Soluble Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

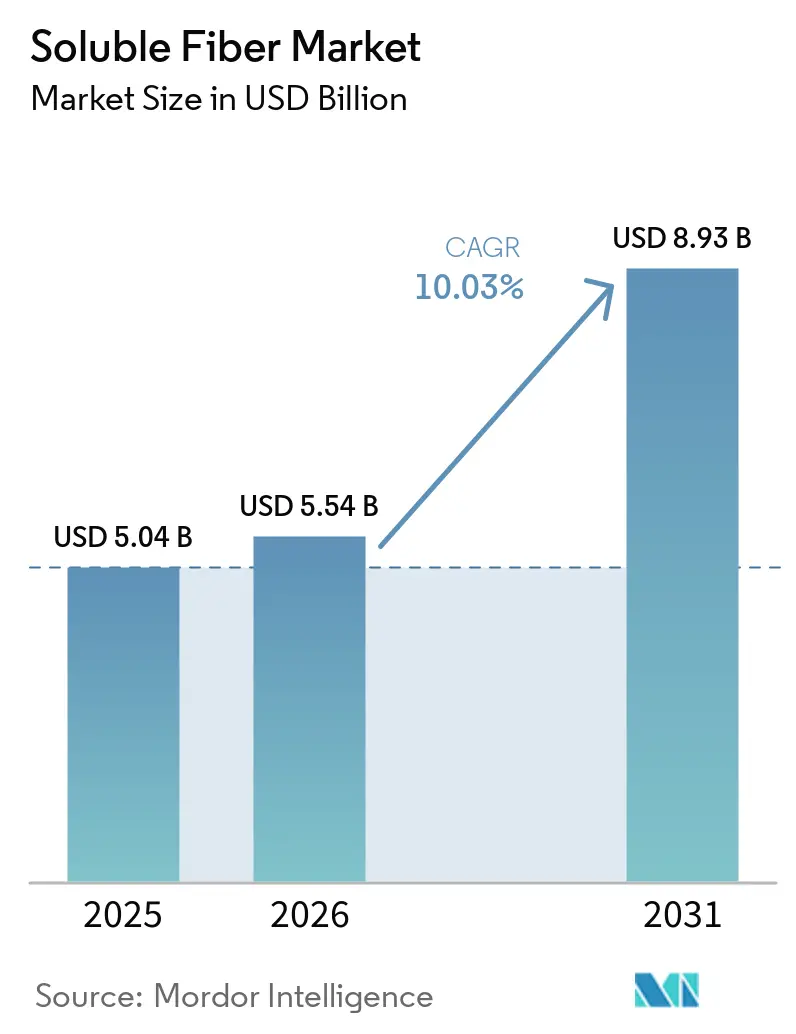

| Market Size (2026) | USD 5.54 Billion |

| Market Size (2031) | USD 8.93 Billion |

| Growth Rate (2026 - 2031) | 10.03% CAGR |

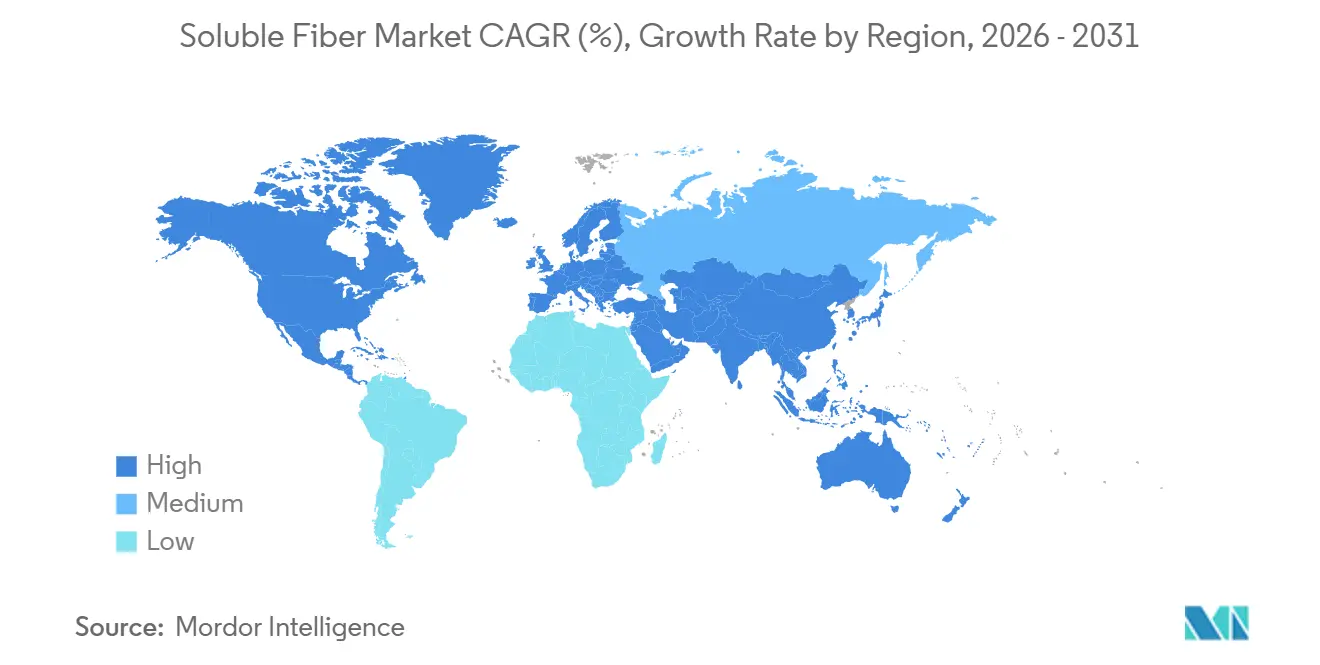

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soluble Fiber Market Analysis by Mordor Intelligence

The soluble fiber market size was valued at USD 5.04 billion in 2025 and estimated to grow from USD 5.54 billion in 2026 to reach USD 8.93 billion by 2031, at a CAGR of 10.03% during the forecast period (2026-2031). Regulatory moves that elevate fiber from a “nice-to-have” to a front-of-pack priority, together with mounting clinical evidence linking select fibers to gut-microbiome health, are reshaping product reformulation agendas across food, beverage, and supplement categories. Brands are no longer adding fiber only for bulk; they now treat it as a multifunctional ingredient that can mask sugar reduction, extend shelf life, and enable disease-risk-reduction claims under both U.S. and European frameworks. Technological advances, such as enzymatic hydrolysis, which yields clear, low-viscosity syrups, allow liquid fibers to be used directly as a substitute for high-fructose corn syrup without altering processing protocols. Finally, personalized-nutrition platforms that pair microbiome sequencing with custom fiber blends are turning a once-commoditized ingredient into a subscription-based wellness solution, anchoring repeat purchase behavior at premium price points.

Key Report Takeaways

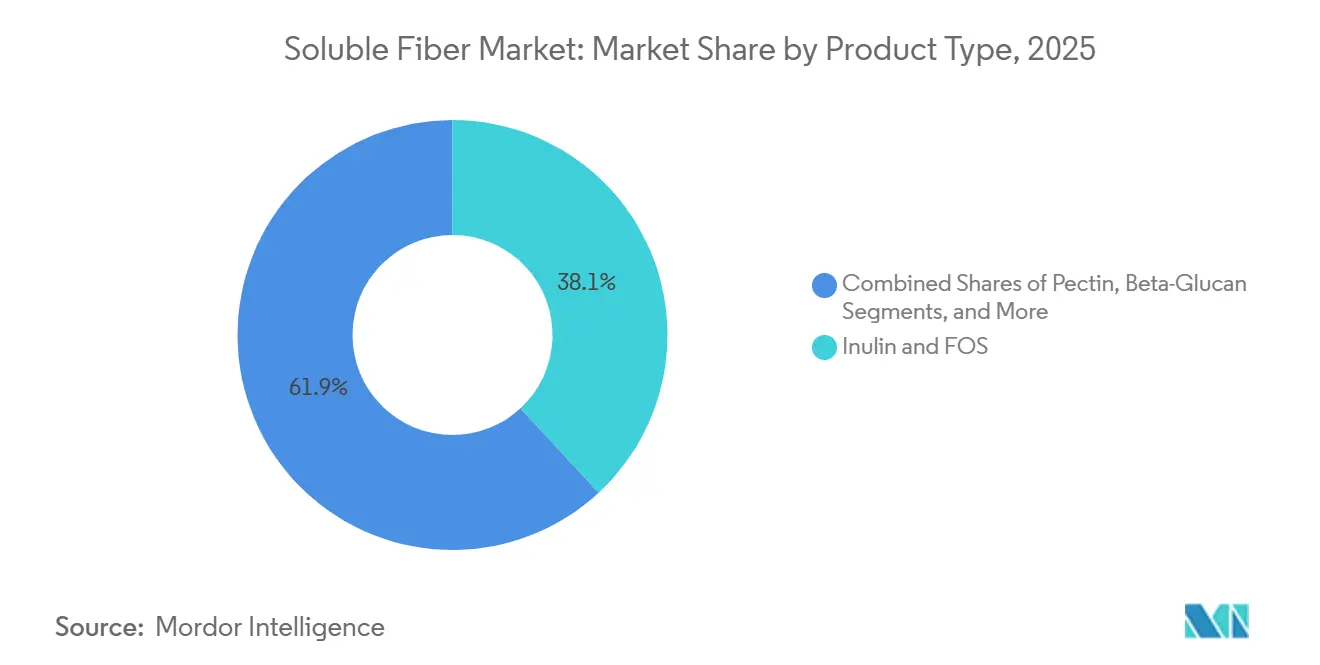

- By type, inulin and fructooligosaccharides commanded 38.05% of the soluble fiber market share in 2025, whereas beta-glucan is expected to expand at an 11.35% CAGR through 2031.

- By source, cereals and grains supplied 45.63% of the soluble fiber market size in 2025, while legumes and nuts are expected to represent the fastest-growing source at a 10.68% CAGR.

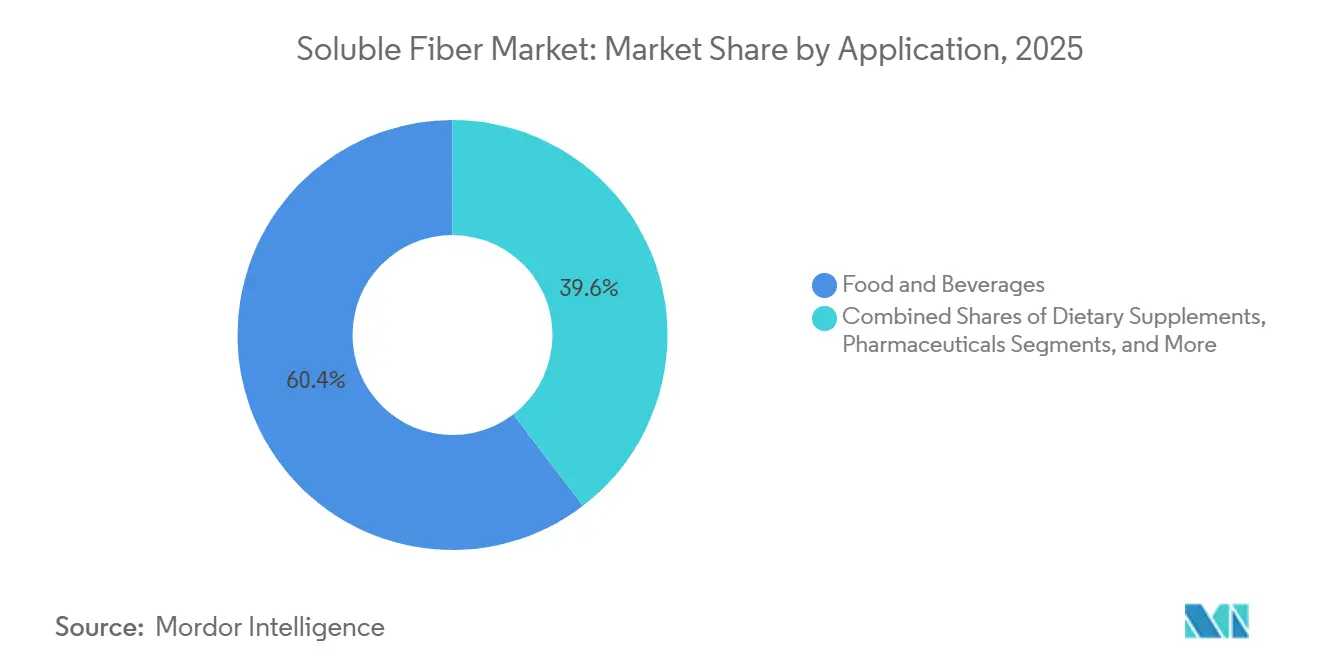

- By application, food and beverages accounted for 60.38% of revenue in 2025; dietary supplements are expected to grow at a 11.18% CAGR through 2031.

- By form, powder variants accounted for 71.82% of sales in 2025, yet liquid and syrup fibers are expected to grow at a 10.45% CAGR.

- By geography, North America accounted for 42.86% of 2025 revenue, while Asia-Pacific is expected to be the fastest-growing region at a 10.94% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soluble Fiber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for prebiotic foods and microbiome-support products | +2.1% | Global, led by APAC and North America | Medium term (2-4 years) |

| Application in sugar-reduction reformulation | +1.8% | North America & Europe core, expanding to Latin America | Short term (≤2 years) |

| Expansion of fiber claims in mainstream packaged foods | +1.5% | Global, accelerated by labeling mandates | Medium term (2-4 years) |

| Increased use in diabetic-friendly products | +1.2% | North America, Europe, urban APAC | Long term (≥4 years) |

| Clean-label replacement of synthetic bulking agents | +1.0% | Europe & North America, spillover to APAC premium segments | Medium term (2-4 years) |

| Demand for satiety support in weight-management formulations | +0.9% | North America & Europe, emerging in Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising demand for prebiotic foods and microbiome-support products

Consumer understanding of the gut-brain axis and short-chain fatty acid production has migrated from niche wellness circles into mainstream purchasing criteria, with prebiotic-labeled products growing 34% in unit sales across United States retail channels in 2025, according to the USDA Economic Research Service[1]Source: USDA Economic Research Service, “Prebiotic Food Market Trends,” ERS.usda.gov. Inulin and fructooligosaccharides selectively feed Bifidobacterium and Lactobacillus species, generating butyrate and propionate that modulate intestinal barrier integrity and systemic markers of inflammation. Clinical trials published in 2025 demonstrated that 10 grams per day of chicory inulin reduced fecal calprotectin by 22% in adults with mild inflammatory bowel symptoms, providing formulators with dose-response data to substantiate structure-function claims under FDA guidelines. Japan's Foods for Specified Health Uses system approved 14 new prebiotic fiber applications in 2025, including beta-glucan from barley at 3 grams per serving for cholesterol management, expanding the regulatory precedent for fiber-based health claims in Asia-Pacific markets, according to the Ministry of Health, Labor and Welfare, Japan[2]Source: Ministry of Health, Labour and Welfare Japan, “FOSHU Approvals,” MHLW.go.jp. Personalized-nutrition platforms now pair microbiome sequencing with fiber-blend recommendations, creating a feedback loop in which consumers validate prebiotic efficacy through follow-up stool testing, which, in turn, drives repeat purchases and brand loyalty.

Application in sugar-reduction reformulation in beverages, dairy, bakery, and snacks

The FDA's 2024 final rule on front-of-pack nutrition labeling requires added-sugar disclosure in both absolute grams and as a percentage of the daily value, making sugar-reduction reformulation a compliance imperative rather than a voluntary marketing strategy[3]Source: U.S. Food and Drug Administration, “Front-of-Pack Nutrition Labeling Final Rule,” FDA.gov . Soluble fibers deliver bulk, mouthfeel, and sweetness-masking without triggering added-sugar penalties, enabling beverage manufacturers to achieve 30-50% sugar reduction while maintaining sensory profiles. Resistant dextrin and soluble corn fiber exhibit neutral taste and high solubility, allowing clear-beverage applications in sports drinks and flavored waters without haze formation or sedimentation. The USDA's 2025 school-meal sodium and sugar limits capped added sugars at 10% of total calories, forcing dairy processors to reformulate chocolate milk with inulin and polydextrose blends that preserve sweetness perception at 40% lower sucrose levels. Bakery applications leverage beta-glucan's water-binding capacity to extend shelf life and reduce staling, delivering dual benefits: reduced sugar intake and improved product economics through lower waste rates.

Increased use in diabetic-friendly products

Beta-glucan's ability to attenuate postprandial glucose spikes by forming viscous gels in the small intestine has positioned it as a cornerstone ingredient in diabetic-friendly formulations. EFSA approved a health claim in 2024 stating that 4 grams of oat or barley beta-glucan per 30 grams of available carbohydrate reduces the post-meal blood glucose rise, providing formulators with precise dosing guidance for substantiating the claim. The American Diabetes Association's 2025 Standards of Medical Care elevated fiber intake recommendations to 30-35 grams per day for adults with type 2 diabetes, creating clinical endorsement for high-fiber product categories. Psyllium husk, though less prevalent than inulin or beta-glucan, demonstrated superior glycemic control in meta-analyses, with 10.5 grams per day reducing HbA1c by 0.97 percentage points over 8 weeks; however, its gritty texture limits its inclusion in beverages and baked goods. Diabetic-friendly product launches grew 28% in 2025, with soluble fibers appearing in meal-replacement shakes, low-glycemic snack bars, and fortified breads, often combined with chromium picolinate or alpha-lipoic acid to amplify insulin-sensitizing effects.

Demand for satiety support in weight-management formulations

Soluble fiber's gastric distension and ghrelin-suppression mechanisms are being leveraged in weight-management products that deliver pharmaceutical-grade efficacy without prescription requirements. Glucomannan, a soluble fiber from konjac root, swells to 50 times its dry weight in the stomach, creating mechanical satiety that reduces ad libitum energy intake by 8-12% in controlled trials. The European Food Safety Authority approved a weight-loss claim for glucomannan in 2024, stating that 3 grams per day, taken in three 1-gram doses before meals, when combined with energy-restricted diets, contributes to weight loss. Meal-replacement shakes incorporate inulin and resistant dextrin at 10-15 grams per serving to extend satiety duration, with consumer testing showing 2.3-hour increases in time-to-next-meal compared to fiber-free controls. The weight-management segment is attracting pharmaceutical companies exploring fiber-drug combinations, with preclinical studies testing inulin co-administration with GLP-1 agonists to amplify satiety signaling and reduce gastrointestinal side effects.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chicory-root and inulin supply concentration | -1.4% | Europe core, ripple to North America and APAC | Short term (≤2 years) |

| Gastrointestinal tolerance limits (bloating, FODMAPs) | -1.1% | Global, high-dose supplements most affected | Medium term (2-4 years) |

| Regulatory tightening on fiber definition & claims | -0.8% | Europe & North America, emerging in APAC | Long term (≥4 years) |

| Competition from alternative functional ingredients | -0.7% | Global, varies by category | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chicory-root and inulin supply concentration causing raw-material volatility

Belgium and the Netherlands cultivate approximately 12,000 hectares of chicory root combined, representing 65% of the global inulin-grade chicory supply, creating a geographic bottleneck that amplifies weather-related yield shocks at Cosucra. The 2024 growing season experienced 18% below-average rainfall during root-bulking phases, reducing per-hectare yields from 45 tonnes to 37 tonnes and tightening inulin spot prices by 23% year-over-year. Chile's 3,000 hectares of chicory cultivation provide counter-seasonal supply, yet logistical costs and lower fructan content (14-16% versus 18-20% in European roots) limit its ability to stabilize global pricing. Vertical integration strategies are emerging as a risk-mitigation response, with Cosucra contracting over 400 farmers within a 60-kilometer radius of its Belgian facility, guaranteeing harvest-to-extraction timelines under 48 hours to preserve fructan chain length. Alternative sources such as Jerusalem artichoke and agave offer diversification potential, yet lack established agricultural infrastructure and extraction protocols, requiring 5-7 years of agronomic development before reaching commercial scale.

Gastrointestinal tolerance limits (Bloating, FODMAPs)

Fermentation of soluble fibers by colonic bacteria produces gas and short-chain fatty acids, which can trigger bloating, flatulence, and abdominal discomfort in individuals with irritable bowel syndrome or small intestinal bacterial overgrowth. Inulin and fructooligosaccharides are classified as high-FODMAP ingredients, restricting their use in products targeting gut-sensitive consumers who represent an estimated 15-20% of adults in developed markets. Clinical tolerance thresholds vary by fiber type and individual microbiome composition, with studies showing that 10 grams per day of chicory inulin causes mild gastrointestinal symptoms in 30% of participants, rising to 60% at 20 grams per day. This dose-response relationship constrains inclusion rates in single-serving products, limiting formulators' ability to achieve "excellent source of fiber" claims (≥5 grams per serving) without risking consumer complaints. Personalized-fiber approaches are emerging, with companies offering microbiome-test kits that predict individual tolerance to specific fiber types, yet these services remain niche and expensive, with testing costs exceeding USD 150 per consumer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Beta-Glucan Outpaces Inulin Despite Smaller Base

Beta-glucan is forecast to grow at 11.35% annually through 2031, exceeding the category average by 132 basis points, while inulin and fructooligosaccharides held 38.05% market share in 2025. This divergence reflects beta-glucan's dual-claim eligibility for cholesterol reduction and glycemic control under both FDA and EFSA frameworks, enabling formulators to command premium pricing in functional-food categories. Oat beta-glucan's solubility advantage over barley beta-glucan simplifies beverage applications, with suppliers developing enzymatically hydrolyzed variants that maintain viscosity at pH 3.5-4.0 for use in acidic fruit drinks. Pectin, sourced primarily from citrus peel and apple pomace, serves niche applications in jams, confectionery, and pharmaceutical capsules, where its gelling properties cannot be replicated by other soluble fibers. Polydextrose functions as a bulking agent in sugar-free confections and baked goods, yet its synthetic classification limits appeal in clean-label formulations. Resistant dextrin and soluble corn fiber are gaining traction in clear-beverage applications due to their neutral taste and high solubility, with Ingredion's USD 100 million Indianapolis investment in February 2025 expanding resistant-maltodextrin capacity by 40,000 tonnes annually. Other soluble fibers, including acacia gum, psyllium, and guar gum, occupy specialized niches where emulsification, viscosity modification, or therapeutic dosing justifies their higher costs relative to commodity inulin.

Regulatory compliance factors are reshaping type preferences, with EFSA's degree-of-polymerization ≥10 threshold for fiber health claims eliminating short-chain fructooligosaccharides from claim eligibility and concentrating demand among long-chain inulin suppliers. Yeast-derived beta-glucan, extracted from Saccharomyces cerevisiae, offers immune-modulation benefits distinct from cereal beta-glucan's metabolic effects, yet lacks approved health claims in major markets, confining it to dietary-supplement applications. The type segmentation is experiencing bifurcation, with commodity inulin competing on price in bakery and dairy applications, while specialty fibers such as beta-glucan and resistant dextrin command premiums in functional beverages and clinical-nutrition products. Tate & Lyle's EUR 25 million Slovakia investment in PROMITOR resistant-dextrin syrups targets the beverage segment, where liquid forms enable inline dosing and eliminate powder-handling infrastructure.

By Source: Legume and Nut Fibers Gain on Protein Co-Extraction Economics

Legumes and nuts are projected to grow at 10.68% through 2031, driven by pulse-protein extraction processes that yield high-purity galactomannans as co-products, improving process economics and reducing fiber costs by 15-20% compared to dedicated chicory cultivation. Cereals and grains commanded 45.63% of sourcing share in 2025, anchored by oat and barley beta-glucan's established regulatory approvals and wheat-bran arabinoxylans' low cost in bakery applications. Fruits and vegetables, primarily citrus peel and apple pomace for pectin extraction, face margin pressure from competing uses such as animal feed and biofuel feedstock, with pectin prices rising 14% in 2025 as citrus-processing volumes declined. Roots and tubers, dominated by chicory and Jerusalem artichoke, supply the majority of inulin and fructooligosaccharides, yet geographic concentration in Belgium and the Netherlands creates supply-chain vulnerability to weather shocks and pest outbreaks. Other sources, including seaweed-derived alginates and microbial fermentation of resistant dextrin, represent emerging supply routes that bypass agricultural variability, with Cargill's USD 45 million Poland investment in microbial fermentation capacity commercialized in 2024.

The shift toward legume and nut sources aligns with broader plant-protein trends, where pea, chickpea, and lentil processing generates fiber-rich fractions that formulators incorporate into protein bars, meat analogs, and dairy alternatives. Roquette's acquisition of Tereos's Nutriose resistant-dextrin business in 2024, combined with its EUR 400 million pea-protein investment, positions the company to offer integrated protein-fiber solutions that simplify formulation and reduce ingredient counts. Seaweed sources such as Laminaria and Ascophyllum yield alginates and carrageenans with unique gelling and thickening properties, yet their classification as hydrocolloids rather than dietary fibers limits their contribution to fiber-content claims. Microbial fermentation routes, where engineered bacteria produce resistant dextrin or beta-glucan from glucose feedstocks, offer year-round production independence from agricultural cycles, yet capital intensity and consumer acceptance of fermentation-derived ingredients remain barriers to widespread adoption.

By Application: Dietary Supplements Leverage Personalized-Nutrition Platforms

Dietary supplements are forecast to grow at 11.18% annually through 2031, outpacing food and beverage applications, which held a 60.38% share in 2025. This acceleration reflects personalized-nutrition platforms that pair microbiome sequencing with tailored fiber-probiotic blends, creating subscription revenue models and higher per-consumer lifetime value. Prebiotic supplements targeting specific health outcomes, gut health, immune support, and metabolic wellness command USD 25-40 per month retail prices, compared to USD 8-12 for generic fiber powders, enabling brands to justify direct-to-consumer distribution and bypass retailer margin compression. Pharmaceutical applications, including fiber-based laxatives and cholesterol-management therapies, benefit from clinical-trial substantiation and physician recommendations, yet face generic competition and reimbursement pressures that limit volume growth. Animal feed applications incorporate inulin and beta-glucan as prebiotic additives to improve gut health and feed conversion ratios in poultry, swine, and aquaculture, with the European Union's 2024 ban on prophylactic antibiotic use in livestock driving prebiotic adoption as a non-pharmaceutical alternative.

Personal care and cosmetics applications remain niche, with inulin and beta-glucan appearing in moisturizers and serums for their humectant and film-forming properties, yet lack of efficacy differentiation versus hyaluronic acid and glycerin limits market penetration. Food and beverage applications span bakery, dairy, beverages, and snacks, where soluble fibers deliver multifunctional benefits including sugar reduction, shelf-life extension, texture modification, and fiber-content claims. The beverage segment is experiencing the fastest growth within food applications, driven by clear-fiber technologies that enable fortification of sports drinks, flavored waters, and ready-to-drink teas without haze or sedimentation. Ingredion's USD 50 million Cedar Rapids investment in February 2025 expanded soluble-fiber capacity for beverage applications, targeting the North American market where front-of-pack labeling mandates are accelerating reformulation cycles.

By Form: Liquid and Syrup Variants Simplify Beverage Fortification

Powder forms held 71.82% market share in 2025, yet liquid and syrup variants are growing at 10.45%, driven by beverage manufacturers' preference for inline dosing systems that eliminate powder-handling infrastructure and reduce contamination risks. Resistant-dextrin syrups at 70-75% solids content match the viscosity and sweetness profiles of high-fructose corn syrup, enabling formulators to achieve 30-50% sugar reduction through direct substitution without reformulating mixing protocols. Tate & Lyle's EUR 25 million Slovakia investment targets liquid PROMITOR production, with enzymatic hydrolysis processes that maintain solubility and stability across pH 3.0-7.0, covering the full range of beverage applications from acidic fruit drinks to neutral dairy alternatives. Powder forms retain dominance in bakery, dairy, and supplement applications, where dry blending and longer shelf life justify the additional handling complexity.

Liquid forms command 15-20% price premiums over powder equivalents on a dry-solids basis, yet deliver cost savings through reduced labor, equipment, and quality-control requirements in beverage production. Clear-fiber technologies, which use enzymatic or thermal treatments to reduce molecular weight and eliminate haze-forming aggregates, enable the fortification of transparent beverages such as sports drinks and flavored waters, which represent high-growth, premium-priced categories. ADM's USD 26 million Erlanger investment in January 2026 expanded liquid-fiber capabilities for the North American beverage market, with inline blending systems that allow real-time fiber-content adjustments based on batch-specific sugar levels. Syrup forms also reduce transportation costs per unit of fiber, with 70% solids content delivering 2.3 times the fiber per kilogram compared to spray-dried powders at 95% purity, lowering freight expenses and carbon footprints for transcontinental shipments.

Geography Analysis

North America commanded 42.86% of market share in 2025, driven by the FDA's 2024 front-of-pack labeling final rule that mandates added-sugar disclosure in grams and percentage-of-daily-value, forcing beverage and dairy manufacturers to reformulate with soluble fibers that deliver bulk and sweetness masking without added-sugar penalties. The USDA's 2025-2030 Dietary Guidelines elevated fiber from an underconsumed nutrient to a priority intervention, with recommendations increasing to 28-34 grams per day for adults, creating regulatory endorsement for high-fiber product categories. United States school-meal programs capped added sugars at 10% of total calories in 2025, catalyzing reformulation of chocolate milk, breakfast cereals, and snack bars with inulin and resistant-dextrin blends that preserve sensory profiles at 40% lower sucrose levels, according to the USDA Food and Nutrition Service. Canada's front-of-pack nutrition symbol, implemented in 2024, requires warning labels on products high in saturated fat, sodium, or sugars, incentivizing fiber fortification to improve nutrient density and avoid stigmatizing symbols. Mexico's sugar-sweetened beverage tax, increased to 2 pesos per liter in 2024, is driving reformulation toward soluble fibers in carbonated soft drinks and aguas frescas, with domestic inulin production from agave expanding to reduce import dependence on European chicory suppliers.

Asia-Pacific is forecast to grow at 10.94% through 2031, propelled by China's GB 28050 nutrition-labeling revision that introduced prebiotic claims for inulin and resistant dextrin, and India's Food Safety and Standards Authority approval of chicory-root fiber for bakery applications up to 10% inclusion, according to the National Health Commission of the PRC. Japan's Foods for Specified Health Uses system approved 14 new prebiotic fiber applications in 2025, including beta-glucan from barley at 3 grams per serving for cholesterol management, expanding regulatory precedent for fiber-based health claims, according to the Ministry of Health, Labour and Welfare Japan. China's urbanization and rising disposable incomes are shifting consumption toward functional foods and dietary supplements, with prebiotic-fiber sales growing 41% in e-commerce channels during 2025. India's growing middle class and increasing diabetes prevalence, estimated at 101 million adults in 2025, are driving demand for diabetic-friendly products fortified with beta-glucan and psyllium, yet infrastructure gaps in cold-chain logistics limit liquid-fiber adoption outside major metropolitan areas. Australia's Health Star Rating system, revised in 2024 to award bonus points for fiber content above 3 grams per serving, is incentivizing reformulation across snack and breakfast categories, with domestic oat-beta-glucan production expanding to serve regional demand.

Europe's growth is tempered by chicory-root supply concentration in Belgium and the Netherlands, where combined cultivation spans only 12,000 hectares and climate volatility in 2024 reduced root yields by 18%, tightening inulin spot prices by 23% year-over-year. The European Food Safety Authority's 2025 guidance requiring degree-of-polymerization ≥10 for fiber health claims eliminated short-chain fructooligosaccharides from claim eligibility, concentrating market share among suppliers with chromatography-validated specifications. Germany's Nutri-Score labeling system, adopted by 60% of major retailers in 2025, awards favorable ratings to products with fiber content above 4.7 grams per 100 grams, driving reformulation in bakery and dairy categories. The United Kingdom's reformulation program, targeting 20% sugar reduction across packaged foods by 2027, is accelerating soluble-fiber adoption in confectionery and biscuits, with resistant-dextrin blends replacing glucose syrup in reduced-sugar formulations. South America's growth centers on Brazil, where the National Health Surveillance Agency approved inulin for infant-formula applications in 2024, opening a high-value segment worth an estimated USD 180 million annually. Argentina's economic volatility and currency depreciation are constraining import capacity for European chicory inulin, spurring domestic agave cultivation and extraction projects in Mendoza and San Juan provinces. Middle East and Africa markets are nascent, with Saudi Arabia's food-fortification mandates and South Africa's sugar tax creating early demand signals, yet limited local fiber-ingredient production and high import duties restrict market development.

Competitive Landscape

The soluble fiber industry registers a moderate concentration, indicating moderate fragmentation with five players, Südzucker, Cargill, Cosucra, Archer Daniels Midland, and Ingredion, holding meaningful but non-dominant positions. Strategic differentiation hinges on vertical integration depth, with Cosucra's 400-farmer chicory network within a 60-kilometer radius of its Belgian extraction facility enabling harvest-to-inulin timelines under 48 hours, preserving fructan chain length and prebiotic potency that commands 8-12% price premiums in pharmaceutical-grade applications. Capacity expansions are shifting toward liquid and syrup forms, which simplify beverage fortification and reduce customers' capital requirements for powder-handling infrastructure.

Tate & Lyle's EUR 25 million investment in PROMITOR-resistant dextrin syrups in Slovakia targets viscosity profiles that mimic those of high-fructose corn syrup, allowing formulators to achieve 30-50% sugar reduction through direct substitution. White-space opportunities exist in personalized-fiber blends paired with microbiome sequencing, where subscription models generate recurring revenue and higher customer lifetime value compared to one-time retail purchases. Emerging disruptors include fermentation-derived fiber producers that bypass agricultural variability and geographic concentration risks, with Cargill's USD 45 million Poland investment in microbial resistant-dextrin production commercialized in 2024.

Technology adoption centers on enzymatic hydrolysis processes that reduce molecular weight and eliminate haze formation in clear beverages, with ADM's USD 26 million Erlanger investment in January 2026 expanding inline blending capabilities for real-time fiber-content adjustments. Patent filings in 2025 concentrated on fiber-protein co-extraction methods from pulse crops, with Roquette's acquisition of Tereos's Nutriose business positioning it to offer integrated solutions that reduce ingredient counts and simplify formulation. Smaller players such as Nexira leverage ethical-sourcing narratives around acacia gum from sub-Saharan Africa, satisfying retailer requirements for deforestation-free supply chains and traceability to the tree level.

Soluble Fiber Industry Leaders

Südzucker AG

Cargill Inc.

Cosucra Groupe Warcoing

Archer Daniels Midland Company

Ingredion Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Archer Daniels Midland announced a USD 26 million investment in its Erlanger, Kentucky facility to expand soluble-fiber production capabilities, focusing on liquid-resistant dextrin formulations for the North American beverage market.

- February 2025: Ingredion Inc. committed USD 100 million to expand the resistant-maltodextrin capacity at its Indianapolis, Indiana, facility by 40,000 tonnes annually, targeting growth in dietary supplements and functional beverages.

- February 2025: Layn Natural Ingredients introduced its innovative beta-glucan ingredient, Galacan, at Expo West. According to Layn, Galacan is designed as a next-generation, water-soluble alternative to traditional beta-glucans derived from mushrooms, oats, and yeast.

- December 2024: Tate & Lyle announced a strategic partnership with BioHarvest to develop next-generation plant-based ingredients using botanical synthesis technology, enabling sustainable production of non-GMO plant-derived ingredients without traditional agricultural constraints. The collaboration aims to develop more affordable, accessible ingredients for the food and beverage industry.

Global Soluble Fiber Market Report Scope

Soluble fiber refers to a type of dietary fiber that dissolves in water to form a gel-like substance, helping support digestive health and regulate blood sugar and cholesterol levels. The soluble fiber market is segmented by type, source, application, form, and geography. By type, the market includes inulin and FOS, pectin, beta-glucan, polydextrose, resistant dextrin/soluble corn fiber, and other soluble fibers such as acacia, psyllium, and guar. By source, the market covers cereals and grains, fruits and vegetables, roots and tubers (such as chicory and Jerusalem artichoke), legumes and nuts, and other sources, including seaweed and microbial origins. Based on application, the market is segmented into food and beverages, dietary supplements, pharmaceuticals, animal feed, personal care and cosmetics, and other uses. By form, the market includes powder and liquid/syrup. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million).

| Inulin and FOS |

| Pectin |

| Beta-Glucan |

| Polydextrose |

| Resistant Dextrin/Soluble Corn Fiber |

| Other Soluble Fibers (Acacia, Psyllium, Guar, etc.) |

| Cereals and Grains |

| Fruits and Vegetables |

| Roots and Tubers (Chicory, Jerusalem Artichoke) |

| Legumes and Nuts |

| Others (Seaweed, Microbial) |

| Food and Beverages |

| Dietary Supplements |

| Pharmaceuticals |

| Animal Feed |

| Personal Care and Cosmetics |

| Others |

| Powder |

| Liquid/Syrup |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Type | Inulin and FOS | |

| Pectin | ||

| Beta-Glucan | ||

| Polydextrose | ||

| Resistant Dextrin/Soluble Corn Fiber | ||

| Other Soluble Fibers (Acacia, Psyllium, Guar, etc.) | ||

| By Source | Cereals and Grains | |

| Fruits and Vegetables | ||

| Roots and Tubers (Chicory, Jerusalem Artichoke) | ||

| Legumes and Nuts | ||

| Others (Seaweed, Microbial) | ||

| By Application | Food and Beverages | |

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Form | Powder | |

| Liquid/Syrup | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the soluble fiber market by 2031?

The soluble fiber market size is forecast to reach USD 8.93 billion by 2031, expanding at a 10.03% CAGR between 2026 and 2031.

Which soluble fiber type is growing fastest?

Beta-glucan is expected to register the highest growth at an 11.35% CAGR through 2031, outperforming the overall soluble fiber market.

Why are liquid soluble fibers gaining popularity in beverages?

Liquid and syrup forms match the viscosity of high-fructose corn syrup, allow inline dosing, and eliminate powder handling, supporting rapid reformulation for sugar-reduction targets.

Which region leads the market in revenue, and which grows fastest?

North America led with 42.86% of 2025 revenue, while Asia-Pacific is the fastest-growing region at a 10.94% CAGR to 2031.

Page last updated on: