Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 534.37 Billion |

| Market Size (2031) | USD 683.28 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemical Logistics Market Analysis by Mordor Intelligence

The Chemical Logistics Market size is estimated at USD 534.37 billion in 2026, and is expected to reach USD 683.28 billion by 2031, at a CAGR of 5.04% during the forecast period (2026-2031).

Digital-twin simulations, artificial-intelligence visibility systems, and low-carbon transport mandates are reshaping supply-chain orchestration, rewarding providers that blend compliance rigor with cost discipline. Asia-Pacific’s surging chemical output and widening consumption base are lengthening ton-mile demand even as production overcapacity prompts corridor diversification. Multimodal networks, especially rail-sea combinations, are delivering up to 81% emissions savings compared with road-only routes, creating a structural cost advantage for operators that master interface complexity. Tightened EU ADR and CLP rules, together with rising US hazmat fees, are accelerating consolidation as smaller fleets struggle to finance compliance infrastructure. Finally, premium growth is migrating to temperature-controlled and value-added services areas where specialized assets, telematics, and certified staff generate defensible margins.

Key Report Takeaways

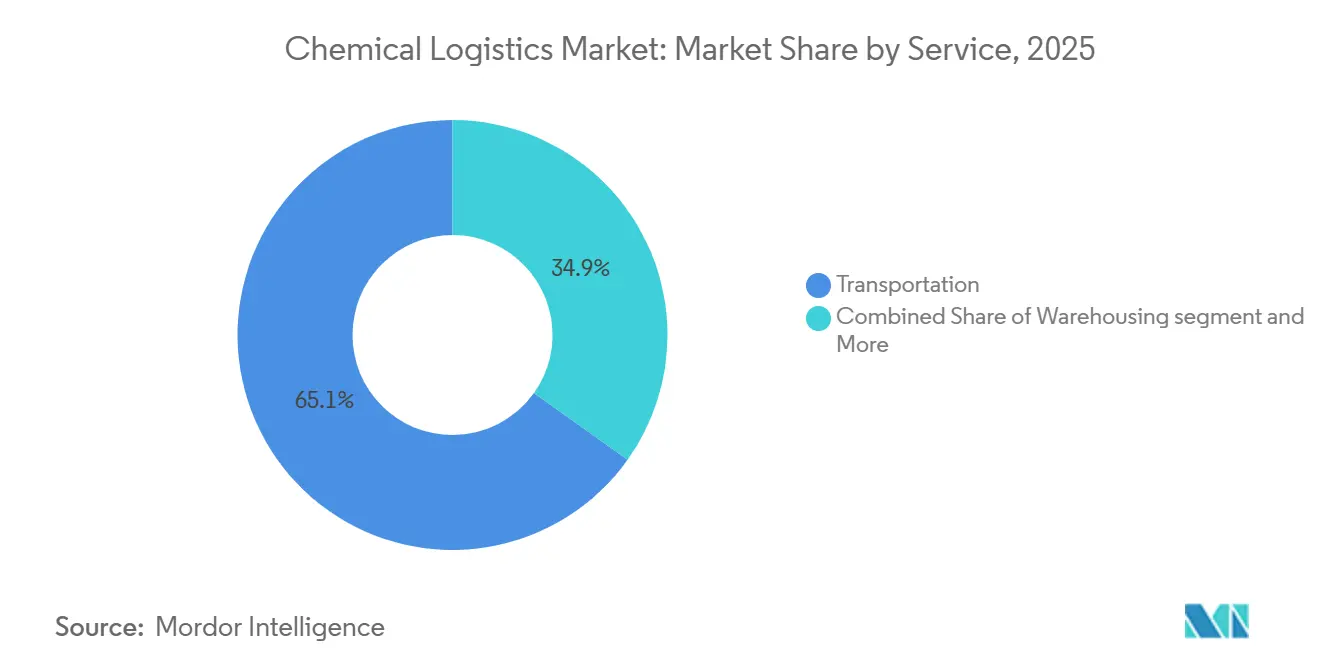

- By service type, transportation held 65.14% of the chemical logistics market share in 2025, whereas Other Services are advancing at a 6.41% CAGR to 2031.

- By end-user, Oil & Gas commanded 30.57% of the chemical logistics market size in 2025, while Specialty Chemicals is projected to post a 6.72% CAGR through 2031.

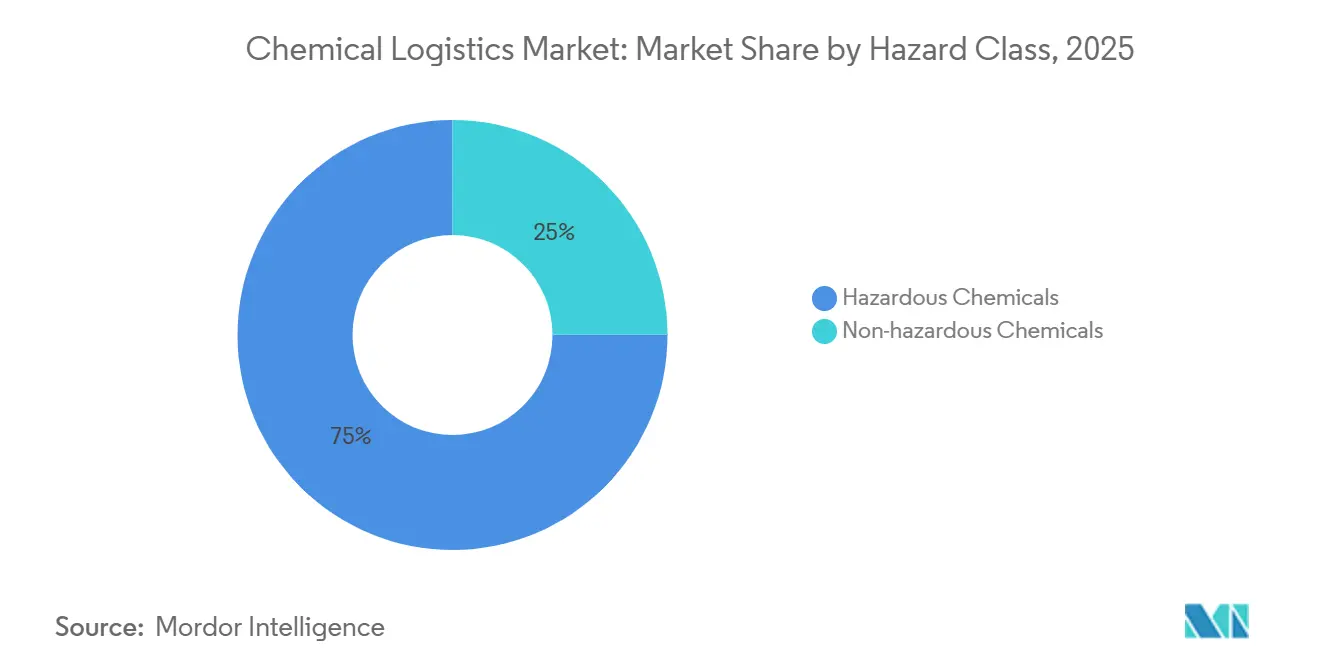

- By hazard class, hazardous chemicals accounted for 75.04% of 2025 shipments, yet non-hazardous cargo is growing at a 5.64% CAGR to 2031.

- By temperature control, non-temperature-controlled flows captured 61.53% share in 2025, but temperature-controlled logistics is expanding at 7.25% CAGR to 2031.

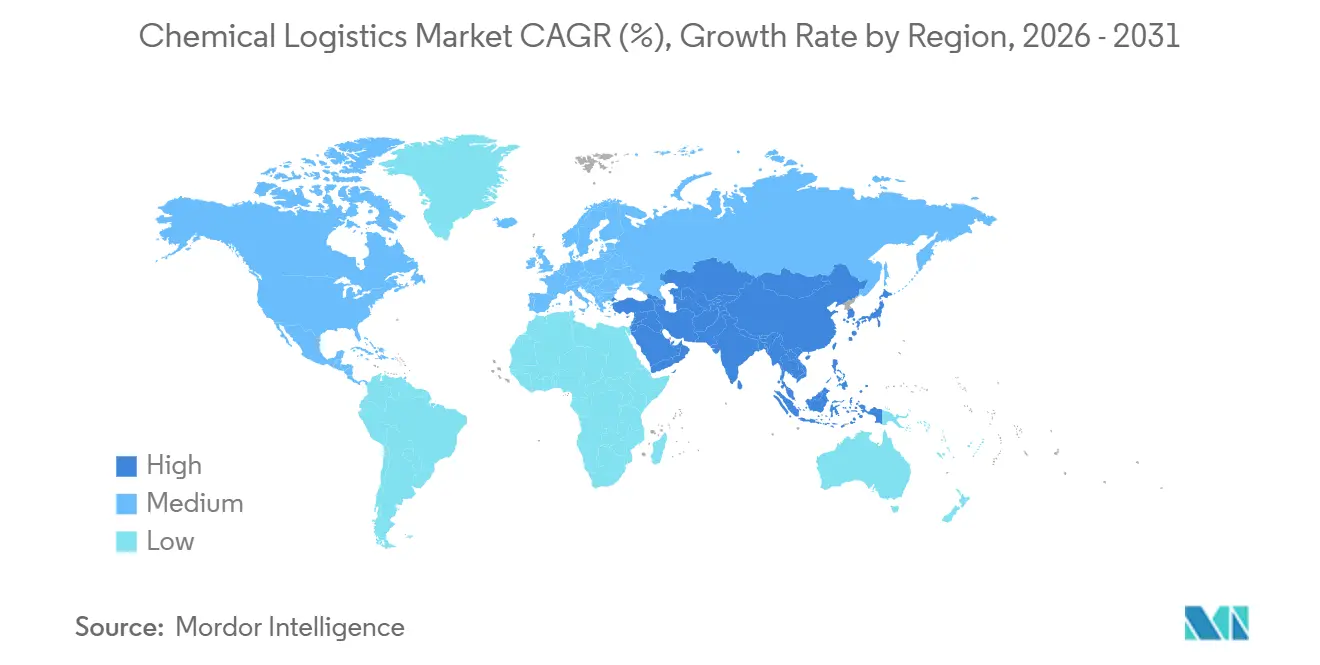

- By geography, Asia-Pacific led with 39.21% revenue share in 2025 and is expanding at a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Chemical Logistics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Asian chemical production | +1.3% | Asia-Pacific, Middle East, Europe | Medium term (2-4 years) |

| Multimodal networks for hazardous goods | +0.7% | Global | Long term (≥ 4 years) |

| Regulatory push for safer, greener assets | +0.9% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Outsourcing to 3PL/4PL specialists | +0.8% | Global | Medium term (2-4 years) |

| Low-carbon methanol & bio chains | +0.5% | Europe, Asia-Pacific, Americas | Long term (≥ 4 years) |

| AI-driven visibility & digital twins | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Asian Chemical Production Boosting Long-haul Volumes

India’s PCPIR zones and mainland China’s capacity additions have shifted export lanes toward Europe and North America, lengthening voyage distances and raising ton-mile demand. Post-Red Sea routing changes have further extended typical Asia-Europe transits, supporting vessel-utilization and intermodal opportunities across rail-sea corridors. Government incentives in India are concentrating output in coastal clusters, yet inland consumption patterns are forcing longer domestic hauls that reward operators with integrated rail, road, and barge solutions.

Rising Use of Multimodal Networks for Hazardous Goods Cost & Safety

Sea-rail systems cut greenhouse-gas emissions by 81% and logistics costs by 70% versus road-only haulage, but adoption hinges on seamless regulatory alignment at modal junctions. The US Federal Railroad Administration highlights dual-mode locomotives and intermittent electrification as cost-effective for bulk chemical corridors when supported by utility partnerships. European operators such as Bertschi already avoid 300,000 tons of CO₂ annually through integrated terminals that synchronize rail, barge, and road legs[1].Bertschi Group, “Sustainability and Intermodal Transport,” bertschi.com

Regulatory Push for Safer, Greener Logistics Assets & Practices

The EU’s revised CLP Regulation activated digital labeling and refillable-packaging mandates in December 2024, compelling fleet owners to deploy track-and-trace and reusable-container pools. ADR 2025 tightens vehicle specifications and driver certifications, while US hazmat fees have risen to USD 3,000 per carrier, pushing compliance costs sharply higher. These converging rules favor incumbents with dedicated hazmat fleets and legal departments.

Outsourcing of Supply-chain Functions to 3PL/4PL Specialists

About 76% of chemical producers plan to boost third-party reliance as they reallocate internal capital toward R&D. DHL’s EUR 2 billion (USD 2.33 billion) health-logistics program is adding GDP-certified hubs and temperature-controlled fleets that single-plant producers cannot economically replicate. New 4PL models give shippers a single point of accountability while aggregating capacity across multiple carriers.

Restraints Impact Analysis of Chemical Logistics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & insurance requirements | -0.9% | Global | Medium term (2-4 years) |

| Fragmented multi-jurisdiction compliance | -0.6% | Global | Long term (≥ 4 years) |

| Fuel-price volatility | -0.8% | Global | Short term (≤ 2 years) |

| Shortage of certified hazmat drivers | -1.0% | Asia, Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex-heavy Asset & Insurance Requirements

Stainless-steel ISO tanks, temperature-controlled chassis, and explosion-proof warehouses cost 2-3 times more than general-cargo equivalents. Peacock Container’s USD 350 million sustainability-linked facility extension underlines the scale of capital required for fleet renewal[2]Peacock Container, “Sustainability-Linked Debt Facility Extension,” peacockcontainer.com. Insurance premiums now absorb up to 5% of revenue for dangerous-goods hauls, magnifying entry barriers.

Fragmented Multi-jurisdiction Compliance Burdens

Differences in hazard classification, labeling, and documentation across borders force operators to maintain parallel compliance protocols. The latest UN Model Regulations add sodium-ion battery rules that some states will not adopt until 2027, obligating mid-journey relabeling when cargo crosses early-adopter borders. African corridors are especially complex, with each member of the African Continental Free Trade Area retaining unique hazmat codes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Chemical Logistics Market Segment Analysis

By Service Type:

Integrated Solutions Lift ProfitabilityTransportation retained 65.14% of the chemical logistics market share in 2025 because physical movement remains unavoidable. Yet Other Services, covering blending, compliance management, and orchestration platforms, are forecast to grow at a 6.41% CAGR, reflecting shipper demand for one-stop solutions that reduce administrative burden. Value-added warehousing anchors working-capital programs by positioning inventory near consumption hubs, while digital platforms capture data exhaust that underpins predictive scheduling and emission reporting. DHL’s acquisition of CryoPDP added 600,000 temperature-sensitive shipments annually, demonstrating how tuck-ins can accelerate capability expansion.

Second-generation 4PL models monetize orchestration by bundling carrier procurement, control-tower analytics, and compliance documentation in subscription packages. As shippers embed these APIs into enterprise resource planning systems, switching costs rise, allowing logistics providers to defend margins even in commodity haulage. Consequently, the chemical logistics market is witnessing a migration of profit pools from tonnage toward information, risk management, and near-customer customization.

By End-User Industry:

Specialty Chemicals AccelerateOil & Gas held 30.57% of the chemical logistics market size in 2025 due to entrenched refinery-to-petrochemical flows, but its low growth exposes providers to price pressure. Specialty Chemicals is slated for a 6.72% CAGR as lithium-ion battery electrolytes and pharmaceutical intermediates demand precision handling, chain-of-custody records, and temperature-stable environments. Argonne National Laboratory projects battery-grade electrolyte output to exceed 1,300 GWh by 2030, multiplying demand for moisture-controlled tank containers.

Pharmaceutical and cosmetics traffic supplies revenue stability because GDP or GMP protocols mandate certified storage and tracked transportation, giving compliant carriers pricing power. Cosmetics raw-materials shifts toward botanical extracts create small-lot, high-frequency lanes that are unsuitable for bulk tanker fleets but ideal for ISO tank relocation and regional depot networks. Thus, the chemical logistics market faces bifurcated growth where low-margin commodity flows coexist with high-service specialty niches requiring differentiated expertise[3]Argonne National Laboratory, “Lithium-Ion Battery Production and Supply Chain Analysis,” anl.gov .

By Hazard Class:

Compliance Costs Define Competitive MoatsHazardous cargo comprised 75.04% of 2025 shipments, anchoring premium rate structures that offset elevated insurance and asset costs. Non-hazardous shipments, growing at a 5.64% CAGR, are benefiting from green-chemistry reformulations that downgrade hazard classes, reducing documentation and equipment requirements. PHMSA lifted hazmat registration to USD 3,000 and civil penalties of over USD 100,000 per day, creating existential risks for non-compliant operators.

Leading fleets exploit these barriers by embedding compliance software that automates MSDS retrieval, label printing, and cross-regulation validation, cutting administrative lead times. However, general-freight entrants are targeting non-hazardous volumes through price competition, pushing incumbents to defend share via service reliability and digital transparency. This divide is steering the chemical logistics market toward dual-track competition where expertise trumps scale in hazmat, whereas cost leadership matters more in benign categories.

By Temperature Control:

Cold Chain Outpaces BulkAlthough non-temperature-controlled loads still make up 61.53% of volume, the temperature-controlled segment is expanding at a 7.25% CAGR, outstripping every other slice of the chemical logistics market. IoT devices now provide real-time temperature and pressure alarms, and many fleets add redundant power sources and phase-change materials to satisfy pharmaceutical and battery-electrolyte stability windows. Maersk’s remote-container-management program offers lane-level temperature assurance, minimizing excursion-related product write-offs.

Higher yields offset capital intensity: premium freight rates can be 150% above ambient-cargo levels, and shippers are willing to pay when a single temperature spike can destroy USD 5 million of active pharmaceutical ingredient. Expansion of electric-vehicle battery corridors across Europe and Asia-Pacific adds incremental, specification-heavy flows that small domestic haulers struggle to serve. Consequently, investment in advanced reefer tanks and telematics will remain a key differentiator within the chemical logistics market.

Geography Analysis

APAC Chemical Logistics Market

Asia-Pacific accounted for 39.21% of global revenue in 2025 and will expand at a 6.31% CAGR through 2031. China’s export overcapacity is propelling intra-Asian trade and rerouting cargo toward India and Southeast Asia, creating fresh multimodal lanes where ports, dedicated freight corridors, and coastal shipping converge. India’s PCPIR clusters anchor integrated complexes along the western and eastern seaboards, but inland demand growth is extending domestic road-rail legs, amplifying demand for ISO-tank repositioning services.

North America and Europe Chemical Logistics Market

North America and Europe remain premium markets, underpinned by extensive rail networks, strict safety rules, and high digital-adoption rates. Revised ADR and CLP frameworks in Europe require upgraded fleets and digital labels, encouraging shippers to lock in long-term contracts with certified providers. In North America, integrated rail corridors linking Gulf-Coast petrochemical complexes to Midwest consumers provide cost-effective, low-emission options that favor operators owning trans-load terminals.

South America and Africa Chemical Logistics Market

South America and Africa offer upside tempered by infrastructure gaps. Prolonged port dwell times in Lagos, Durban, and Mombasa inflate inventory costs and compel carriers to build buffer stocks. The African Continental Free Trade Area aspires to harmonize customs procedures, but interim fragmentation necessitates country-specific expertise and localized partnerships[4]MDPI, “African Continental Free Trade Area and Logistics Challenges,” mdpi.com . Despite these hurdles, nearshoring trends in Latin America are driving chemical manufacturers to relocate intermediate-processing stages closer to US buyers, stimulating corridor development for providers with bilingual staff and customs-broker networks.

Competitive Landscape

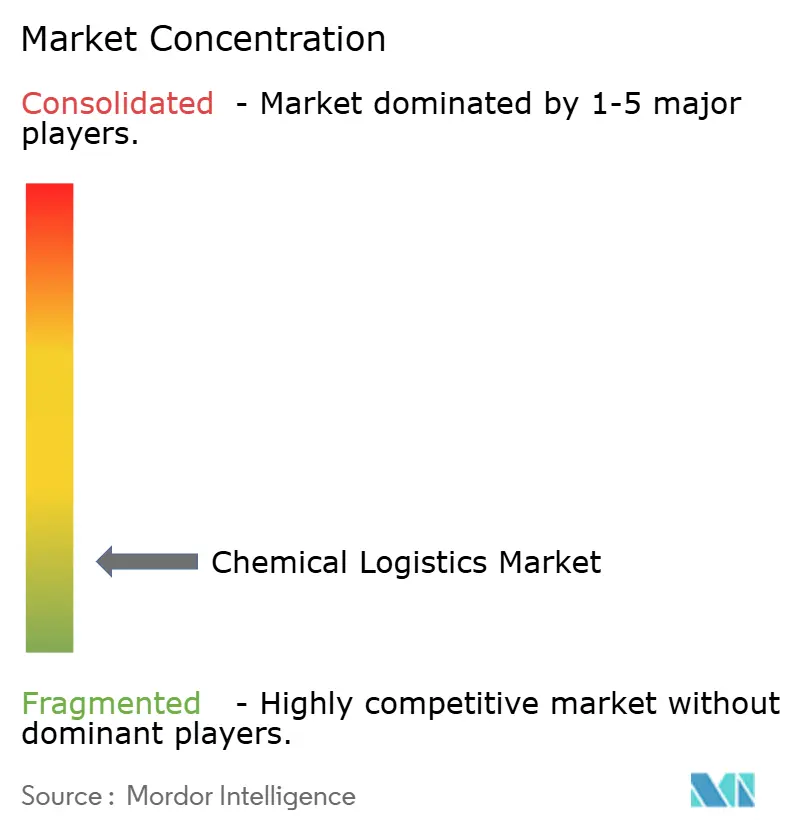

The chemical logistics market is fragmented; the top five providers captured roughly 25% global share in 2025. Scale, specialized assets, and compliance infrastructure underpin competitive advantage. DHL, Kuehne + Nagel, and Maersk integrate transportation, warehousing, and digital orchestration, enabling one-invoice models that resonate with multinational shippers. DSV consolidated its position by acquiring DB Schenker for EUR 14.3 billion (USD 16.70 billion), targeting DKK 9.0 billion (USD 1.41 billion) in annual synergies by 2028.

Strategic focus areas include temperature-controlled capacity, sustainability metrics, and digital platforms. DHL’s EUR 2 billion (USD 2.33 billion) health-logistics outlay adds GDP-compliant nodes across all continents, while Kuehne + Nagel’s visibility suite provides shipment-level carbon accounting, aligning with chemical-producer Scope 3 targets. Emerging digital brokers aggregate spare tank-container capacity but often lack licenses, insurance cover, and driver pools to manage hazmat moves, limiting disruption risk.

Asset specialists such as HOYER, Den Hartogh, and Bertschi maintain an edge in ISO-tank, rail-linked depots, and intermodal know-how, cultivating long-term contracts that cushion cyclical downturns. Tanker owners are greening fleets; NYK-Stolt ordered six methanol-ready ships capable of battery-hybrid propulsion, anticipating tightening IMO rules. Ultimately, competitive intensity will pivot on the ability to fuse compliance, sustainability, and digital transparency into integrated service propositions.

Chemical Logistics Industry Leaders

Deutsche Post DHL Group

Kuehne + Nagel

BDP International

DSV

A.P. Moller - Maersk

- *Disclaimer: Major Players sorted in no particular order

Chemical Logistics Market Companies Covered in this Report

- DHL Supply Chain

- Kuehne + Nagel International AG

- Maersk Logistics & Services

- HOYER Group

- C.H. Robinson Worldwide

- BDP International

- DSV (incl. DB Schenker)

- Rhenus SE & Co. KG

- A&R Logistics (Quantix)

- CEVA Logistics (Acquired by CMA CGM)

- Al-Futtaim Logistics

- Petrochem Middle East (PME)

- Sinotrans Chemical Logistics

- Bertschi AG

- Suttons Group

- Den Hartogh Logistics

- Brenntag Logistics Services

- MOL Chemical Tankers

- Stolt-Nielsen Ltd.

- Katoen Natie N.V.

- Toll Group

- Yusen Logistics Co., Ltd. (Nippon Yusen Group)

- Hellmann Worldwide Logistics SE & Co. KG*

Recent Industry Developments in Chemical Logistics Market

- November 2025: A major operator expanded its El Paso facility by 20,252 m² to support US–Mexico chemical flows and acquired Eastway for specialized cargo handling.

- September 2025: DHL bought SDS Rx to deepen final-mile radiopharmaceutical coverage in the United States.

- April 2025: DSV completed the DB Schenker takeover for approximately DKK 106.7 billion (USD 16.67 billion), creating a 160,000-employee global network.

- April 2025: DHL earmarked EUR 2 billion (USD 2.33 billion) for new GDP-compliant pharma hubs, allocating half the spend to the Americas.

Chemical Logistics Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the chemical logistics market as the aggregate revenue earned from transportation, warehousing, distribution, inventory management, and other value-added services that handle bulk and packaged chemicals across all hazard classes by road, rail, sea, air, and pipelines.

Scope exclusion: Direct-to-consumer parcel delivery of household chemical products is outside this assessment.

Segments Covered in This Report

- By Service

- Transportation

- Road

- Rail

- Sea/Ocean

- Air

- Warehousing, Distribution & Inventory Management

- Other Services

- Transportation

- By End-user Industry

- Pharmaceutical

- Cosmetics & Personal Care

- Oil & Gas

- Specialty Chemicals

- Other End-users

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed global 3PL managers, tanker-operator planners, chemical-plant logistics heads in Asia, Europe, and North America, and regional regulators overseeing dangerous-goods transit. Their insights clarified real-world cost ratios, capacity utilization swings, and emerging safety practices that secondary material alone could not quantify.

Desk Research

We began with public datasets such as UN Comtrade trade codes, OECD-ITF freight performance panels, the International Council of Chemical Associations' production indices, and national hazmat flow statistics from agencies like the US Bureau of Transportation Statistics. Company filings, investor presentations, and reputable trade journals added service mix and pricing context. Subscription tools including D&B Hoovers for 3PL financials and Dow Jones Factiva for deal tracking rounded out the desk review. These sources illustrate, rather than exhaust, the reference pool our analysts consulted.

Market-Sizing & Forecasting

A top-down build starts with global chemical output (tons and value) and applies mode-wise logistics spend shares that are narrowed by hazard class and temperature control. This is followed by regional trade reconstructions. Select bottom-up checks, sampled carrier revenues, port throughput, and average selling price × volume calculations validate and fine-tune totals. Key model drivers include chemical production tonnage, Freightos Baltic rate indices, new tank-container fleet additions, industrial GDP shifts, and announced chemical CAPEX pipelines. Multivariate regression, supplemented by scenario analysis for regulation or fuel-price shocks, projects the 2025-2030 trajectory.

Data Validation & Update Cycle

Outputs pass variance screens against independent freight metrics before two-level analyst reviews. Reports refresh every twelve months, with interim revisions when material events, such as regulation, strike, or supply shock, trigger re-contact of core respondents. A final sense-check is completed immediately before client release.

How Mordor Intelligence's Chemical Logistics Market Size Compares to Other Published Estimates

Published figures often differ because each firm chooses unique service baskets, pricing assumptions, and refresh rhythms. When we select inputs, we align them with observable trade flows and verified carrier billings, so decision-makers know exactly what the number embodies.

Key gap drivers include varying treatment of warehousing, exclusion of non-hazardous cargo by some publishers, divergent exchange-rate bases, and inconsistent uplift factors for fuel surcharges, which together widen estimate spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 509.8 B | Mordor Intelligence | |

| USD 303.1 B | Global Consultancy A | Covers transportation only; pipelines reported separately |

| USD 291.9 B | Research Publisher B | Uses fixed 2021 currency rates; omits non-hazardous flows |

| USD 275.1 B | Industry Journal C | Relies on averaged carrier revenues; overlooks recent freight-rate surge |

The comparison shows that when scope breadth, current pricing, and multi-source validation come together, Mordor delivers a balanced, transparent baseline that practitioners can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the projected value of the chemical logistics market in 2031?

The chemical logistics market size is forecast to reach USD 683.28 billion by 2031.

Which region will grow the fastest through 2031?

Asia-Pacific is expected to register a 6.31% CAGR, the highest among all regions.

Which service category is expanding more quickly than transportation?

Other Services including blending, compliance, and orchestration are advancing at a 6.41% CAGR.

Why are temperature-controlled shipments gaining share?

Their 7.25% CAGR is fueled by pharmaceutical chemicals and battery electrolytes that demand strict thermal stability.

How is regulation influencing market consolidation?

Higher ADR, CLP, and hazmat-fee requirements elevate compliance costs, encouraging mergers among operators that can spread fixed costs over larger volumes.

Page last updated on: