Citrus Flavors Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 7.10 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

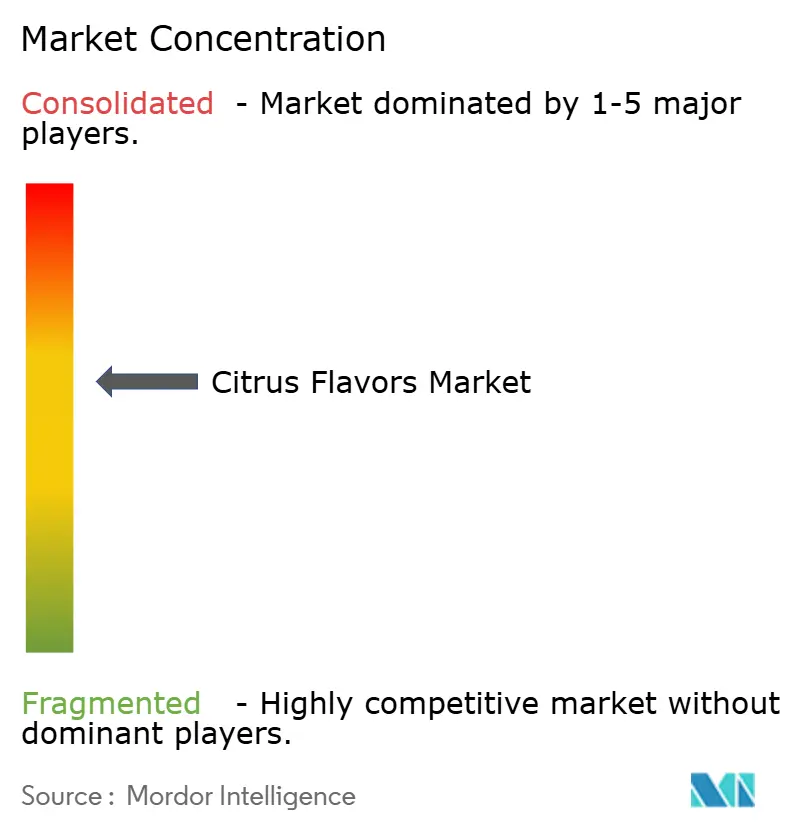

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Citrus Flavors Market Analysis by Mordor Intelligence

The citrus flavors market reached USD 5.10 billion in 2025, valued at USD 5.39 billion in 2026, and is forecast to expand to USD 7.10 billion by 2031, registering a CAGR of 5.67% from 2026 to 2031. This growth reflects a structural shift toward natural formulations rather than simple volume expansion. Regulatory pressures, such as the U.S. Food and Drug Administration's 21 CFR 101.22 labeling mandates and the European Union's Regulation 2025/1112 on natural flavor authentication, are driving manufacturers to invest in traceable, clean-label supply chains[1]Source: European Union, “Regulation ( EU ) 2025/1112,” eur-lex.europa.eu. While orange maintains cost leadership, lime’s sharper acidity aligns with low-sugar beverage reformulations, making it the fastest-growing flavor across functional drinks and savory seasonings. In North America, growth is driven less by population scale and more by vertically integrated supply chains that connect Florida and California growers to flavor houses through cold-press extraction hubs. Meanwhile, the Asia-Pacific region is expected to grow the fastest, as DSM-Firmenich and Givaudan establish new plants in India and Indonesia, reducing lead times for yuzu- and calamansi-based product launches.

Key Report Takeaways

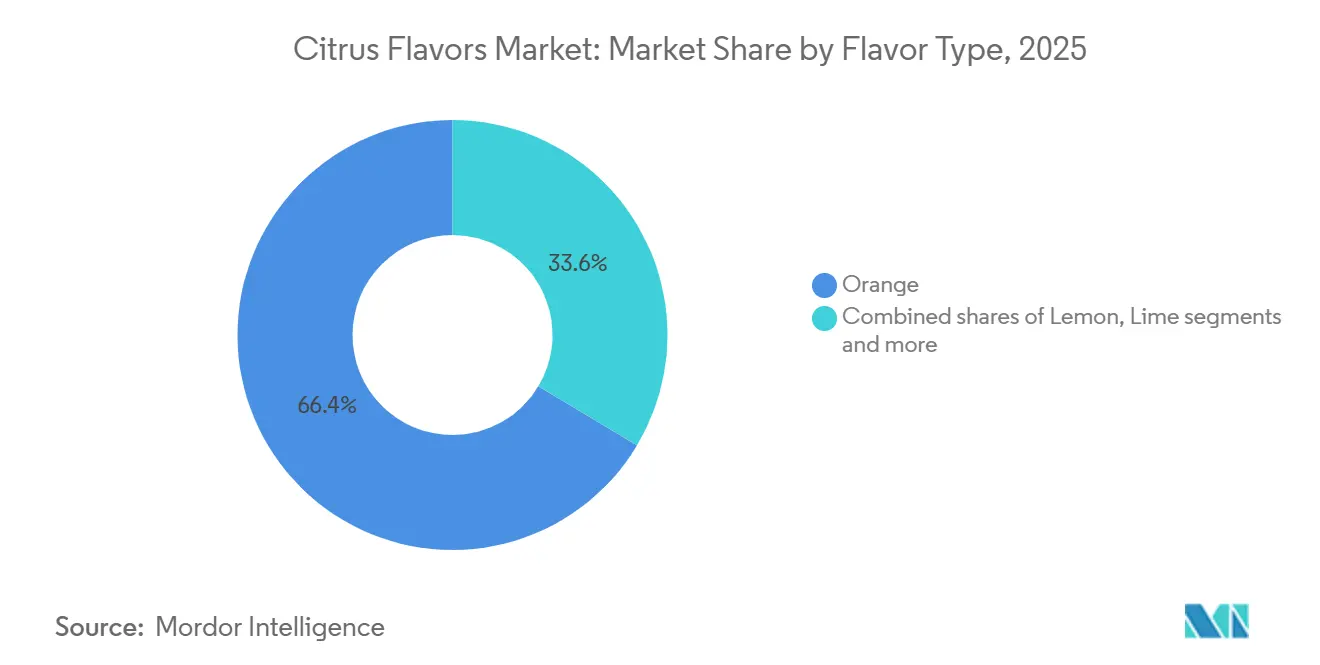

- By flavor type, orange led with 66.43% of the citrus flavors market share in 2025, while lime is projected to expand at a 5.58% CAGR through 2031.

- By nature, natural flavors accounted for 70.05% of the citrus flavors market in 2025 and are projected to rise at a 5.17% CAGR to 2031.

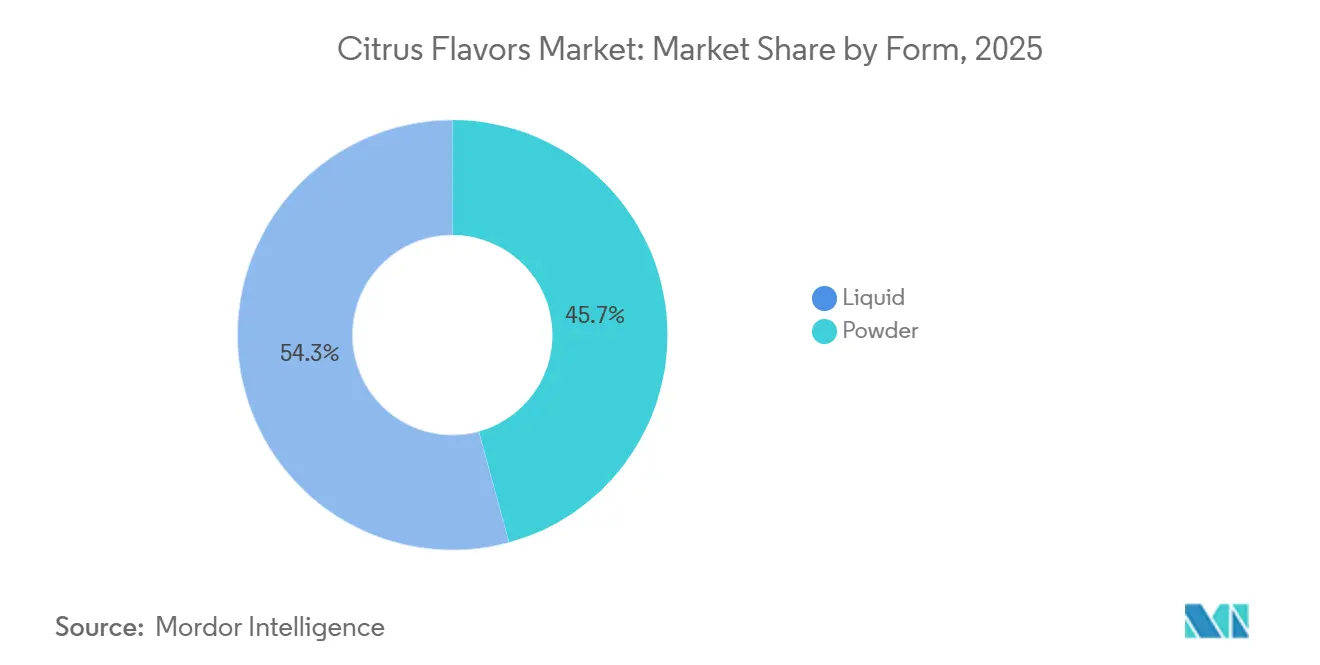

- By form, liquids held 54.26% in 2025, whereas powders are set to register the highest CAGR of 5.06% through 2031.

- By application, beverages accounted for 56.08% in 2025, yet savory and snacks will advance at a 5.29% CAGR during 2026-2031.

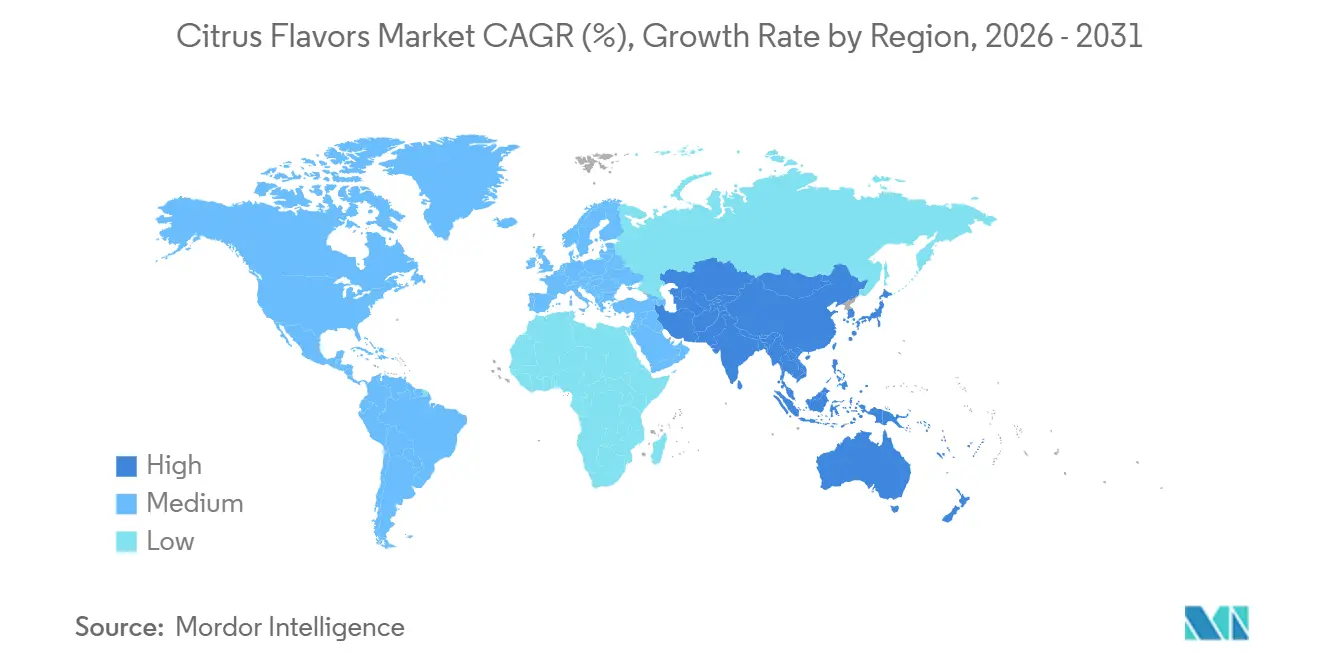

- By geography, North America commanded 38.41% in 2025, while the Asia-Pacific is forecast to post the fastest 5.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Citrus Flavors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label ingredients in food and beverages | +1.2% | Global, with North America and Europe leading regulatory enforcement | Medium term (2-4 years) |

| Demand for fresh, tangy, and refreshing flavor profiles | +0.9% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Growth of functional and fortified beverages | +1.1% | North America, Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Rising popularity of exotic citrus varieties | +0.7% | Asia-Pacific origin, expanding to North America and Europe | Long term (≥ 4 years) |

| Increasing use of citrus flavors in personal care and pharmaceuticals | +0.6% | Europe and North America, with regulatory spillover to Asia-Pacific | Long term (≥ 4 years) |

| Advancements in flavor extraction and formulation technologies | +0.8% | Global, with R&D concentrated in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and clean-label ingredients in food and beverages

Consumer distrust of synthetic additives has elevated natural citrus flavors from a premium option to a baseline expectation, particularly in North America and Europe. Consumers are increasingly checking ingredient lists and preferring products that feel simple, familiar, and less processed. This has made natural citrus flavors more attractive because they can deliver a recognizable fruit profile while fitting clean-label positioning. Food and beverage manufacturers are responding by reformulating products with natural flavor solutions and reducing reliance on artificial additives. Citrus flavors benefit from this shift because they support both taste and marketing claims around freshness, authenticity, and better-for-you products. Brands are responding by shortening ingredient decks: Coca-Cola's reformulated Sprite variants across ASEAN markets in 2025 replaced artificial lemon-lime flavor with natural citrus extracts, a shift that required partnerships with regional suppliers to secure non-GMO certification. Additionally, the rising demand for organic and sustainably sourced ingredients has further propelled the adoption of natural citrus flavors.

Demand for fresh, tangy, and refreshing flavor profiles

Citrus flavors are widely associated with brightness, freshness, and a crisp taste experience, making them highly sought after in beverages, confectionery, dairy, and snacks. Brands increasingly aim to create an uplifting, refreshing sensory appeal, aligning with changing consumer lifestyles that favor lighter, more invigorating flavors. Citrus notes such as lemon, lime, orange, and grapefruit are particularly versatile, adding a vibrant, modern touch to a wide range of products. The shift toward tangy, low-sugar profiles is reshaping the citrus flavor landscape, with lime and grapefruit gaining prominence over sweeter orange variants in beverage applications. For instance, Siggi's introduced a yuzu-flavored skyr in March 2025, leveraging the Japanese citrus's tart profile to stand out in the competitive high-protein dairy segment and appeal to home bakers seeking bakery-quality tang. The growing popularity of citrus-based hard seltzers further underscores this trend, with brands like White Claw and Truly expanding lime and grapefruit SKUs, which are outperforming traditional orange offerings.

Growth of functional and fortified beverages

The functional beverage category is growing as consumers increasingly seek drinks that provide hydration, immune support, energy, and overall wellness benefits. Citrus flavors naturally align with this trend due to their strong association with health, vitality, and vitamin C. These flavors are frequently used to mask the bitterness of active ingredients in functional beverages while enhancing the overall taste profile. As a result, citrus flavors have become a preferred choice for sports drinks, immunity-boosting beverages, electrolyte products, and nutritional shots. Additionally, vitamin C fortification presents a synergistic opportunity, as orange and acerola cherry extracts contribute both ascorbic acid and authentic citrus notes. This allows brands to simplify ingredient labels by eliminating standalone vitamin additives. Advancements in encapsulation technology have further supported this trend. For instance, spray-dried citrus powders with maltodextrin carriers enable gradual flavor release during consumption, extending sensory impact and justifying premium pricing in the sports nutrition market.

Rising popularity of exotic citrus varieties

Yuzu, finger lime, calamansi, and blood orange have evolved from chef-driven novelties to mainstream ingredients, a shift fueled by social media's promotion of visually distinctive products and consumers' willingness to pay 20-30% premiums for perceived authenticity. Australian finger lime exports to North America increased by 140% between 2023 and 2025, driven by demand from craft cocktail bars and premium ice cream brands that utilize the fruit's caviar-like vesicles for both flavor and texture[2]Source: Australian Bureau of Statistics, "Agricultural Production Statistics," abs.gov.au. Calamansi, native to the Philippines, has gained popularity in Southeast Asian beverage markets, where its lime-mandarin hybrid profile aligns with local taste preferences. However, supply-side challenges persist: yuzu cultivation outside Japan remains limited due to slow tree maturation (5-7 years to first harvest) and vulnerability to citrus greening, restricting annual global output to approximately 25,000 metric tons and keeping wholesale prices three times those of conventional lemons. Flavor houses are addressing these challenges through advancements in biotechnology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing risks of adulteration and authenticity | -0.4% | Global, with enforcement gaps in Asia-Pacific and South America | Short term (≤ 2 years) |

| Strict food safety and labeling regulations | -0.3% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Seasonal supply fluctuations and price volatility in citrus crops | -0.5% | Global, acute in Florida, Spain, and Brazil | Short term (≤ 2 years) |

| Oxidation/stability challenges in high-acid matrices | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict food safety and labeling regulations

The FDA's and the EU's regulations impose analytical burdens that disproportionately affect mid-tier suppliers lacking in-house mass spectrometry and isotopic ratio analysis capabilities, effectively raising barriers to entry and consolidating market share among vertically integrated majors. The European Food Safety Authority's 2025 guidance requires documentation of every processing step, from harvest to distillation, to substantiate "natural" claims, a standard that has forced smaller European flavor houses to either invest in lab upgrades or exit the natural segment entirely. Allergen labeling for citral (above 0.001% in leave-on cosmetics per EU Regulation 1223/2009) and limonene (above 0.01% in rinse-off products) has fragmented product portfolios, with brands reformulating or discontinuing SKUs rather than navigating complex disclosure requirements. Paradoxically, stringent rules may benefit the sector in the long term by eliminating low-quality competitors and restoring consumer trust, yet the near-term effect is margin compression and delayed product launches as formulations undergo iterative testing to meet evolving standards.

Seasonal supply fluctuations and price volatility in citrus crops

Citrus production faces significant challenges due to hurricanes, frost, and disease, leading to price volatility that disrupts long-term supply contracts. This forces flavor houses to maintain 6-9 months of inventory, increasing working capital requirements and spoilage risks. In the 2024-25 season, Florida's citrus harvest dropped to 15.85 million boxes, a 29% decline from the previous year and the lowest since 1936, driving U.S. orange juice futures to USD 4.12 per pound by December 2024[3]Source: United States Department of Agriculture, "CITRUS - USDA NASS," nass.usda.gov. Similarly, Spain's 2024 citrus output fell by 10.7% to 5.6 million metric tons, a 16-year low, due to drought and heat stress, tightening European supply and raising spot prices for lemon oil. Additionally, citrus greening disease (Huanglongbing) has infected 90% of Florida's trees, with no commercial cure available. This has prompted a structural shift toward sourcing from Brazil and South Africa, where disease pressure is comparatively lower. While forward contracts and futures hedging help mitigate some volatility, smaller flavor houses often lack the financial tools to manage these risks effectively, leaving them vulnerable to spot-market price spikes that can significantly impact quarterly margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor Type: Orange Dominance Masks Lime's Velocity

Orange flavors dominate the market with a substantial 66.43% share in 2025, reflecting decades of supply-chain optimization around Florida, Brazil, and Spain, where cold-press infrastructure and co-product economics (juice, oil, peel) create cost advantages that newer varieties cannot match. The versatility of orange flavor across multiple applications, including beverages, confectionery, bakery, and dairy, further strengthens its market position. Its natural sweetness and widespread consumer acceptance make it a preferred choice for manufacturers aiming to cater to both health-conscious and indulgent segments.

Lime flavors are advancing at a 5.58% CAGR through 2031, as manufacturers incorporate these flavors into premium product formulations to meet evolving consumer preferences. Brands are reformulating lemonades and seltzers to reduce sugar content, relying on lime's sharper acidity to maintain flavor intensity without sweetness. Lime's supply is more geographically dispersed in Mexico, India, and Egypt, collectively producing 8 million metric tons annually, reducing single-origin risk and stabilizing prices, a structural advantage that supports its faster growth trajectory. Grapefruit's resurgence in craft cocktails and functional waters, driven by its naringin content, which modulates cytochrome P450 enzymes and enhances drug bioavailability, has prompted flavor houses to invest in debittering technologies. Lemon remains the workhorse in bakery and dairy.

By Nature: Natural's Premium Narrows as Synthetics Improve

The natural citrus flavors commanded a 70.05% share in 2025, growing at a 5.17% CAGR. The natural segment's growth is driven by increasing consumer demand for clean-label products and stringent regulatory frameworks. Regulatory bodies, such as the U.S. FDA's CFR 101.22 and the European Union's Regulation 2025/1112, have emphasized the importance of natural flavor authentication, compelling manufacturers to invest in advanced extraction technologies and traceable supply chains. Additionally, rising awareness of the health benefits of natural citrus flavors, such as their antioxidant properties and vitamin C content, has further fueled their adoption across beverages, confectionery, and functional food applications.

Artificial flavors, once stigmatized, are regaining ground in cost-sensitive applications where sensory parity with natural equivalents has significantly improved. Biotechnology advancements are playing a pivotal role in bridging the gap between natural and artificial flavors, enabling the production of cost-effective, high-quality artificial citrus flavors. These flavors are increasingly being utilized in processed foods, carbonated beverages, and snacks, where cost efficiency and consistent flavor profiles are critical. The artificial segment also benefits from its ability to offer unique and customizable flavor combinations, catering to evolving consumer preferences in niche markets.

By Form: Powder's Stability Edge Drives Catch-Up Growth

Liquid citrus flavors held a 54.26% share in 2025, reflecting their ease of integration into beverage and dairy formulations where homogeneous dispersion is critical. Liquid forms retain dominance in beverages where immediate solubility and clarity are non-negotiable. Advancements in nanoemulsion technology, enabled by high-pressure homogenization, have enabled citrus oils to disperse seamlessly in clear waters, sports drinks, and functional beverages without clouding, addressing a long-standing formulation challenge. Additionally, liquid citrus flavors are increasingly used in ready-to-drink (RTD) cocktails and health-focused beverages, driven by consumer demand for natural and refreshing flavor profiles.

Powder formats are forecast to grow at a 5.06% CAGR, signaling a structural shift toward formats that prioritize shelf-life, cost-efficiency, and logistics over sensory immediacy. Spray-drying techniques, employing carriers such as maltodextrin, gum arabic, or modified starches, encapsulate volatile terpenes in a protective matrix. This process extends shelf-life at ambient temperatures and reduces reliance on the cold chain, making powder formats ideal for regions with limited refrigerated transport infrastructure, such as sub-Saharan Africa and Southeast Asia. Furthermore, powdered citrus flavors are gaining traction in bakery, confectionery, and instant beverage mixes due to their ease of storage, precise dosing, and compatibility with dry formulations.

By Application: Savory Snacks Emerge as Dark Horse

Beverage applications accounted for 56.08% of the market in 2025, driven by growing demand for ready-to-drink teas, lemonades, and functional waters. These products leverage citrus acids to enhance electrolyte absorption and mask bitterness from caffeine or plant-based proteins, catering to health-conscious consumers. The rise of low-sugar and clean-label beverages has further fueled the adoption of citrus flavors, as they provide natural sweetness and tanginess without added sugars or artificial ingredients. Citrus flavors are increasingly used in sparkling water and energy drinks, where their refreshing, invigorating profiles appeal to younger consumers. The growing trend of alcohol-free beverages, such as mocktails and flavored seltzers, has also boosted demand for citrus flavors, as they offer a versatile base for creating complex, appealing taste profiles.

The savory and snacks segment is projected to register the fastest growth, with a 5.29% CAGR during the forecast period. Citrus powders in chip seasonings offer a solution to oxidation challenges associated with liquid extracts while delivering authentic lime-chili or lemon-pepper profiles. These flavors resonate strongly with Gen Z's preference for bold, globally inspired tastes. Furthermore, the use of citrus acids, such as citric and malic acids, provides tanginess without the high sodium content of traditional salt-and-vinegar profiles, aligning with FDA guidelines to reduce sodium intake below 2,300 mg per day. In the bakery and confectionery segment, while growth remains steady, innovation continues with the incorporation of citrus flavors into premium offerings such as artisanal chocolates, fruit-filled pastries, and zesty frostings, appealing to consumers seeking unique and indulgent experiences.

Geography Analysis

North America dominated the market with a 38.41% share in 2025, driven by robust vertically integrated supply chains connecting Florida and California citrus growers to flavor houses through advanced cold-press extraction hubs. The region's growing demand for clean-label products continues to drive innovation in citrus-based flavors. The United States remains the largest contributor, with citrus flavors being widely used in beverages such as sparkling waters, energy drinks, and functional beverages, catering to the increasing health-conscious consumer base. While Canada and Mexico contribute modestly, Mexico's annual lime production of 2.5 million metric tons positions it as a key supplier, especially as Florida grapples with the ongoing citrus greening crisis.

The Asia-Pacific region is expected to register the fastest CAGR of 5.38%, fueled by urbanization, rising disposable incomes, and the commercialization of local citrus varieties such as yuzu, calamansi, and finger lime. China and India, the region's largest markets, exhibit distinct trends. In China, the premiumization of products has driven demand for imported citrus varieties like yuzu and blood orange, particularly in craft cocktails and artisanal desserts. Meanwhile, India's price-sensitive market focuses on lemon and lime for traditional beverages like nimbu pani and masala soda. Additionally, Australia's growing exports of finger lime to North America highlight the increasing global demand for unique citrus flavors.

Europe's stringent regulatory environment has reshaped the market, consolidating share among vertically integrated players while creating barriers for smaller suppliers lacking advanced analytical capabilities. This dynamic has bolstered consumer trust in the region's flavor houses. Germany, the UK, and France lead in functional beverage innovation, leveraging citrus acids to mask bitterness in plant-based proteins and fortified waters. Meanwhile, Italy and Spain focus on traditional applications such as limoncello and orange-infused olive oils, which command premium pricing in export markets. The region's emphasis on sustainability and traceability further enhances its competitive edge in the global market.

Competitive Landscape

The citrus flavors market exhibits a moderately concentrated structure, with major players such as Givaudan, IFF, and Symrise dominating upstream cold-press and supercritical CO₂ extraction capacities. Meanwhile, regional specialists such as Florida Food Products, Citromax, and Treatt maintain a competitive edge through proximity to citrus-growing regions and proprietary debittering processes for grapefruit and lime peel oils. This fragmented market structure creates opportunities for strategic maneuvers. For instance, MCI Miritz's March 2025 acquisition of Florida Worldwide Citrus, for an undisclosed sum, enabled the South Korean conglomerate to secure long-term supply for its Asian beverage clients, bypassing volatile spot markets. This vertical integration strategy highlights a competitive advantage that smaller players often cannot replicate due to capital constraints.

Strategic initiatives in the market are concentrated in three key areas: capacity expansion in high-growth regions, mergers and acquisitions to secure access to raw materials, and technology partnerships to enhance product stability and reduce costs. Examples include Givaudan's facility expansion in Indonesia, SDM-Firmenich's investments in India, and Symrise's collaboration with GEA on advanced spray-drying systems. Additionally, emerging opportunities in biotechnology-derived flavors are gaining traction. Givaudan's 2025 patent filing for fermentation-derived yuzu using engineered yeast strains exemplifies efforts to overcome agricultural bottlenecks while maintaining "natural" status under FDA definitions. If regulatory acceptance solidifies, such innovations could disrupt traditional supply chains.

Technological advancements remain a critical competitive differentiator. Supercritical CO₂ extraction, for example, achieves over 95% limonene purity while eliminating solvent residues, making it highly desirable for pharmaceutical and personal care applications subject to stringent regulatory scrutiny. However, only a limited number of global facilities possess this capability, creating a structural advantage for established players. Furthermore, blockchain-based traceability solutions, such as Givaudan's 2025 collaboration with IBM Food Trust to track Brazilian orange oil from grove to formulation, aim to combat adulteration and enhance transparency. As regulatory compliance costs continue to rise, the competitive landscape is expected to consolidate further, favoring larger, well-capitalized players.

Citrus Flavors Industry Leaders

-

Givaudan SA

-

DSM-Firmenich

-

International Flavors & Fragrances (IFF)

-

Kerry Group plc

-

Symrise AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Unifrutti acquired a 400-hectare farm in Sicily, Italy, specializing in blood orange and mandarin cultivation, investing an estimated EUR 25 million (USD 27 million) to secure direct supply for European premium segments and bypass traditional commodity channels, reducing procurement costs.

- October 2025: DSM-Firmenich completed its Thuravoor, India facility expansion, adding 15,000 square meters of production space and increasing citrus flavor capacity by 30%, targeting the subcontinent's functional beverage and dairy segments with an estimated USD 40 million investment.

- August 2025: DSM-Firmenich broke ground on a new facility in Vadodara, India, with an estimated USD 60 million investment; the plant, operational by Q4 2027, will house supercritical CO₂ extraction lines and serve Asia-Pacific's growing demand for natural citrus flavors.

- March 2025: MCI Miritz completed the acquisition of Florida Worldwide Citrus for an undisclosed sum, positioning the South Korean conglomerate to bypass volatile spot markets and secure long-term citrus oil supply for its Asian beverage clients, with annual procurement volumes estimated at 500-600 metric tons

Global Citrus Flavors Market Report Scope

Citrus flavors are bright, tangy, and aromatic taste profiles derived primarily from the rind (peel) and juice of fruits in the Rutaceae family, including lemons, limes, oranges, grapefruits, and tangerines. They are characterized by a combination of high acidity (citric acid), subtle sweetness, and a zesty, aromatic oil content.

The citrus flavors market is segmented by flavor type, nature, form, application, and geography. Based on flavor type, the market is segmented into orange, lemon, lime, grapefruit, and others. By nature, the market is segmented into natural and artificial. By form, the market has been segmented into liquid and powder. By application, the market is segmented into food and beverage, personal care and cosmetics, pharmaceutical and nutraceutical. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Orange |

| Lemon |

| Lime |

| Grapefruit |

| Others |

| Natural |

| Artificial |

| Liquid |

| Powder |

| Food and Beverage | Bakery and Confectionery |

| Dairy and Frozen Desserts | |

| Beverage | |

| Savory and Snacks | |

| Others | |

| Personal Care and Cosmetics | |

| Pharmaceutical and Nutraceutical | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Flavor Type | Orange | |

| Lemon | ||

| Lime | ||

| Grapefruit | ||

| Others | ||

| By Nature | Natural | |

| Artificial | ||

| By Form | Liquid | |

| Powder | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Dairy and Frozen Desserts | ||

| Beverage | ||

| Savory and Snacks | ||

| Others | ||

| Personal Care and Cosmetics | ||

| Pharmaceutical and Nutraceutical | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global citrus flavors market?

The citrus flavors market size stands at USD 5.39 billion in 2026 and is projected to reach USD 7.10 billion by 2031 according to Mordor Intelligence.

Which flavor type holds the largest share?

Orange accounted for 66.43% of citrus flavors market share in 2025, driven by entrenched juice-oil co-product economics.

Which region will grow the fastest between 2026 and 2031?

Asia-Pacific is forecast to record the quickest 5.38% CAGR on the back of new capacity in India and Indonesia.

Why are citrus powders gaining popularity?

Spray-dried powders offer 18-24-month shelf life, enabling distribution in hot climates and driving a 5.06% CAGR for the format.

What technological advances are shaping the market?

Supercritical CO₂ extraction and advanced spray drying enable higher flavor retention and cleaner labels, supporting the rapid growth of powder formats.

Page last updated on: