India Hazardous Chemical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

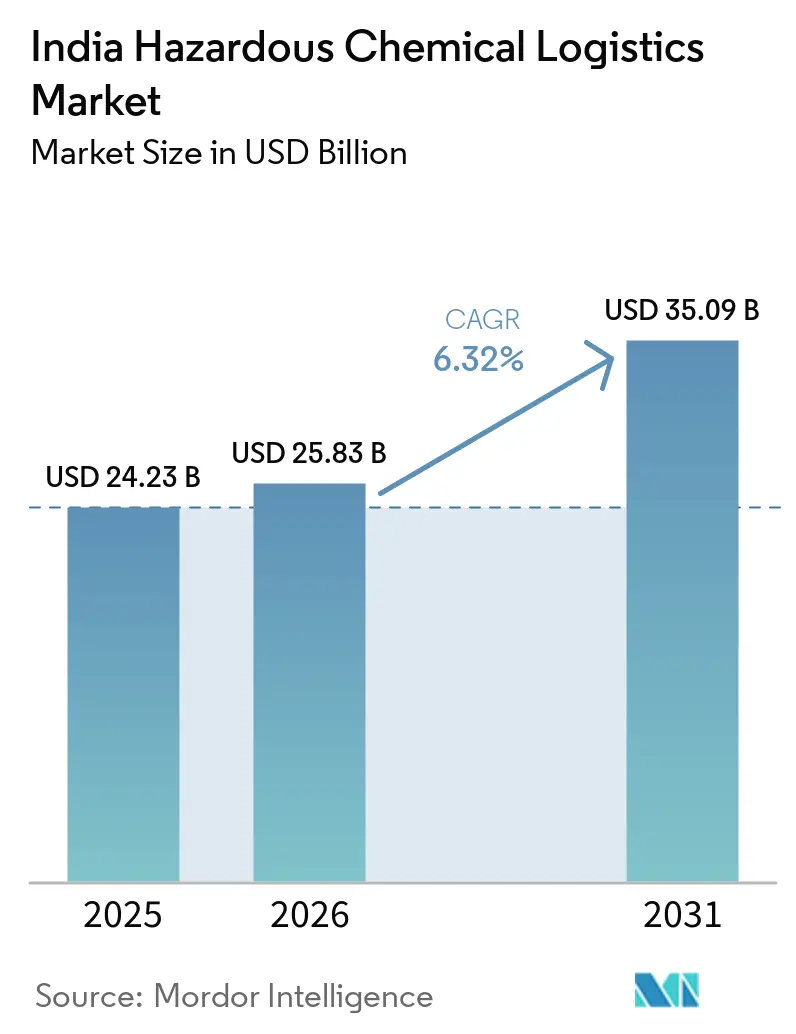

| Base Year Market Size (2025) | USD 24.23 Billion |

| Market Size (2026) | USD 25.83 Billion |

| Market Size (2031) | USD 35.09 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

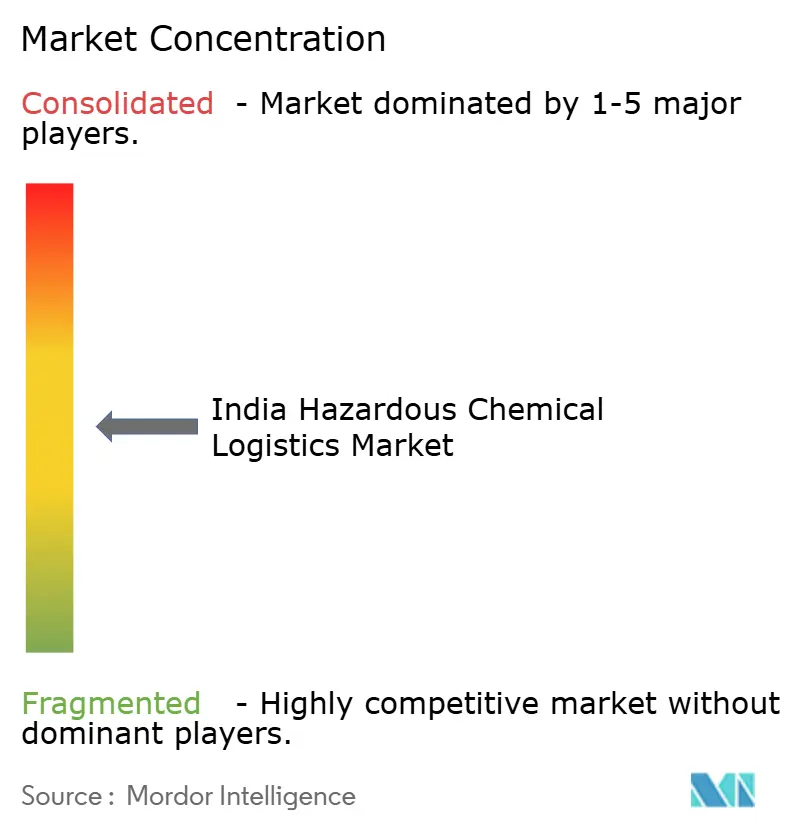

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Hazardous Chemical Logistics Market Analysis by Mordor Intelligence

India hazardous chemical logistics market size is expected to increase from USD 24.23 billion in 2025 to USD 25.83 billion in 2026 and reach USD 35.09 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

This trajectory reflects a blend of new petrochemical capacity along the coastline, rising demand for outsourced compliance services, and multimodal investments that shift bulk cargo from roads to pipelines, rail, and inland waterways. Producer preference for “one-stop” 3PL contracts, coupled with Petroleum and Explosives Safety Organization (PESO) mandates such as AIS-140 telematics and driver certification, is steering shippers toward large providers that can fund hazmat-graded fleets and warehouses. On the supply side, shortages of PESO-certified drivers lift wage premiums and keep fleet utilization tight, helping organized players defend margins. Meanwhile, greenfield projects such as Indian Oil’s Paradip cracker and Petronet LNG’s Dahej propane-dehydrogenation complex guarantee a steady stream of hazardous liquid and gas cargoes through 2031.

Key Report Takeaways

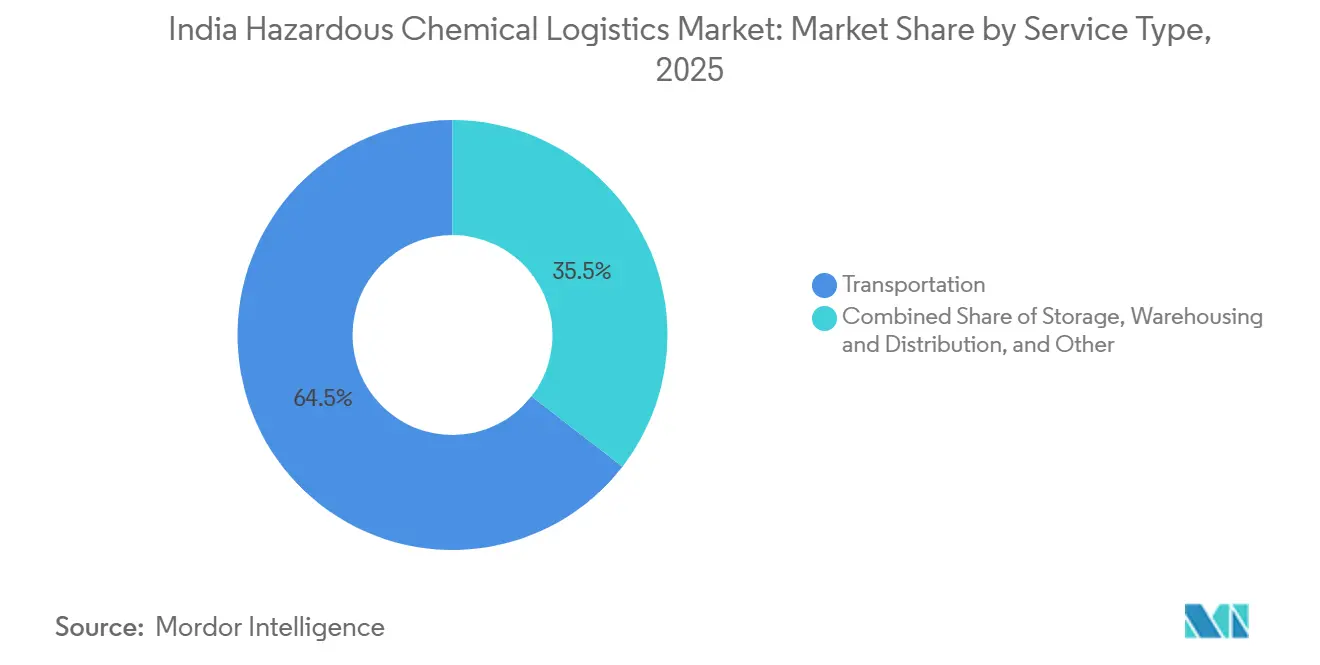

- By service type, transportation led with 64.51% of the India hazardous chemical logistics market share in 2025; value-added services are projected to expand at a 9.52% CAGR through 2031.

- By hazardous chemical class, flammable liquids commanded 37.53% of the India hazardous chemical logistics market size in 2025, while toxic substances are forecast to post an 8.65% CAGR to 2031.

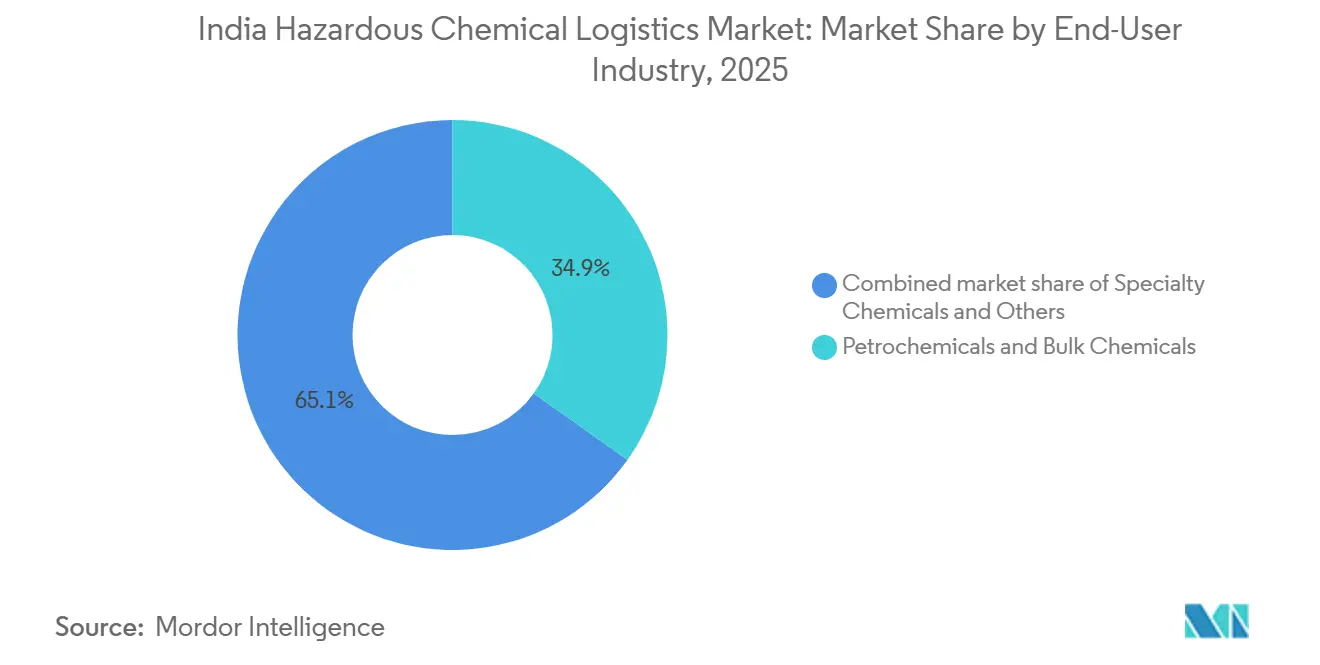

- By end-user, petrochemicals and bulk chemicals accounted for 34.88% of the India hazardous chemical logistics market share in 2025; pharmaceuticals and life sciences are on track for an 11.36% CAGR.

- By region, West India captured 40.11% of the logistics spend of the India hazardous chemical logistics market share in 2025, whereas South India is anticipated to grow at an 8.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Hazardous Chemical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of India's Overall Chemical Output (Bulk & Basic) | +1.8% | National, concentrated in Gujarat, Maharashtra, Odisha, Tamil Nadu | Long term (≥ 4 years) |

| Surge in Specialty & Pharma-Chemical Production Requiring Compliant Logistics | +1.5% | National, with early gains in Gujarat (Dahej, Ankleshwar), Himachal Pradesh (Una), Telangana (Hyderabad) | Medium term (2-4 years) |

| Expansion of Petrochemical & Refining Capacity Across Coastal Clusters | +1.3% | West India (Dahej, Hazira, Jamnagar), East India (Paradip, Haldia), South India (Cuddalore, Ennore) | Long term (≥ 4 years) |

| Stricter Hazardous-Materials Rules (PESO, IMDG, DG Shipping) Raising Outsourcing Demand | +0.9% | National, spill-over to coastal states (Gujarat, Maharashtra, Odisha, Tamil Nadu) | Short term (≤ 2 years) |

| Development of Petroleum, Chemicals & Petrochemicals Investment Regions (PCPIRs) | +0.6% | Gujarat (Dahej), Odisha (Paradip), Andhra Pradesh (Visakhapatnam), Tamil Nadu (Cuddalore-Nagapattinam) | Long term (≥ 4 years) |

| Inland-Waterway Corridors (NW-1, 4, 5) Opening Low-Cost Chemical Routes | +0.4% | East India (Ganga basin, Odisha coast), South India (Krishna-Godavari delta) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of India’s Overall Chemical Output (Bulk & Basic)

India’s chemicals output reached more than USD 220 billion in 2025 and is pegged to keep rising as new crackers in Rajasthan and Odisha ramp up capacity. Each additional tonne of caustic soda, chlorine, or methanol must move in PESO-certified tankers, ISO containers, or rail rakes, driving sustained demand for compliant logistics services. Indian Oil’s Paradip–Haldia pipeline alone is expected to displace roughly 10,000 annual truck trips, freeing road bandwidth for specialty cargoes. Similar pipeline and tank-farm expansions by Aegis Logistics show how storage and evacuation assets scale line by line with upstream production. The long-term volume uplift persists because India’s per capita petrochemical consumption is one-third the world average.

Surge in Specialty & Pharma‐Chemical Production Requiring Compliant Logistics

Specialty and pharmaceutical chemicals entail smaller lot sizes, stricter temperature bands, and real-time traceability. New active pharmaceutical ingredient (API) parks in Una and Vizag, plus fluorochemical investments in Gujarat and Tamil Nadu, create high-margin lanes for temperature-controlled trucking, repackaging, and emergency response planning. Snowman Logistics and Kuehne + Nagel are already commissioning 15-25 °C warehouses with gas detection and batch-level barcoding to win five-year outsourcing contracts. Mid-term growth remains solid as commissioned plants ramp from trial to commercial output over 24-36 months.

Expansion of Petrochemical and Refining Capacity Across Coastal Clusters

Coastal clusters such as Dahej, Paradip, and Cuddalore attract new crackers because they offer access to feedstock, deep-draft jetties, and pipeline links to inland consumption centers. Paradip’s upcoming 1.5 million tpa naphtha cracker integrates with a 344 km pipeline, slashing road tanker movements and accident risk. In Maharashtra, two new liquid-cargo berths at Jawaharlal Nehru Port Trust add swing capacity for bulk acids and solvents, shortening vessel wait times indianinfrastructure.com. Over a four-year horizon, each coastal mega-project multiplies the inbound ammonia, LPG, and naphtha cargos that must be stored, degassed, and evacuated in accordance with International Maritime Dangerous Goods (IMDG) protocols.

Stricter Hazardous-Materials Rules (PESO, IMDG, DG Shipping) Raising Outsourcing Demand

New rules compel every hazmat truck to carry AIS-140 telematics with NavIC positioning, battery backup, and a panic button. Maharashtra added a three-day driver-training mandate with annual refreshers in September 2024, and similar statutes are rolling out statewide. Shippers are short on compliance bandwidth; therefore, they shift loads to third-party specialists who already run certified fleets and PESO-graded yards. Allcargo’s newly opened Uran chemical warehouse features capex premium foam suppression, in-rack sprinklers, and battery-powered forklifts that few small fleets can finance. This near-term compliance shock sends more volume to national 3PLs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Compliance Costs for Hazmat-Graded Fleets and Warehouses | -0.8% | National, acute in tier-2/tier-3 cities lacking PESO-certified infrastructure | Short term (≤ 2 years) |

| Acute Shortage of HAZMAT-Certified Drivers and Handlers | -0.7% | National, severe in East India (Odisha, West Bengal, Bihar) and Central India | Medium term (2-4 years) |

| State-Wise Regulatory Fragmentation Slowing Multimodal Transfers | -0.5% | National, bottlenecks at Gujarat-Rajasthan, Maharashtra-Karnataka, Odisha-West Bengal borders | Medium term (2-4 years) |

| CRZ Clearance Delays for New Coastal Chemical Terminals | -0.3% | Coastal states (Gujarat, Maharashtra, Tamil Nadu, Odisha, Andhra Pradesh) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Compliance Costs for Hazmat-Graded Fleets & Warehouses

A stainless-steel chemical tanker that meets PESO’s Static & Mobile Pressure Vessels Rules 2016 costs USD 60,000-85,000, roughly double a standard fuel tanker. Annual certifications, specialized insurance, and driver training add another USD 6,000-10,000 per vehicle, making fleet renewal a capital-intensive exercise for small operators. Warehouse automation is equally pricey: Godrej’s new 120-foot rack-clad store in Mumbai required robotic shuttles and explosion-proof wiring, pushing investment past USD 500 per square foot. In the short run, high entry costs curb fresh capacity and slow response to demand spikes.

Acute Shortage of HAZMAT-Certified Drivers and Handlers

India faces a 2.2 million shortfall in skilled drivers, and only a fraction hold hazmat endorsements. Earnings lag city driving gigs, and health risks deter new entrants, leading to empty seats on otherwise available tankers. The government's plan to set up 1,600 training institutes is welcome, yet the first graduates will not enter the workforce until 2027, prolonging the squeeze. As a stopgap, major 3PLs run in-house academies, but small carriers cannot match those stipends, limiting national capacity growth. The restraint’s impact peaks in the medium term until a fresh labor supply materializes.[1]Press Information Bureau, “India Faces 2.2 Million Driver Shortage,” pib.gov.in

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates but Services Accelerate

Transportation accounted for 64.51% of the India hazardous chemical logistics market share in 2025, reflecting the country’s reliance on road tankers for last-mile delivery. Rail is regaining ground as AVG Logistics’ ISO-tank trains cut unit costs by 25% and bypass driver shortages. Sea and inland waterways remain underpenetrated despite clear cost advantages; draft limits on National Waterways 4 and 5 keep barge sizes small. Over 2026-2031, value-added services, led by blending, relabeling, and emergency-response planning, will post the fastest 9.52% CAGR as pharma and specialty shippers outsource compliance headaches. Snowman’s new 50,000 sq ft hazmat-cold store in Tamil Nadu and Kuehne+Nagel’s expanded 450,000 m² contract-logistics footprint show providers pivoting toward high-margin ancillary work that cushions rate volatility.

The India hazardous chemical logistics market size for value-added services is forecast to advance steadily as PESO tightens warehouse rules. AIS-140 telematics unlock geo-fencing, predictive maintenance, and batch-level audit trails, thereby raising switching costs. Bigger players leverage captive tech stacks to bundle transport with warehousing, thus improving retention and margin per load. Investments in foam-suppressed racks and battery-powered forklifts set entry barriers that small regional carriers struggle to cross, signaling ongoing consolidation.[2]Ministry of Road Transport and Highways, “Mandatory AIS-140 Tracking Devices for Hazardous Goods Vehicles,” morth.nic.in

By Hazardous Chemical Class: Flammables Lead, Toxics Grow Fastest

Flammable liquids held 37.53% of the India hazardous chemical logistics market size in 2025, fueled by naphtha and methanol flows from coastal refineries to inland converters. Dedicated stainless-steel tankers and pipeline corridors, such as Indian Oil’s Paradip-Haldia link, support efficiency gains by shifting bulk loads off congested highways. The fastest growth, however, will come from toxic substances, projected at an 8.65% CAGR to 2031 as lithium-battery electrolytes, fluoropolymers, and pharmaceutical precursors ramp up.

India hazardous chemical logistics market share for toxic cargoes will widen as Neogen’s 30,000 tpy electrolyte unit and Altmin’s lithium-iron-phosphate plant go live. Handling protocols require nitrogen-purged containers and temperature monitoring to pre-empt thermal runaway, making each tonne of toxics more service-intensive than a tonne of bulk solvents. Operators with sealed-floor warehouses, gas-detection arrays, and 24 × 7 emergency squads are positioned to capture premium contracts, while small fleets stay focused on lower-hazard flammables.

By End-User Industry: Petrochemicals Largest, Pharma Fastest

Petrochemicals and bulk chemicals accounted for 34.88% of the India hazardous chemical logistics market share in 2025, riding on mega-sites such as Reliance’s Jamnagar refinery and Petronet LNG’s Dahej complex. Volume stability, long contract tenures, and dedicated pipelines make this base load attractive for asset-heavy 3PLs. On the flip side, pharmaceuticals and life sciences will clock the swiftest 11.36% CAGR as Production Linked Incentive (PLI) parks in Una district (Himachal Pradesh), and Vizag coalesce into new API hubs.

The India hazardous chemical logistics market dedicated to pharma is expanding as small-batch, temperature-sensitive APIs require GDP-compliant (Good Distribution Practice) storage, validated reefers, and batch traceability. Snowman and DHL Supply Chain are adding clean rooms and 15-25 °C zones to lock in pharmaceutical clients for five-year bundles. Meanwhile, petrochemical shippers remain cost-centric, negotiating take-or-pay contracts that underpin tank-farm utilization for players like Aegis Logistics.[3]Department of Pharmaceuticals, “Production Linked Incentive (PLI) Scheme for Promoting Domestic Manufacturing of Active Pharmaceutical Ingredients (APIs),” pharmaceuticals.gov.in

Geography Analysis

West India dominated 2025 spending with a 40.11% share, thanks to the Dahej-Hazira PCPIR, Jamnagar’s refining complex, and container gateways at Mundra and Kandla. Continuous tank-farm upgrades, LNG regasification expansions, and two fresh berths at Jawaharlal Nehru Port Trust keep the corridor attractive for bulk liquids. Yet capacity is tightening; driver shortages and road congestion are lifting landed costs, urging shippers to consider rail and coastal barges where draft permits are available.

South India is set to post the fastest 8.45% CAGR through 2031. Catalysts include Haldia Petrochemicals’ USD 10 billion oil-to-chemicals project at Cuddalore and Chennai Petroleum’s new refinery-cracker combo at Nagapattinam. Battery-materials plants in Telangana and Andhra Pradesh add toxic cargo lanes, requiring nitrogen-blanketed tankers and refrigerated trucks from Hyderabad to Pune and Bengaluru assembly plants. Dedicated chemical jetties planned for Cuddalore and Kakinada, once approved, will cut trucking distances by over 250 km per trip and alleviate highway risk.

East India’s share is smaller but rising as Indian Oil’s USD 7.39 billion Paradip complex and a new green-hydrogen jetty position Odisha as an ammonia-export node. The Paradip-Haldia 344 km pipeline eliminates up to 10,000 hazardous truck runs annually on National Highway-16, though inland waterways still face draft limitations that limit barge sizes. State-wise variations in permit cycles and Coastal Regulation Zone clearances remain hurdles, but Jalvahak dredging and public-private jetty investments should unlock fuller loads by 2028.[4]Department of Chemicals and Petrochemicals, “Petroleum, Chemicals and Petrochemical Investment Regions (PCPIR),” chemicals.gov.in

Competitive Landscape

Global integrators (DHL Supply Chain, DSV, Kuehne + Nagel) and domestic specialists (Aegis Logistics, TCI Chemlog, Allcargo) vie for multi-year take-or-pay contracts with petrochemical majors. Deep pockets help the big five fund PESO-graded terminals, AIS-140 retrofits, and in-house driver academies, creating moats around fleet scale and compliance know-how. Driver scarcity pushes wages up 15-20%, but premium rates offset cost inflation for organized fleets.

Strategically, incumbents double down on integrated propositions. Aegis earmarked USD 177 million in FY 2025 for 61,000 kiloliters of new storage and an ammonia terminal due by FY 2027, while lining up a USD 484 million IPO for its Aegis Vopak joint venture. Allcargo opened a 160,000 sq ft Grade-A chemical store near Mumbai with foam suppression and WMS, and mapped three more PESO sites in Bhiwandi, Vapi, and North India. These moves lock shippers into bundled storage-plus-distribution deals that smooth revenue across cycles.

White-space opportunities orbit inland waterways, where no IMDG-certified barge operator yet dominates. AVG Logistics’ ISO-tank rail model translates readily to barge service once National Waterways 1, 4, and 5 reach full dredge depths. Foreign specialists like Den Hartogh, newly allied with Bhatinda Industrial Gases, eye cryogenic-gas transport niches where expertise and safety records command premium yields even at modest volumes.

India Hazardous Chemical Logistics Industry Leaders

Aegis Logistics Ltd

TCI Chemlog

DHL Group

MOL Chemical Tankers

Rhenus Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Petronet LNG expanded the Dahej terminal to 22.5 MMTPA, adding 5 MMTPA of regas throughput.

- March 2026: Den Hartogh Logistics signed a capacity expansion pact with Bhatinda Industrial Gases.

- February 2026: JSW JNPT Liquid Terminal received a completion certificate for two new berths at Jawaharlal Nehru Port Trust.

- February 2026: The government cleared a USD 96 million dedicated green-hydrogen jetty at Paradip Port.

India Hazardous Chemical Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea / Coastal and Inland Waterways | |

| Air | |

| Storage, Warehousing and Distribution | |

| Value Added Services |

| Flammable Liquids |

| Compressed Gases |

| Corrosive Substances |

| Toxic Substances |

| Oxidizing Substances |

| Radioactive Materials |

| Other Chemicals |

| Petrochemicals and Bulk Chemicals |

| Specialty Chemicals |

| Pharmaceuticals and Life Sciences |

| Agrochemicals and Fertilizers |

| Batteries, Electronics and EV Materials |

| Other Industries |

| North India |

| South India |

| West India |

| East India |

| Central India |

| Segmentation by Service Type | Transportation | Road |

| Rail | ||

| Sea / Coastal and Inland Waterways | ||

| Air | ||

| Storage, Warehousing and Distribution | ||

| Value Added Services | ||

| Segmentation by Hazardous Chemical Class | Flammable Liquids | |

| Compressed Gases | ||

| Corrosive Substances | ||

| Toxic Substances | ||

| Oxidizing Substances | ||

| Radioactive Materials | ||

| Other Chemicals | ||

| Segmentation by End-User Industry | Petrochemicals and Bulk Chemicals | |

| Specialty Chemicals | ||

| Pharmaceuticals and Life Sciences | ||

| Agrochemicals and Fertilizers | ||

| Batteries, Electronics and EV Materials | ||

| Other Industries | ||

| Segmentation by Region | North India | |

| South India | ||

| West India | ||

| East India | ||

| Central India |

Key Questions Answered in the Report

How large is the India hazardous chemical logistics market today?

The India hazardous chemical logistics market size reached USD 24.23 billion in 2025 and is projected at USD 35.09 billion by 2031.

Which service segment is expanding the fastest?

Value-added services such as blending, repackaging, labeling, and emergency planning are set for a 9.52% CAGR through 2031

What geography will drive future growth?

South India should log the quickest 8.45% CAGR as new petrochemical and battery-material hubs come online around Cuddalore, Ennore, Telangana, and Andhra Pradesh.

Why is driver availability a concern?

India is short about 2.2 million commercial drivers, and hazmat endorsements add extra training time and cost, creating a structural labor gap.

How are new safety rules affecting costs?

PESO mandates for AIS-140 telematics and annual driver refreshers lift capital and operating costs, prompting many shippers to outsource to specialized 3PLs that already comply.

Page last updated on: