Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.75 Billion |

| Market Size (2026) | USD 10.14 Billion |

| Market Size (2031) | USD 12.35 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

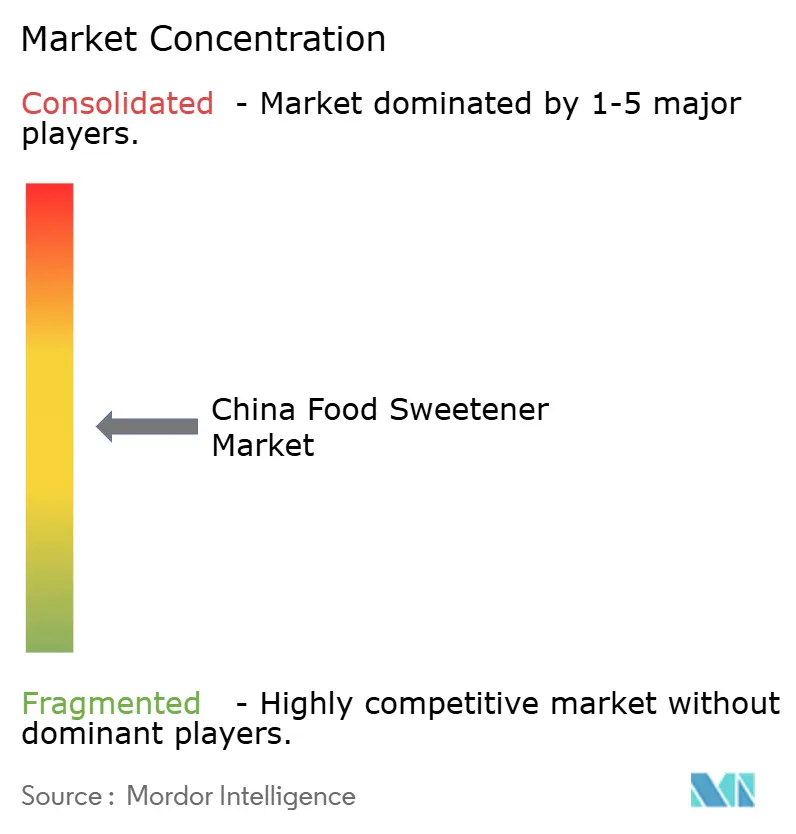

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Food Sweetener Market Analysis by Mordor Intelligence

The China food sweetener market size was valued at USD 9.75 billion in 2025 and estimated to grow from USD 10.14 billion in 2026 to reach USD 12.35 billion by 2031, at a CAGR of 4.02% during the forecast period (2026-2031). The market's growth trajectory is significantly influenced by regulatory measures, such as mandatory front-of-pack sugar labeling, which has intensified reformulation efforts across key segments like beverages and dairy products. Sucrose continues to dominate the market; however, the demand for high-intensity and plant-based sweeteners is rising rapidly. This shift is driven by increasing health concerns, particularly the rising prevalence of diabetes and obesity among the population. Both multinational corporations and domestic players are heavily investing in advanced technologies like precision fermentation to reduce production costs for rare sugars, including allulose. Additionally, the imposition of anti-dumping duties on erythritol has prompted producers to pivot their strategies toward manufacturing higher-margin sweeteners. Furthermore, the ongoing trends of urbanization and increasing disposable incomes are fueling consumer preferences for premium, clean-label products. These products emphasize the use of natural ingredients, aligning with the growing demand for healthier and more sustainable alternatives to synthetic sweeteners.

Key Report Takeaways

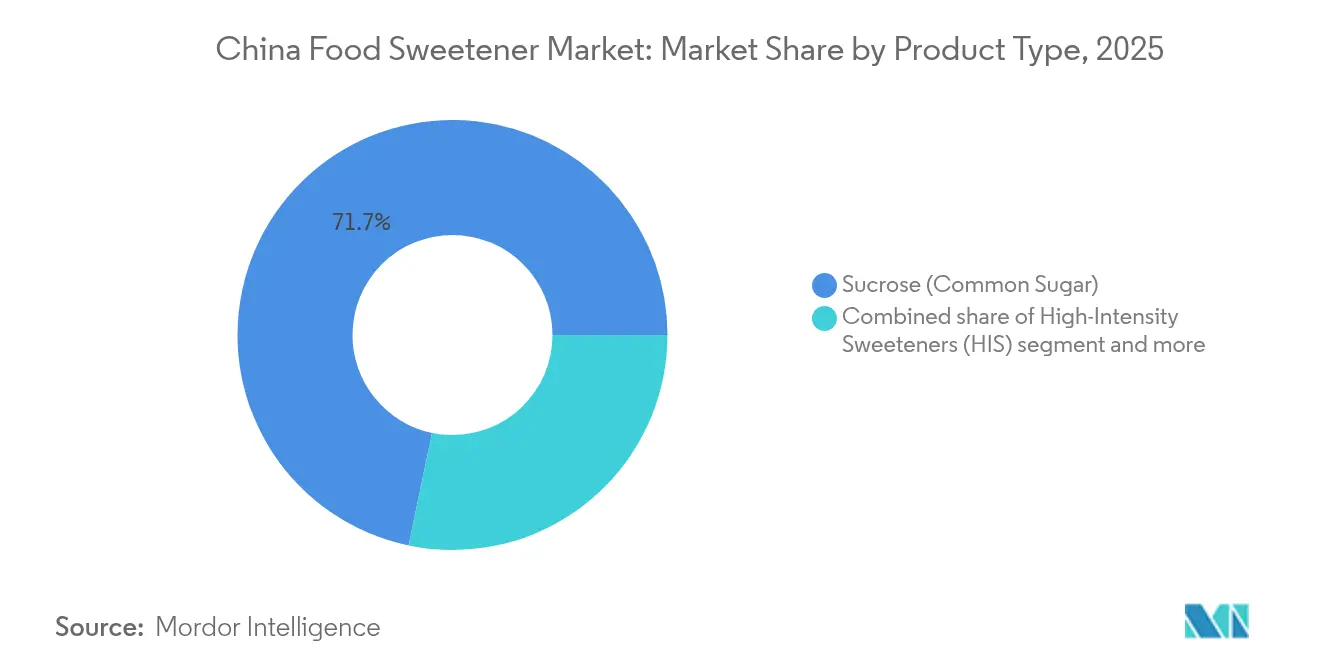

- By product type, sucrose led with 71.72% China food sweetener market share in 2025, while high-intensity sweeteners are forecast to expand at a 4.67% CAGR to 2031.

- By source, artificial sweeteners accounted for 77.12% of the Chinese food sweetener market in 2025, whereas plant-based variants are projected to grow at a 5.94% CAGR through 2031.

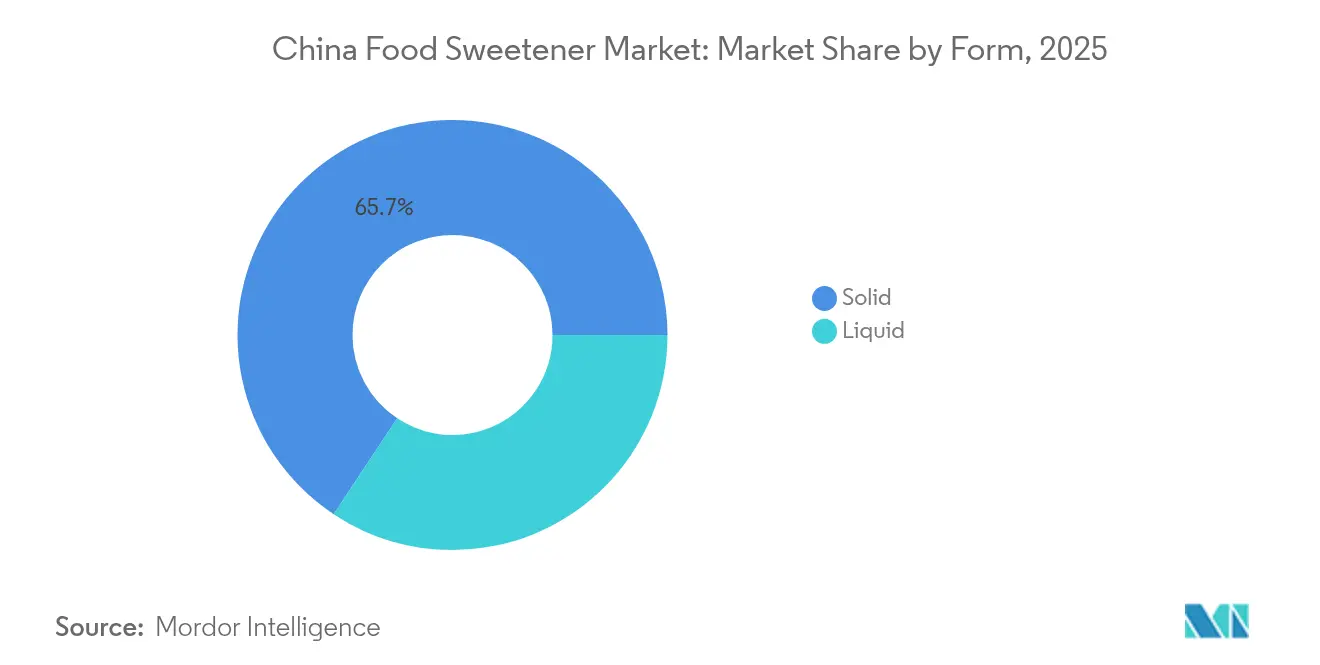

- By form, solid formats commanded 65.68% of 2025 revenue; liquid and syrup formats are advancing at a 4.94% CAGR on the back of beverage innovation.

- By application, food captured 60.93% of value in 2025, yet beverages are set to rise at a 5.66% CAGR and outpace all other end uses.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Food Sweetener Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of processed food and beverage categories | +1.2% | National, with concentration in tier-1 and tier-2 cities (Beijing, Shanghai, Guangzhou, Chengdu) | Medium term (2-4 years) |

| Rising diabetes and obesity spur demand for low-/no-calorie sweeteners | +0.9% | National, with higher prevalence in urban coastal regions | Long term (≥ 4 years) |

| Shift toward natural and clean-label ingredients | +0.8% | Tier-1 cities and affluent coastal provinces (Zhejiang, Jiangsu, Guangdong) | Medium term (2-4 years) |

| Easy availability to raw material | +0.5% | National, with corn-belt provinces (Heilongjiang, Jilin, Inner Mongolia) and stevia cultivation zones (Yunnan, Guizhou, Sichuan) | Short term (≤ 2 years) |

| Technological advancements in extraction and processing | +0.6% | National, with research hubs in Beijing, Shanghai, Shandong | Medium term (2-4 years) |

| Rising consumer preference for natural sweeteners | +0.7% | Tier-1 and tier-2 cities, expanding to tier-3 via e-commerce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of processed food and beverage categories

Categories such as bakery products, confectionery, dairy desserts, ready-to-drink teas, energy drinks, flavored waters, and functional beverages heavily depend on added sweeteners, driving an increase in overall sweetener usage. In 2024, China's food manufacturing industry generated USD 334.24 billion in revenue, as reported by the National Bureau of Statistics of China [1]Source: National Bureau of Statistics of China, "manufacture of foods", stats.gov.cn. The expansion of product lines by companies, through new flavors, varied pack sizes, or limited editions, requires unique sweetener blends or dosages for each iteration, further boosting sweetener demand even if per-capita consumption per SKU remains stable. Urbanization in China is raising per-capita incomes and increasing dining-out frequency, accelerating the consumption of processed food and beverages. Modern processed foods and drinks rarely rely solely on sucrose. Instead, formulators use a combination of sucrose, starch sweeteners, polyols, and high-intensity sweeteners (HIS) to balance taste, cost, texture, and caloric content, thereby expanding the market beyond basic sugar. This trend has created a growing demand for sweeteners that provide zero or low calories without compromising flavor. Swire Coca-Cola has noted this shift, reporting that its brands now include low- or no-sugar variants. This trend is not limited to beverages; bakery, dairy, and sauces categories are also reformulating their products to meet consumer expectations for reduced sugar, although challenges related to texture and shelf life persist.

Rising diabetes and obesity spur demand for low-/no-calorie sweeteners

China is prioritizing sugar reduction in its national health strategies due to the increasing prevalence of diabetes and obesity. According to the International Diabetes Federation, China will have approximately 148 million people living with diabetes in 2024, the highest number globally [2]Source: International Diabetes Federation, "IDF Diabetes Atlas - Eleventh Edition (2025)", idf.org. Public campaigns and media have raised awareness of sugar-related risks, prompting consumers to consider low- and no-calorie sweeteners as alternatives to sucrose, offering sweetness without the associated glycemic and caloric impact. The National Institute of Health projects that by 2025, 41% of Chinese adults will have a high BMI, with 9% classified as obese [3]Source: National Institute of Health, "Obesity and Occupational Disparities in Urban China", pmc.ncbi.nlm.nih.gov. As consumers increasingly associate long-term sugar consumption with obesity, they are showing a growing preference for plant-based and bio-converted sweeteners, which provide fewer calories and are perceived as more "natural." The government's "Weight Management Years" initiative (2024-2027) and the "Healthy China 2030" blueprint focus on reducing sugar consumption, requiring schools and public institutions to restrict high-sugar products in cafeterias and vending machines. Effective March 16, 2027, GB 28050-2025 will mandate front-of-pack sugar labeling, making it easier for consumers to identify high-sugar products and likely accelerating reformulation efforts. This trend highlights the importance of food-service channels in adopting low-calorie sweeteners. However, many smaller restaurants lack the technical expertise to reformulate recipes, creating a challenge that ingredient suppliers must address with comprehensive solutions.

Shift toward natural and clean-label ingredients

China's food sweetener market is undergoing a notable transformation. The market is shifting focus from traditional and artificial sweeteners to plant-based and easily recognizable alternatives, such as stevia, monk fruit, erythritol, and allulose. This trend not only drives volume growth but also underscores the growing importance of these alternatives. Stevia and monk fruit, both plant-derived, are promoted as clean, low-calorie options and are increasingly used in products marketed as "natural" or "better-for-you" in China and globally. Additionally, newer sugars like allulose and tagatose, which replicate sugar's taste while offering fewer calories and a lower glycemic impact, are rapidly gaining popularity. This growth follows their regulatory approval in China, particularly in sugar-free beverages and diabetic-friendly foods. Food and beverage manufacturers are actively reformulating existing products and creating new ones, including sugar-free drinks, low-sugar confectionery, and high-protein snacks, by utilizing natural or clean-label sweeteners. These efforts align with regulatory sugar-reduction objectives and reinforce brand commitments. Although these clean sweeteners represent a smaller share of the total sweetener volume, their premium positioning significantly boosts market revenue and profit margins. As global and Chinese brands incorporate these sweeteners into beverages, dairy, and baked goods, what was once a niche segment is now becoming mainstream. This development signifies a structural shift in growth patterns, moving away from conventional sugars and older synthetic sweeteners.

Technological advancements in extraction and processing

Precision fermentation and enzymatic conversion are driving down production costs and enhancing taste profiles for next-generation sweeteners. Continuous fermentation systems have significantly reduced sucralose production costs, while synthetic biology is expected to lower allulose production costs. CRISPR and gene-editing technologies are being utilized to improve stevia plants, increasing yields of desirable steviol glycosides. In 2024, Ingredion introduced its ENLITEN stevia sweetener, enabling up to a 95% reduction in sugar content in formulations. Additionally, Cargill launched its Asia-Pacific Innovation Center in Shanghai in 2024 to expedite the development of sweetener blends tailored to regional taste preferences. Enzymatic conversion methods are also expanding the applications of steviol glycosides. For example, GB 2760-2024, effective February 8, 2025, permits enzyme-produced steviol glycosides in modulated milk powder (0.3 grams per kilogram), processed cheese (0.4 grams per kilogram), and instant rice or flour (0.4 grams per kilogram). These incremental regulatory approvals indicate a shift toward natural sweeteners replacing synthetic alternatives in categories where taste and clean-label claims command premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety perceptions and skepticism toward artificial sweeteners | -0.4% | National, with stronger impact in tier-1 cities and affluent coastal regions | Medium term (2-4 years) |

| Regulatory complexity and compliance burden for plant-based sweeteners | -0.3% | National, affecting all manufacturers seeking novel ingredient approvals | Long term (≥ 4 years) |

| Technical and formulation challenges | -0.2% | National, with greater impact in bakery, confectionery, and dairy applications | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.3% | National, with concentration in corn-belt provinces and stevia cultivation zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Safety perceptions and skepticism toward artificial sweeteners

Although large meta-analyses have found no significant link between artificial sweetener consumption and cancer risk, many Chinese consumers remain skeptical. They associate sweeteners like aspartame, saccharin, and cyclamate with potential long-term health risks, such as cancer and gut issues. Social media discussions, occasional recalls of artificial additives, and news about safety reviews have heightened these concerns. Consequently, some consumers are avoiding these "chemical" sweeteners in favor of sugar or perceived "natural" alternatives. While China's food safety authorities have confirmed that common artificial sweeteners, like aspartame, are safe when used within national standards, these assurances have not fully alleviated consumer doubts. This disconnect between official statements and public skepticism has prompted brands to act cautiously. Many have limited their messaging on artificial sweeteners and, in some cases, have removed them from products targeting health-conscious consumers. This perception gap poses a strategic challenge for manufacturers: reformulating with natural sweeteners increases ingredient costs by 50-150%. However, ignoring consumer concerns risks losing market share to competitors emphasizing clean-label products. Social media further exacerbates the issue, as influencers and health bloggers frequently cite incomplete or outdated studies, making it challenging for brands to counter misinformation with credible, peer-reviewed evidence.

Regulatory complexity and compliance burden for plant-based sweeteners

Regulatory complexities and compliance burdens hinder China's food sweetener market by causing delays, increasing costs, and creating uncertainties for manufacturers aiming to launch or expand plant-based sweeteners. Although the approval process for stevia derivatives, monk fruit extracts, and similar bio-converted products has accelerated, it still requires extensive safety data, stability studies, and production documentation. This requirement has slowed their market penetration compared to more established sweeteners. Effective February 8, 2025, GB 2760-2024 will impose combined maximum limits on specific sweeteners, forcing manufacturers to reformulate products that previously relied on single-sweetener solutions. For example, the combined use of aspartame, acesulfame-K, and aspartame methyl ester will be restricted to specified thresholds, requiring companies to invest in analytical testing and reformulation trials. Approvals for novel food ingredients add further delays: D-allulose, after years of review, will be approved on July 2, 2025, while stevia polyphenols will gain approval in February 2025 with a maximum daily intake of 500 mg. Smaller manufacturers, often lacking regulatory expertise and financial resources, face significant challenges navigating these approval pathways. This situation creates a barrier to entry that benefits multinational ingredient suppliers with established government relationships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sucrose Dominance Masks High-Intensity Sweetener Surge

Sucrose accounted for a significant 71.72% share of the market in 2025, highlighting its established role in traditional Chinese sweets, baked goods, and home cooking. However, high-intensity sweeteners are anticipated to grow at a 4.67% CAGR through 2031, driven primarily by beverage reformulation. Among these sweeteners, stevia is gaining popularity due to its clean-label attributes. In contrast, sucralose remains a key ingredient in carbonated soft drinks and flavored waters because of its stability under acidic pH levels and high-temperature processing. Saccharin and cyclamate, once prevalent in lower-tier markets, are declining as consumers shift toward stevia and monk fruit. Neotame and acesulfame-K are predominantly used in blended systems to mitigate off-notes.

Dextrose and maltodextrin function as bulking agents in reduced-sugar products. Despite health-related concerns, high-fructose corn syrup (HFCS) continues to be widely used in processed foods, with China expected to lead in HFCS consumption growth among major markets. Sorbitol and xylitol are commonly used in sugar-free chewing gum and diabetic-friendly confections, but their laxative effects at higher doses limit broader adoption. The "Others" category includes emerging alternatives like monk fruit extract and allulose. While these options are gaining traction in premium product lines, their growth is constrained by supply limitations and high costs.

By Source: Artificial Sweeteners Retain Lead as Plant-Based Variants Accelerate

Artificial sweeteners, including sucralose, aspartame, and acesulfame-K, accounted for a dominant 77.12% market share in 2025. These sweeteners offer a cost advantage of 50-70% compared to natural alternatives and deliver reliable performance across various applications. Meanwhile, plant-based sweeteners are expected to grow at a 5.94% CAGR through 2031, driven by increasing consumer demand for clean-label ingredients and recent regulatory approvals for innovative plant-derived options. For instance, the National Health Commission approved stevia polyphenols in February 2025, establishing a maximum daily intake of 500 mg. Additionally, in December 2024, the commission expanded the use of steviol glycosides produced through enzymatic conversion. Companies such as Guilin Layn and Sunwin Stevia are scaling up the production of high-purity stevia extracts, while Sweegen is commercializing fermentation-derived Reb M and Reb D steviol glycosides, which effectively eliminate the bitter aftertaste associated with earlier stevia formulations.

Fermentation and bio-engineered sweeteners, though still in the early stages, represent a strategically significant segment. These sweeteners utilize synthetic biology to produce rare sugars like allulose and tagatose at lower costs than traditional extraction methods. For example, D-allulose received novel food ingredient approval on July 2, 2025, and synthetic biology is anticipated to further reduce production costs. While artificial sweeteners are projected to retain their majority market share through 2031 due to their cost and performance benefits, the growth momentum favors plant-based and fermentation-derived sweeteners. This trend is particularly evident in premium product lines, where clean-label claims support higher pricing.

By Form: Solid Sweeteners Dominate, Yet Liquids Gain in Beverages and E-Commerce

In 2025, solid sweeteners accounted for 65.68% of the market, highlighting their preference in bakery, confectionery, and tabletop applications, where ease of handling and shelf stability are essential. Granulated sucrose, powdered erythritol, and blended sweetener sachets dominate retail channels, while industrial users rely on bulk bags for large-scale production. Liquid and syrup variants are projected to grow at a 4.94% CAGR through 2031, driven by beverage reformulations and the increasing e-commerce distribution of concentrated sweetener drops for home use. Liquid sweeteners provide better dispersion in cold beverages and eliminate the need for dissolution, streamlining production and reducing energy costs. High-fructose corn syrup (HFCS) remains the leading liquid sweetener in processed foods, with China expected to experience the highest growth in HFCS consumption among major markets.

E-commerce platforms like Tmall and JD.com are driving the popularity of liquid stevia and monk fruit concentrates for home use, as consumers add drops to coffee, tea, and yogurt to customize sweetness levels. Solid sweeteners are expected to retain their majority share due to their versatility and well-established supply chains. However, liquids are anticipated to grow faster, particularly in the beverage and food-service sectors, where quick dissolution and ease of dosing are critical. Blended liquid sweetener systems, such as 60% sucralose, 20% stevia, and 20% erythritol, are emerging as a preferred solution for taste optimization, though they introduce challenges in formulation and ingredient sourcing.

By Application: Food Segment Leads, Yet Beverages Drive Faster Growth

In 2025, the food segment accounted for 60.93% of the market share, covering bakery and confectionery, dairy and desserts, meat and savory products, nutraceuticals and functional foods, as well as sauces, dressings, and spreads. Sucrose continues to be the preferred sweetener in traditional Chinese confections like mooncakes, tangyuan, and candied fruits due to its critical role in texture, browning, and moisture retention, which are challenging to replicate with alternatives. The bakery sector faces specific hurdles: sugar not only imparts sweetness but also contributes to bulk, crust color, and crumb structure. Replacing it with high-intensity sweeteners requires the addition of bulking agents such as maltodextrin or polydextrose, which increases costs and complicates formulations.

Yogurt manufacturers are reformulating quickly, leveraging consumers' willingness to pay a premium for "low sucrose" and "no sucrose" options. Ice cream producers encounter technical difficulties, as sweeteners impact viscosity, freezing points, and melting behavior. To address this, they use blended systems to replicate sucrose's sensory attributes. Nutraceuticals and functional foods, including protein bars, meal replacements, and vitamin-fortified snacks, are increasingly adopting sugar-free formulations. Ingredients like stevia, monk fruit, or erythritol are being used to align with health-conscious consumer preferences. The beverage sector is projected to grow at a 5.66% CAGR through 2031, driven by the demand for sugar-free tea, wellness waters, and carbonated soft drinks. To meet the growing preference for zero-sugar options, carbonated soft drink manufacturers are reformulating their offerings. For instance, Coca-Cola launched the limited-edition Coca-Cola Oreo Zero Sugar in China in 2024, while Swire Coca-Cola reported increased sales of low-sugar tea beverages.

Geography Analysis

China's sweetener consumption shows significant regional differences, shaped by income levels, dietary habits, and the influence of Western food trends. Tier-1 cities such as Beijing, Shanghai, Guangzhou, and Shenzhen are at the forefront of adopting sugar-free and low-sugar products. Health-conscious consumers in these cities are willing to pay extra for clean-label ingredients. In tier-2 cities like Chengdu, Hangzhou, and Wuhan, demand is growing rapidly. Rising incomes and increased e-commerce penetration are making premium sweeteners more accessible, though consumers in these markets remain more price-sensitive than those in tier-1 cities. Meanwhile, tier-3 and lower-tier cities continue to favor traditional sugar. However, growing awareness of diabetes and obesity risks is gradually influencing consumer behavior. E-commerce platforms like Tmall and JD.com are helping bridge the gap between urban and rural areas by delivering liquid stevia and monk fruit concentrates directly to consumers, encouraging experimentation with these newer formats.

Coastal provinces such as Zhejiang, Jiangsu, and Guangdong are early adopters of Western food trends, including sugar reduction, due to their higher per-capita incomes and greater exposure to international brands. In southern China, particularly Guangdong and Fujian, there is a cultural preference for sweeter beverages and desserts, leading to higher per-capita sweetener consumption compared to northern regions. In contrast, northern China's food culture is more focused on savory flavors, resulting in lower sweetener usage in traditional dishes. However, urbanization and Western influences are gradually diminishing these regional differences. Inland and western provinces like Sichuan, Yunnan, and Guizhou are emerging as key areas for stevia cultivation. Local governments are offering subsidies to farmers transitioning from traditional crops to stevia, which provides higher margins and requires less water. This vertical integration is reducing China's reliance on stevia leaf imports from Paraguay and India, although smaller growers face challenges in maintaining consistent quality.

The government's "Weight Management Years" initiative (2024-2027) and GB 28050-2025, which requires front-of-pack sugar labeling starting March 16, 2027, are accelerating reformulation efforts across the country. Schools and public institutions in tier-1 cities have already restricted high-sugar products in cafeterias and vending machines, setting an example likely to influence lower-tier markets. However, enforcement varies by province, with wealthier coastal regions implementing stricter compliance than inland areas. Regional taste preferences also play a role in sweetener selection: northern consumers prefer less-sweet profiles, making stevia and monk fruit more appealing, while southern consumers often require blended sweeteners to match the sweetness intensity of traditional sugar. These regional differences complicate national product launches, pushing manufacturers to develop regional variants or risk underperformance in key markets.

Competitive Landscape

The Chinese food sweetener market is moderately fragmented, with multinational companies like Cargill Incorporated, Tate and Lyle Plc, Sunwin Stevia International, Inc., Archer Daniels Midland Company, and Ingredion Corporation competing alongside domestic players such as Baolingbao Biology, Shandong Futaste, Guilin Layn, and Zhucheng Haotian. The high-intensity sweetener segment is even more fragmented. Shandong Futaste leads in acesulfame-K production, Guilin Layn specializes in stevia extracts, and global companies like Ingredion and Sweegen are advancing fermentation-derived Reb M and Reb D steviol glycosides to overcome taste issues associated with earlier stevia versions. Companies are increasingly adopting vertical integration strategies, such as Baolingbao's investment in upstream corn processing to secure feedstock, along with horizontal diversification.

Fermentation-derived rare sugars, including allulose, tagatose, and D-psicose, which received regulatory approvals in 2025, represent significant opportunities. These sugars offer taste profiles closer to sucrose compared to synthetic alternatives. To meet growing consumer demand for non-caloric natural sweeteners, companies are innovating in stevia-based products. Additionally, market players are focusing on research and development to introduce sustainable and organic sweeteners, driving market growth further.

Emerging disruptors include fermentation startups utilizing synthetic biology to produce steviol glycosides and rare sugars at lower costs than traditional extraction methods. Precision fermentation is expected to significantly reduce allulose production costs. Furthermore, CRISPR and gene-editing technologies are being employed to optimize stevia plants for higher yields of desirable steviol glycosides. Technology remains the key differentiator in capturing market share. Companies capable of delivering natural sweeteners with superior taste profiles at competitive prices are likely to dominate premium product segments, while those relying on traditional synthetic sweeteners risk margin compression as consumer preferences shift toward clean-label options.

China Food Sweetener Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Incorporated

-

Sunwin Stevia International, Inc.

-

Ingredion Incorporated

-

Tate and Lyle Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Cargill has invested USD 4 million to expand its Shanghai innovation center, increasing its size to 3,000 square meters and equipping it with advanced technology to drive food innovation in China.

- May 2024: Tate and Lyle Plc has partnered with Chinese stevia farmers. Together, they are implementing a science-led program to promote sustainable stevia farming practices and reduce its environmental impact. This initiative also supports the Dongtai community.

- July 2022: Sweegen Inc launched Bestevia LQ, a collection of liquid stevia-based sweeteners. the sweeteners are designed to use in carbonated soft drinks, confectionery items, liquid sweeteners, dessert toppings, and concentrated fruit/flavored syrup. the company claims that the product meets the regulatory standards for countries in the Asia-Pacific.

China Food Sweetener Market Report Scope

By Product Type

| Sucrose (Common Sugar) | |

| Starch Sweeteners and Sugar Alcohols | Dextrose |

| High-Fructose Corn Syrup (HFCS) | |

| Maltodextrin | |

| Sorbitol | |

| Xylitol | |

| Erythritol | |

| Other Sugar Alcohols | |

| High-Intensity Sweeteners (HIS) | Sucralose |

| Aspartame | |

| Saccharin | |

| Neotame | |

| Stevia | |

| Acesulfame-K | |

| Cyclamate | |

| Other HIS | |

| Others |

By Source

| Artificial |

| Plant-based |

| Fermentation/Bio-engineered |

By Form

| Solid |

| Liquid/Syrup |

By Application

| Food | Bakery and Confectionery |

| Dairy and Desserts | |

| Meat and Savory Products | |

| Nutraceuticals and Functional Foods | |

| Sauces, Dressings and Spreads | |

| Other Processed Foods | |

| Beverages |

| By Product Type | Sucrose (Common Sugar) | |

| Starch Sweeteners and Sugar Alcohols | Dextrose | |

| High-Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Sorbitol | ||

| Xylitol | ||

| Erythritol | ||

| Other Sugar Alcohols | ||

| High-Intensity Sweeteners (HIS) | Sucralose | |

| Aspartame | ||

| Saccharin | ||

| Neotame | ||

| Stevia | ||

| Acesulfame-K | ||

| Cyclamate | ||

| Other HIS | ||

| Others | ||

| By Source | Artificial | |

| Plant-based | ||

| Fermentation/Bio-engineered | ||

| By Form | Solid | |

| Liquid/Syrup | ||

| By Application | Food | Bakery and Confectionery |

| Dairy and Desserts | ||

| Meat and Savory Products | ||

| Nutraceuticals and Functional Foods | ||

| Sauces, Dressings and Spreads | ||

| Other Processed Foods | ||

| Beverages | ||

Key Questions Answered in the Report

What is the 2026 value of the China food sweetener market?

It is valued at USD 10.14 billion in 2026.

How fast will low-calorie beverage sweetener demand grow?

Beverage applications are forecast to rise at a 5.66% CAGR through 2031.

Which segment leads the market by source?

Artificial sweeteners held 77.12% of 2025 revenue.

Why is allulose gaining interest among manufacturers?

D-allulose won novel-food approval in July 2025 and can now be used in beverages, bakery, and confectionery.

Page last updated on: