Vitamins Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

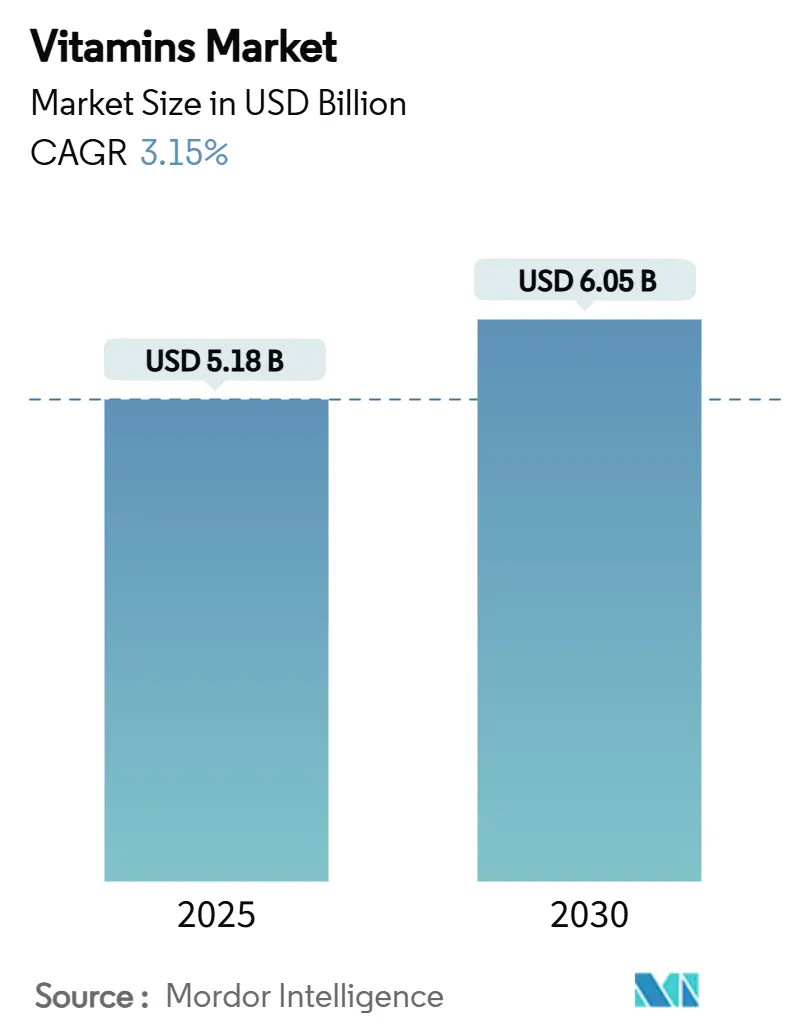

| Market Size (2025) | USD 5.18 Billion |

| Market Size (2030) | USD 6.05 Billion |

| Growth Rate (2025 - 2030) | 3.15% CAGR |

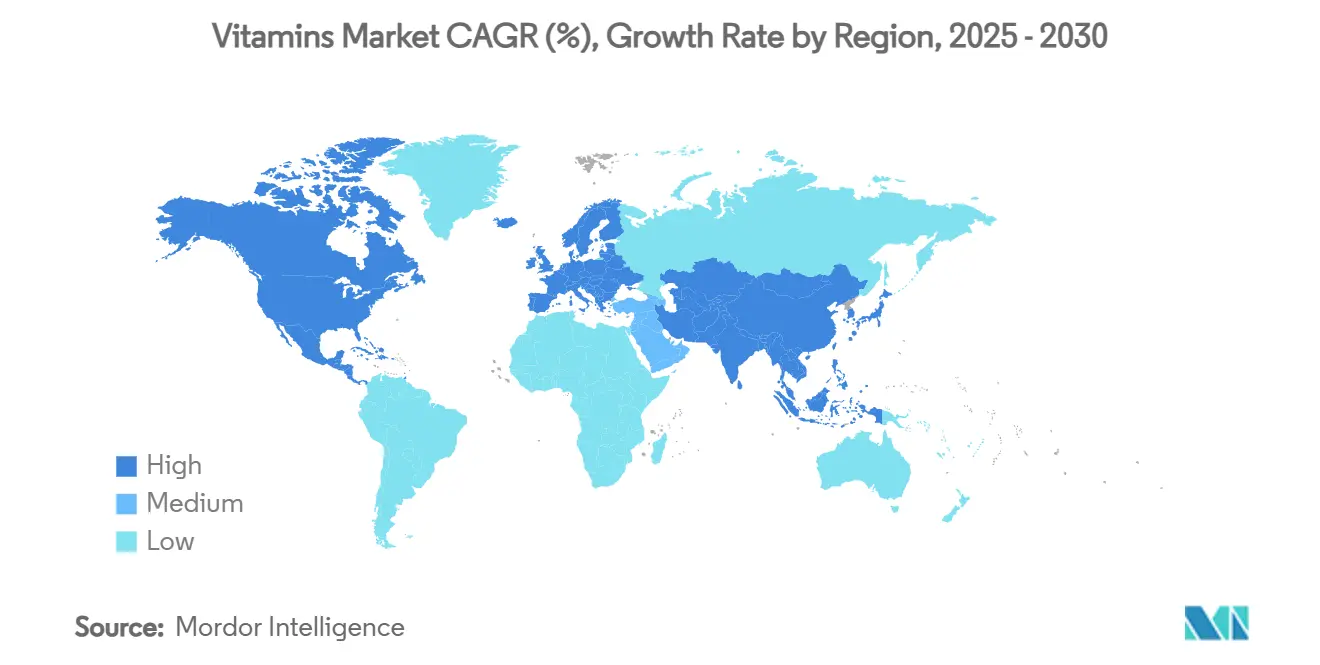

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

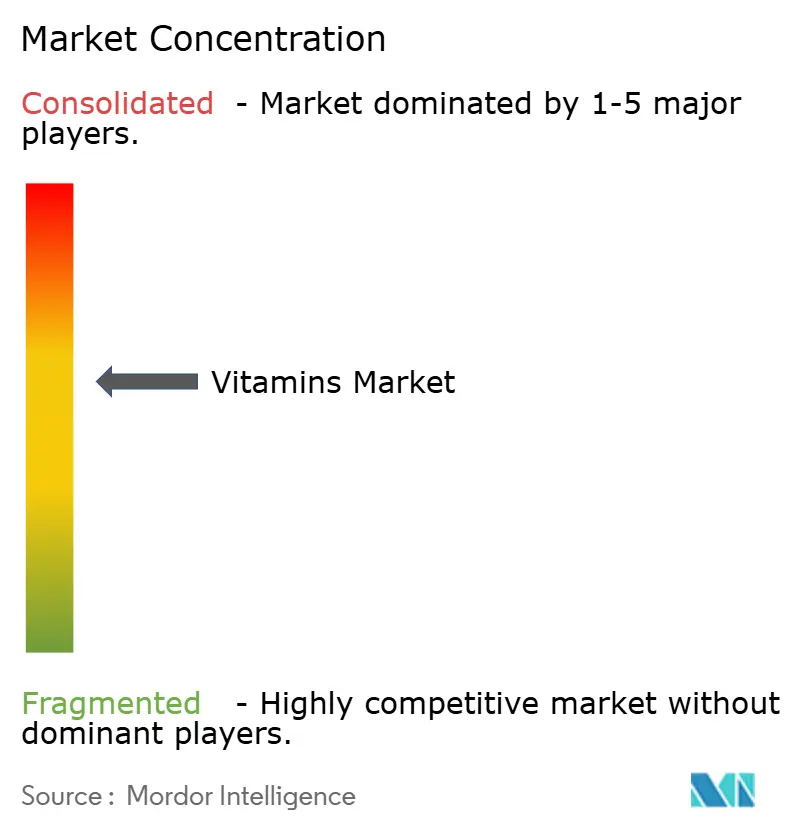

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vitamins Market Analysis by Mordor Intelligence

The vitamins market size is expected to grow from USD 5.18 billion in 2025 to USD 6.05 billion by 2030, at a CAGR of 3.15%. The market is transitioning from traditional volume-based sales strategies to sophisticated value-driven approaches through advanced biotechnology applications, precision fermentation techniques, and clean-label product development. Increased global regulatory oversight has compelled companies to implement comprehensive traceability systems and rigorous source authentication protocols. Premium products are gaining significant momentum, particularly in functional foods, beverages, and nutricosmetics segments, where consumers increasingly prioritize scientifically validated solutions for metabolic health optimization, immune system enhancement, and beauty-from-within applications. While supply chain consolidation continues across the industry, companies maintain robust innovation programs to address critical challenges, including bioavailability improvements, counterfeiting prevention measures, and sustainable raw material sourcing requirements.

Key Report Takeaways

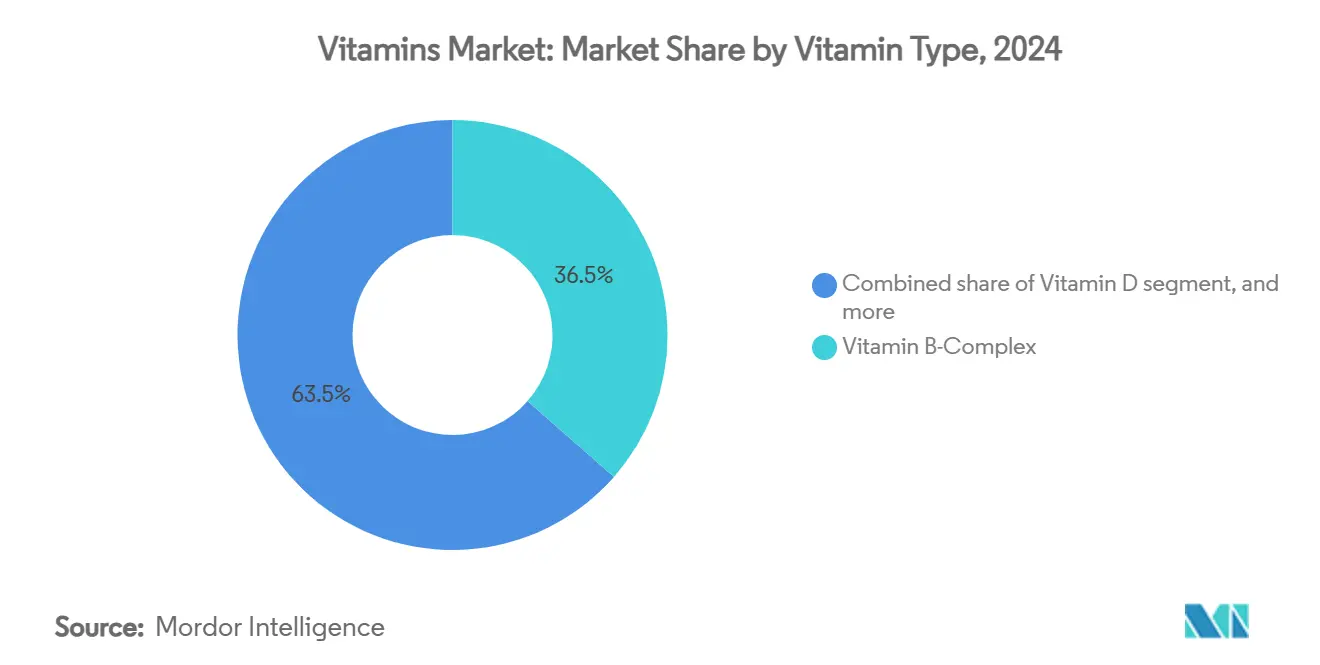

- By vitamin type, Vitamin B-complex held 36.48% of the 2024 vitamins market share, and Vitamin D is projected to grow at a 9.81% CAGR to 2030.

- By source, the synthetic segment captured 64.71% share in 2024, while natural sources are set to expand at an 11.28% CAGR through 2030.

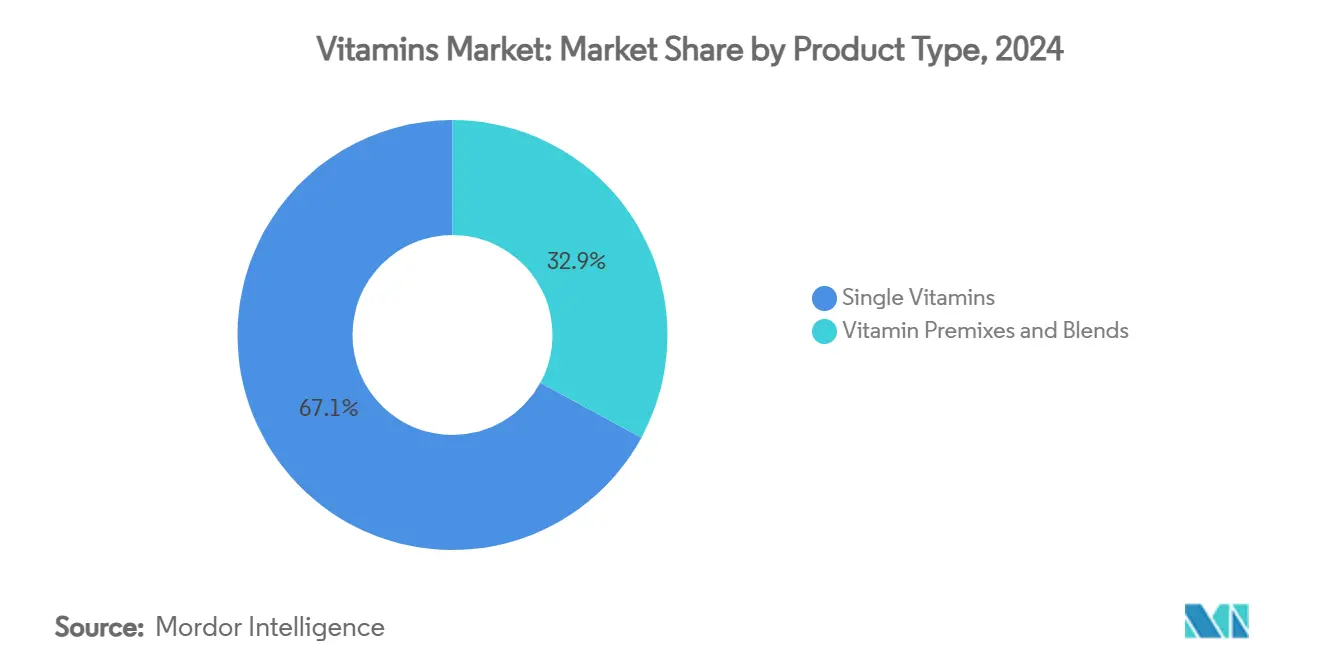

- By product type, the single-vitamins segment led with 67.08% share in 2024; vitamin premixes and blends are forecast to rise at a 7.89% CAGR over 2025-2030.

- By form, powders accounted for 71.23% share in 2024, and liquids are expected to advance at a 10.87% CAGR to 2030.

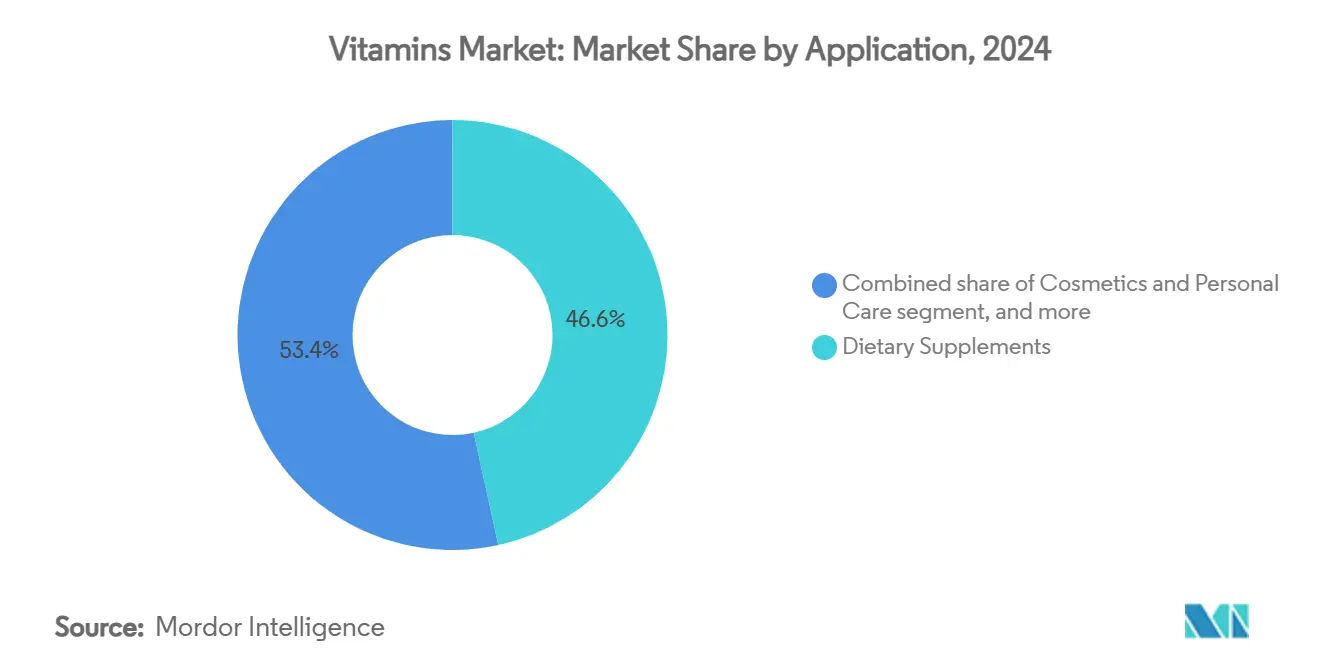

- By application, dietary supplements commandeda 46.58% share in 2024, whereas cosmetics and personal care applications are projected to post a 9.32% CAGR over the forecast period.

- By geography, Asia-Pacific dominated with a 37.48% share in 2024; the Middle East and Africa region is set to be the fastest climber at 8.08% CAGR to 2030.

Global Vitamins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of functional foods and beverages | +0.8% | Global, with strong momentum in North America and Europe | Medium term (2-4 years) |

| Rising focus on preventive healthcare | +0.6% | Global, particularly developed markets | Long term (≥ 4 years) |

| Growing Geriatric Population and Aging-Related Nutritional Needs | +0.5% | Global, with concentration in Japan, Europe, and North America | Long term (≥ 4 years) |

| Heightened Prevalence of Vitamin Deficiencies | +0.4% | Global, with higher impact in developing regions | Medium term (2-4 years) |

| Growing demand for anti-aging and beauty-from-within solutions | +0.3% | North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Government initiatives and fortification programs | +0.2% | Developing markets in Asia-Pacific, Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Functional Foods and Beverages

The global demand for vitamin ingredients, premixes, and customized nutrient solutions is increasing due to the shift toward functional foods and beverages. According to Glanbia Nutritionals' 2023 report, 72% of consumers prefer functional beverages with added health benefits, while 44% actively seek products with natural ingredients[1]Source: Glanbia Nutritionals, "European Functional Beverage Market Insights for 2023," glanbianutritionals.com. This trend creates opportunities for ingredient suppliers and contract manufacturers to support product innovation. New product launches globally are incorporating vitamins to target healthy aging, immunity, energy, and beauty-from-within trends. Gen Z and millennial consumers are driving this demand through their preference for vitamin-infused functional foods and beverages that align with their wellness objectives. Companies are expanding their product offerings to meet this demand. In October 2023, PLAYR1 introduced functional beverages containing vitamins, minerals, electrolytes, and pharma-grade nutraceuticals like vitamin B-complex, without artificial sweeteners, colors, or added sugars. These product launches are encouraging beverage manufacturers and food processors to work with B2B vitamin suppliers for high-quality, stable, and customizable vitamin solutions, contributing to market growth across the supply chain.

Rising Focus on Preventive Healthcare

Healthcare cost inflation and aging demographics are driving a shift toward preventive nutrition strategies, with vitamin supplementation emerging as a cost-effective intervention to reduce chronic disease risks. In 2023, the U.S. national health expenditure reached 17.6% of GDP, marking both a year-on-year increase and establishing the U.S. as the highest healthcare spender among developed nations relative to GDP. This economic pressure is compelling healthcare systems and policymakers to emphasize prevention over treatment, creating opportunities for vitamins as practical, scalable solutions. Medical endorsements are validating vitamin use in preventive medicine, transitioning it from discretionary wellness spending to essential healthcare, particularly important as healthcare systems manage limited resources. Employers are integrating vitamin supplementation into workplace wellness programs to reduce healthcare costs and improve workforce productivity. The post-pandemic health awareness has transformed vitamin supplementation from an optional lifestyle choice to a fundamental component of personal health management. These factors are increasing demand across the B2B vitamins supply chain, with manufacturers and ingredient suppliers working together to develop solutions that address this preventive health trend.

Growing Geriatric Population and Aging-Related Nutritional Needs

The growth of the global elderly population is a significant driver for the vitamins market, influencing nutritional demand patterns and consumer preferences. According to the World Economic Forum, the global population aged 65 and older is expected to reach 1.6 billion by 2050, doubling current figures, with Asia experiencing the most substantial demographic shift. Countries like South Korea, Hong Kong, and Japan are projected to have nearly 40% of their populations aged 65 or older by mid-century[2]Source: World Economic Forum, "The world's oldest populations," weforum.org. This demographic transformation is reshaping healthcare systems and nutritional supplement markets across these regions. The increasing elderly population correlates with higher rates of chronic conditions, including osteoporosis, cardiovascular disease, and cognitive decline, which have established nutritional links. Vitamins, including vitamin D, calcium, B-complex, and antioxidants, are essential for bone health, immunity, energy metabolism, and brain function. This has increased the demand for vitamin-enriched functional foods, beverages, and supplements designed for older adults. The growing awareness of preventive healthcare among the aging population has further strengthened the market for specialized vitamin formulations and age-specific nutritional products.

Heightened Prevalence of Vitamin Deficiencies

The global vitamins market continues to expand due to persistent vitamin deficiencies and undernutrition worldwide. In 2023, global undernourishment reached 9.1%, with Sub-Saharan Africa recording the highest rate at 23.2% of its population. These statistics highlight the need for nutritional interventions to address both direct deficiencies and "hidden hunger," where individuals consume adequate calories but lack essential micronutrients. The WHO's Vitamin and Mineral Nutrition Information System documents significant micronutrient deficiencies across developed and developing economies, supporting national and private-sector supplementation programs. Several factors contribute to these deficiencies, including indoor-focused work environments limiting vitamin D synthesis, increased consumption of processed foods, and restrictive dietary patterns. These elements create consistent market demand regardless of economic conditions. The increased availability of diagnostic testing has improved deficiency identification, increasing demand for therapeutic and maintenance supplementation. Healthcare professionals now recognize vitamin deficiencies as controllable risk factors for chronic diseases, leading to increased prescriptions and recommendations. These developments create significant B2B opportunities throughout the supply chain, as ingredient suppliers, contract manufacturers, and brand owners respond to the global demand for vitamin-enriched products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and adulterated products | -0.4% | Global, with concentration in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Supply chain disruptions and raw material shortages | -0.3% | Global, with particular impact on China-dependent supply chains | Medium term (2-4 years) |

| Short shelf life and stability challenges for specific vitamins | -0.2% | Global, affecting all market segments | Long term (≥ 4 years) |

| Consumer fatigue toward pill burden and vitamin skepticism | -0.1% | Developed markets, particularly North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Adulterated Products

The global vitamins market faces significant challenges from counterfeit and adulterated products, which undermine consumer confidence and create regulatory compliance issues. Despite enforcement efforts by regulatory bodies like the FDA, the extensive international counterfeiting networks continue to impact product integrity across markets. Regions with limited regulatory oversight, particularly in developing countries, face heightened risks. Price-sensitive consumers in these areas often purchase from unverified sources, increasing their exposure to unsafe or substandard products. The rise of e-commerce has further complicated this issue, as counterfeiters use sophisticated packaging and labeling techniques that make detection challenging for both consumers and distributors. The FDA's enhanced foreign facility inspection program represents one step toward strengthening market safeguards. However, the complex and global nature of vitamin supply chains creates ongoing enforcement challenges. Effective solutions require coordinated international regulatory efforts and implementation of traceability technologies, including serialization and blockchain systems.

Supply Chain Disruptions and Raw Material Shortages

The global vitamins market experiences significant challenges due to supply chain vulnerabilities and raw material constraints, leading to price volatility and market uncertainty. China's dominant position in vitamin production, particularly for vitamins C, E, and B-complex, makes the market susceptible to disruptions from geopolitical tensions, policy changes, and environmental regulations. The implementation of stricter environmental oversight in China has increased production constraints, while rising labor and shipping costs continue to affect supply economics and global pricing. The 2024 explosion and fire at BASF's Ludwigshafen facility disrupted global supplies of vitamins A, E, and carotenoids, with recovery beginning in 2025[3]Source: BASF, "BASF declares Force Majeure for selected vitamin A, vitamin E, and carotenoid products as well as selected aroma ingredients," basf.com. This incident demonstrated the market's vulnerability to concentrated production facilities by affecting multiple industries dependent on these micronutrients. Manufacturing incidents, including plant fires and maintenance shutdowns, continue to cause supply shortfalls and price increases, particularly in vitamin E markets. In response to these ongoing challenges, the American Feed Industry Association advocates for expanded domestic vitamin production to enhance supply chain resilience and stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vitamin Type: B-Complex Dominance Amid D-Vitamin Acceleration

Vitamin B-Complex holds 36.48% market share in 2024, maintaining its dominant position due to increased awareness of metabolic health and energy metabolism needs across various demographic groups. The segment's strength stems from its wide applications, ranging from basic nutrition supplements to specialized formulations for neurological and cardiovascular health. Vitamin D exhibits the highest growth potential with a projected CAGR of 9.81% through 2030, driven by deficiency awareness initiatives and research supporting its immune system benefits.

Vitamin C experiences market pressure from excess capacity and price competition, while Vitamin A production faces constraints from supply chain issues and regulatory requirements. Vitamin E prices remain unstable due to supply-demand gaps, with production limited to select global facilities. Vitamin K, though a smaller segment, shows growth potential in bone health applications and cardiovascular health research. The "Others" segment encompasses new vitamin forms and delivery systems that target bioavailability improvements, demonstrating the industry's shift toward enhanced product effectiveness over basic production.

By Source: Synthetic Stability Versus Natural Momentum

The synthetic source segment holds a 64.71% market share in 2024, supported by established manufacturing infrastructure, economies of scale, and significant cost advantages for large-scale applications across the pharmaceutical and food industries. The natural sources segment is growing at a CAGR of 11.28% through 2030, driven by increasing consumer demand for clean-label products, health consciousness, and premium positioning strategies in developed markets. Consumers demonstrate increased willingness to pay higher prices for natural products, despite similar bioavailability to synthetic alternatives, primarily due to perceived health benefits and environmental considerations.

Plant-derived natural vitamins gain market share due to sustainability benefits, lower environmental impact, and compatibility with vegetarian and vegan diets, while animal-derived sources face challenges from ethical consumption trends and growing concerns about industrial farming practices. The market distinction between synthetic and natural sources is shifting toward sustainable versus conventional production methods, as biotechnology advances enable natural classification through new manufacturing processes, including fermentation and bio-identical synthesis techniques.

By Product Type: Single Vitamins Lead While Premixes Accelerate

Single vitamin ingredients hold a dominant 67.08% market share in 2024, driven by the fundamental need for targeted nutritional interventions and therapeutic applications requiring precise dosing. This segment maintains its strong position as specific vitamin deficiencies and therapeutic needs continue to generate substantial demand, even amid the growing popularity of comprehensive nutrition solutions. Vitamin premixes and blends are projected to grow at a 7.89% CAGR through 2030, as manufacturers seek streamlined sourcing and formulation processes to reduce complexity and enhance quality control.

The premix segment's expansion is supported by the food and beverage industry's adoption of turnkey solutions that provide consistent fortification levels while minimizing formulation risks. Manufacturers use custom premix solutions to develop products with proprietary vitamin combinations targeting specific consumer needs, from immune support to cognitive health. DSM-Firmenich's focus on customized premix solutions exemplifies how industry leaders use formulation expertise to expand into higher-value market segments. The growth in personalized nutrition further strengthens the premix segment, as companies develop specialized formulations for specific demographic groups, health conditions, and lifestyle needs.

By Form: Powder Dominance Challenged by Liquid Innovation

Powder formulations hold a 71.23% market share in 2024, due to their superior stability, cost-effectiveness, and well-established manufacturing infrastructure that supports large-scale production. The powder segment's dominance stems from its versatility across multiple applications, from direct dietary supplementation to comprehensive food fortification programs, where product stability and extended shelf life are essential factors. The segment benefits from simplified storage requirements, reduced transportation costs, and efficient bulk handling capabilities.

Liquid formulations are growing at a 10.87% CAGR through 2030, driven by enhanced bioavailability requirements and increasing consumer demand for convenient administration formats. The liquid segment's expansion is particularly notable in pharmaceutical and cosmetic applications where rapid absorption and precise dosing are essential, especially in pediatric and geriatric markets where liquid forms are easier to consume. This growth is further supported by innovations in stabilization technologies and packaging solutions that extend product shelf life.

By Application: Supplements Dominate While Cosmetics Surge

Dietary supplements hold a 46.58% market share in 2024, representing the segment's established position and widespread consumer acceptance across age groups, income levels, and health consciousness levels. This dominance reflects vitamins' essential role in addressing nutritional deficiencies, supporting immune function, maintaining bone health, and promoting overall wellness. The cosmetics and personal care segment is expected to grow at a 9.32% CAGR through 2030, supported by the increasing demand for nutricosmetics that incorporate vitamins for skin health, hair vitality, nail strength, and anti-aging benefits.

The food and beverages segment expands through functional food trends, consumer preference for fortified products, and mandatory fortification requirements in several countries. The pharmaceutical segment utilizes vitamins in drug development, combination therapies, and specialized treatments for deficiency-related conditions. Animal feed and pet nutrition maintain steady growth, supported by premium pet food demand, increasing pet humanization trends, and the focus on optimizing livestock nutrition for improved productivity. Recent regulatory developments, such as the European Commission's approval of calcidiol monohydrate as a vitamin D source in food supplements, indicate continued support for new vitamin applications and formulations.

Geography Analysis

Asia-Pacific holds 37.48% market share in 2024, primarily due to China's manufacturing capabilities and India's growing consumer market supported by increased disposable incomes and health awareness initiatives. The region's manufacturing infrastructure includes advanced production facilities, quality control systems, and efficient supply chain networks. Consumer demand is further strengthened by rapid urbanization, increasing health consciousness, and evolving dietary preferences across major economies like Japan, South Korea, and Southeast Asian nations.

The Middle East and Africa region demonstrates the highest growth rate at 8.08% CAGR through 2030. This growth is driven by comprehensive government nutrition fortification programs, improved healthcare infrastructure, and increasing vitamin supplement adoption. The region's expansion is supported by strategic economic diversification initiatives, rising health awareness, and targeted public health programs addressing nutritional deficiencies across urban and rural populations.

North America and Europe maintain stable market positions with well-defined regulatory structures and established consumer bases. These regions focus on premium products, research-driven innovation, and specialized formulations. Market growth is sustained by aging populations, increasing emphasis on preventive healthcare, and growing demand for personalized nutrition solutions across different demographic segments. South America exhibits moderate growth potential through increasing economic development and an expanding middle class. The region's market development benefits from ongoing regulatory harmonization efforts, improved distribution networks, and enhanced manufacturing capabilities.

Competitive Landscape

The vitamin ingredients market demonstrates moderate consolidation, with a score of 6 out of 10. Established players maintain competitive advantages through vertical integration and technological innovation while facing competition from emerging biotechnology companies and regional manufacturers. The major players in the market include DSM-Firmenich, BASF SE, Foodchem International Corporation, Merck KGaA, and Glanbia PLC.

Companies like DSM-Firmenich and BASF SE maintain market leadership through extensive research and development investments, proprietary manufacturing processes, and strong distribution networks. The companies also benefit from economies of scale and long-standing relationships with key customers across the pharmaceutical, food, and dietary supplement industries. Market opportunities exist in personalized nutrition and precision fermentation technologies, where companies like Biosyntia and other biotechnology firms compete through innovative production methods and sustainable manufacturing.

These emerging players focus on developing bio-based alternatives to synthetic vitamins and improving production efficiency through advanced fermentation techniques. The market's shift toward application-specific solutions and enhanced bioavailability creates opportunities for companies that combine traditional vitamin manufacturing with advanced delivery systems and targeted therapeutic applications. This evolution is driven by increasing consumer demand for efficacious supplements and the growing incorporation of vitamins in functional foods and beverages.

Vitamins Industry Leaders

-

DSM-Firmenich

-

BASF SE

-

Foodchem International Corporation

-

Merck KGaA

-

Glanbia PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: At the 2025 Food Ingredients China trade show in Shanghai, Louis Dreyfus Company (LDC) introduced a new range of plant-based vitamin E products. The portfolio includes mixed tocopherols, acetate, and succinate derivatives to meet the growing demand for natural nutritional ingredients in China. The products serve multiple applications, including food additives, pharmaceuticals, and cosmetics, and provide improved bioavailability compared to synthetic alternatives.

- January 2024: DSM partnered with Azelis Pharmaceuticals and Healthcare to strengthen and expand Azelis Pharmaceuticals and Healthcare’s lateral value chain in India with DSM’s complete range of vitamins for use in pharmaceutical solutions.

- July 2023: BASF expanded its vitamin A formulation plant at the Ludwigshafen Verbund site. The company increased vitamin A acetate production capacity to 3,800 metric tons annually in July 2021 and completed the construction of a new formulation facility. The integration of this plant into the existing Verbund system, using digital testing tools and mobile devices, enables efficient operations and produces vitamin A powder for the animal nutrition market.

Global Vitamins Market Report Scope

| Vitamin A |

| Vitamin B-Complex |

| Vitamin C |

| Vitamin D |

| Vitamin E (incl. Tocopherols, Tocotrienols) |

| Vitamin K |

| Others |

| Synthetic | |

| Natural | Plant Derived |

| Animal Derived |

| Single Vitamin Ingredients |

| Vitamin Premixes and Blends |

| Powders |

| Liquids |

| Others |

| Food and Beverages |

| Dietary Supplements |

| Animal Feed and Pet Nutrition |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vitamin Type | Vitamin A | |

| Vitamin B-Complex | ||

| Vitamin C | ||

| Vitamin D | ||

| Vitamin E (incl. Tocopherols, Tocotrienols) | ||

| Vitamin K | ||

| Others | ||

| By Source | Synthetic | |

| Natural | Plant Derived | |

| Animal Derived | ||

| By Product Type | Single Vitamin Ingredients | |

| Vitamin Premixes and Blends | ||

| By Form | Powders | |

| Liquids | ||

| Others | ||

| By Application | Food and Beverages | |

| Dietary Supplements | ||

| Animal Feed and Pet Nutrition | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global vitamins market?

The vitamin ingredients market is valued at USD 5.18 billion in 2025.

Which vitamin type dominates the market?

Vitamin B-Complex leads with 36.48% market share in 2024.

Which source category is growing fastest?

Natural vitamin sources are forecast to expand at an 11.28% CAGR from 2025-2030.

Why are liquid vitamin formulations gaining popularity?

Liquids provide superior bioavailability and are easier to ingest for children and older adults, driving a 10.87% CAGR through 2030.

Page last updated on: