India Chemical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

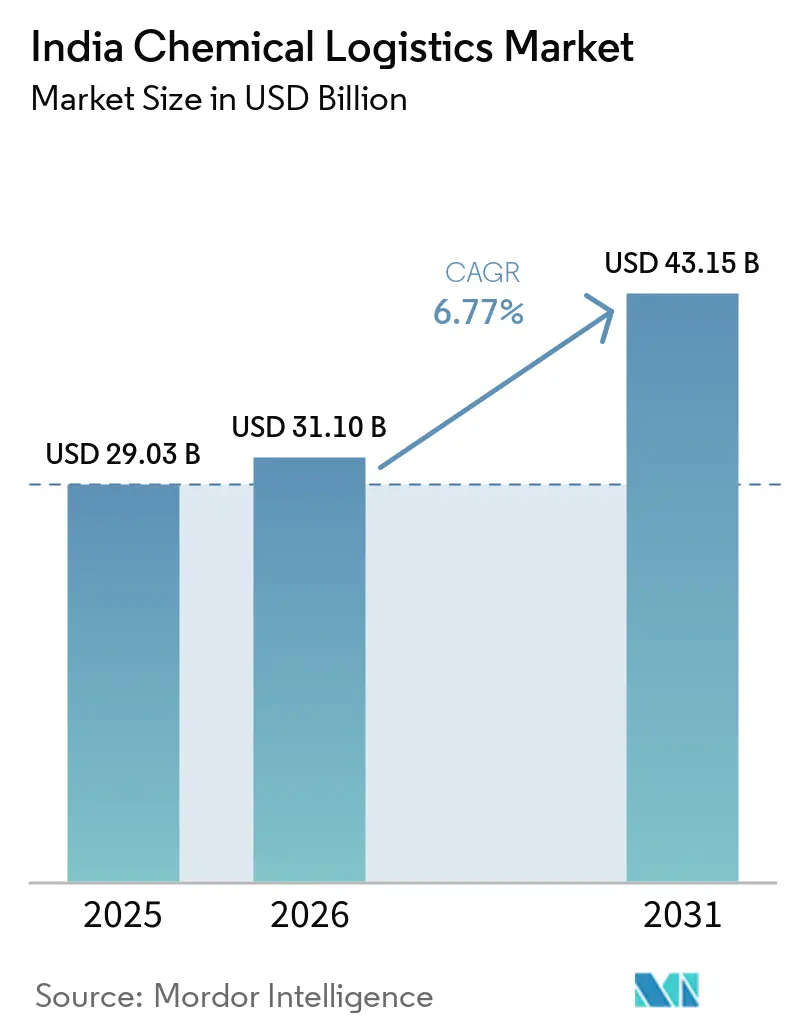

| Base Year Market Size (2025) | USD 29.03 Billion |

| Market Size (2026) | USD 31.10 Billion |

| Market Size (2031) | USD 43.15 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

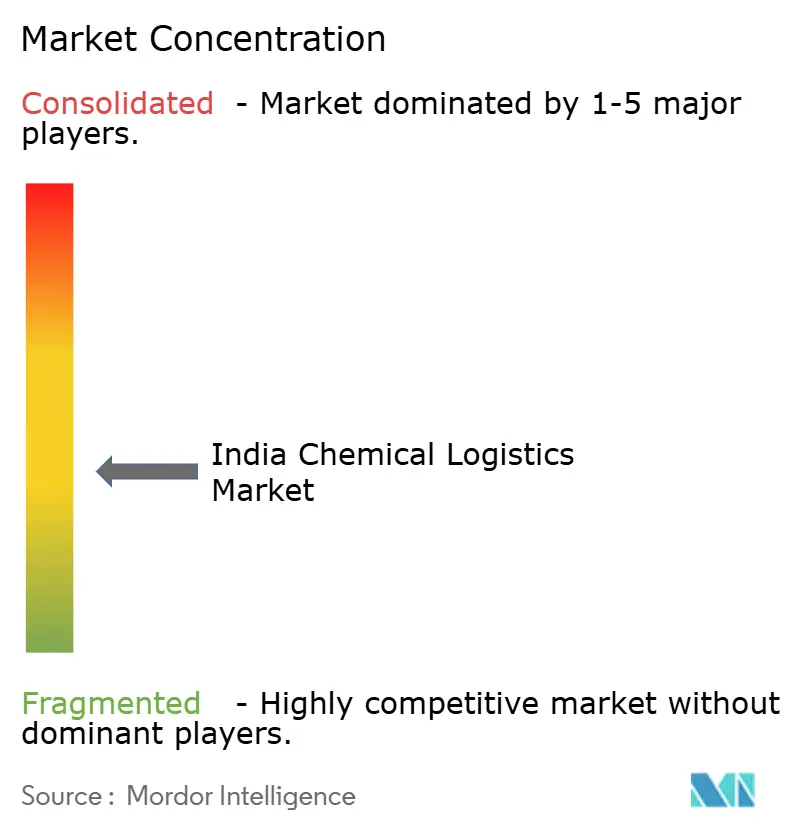

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Chemical Logistics Market Analysis by Mordor Intelligence

The India chemical logistics market size is expected to increase from USD 29.03 billion in 2025 to USD 31.10 billion in 2026 and reach USD 43.15 billion by 2031, growing at a CAGR of 6.77% over 2026-2031.

Growth in the India chemical logistics market is being supported by stricter handling requirements for hazardous cargo and by the rising need for safer storage, movement, and documentation across the supply chain. Investments in rail links, port connectivity, and multimodal corridors are also changing network design, gradually reducing reliance on fragmented road-only movements for bulk cargo. Export-oriented specialty chemicals and time-sensitive pharmaceutical cargo are adding demand for traceability, cold-chain handling, and bundled service execution in the Indian chemical logistics market, and new rail-linked cold-chain offerings are reinforcing that shift. Competition remains balanced between global integrators and domestic specialists, and the edge is increasingly coming from compliance depth, asset ownership, and service integration rather than pure freight rates. The main operating constraint remains execution capacity, as the shortage of trained drivers for heavy commercial vehicles remains large and continues to tighten hazardous cargo operations across the India chemical logistics market.

Key Report Takeaways

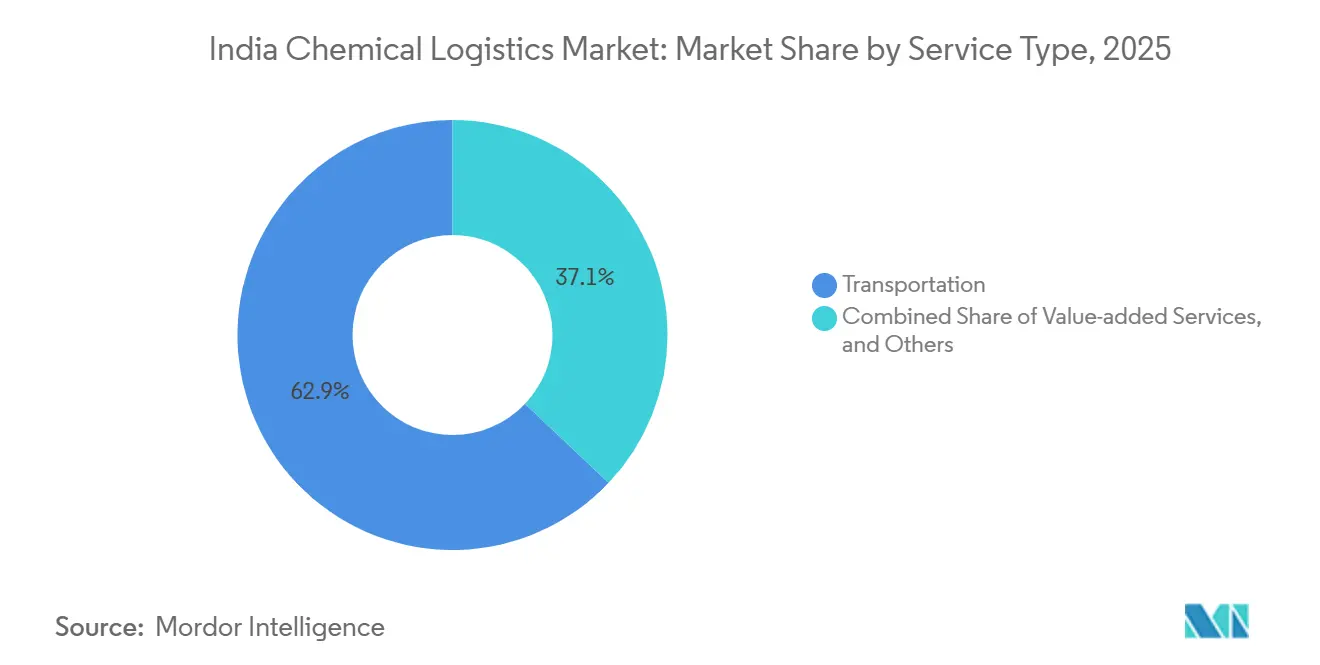

- By logistics function, transportation held 62.93% of the India chemical logistics market share in 2025, while value-added services are projected to expand at a 9.60% CAGR through 2031.

- By hazard class, hazardous chemicals held 64.12% share in 2025, and are growing at a CAGR of 8.77% through 2031.

- By temperature control, non-temperature-controlled logistics accounted for 71.29% of the India chemical logistics market size in 2025, while temperature-controlled logistics are forecast to grow at a 9.91% CAGR through 2031.

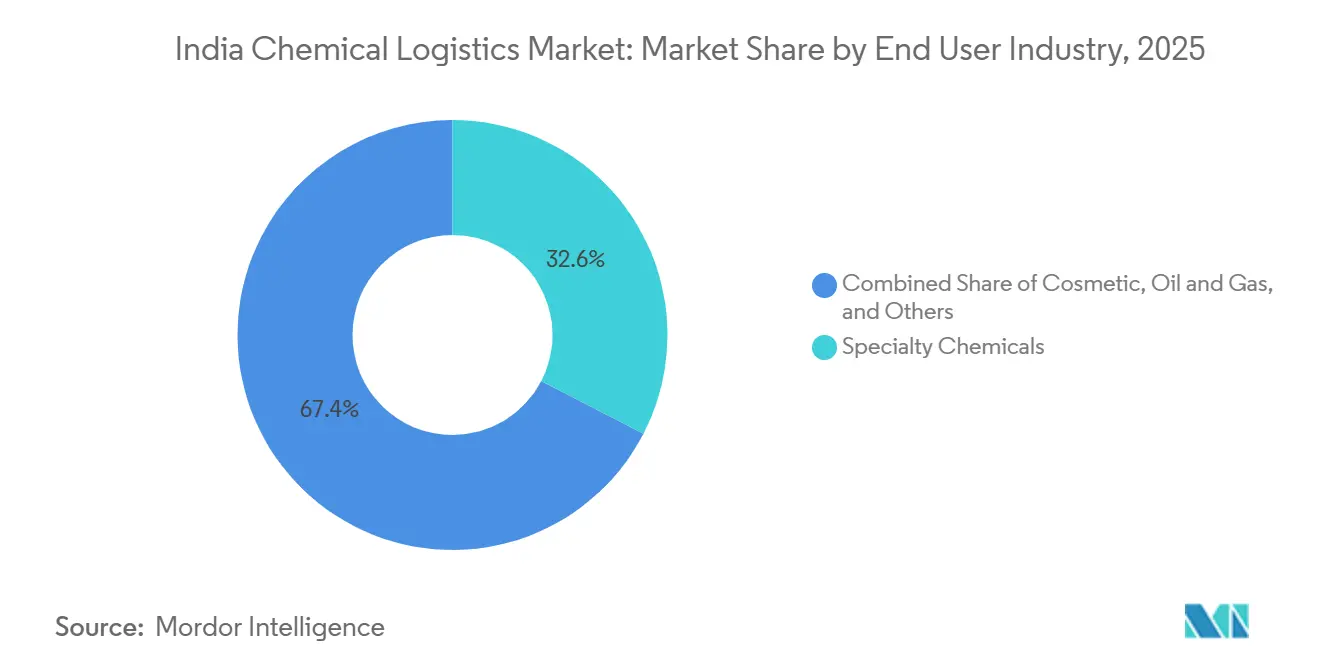

- By end-user industry, specialty chemicals held 32.6% share in 2025, while pharmaceutical logistics is projected to grow at a 10.22% CAGR through 2031.

- By region, the West accounted for 29.07% of the India chemical logistics market size in 2025, while the South is forecast to expand at an 8.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Chemical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening bulk-cargo safety norms under BIS mandatory certification | +0.6% | National, with early compliance activity at JNPT, Mundra, and Hazira | Short term (≤ 2 years) |

| Growing multi-modal chemical corridors under PM Gati-Shakti | +1.4% | National, concentrated in the Western DFC corridor and the Energy-Mineral-Cement Economic Corridor. | Medium term (2-4 years) |

| Surge in specialty-chemical exports exceeding 10% YoY in FY25 | +1.2% | West, especially Gujarat, and South, especially Andhra Pradesh and Tamil Nadu, with spillover to APAC and EU trade lanes | Short term (≤ 2 years) |

| Cold-chain demand for high-value pharma APIs | +1.0% | South, especially Hyderabad and Chennai, and West, especially Pune and Ahmedabad, with growing air freight nodes in the North. | Medium term (2-4 years) |

| Blockchain-enabled wagon tracing pilots by CONCOR | +0.4% | National, rail-corridor hubs on the W-DFC and E-DFC | Medium term (2-4 years) |

| Standardization of flexitank and ISO-tank handling at Indian ports | +0.6% | JNPT, Mundra, Hazira, Chennai, and Visakhapatnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Bulk-Cargo Safety Norms Drive Compliance-Led Logistics Upgrades

Mandatory certification and stricter inspection discipline are pushing the India chemical logistics market toward greater equipment integrity and stronger process control. Bulk cargo operators are upgrading pressure-tested assets, monitoring systems, and documentation procedures to continue serving regulated lanes without disruption. This raises fixed costs for all participants, but larger fleets can spread that burden across higher shipment volumes and longer customer contracts. Smaller carriers, therefore, face weaker economics in hazardous lanes, especially where buyers now expect audited compliance and more formal safety safeguards. Over the forecast period, this compliance-led reset should leave organized operators with a stronger negotiating position in the India chemical logistics market.

PM Gati-Shakti Multimodal Corridors Redefine Chemical Freight Economics

PM Gati-Shakti is changing freight economics in the India chemical logistics market by improving links between plants, rail corridors, terminals, and ports[1]"PM Gati Shakti: Rs 11.17 Lakh Crore Mega Push with 434 Projects to Transform India's Logistics." India Shipping News, 2025.. The practical effect is not only better line-haul speed, but also stronger schedule reliability for bulk and containerized chemical cargo. As more traffic moves through dedicated freight and cargo-terminal infrastructure, chemical shippers can work with leaner buffers and tighter dispatch planning. This is gradually shifting supply chains away from fragmented road-only loops and toward integrated rail and port combinations. Logistics providers that pair corridor access with chemical warehousing and compliance support are likely to capture a larger share of the India chemical logistics market over time.

Specialty-Chemical Export Surge Creates Dedicated Logistics Sub-Segments

Rising specialty-chemical exports are creating a more specialized operating model inside the India chemical logistics market. These cargoes require tighter temperature control, batch traceability, and dedicated tank or container configurations than for standard bulk movements. That raises the revenue intensity of logistics even when physical shipment volume is lower than in commodity chemicals. It also widens the gap between operators that own specialized assets and those that compete mainly on generic trucking capacity. As export lanes stabilize, the India chemical logistics market should see more long-duration contracts tied to service quality, documentation accuracy, and cargo integrity.

Cold-Chain Demand for Pharma APIs Redefines Temperature-Sensitive Chemical Logistics

Cold-chain demand from pharmaceutical APIs is lifting the service threshold across the India chemical logistics market. Biologics, high-potency ingredients, and related export flows need validated temperature ranges, faster custody transfer, and cleaner handoff processes than ambient cargo. Maersk and CONCOR launched India’s first dedicated weekly reefer rail service from Hyderabad to Nhava Sheva in May 2026, and the service is expected to save 3,000 tons of GHG emissions each year[2]"CONCOR Takes a Giant Leap in Cold Chain Logistics with First-Ever Pharma Reefer Export to Singapore." India Shipping News, December 2025.. Moves like this are expanding modal choice for sensitive chemical cargo while lowering dependence on road-only cold transport. Operators that build rail-linked cold-chain infrastructure now should hold a stronger position in the India chemical logistics market as pharma exports scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Under-investment in DG cargo rail sidings | -0.7% | National, severe in East India and Central India | Medium term (2-4 years) |

| Driver-skill shortage for hazmat tank-trucks | -0.8% | National, concentrated in tier-2 cities and East India | Medium term (2-4 years) |

| Limited refrigerated warehouse capacity outside tier-1 cities | -0.5% | North and Central India, with secondary clusters in Rajasthan and Madhya Pradesh | Long term (≥ 4 years) |

| High insurance premiums after the Vizag LG Polymer incident | -0.4% | National, concentrated in petrochemical corridors on the East Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Under-Investment in DG Cargo Rail Sidings Limits Rail Modal Shift

Under-investment in DG cargo rail sidings is slowing the modal shift that many shippers want in the India chemical logistics market. The gap is more visible in eastern and central corridors, where chemical plants still rely heavily on road tankers because dedicated rail-linked infrastructure is limited. Hazardous-commodity sidings also demand more capital, more approvals, and longer execution timelines than ordinary cargo facilities. That keeps road as the default choice for a large part of bulk DG traffic, even where rail could lower cost and improve safety. Until rail-linked hazardous cargo infrastructure improves, the India chemical logistics market will continue to carry avoidable trucking exposure in several inland corridors.

Driver-Skill Shortage Constrains Hazmat Tank-Truck Capacity Nationally

The shortage of trained drivers remains one of the clearest structural limits on the India chemical logistics market. India faced a shortfall of 2.2 million skilled drivers in the April 2025 Lok Sabha reply, and the planned 1,600 driver training institutes will take time to ease that gap. The pool of hazmat-endorsed drivers is even tighter, which directly restricts the availability of DG-rated tank-truck capacity. Larger logistics companies can partly manage the issue through in-house training and stronger retention practices, but smaller carriers cannot match that effort at the same scale. This keeps wage pressure high and leaves the India chemical logistics market more dependent on organized operators for sensitive cargo movements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Anchors Volume as Value-Added Services Race Ahead

Transportation held 62.93% of the India chemical logistics market share in 2025, making it the report's core volume engine. Road continues to dominate because many chemical plants still sit away from railheads and ports, and buyers need flexible last-mile delivery across industrial belts. This also suits the large base of smaller shippers that move limited batches and cannot always fill dedicated rail or coastal lots. Rail is still gaining relevance in transportation, as carriers widen their liquid-cargo offerings and use containerized solutions to serve longer corridors.

Value-added services are projected to expand at a 9.60% CAGR through 2031, making it the fastest-growing function in the India chemical logistics industry. Chemical shippers increasingly want one provider to manage tracking, temperature logging, customs support, hazmat paperwork, and exception handling. Warehousing, distribution, and inventory management, therefore, remain important because customers are asking for safer storage and tighter stock control near major manufacturing belts. The result is a shift from pure freight execution toward bundled service models where compliance and visibility carry as much value as movement.

By Hazard Class: Hazardous Chemicals Dominant as Compliance Complexity Raises Entry Barriers

Hazardous chemicals accounted for 64.12% of the India chemical logistics market share in 2025 and are also the fastest-growing segment, with a CAGR of 8.77% through 2031, reflecting the significant role of petrochemicals, agrochemicals, and industrial solvents in the India chemical logistics market. The segment is large not only because of volume, but also because each shipment carries a heavier service burden. DG-rated tankers, UN-rated packaging, documented safety procedures, and endorsed drivers all lift the revenue value of hazardous cargo.

Hazardous chemicals remain the most defensible part of the India chemical logistics industry because compliance complexity raises the cost of entry. Operators need PESO-grade terminals, retrofitted fleets, digital records, and trained staff before they can compete credibly in this lane. That creates durable moats for organized companies and limits how quickly new carriers can scale in the regulated cargo market. It also means margin pressure tends to fall harder on smaller operators that lack the systems needed to manage safety and documentation at scale.

By Temperature Control: Non-Temperature Controlled Dominance Masks Accelerating Cold-Chain Build-Out

Non-temperature-controlled logistics accounted for 71.29% of the India chemical logistics market size in 2025, thereby remaining the dominant format of the market. This majority position reflects the heavy movement of fertilizers, base petrochemicals, and other products that can travel under ambient conditions. The segment should retain the lead through 2031 because it still carries the bulk of volumes across the network. Even so, the earnings mix is shifting because colder and more tightly managed cargoes are growing faster than ambient traffic.

Temperature-controlled logistics is projected to grow at a 9.91% CAGR through 2031, marking the fastest expansion in the temperature-control segment of the India chemical logistics market. That pace is being driven by pharma APIs, higher-value specialty materials, and battery-related intermediates that cannot tolerate wide thermal variation. Maersk’s reefer rail service from Hyderabad offers exporters an end-to-end cold-chain solution that integrates inland rail with ocean freight under a single operating model. As more shippers seek validated handling and live visibility, temperature-controlled networks should narrow the gap with ambient logistics in the second half of the forecast period.

By End-User Industry: Specialty Chemicals Lead by Share as Pharma Drives the Fastest Growth

Specialty chemicals accounted for 32.6% of end-user demand in 2025, making it the largest consumption segment in the India chemical logistics market. The category spans agrochemicals, dyes and pigments, performance chemicals, and semiconductor-linked inputs, so handling needs vary widely by product and destination. Some shipments move as ambient bulk cargo, while others need strict segregation, clean storage, and more exact documentation. Cosmetics, oil and gas, and other end users made up the rest of the mix and continued to support baseline freight volumes across multiple corridors.

Pharmaceutical logistics is projected to expand at a 10.22% CAGR through 2031, which makes it the fastest-growing end-user segment in the India chemical logistics industry. The driver is not only export growth, but also the higher handling discipline required for APIs, biosimilars, oncology inputs, and other sensitive materials. This shifts value toward operators that can deliver compliant cold storage, real-time visibility, and controlled transfers from plant to export gateway. As drug manufacturers scale more advanced product lines, the pharma corridor should remain one of the highest-value pockets of the India chemical logistics market.

Geography Analysis

The West region accounted for 29.07% of India chemical logistics market size in 2025 and remained the largest regional base in 2026. Gujarat anchors this position through Kandla, Hazira, and Dahej, which together give chemical producers port access, industrial density, and bulk-handling depth. Maharashtra adds pharmaceutical and petrochemical demand, along with strong financial and distribution linkages around Mumbai and Pune. NITI Aayog’s July 2025 chemical sector report recommended 8 port-based chemical clusters, and the West already offers the clearest operating template for that model[3]“Powering India’s Participation in Global Value Chains,” NITI Aayog, niti.gov.in. As land costs rise in older hubs, the West is also extending inland toward lower-cost logistics nodes that can still connect into the same corridor system.

The South is the fastest-growing geography in the India chemical logistics market, with an 8.15% CAGR through 2031. New energy, refining, battery-material, and pharmaceutical investments are widening the region’s need for liquid handling, cold-chain support, and specialized tanker movements. Hyderabad is strengthening its role as the leading pharma export corridor, and Maersk’s weekly reefer rail link to Nhava Sheva reinforces that position. Port activity on the South and East Coast is also improving the case for more specialized liquid-chemical gateways over the forecast period.

North India remains important for pharmaceutical and specialty-chemical distribution because the National Capital Region connects manufacturing demand with a large inland consumption base. Central India is becoming increasingly relevant as a transit hub between western production centers and eastern markets, boosting the value of inland terminals and cross-country rail links. East India should gain weight as petrochemical investments progress around Haldia, Kolkata, and Odisha, but weak DG rail-siding infrastructure still limits a faster modal shift. Across these regions, the India chemical logistics market is becoming more corridor-led, with location advantage increasingly defined by how well plants connect to ports, rail, and compliant storage.

Competitive Landscape

The India chemical logistics market remains moderately fragmented, with large players such as Aegis Logistics, TCI, DHL Supply Chain, Kuehne+Nagel, and Maersk holding a visible but not dominant position. That leaves a long tail of regional transporters, terminal operators, and single-mode carriers with a substantial share of total volume. Global integrators compete on network breadth, compliance depth, and the ability to bundle transport, warehousing, customs, and visibility into one contract. The DSV acquisition of DB Schenker for EUR 14.3 billion (USD 16.7 billion) is reshaping the competitive landscape by creating a larger European-origin player with stronger reach in India. Domestic specialists are responding by deepening local infrastructure, strengthening DG compliance, and focusing on high-barrier cargo lanes rather than competing solely on price.

Technology is becoming the clearest separator in the India chemical logistics market. Shippers increasingly expect live visibility on location, custody, temperature, and documentation status, especially when cargo moves across multiple modes. This is raising the value of digital compliance tools and integrated control towers for both export-linked specialty chemicals and time-sensitive pharmaceutical cargo. Mid-sized operators that combine ISO tanks, rail-linked access, and auditable process control are gaining credibility because they address more of the shipment lifecycle in a single design.

Recent company actions show where the market is moving. Aegis Logistics is expanding storage capacity at Mumbai Port, Maersk has launched a dedicated reefer rail service for pharmaceutical exports[4]“Pharmaceutical Exporters Benefit from Maersk Reefer Rail Service Hyderabad Mumbai,” Maersk, maersk.com , and DSV is using a large-scale acquisition to widen its global logistics footprint into markets such as India. These moves point to a competitive model built around owned assets, corridor control, and specialized execution rather than generic freight brokerage. The India chemical logistics market should therefore remain medium in concentration through the forecast period, even as organized players strengthen their hold over the most regulated and highest-value lanes.

India Chemical Logistics Industry Leaders

-

Aegis Logistics Limited

-

Allcargo Logistics Ltd.

-

Transport Corporation of India (TCI)

-

Deccan Transcon Leasing Pvt. Ltd.

-

HOYER Global Transport India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: A.P. Moller Maersk launched India’s first dedicated weekly reefer rail service with an end-to-end cold-chain solution covering inland rail, ocean freight, documentation compliance, and cold-chain advisory, setting a new benchmark for temperature-sensitive pharma export logistics from India.

- May 2026: Welspun One signed an LoI with Balmer Lawrie; they signed a Letter of Intent to sublease approximately 65,000 sq ft of Grade A+ warehousing space at WTC Nhava Sheva within the JNPA Special Economic Zone for 5 years, extending port-linked CFS operations into SEZ warehousing and value-added logistics services.

- May 2026: Kuehne+Nagel expanded its healthcare and pharmaceutical logistics network in India by opening a temperature-controlled airfreight cross-dock facility in Hyderabad. The facility supports pharmaceutical and medical shipments within temperature ranges of +2 °C to +8 °C and +15 °C to +25 °C, enhancing cold-chain handling from a key API and vaccine manufacturing cluster.

- December 2025: DHL completed the acquisition of CRYOPDP, adding clinical trial and specialized pharma logistics capabilities globally, with India operations benefiting from GDP-certified temperature-controlled infrastructure deployed under DHL’s Strategy 2030

India Chemical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| Hazardous Chemicals |

| Non-hazardous Chemicals |

| Temperature-Controlled (Refrigerated/Heated) |

| Non-Temperature-Controlled |

| Pharmaceutical |

| Cosmetic |

| Oil and Gas |

| Specialty Chemicals |

| Other End-Users |

| North |

| Central |

| West |

| East |

| South |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Hazard Class | Hazardous Chemicals | |

| Non-hazardous Chemicals | ||

| By Temperature Control | Temperature-Controlled (Refrigerated/Heated) | |

| Non-Temperature-Controlled | ||

| By End Use Industry | Pharmaceutical | |

| Cosmetic | ||

| Oil and Gas | ||

| Specialty Chemicals | ||

| Other End-Users | ||

| By Region | North | |

| Central | ||

| West | ||

| East | ||

| South |

Key Questions Answered in the Report

What is the 2031 outlook for chemical logistics in India?

The India chemical logistics market is projected to reach USD 43.15 billion by 2031 from USD 31.10 billion in 2026, advancing at a 6.77% CAGR over 2026-2031.

Which logistics function is the largest in this space?

Transportation is the largest function, with a 62.93% share in 2025, because roads still dominate last-mile chemical movement across industrial corridors.

Which end-user group is growing the fastest through 2031?

Pharmaceutical logistics is the fastest-growing end-user segment, with a forecast CAGR of 10.22%, supported by API exports and rising cold-chain needs.

Why is temperature-controlled handling gaining importance in India?

Temperature-controlled logistics is projected to grow at a 9.91% CAGR, as pharma APIs, specialty materials, and some battery-related intermediates require validated thermal control and real-time visibility.

Which region leads chemical logistics demand in India?

The West leads with 29.07% share in 2025, supported by Gujarat’s port network and Maharashtra’s pharmaceutical and petrochemical base.

What is the main operational risk for providers in this field?

The biggest structural constraint is the shortage of trained drivers, especially for hazmat operations, which keeps capacity tight and favors larger, organized operators.

Page last updated on: