Citrus Lime Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

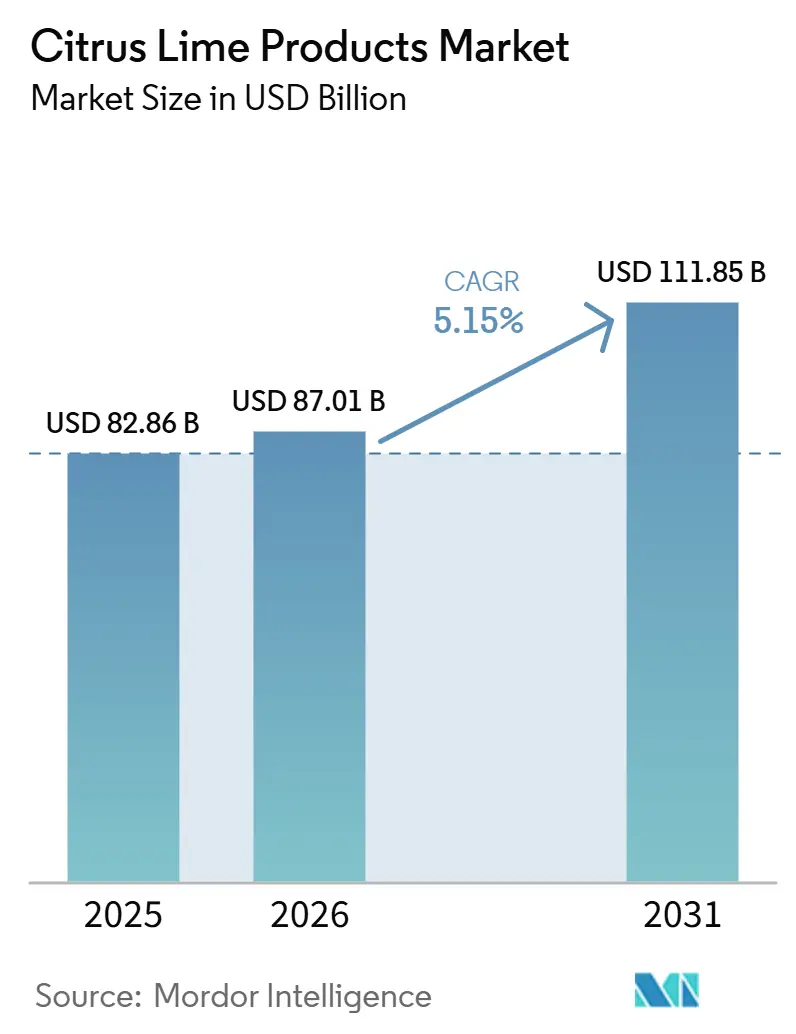

| Market Size (2026) | USD 87.01 Billion |

| Market Size (2031) | USD 111.85 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Citrus Lime Products Market Analysis by Mordor Intelligence

The citrus lime products market size is projected to be USD 82.86 billion in 2025, USD 87.01 billion in 2026, and reach USD 111.85 billion by 2031, growing at a CAGR of 5.15% from 2026 to 2031. The forecast reflects steady demand across beverages, concentrates, essential oils, and processed formats that serve both consumer and industrial use cases. Lime products remain relevant across carbonated mixers, ready to drink cocktails, nutraceutical formulations, and flavor systems, which helps the citrus lime products market absorb weakness in any single channel. The role of lime as a functional ingredient with a recognized nutritional profile is also supporting premium positioning in several application areas. Competition remains fragmented because branded beverage companies, ingredient specialists, and commodity-linked processors compete through different capabilities rather than through one common model. Supply concentration in Mexico still matters because heavy dependence on one origin can transmit cost pressure into downstream categories even when end demand stays firm.

Key Report Takeaways

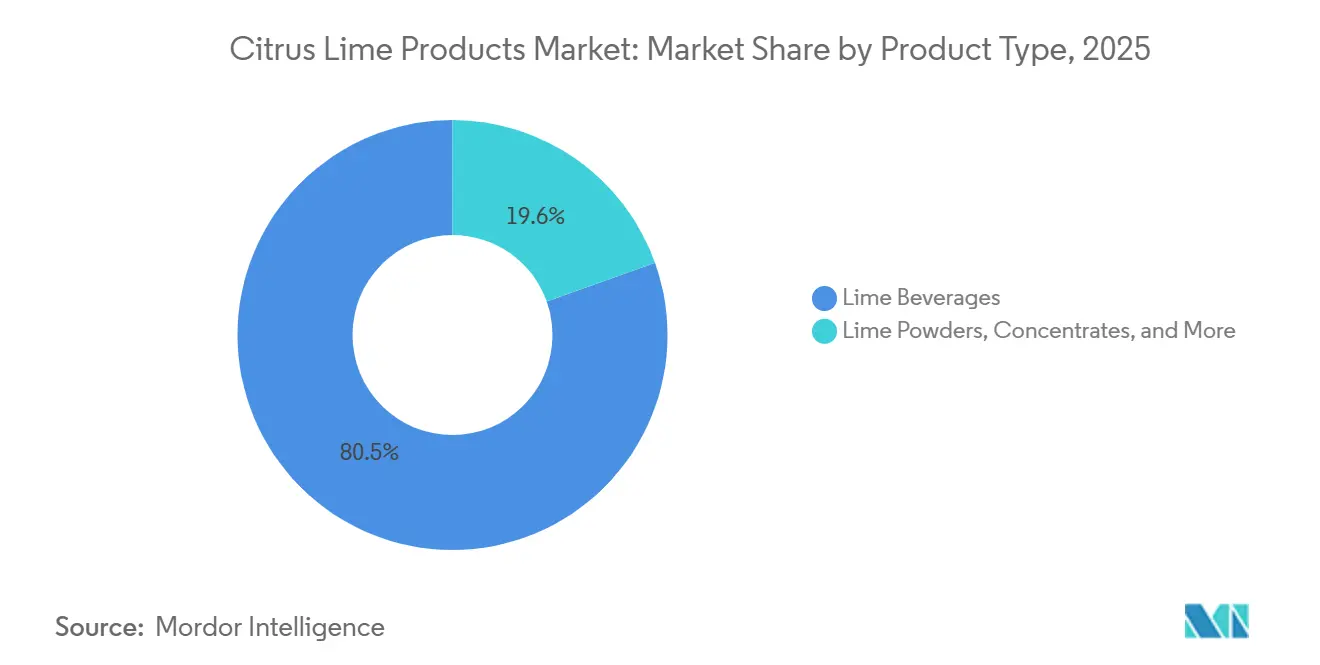

- By product type, lime beverages held 80.45% of the citrus lime products market share in 2025, while lime concentrates are forecast to expand at a 6.92% CAGR through 2031.

- By packaging type, PET or Glass Bottles accounted for a 65.49% share of the citrus lime products market size in 2025, while cans recorded the highest projected CAGR at 6.32% through 2031.

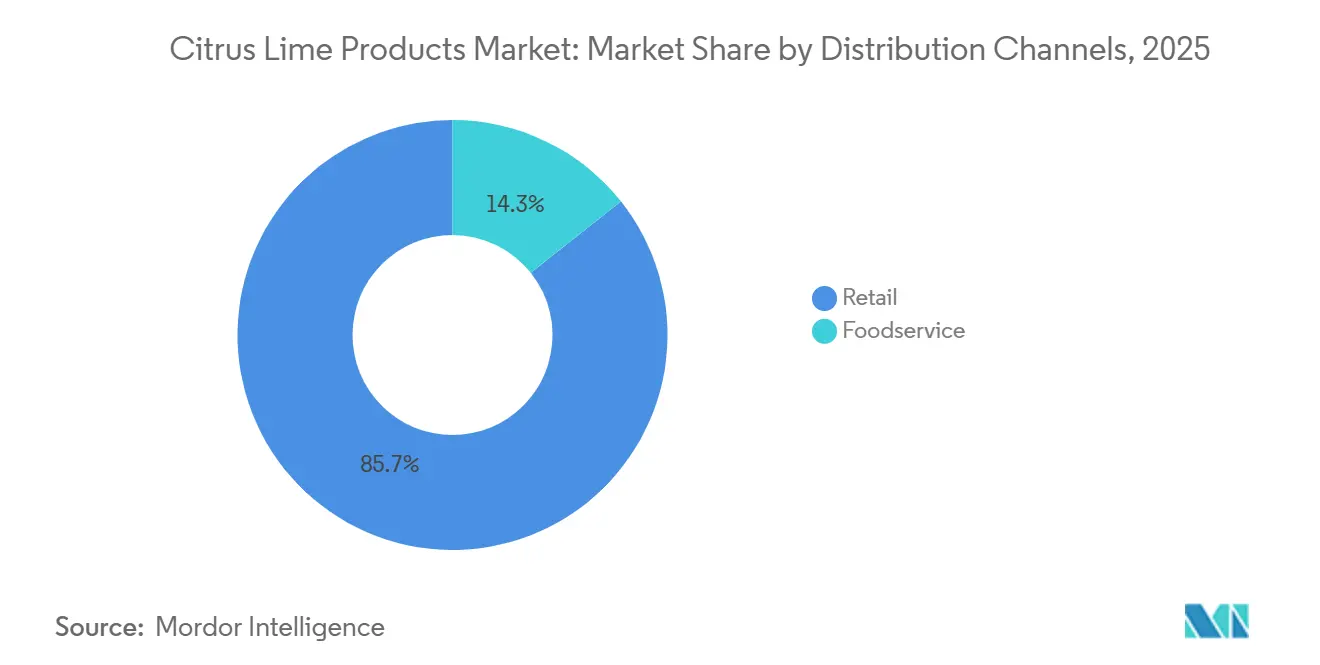

- By distribution channel, retail held 85.68% of revenue in 2025, while foodservice recorded the highest projected CAGR at 6.66% through 2031.

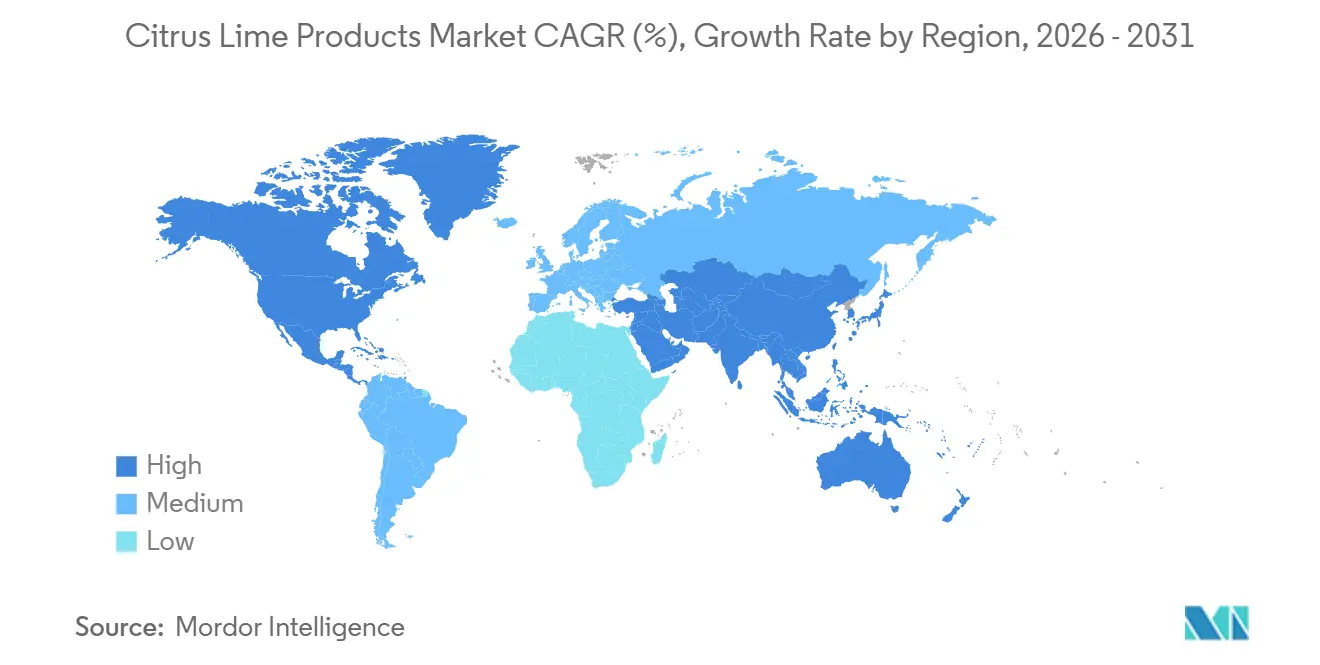

- By geography, Asia-Pacific accounted for a 38.32% share of the citrus lime products market size in 2025, while Europe is forecast to expand at a 6.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Citrus Lime Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand For Fresh And Natural Drinks | +0.8% | Global, with concentrated impact in North America, Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Growing Popularity Of Health-Oriented Drinks | +0.7% | Global; particularly pronounced in Gen Z-heavy markets in North America, Europe, and Southeast Asia | Long term (≥ 4 years) |

| Increasing Use Of Lime In Culinary Applications Across Households And Foodservice | +0.5% | North America, Latin America; spill-over into Western Europe and Southeast Asia | Short term (≤ 2 years) |

| Strong Association Of Lime With Vitamin C And Immunity Benefits | +0.5% | Global; highest in emerging markets including India, Brazil, and MEA | Long term (≥ 4 years) |

| Rising Preference For Clean-Label And Minimally Processed Products | +0.6% | North America and EU core; expanding rapidly in APAC premium retail | Medium term (2–4 years) |

| Product Innovation In Juice Concentrates, Powders, Cordials, And Extracts | +0.7% | Global, with early gains in Europe, North America, and export-oriented Southeast Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand For Fresh And Natural Drinks

Consumer demand is increasingly shifting toward citrus products that deliver a taste and sensory profile closer to fresh fruit, while interest in heavily artificial citrus profiles continues to weaken. This shift is raising quality expectations for not-from-concentrate juices, fresh-squeezed bar programs, and other formats that rely on transparent ingredient recognition and a clear connection to natural citrus inputs. In October 2024, Döhler Group and FGF Trapani announced a joint venture to develop citrus fiber solutions processed directly from fresh citrus peels, underscoring how suppliers are adapting product development strategies to support natural, minimally processed, and recognizable ingredient positioning. This demand pattern is enabling premium formats to protect and capture value more effectively than lower-priced citrus drinks that compete primarily on flavor intensity, discounting, and promotional activity. As a result, the citrus lime products market is generating stronger value capture across premium beverages, concentrates, and ingredient systems than headline volume growth alone suggests.

Growing Popularity Of Health-Oriented Drinks

Health-oriented beverage demand is widening the role of lime beyond refreshment and into functional consumption occasions. Lime concentrates are increasingly suitable for hydration products, immunity-positioned drinks, and adjacent wellness formats because they offer consistent acidity, flavor intensity, and easier formulation than fresh fruit. The April 2026 launch of GHOST Energy x 7UP Lemon Lime shows that citrus lime flavor is also moving into the functional energy segment through established distribution networks. This creates a more diversified demand base for processors and ingredient suppliers that serve beverage companies rather than only retail shelf products. The citrus lime products market is therefore gaining from category expansion as much as from repeat demand in traditional beverage lines.

Product Innovation In Juice Concentrates, Powders, Cordials, And Extracts

Innovation in the ingredient tier is expanding well beyond basic flavor reformulation, as suppliers increasingly focus on functionality, sustainability, and higher-value applications. The October 2024 joint venture between Döhler and FGF Trapani, which focuses on citrus fiber solutions made from fresh citrus peels, underscores the growing industry emphasis on by-product utilization, waste reduction, and the creation of new ingredient revenue streams. The June 2026 sanctioned acquisition of Treatt plc by Döhler would further indicate that citrus oils and flavor capabilities are becoming more strategic within global ingredient platforms, particularly as manufacturers seek differentiated, natural, and traceable citrus-based inputs. These developments are important because they support the repositioning of lime concentrates and extracts from largely commodity-based products to specialty ingredients with broader application potential. As a result, the citrus lime products market should continue to favor suppliers that can deliver consistent process control, authentic flavor profiles, reliable quality, and traceable sourcing.

Strong Association Of Lime With Vitamin C And Immunity Benefits

Lime continues to benefit from consumers’ strong association of the fruit with vitamin C, freshness, and everyday immunity support. This perception is strengthening its value proposition across product formats where manufacturers position lime as more than a basic flavor note. It supports premium price points in applications that emphasize functional benefits, natural ingredients, and health-oriented consumption occasions. It also drives demand for lime concentrates, extracts, and essential oils, which formulators use in wellness-oriented beverages, dietary supplements, functional foods, and other health-focused products. This trend is expanding the commercial role of lime products across pharmacy-linked, nutraceutical, and specialty health channels in several emerging markets, where consumers increasingly seek convenient products aligned with preventive health and immune support. In the citrus lime products market, this broader positioning helps extend revenue potential beyond mainstream grocery and conventional soft drinks while creating additional opportunities in higher-value health and wellness applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal Supply Fluctuations Affecting Raw Material Availability | -0.7% | North America (Mexico supply dependency), South America, and EU (Brazil supply exposure) | Short term (≤ 2 years) |

| Availability Of Substitute Citrus Flavors Such As Orange, Grapefruit, And Others | -0.5% | Global; competition most intense in carbonated soft drink and juice categories in mature markets | Long term (≥ 4 years) |

| Short Shelf Life Of Fresh Lime Products | -0.4% | Asia-Pacific and MEA (infrastructure-constrained markets); less relevant for concentrate sub-segment | Medium term (2–4 years) |

| Price Volatility In Fresh Lime And Processed Lime Inputs | -0.6% | North America (key lime pricing), Latin America, EU (Tahiti lime from Brazil) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Seasonal Supply Fluctuations Affecting Raw Material Availability

Mexico accounted for more than 88.70% of U.S. lime import volumes in 2024, while Colombia held 8.40%, which shows how concentrated North American sourcing remains[1]Source: International Fresh Produce Association, “U.S. Limes Market Annual Report,” International Fresh Produce Association, freshproduce.com. USDA GAIN reported that wholesale key lime prices in Mexico City rose from MXN 27.50 per kg in January 2023 to MXN 50.00 per kg in January 2024 after drought conditions affected major producing states. Brazil also faced weather disruption in 2024, and USDA GAIN noted that average industry lime prices in Q1 2025 were 55.00% higher than in Q1 2024. These shifts create margin pressure for processors that depend heavily on fresh lime inputs and cannot offset the change through scale or flexible sourcing. The citrus lime products market is therefore pushing larger buyers toward origin diversification and tighter procurement planning.

Price Volatility In Fresh Lime And Processed Lime Inputs

Input cost swings remain a direct margin risk across beverages, concentrates, and essential oils. USDA GAIN reported that Brazil’s Tahiti lime prices reached BRL 38.81 per 27-kg box, or USD 6.97, during June 9-12, 2025, driven by drought-related crop losses and strong processing demand[2]Source: United States Department of Agriculture Foreign Agricultural Service, “The Rise of Lime Production in Brazil's Citrus Heartland,” USDA GAIN, fas.usda.gov. When finished product contracts are fixed and raw material costs rise quickly, manufacturers lose the benefit of strong end demand because gross margins compress instead of expanding. Smaller cordial and concentrate producers are more exposed because they often have less balance sheet flexibility and fewer multi-origin sourcing options than large integrated operators. The citrus lime products market is likely to favor processors and traders that can manage volatility through scale, storage, contracting discipline, and broader origin access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Anchor Revenue, Concentrates Drive Value Growth

Lime beverages held 80.45% of the product type market in 2025, which made them the largest product category by a wide margin. This lead reflects strong penetration across alcoholic and non-alcoholic formats, including carbonated drinks, juices, and ready-to-drink cocktails. Lime concentrates are projected to grow at a 6.92% CAGR through 2031, and that makes them the strongest expansion area within the citrus lime products market. Their appeal comes from year-round flavor consistency, easier transport, and the ability to serve beverage manufacturers, foodservice operators, and industrial flavor users through one ingredient format.

Lime powder, essential oils and extracts, and processed lime products remain smaller in value but serve distinct commercial roles. Essential oils carry premium relevance in flavor, fragrance, and personal care applications, while processed lime formats support convenience and portion control in institutional foodservice. USDA GAIN reported that Mexico’s lime volumes allocated for processing rose from 430,000 metric tons in MY 2023/24 to a forecast 500,000 metric tons in MY 2024/25, which expands the raw material base available to ingredient processors. That supply shift supports concentrate and extract output and strengthens the citrus lime products market as processing capacity becomes more aligned with demand growth.

By Packaging Type: Bottles Retain Volume Share, Cans Capture New Consumption Occasions

PET or Glass Bottles held 65.49% of the packaging market in 2025, which reflects their strength across retail juice, cordial, and multi-serve beverage formats. Their range spans value-focused PET packs and premium glass presentations, so the format remains useful across income levels and product positions. Cans are forecast to grow at a 6.32% CAGR through 2031 as ready-to-drink lime beverages, alcoholic mixers, and energy-adjacent products expand. This shift is becoming more visible in the citrus lime products market because cans fit portability, light protection, and strong shelf branding needs.

Crown Holdings noted that aluminum cans are among the fastest-growing beverage packaging formats globally and offer full-surface branding advantages for premium beverage positioning. Britvic’s 2024 preliminary results showed investment in a new can line in Great Britain, a second line ordered for 2025, and a EUR 6 million expansion in Ireland, which signals active infrastructure alignment with canned beverage growth. Bottles should remain the volume base for everyday consumption, but cans are opening new on-the-go, premium, and alcoholic occasions that were less developed before. That balance keeps the citrus lime products market anchored in established pack formats while still allowing mix improvement through faster-growing can lines.

By Distribution Channel: Retail Dominates, Foodservice Closes the Gap

Retail accounted for 85.68% of distribution revenue in 2025, which confirms that lime products remain deeply tied to everyday household buying patterns. Supermarkets, hypermarkets, convenience stores, specialty retailers, and online channels all contribute to that base. Foodservice is forecast to grow at a 6.66% CAGR through 2031, and that makes it the fastest channel within the citrus lime products market. The shift is linked to wider use of standardized lime inputs in bars, restaurants, quick service formats, and premium nonalcoholic beverage programs.

Retail still benefits from staple pantry demand and repeat household usage, especially in beverage mixing and cooking applications. Foodservice, however, often carries higher unit economics because operators pay for convenience, consistency, and stronger presentation outcomes in finished drinks and dishes. This channel also supports use cases that favor fresh juice, syrups, concentrates, and processed portions rather than a single product format. As these operating patterns deepen, the citrus lime products market should see foodservice narrow part of the gap without displacing retail’s core scale advantage.

Geography Analysis

Asia-Pacific held 38.32% of the citrus lime products market share in 2025, which made it the largest regional revenue contributor. The region benefits from the long-standing role of lime in household cooking, street beverages, foodservice menus, and growing packaged drink demand across India, China, Vietnam, Thailand, and Indonesia. India and Vietnam also strengthen the regional position because they contribute to both consumption and processing activity. China adds further demand through expanding modern retail and e-commerce access for bottled and ready-to-drink citrus beverages. India’s April 2025 bilateral agreement with Brazil for Tahiti lime access should also broaden supply options for regional processors over time.

Europe is projected to grow at a 6.79% CAGR through 2031, which makes it the fastest-growing regional block in the citrus lime products market. USDA GAIN reported that the European Union absorbed 76.00% to 80.00% of Brazil’s total lime export volumes, which shows how important the supply corridor already is for the region’s concentrate and ready-to-drink manufacturing base. Product launches such as Absolut Vodka and Sprite across the UK, Germany, Spain, and the Netherlands are helping create new lime-led consumption occasions in canned ready to drink formats[3]Source: Absolut, “Absolut Vodka and Sprite Ready-To-Drink Cocktail Now Available,” Absolut, absolut.com. Premiumization, cocktail culture, and packaging alignment are therefore reinforcing one another in this region.

South America plays a dual role in the citrus lime products market because it is both a major producing base and an increasingly formalized demand center. Brazil’s Tahiti lime production reached 1.72 million metric tons in 2023, and exports rose from 118,866 metric tons in 2020 to 175,837 metric tons in 2024, which shows stronger integration with global ingredient supply chains. Colombia is also gaining relevance, with its share of U.S. lime imports rising from 5.10% to 8.40% in one year, which modestly reduces single-origin dependence in North America. In the Middle East and Africa, urban demand for ready to drink beverage formats is rising, which should support additional use of lime-based flavor systems where cold chain and modern retail continue to expand.

Competitive Landscape

The citrus lime products market has a concentration score of 3 out of 10, which reflects broad fragmentation across branded beverage companies, ingredient specialists, commodity traders, and regional processors. No single participant controls the space in a way that sets pricing or category direction across all product formats. PepsiCo and The Coca-Cola Company remain visible at the branded beverage level through new lime launches and marketing support. Coca-Cola Europacific Partners launched Coca-Cola Lime and Coca-Cola Zero Sugar Lime in Great Britain in January 2025 with a multi-million-pound campaign that included influencer activity, social media, and live experiences. PepsiCo also launched limited-edition Pepsi Lime in the U.S. in April 2024 in 12 oz cans and 20 oz bottles, which reinforced lime as an active seasonal flavor platform for major carbonated soft drink brands.

At the ingredient level, scale and technical capability are becoming more important competitive tools in the citrus lime products market. Döhler’s cash offer for Treatt plc, sanctioned on June 30, 2026, brought citrus and essential oil expertise into a larger integrated ingredient platform. The earlier October 2024 joint venture with FGF Trapani also showed that citrus fibre and peel-based ingredient development is part of the same broader strategic push. These actions suggest that flavor authenticity, processing know-how, and raw material utilization are becoming harder to separate from competitive strength.

The citrus lime products market also has room for growth at the boundary between classic refreshment and functional beverages. Keurig Dr Pepper and GHOST Energy entered that space in April 2026 with GHOST Energy x 7UP Lemon Lime, which brought an established citrus profile into the energy segment through national distribution. Pernod Ricard and The Coca-Cola Company also extended lime-led ready to drink consumption through Absolut Vodka and Sprite in European canned formats. The result is a market where leading companies compete less on scale alone and more on channel reach, application depth, and the ability to turn lime into new product occasions.

Citrus Lime Products Industry Leaders

PepsiCo Inc.

The Coca-Cola Company

Pernod Ricard

The Wonderful Company LLC

Maruti Agro Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Keurig Dr Pepper and GHOST Energy launched GHOST Energy x 7UP Lemon Lime, the first licensed lemon-lime flavour from the KDP portfolio produced in collaboration with GHOST, targeting the high-growth functional energy drink segment through KDP's national distribution network.

- April 2025: Sierra Tequila, part of Stock Spirits Group, entered the ready-to-drink (RTD) category with the launch of its Sierra Margarita range in Lime and Strawberry flavors. Made with original Sierra Tequila, the canned cocktails were introduced to meet growing consumer demand for convenient, premium-quality agave-based RTD beverages and to strengthen the brand's presence in the expanding RTD spirits market.

- January 2025: The Coca-Cola Company reintroduced Coca-Cola Lime and Coca-Cola Zero Sugar Lime in the UK, marking the return of the lime-flavoured variant after nearly two decades. The launch expands the company's flavoured cola portfolio, catering to growing consumer demand for refreshing citrus-infused soft drinks and supporting product innovation within the carbonated beverages segment.

Global Citrus Lime Products Market Report Scope

| Lime Beverages | Alcoholic Beverages | Lime-Infused Spirits |

| Ready-To-Drink Cocktails | ||

| Others | ||

| Non-Alcoholic Beverages | Carbonated Drinks | |

| Sports and Energy Drinks | ||

| Juices | ||

| Others | ||

| Lime Powder | ||

| Lime Concentrates | ||

| Lime Essential Oils and Extracts | ||

| Processed Lime Products (frozen pearls, slices, puree) | ||

| Cans |

| Glass/PET Bottles |

| Others |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Lime Beverages | Alcoholic Beverages | Lime-Infused Spirits |

| Ready-To-Drink Cocktails | |||

| Others | |||

| Non-Alcoholic Beverages | Carbonated Drinks | ||

| Sports and Energy Drinks | |||

| Juices | |||

| Others | |||

| Lime Powder | |||

| Lime Concentrates | |||

| Lime Essential Oils and Extracts | |||

| Processed Lime Products (frozen pearls, slices, puree) | |||

| By Packaging Type | Cans | ||

| Glass/PET Bottles | |||

| Others | |||

| By Distribution Channels | Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | |||

| Specialty Stores | |||

| Online Retail Channels | |||

| Other Distribution Channels | |||

| Foodservice | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Sweden | |||

| Poland | |||

| Belgium | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Indonesia | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current size of citrus lime products in 2026?

The citrus lime products market size stands at USD 87.01 billion in 2026 and is projected to reach USD 111.85 billion by 2031 at a 5.15% CAGR.

Which product category leads revenue generation in this space?

Lime beverages are the largest category, holding 80.45% of product type revenue in 2025, which reflects broad use across alcoholic and non-alcoholic formats.

Which product segment is growing the fastest through 2031?

Lime concentrates are forecast to expand at a 6.92% CAGR through 2031 because they offer flavor consistency, easier transport, and wide application across beverages and foodservice.

Why is Europe the fastest-growing regional area?

Europe is projected to grow at a 6.79% CAGR through 2031 because premium ready to drink formats, cocktail culture, and stable import links with Brazil are strengthening regional demand.

Page last updated on: