Citrus Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

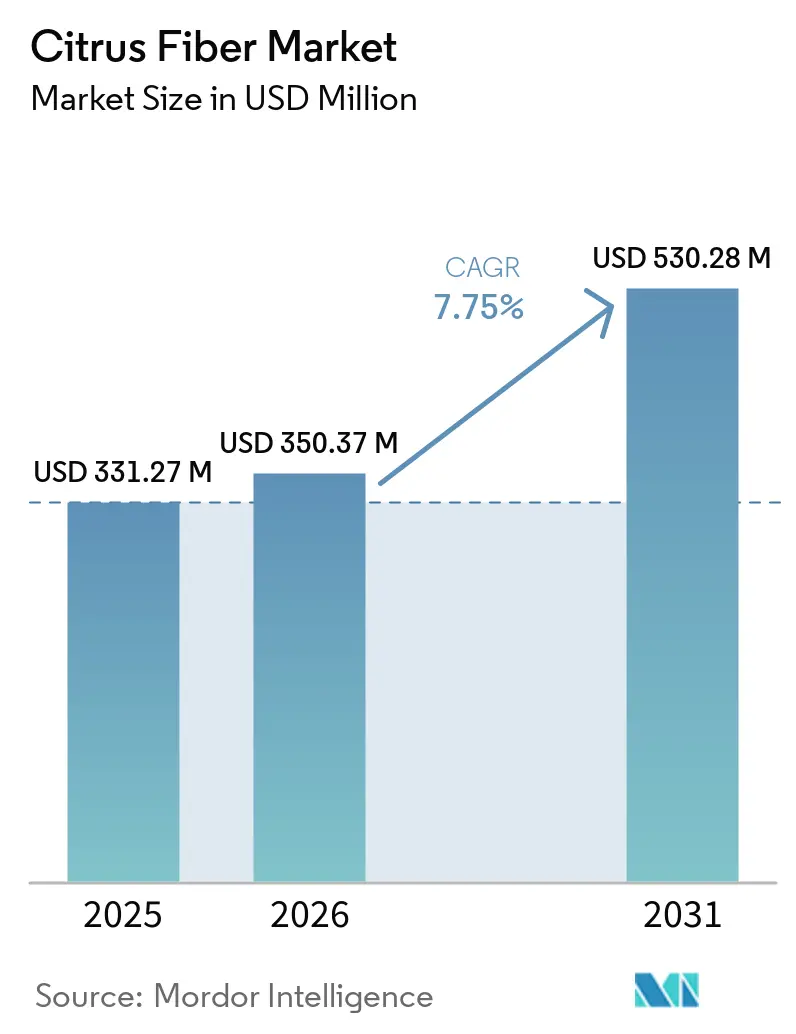

| Market Size (2026) | USD 350.37 Million |

| Market Size (2031) | USD 530.28 Million |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Citrus Fiber Market Analysis by Mordor Intelligence

The Citrus fiber market size is projected to be USD 331.27 million in 2025, USD 350.37 million in 2026, and reach USD 530.28 million by 2031, growing at a CAGR of 7.75% from 2026 to 2031. The citrus fiber market is moving forward on the back of clean-label reformulation, because food and beverage companies are under steady pressure to remove synthetic additives without giving up texture, moisture retention, or stability. The citrus fiber market is also benefiting from the use of orange, lemon, lime, and grapefruit peel side streams, which supports both raw material recovery and ingredient transparency for manufacturers working with stricter sourcing standards. Europe remained the largest regional center in 2025 because food additive rules continue to favor simpler ingredient declarations, while North America is expanding faster as fiber enrichment and GLP-1-adjacent product development gain more attention in food formulation pipelines. Competition in the citrus fiber market remains fragmented, but the Tate & Lyle acquisition of CP Kelco has raised the scale advantage of the largest suppliers and increased attention on capacity, technical service, and product specialization. The citrus fiber market also continues to attract opportunity in cosmetics, organic-certified supply chains, and granule formats, where suppliers can solve formulation issues that standard hydrocolloids do not address as neatly

Key Report Takeaways

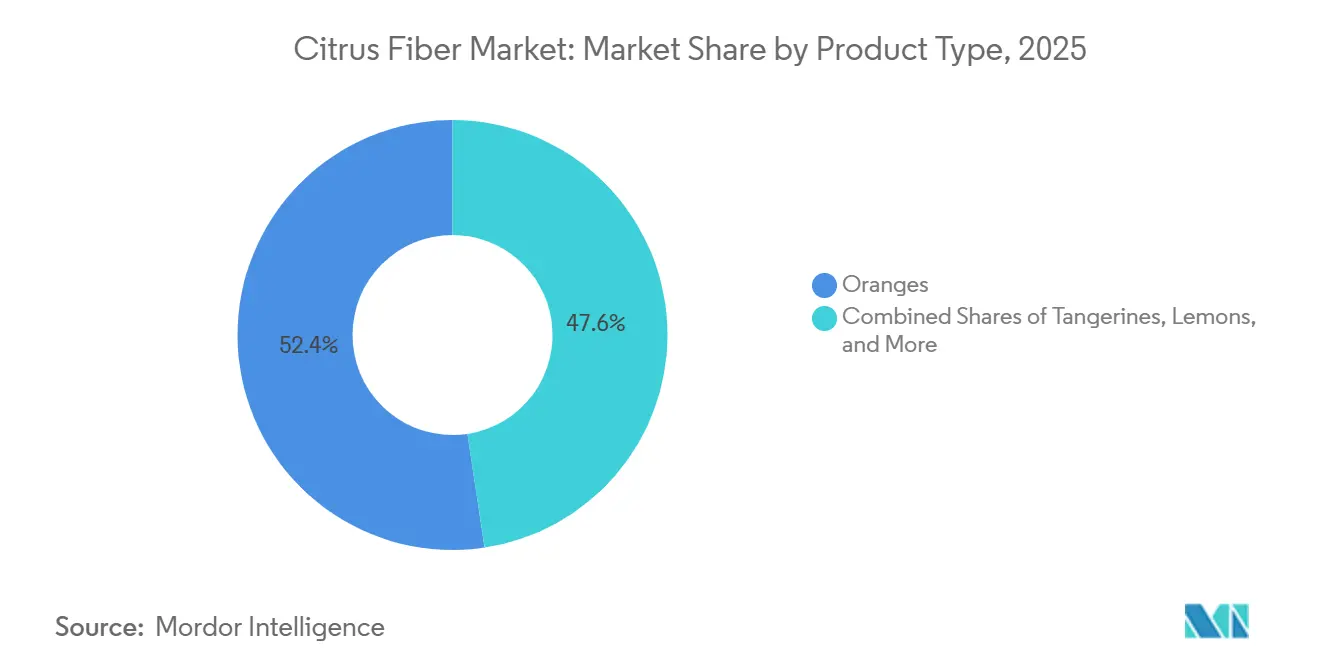

- By source, oranges held 52.38% of the citrus fiber market share in 2025, while lemons and limes recorded the fastest projected CAGR at 9.25% through 2031.

- By form, powder accounted for 45.38% of the citrus fiber market size in 2025, while granules is forecast to expand at a 9.11% CAGR through 2031.

- By nature, natural held 65.78% share in 2025, while organic is projected to grow at an 8.68% CAGR through 2031.

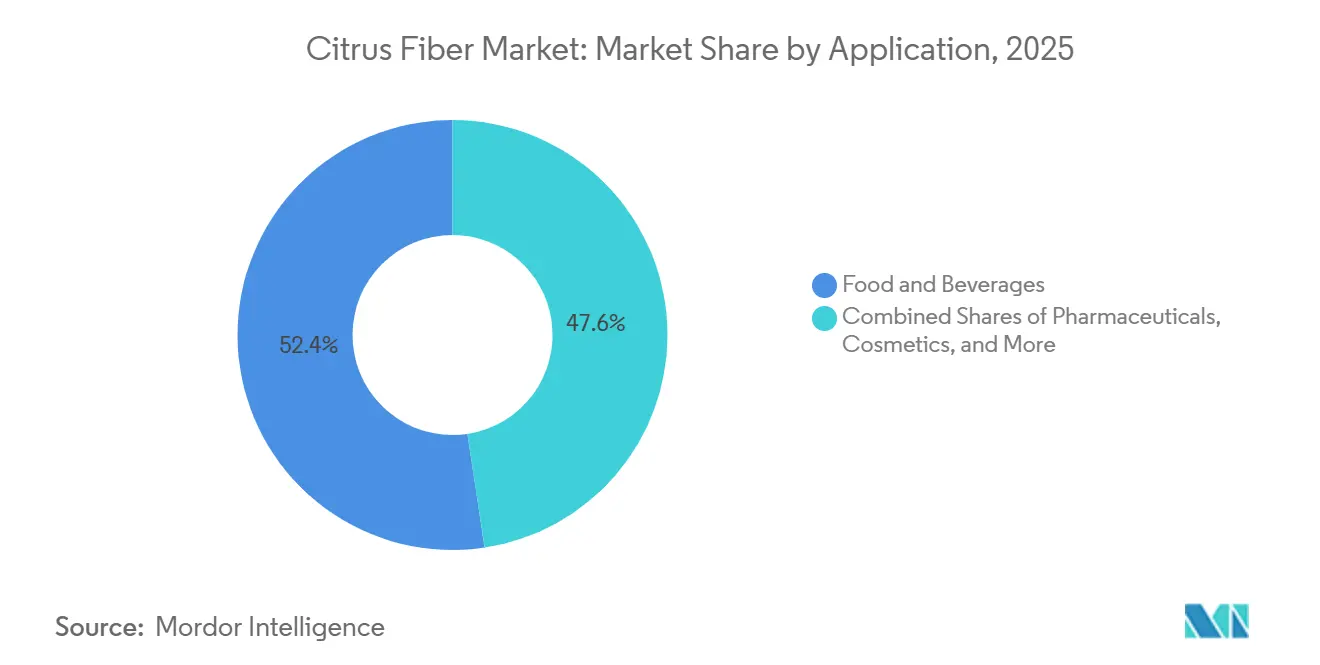

- By application, food and beverages led with 52.38% revenue share in 2025, while cosmetics and personal care is forecast to advance at a 9.02% CAGR through 2031.

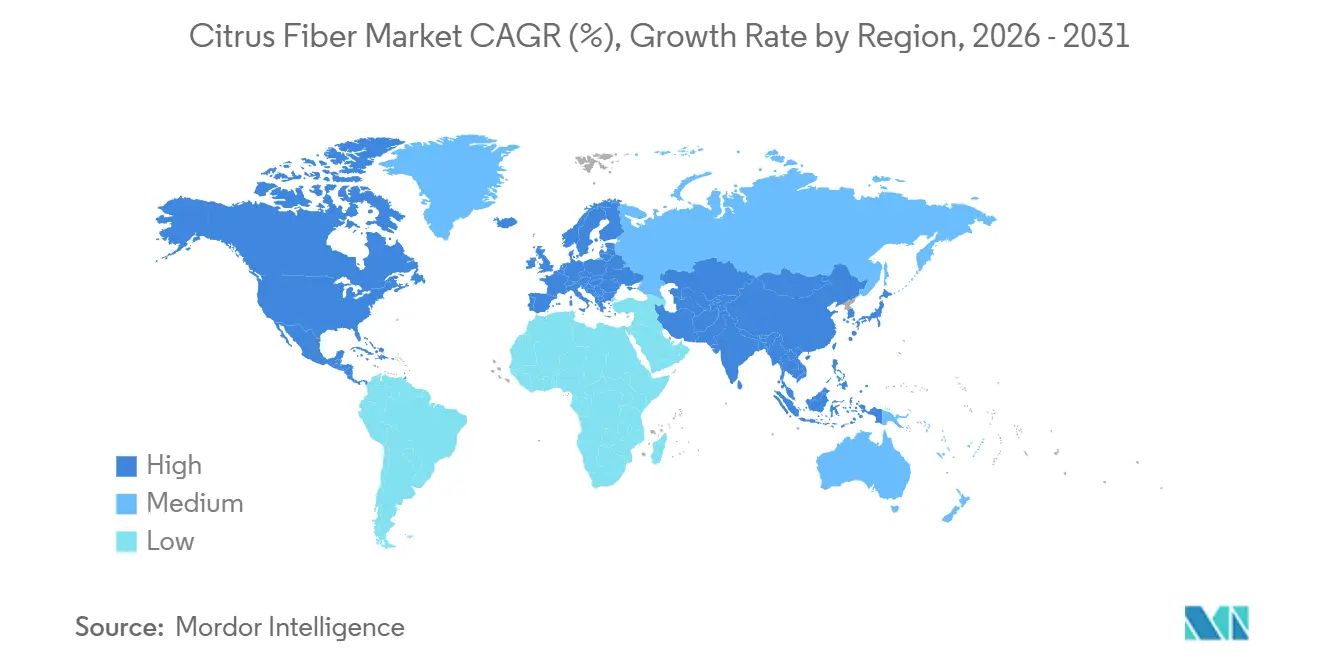

- By geography, Europe led with 38.28% share in 2025, while North America posted the highest projected CAGR at 8.26% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Citrus Fiber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Clean-Label Ingredients | +1.8% | Global | Short term (≤ 2 years) |

| Increasing Focus on Dietary Fiber Enrichment | +1.5% | Global | Medium term (2-4 years) |

| Rising Demand for Fat and Calorie Reduction Solutions | +1.2% | North America & EU | Medium term (2-4 years) |

| Growth of the Bakery and Processed Food Industries | +1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Regulatory Support for Natural Ingredients | +0.8% | North America & EU | Medium term (2-4 years) |

| Rising Technological Advancements in Fiber Manufacturing | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Clean-Label Ingredients

Clean-label reformulation has become a practical requirement for many packaged food launches, and that is lifting the role of citrus fiber in modern ingredient systems. Ingredion expanded FIBERTEX citrus fiber across EMEA in July 2024 and into Asia-Pacific in September 2024, which showed that large suppliers were seeing broad demand rather than isolated regional interest. Citrus fiber is appealing because it can support water binding, emulsification, gelling, and texture control in one ingredient, so manufacturers can often reduce the number of items listed on the label. The FDA has already issued GRAS response letters that support citrus fiber use across food applications, which gives product developers a clearer regulatory path when they replace synthetic additives or gums[1]Source: US Food and Drug Administration, “Agency Response Letter GRAS Notice No. GRN 000943,” FDA GRAS Notice Inventory, fda.gov. In Europe, food additive scrutiny remains strong under Regulation (EC) No. 1333/2008, and that keeps demand firm for ingredients that help brands stay closer to an E-number-free declaration.

Increasing Focus on Dietary Fiber Enrichment

Dietary fiber intake is still below recommended levels in many major markets, and that gap continues to support the citrus fiber market. The World Health Organization recommends at least 25 grams of naturally occurring dietary fiber per day for adults, and public health literature still points to persistent underconsumption across large populations[2]Source: World Health Organization, “Healthy Diet,” World Health Organization, who.int. The US Dietary Guidelines Advisory Committee also confirmed in December 2024 that dietary fiber remains one of the most underconsumed nutrients for Americans aged 1 year and older. Citrus fiber fits this need because it brings both soluble and insoluble fractions, which lets manufacturers improve nutrition claims while still managing texture, moisture, and stability. That combination makes the citrus fiber market relevant across everyday foods, where fortification only works when the ingredient can be added without creating sensory problems.

Rising Demand for Fat and Calorie Reduction Solutions

Citrus fiber can bind large amounts of water and meaningful levels of oil, which helps it act as a fat mimetic in bakery and related formulations. Peer-reviewed work cited showed that citrus by-products can support fat reduction in bakery systems while helping preserve mouthfeel and structure, which explains the continued use of citrus fiber in reduced-fat development work. European nutrition and health claim rules also support the use of functional ingredients when manufacturers want to substantiate reduced-fat and fiber-related claims in a compliant way. This matters more now because product developers are trying to build foods that align with calorie control, satiety, and better nutritional density without making the label more complex. The citrus fiber market therefore gains from both technical need and label need in the same formulation cycle.

Growth of the Bakery and Processed Food Industries

Bakery remains one of the clearest demand anchors for the citrus fiber market because the ingredient helps with moisture retention, crumb structure, shelf life, and fat replacement. The bakery products market stands at USD 524.99 billion in 2026 and is forecast to reach USD 647.68 billion by 2031 at a CAGR of 4.29%, which keeps a large end-use base in place for citrus fiber suppliers. Citrus fiber is also useful in gluten-free bakery, where it can support water distribution and improve cohesion in systems that cannot rely on gluten functionality. As food production lines become more automated, processors are giving more attention to ingredient flowability, dispersion, and dosing accuracy. That shift helps explain why the citrus fiber market is seeing stronger interest in granules, which suit high-throughput systems better than fine powders in some applications.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Cost Compared to Conventional Hydrocolloids | -1.2% | Global | Short term (≤ 2 years) |

| Formulation Complexity During Ingredient Replacement | -0.9% | North America & EU | Medium term (2-4 years) |

| Availability of Alternative Fiber Ingredients | -0.7% | Global | Long term (≥ 4 years) |

| Supply Chain Disruptions from Climate and Disease Risks | -0.8% | South America, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Cost Compared to Conventional Hydrocolloids

Citrus fiber still carries a cost premium against simpler texturizers such as xanthan gum, locust bean gum, or modified starches in many formulations. Processing methods that involve homogenization, drying, and tight particle control raise manufacturing costs, especially when suppliers target high and consistent functionality rather than commodity output. Raw material pressure adds to this issue, because Brazil's 2024/25 orange processing season fell to 194.8 million 40.8-kg boxes, which reduced peel availability in the largest orange processing chain. Even so, suppliers continue to argue that one citrus fiber ingredient can replace several mono-functional additives, which can improve total formulation economics even when unit pricing looks higher at first review. The restraint remains real, especially in price-sensitive product lines where procurement teams still focus on direct ingredient cost more than total system cost.

Formulation Complexity During Ingredient Replacement

Replacing legacy hydrocolloids with citrus fiber often requires changes in mixing speed, sequence, shear, or hydration control, which slows adoption in existing plants. Citrus fiber does not always behave like a direct 1:1 substitute, and under-activation can leave the finished product with weaker texture or inconsistent viscosity. This makes the development cycle longer for manufacturers that do not have dedicated texturizing expertise or strong supplier support. Suppliers such as Ingredion and JRS try to close that gap with technical guidance and application support, which has become an important commercial differentiator in the citrus fiber market. The issue is most visible in smaller companies, where limited pilot capacity and fewer reformulation resources can delay commercial conversion even when the ingredient is attractive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Orange Dominance Faces Lemon-Lime Disruption

Oranges accounted for 52.38% of the citrus fiber market share in 2025, which reflected the deep raw material base created by the global orange juice processing chain. Brazil remained central to that structure, and CitrusBR data showed that member companies processed around 171.0 million boxes in the 2024/25 season even after a sharp decline from the previous year. That same dependence also creates risk, because citrus greening disease and weather disruption reduced the 2024/25 Brazilian processing season by 27.3% year on year, which tightened peel availability for ingredient extraction. The citrus fiber market therefore remains heavily supported by orange peel, but it is no longer comfortable relying on one dominant source stream. Procurement teams are paying more attention to source resilience, not only to volume availability.

Lemons and limes are projected to grow at a 9.25% CAGR through 2031, which makes them the fastest-growing source segment in the citrus fiber market. This shift reflects a clear move by suppliers toward less constrained peel streams and a more balanced sourcing model. CEAMSA's January 2026 acquisition of PeelPioneers' Finix fiber line directly supported that direction and gave the company access to a lemon and lime peel-focused platform that can be scaled in Spain. Grapefruits, tangerines, and mandarins remain smaller sources, and they are used more selectively in regional supply chains or in formulations where flavor profile and sensory character matter more. Cargill's FiberDesign™ Citrus line, which uses lemon and lime peel for beauty formulations, also shows that source selection is becoming more application-specific as the citrus fiber market broadens beyond food.

By Form: Powder Leads While Granules Capitalize on Automation Trends

Powder held 45.38% of the citrus fiber market size in 2025, and it remained the leading form because most bakery and dairy plants already work with dry ingredient systems designed for powders. Standardized particle size and moisture control also fit existing food safety and quality routines, which helps explain the continued presence of established powder lines from JRS and Ingredion. Powder is therefore still the default choice in the citrus fiber market where familiarity, infrastructure, and workflow compatibility matter most. It works well in bakery premixes, dairy bases, and formulated dry systems that depend on predictable handling. Those advantages help protect the installed base even as other forms gain attention.

Granules, however, are projected to expand at a 9.11% CAGR through 2031, which makes them the fastest-growing form in the citrus fiber market. Their appeal is tied to process performance, because granules can reduce dust, improve flow through dosing systems, and disperse more evenly in some high-moisture applications. That makes them attractive for large processors that are upgrading automation and want fewer interruptions in continuous production environments. Research published in Sustainable Food Technology also showed that thermal and mechanical processing can change fiber structure and functionality, which supports more customized granule offerings for industrial users. The form shift does not weaken powder today, but it does show that the citrus fiber market is becoming more process-driven as customers ask for ingredients built around plant performance, not just composition.

By Nature: Natural Segment Anchors Volume While Organic Commands Premium Growth

The natural segment represented 65.78% of the citrus fiber market in 2025, which reflected the wide use of standard non-organic citrus peel fiber in mainstream clean-label formulations. The natural segment benefits from broader raw material access, simpler supply management, and a large installed base of products such as NUTRAVA, Citri-Fi, and HERBACEL that already fit non-GMO and clean-label positioning . In practice, that means many food manufacturers can secure the label benefits they want without taking on the added traceability burden of certified organic sourcing. This keeps the natural segment central to volume movement across bakery, dairy, savory, and meat alternative applications. It also means the citrus fiber market still depends on standard grades for its broadest commercial reach.

Organic is forecast to grow at an 8.68% CAGR through 2031, which keeps it close to the overall pace of the citrus fiber market. Growth is being supported by premium retail channels in Europe and North America, where organic certification still carries pricing power and stronger shelf positioning. Supply remains tighter here because organic citrus acreage is limited and certified peel collection requires segregation and documentation from field to finished ingredient. Fiberstar addressed that opportunity with its USDA Certified Organic Citri-Fi 400 series, which gave brands a direct route into organic reformulation without giving up citrus fiber functionality. The result is a smaller segment today, but one with stronger premium characteristics and more disciplined supply economics.

By Application: Food and Beverages Dominates but Cosmetics Reshapes the Growth Profile

Food and beverages accounted for 52.38% of the citrus fiber market share in 2025, which made this the largest application segment by a wide margin. Bakery and confectionery remained the main anchor, because citrus fiber helps retain moisture, support crumb texture, extend shelf life, and reduce fat in breads, biscuits, muffins, croissants, and fillings. Dairy and dairy alternatives also stayed important, as citrus fiber performs well in systems that need stable texture during thermal processing and cold storage. Pharmaceutical and animal feed uses added steady demand, with JRS highlighting applications in tablet systems and feed formulations that value high total dietary fiber and a clean profile. This broad end-use base keeps the citrus fiber market closely tied to food formulation needs, even as newer applications begin to grow faster.

Cosmetics and personal care is forecast to expand at a 9.02% CAGR through 2031, which gives the citrus fiber market one of its clearest premium growth pockets. The appeal comes from citrus fiber's role in emulsion stabilization and texture building, especially in formulations that want to avoid PEG-derived emulsifiers and other synthetic inputs under tighter consumer and regulatory scrutiny. Cargill's FiberDesign Citrus line and Tate & Lyle's KELCOSENS PiEL Citrus Fiber show that suppliers are no longer treating beauty as a side outlet for food-grade material. Instead, they are building dedicated portfolios around certification, texture performance, and formulation support. That raises the growth profile of the citrus fiber market because cosmetic applications can support stronger pricing and a more specialized product mix.

Geography Analysis

Europe held 38.28% of the citrus fiber market share in 2025, which kept it as the largest regional segment. The region benefits from advanced ingredient infrastructure and long-standing scrutiny of food additives under Regulation (EC) No. 1333/2008[3]Source: European Parliament and Council, “Regulation (EC) No. 1333/2008 on Food Additives,” EUR-Lex, eur-lex.europa.eu. That regulatory setting supports demand for ingredients that simplify declarations while still performing across bakery, dairy, meat, and savory products. Germany remained an active demand center because transparent-label food products have gained more shelf importance across packaged categories. Italy and Spain also matter because Mediterranean citrus processing supports local peel availability and closer integration between raw material recovery and ingredient production. CEAMSA's position in Spain reflects that regional supply link and shows how Europe combines demand pull with in-region processing capability.

North America is projected to grow at an 8.26% CAGR through 2031, which makes it the fastest-growing region in the citrus fiber market. Growth is being driven by clean-label reformulation, broader interest in fiber-enriched products, and the ongoing expansion of GRAS-supported use categories in the United States. The July 2024 supplemental GRAS filing tied to GRN 943 widened approved use levels across processed meat and poultry, baked goods, non-milk meal replacement beverages, and ready-to-eat breakfast cereals, which expanded the addressable base for formulators FDA.GOV. The US Dietary Guidelines Advisory Committee also strengthened the nutrition case in December 2024 by reaffirming that dietary fiber remains underconsumed across age groups. Canada and Mexico add support through processed food growth, but the United States remains the main engine because of its scale, regulatory clarity, and stronger innovation pipeline.

Asia-Pacific is the third-largest regional cluster in the citrus fiber market and continues to gain traction through China, Japan, and India. Japan's long-standing interest in health-forward ingredients supports adoption in beverages, dairy, and confectionery. China combines citrus production scale with a growing food ingredient user base, which gives the region both supply and demand advantages over time. South America plays a distinct role because it is not only a demand region but also a major feedstock and production base, especially through Brazil's citrus processing corridor. Middle East and Africa remains the smallest regional group, but demand is improving in Gulf markets where premium packaged foods and imported natural ingredients are becoming more visible. These patterns mean the citrus fiber market is still led by Europe today, but its next wave of growth is being shared more broadly across North America and selected Asia-Pacific countries.

Competitive Landscape

The citrus fiber market remains fragmented, with a small group of large specialty ingredient suppliers and a long list of regional participants. Tate & Lyle, Ingredion, Cargill, Fiberstar, CEAMSA, and JRS are among the most visible companies because they pair ingredient production with application support, regulatory knowledge, and broader commercial reach. This structure means scale matters, but technical service and application fit still decide many customer wins. It also means the citrus fiber market is active enough for consolidation, yet still open enough for smaller players to compete in price-led or region-led positions.

The largest strategic move in recent years was Tate & Lyle's acquisition of CP Kelco for USD 1.8 billion in November 2024. That deal combined CP Kelco's citrus fiber capacity and product lines with Tate & Lyle's wider commercial infrastructure and R&D depth. Another notable move came in January 2026, when CEAMSA acquired PeelPioneers' Finix citrus fiber line and related intellectual property, which strengthened its supply diversification and Spanish production plans. Ingredion also expanded its FIBERTEX® citrus fiber rollout across EMEA and Asia-Pacific in 2024, which showed that geographic expansion remains a practical route to share gain. These moves show that growth in the citrus fiber market is being pursued through acquisition, regional rollout, and product specialization at the same time.

There are still clear openings in cosmetics-grade citrus fiber, organic-certified supply chains, and granule formats tailored for automated food plants. Cargill and Tate & Lyle have already developed cosmetic-specific offerings, which suggests that application-led portfolio design can create stronger pricing power than standard food-grade volumes alone. Regional suppliers such as Yantai Andre Pectin, Hebei Lemont Biotechnology, and Nans Products remain relevant because they can compete on proximity and pricing in selected APAC accounts. Even so, the citrus fiber market increasingly rewards companies that can combine secure peel sourcing, scalable processing, regulatory credibility, and hands-on formulation support. That balance keeps the field competitive, but it also gives larger integrated suppliers a clearer advantage as requirements become more technical.

Citrus Fiber Industry Leaders

Cargill, Incorporated

Tate & Lyle PLC

Ingredion Inc.

Fiberstar, Inc.

CEAMSA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Fiberstar launched Citri-Fi Pro, a natural citrus fiber ingredient designed to replace up to 75% of acacia gum or modified food starch in beverage emulsions. The product addresses ethical and supply chain risks associated with acacia gum sourced from conflict-affected regions, and was developed in response to accelerating clean-label beverage reformulation demand signaled at Fi Europe 2025.

- January 2026: CEAMSA (Compañía Española de Algas Marinas) acquired the Finix citrus fiber line and associated intellectual property from Dutch circular ingredient company PeelPioneers, following the latter's December 2025 bankruptcy. The acquisition expands CEAMSA's CEAMFIBRE range and enables planned production scale-up at its Spanish facilities, reinforcing the company's international growth strategy in natural fiber texturizers.

- November 2024: Tate & Lyle completed the acquisition of CP Kelco from J.M. Huber Corporation for total consideration of USD 1.8 billion, settled through the issuance of 75 million new Tate & Lyle ordinary shares and USD 1.15 billion in net cash. CP Kelco's NUTRAVA and KELCOSENS citrus fiber product lines, together with a 5,000 MT Brazil-based production facility, were integrated into the combined entity, which began operating as a unified business from April 2025.

Global Citrus Fiber Market Report Scope

| Orange |

| Tangerines and Mandarins |

| Grapefruits |

| Lemons and Limes |

| Powder |

| Granules |

| Natural |

| Organic |

| Food and Beverages | Bakery and Confectionery |

| Beverages | |

| Dairy and Dairy Alternatives | |

| Meat Alternatives | |

| Others | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Animal Feed | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Source | Orange | |

| Tangerines and Mandarins | ||

| Grapefruits | ||

| Lemons and Limes | ||

| By Form | Powder | |

| Granules | ||

| By Nature | Natural | |

| Organic | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Beverages | ||

| Dairy and Dairy Alternatives | ||

| Meat Alternatives | ||

| Others | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Animal Feed | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value forecast for citrus fiber?

The Citrus fiber market is projected to reach USD 530.28 million by 2031, rising from USD 350.37 million in 2026 at a CAGR of 7.75%.

Which region leads citrus fiber demand today?

Europe led in 2025 with 38.28% share, supported by strong clean-label demand and tighter food additive standards.

Which region is expanding the fastest through 2031?

North America is projected to grow at an 8.26% CAGR through 2031, helped by reformulation activity and broader FDA-supported use categories.

Which source segment is growing the fastest?

Lemons and limes is the fastest-growing source segment, with a projected CAGR of 9.25% through 2031 as suppliers diversify peel sourcing.

Page last updated on: