China Chemical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

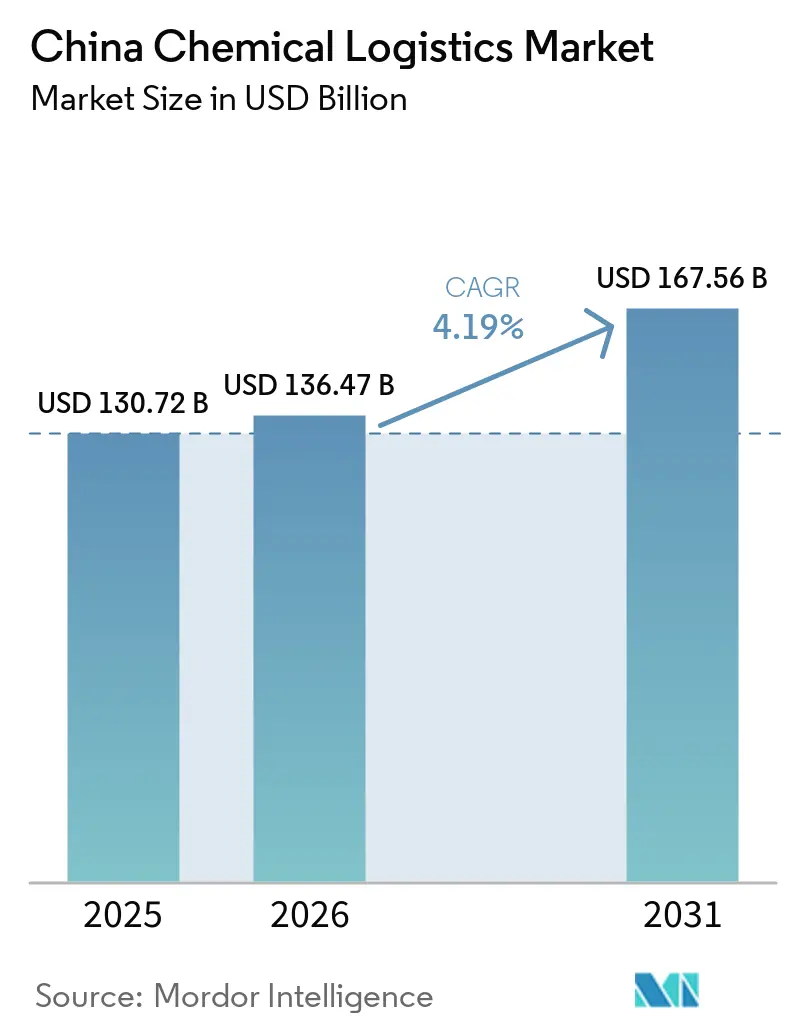

| Base Year Market Size (2025) | USD 130.72 Billion |

| Market Size (2026) | USD 136.47 Billion |

| Market Size (2031) | USD 167.56 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

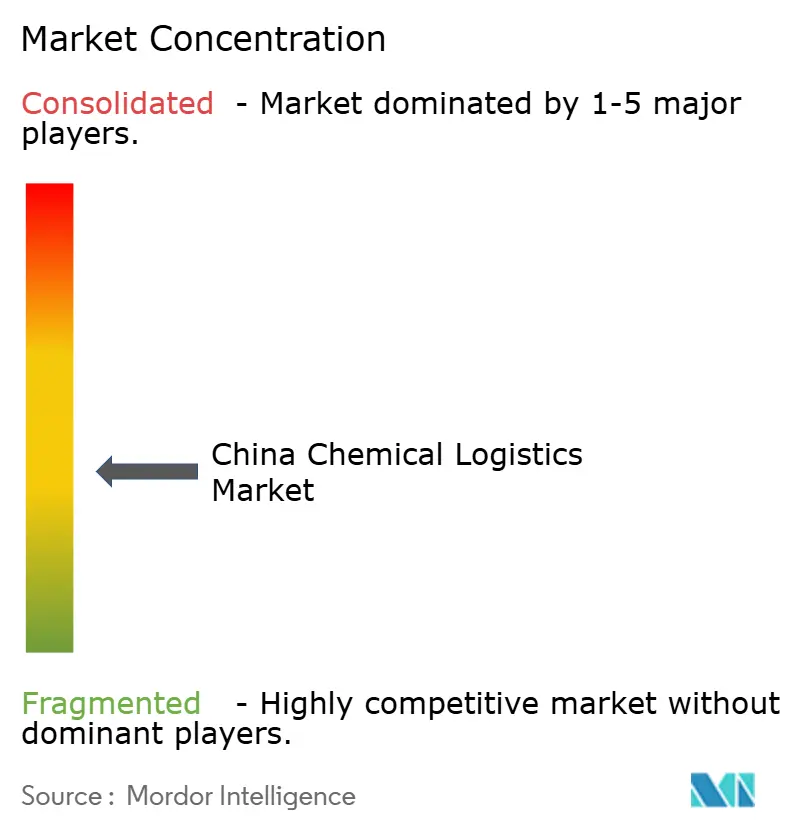

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Chemical Logistics Market Analysis by Mordor Intelligence

The China chemical logistics market size is projected to be USD 130.72 billion in 2025, USD 136.47 billion in 2026, and reach USD 167.56 billion by 2031, growing at a CAGR of 4.19% from 2026 to 2031.

The China chemical logistics market remains anchored by heavy transport assets because specialized tank trucks, coastal tankers, rail wagons, and multimodal links still determine service reach and operating scale. Demand is also staying concentrated in hazardous cargo because downstream petrochemicals and battery materials require compliant handling, traceability, and route discipline across long domestic corridors. The China chemical logistics market is also shifting toward higher-precision services as pharmaceutical cold-chain requirements and specialty-chemical quality controls pull investment into temperature-controlled storage and monitored distribution. Regulatory tightening in 2026 is raising the cost of non-compliance, which is favoring larger operators that already have digital controls, licensed fleets, and safer operating networks. At the same time, the inland shift in petrochemical production and the need for road, rail, river, and coastal switching are creating fresh expansion room for operators that can serve western and central lanes with consistent compliance and multimodal execution.

Key Report Takeaways

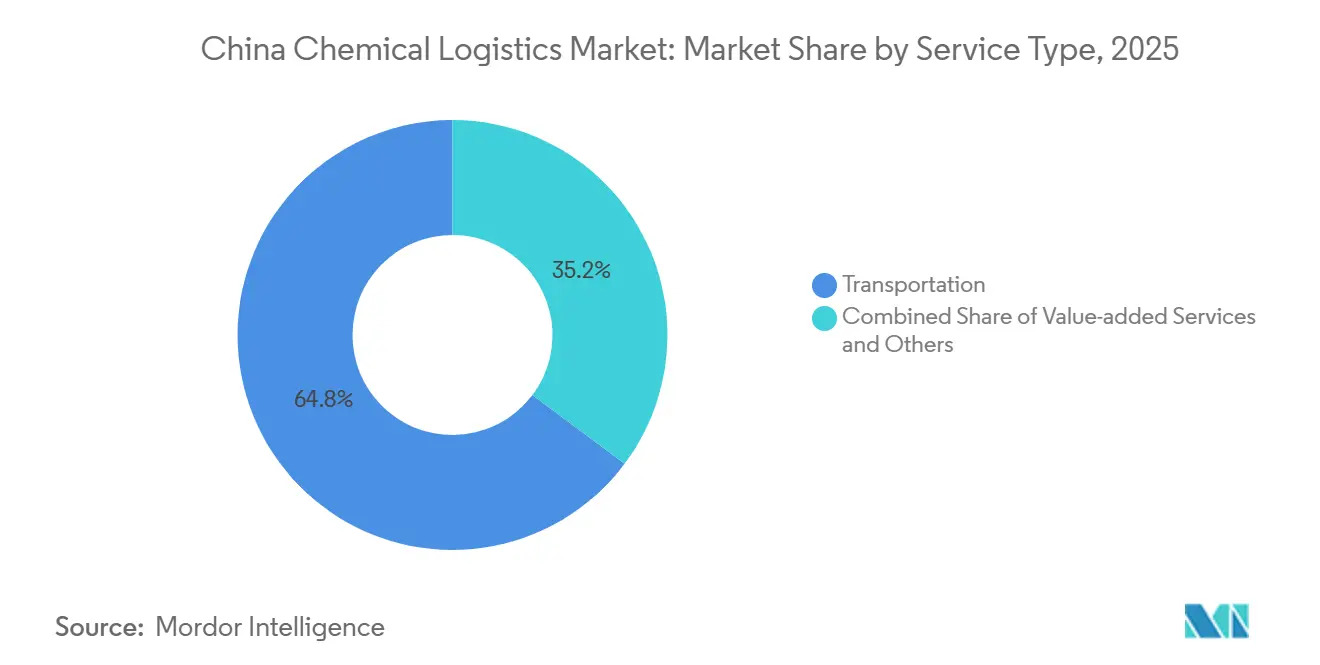

- By service type, transportation accounted for 64.77% of China chemical logistics market size in 2025, while value-added services and others recorded the highest projected CAGR at 7.31% through 2031.

- By hazard class, hazardous chemicals held 66.5% of the China chemical logistics market share in 2025 and also posted the fastest projected CAGR at 6.19% through 2031.

- By temperature control, non-temperature-controlled logistics accounted for 71.5% of China chemical logistics market share in 2025, while temperature-controlled handling advanced at the highest projected CAGR of 7.33% through 2031.

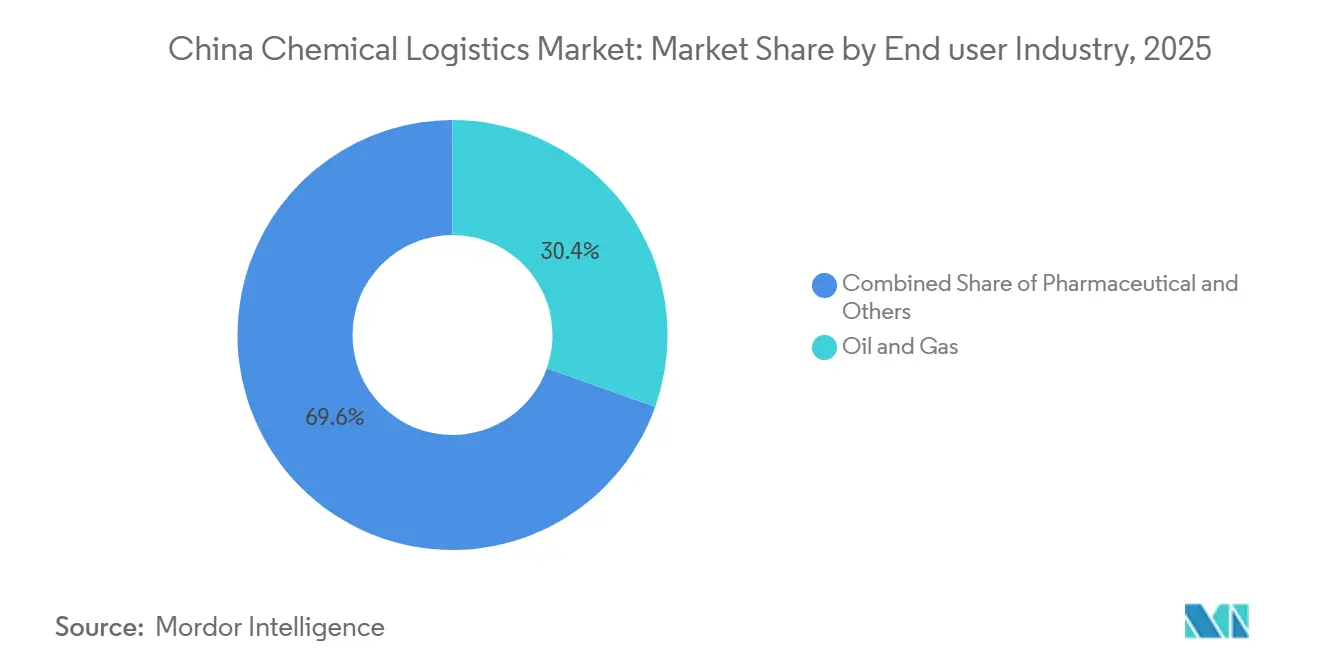

- By end-use industry, oil and gas captured a 30.41% share of China chemical logistics market size in 2025, while pharmaceuticals registered the fastest projected CAGR at 7.64% through 2031.

- By region, East China accounted for 24.1% of revenue in 2025, while Southwest China recorded the highest projected CAGR of 5.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Chemical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sino-EU dangerous-goods transport accords easing cross-border compliance | +0.3% | North China, East China, and Europe rail and sea corridors | Short term (≤ 2 years) |

| Petrochemical capacity west-to-east shift boosting domestic lane volumes | +0.8% | Northwest, Central, and Southwest China | Medium term (2-4 years) |

| E-commerce demand for specialty packaging chemicals | +0.4% | East China, South China | Short term (≤ 2 years) |

| IMO 2026 decarbonization targets are forcing fleet renewal of chemical tankers | +0.5% | Coastal China, including Shanghai, Tianjin, Guangzhou, and Ningbo | Medium term (2-4 years) |

| Beijing-Tianjin-Hebei Haz-Chem One-Permit pilot reducing administrative costs | +0.2% | North China, including Beijing, Tianjin, and Hebei | Short term (≤ 2 years) |

| Growth of lithium-ion battery recycling clusters in Southwest China | +0.6% | Southwest China, including Sichuan, Yunnan, and Guizhou, with spillover to Central China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Capacity West-To-East Shift Boosting Domestic Lane Volumes

The China chemical logistics market is being reshaped by the shift of petrochemical capacity from coastal clusters toward inland and western provinces. Coal-to-chemicals investments in Xinjiang, Ningxia, Shaanxi, and Sichuan are boosting long-haul domestic shipments of methanol, ethylene glycol, aromatics, and acetic acid. Existing East China logistics systems were built more around import and export flows, so they are less efficient for these inland-origin domestic lanes. The Jiangling Petrochemical Terminal at Wuhan Port is a direct response to that change because it adds a large public petrochemical node on the upper-middle Yangtze and connects more inland output with eastern demand centers[1]Source: Baird Maritime, “Wuhan Port's New Petrochemical Terminal Opens, Boosting Chemical Storage Capacity,” Baird Maritime, bairdmaritime.com. Hebei's 2025 push to prioritize 60 chemical projects worth CNY 201 billion (USD 27.8 billion) shows that inland chain extension is not limited to western China and is also building a northern vector for new freight demand. As that production map changes, the China chemical logistics market is placing a premium on operators that can combine river, rail, and road movements on a single service platform rather than rely solely on coastal port-based freight networks.

IMO 2026 Decarbonization Targets Forcing Fleet Renewal of Chemical Tankers

The China chemical logistics market is also being driven by a fleet renewal cycle tied to IMO decarbonization and vessel-efficiency standards. Guangzhou Shipyard International delivered the first of 4,74,500-dwt LR1 chemical and product tankers ahead of schedule in 2025, and the vessels met EEDI Phase 3 requirements while also reserving dual-fuel conversion capability. Nanjing Tanker Corporation also ordered 3 methanol-ready 6,600-dwt stainless steel chemical tankers in 2025, with delivery planned for the first half of 2028, indicating that owners are still committing capital despite a softer rate backdrop. SSY expected 46% of the global chemical tanker orderbook to deliver in 2026, suggesting near-term supply pressure may emerge before older tonnage leaves the fleet. COSCO SHIPPING Energy Transportation also ordered a 9,200-dwt stainless-steel chemical tanker in May 2025, reinforcing that domestic operators are still expanding specialized coastal capacity. The China chemical logistics market is therefore moving toward a structure in which decarbonization compliance and hazardous-cargo monitoring are increasingly handled through a single digital operating system rather than through separate regulatory workflows.

E-Commerce Demand for Specialty Packaging Chemicals (Inks, Coatings, Adhesives)

The China chemical logistics market is seeing a structural shift in demand toward specialty packaging chemicals used in inks, coatings, adhesives, and dispersants. These products move in lower volumes than bulk commodities, but they need tighter hazard handling, cargo segregation, and, in some cases, controlled temperatures. BASF's commissioning of its high-performance dispersant line in Nanjing in November 2025 is a clear sign that East China's packaging and printing supply chains are bringing more specialty-chemical capacity closer to demand centers. That shift is changing freight patterns from consolidated, full-truck chemical loads to more fragmented, time-sensitive shipments that still require dangerous-goods compliance. Operators that once focused on bulk commodity lanes are adding less-than-truckload specialty capability because the service model is more demanding and the value-added component is higher. In the China chemical logistics market, this is widening the gap between operators that can support precise packaging-chemical movements and those still built mainly for standard bulk transport.

Growth of Lithium-Ion Battery Recycling Clusters in Southwest China

The China chemical logistics market is emerging as a new growth center in Southwest China as lithium-ion battery recycling capacity and regulatory oversight expand in tandem. China retired 819,000 tons of lithium-ion batteries in 2025, up 90.5% year over year, while recycled volumes reached 301,668 tons, which shows how quickly reverse hazardous flows are entering the logistics system. Administrative measures effective in April 2026 now require integrated vehicle-battery retirement, full-chain traceability, and stronger producer responsibility, pushing the segment toward more formal, scalable logistics networks. Capacity additions in Sichuan and Yunnan are reinforcing Southwest China's role as a collection, discharge, and processing corridor for spent batteries and intermediate materials. Because end-of-life lithium packs fall under Class 9 dangerous goods rules, the logistics requirements extend beyond simple transport and include controlled collection, storage, discharge, and onward movement to hydrometallurgical plants. The China chemical logistics market is therefore opening a durable sub-segment for operators that can manage battery waste, electrolyte-related materials, and recycled precursors across difficult Southwest terrain and upgraded corridor infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightened tunnel restrictions after the 2025 Guoliang accident | -0.3% | Central China, with national spillover to inter-provincial hazardous routes | Short term (≤ 2 years) |

| Rail-tank-wagon shortage because of steel capacity curbs | -0.4% | National, concentrated in North and Northwest China | Medium term (2-4 years) |

| Mandatory RFID tracking for Class 8 corrosives is raising compliance costs | -0.3% | National, with early pressure in the East and South China industrial hubs | Short term (≤ 2 years) |

| Rising coastal port congestion surcharges for IMO Type II cargoes | -0.4% | Coastal China, including Shanghai, Tianjin, Ningbo, and Guangzhou | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightened Tunnel Restrictions after the 2025 Guoliang Accident

The China chemical logistics market is facing longer route times on several hazardous road corridors after tighter tunnel controls followed the 2025 Guoliang incident. This matters because provinces such as Henan, Shanxi, Shaanxi, Sichuan, and Guizhou depend heavily on tunnel-rich road infrastructure for inter-provincial movement. When routes are restricted or time windows are narrowed, affected lanes can no longer support the same just-in-time delivery rhythm demanded by downstream chemical users. The Ministry of Transport's revised dangerous-goods road transport regulations, introduced in February 2026, strengthened satellite-monitored route compliance. It raised penalties for deviations, which increases the cost burden on smaller carriers without integrated fleet systems. That cost pressure is likely to accelerate consolidation, as many smaller road operators cannot absorb new technology and compliance costs at the same pace as larger fleets. The China chemical logistics market is therefore seeing shipper demand shift toward providers that can either prove safe rerouting discipline or switch volumes to other modes when roads become less reliable.

Rail-Tank-Wagon Shortage Because of Steel Capacity Curbs

The China chemical logistics market is also constrained by limited rail tank wagon availability at a time when shippers need more modal flexibility. China's crude steel output fell 4.4% year over year to 961 million metric tons in 2025, and output is expected to decline again in 2026 under carbon-intensity goals, which tighten supply for specialized wagon manufacturing. Rail authorities in Taiyuan, Hohhot, Lanzhou, and Xi'an also tightened approvals for non-power-coal cargoes in 2025, disrupting chemical rail movement across important northern corridors. The OECD's 2025 steel outlook shows that global excess capacity remains high, but China's domestic discipline, rather than global surplus, is the practical issue for wagon supply. Shippers that cannot secure rail slots are forced back onto road tankers, which raise per-ton logistics costs and increase exposure to hazardous road compliance rules. In the China chemical logistics market, operators that control both rail access and road capacity are better placed to protect service continuity and pricing power through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Anchors Revenue, Value-Added Services Drive Growth

Transportation accounted for 64.77% of revenue in 2025, making it the largest component of the China chemical logistics market size. That position reflects the asset-heavy nature of the China chemical logistics market, where chemical movement still depends on tank trucks, rail wagons, coastal tankers, and inland waterway links rather than on pure digital brokerage models. Road transport remains the key intra-regional mode because it offers routing flexibility for short-haul dangerous goods movements across industrial clusters. Sea and inland waterways handle much of the higher-volume inter-provincial flow, and the Wuhan petrochemical terminal adds a meaningful public node to that system with 3.55 million tons of annual capacity.

Value-added services are forecast to grow at a 7.31% CAGR through 2031, which is the fastest pace among logistics functions. HOYER's November 2025 expansion at the Covestro Integrated Site in Shanghai shows why, because the site combines automated filling, temperature-controlled warehousing, and round-the-clock monitoring into one compliance-heavy service model[2]Source: Hoyer Group, “HOYER Expands Service Portfolio at Shanghai Site,” Bulk Distributor, bulk-distributor.com. In the China chemical logistics market, that growth path points to higher spending on outsourced blending support, in-plant operations, and documentation-intensive services rather than on transport alone.

By Hazard Class: Hazardous Chemicals Dominate Volumes and Lead Growth

Hazardous chemicals accounted for 66.5% of the China chemical logistics market in 2025 and posted the fastest projected CAGR of 6.19% through 2031. This dual lead shows that the China chemical logistics market remains centered on flammable liquids, corrosives, reactive products, and battery-related materials that require specialized handling. The new compliance environment strengthens that position because hazardous cargo cannot move without licensed carriers, route controls, and more structured traceability. China's Hazardous Chemicals Safety Law, effective from May 2026, is reinforcing that shift by raising operating standards across the hazardous chemical lifecycle.

The result is faster share migration toward operators that already have digital control systems and compliant assets. RFID-linked management for corrosives is adding another layer of discipline in parks and storage environments where inspection requirements are rising. Non-hazardous chemicals still account for a substantial share of the China chemical logistics market, mainly through base polymers, fertilizers, and food-grade chemical ingredients, which are handled under broader freight standards. Even so, the distinction between hazardous and non-hazardous service quality is narrowing, as many shippers are extending traceability tools across their broader portfolios after seeing the operational benefits of hazardous cargo. That means hazardous regulation is not only shaping its own segment, but also lifting service expectations across the wider China chemical logistics market.

By Temperature Control: Ambient Volumes Mask Accelerating Cold-Chain Build

Non-temperature-controlled logistics accounted for 71.5% of China chemical logistics market size in 2025, reflecting the large volume of ambient petrochemicals, commodity solvents, and base polymers moved across China. That dominant share does not change the fact that the China chemical logistics market is investing more heavily in temperature-sensitive handling than before. Temperature-controlled logistics is projected to grow at a 7.33% CAGR through 2031, the fastest growth rate across all segment types in the report. The main demand comes from pharmaceutical chemical precursors, enzyme-based specialty products, and selected electronic-grade materials that need tighter thermal protection.

This trend is already showing up in facility design and network planning. HOYER's Shanghai expansion included 3 temperature-controlled warehouses with ammonia refrigeration for MDI storage, a clear sign that chemical operators are building more controlled environments within industrial sites. SF Holding's pharmaceutical logistics center at Ezhou Huahu International Airport also includes refrigerated, frozen, and cool zones that meet GDP standards and support more precise handling workflows.

By End Use Industry: Oil and Gas Anchors, Pharmaceutical Leads Forward Growth

Oil and gas accounted for 30.41% of China chemical logistics market size in 2025, while pharmaceuticals are forecast to grow at the fastest CAGR of 7.64% through 2031. Oil and gas remain the anchor, as inter-regional petrochemical flows from Xinjiang, Shandong, and Sichuan continue to drive high-volume movement of feedstocks, process chemicals, and refined derivatives. Those lanes support the largest absolute freight base in the China chemical logistics market, especially for long-distance hazardous cargo movement. Pharmaceuticals, however, are becoming the most attractive growth pocket because it requires higher service precision, tighter temperature control, and stronger distribution discipline.

That shift is visible in corporate strategy. Kerry Logistics Network was selected by Teva Pharmaceuticals as the exclusive 4PL provider for pharmaceutical distribution in the Greater Bay Area in March 2025, underscoring the role of long-term contracts in favoring operators with healthcare-grade logistics capabilities. Specialty chemicals sit between these two poles because packaging, electronics, and performance materials create more demanding service needs than bulk commodities but broader volume than pharmaceuticals. Cosmetics remain smaller, though their growth still supports careful ingredient handling and cleaner storage conditions. Across the China chemical logistics market, this mix is gradually reducing reliance on pure commodity transport and improving the role of higher-margin specialty and pharma-linked service models.

Geography Analysis

East China accounted for 24.1% of revenue in 2025, giving it the largest regional share in the China chemical logistics market. The region is led by the Shanghai, Jiangsu, and Zhejiang production triangle, which combines specialty chemicals, pharmaceuticals, and packaging materials in the country's densest industrial cluster. Milkyway Chemical Supply Chain's stated focus on East, North, and Southwest China reflects the strong alignment between network investment and this regional demand hierarchy[3]Milkyway Chemical Supply Chain Service Co. Ltd., “2025 Interim Report,” HKEx, hkexnews.hk. The Yangtze River system strengthens East China's role by providing a cost-efficient inland alternative to road transport and linking coastal demand with central production corridors.

North China ranks second in scale because the Beijing-Tianjin-Hebei corridor combines industrial demand with policy support for the movement of hazardous cargo. Hebei's chemical investment program in 2025 and the Haz-Chem One-Permit pilot both support faster administrative flow across a region that already handles major industrial and distribution volumes. Northeast China remains tied to the Dalian and Shenyang port complexes, while South China continues to play a strong role in specialty and fine chemicals. Clariant's CHF 80 million (USD 99.8 million) expansion in Daya Bay reinforces South China's position in care chemicals and pharmaceutical excipients, underscoring the need for greater care in the Pearl River Delta. Central China is becoming more strategic because the Yangtze axis and the Wuhan terminal now support stronger interchange between inland production and eastern consumption.

Southwest China is forecast to grow at a 5.57% CAGR through 2031, making it the fastest-growing regional part of the China chemical logistics market. Its rise comes from lithium battery recycling, the New Land-Sea Corridor, and coal-to-chemicals development in provinces such as Guizhou and Sichuan. Northwest China remains the longer-term frontier because Xinjiang and Gansu are adding upstream and downstream chemical flow potential tied to coal-to-chemicals and long-distance distribution. As production disperses inland, relay hubs at provincial borders become more important than a model built mainly around coastal exits. That means the China chemical logistics market is no longer organized only by coast-first trade logic, and network architecture is being redrawn around inland production corridors and multimodal interchange points.

Competitive Landscape

The China chemical logistics market is moderately fragmented. The concentration level leaves wide room for provincial operators and specialist carriers, which is why the China chemical logistics market does not behave like a tightly consolidated national network. State-owned enterprises such as Sinotrans, Sinochem Logistics, China COSCO Shipping Logistics, and Sinopec Chemical Commercial Holding retain strong positions on major corridors because they benefit from access to infrastructure, entrenched shipper relationships, and institutional scale. International specialists such as HOYER Group, Stolt Tank Containers, Bertschi Group, and Den Hartogh Logistics compete more on compliance depth, specialized equipment, and service consistency for multinational customers.

Technology is becoming the main driver of gains across the China chemical logistics market. Operators now need route optimization, dangerous goods traceability, and temperature visibility within a single operating model rather than as separate features. The gap between domestic and international providers is narrowing as local firms expand their multimodal reach and enhance specialized execution. Stolt-Nielsen's Shanghai SC-Stolt Shipping joint venture and Tianjin Lingang Stolthaven Terminal remain good examples of how international groups use partnership structures to stay present in regulated domestic lanes. HOYER's 2025 expansion at Covestro's Shanghai site is another example, as it tied filling, storage, and monitoring into a client-embedded service model rather than a stand-alone transport offer.

Strategic activity is also spreading into adjacent services that can reshape the China chemical logistics market over time. Stolt-Nielsen's acquisition of Suttons International added scale in ISO tanks and widened access to product categories that matter in China-linked flows. Kerry Logistics Network's exclusive 4PL agreement with Teva strengthened its pharmaceutical distribution capabilities in the Greater Bay Area, supporting the move toward higher-value precision services[4]Source: Kerry Logistics Network, “KLN Selected by Teva as Its Exclusive 4PL Service Provider in the Greater Bay Area,” PR Newswire, prnewswire.com . The China chemical logistics market is therefore likely to keep rewarding operators that pair scale with compliant infrastructure, digital controls, and the ability to serve both bulk and precision cargo without service breaks. Smaller providers can remain relevant, but they will face a harder path, where laws, traceability, and equipment standards rise faster than their pricing power.

China Chemical Logistics Industry Leaders

Sinotrans Limited

Sinochem Logistics

Milkyway Chemical Supply Chain Service Co., Ltd.

Yongtaiyun Chemical Logistics

China COSCO Shipping Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Stolt-Nielsen entered a joint venture agreement to sell 50% of Avenir LNG to Nippon Yusen Kabushiki Kaisha (NYK Line), creating a jointly owned and operated small-scale LNG bunkering and supply venture, subject to regulatory approvals anticipated in Q2 2026.

- November 2025: Stolt-Nielsen Limited acquired 100% of Suttons International Holdings Limited, a UK-based ISO tank operator, for approximately USD 75.2 million. The acquisition added over 11,000 ISO tank containers to Stolt Tank Containers' fleet, expanded the product portfolio to include gas distribution and China domestic services, and positioned Stolt Tank Containers as the global leader with approximately 65,000 ISO units across 22 full-service depots.

- November 2025: HOYER Group officially opened its new service facility within the Covestro Integrated Site Shanghai, assuming full responsibility for MDI drum and IBC tote filling, storage, and logistical management. The facility features 4 fully automated drum filling systems, 3 temperature-controlled warehouses with ammonia refrigeration, and a 24/7 central control room, a significant addition to HOYER's China chemical logistics service infrastructure.

- October 2025: HOYER Group signed a strategic cooperation agreement with Green Energy Origin (GEO) in Liyang, Jiangsu, to provide end-to-end logistics for electrolytes, CNT slurry, and key battery raw materials with a 4-6 hour rapid local response capability for customers in Europe and North America, directly supporting China's battery material export corridors.

China Chemical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| Hazardous Chemicals |

| Non-hazardous Chemicals |

| Temperature-Controlled (Refrigerated/Heated) |

| Non-Temperature-Controlled |

| Pharmaceutical |

| Cosmetic |

| Oil and Gas |

| Specialty Chemicals |

| Other End-Users |

| North |

| Northeast |

| East |

| Central |

| South |

| Southwest |

| Northwest |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Hazard Class | Hazardous Chemicals | |

| Non-hazardous Chemicals | ||

| By Temperature Control | Temperature-Controlled (Refrigerated/Heated) | |

| Non-Temperature-Controlled | ||

| By End Use Industry | Pharmaceutical | |

| Cosmetic | ||

| Oil and Gas | ||

| Specialty Chemicals | ||

| Other End-Users | ||

| By Region | North | |

| Northeast | ||

| East | ||

| Central | ||

| South | ||

| Southwest | ||

| Northwest |

Key Questions Answered in the Report

How large is China's chemical logistics in 2026?

The China chemical logistics market is valued at USD 136.47 billion in 2026.

Which logistics function leads revenue in China?

Transportation is the leading function, accounting for 64.77% of revenue in 2025, as chemical movement still depends heavily on specialized physical assets and multimodal links.

Which cargo class is growing fastest in China's chemical logistics?

Hazardous chemicals are the largest and fastest-growing hazard class, accounting for 66.5% of revenue in 2025 and a projected 6.19% CAGR through 2031.

Why is temperature-controlled handling gaining importance?

Temperature-controlled handling is projected to grow at 7.33% CAGR through 2031 due to pharmaceutical cold-chain needs and tighter quality requirements for specialty chemicals.

Which end-user group offers the best growth outlook?

Pharmaceuticals are the fastest-growing end-user segment, with a 7.64% CAGR through 2031, supported by stronger GDP growth and broader biotech expansion.

Which region is growing fastest across China?

Southwest China is projected to grow at a 5.57% CAGR through 2031, driven by battery recycling, inland industrial expansion, and corridor upgrades linked to the New Land-Sea route.

Page last updated on: