation timelines. Mexico benefits from proximity to US markets but lags in adopting advanced software, primarily due to smaller plant sizes and limited capital budgets. High-profile breaches, such as the Change Healthcare incident, are driving adoption of ISO 27001 and the NIST Framework across the region.

Europe is revalidating legacy platforms because the Annex 11 draft issued in 2025 elevates data integrity and supplier audit thresholds. Germany, France, and the United Kingdom lead MES-ERP convergence pilots tied to Industry 4.0 programs, while GDPR and the AI Act compel sovereign-cloud configurations that increase deployment spend by 15-20% relative to public-cloud-only architecture. Mid-sized manufacturers face implementation costs of USD 1.5-10 million for validated roll-outs, prompting outsourcing to CDMOs with turnkey systems.

Asia-Pacific is growing at 14.71% CAGR through 2031, underpinned by China’s enforcement of data-integrity controls that obligate local hosting and real-time regulator access. India’s CDMO sector invested USD 2.1 billion in capacity in 2024, adopting MES platforms to secure export approval. Japan advances electronic batch record adoption, though cultural preference for on-premises solutions tempers SaaS adoption. South Korea and Australia expand biologics capacity, using advanced MES suites for real-time process orchestration. Meanwhile, the pharmaceutical management software market gains momentum across the Middle East and South America as governments seek drug-supply self-sufficiency, though smaller plant footprints and skills gaps moderate growth trajectories.

Competitive Landscape

The market remains moderately fragmented, but consolidation is on the rise as buyers favor integrated platforms that converge MES, QMS, and regulatory data. Enterprise resource planning incumbents SAP, Oracle, and Microsoft extend life sciences clouds with sovereign options and AI analytics to retain share. Vertical specialists such as Veeva Systems, MasterControl, Siemens, and Dassault Systèmes continue to gain traction by bundling validated content, rapid-deployment templates, and industry-specific data models. Veeva disclosed that 78% of new QMS clients selected SaaS in 2025 for automatic upgrades, but two-thirds opted for private Vault Manufacturing instances to comply with residency requirements.

Siemens and Dassault Systèmes dominate in biologics manufacturing through recipe-driven MES capable of sub-100-unit lots, while Rockwell Automation and Emerson integrate plant-level automation with enterprise IT for multi-site CDMOs. Vendors differentiate on cybersecurity, offering ISO 27001 certification, zero-trust architectures, and post-event penetration testing following incidents such as the Change Healthcare breach. Low-code disruptors target mid-tier buyers with rapid workflow configuration that reduces validation overheads, but large pharma stays cautious due to patent and data-integrity risks.

White-space innovations include AI-assisted deviation management, blockchain serialization for emerging markets, and predictive maintenance that correlates equipment health with batch quality metrics.

Pharmaceutical Management Software Industry Leaders

AssurX, Inc.

AXSource

EtQ Management Consultants, Inc.

Dassault Systèmes SE

IQVIA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Veeva and Zifo partnered to accelerate quality control modernization, merging laboratory informatics with enterprise quality dashboards

- August 2024: Valsoft bought Anju Software to bolster regulatory and quality management offerings

Global Pharmaceutical Management Software Market Report Scope

Quality management software is an automated system that helps an organization achieve its quality policies and goals, as outlined in the report's scope. It can be used for various purposes, such as tracking documents, identifying nonconformities, taking corrective action, and managing employees. Quality management software ensures that a product maintains its quality and is manufactured according to industry standards.

The Pharmaceutical Management Software Market Report is Segmented by Solution Type (Enterprise Resource Planning, Manufacturing Execution Systems, Quality and Compliance Management, Supply-Chain and Inventory Management, Customer and Commercial, Knowledge and Data Management), Deployment Model (On-Premise, Cloud-Based, Hybrid), End User (Pharmaceutical Companies, Biotechnology Firms, CDMOs and CMOs, CROs, Hospitals and Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Enterprise Resource Planning (ERP) |

| Manufacturing Execution Systems (MES) |

| Quality / Compliance Management (QMS & eBR) |

| Supply-Chain / Inventory Management |

| Customer / Commercial (CRM, PBM) |

| Knowledge & Data Management |

| On-Premise |

| Cloud-Based |

| Hybrid |

| Pharmaceutical Companies |

| Biotechnology Firms |

| CDMOs / CMOs |

| CROs |

| Hospitals & Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Enterprise Resource Planning (ERP) | |

| Manufacturing Execution Systems (MES) | ||

| Quality / Compliance Management (QMS & eBR) | ||

| Supply-Chain / Inventory Management | ||

| Customer / Commercial (CRM, PBM) | ||

| Knowledge & Data Management | ||

| By Deployment Model | On-Premise | |

| Cloud-Based | ||

| Hybrid | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Firms | ||

| CDMOs / CMOs | ||

| CROs | ||

| Hospitals & Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for spending on platforms that manage pharmaceutical quality, manufacturing, and regulatory data?

The pharmaceutical management software market is projected to grow at an 11.67% CAGR from 2026 to 2031.

Which solution type currently holds the largest revenue?

Manufacturing Execution Systems led with 36.12% share in 2025.

Why are hybrid deployments gaining traction?

Hybrid models allow companies to keep validated batch records on-premise for compliance while running analytics in sovereign clouds, balancing agility with residency mandates.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 14.71% CAGR through 2031, driven by China’s and India’s manufacturing investments.

How do electronic batch records impact deviation investigations?

EBR implementations have reduced average deviation-resolution time from 28 days to 11 days by automating root-cause workflows.

Page last updated on: