Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

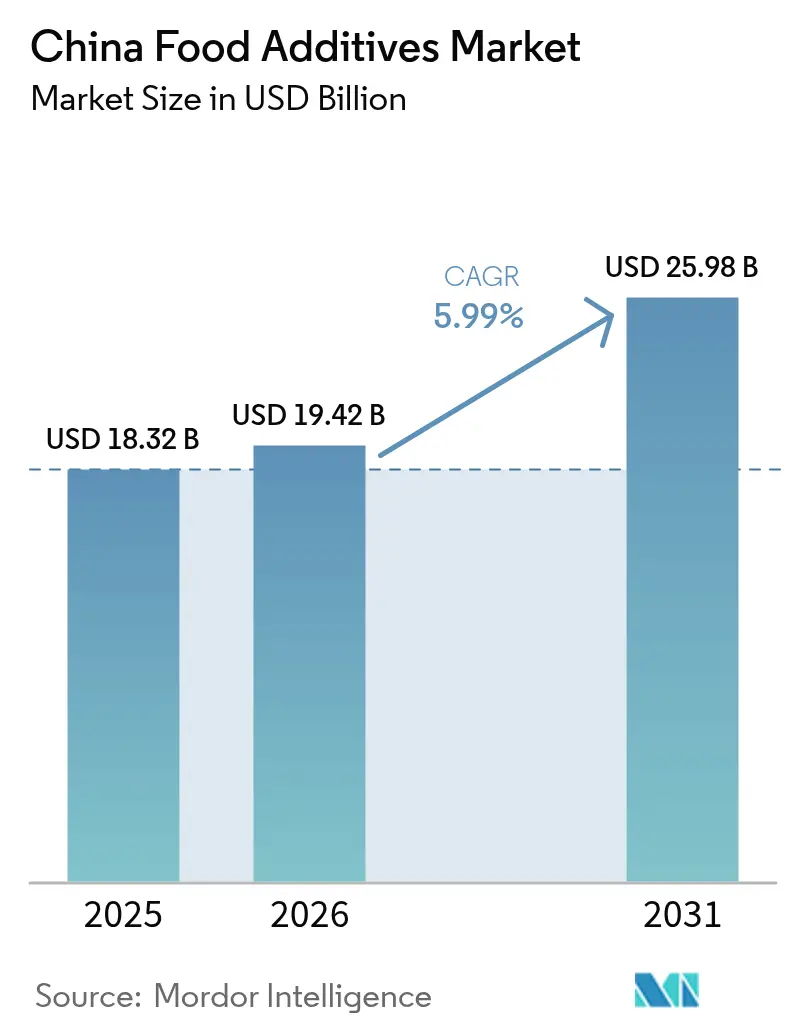

| Base Year Market Size (2025) | USD 18.32 Billion |

| Market Size (2026) | USD 19.42 Billion |

| Market Size (2031) | USD 25.98 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Food Additives Market Analysis by Mordor Intelligence

The China food additives market size was valued at USD 18.32 billion in 2025 and estimated to grow from USD 19.42 billion in 2026 to reach USD 25.98 billion by 2031, at a CAGR of 5.99% during the forecast period (2026-2031). Factors such as rapid urbanization, an expanding middle class, and a rising preference for packaged and convenience foods are driving significant changes in purchasing behaviors and spurring innovation in food ingredients. The introduction of GB 2760-2024 in February 2025 has not only redefined classifications and usage limits for additives but has also intensified reformulation efforts across the industry. This regulatory shift underscores the importance of compliance capabilities as a vital competitive edge for market players. Domestic leaders are leveraging their manufacturing scale to maintain dominance, while international suppliers are boosting local production capacities to align with stringent origin-labeling mandates. Additionally, investments from manufacturers are increasingly directed towards advanced technologies such as fermentation and biotechnology. These advancements are enabling the rapid development of natural, clean-label, and functional solutions that cater to the evolving preferences of health-conscious and informed consumers. The market's growth trajectory reflects a dynamic interplay of regulatory changes, technological advancements, and shifting consumer expectations.

Key Report Takeaways

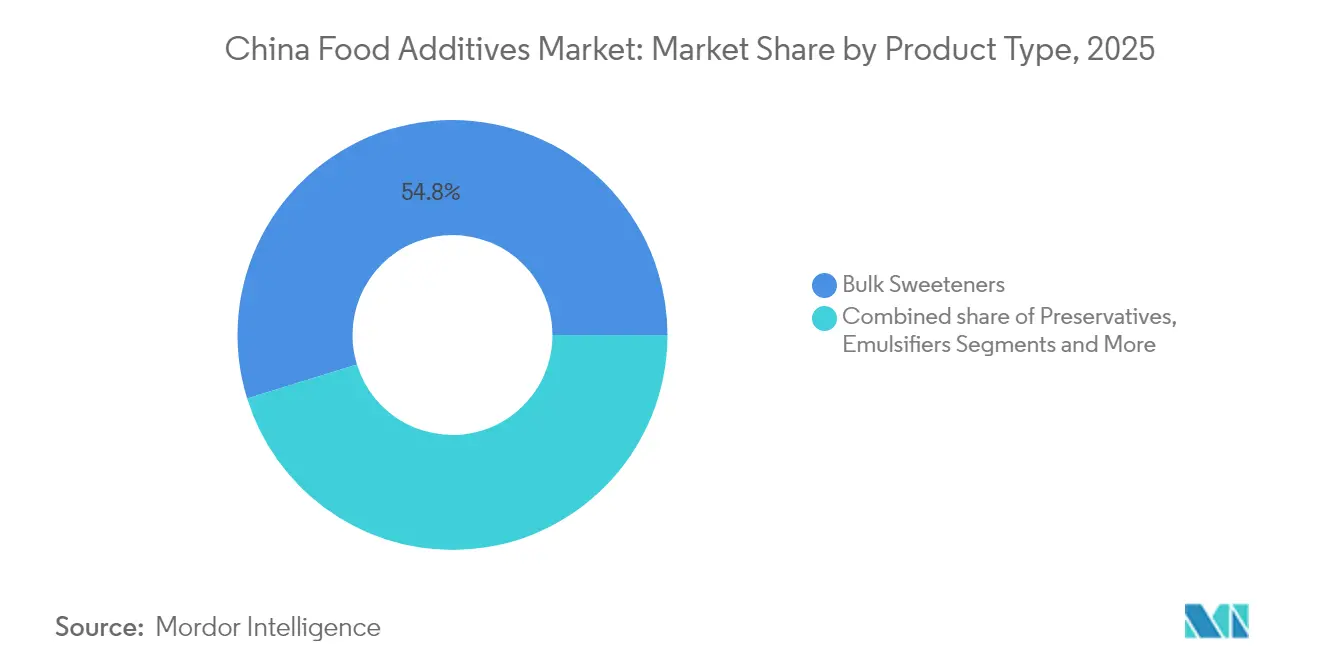

- By product type, Bulk Sweeteners led with 54.78% of the China food additives market share in 2025, while Food Colorants are projected to record the fastest 7.12% CAGR through 2031.

- By form, Dry additives accounted for 66.75% of the China food additives market size in 2025; Liquid formats are forecast to expand at a 6.74% CAGR to 2031.

- By source, Synthetic variants held 68.40% of the China food additives market share in 2025, whereas Natural sources are expected to grow at a leading 7.20% CAGR.

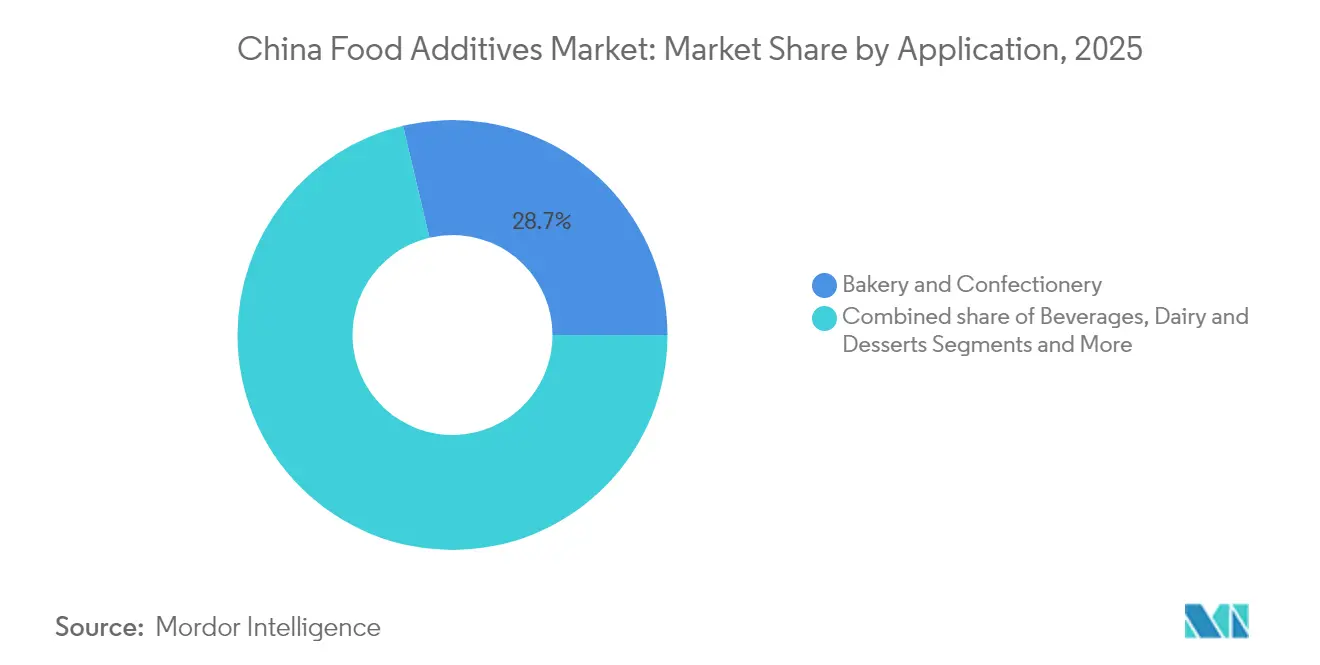

- By application, Bakery and Confectionery captured 28.70% of the China food additives market size in 2025, while Dairy and Desserts are set to advance at a 6.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Food Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Shelf Stable and Ready-to-Eat Foods | +1.2% | Tier-1 and Tier-2 cities, expanding to smaller urban centers | Medium term (2-4 years) |

| Consumer Inclination Towards Low-Calorie Diet Fuels Sugar Substitutes Additives | +0.9% | Beijing, Shanghai, Guangzhou, Shenzhen leading adoption | Short term (≤ 2 years) |

| Amplifying Demand for Natural and Clean-Label Food Additives | +1.5% | Coastal cities and affluent urban areas, gradual rural penetration | Long term (≥ 4 years) |

| Adoption of Advanced Technologies Reshaping Food Processing Industry | +0.8% | Industrial clusters in Shandong, Jiangsu, Guangdong provinces | Medium term (2-4 years) |

| Increasing Consumer Preference for Fortified and Functional Food and Beverages | +1.1% | Urban centers with health-conscious demographics nationwide | Medium term (2-4 years) |

| Rise in Traditional Medicine Beverages Using Natural Additives | +0.7% | Traditional medicine regions: Beijing, Guangzhou, Chengdu, expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Shelf Stable and Ready-to-Eat Foods

The growing demand for shelf-stable and ready-to-eat foods is fueling the market growth. This trend is fueled by the increasing urbanization, rising disposable incomes, and changing consumer lifestyles that prioritize convenience. According to the National Bureau of Statistics of China, the urbanization rate in China reached 66.16% in 2023, reflecting a steady increase in urban dwellers who often prefer ready-to-eat food options due to their busy schedules [1]National Bureau of Statistics of China, "Urbanization in China", www.stats.gov.cn. The shift in dietary habits, particularly among younger consumers, has further amplified the demand for processed and packaged foods. Additionally, the China Food Additives and Ingredients Association (CFAA) has reported a consistent rise in the production and consumption of food additives, driven by the expanding processed food industry. Food additives play a crucial role in enhancing the shelf life, flavor, texture, and nutritional value of ready-to-eat products, making them indispensable in meeting the evolving consumer preferences. These factors collectively contribute to the growing reliance on food additives to support the production of high-quality, convenient food products in the country.

Consumer Inclination Towards Low-Calorie Diet Fuels Sugar Substitutes Additives

The growing consumer preference for low-calorie diets is a key driver in the market, particularly in the sugar substitutes segment. The Chinese government has been actively promoting healthier dietary habits through initiatives such as the "Healthy China 2030" plan, which emphasizes reducing sugar consumption to combat rising obesity and diabetes rates [2]National Institute of Health, "The Tsinghua–Lancet Commission on Healthy Cities in China: unlocking the power of cities for a healthy China", www.pmc.ncbi.nlm.nih.gov. This initiative aligns with the increasing awareness among consumers about the adverse health effects of excessive sugar intake, further encouraging the shift toward sugar substitutes. Additionally, the China Food Additives & Ingredients Association (CFAA) has reported a steady increase in the production and adoption of sugar substitutes, driven by both consumer demand and regulatory support. The association highlights that advancements in food technology and the introduction of innovative sugar substitute products, such as stevia and erythritol, have also contributed to this growth. These factors are expected to sustain the growth of sugar substitute additives in the forecast period.

Amplifying Demand for Natural and Clean-Label Food Additives

The growing consumer preference for natural and clean-label food additives is a key driver of the China Food Additives Market. This trend is fueled by increasing health awareness, rising disposable incomes, and the demand for transparency in food labeling. Consumers are increasingly seeking products with recognizable and natural ingredients, avoiding artificial additives and preservatives. According to the National Bureau of Statistics of China, the country's food manufacturing industry witnessed a growth rate of 6.3% in 2023 [3]National Bureau of Statistics of China, "China Industrial Production", www.stats.gov.cn , reflecting the rising demand for healthier and more natural food products. Furthermore, the China Food Additives and Ingredients Association (CFAA) has reported a steady increase in the adoption of clean-label additives by food manufacturers, driven by consumer demand for minimally processed and chemical-free ingredients. This shift is further supported by government initiatives promoting food safety and quality standards, which encourage manufacturers to adopt natural and clean-label solutions. These factors are expected to continue influencing the market positively during the forecast period.

Adoption of Advanced Technologies Reshaping Food Processing Industry

The adoption of advanced technologies is significantly reshaping the food processing industry, acting as a key driver for the China Food Additives Market. The integration of automation, artificial intelligence (AI), and Internet of Things (IoT) in food processing has enhanced efficiency, reduced waste, and improved product quality. According to the Ministry of Industry and Information Technology (MIIT) of China, the food processing sector has seen a steady increase in technological investments, with a reported growth of 8% in automation-related expenditures in 2023. Additionally, the China Food Additives & Ingredients Association (CFAA) highlights that over 60% of food processing companies in China have adopted at least one form of advanced technology to streamline operations and meet rising consumer demands. These advancements are expected to continue driving the market during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concern Associated with Synthetic Sweeteners | -0.8% | Urban centers with health-conscious consumers, particularly tier-1 cities | Short term (≤ 2 years) |

| Higher Demand for Fresh and Organic Products | -0.6% | Affluent coastal cities and organic farming regions | Medium term (2-4 years) |

| Rising Consumer Skepticism Toward Food Additives Influences Market Dynamics | -0.9% | Educated urban populations nationwide, strongest in Beijing, Shanghai | Long term (≥ 4 years) |

| Government Regulation and Sugar Tax to Impact the Market Growth | -0.5% | National implementation with pilot programs in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concern Associated with Synthetic Sweeteners

Growing health concerns associated with artificial sweeteners is hindering the market growth. These synthetic sweeteners, often used as sugar substitutes, have been linked to various health issues, including metabolic disorders, increased risk of diabetes, and potential long-term effects on gut health. Studies have also suggested that excessive consumption of artificial sweeteners may disrupt the body's natural ability to regulate blood sugar levels, potentially leading to weight gain and other related health complications. Furthermore, there is ongoing debate regarding the carcinogenic potential of certain artificial sweeteners, which has further fueled consumer skepticism. As a result, consumers are becoming increasingly aware of these risks, leading to a shift in preference toward natural sweeteners and clean-label products. This trend is compelling manufacturers to reformulate their products, which could impact the market dynamics and growth potential during the forecast period. Additionally, regulatory scrutiny surrounding the use of artificial sweeteners is intensifying, with authorities imposing stricter guidelines and labeling requirements. These factors collectively pose challenges for the growth of artificial sweeteners within the food additives market in China.

Rising Consumer Skepticism Toward Food Additives Influences Market Dynamics

Rising consumer skepticism toward food additives is emerging as a significant market restraint. Consumers are increasingly concerned about the potential health risks associated with synthetic additives, such as preservatives, flavor enhancers, and artificial colorants. This growing awareness is driven by heightened access to information, regulatory scrutiny, and a preference for clean-label products. As a result, manufacturers are facing challenges in maintaining consumer trust while adhering to regulatory standards. The demand for natural and organic alternatives is rising, compelling companies to reformulate products and invest in research and development to meet evolving consumer preferences. This shift is reshaping market dynamics, influencing product innovation, and creating a competitive landscape where transparency and ingredient sourcing play a critical role in gaining consumer loyalty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bulk Sweeteners Dominates, Food Colorants Accelerates

In 2025, Bulk Sweeteners secured a dominant 54.78% share of the China food additives market, driven by the country's strong position in MSG and amino acid production. This leadership ensures a stable and consistent demand for bulk sweeteners, particularly in applications such as umami-rich condiments and convenience noodles. These products rely heavily on bulk sweeteners to enhance flavor profiles and meet consumer expectations for taste and affordability. Additionally, the growing popularity of processed and packaged foods in China further supports the demand for bulk sweeteners, as manufacturers seek cost-effective solutions to maintain product quality and appeal.

Food colorants in China's food additives sector are expanding at a notable 7.12% CAGR, fueled by increasing demand from artisanal bakeries and premium confectioners. These businesses are focusing on creating visually appealing, vibrant, and photo-ready products to attract consumers who value aesthetics alongside taste. Government initiatives promoting the use of botanical pigments are further accelerating this growth. Manufacturers are increasingly replacing synthetic colorants, such as tartrazine and sunset yellow, with natural alternatives like gardenia blue and beetroot red. This transition aligns with the rising consumer preference for clean-label products and natural ingredients, as well as the broader trend toward sustainability and health-conscious consumption. The growing adoption of natural food colorants is also supported by advancements in extraction and processing technologies, which ensure consistent quality and stability in food applications.

By Form: Dry Reigns Supreme, Liquid Gain Momentum

In 2025, dry forms hold a dominant 66.75% share of the market, reflecting their alignment with China's traditional food processing practices and cost-effectiveness. Their widespread use is attributed to several factors, including their storage stability across China's diverse climate conditions and their compatibility with conventional food processing methods. Dry forms are particularly suited for applications such as seasoning blends, dried food products, and other traditional culinary practices, which continue to play a significant role in the country's food industry.

On the other hand, liquid forms are experiencing a faster growth trajectory, with a projected CAGR of 6.74% through 2031. This growth is driven by the rapid expansion of China's beverage industry and the increasing adoption of automated processing technologies. Liquid forms are gaining traction due to their suitability for Western-style processed foods, which often require liquid-compatible additive systems. Additionally, the growing consumer preference for convenience and ready-to-consume products further supports the rising demand for liquid forms in the market.

By Application: Dairy Innovation Meets Traditional Preferences

In 2025, the bakery and confectionery sector accounted for 28.70% of the China food additives market. This significant share was driven by the growing café culture, which has been gaining popularity among younger demographics, and the increasing demand for confectionery products during regional festivals. Gifting traditions tied to these festivals further boosted the consumption of bakery and confectionery items, leading to a higher demand for food additives in this sector. Additionally, the expansion of artisanal bakeries and the introduction of innovative flavors and textures in confectionery products have contributed to the sector's growth.

The dairy and desserts sector is advancing at a 6.92% CAGR, supported by the rising consumer preference for premium yogurt and probiotic ice creams. These products are gaining traction due to their perceived health benefits and the growing trend of functional foods. The increasing focus on health-conscious choices among consumers has further propelled the demand for innovative and high-quality dairy and dessert products, driving the need for food additives in this segment. Furthermore, the introduction of plant-based and lactose-free dairy alternatives has expanded the consumer base, creating new opportunities for food additive applications. The growing influence of Western dessert trends and the rising popularity of indulgent yet health-oriented dessert options have also contributed to the sector's robust growth.

By Source: Natural Transition Reflects Cultural Values

In 2025, synthetic sources dominate the market with a significant 68.40% share. This dominance is largely driven by China's competitive edge in manufacturing, supported by low production costs and a well-established industrial infrastructure. The ability to produce synthetic sources at scale with consistent quality and reliability makes them a preferred choice across various industries. Additionally, synthetic sources offer greater control over production processes, ensuring uniformity and meeting the high demand for cost-effective solutions in both domestic and international markets. These factors collectively reinforce the stronghold of synthetic sources in the market.

Conversely, natural sources are emerging as the fastest-growing segment, with an impressive projected CAGR of 7.20% through 2031. This growth is fueled by a rising consumer inclination toward natural and organic products, particularly among urban populations. The increasing awareness of health and wellness, coupled with a shift toward sustainable and eco-friendly solutions, is driving demand for natural sources. Furthermore, the cultural alignment of natural sources with the principles of traditional Chinese medicine enhances their appeal, as consumers seek products that integrate holistic health benefits with cultural heritage. This trend underscores a broader movement toward sustainability and authenticity, positioning natural sources as a key growth driver in the market.

Geography Analysis

China, as one of the largest producers and consumers of food additives, benefits from its vast population, rapid urbanization, and evolving dietary habits. Eastern China, comprising Shanghai, Jiangsu, and Zhejiang provinces, dominates the market due to its concentrated food processing industries, advanced manufacturing infrastructure, and affluent consumer base with a preference for premium ingredients. Meanwhile, Northern China, led by Beijing and its surrounding provinces, represents the second-largest market. Its growth potential is driven by government policy influences, the integration of traditional medicine, and expanding food processing capabilities, making it a significant contributor to the overall market landscape. Additionally, the growing middle-class population in these urban areas has further amplified the demand for diverse and high-quality food products.

Government regulations and policies in China play a critical role in shaping the food additives market. The Chinese government has implemented stringent food safety standards, such as the Food Safety Law of the People’s Republic of China, which mandates strict quality control measures for food additives. These regulations have encouraged manufacturers to adopt advanced technologies and focus on producing safe and sustainable additives. For example, the government’s initiatives to reduce food waste have driven the demand for shelf-life-extending additives, while policies promoting clean-label products have spurred innovation in natural and organic additives. Local companies, such as Angel Yeast Co., Ltd. and Zhejiang NHU Co., Ltd., have responded to these regulatory changes by investing in research and development to meet both domestic and international standards.

Regional disparities within China also influence the market dynamics. Urban areas dominate the consumption of food additives due to their higher purchasing power and preference for convenience foods. In contrast, rural regions primarily drive the demand for basic additives used in staple food production, such as preservatives and stabilizers. However, the rural market is gradually evolving as infrastructure development and e-commerce penetration improve access to processed and packaged foods. This shift is creating new opportunities for manufacturers to expand their reach and cater to the growing demand for food additives across different regions of China.

Competitive Landscape

China's food additives market, scoring a 4 out of 10 on the concentration scale, reveals a highly fragmented competitive landscape. This score indicates that no single player holds a dominant position, and the market is characterized by the presence of numerous small to medium-sized companies operating across China. The fragmented nature of the market fosters intense competition among participants, driving innovation and diversification in product offerings to cater to the evolving demands of Chinese consumers. Companies in the country are consistently exploring ways to differentiate themselves in this competitive environment, focusing on product quality, pricing strategies, and customer engagement.

Additionally, the competitive environment in China encourages companies to focus on strategic partnerships, mergers, and acquisitions to strengthen their market presence and expand their reach within the domestic industry. Furthermore, the fragmented structure of the market creates opportunities for new entrants in China to establish themselves by offering niche or specialized products. Companies are also investing heavily in research and development to introduce advanced and sustainable food additives, aligning with the growing preference among Chinese consumers for healthier and environmentally friendly options.

The competitive dynamics in the country are further influenced by regulatory frameworks and government policies, which play a crucial role in shaping the strategies of market players. These regulations often focus on ensuring food safety and quality, compelling companies in China to adhere to stringent standards while maintaining cost efficiency. As a result, the market remains dynamic, with continuous shifts in competitive positioning and the emergence of innovative solutions to meet the diverse needs of the Chinese food and beverage industry. The interplay of these factors ensures that the market evolves rapidly, presenting both challenges and opportunities for stakeholders within China.

China Food Additives Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

BASF SE

-

DSM-Firmenich AG

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: At the 2025 Food Ingredients China exhibition, Louis Dreyfus Company (LDC), a top global merchant and processor of agricultural goods, unveiled its new line of plant-based Vitamin E products and broadened its food ingredients offerings.

- August 2024: Angel Yeast, a leading player in the yeast and biotechnology industry, inaugurated a probiotics production facility in Xizang. This expansion enhances its manufacturing capabilities for functional ingredients and underscores its commitment to the development of western China.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China food additives market as the total factory-gate value of ingredients intentionally incorporated into foods and beverages in mainland China to preserve, color, sweeten, texture, flavor, acidify, or catalyze processing. Coverage spans bulk and high-intensity sweeteners, preservatives, emulsifiers, hydrocolloids, enzymes, flavorings, and colorants supplied to processors, food-service blenders, and brand owners.

Scope exclusion: retail packs of table salt, culinary herbs, and commodity starches lie outside this boundary.

Segmentation Overview

-

By Product Type

- Preservatives

- Bulk Sweeteners

- Sugar Substitutes

- Emulsifiers

- Anti-Caking Agents

- Enzymes

- Hydrocolloids

- Food Flavors and Enhancers

- Food Colorants

- Acidulants

-

By Form

- Dry

- Liquid

-

By Source

- Natural

- Synthetic

-

By Application

- Bakery and Confectionery

- Dairy and Desserts

- Beverages

- Meat and Meat Products

- Soups, Sauces, and Dressings

- Other Applications

Detailed Research Methodology and Data Validation

Primary Research

Interviews with food formulators, procurement heads, regional distributors, and regulators across Beijing, Shanghai, Guangzhou, and Chengdu helped us validate average selling prices, gauge the pivot toward natural variants, and clarify enforcement timing for the new GB 2760-2024 standard. These direct conversations closed information gaps left by desk work.

Desk Research

Mordor analysts first assembled time-series from the National Bureau of Statistics of China, General Administration of Customs, FAOSTAT, UN Comtrade, and the China National Center for Food Safety Risk Assessment to map production, trade, and regulatory shifts. Company 10-Ks, Shanghai and Shenzhen filings, trade association white papers, and news archived on Dow Jones Factiva supplied price curves and competitive moves. Patent insights from Questel and shipment tallies on Volza flagged nascent categories. The sources named are illustrative; many additional public datasets were reviewed to verify figures and narratives.

Market-Sizing & Forecasting

A top-down construct converts official output plus net imports to retail-equivalent value, delivering the baseline value. Results are cross-checked through selective bottom-up supplier roll-ups; any segment deviating by more than three points is iteratively adjusted. Key variables include high-intensity sweetener penetration in sodas, natural colorant share in confectionery launches, ex-factory enzyme prices, beverage output, and per-capita packaged food spend. Multivariate regression blended with ARIMA smoothing projects demand with scenario buffers for sugar-tax and sodium-reduction policies.

Data Validation & Update Cycle

Outputs pass automated variance screening, peer audit, and sector-lead sign-off. Models refresh annually and reopen sooner if trade data or policy moves shift demand by over two percent, ensuring clients receive the latest view.

Why Mordor's China Food Additives Baseline Earns Trust

Published estimates diverge because firms differ on ingredient coverage, price progression, and refresh cadence. Narrow scopes, frozen exchange rates, or unchecked assumptions often understate recent inflation and the impact of GB 2760-2024.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.32 B (2025) | Mordor Intelligence | - |

| USD 12.13 B (2024) | Regional Consultancy A | Excludes enzymes and bulk sweeteners; currency fixed at 2023 average |

| USD 3.63 B (2022) | Trade Journal B | Relies on voluntary company disclosures; no import reconciliation |

The comparison shows that Mordor's disciplined variable selection, live price tracking, and yearly refresh provide a balanced, transparent baseline decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the China food additives market?

The market is valued at USD 19.42 billion in 2026.

How fast will the market grow over the next five years?

It is forecast to expand at a 5.99% CAGR, reaching USD 25.98 billion by 2031.

Which product category holds the largest market share?

Bulk Sweeteners lead with 54.78% of the China food additives market share in 2025.

Which application segment is growing fastest?

Dairy and Desserts will climb at a 6.92% CAGR through 2031, propelled by probiotic yogurt, flavored milk, and functional ice cream launches.

Page last updated on: