Citrus Pectin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.30 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Citrus Pectin Market Analysis by Mordor Intelligence

The citrus pectin market size is projected to expand from USD 914.57 million in 2025 and USD 969.91 million in 2026 to USD 1,301.02 million by 2031, registering a 6.05% CAGR between 2026 and 2031. With tightening clean-label regulations and the surging popularity of plant-based trends, the citrus pectin market is undergoing a notable transformation. As the demand for recognizable ingredients grows, so do the regulatory pressures on synthetic hydrocolloids[1]Source: European Commission, "New rules enter into force for a more sustainable and competitive packaging economy ", environment.ec.europa.eu. Brands are increasingly opting for low-methoxyl and amidated grades to align with sugar-reduction mandates, as these grades offer better functionality in reduced-sugar formulations. Meanwhile, specialty pectins sourced from lime and grapefruit are carving out a niche in the premium confectionery segment due to their unique gelling properties and flavor profiles. While Europe remains the dominant player in terms of revenue, the Asia-Pacific region is making rapid strides. This growth is driven by a burgeoning middle class with rising disposable incomes, new production capacities in China to meet local and export demand, and India's streamlined additive regulations that simplify market entry. Fluctuations in raw material prices, coupled with rising energy costs for extraction, are pushing investments towards green technologies and the valorization of circular feedstocks. This trend particularly benefits vertically integrated producers who are already expanding their microwave and ultrasound-assisted production lines, as these technologies enhance efficiency and reduce environmental impact.

Key Report Takeaways

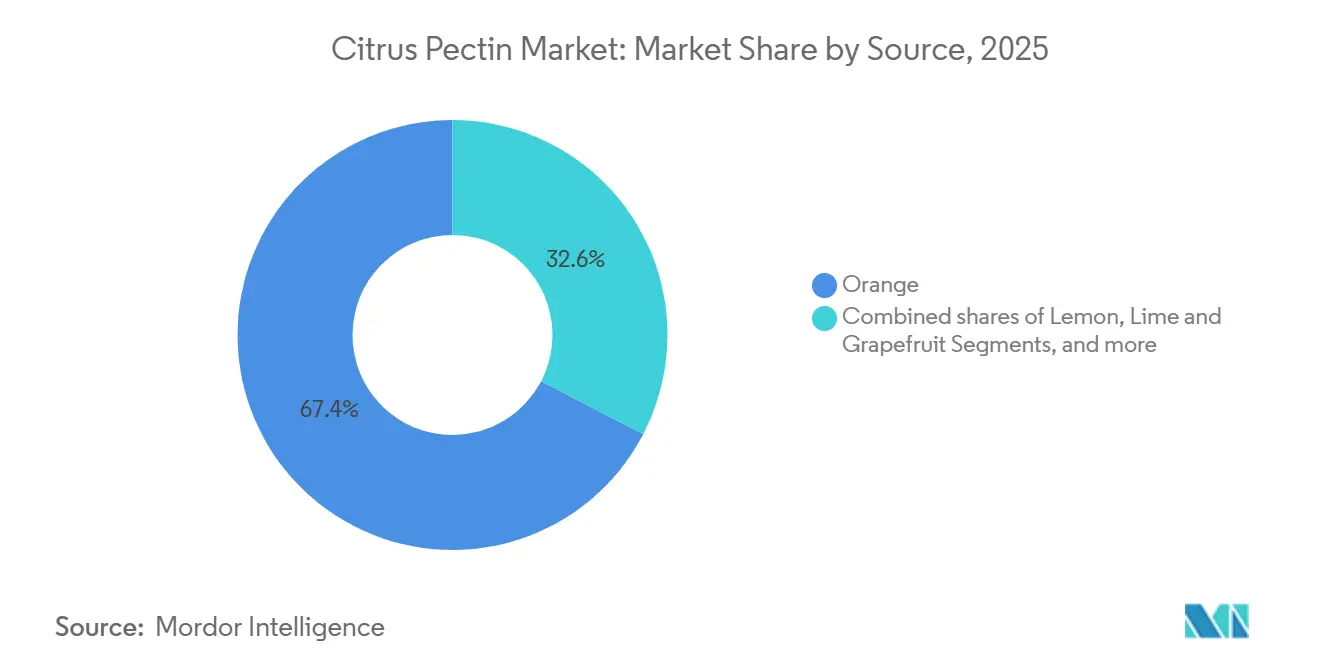

- By source, citrus peel dominated with 84.48% of 2025 revenue, while lime and grapefruit pectin are growing at a 6.38% CAGR through 2031.

- By type, high-methoxyl products led with a 58.35% citrus pectin market share in 2025; low-methoxyl variants posted the fastest 6.42% CAGR over 2026-2031.

- By category, conventional grades accounted for 67.42% of the 2025 citrus pectin market size; organic and natural grades advanced at a 6.79% CAGR.

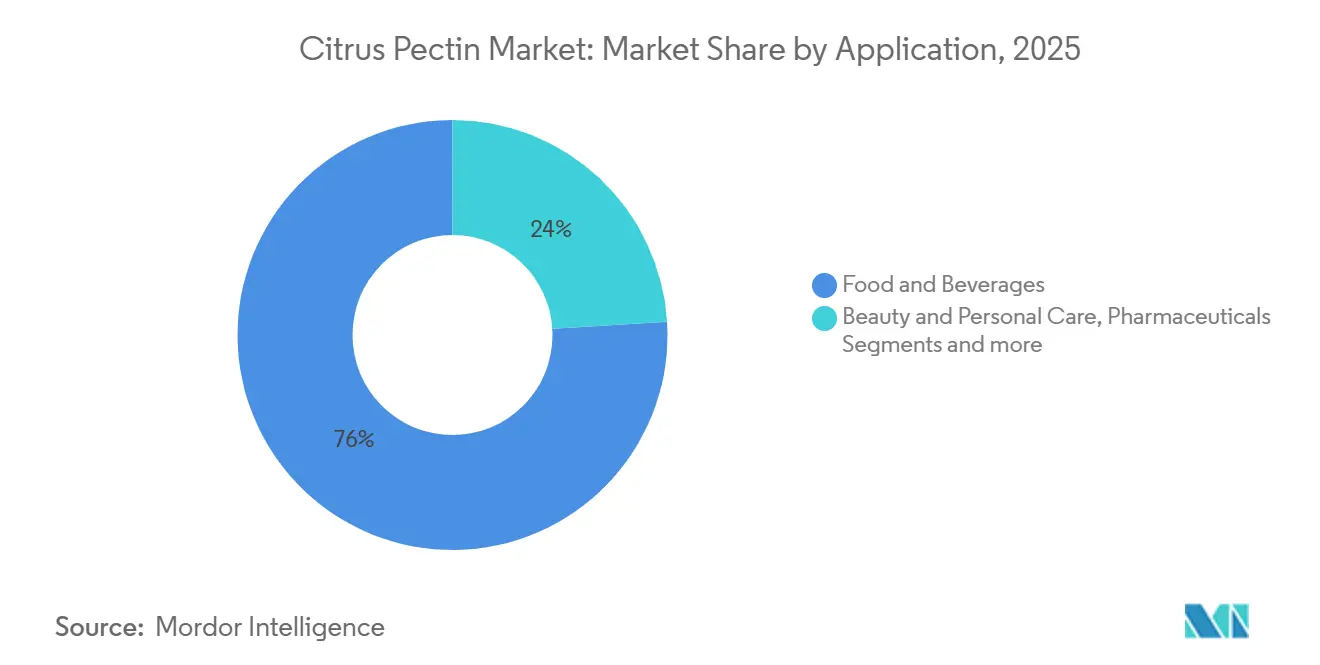

- By application, food and beverage captured 75.25% of 2025 demand; pharmaceutical use registers a 6.74% CAGR to 2031.

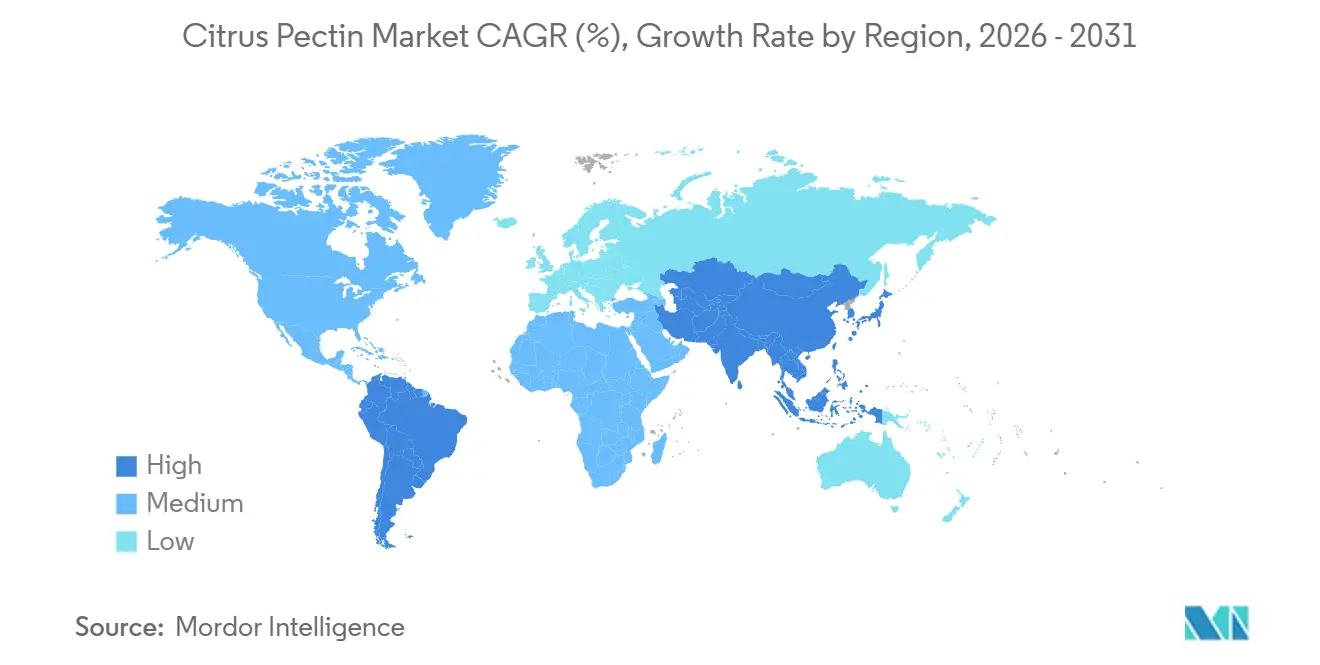

- By geography, Europe commanded 29.60% of 2025 revenue, whereas Asia-Pacific expands at a 7.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Citrus Pectin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label and natural-ingredient demand surge | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of plant-based and vegan diets | +0.7% | Global, led by North America, EU, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing low/no-sugar product launches (LM pectin) | +0.9% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Industrial up-cycling of citrus and apple waste streams | +0.5% | Global, with early adoption in Europe and Brazil | Long term (≥ 4 years) |

| 3-D food printing and novel texture-engineering uses | +0.3% | Asia-Pacific core and Europe, spill-over to North America | Long term (≥ 4 years) |

| Pharma and medical-grade pectin for wound-care scaffolds | +0.6% | Global, led by North America, Europe, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clean-label and natural-ingredient demand surge

As consumers and regulators increasingly favor shorter, more natural ingredient lists, the FDA's February 2026 guidance has intensified scrutiny on "no artificial colors" claims. This shift has hastened the move from synthetic stabilizers to fruit-derived hydrocolloids like pectin, which is widely used as a gelling agent and stabilizer in various food products. In the U.S., E440, which holds GRAS status and EFSA clearance, empowers manufacturers to raise prices for premium yogurt and organic jams by 15-20% in North America and Europe[2]Source: European Food Safety Authority, " Re-evaluation of pectin (E 440i) and amidated pectin (E 440ii) as food additives", efsa.onlinelibrary.wiley.com. The ability to market these products as containing natural, clean-label ingredients appeals to health-conscious consumers, further driving demand. Even with steeper costs for certified peels, organic pectin commands a premium, underscoring the citrus pectin market's shift towards more valuable grades and its alignment with the growing trend of value-added, sustainable food solutions.

Expansion of plant-based and vegan diets

In 2024, the market for plant-based gelatin alternatives hit USD 1.9 billion, with pectin emerging as a key winner. Low-methoxyl pectin, reacting with calcium, creates sugar-free gels. This innovation allows for the production of vegan yogurts and confections without compromising on texture, offering a healthier and more sustainable alternative to traditional gelatin-based products. Furthermore, pharmaceutical capsules made with pectin cater to both halal and kosher requirements, expanding their appeal in Southeast Asia and the Middle East, where dietary and religious compliance significantly influence consumer preferences. Additionally, regulatory endorsements from India's FSSAI and China's GB2760-2024 bolster the cross-border trade of these vegan products, ensuring smoother market entry and adherence to local standards[3]Source: National Center for Biotechnology Information, " Increasing the Activity of the High-Fidelity SpyCas9 Form in Yeast by Directed Mutagenesis of the PAM-Interacting Domain", pmc.ncbi.nlm.nih.gov.

Growing low/no-sugar product launches (LM Pectin)

Legislation aimed at reducing sugar content, coupled with Brix caps, is driving a shift towards calcium-set pectin. These regulations are encouraging manufacturers to explore alternatives that maintain product quality while adhering to health guidelines. Cargill's UniPECTINE LMC Plus showcases strong gelling properties at 20-30 Brix, ensuring the fruit flavor intensity remains vibrant in jams and yogurts, even with reduced sugar levels. Meanwhile, colon-targeted pectin microspheres have achieved gelatin-like performance, enabling sustained release of active ingredients. This advancement presents both pharmaceutical and culinary benefits, such as improved drug delivery systems and enhanced food textures. As a result, the citrus pectin market is reaping rewards from worldwide public health initiatives targeting added sugars, aligning with the growing consumer demand for healthier food options.

Industrial up-cycling of citrus and apple waste streams

Juice processors produce an annual peel waste of up to 20 million tonnes. By extracting pectin from this waste, processors can generate a revenue of USD 400-650 per dry tonne, simultaneously reducing disposal costs. Pectin, a valuable polysaccharide widely used in food, pharmaceuticals, and cosmetics, adds significant value to what would otherwise be discarded as waste. Utilizing microwave-assisted extraction not only boosts yields to over 35% but also cuts energy consumption by 40-50%. This advancement reduces cradle-to-gate emissions in leading EU plants from 9.69 kg CO₂e per kg of product to a mere 5-6 kg, contributing to more sustainable production practices. Furthermore, the EU's Circular Economy directives, alongside Brazil's waste policy, are accelerating capital expenditure payback periods, thereby promoting a circular supply chain in the citrus pectin market. These policies encourage the adoption of innovative technologies and sustainable waste management practices, further driving growth in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price and supply volatility (citrus greening) | -0.7% | Americas (Florida, Brazil) and Asia-Pacific (China) | Short term (≤ 2 years) |

| Complex and evolving global food-additive regulations | -0.4% | Global, with divergence between Europe, China, and India | Medium term (2-4 years) |

| Rising competition from precision-fermentation hydrocolloids | -0.3% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| High energy intensity of advanced extraction technologies | -0.2% | Global, acute in regions with carbon pricing (Europe, California) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-material price and supply volatility (citrus greening)

Florida's juice-orange production has dropped 72% since 2019 due to Huanglongbing (citrus greening), with the 2024–2025 harvest projected at 12 million boxes. This decline has raised pectin feedstock costs by 35–40% year-on-year. Brazil, supplying 70% of global orange-juice concentrate, reported a 44.35% disease incidence in São Paulo groves in 2024. Eradication costs reached USD 1,200 per hectare, leading to the abandonment of 15% of planted areas. The Asian citrus psyllid, the disease's vector, has no commercial cure, making integrated pest management the only mitigation strategy, adding USD 800–1,000 per hectare annually. Pectin manufacturers are diversifying feedstock, with lime and grapefruit peels now valued at USD 150–200 per tonne, and apple pomace reintroduced as a secondary source. However, apple pectin's lower esterification (30–50% vs. 60–75% for citrus) limits its use in high-sugar jams. Forward contracts for citrus peel have extended to 18–24 months, securing supply but reducing flexibility to benefit from spot-market price drops. North America faces the most volatility, as Florida's decline has shifted procurement to Mexico and Central America, increasing logistics costs by 10–15% and exposing supply chains to currency and trade-policy risks.

Complex and evolving global food-additive regulations

The regulatory landscape for pectin is fragmented due to varying purity standards and usage limits. EFSA's 2017 and 2021 evaluations found no need for a numerical ADI for E440i and E440ii but flagged methanol release for infants under 16 weeks, prompting manufacturers to reformulate infant-formula pectin with a DE below 50%. China's GB2760-2024 permits pectin in most food categories, excluding certain raw materials, and caps usage at 3.0 g/kg in fruit and vegetable juices, limiting options for beverage producers in mainland China. India's FSSAI mandates methanol below 1%, sulfur dioxide below 50 mg/kg, and lead below 2.0 mg/kg, with batch-level certificates adding 5–7 days to import clearance. The Codex Alimentarius allows 10,000 mg/kg in infant follow-up formula but limits it to 2,000 mg/kg in medical-purpose infant formula, creating SKU-specific compliance challenges. Small and mid-sized producers face compliance costs exceeding USD 200,000 annually, eroding margins on commodity-grade pectin, while larger, vertically integrated players with in-house labs are better positioned.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Specialty Lime and Grapefruit Variants Accelerate

Orange-based pectin, accounting for 84.48% of the 2025 turnover, highlights the market's reliance on orange and lemon peel streams. Concerns over the risks associated with orange-linked feedstock have led to longer forward-contract tenures and diversified sourcing strategies, bolstering supply security. Even with this concentration, traditional jam producers remain heavily dependent on orange-derived volumes. The dominance of orange-based pectin reflects the limited availability of alternative feedstocks that can match its functionality. Additionally, the market's focus on securing stable supply chains underscores the critical role of orange and lemon peel in pectin production.

Lime and grapefruit pectin is the fastest-growing segment, expanding at a 6.38% CAGR. Formulators appreciate its high galacturonic content, especially for confectionery gels. Meanwhile, grapefruit pectin is finding new applications in digestive supplements, thanks to its mild bitterness. This growth is driven by increasing demand for innovative formulations in the food and nutraceutical industries. Furthermore, the segment's expansion highlights the growing interest in diversifying pectin sources to meet evolving consumer preferences and mitigate supply risks.

By Type: Low-Methoxyl Pectin Captures No-Sugar Momentum

High-methoxyl pectin, commanding a 58.35% revenue share in 2025, stands as the leading segment. Its dominance is largely attributed to its prevalent use in traditional high-Brix jams and jellies. While witnessing a modest annual volume growth of 4.5%, high-methoxyl pectin's stronghold is bolstered by sustained demand in both mature and emerging markets. Notably, its resilience shines in economies with a pronounced consumption of sweet spreads. The segment benefits from its compatibility with high-sugar formulations, which remain popular in various regions. Additionally, its established supply chain infrastructure ensures consistent availability across global markets.

Low-methoxyl pectin emerges as the segment with the most rapid growth, boasting a projected CAGR of 6.42% through 2026 to 2031. This surge is largely driven by legislation curbing added sugars in food. Additionally, amidated low-methoxyl variants are becoming increasingly popular, especially for frozen desserts, due to their ability to prevent freeze-thaw syneresis. Their global market acceptance is further accelerated by EFSA’s E440ii clearance and FDA's GRAS status. The growing consumer preference for low-sugar and functional food products further supports this segment's expansion. Moreover, advancements in production technologies are enabling manufacturers to meet the rising demand efficiently.

By Category: Organic Certification Enhances Margin Mix

Conventional pectin, accounting for 67.42% of 2025 revenue, stands as the dominant segment. Its affordability makes it the go-to choice in price-sensitive markets, underscoring the significance of cost efficiency in food formulation. As a widely used ingredient in mainstream applications, it caters to the demand for cost-effective solutions in the food and beverage industry. Additionally, its consistent performance and availability make it a reliable option for manufacturers aiming to optimize production costs. The segment's dominance also reflects its adaptability across various product categories, including jams, jellies, and dairy products, further solidifying its market position.

Organic and natural pectin, the fastest-growing segment, is set to grow at a 6.79% CAGR through 2031. This growth is bolstered by USDA and EU organic certifications, allowing for shelf-price premiums of 10 to 15%. The rising consumer demand for clean-label products and sustainable sourcing practices further drives the adoption of organic and natural pectin. Moreover, advancements in extraction technologies are expected to support the development of high-quality natural pectin, addressing some supply constraints in the long term. The segment's growth is also fueled by increasing awareness of health benefits associated with organic products, which aligns with the broader trend of health-conscious consumer behavior.

By Application: Pharmaceuticals Outpace Core Food Demand

Food and beverage, accounting for 75.25% of 2025 volumes, leads the pack. Its dominance stems from widespread use in clean-label yogurt, bakery fillings, and premium jams. While it enjoys a steady growth rate of 5.8% CAGR, its commercial applications ensure continued momentum. Even in mature markets where growth appears flat, established food applications bolster demand. The segment benefits from consumer preferences for natural and clean-label products, which continue to drive innovation in formulations. Additionally, the increasing focus on premium and functional food products further supports its growth trajectory.

Medical applications are the fastest-growing segment, expanding at a robust 6.74% CAGR. This surge is fueled by their use in wound-care scaffolds and colon-targeted drug delivery systems. Notably, this segment boasts margins 3–5 times higher than their food-grade counterparts. Additionally, beauty and personal-care applications are gaining traction, and industrial uses are drawing attention for their biodegradability advantages. The rising prevalence of chronic diseases and advancements in drug delivery systems are key factors propelling this segment. Furthermore, the growing emphasis on sustainable and high-margin applications enhances its appeal across industries.

Geography Analysis

By 2025, Europe is set to command 29.60% of the turnover, with projections indicating a growth rate of 5.2% extending to 2031. This growth is largely attributed to decarbonized production initiatives at CP Kelco’s Lille Skensved and Cargill’s Redon plants. These facilities have successfully integrated renewable methods, resulting in a 30-40% reduction in CO₂e emissions per kg of pectin. The region's focus on sustainability and regulatory compliance has positioned it as a leader in environmentally friendly production. Additionally, investments in advanced manufacturing technologies are expected to further enhance efficiency and output.

Asia-Pacific is witnessing the most rapid growth, boasting a 7.03% CAGR. This surge is driven by China's broadened additive code and India's alignment with FSSAI standards. Additionally, Yantai Andre's capacity expansion fortifies the region's supply stability. The region's growing population and increasing demand for processed foods are further fueling the market's expansion. Moreover, government initiatives supporting local production and exports are strengthening the region's competitive edge. Meanwhile, North America is projected to account for 22-24% of the 2025 revenue. However, its growth is tempered at 5.5%, grappling with raw material disruptions stemming from Florida's citrus downturn. In response, procurement strategies have shifted towards Mexico and Central America, albeit with elevated freight expenses. The region's reliance on imports has increased, leading to higher operational costs for manufacturers. Despite these challenges, innovations in product formulations are helping companies maintain their market presence.

South America, spearheaded by Brazil's Bebedouro expansion and bolstered by national waste-valorization incentives, is eyeing a 12-14% market share. The region's focus on utilizing agricultural waste for pectin production has significantly reduced raw material dependency. Furthermore, government policies promoting sustainable practices are attracting investments in the sector. In contrast, the Middle East and Africa are targeting an 8-10% stake, with a notable trend: halal pectin capsules are gaining traction in the pharmaceutical sector, increasingly overshadowing traditional gelatin. Rising consumer awareness about halal-certified products is driving this shift, particularly in countries with significant Muslim populations. Additionally, the growing pharmaceutical industry in the region is creating new opportunities for pectin-based products.

Competitive Landscape

The citrus pectin market shows moderate consolidation. Tate & Lyle's acquisition of CP Kelco for USD 1.8 billion has crafted a diverse multi-hydrocolloid portfolio. This portfolio is strategically positioned to penetrate dairy and bakery systems, with an anticipated revenue synergy pipeline of USD 60 million by late 2025. The acquisition aligns with Tate & Lyle's broader strategy to expand its specialty food ingredients business. Additionally, it strengthens the company's ability to meet evolving consumer demand for functional, clean-label products.

DSM-Firmenich's acquisition of a 90.5% stake in Yantai Andre not only secures a foothold in the Asian supply chain but also tightens its grip on organic feedstock. This move enhances DSM-Firmenich's ability to ensure a stable supply of raw materials critical for pectin production. Furthermore, it positions the company to capitalize on the growing demand for organic and sustainably sourced ingredients in the region.Meanwhile, Cargill's plant in Bebedouro, Brazil, has ramped up its output capacity by 50% through energy-efficient microwave extraction, bolstering its presence in the citrus pectin arena. This technological advancement not only reduces energy consumption but also improves the overall efficiency of the production process. By increasing capacity, Cargill is better equipped to meet the rising global demand for citrus pectin across various applications.

Emerging players like Pectin 360 from Australia, backed by government grants, are championing zero-waste manufacturing, positioning themselves as sustainability frontrunners against established giants. Their innovative approach aligns with global sustainability goals, appealing to environmentally conscious consumers and businesses. Additionally, their government-backed initiatives provide them with a competitive edge in terms of funding and market entry support.While precision-fermentation hydrocolloids have achieved cost parity, putting pressure on commodity-grade pectin, they fall short of the coveted "natural" label. This limitation creates an opportunity for established players to differentiate their products through unique value propositions. By emphasizing prebiotic benefits and securing medical-grade certifications, incumbents can strengthen their market position and appeal to health-focused consumers.

Citrus Pectin Industry Leaders

-

Cargill Inc.

-

International Flavors & Fragrances Inc.

-

DSM-Firmenich

-

Tate & Lyle PLC

-

H&F Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Through the acquisition of an additional 15.5% stake, DSM-Firmenich has boosted its ownership in Yantai DSM Andre Pectin Company Limited from 75% to 90.5%. This strategic move bolsters its foothold in the specialty food ingredient market. Meanwhile, Rich Spring Holdings Limited holds onto a 9.5% stake in Andre Pectin, a prominent producer of apple and citrus pectin.

- March 2025: In India, Cargill unveiled a cost-effective pectin substitute tailored for gummies and jellies, catering to price-sensitive consumers. Alongside this innovation, the company showcased bake-stable fillings and functional blends, underscoring its commitment to delivering solutions for food manufacturers.

- November 2024: With the acquisition of CP Kelco, Tate & Lyle has bolstered its position, emerging as a dominant player in the global specialty food and beverage solutions arena, particularly in natural ingredients like pectin and specialty gums.

Global Citrus Pectin Market Report Scope

Pectin is a polysaccharide starch. It is an amorphous, white, colloidal carbohydrate of high molecular weight found in the cell walls of citrus-based fruits and vegetables. By source, the market is segmented into orange, lemon, lime, and grapefruit, and other sources. Based on the type, the market is segmented into high methoxyl pectin and low methoxyl pectin. By category, the market is segmented into conventional and organic/natural. By application, the market is segmented into food and beverages, beauty and personal care, pharmaceuticals, and other applications. Also, the report offers a detailed analysis of major economies across North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Orange |

| Lemon |

| Lime and Grapefruit |

| Other Sources |

| High Methoxyl Pectin |

| Low Methoxyl Pectin |

| Conventional |

| Organic/Natural |

| Food and Beverages | Jam, Jelly and Preserve |

| Baked Goods | |

| Dairy Products | |

| Other Foods and Beverages | |

| Beauty and Personal Care | |

| Pharmaceuticals | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Orange | |

| Lemon | ||

| Lime and Grapefruit | ||

| Other Sources | ||

| By Type | High Methoxyl Pectin | |

| Low Methoxyl Pectin | ||

| By Category | Conventional | |

| Organic/Natural | ||

| By Application | Food and Beverages | Jam, Jelly and Preserve |

| Baked Goods | ||

| Dairy Products | ||

| Other Foods and Beverages | ||

| Beauty and Personal Care | ||

| Pharmaceuticals | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the citrus pectin market be by 2031?

The citrus pectin market size is forecast to reach USD 1.30 billion by 2031, expanding at a 6.05% CAGR from 2026-2031

Which region is growing fastest in citrus pectin demand?

Asia-Pacific leads with a projected 7.03% CAGR as China and India adopt clean-label and plant-based products on a wider scale

What segment holds the highest citrus pectin market share?

High-methoxyl grades retained 58.35% of 2025 revenue, driven by traditional jam and jelly applications.

Which region shows the fastest demand growth?

Asia-Pacific is forecast to expand at 6.29% CAGR through 2030, supported by rising processed-food consumption and expanding citrus harvests.

Why is low-methoxyl pectin gaining popularity?

Low-methoxyl variants enable sugar-reduced and vegan formulations, aligning with global health mandates and supporting a 6.42% CAGR through 2031

Page last updated on: