Citrus Pulp Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

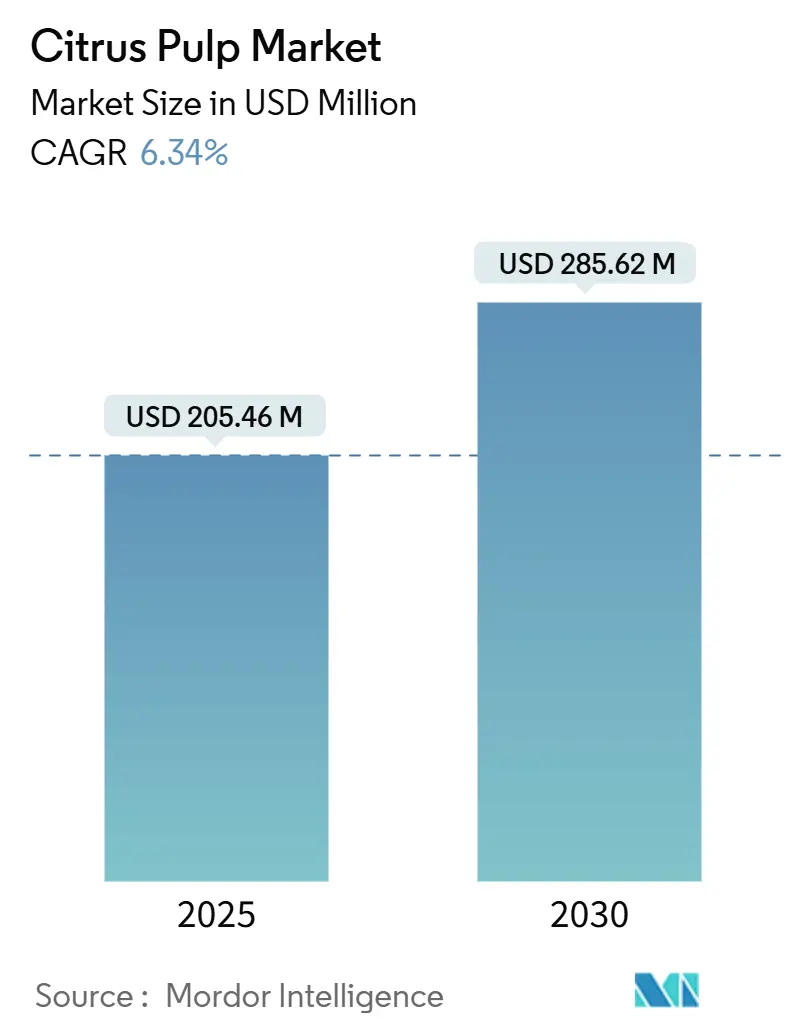

| Market Size (2025) | USD 205.46 Million |

| Market Size (2030) | USD 285.62 Million |

| Growth Rate (2025 - 2030) | 6.34% CAGR |

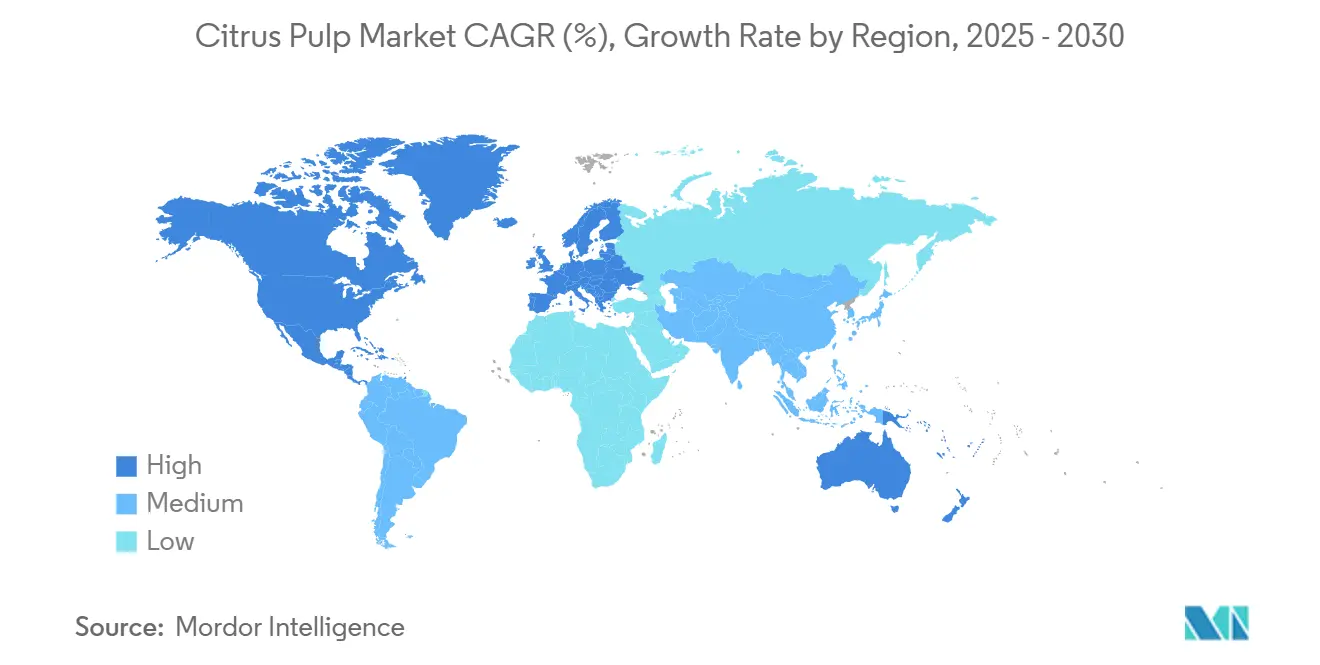

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Citrus Pulp Market Analysis by Mordor Intelligence

The citrus pulp market size stood at USD 205.46 billion in 2025 and is forecast to reach USD 285.62 billion by 2030, advancing at a 6.34% CAGR. Growth stems from waste-valorization economics, rising demand for natural fibers, and expanding functional food applications. South America remains the largest producing base, yet weather-related supply swings and citrus greening disease force processors to diversify sourcing. Asia Pacific drives incremental demand as Chinese processors ramp capacity and regional diets pivot toward clean-label products. Consolidation among vertically integrated agribusinesses strengthens bargaining power with downstream users, while technology upgrades raise extraction yields and widen premium ingredient opportunities.

Key Report Takeaways

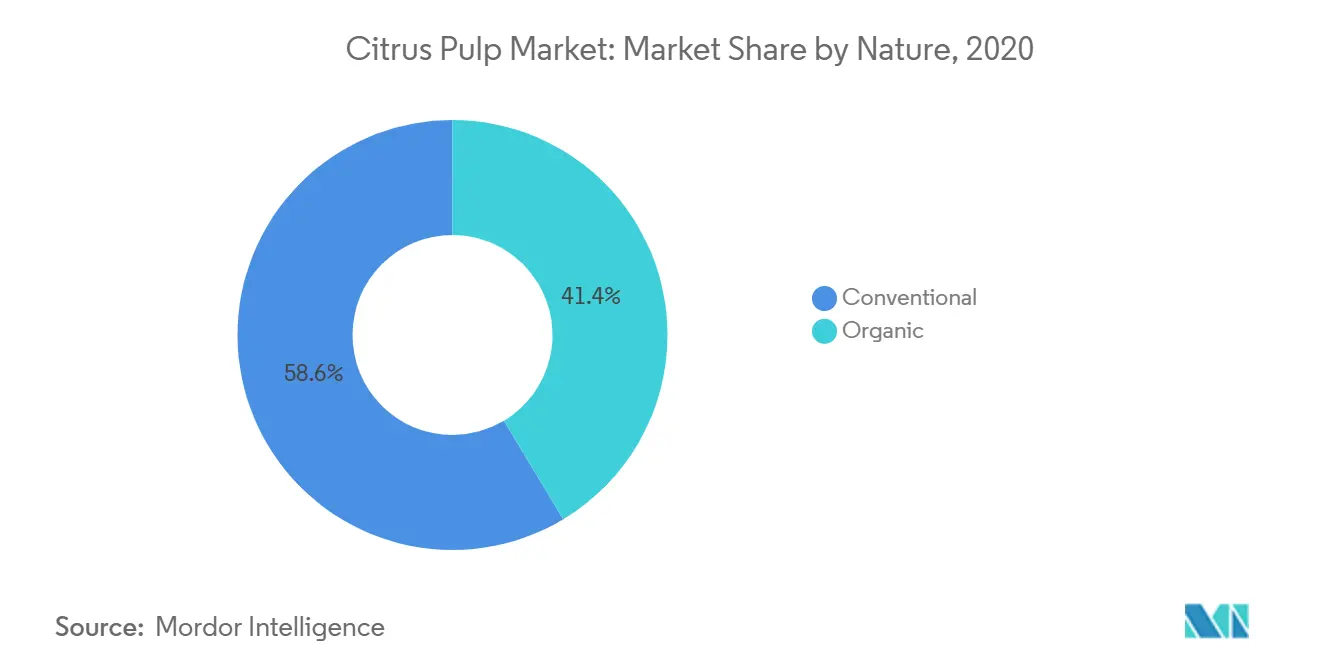

- By nature, conventional pulp accounted for 58.62% of the citrus pulp market share in 2024; the organic segment is projected to grow at a 7.12% CAGR to 2030.

- By source, orange-derived pulp captured 52.30% of the citrus pulp market share in 2024; lemon and lime pulp are set to expand at a 7.45% CAGR through 2030.

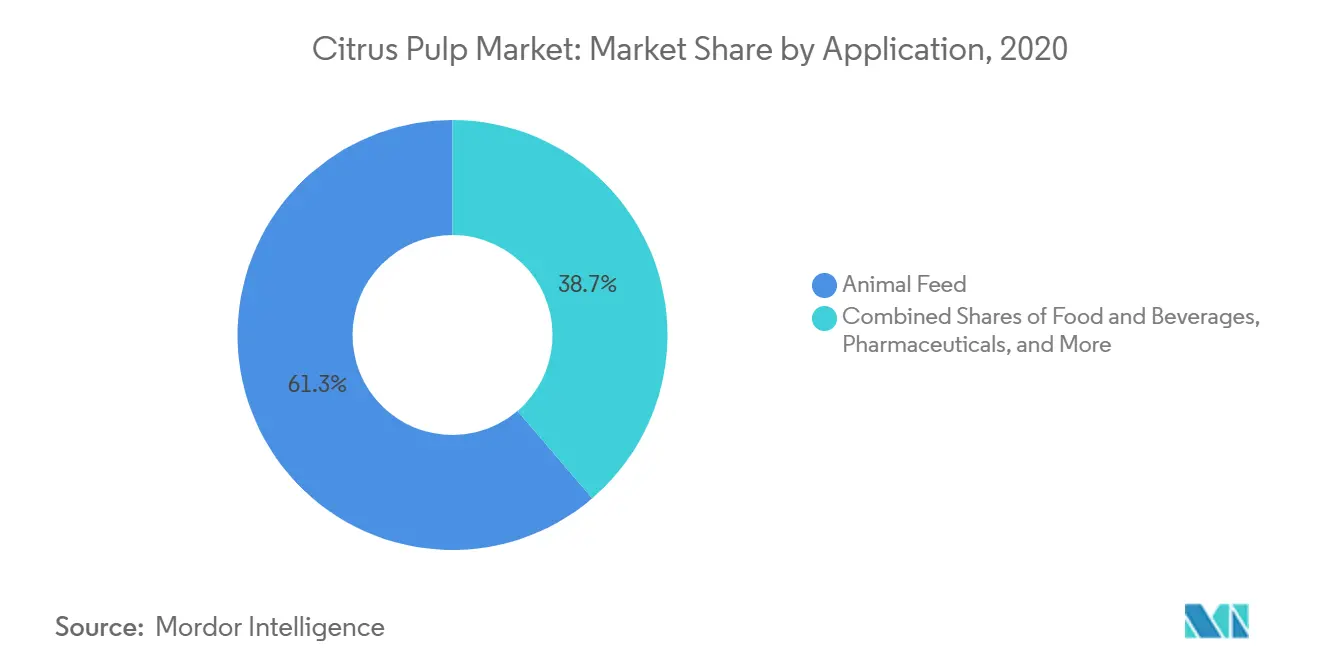

- By application, animal feed represented 61.27% of the citrus pulp market share in 2024; food and beverage uses are advancing at an 8.02% CAGR to 2030.

- By geography, South America held 38.52% of the citrus pulp market share in 2024, while Asia Pacific is projected to post the fastest 8.52% CAGR through 2030.

Global Citrus Pulp Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing integration of citrus pulp into functional foods | +1.2% | Global, with North America & EU leading adoption | Medium term (2-4 years) |

| Surge in clean-label and plant-based product launches | +0.9% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Growing demand for sustainable and eco-friendly animal feed | +0.8% | Global, strongest in EU and North America | Long term (≥ 4 years) |

| Advancements in citrus pulp extraction and processing | +0.7% | Global, concentrated in major processing hubs | Medium term (2-4 years) |

| Rising consumer preference for dietary fiber, antioxidants, and prebiotic supplements | +1.1% | Global, premium markets in developed economies | Medium term (2-4 years) |

| Expansion of biofuel and green energy applications using citrus pulp | +0.6% | Brazil, EU, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Integration of Citrus Pulp into Functional Foods

The functional foods sector increasingly recognizes citrus pulp as a multifunctional ingredient delivering fiber, antioxidants, and natural preservation properties. Food manufacturers are incorporating citrus fiber at inclusion rates of 2-5% in bakery products, beverages, and processed foods to enhance nutritional profiles while maintaining clean-label positioning. This integration addresses consumer demand for transparent ingredient lists while providing technical benefits, including improved texture, moisture retention, and shelf-life extension. The trend accelerates as regulatory frameworks like the FDA's updated dietary fiber definitions create market incentives for fiber-enriched products, with citrus pulp's high pectin content (up to 42.5% of composition) offering superior functionality compared to synthetic alternatives.

Surge in Clean-Label and Plant-Based Product Launches

Clean-label positioning drives unprecedented adoption of citrus pulp as manufacturers replace synthetic additives with natural alternatives. The ingredient's versatility enables multiple functional roles, including emulsification, stabilization, and natural coloring, reducing ingredient list complexity while meeting consumer preferences for recognizable components. Plant-based product developers particularly value citrus pulp's ability to improve texture and mouthfeel in dairy alternatives and meat substitutes, with inclusion rates typically ranging from 1-3% by weight. This trend intersects with regulatory compliance factors, as FSSC 22000 and organic certification standards favor natural processing aids over synthetic alternatives. The momentum is sustained by retail buyers' preference for products with fewer than 10 ingredients, positioning citrus pulp as a strategic consolidation tool for formulators.

Growing Demand for Sustainable and Eco-Friendly Animal Feed

Livestock producers increasingly adopt citrus pulp as a sustainable feed ingredient that reduces environmental impact while maintaining nutritional performance. Research demonstrates that citrus pulp inclusion at 10-45% of ruminant diets maintains fermentation parameters while providing antioxidant benefits that improve meat and milk oxidative stability. The sustainability appeal stems from citrus pulp's role in circular economy models, converting processing waste into valuable nutrition while reducing dependence on grain-based feeds. European Union regulations increasingly favor feed ingredients with lower carbon footprints, creating regulatory tailwinds for citrus pulp adoption. The trend gains momentum as major feed manufacturers seek to differentiate their offerings through sustainability credentials, with citrus pulp's high energy density (approximately 0.85-0.90 relative to corn) providing economic justification alongside environmental benefits.

Advancements in Citrus Pulp Extraction and Processing

Technological innovations in citrus processing are enhancing pulp yield, quality, and functional properties through advanced extraction methods. Steam explosion, enzymatic hydrolysis, and optimized drying techniques increase recovery rates while preserving bioactive compounds, including polyphenols, flavonoids, and carotenoids. Machine vision systems now enable automated citrus grading with diameter accuracy within 1.5mm, improving raw material consistency for downstream pulp processing. These processing improvements address quality control challenges that have historically limited premium applications, with enhanced standardization enabling broader adoption in pharmaceutical and nutraceutical sectors. The integration of membrane concentration and freeze-drying technologies preserves heat-sensitive compounds, expanding market opportunities in high-value applications where bioactivity retention is critical.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable supply due to citrus fruit yield fluctuations | -1.4% | Global, acute in Florida, Brazil, Mediterranean | Short term (≤ 2 years) |

| Stringent sustainability, food safety, and organic certification regulations | -0.8% | EU, North America, developed APAC markets | Medium term (2-4 years) |

| Increased competition from alternative plant fibers | -0.6% | Global, concentrated in food applications | Medium term (2-4 years) |

| Quality Control Challenges | -0.5% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Variable Supply Due to Citrus Fruit Yield Fluctuations

Citrus production volatility creates significant supply chain disruptions that constrain market growth and increase price volatility. According to the United States Department of Agriculture[1]United States Department of Agriculture, "Orange production in the United States", www.usda.gov data from 2024, orange production in the United States declined from 5,254 thousand tons in 2020 to 2,758 thousand tons in 2024. Brazilian production faces similar pressures, with the 2024/25 crop declining 27.4% due to adverse weather and disease pressure, creating global supply shortages that doubled concentrate prices. These fluctuations particularly impact animal feed applications where consistent supply and pricing are critical for livestock operation economics. The constraint intensifies as climate change increases weather volatility, with processing facilities unable to maintain consistent pulp output when raw material availability varies significantly year-over-year.

Stringent Sustainability, Food Safety, and Organic Certification Regulations

Regulatory compliance requirements create significant barriers to market entry and increase operational costs across the citrus pulp value chain. FDA's Produce Safety Rule mandates comprehensive traceability, water quality monitoring, and worker hygiene protocols that require substantial documentation and infrastructure investment. FSSC 22000 certification demands rigorous HACCP implementation, with processing facilities requiring specialized equipment and trained personnel to maintain compliance. Organic certification adds complexity through soil amendment restrictions, pesticide prohibitions, and separation requirements that increase production costs by 15-25% compared to conventional operations. These regulatory frameworks, while ensuring product safety and quality, create competitive disadvantages for smaller processors and limit market access in premium applications where certification is mandatory. The constraint is particularly acute in export markets where multiple certification standards may apply simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Organic Segment Drives Premium Growth

In 2024, conventional citrus pulp dominates the market with a 58.62% share, capitalizing on well-established supply chains and cost advantages for bulk applications. Meanwhile, the organic segment is set to grow at a 7.12% CAGR through 2030, driven by its premium appeal to health-conscious consumers and favorable regulatory trends in Europe. Obtaining organic certification requires strict compliance with soil amendment standards and pesticide restrictions. These rigorous requirements, while increasing production costs, create supply constraints that support premium pricing. The conventional segment primarily serves animal feed and industrial applications, where cost efficiency takes precedence over certification premiums. On the other hand, organic variants cater to functional foods, nutraceuticals, and premium animal nutrition markets.

Processing facilities are increasingly investing in organic certification infrastructure to tap into premium market opportunities. Certified operations achieve price premiums of 25-40% compared to conventional alternatives. The organic segment benefits from regulatory support, including the EU's organic action plans and the USDA's program expansions, fostering favorable conditions for certified producers. Conventional pulp remains critical for high-volume applications, particularly in commodity animal feed markets, where cost competitiveness is the primary purchasing factor, limiting the value proposition of organic certification.

By Source: Orange Dominance Faces Lemon-Lime Challenge

In 2024, orange-derived pulp holds a dominant 52.30% share of the market, benefiting from the fruit's leadership in global citrus production and a robust processing infrastructure. At the same time, lemon and lime sources are the fastest-growing segment, achieving a 7.45% CAGR. According to the Agriculture Institute[2]Agriculture Institute, "Citrus Production", www.agriculture.institute data from 2023, the annual production of citrus fruits in India was 5,303 thousand metric tons. This growth is driven by their specialized use in nutraceuticals and premium functional foods, where their distinct flavor profiles and bioactive compounds offer a competitive edge. Grapefruit pulp serves niche markets in dietary supplements and specialized animal nutrition, while tangerine and mandarin sources focus on premium juice blends and artisanal food products. The variety of citrus sources enables processors to adjust their product portfolios in response to seasonal availability and changing market demands.

Processing economics favor orange pulp due to economies of scale and established supply chains. Large facilities, primarily designed for orange juice production, consistently produce significant pulp volumes. In contrast, lemon and lime processing typically occurs in smaller, specialized facilities that can secure premium pricing for niche applications. Recent research reveals that enzymatic processing of mandarin varieties can enhance bioactive compound retention by up to 67%, creating opportunities for high-value applications. Additionally, diversifying the supply chain across multiple citrus sources mitigates risks associated with disease outbreaks and weather events that disproportionately affect single-variety operations.

By Application: Feed Leadership Challenged by Food Innovation

In 2024, animal feed applications hold a leading 61.27% market share, capitalizing on the high energy density and nutritional benefits of citrus pulp in ruminant diets. Studies show that including citrus pulp at 10-45% in feed rations supports rumen fermentation while delivering antioxidant benefits that enhance meat and milk quality. Meanwhile, the food and beverage sector is set to grow at an 8.02% CAGR through 2030, driven by increasing demand for clean-label products and functional ingredients. The pharmaceutical sector targets niche markets, focusing on dietary supplements and nutraceutical formulations. Additionally, citrus pulp is utilized in industrial applications, including biofuel production and cosmetic ingredients.

In the food and beverage sector, regulatory recognition of citrus fiber as a qualified health claim ingredient provides a marketing advantage for products using standardized preparations. Also use of many citrus-based beverages and bakery products is driving the market demand. According to the UNESDA[3]UNESDA, "Annual consumption of non-alcoholic beverages in the United Kingdom (UK)", www.unesda.org data from 2024, annual consumption of non-alcoholic beverages was 15,496 million liters in the United Kingdom. Furthermore, advancements in processing methods, such as steam explosion and enzymatic hydrolysis, are improving functional properties for food applications. These innovations enhance bioactive retention, supporting premium product positioning. While the animal feed sector faces challenges from alternative fiber sources and fluctuating citrus supply, its proven nutritional benefits and cost-effectiveness sustain its market leadership. In contrast, the pharmaceutical sector encounters strict quality control and regulatory requirements, which limit market entry but enable premium pricing for compliant suppliers.

Geography Analysis

South America commands 38.52% market share in 2024, driven by Brazil's dominance in orange processing and established infrastructure supporting large-scale pulp production. The region benefits from favorable growing conditions and integrated supply chains connecting citrus groves directly to processing facilities, enabling cost-efficient bulk production. However, recent challenges, including citrus greening disease and adverse weather, created supply volatility, with Brazilian orange production declining 27.4% in the 2024/25 crop cycle. Despite these headwinds, South America maintains competitive advantages through economies of scale and established export relationships, particularly in animal feed markets where cost competitiveness determines purchasing decisions. The region's processing facilities are increasingly investing in value-added applications, including bioactive extraction and organic certification, to capture premium market opportunities.

Asia Pacific emerges as the fastest-growing region at 8.52% CAGR through 2030, supported by expanding citrus processing capacity and rising domestic demand for functional ingredients. China leads regional growth with citrus production reaching 64 million tonnes in 2023, representing 7% annual increase, while processing investments target both domestic consumption and export markets. The region benefits from government support for agricultural processing modernization and growing consumer awareness of functional food benefits. Japan's establishment of LEMONITY agricultural company in 2025, targeting 100 hectares of domestic lemon production within 10 years, demonstrates regional commitment to supply chain localization. Asia Pacific's growth trajectory reflects urbanization trends and rising disposable incomes that support premium ingredient adoption in processed foods and nutraceuticals.

North America and Europe represent mature markets with stable demand patterns focused on premium applications, including organic certification and specialized functional ingredients. These regions benefit from stringent regulatory frameworks that favor natural ingredients over synthetic alternatives, creating market opportunities for certified citrus pulp products. The European Union's organic action plans and sustainability mandates support market development, while North American clean-label trends drive functional food adoption. Middle East and Africa show emerging potential, with Egypt increasing citrus processing utilization by 50% in 2024/25 to capitalize on global juice shortages and export opportunities. Regional market dynamics increasingly reflect supply chain diversification strategies as processors seek geographic risk mitigation through multi-sourcing approaches.

Competitive Landscape

The citrus pulp market exhibits high concentration with an 8 out of 10 rating, dominated by vertically integrated agribusiness conglomerates that control significant portions of the citrus processing value chain. Major players, including Louis Dreyfus Company, Citrosuco, and Archer-Daniels-Midland, leverage economies of scale and integrated operations spanning from citrus cultivation through final product distribution. Strategic consolidation continues to reshape competitive dynamics, exemplified by Limoneira's merger with Sunkist Growers effective Q1 2026, which projects USD 5 million in annual cost savings through shared infrastructure and streamlined marketing operations.

Market leaders increasingly focus on value-added applications, technological processing improvements, and geographic diversification to mitigate supply volatility and capture premium pricing opportunities. Competitive strategies emphasize vertical integration, technological innovation, and market diversification to maintain competitive advantages in an increasingly complex regulatory environment. Companies invest heavily in processing technology upgrades, including steam explosion, enzymatic hydrolysis, and advanced drying systems that improve yield and product quality while reducing environmental impact.

White-space opportunities exist in specialized applications, including pharmaceutical-grade pulp, organic certification, and bioactive compound extraction, where regulatory barriers limit competition. Emerging disruptors focus on niche markets, including biofuel applications and specialized animal nutrition, while established players defend market share through scale advantages and established customer relationships. FSSC 22000 and organic certification requirements create competitive moats for certified facilities while limiting market access for smaller processors lacking compliance infrastructure.

Citrus Pulp Industry Leaders

-

Louis Dreyfus Company

-

Cargill Inc.

-

Bunge Limited

-

Ingredion Incorporated

-

SunOpta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Louis Dreyfus Company acquired Cacique, expanding its integrated citrus operations and processing capabilities. The acquisition strengthens LDC's position in citrus value chains and supports geographic diversification strategies across multiple production regions.

- December 2023: The United Arab Emirates imported 20 metric tons of Khasi Mandarin oranges from the Meghalaya Directorate of Horticulture and Agricultural Marketing Board of India to meet the consumption demand for oranges and orange-based products for humans and livestock.

Global Citrus Pulp Market Report Scope

| Organic |

| Conventional |

| Orange |

| Grapefruit |

| Lemon and Lime |

| Tangerine/Mandarine |

| Food and Beverages |

| Pharmaceuticals |

| Animal Feed |

| Other Applications |

| North America |

| Europe |

| Asia Pacific |

| South America |

| Middle East and Africa |

| By Nature | Organic |

| Conventional | |

| By Source | Orange |

| Grapefruit | |

| Lemon and Lime | |

| Tangerine/Mandarine | |

| By Application | Food and Beverages |

| Pharmaceuticals | |

| Animal Feed | |

| Other Applications | |

| By Geography | North America |

| Europe | |

| Asia Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the projected value of the citrus pulp market by 2030?

The citrus pulp market is forecast to reach USD 285.62 billion by 2030, reflecting a 6.34% CAGR during 2025-2030.

Which region leads global production of citrus pulp?

South America holds 38.52% of global supply, anchored by large-scale Brazilian processing operations.

Which segment is expanding fastest within the citrus pulp market?

Food and beverage applications are advancing at an 8.02% CAGR as formulators seek clean-label fiber and antioxidant ingredients.

Why is organic citrus pulp gaining traction?

Organic variants grow at 7.12% CAGR because retailers and foodservice operators prefer certified ingredients that meet clean-label and sustainability expectations.

Page last updated on: