Food Fibers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.04 Billion |

| Market Size (2031) | USD 15.99 Billion |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Fibers Market Analysis by Mordor Intelligence

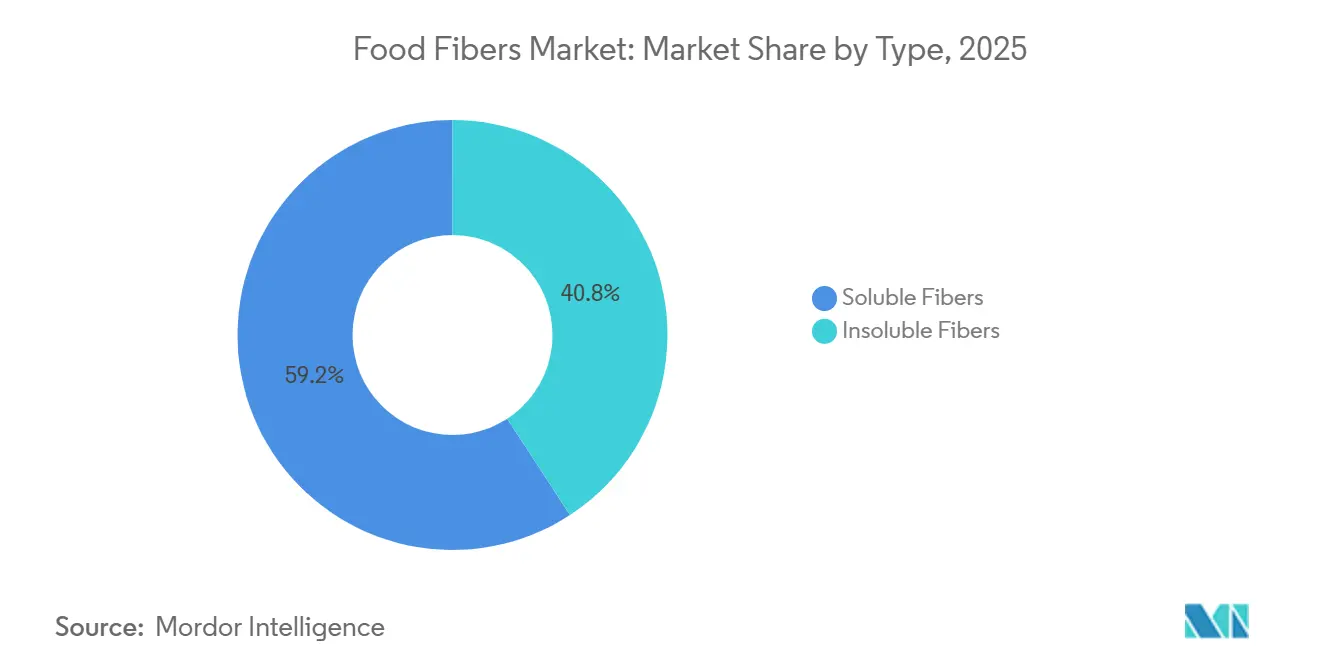

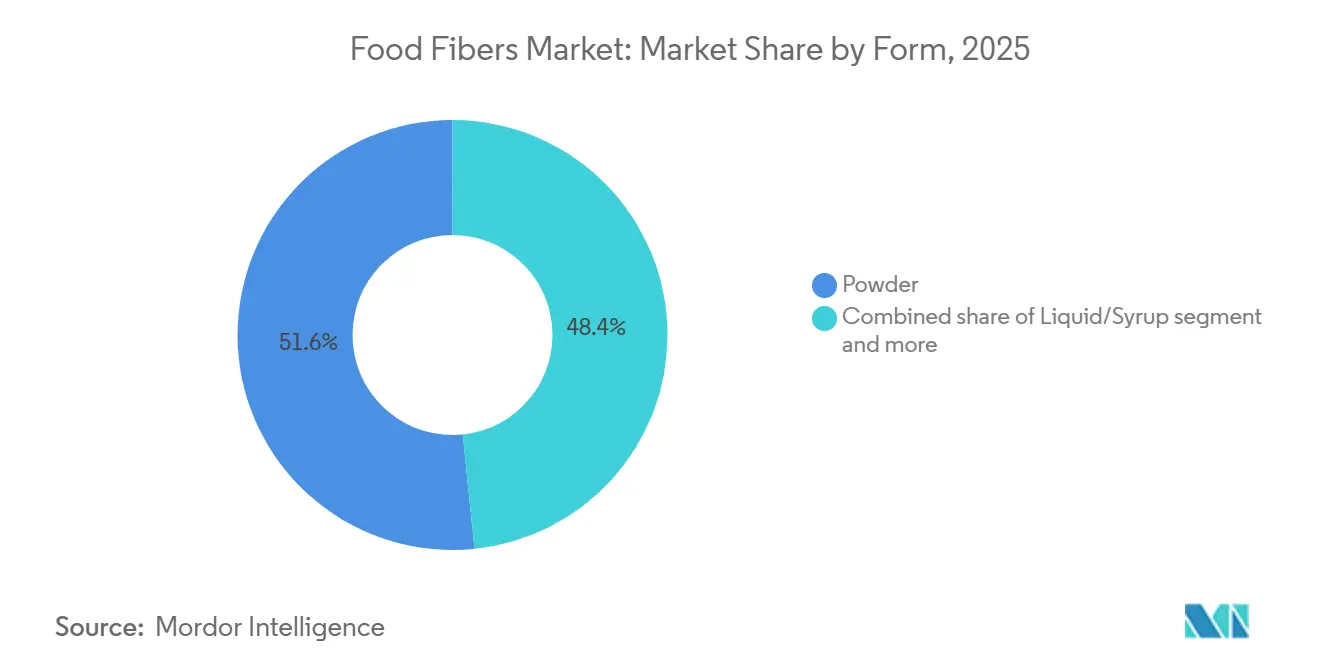

The food fibers market size is projected to expand from USD 9.29 billion in 2025 and USD 10.04 billion in 2026 to USD 15.99 billion by 2031, registering a compound annual growth rate (CAGR) of 9.75% between 2026 to 2031. This growth reflects how manufacturers are aligning with regulatory sugar-reduction targets and consumer preferences for foods that support metabolic health. Soluble fibers accounted for 59.21% of the market value in 2025, as they act as sugar substitutes while providing prebiotic benefits that resonate with gut-health trends. Insoluble fibers are anticipated to grow at a faster rate of 11.28% annually, driven by their application as cost-effective bulking agents in bakery and meat processing, where tolerance to high-shear processing is essential. Cereals and grains remained the dominant raw material category in 2025; however, nuts and seeds are expanding at a CAGR of 11.77%, supported by the growing demand for clean-label and allergen-friendly formulations. Powder formats held a 51.64% revenue share due to their ease of integration into dry mixes, while liquid and syrup formats are growing at a CAGR of 13.01%, driven by beverage manufacturers aiming to improve mouthfeel. End-use demand is increasingly shifting from mainstream food and beverage applications to direct-to-consumer dietary supplements, where fiber is positioned as a solution for metabolic health.

Key Report Takeaways

- By type, soluble fibers captured 59.21% of food fibers market share in 2025, while insoluble fibers are forecast to expand at an 11.28% CAGR through 2031.

- By source, cereals and grains held 49.01% of the food fibers market size in 2025, whereas nuts and seeds are projected to grow at an 11.77% CAGR between 2026 and 2031.

- By form, powder formats controlled 51.64% of the food fibers market size in 2025, while liquid and syrup formats are advancing at a 13.01% CAGR to 2031.

- By application, food and beverage accounted for 48.02% of the food fibers market size in 2025, and dietary supplements are recording a 12.45% CAGR through 2031.

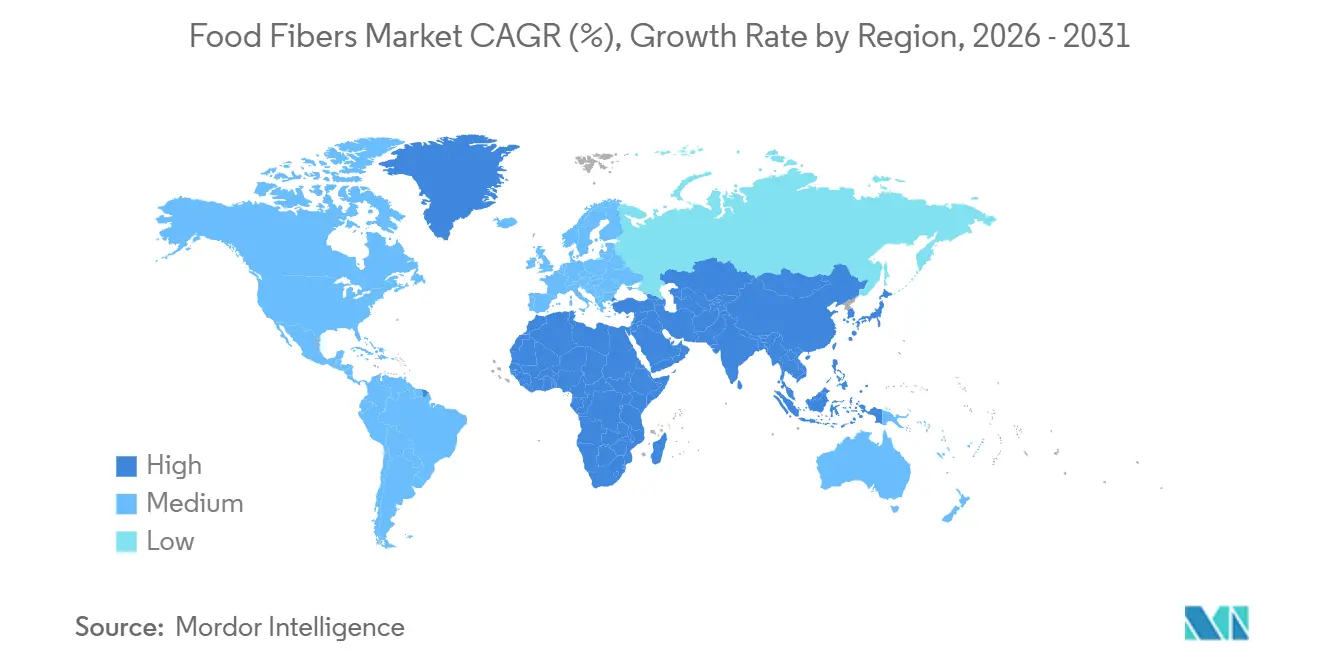

- By geography, North America led with a 40.73% revenue share in 2025, whereas Asia-Pacific is the fastest region, expanding at an 11.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Fibers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geography Relevance | Impact Timeline |

|---|---|---|---|

| Consumer demand for fiber-enriched foods, beverages, and supplements targeting digestive health | +2.1% | Global, with peak adoption in North America and Western Europe | Medium term (2-4 years) |

| Technological advancements in enzymatic and membrane-based fiber extraction methods | +1.4% | Global, concentrated in North America, Europe, and Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Functional foods promoting fiber for cardiovascular health, satiety, and glycemic control | +1.8% | North America and Europe lead, with accelerating uptake in urban Asia-Pacific | Medium term (2-4 years) |

| Preference for clean-label fiber sources over chemically modified ingredients | +1.3% | Global, strongest in North America and Western Europe | Short term (≤ 2 years) |

| Rising plant-based diets boosting consumption of naturally fiber-rich foods | +1.6% | Global, with notable momentum in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Use of soluble fibers to reduce sugars and calories in processed foods | +1.5% | Global, driven by sugar-tax legislation in Europe, Latin America, and select Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer demand for fiber-enriched foods, beverages, and supplements targeting digestive health

Digestive wellness has moved from being a niche category in health-food stores to becoming a mainstream offering in retail, with fiber-enriched products now having dedicated shelf space in conventional supermarkets. The United States Department of Agriculture's 2025 Dietary Guidelines highlighted the significant gap in fiber intake, noting that 95% of American adults fail to meet the recommended daily levels. This statistic is being utilized by brands in their on-pack messaging [1]Source: United States Department of Agriculture, “Dietary Guidelines 2025,” dietaryguidelines.gov. Claims related to prebiotic fibers, such as inulin and fructooligosaccharides (FOS), have grown as advancements in microbiome science are communicated to consumers, particularly in relation to gut-brain axis health. Supplement manufacturers are revising their fiber blends to include resistant starches and beta-glucans, aiming to address not only digestive regularity but also immune system support and cholesterol management. This increasing demand is reshaping ingredient procurement strategies, with buyers focusing on fibers that provide multiple health benefits within a single formulation.

Technological advancements in enzymatic and membrane-based fiber extraction methods

Enzymatic extraction and membrane filtration are replacing traditional alkali-based methods, enabling manufacturers to isolate fibers with higher purity and reduced environmental impact. For example, Roquette's investment in enzyme-assisted extraction of pea fiber by 2025 resulted in a 40% reduction in water usage and a 22% increase in soluble fiber yield. This advancement not only lowers the cost per functional unit but also enhances sustainability credentials. Additionally, supercritical carbon dioxide (CO2) extraction is becoming popular for specialty fibers derived from seeds and nuts, as it preserves heat-sensitive polyphenols that provide antioxidant benefits. These process innovations are critical as formulators increasingly demand fibers with neutral taste profiles and minimal impact on product color, attributes that older mechanical milling techniques often fail to achieve. The shift toward precision extraction also supports traceability, which is a key requirement for European Union organic certification and is increasingly emphasized under voluntary corporate sustainability commitments.

Functional foods promoting fiber for cardiovascular health, satiety, and glycemic control

Cardiovascular health positioning has become an important differentiator, particularly for beta-glucan derived from oats and barley, which are supported by Food and Drug Administration (FDA)-qualified health claims linking a daily intake of 3 grams to reduced blood cholesterol levels [2]Source: U.S. Food & Drug Administration “Review of the Scientific Evidence on the Physiological Effects of Certain Non-Digestible Carbohydrates,” fda.gov. Satiety-focused products are targeting the weight-management segment, with soluble fibers such as glucomannan and psyllium husk showing clinically validated effects on delaying gastric emptying and suppressing appetite. Glycemic control messaging is gaining traction in the Asia-Pacific region, where diabetes prevalence is increasing faster than in any other part of the world. India's National Institute of Nutrition has endorsed whole-grain and fiber-rich diets in its 2024 guidelines, encouraging local brands to fortify staples like chapati flour with resistant starch. The convergence of these three health platforms, namely cardiovascular health, satiety, and glycemic control, is driving co-formulation strategies, with brands combining multiple fiber types to address overlapping consumer concerns within a single product.

Preference for clean-label fiber sources over chemically modified ingredients

Consumer scrutiny of clean-label products has increased, with a growing rejection of fibers perceived as synthetic or heavily processed, such as polydextrose and certain resistant maltodextrins, despite their regulatory approval. Ingredion reported during its 2025 earnings call that demand for non-genetically-modified-organism (non-GMO), organic-certified fibers grew by 18% year-over-year, surpassing the growth rate of conventional fiber sales by a factor of three. This shift is driving suppliers to invest in identity-preserved supply chains for ancient grains and heirloom legumes. While these options command price premiums, they align with consumer expectations for transparency. Retailers such as Whole Foods Market and Tesco have removed products containing chemically modified starches, accelerating reformulation efforts and increasing the need for ingredient suppliers to validate the botanical origin and minimal processing of their fiber products. This trend is particularly significant in Europe, where the European Food Safety Authority's stringent novel-food approval process has heightened consumer caution regarding unfamiliar fiber names on ingredient labels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and regulatory challenges in dietary fiber labeling and functionality definitions | -0.8% | Global, with acute impact in North America and Europe due to stringent labeling enforcement | Short term (≤ 2 years) |

| Regulatory challenges restricting fiber health claims on packaging across jurisdictions | -0.6% | Global, most pronounced in Europe and Asia-Pacific where claim substantiation requirements are rigorous | Medium term (2-4 years) |

| Complex regulations affecting isolated and synthetic fiber approvals in multiple markets | -0.5% | Global, with highest barriers in European Union and select Asia-Pacific countries | Long term (≥ 4 years) |

| Technical difficulties maintaining fiber functionality during high-temperature and high-shear processing | -0.7% | Global, particularly impacting shelf-stable and retort-processed food categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price volatility and regulatory challenges in dietary fiber labeling and functionality definitions

Raw material costs for wheat bran and oat fiber fluctuated by 25% to 35% between 2024 and 2025, primarily due to drought conditions in the North American Great Plains and export restrictions from Black Sea producers. This price volatility has significantly impacted the profit margins of fiber suppliers operating under fixed-price contracts with food manufacturers. Consequently, some suppliers have opted to reformulate blends using lower-cost alternatives, such as sugarcane bagasse or rice bran, although these alternatives may not deliver the same functional performance. Adding to these challenges, regulatory uncertainty has created further complications. The Food and Drug Administration's (FDA) 2024 guidance on resistant maltodextrin reclassified certain variants as non-fiber, forcing brands to either reformulate products or remove fiber claims. This adjustment resulted in an estimated cost of USD 120 million for the industry in packaging and inventory write-offs. Furthermore, varying definitions of dietary fiber across different markets, where a fiber may qualify in the United States but not under Codex Alimentarius or European Union standards, have made multinational product development more complex and increased compliance costs.

Regulatory challenges restricting fiber health claims on packaging across jurisdictions

Health claim substantiation requirements vary significantly across regions, creating challenges for marketing flexibility. The European Food Safety Authority (EFSA) rejected 78 percent of fiber-related health claim applications between 2020 and 2025, primarily due to insufficient clinical evidence or unclear cause-and-effect relationships. This high rejection rate discourages companies from investing in the development of health claims. In comparison, the United States Food and Drug Administration permits qualified health claims for specific fibers, such as psyllium and beta-glucan, but only after the submission of comprehensive dossiers and peer-reviewed trial data. This rigorous process often creates significant hurdles for smaller ingredient suppliers. In the Asia-Pacific region, additional challenges are present. For instance, China's National Health Commission (NHC) requires domestic clinical trials for imported fiber ingredients seeking health claims. This process typically extends timelines by 18 to 24 months and incurs costs ranging from USD 500,000 to USD 1 million. These strict regulations force brands to rely on structure-function statements or implied benefits, which reduces product differentiation and limits opportunities for premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Insoluble Fibers Gain Share as Bakery Reformulation Accelerates

Insoluble fibers are anticipated to grow at a compound annual growth rate (CAGR) of 11.28% from 2026 to 2031, exceeding the market average growth rate of 9.75%. This growth is primarily driven by bakery and snack manufacturers looking for cost-effective texture modifiers that can withstand high-temperature baking without affecting crumb structure. Cellulose, which represents the largest segment within insoluble fibers, is increasingly being incorporated into gluten-free formulations to mimic the structural integrity traditionally provided by wheat gluten. This shift has resulted in a 14% year-over-year increase in cellulose usage in bread and pasta. Resistant starch, particularly Type 2 derived from high-amylose corn, is gaining popularity in extruded snacks as it offers both fiber fortification and reduced oil absorption during frying. This dual benefit helps lower production costs while enhancing the nutritional profile of the products.

Soluble fibers accounted for 59.21% of the market value in 2025, with inulin leading in dairy and beverage applications due to its prebiotic properties and neutral taste profile, which align with clean-label trends. Pectin continues to play a significant role in fruit preparations and confectionery; however, its growth is being challenged by alternatives such as gellan gum and other hydrocolloids that provide better heat stability. Beta-glucan, sourced from oats and barley, is carving out a premium niche in cardiovascular health products. This is supported by Food and Drug Administration (FDA)-qualified health claims, allowing brands to charge 20% to 30% higher prices compared to generic fiber blends.

By Source: Nuts and Seeds Surge as Allergen-Friendly and Sustainability Narratives Converge

Nuts and seeds are expected to grow at a compound annual growth rate (CAGR) of 11.77% from 2026 to 2031, making them the fastest-growing source category. This growth is attributed to their dual appeal as allergen-friendly alternatives to soy and wheat, while also providing high fiber content, protein, and healthy fats. Chia and flax seeds, in particular, are being processed into fine powders that can be seamlessly incorporated into baked goods, smoothies, and energy bars. Brands are also highlighting their omega-3 fatty acid content as an additional benefit, which supports premium pricing. Furthermore, sunflower seed fiber is emerging as a cost-effective option for manufacturers aiming to diversify away from traditional grain sources, offering comparable bulking properties at 10% to 15% lower costs per kilogram.

Cereals and grains accounted for 49.01% of the sourcing share in 2025, supported by well-established wheat bran and oat fiber supply chains that benefit from co-product economics in flour milling and oat processing. However, this dominance is gradually declining as brands respond to gluten-avoidance trends and seek innovative narratives that cereals cannot provide. Fruits and vegetables contribute moderate but stable volumes, with apple fiber and citrus fiber valued for their water-binding properties in meat products and their clean-label appeal in organic formulations.

By Form: Liquid and Syrup Formats Capture Beverage and Dairy Fortification Demand

Liquid and syrup fiber forms are expected to grow at a compound annual growth rate (CAGR) of 13.01% from 2026 to 2031, making them the fastest-growing segment among fiber forms. This growth is attributed to beverage manufacturers focusing on ease of blending and consistent dispersion in high-speed production lines. Soluble corn fiber syrups, in particular, are replacing high-fructose corn syrup in reduced-sugar soft drinks and sports beverages. These syrups provide mild sweetness and fiber fortification without the viscosity challenges often associated with powder suspensions. Additionally, dairy processors are using liquid inulin in yogurt and kefir formulations to enhance creaminess while offering prebiotic functionality, which aligns with marketing strategies centered on gut health.

Powder formats accounted for 51.64% of sales in 2025, highlighting their versatility in dry-mix applications such as protein powders, baking mixes, and instant soups. These formats provide extended shelf life and simplified logistics compared to liquid alternatives. The growth of this segment is further supported by advancements in agglomeration and instantization technologies, which improve dispersibility and minimize clumping and sedimentation issues that have historically affected fiber-enriched beverages. Other forms, including granules and flakes, cater to niche applications like breakfast cereals and snack bars. These forms include visible fiber particles that enhance the perception of whole-grain authenticity and add textural appeal to the products.

By Application: Dietary Supplements Outpace Food and Beverage as Direct-to-Consumer Channels Expand

Dietary supplements are expected to grow at a compound annual growth rate (CAGR) of 12.45% from 2026 to 2031, surpassing the food and beverage market's growth rate of 9.2%. This growth is being driven by direct-to-consumer brands that are leveraging subscription models and personalized nutrition platforms to position fiber as a targeted wellness solution rather than a passive ingredient. Capsule and gummy formats are leading the market, with manufacturers combining multiple fiber types, such as psyllium, inulin, and glucomannan, to address common health concerns like constipation, weight management, and cholesterol reduction within a single product. Regulatory pathways for dietary supplements are less stringent compared to those for food health claims, allowing brands to make structure-function statements that suggest benefits without requiring the clinical substantiation needed for qualified health claims.

Food and beverage applications accounted for 48.02% of end-use value in 2025, with bakery and confectionery products leading this segment due to fiber's role in moisture retention and shelf-life extension. Dairy and frozen desserts are increasingly incorporating soluble fibers to reduce fat content while maintaining creaminess, which appeals to calorie-conscious consumers without compromising indulgence. Additionally, meat, poultry, and seafood processors are using insoluble fibers as binders and extenders, which help improve yield and texture in restructured products such as chicken nuggets and fish sticks.

Geography Analysis

North America accounted for 40.73% of global revenue in 2025, driven by a regulatory framework that allows qualified health claims for specific fibers and a consumer base focused on digestive wellness solutions. The United States leads in per-capita fiber supplement consumption, with established brands such as Metamucil and Benefiber maintaining strong retail positions. At the same time, challenger brands are gaining momentum through e-commerce and subscription-based models. In Canada, the 2024 update to its Food and Drug Regulations expanded the list of recognized dietary fibers, enabling brands to make fiber content claims for ingredients like resistant dextrin and polydextrose. This regulatory change has encouraged reformulation efforts across packaged food products [3]Source: Government of Canada, “List of Dietary Fibres Reviewed and Accepted by Health Canada’s Food Directorate,” canada.ca.

Asia-Pacific is expected to grow at a compound annual growth rate of 11.01% from 2026 to 2031, making it the fastest-growing region. This growth is supported by urbanization, rising disposable incomes, and government-led nutrition initiatives in countries such as China and India. China's Healthy China 2030 initiative emphasizes whole-grain consumption and increased fiber intake, prompting state-owned food enterprises to fortify staples like noodles and steamed buns with resistant starch and oat fiber. In India, the National Institute of Nutrition's 2024 dietary guidelines endorsed fiber-rich diets, influencing school meal programs and public distribution systems to incorporate millet and pulse flours, which are naturally high in fiber. In Japan, the aging population is driving demand for fiber supplements targeting constipation and cardiovascular health, with inulin and partially hydrolyzed guar gum leading sales in pharmacy and convenience store channels.

Europe's growth is moderated by stringent European Food Safety Authority (EFSA) health claim requirements and consumer skepticism toward novel fibers. However, the region remains an important market for organic and sustainably sourced ingredients. Germany leads in fiber consumption, supported by a cultural preference for whole-grain bread and a robust natural products retail sector that prioritizes fiber content in product offerings. France's Nutri-Score labeling system rewards fiber-rich products with higher scores, encouraging reformulation and providing a competitive advantage for brands that meet fiber content thresholds.

Competitive Landscape

The food fibers market shows moderate concentration, with the top five suppliers, including Cargill, Archer Daniels Midland, Tate and Lyle, Ingredion, and Roquette, accounting for approximately 45% of global capacity. Despite this, these companies face consistent competition from regional specialists who offer unique fiber sources such as acacia gum, konjac glucomannan, and ancient-grain fibers. Strategic trends highlight a clear divide in approaches. Large multinational companies focus on vertical integration by securing feedstock supply through long-term contracts with grain cooperatives and investing in proprietary extraction technologies to reduce costs and improve functionality. On the other hand, smaller players differentiate themselves by emphasizing organic certification, non-genetically-modified-organism (non-GMO) verification, and single-origin narratives, which help them achieve premium pricing in natural and specialty markets.

Opportunities are emerging in thermostable fibers that retain their functionality during retort and ultra-high-temperature processing. This innovation could address unmet needs in shelf-stable meal and infant formula applications, which are currently underserved by existing fiber options. Technology innovation remains a key competitive factor, with leading companies investing in enzymatic extraction, membrane filtration, and supercritical fluid processing. These methods produce fibers with neutral taste, high purity, and minimal environmental impact, attributes that appeal to both product developers and sustainability-focused procurement teams. For instance, Tate and Lyle's 2025 patent filing for a soluble fiber blend that remains stable at pH levels below 3.5 addresses a significant challenge in acidic beverages. This development could enable fiber fortification in carbonated soft drinks and fruit juices, which previously faced precipitation issues.

Additionally, emerging disruptors are utilizing precision fermentation to create novel polysaccharides with tailored molecular weights and prebiotic profiles. This technology has the potential to bypass agricultural supply chain volatility and ensure consistent year-round production. Compliance with International Organization for Standardization (ISO) 22000 food safety standards and voluntary certifications, such as Non-GMO Project Verified and United States Department of Agriculture (USDA) Organic, is increasingly becoming a baseline requirement for market access. This is particularly evident in North America and Europe, where retailer and consumer expectations for third-party validation have significantly intensified.

Food Fibers Industry Leaders

Ingredion Incorporated

Cargill, Incorporated

Tate & Lyle PLC

Archer Daniels Midland Company

Roquette Frères SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Layn launched Galacan, a beta-glucan product manufactured through precision fermentation at its biotech facility. The product offers improved functionality for supplements, foods, and beauty products.

- November 2024: Tate & Lyle completed its acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business. The combination enhances Tate & Lyle's portfolio with nature-based ingredients including pectin and citrus fibers, strengthening their position in clean-label and functional ingredient markets

- June 2024: Cargill Incorporation established a technology hub in Atlanta, Georgia, to focus on digital transformation in food and agriculture. The facility develops digital solutions to improve global food supply chain efficiency and sustainability, which affects fiber ingredient sourcing and distribution.

Global Food Fibers Market Report Scope

Food fiber, also referred to as dietary fiber, comprises compounds found in plants that are not fully digestible by the human gut. Commercially, fibers are extracted from fruits and vegetables and may be isolated or modified during processing. The food fibers market is categorized by type, source, form, application, and geography. By type, the market is divided into soluble and insoluble fibers. The soluble fibers segment includes inulin, pectin, polydextrose, beta-glucan, arabinoxylan, resistant maltodextrin, and other soluble fibers. The insoluble fibers segment comprises cellulose, hemicellulose, lignin, chitin and chitosan, resistant starch, and other insoluble fibers. By source, the market is segmented into cereals and grains, fruits and vegetables, nuts and seeds, and others. By form, the market is categorized into powder, liquid/syrup, and others. Based on application, the market is segmented into food and beverages, dietary supplements, and pharmaceuticals. Within the food and beverage application, the market is further segmented into bakery and confectionery, dairy, meat, poultry and seafood, beverages, and other food and beverage products. Geographically, the report analyzes key regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Soluble Fibers | Inulin |

| Pectin | |

| Polydextrose | |

| Beta-glucan | |

| Arabinoxylan | |

| Resistant Maltodextrin | |

| Other Soluble Fibers | |

| Insoluble Fibers | Cellulose |

| Hemicellulose | |

| Lignin | |

| Chitin and Chitosan | |

| Resistant Starch | |

| Other Insoluble Fibers |

| Cereals and Grains |

| Fruits and Vegetables |

| Nuts and Seeds |

| Others |

| Powder |

| Liquid / Syrup |

| Others |

| Food and Beverage | Bakery and Confectionery |

| Dairy and Frozen Desserts | |

| Meat, Poultry and Seafood | |

| Beverages | |

| Other Food and Beverages | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Animal Nutrition and Pet Food | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Soluble Fibers | Inulin |

| Pectin | ||

| Polydextrose | ||

| Beta-glucan | ||

| Arabinoxylan | ||

| Resistant Maltodextrin | ||

| Other Soluble Fibers | ||

| Insoluble Fibers | Cellulose | |

| Hemicellulose | ||

| Lignin | ||

| Chitin and Chitosan | ||

| Resistant Starch | ||

| Other Insoluble Fibers | ||

| By Source | Cereals and Grains | |

| Fruits and Vegetables | ||

| Nuts and Seeds | ||

| Others | ||

| By Form | Powder | |

| Liquid / Syrup | ||

| Others | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Dairy and Frozen Desserts | ||

| Meat, Poultry and Seafood | ||

| Beverages | ||

| Other Food and Beverages | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Animal Nutrition and Pet Food | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the food fibers market in 2031?

The food fibers market size is forecast to reach USD 15.99 billion by 2031.

Which region is growing fastest for food fibers sales?

Asia-Pacific posts the highest CAGR at 11.01%, driven by China and India.

Why are soluble fibers important in sugar-reduced products?

Soluble fibers replace sugar bulk, reduce calories, and add prebiotic benefits without raising glycemic load.

Which source category is expanding fastest?

Nuts and seeds lead growth at an 11.77% CAGR because they pair fiber with protein and healthy fats.

Page last updated on: