Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

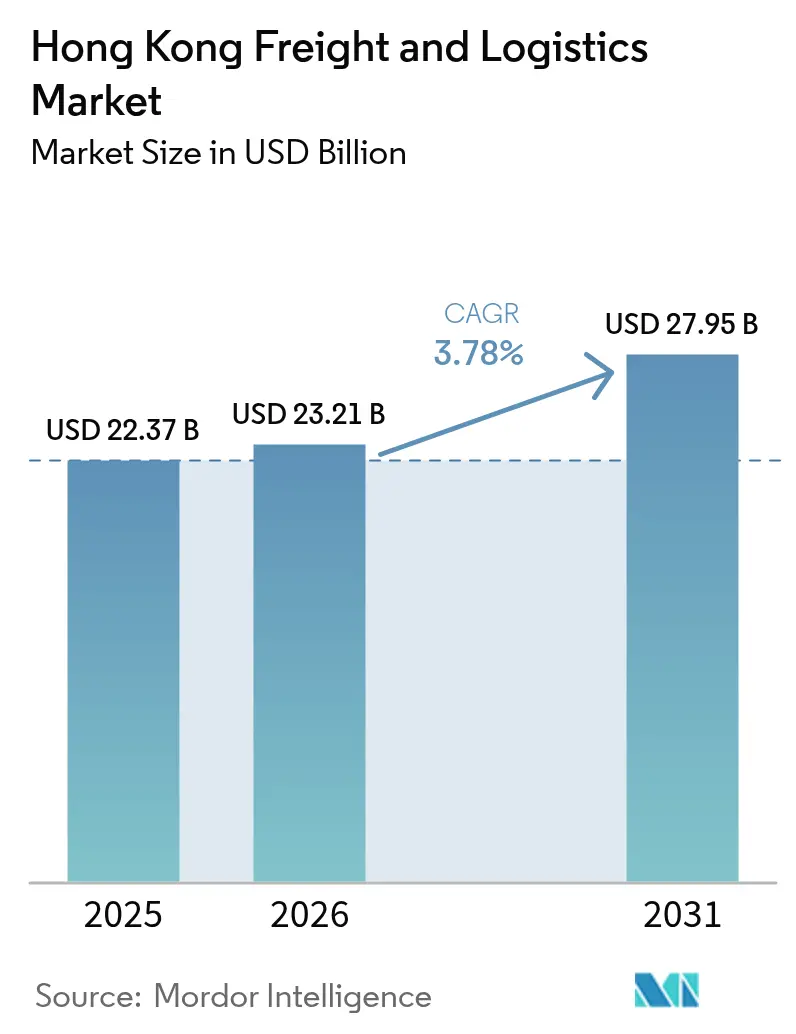

| Base Year Market Size (2025) | USD 22.37 Billion |

| Market Size (2026) | USD 23.21 Billion |

| Market Size (2031) | USD 27.95 Billion |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

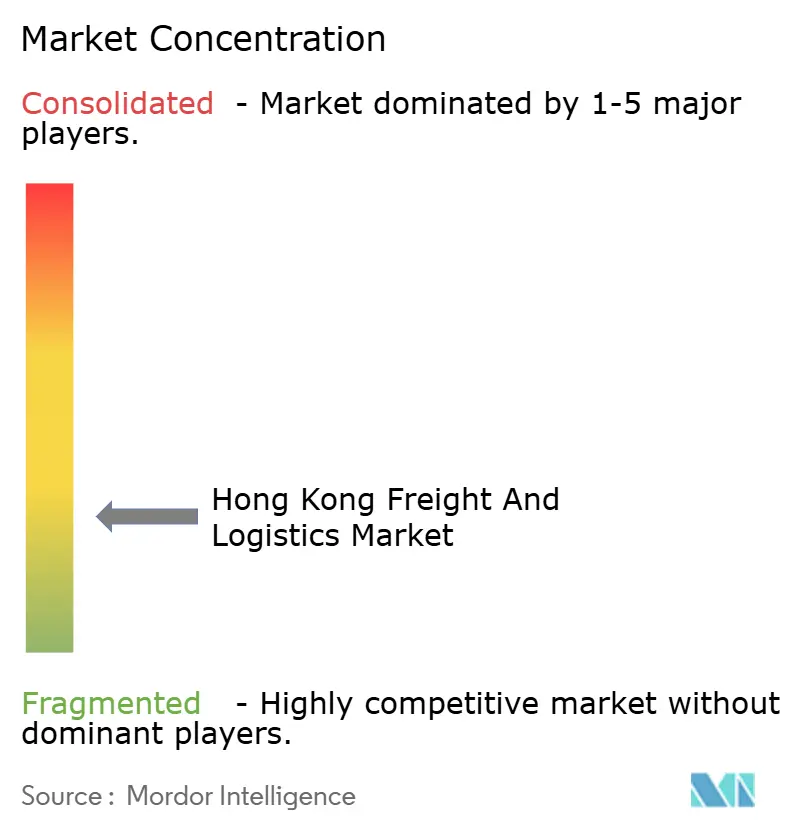

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Freight And Logistics Market Analysis by Mordor Intelligence

The Hong Kong Freight And Logistics Market size is expected to grow from USD 22.37 billion in 2025 to USD 23.21 billion in 2026 and is forecast to reach USD 27.95 billion by 2031 at 3.78% CAGR over 2026-2031.

Robust cross-border e-commerce growth, government-backed infrastructure upgrades, and increasing demand for temperature-controlled logistics underpin steady expansion. Competitive pressures from mainland China ports, elevated operating costs, and labor shortages moderate—but do not derail—growth momentum. Large-scale mergers such as DSV’s purchase of DB Schenker and CK Hutchison’s ports divestment reshape market structure, while automation investments at Hong Kong International Airport (HKIA) raise service efficiency. Warehouse oversupply near HKIA keeps rents soft, yet premium cold-chain facilities maintain pricing power.

Key Report Takeaways

- By logistics function, freight transport held 58.45% of the Hong Kong freight and logistics market share in 2025, while courier, express, and parcel services are advancing at a 4.44% CAGR through 2031.

- By freight transport mode, road captured 61.40% share in 2025, whereas air freight is forecast to accelerate at 4.55% CAGR to 2031.

- By CEP destination, domestic services accounted for 65.25% of the Hong Kong freight and logistics market size in 2025, and international CEP is projected to expand at 4.62% CAGR over 2026-2031.

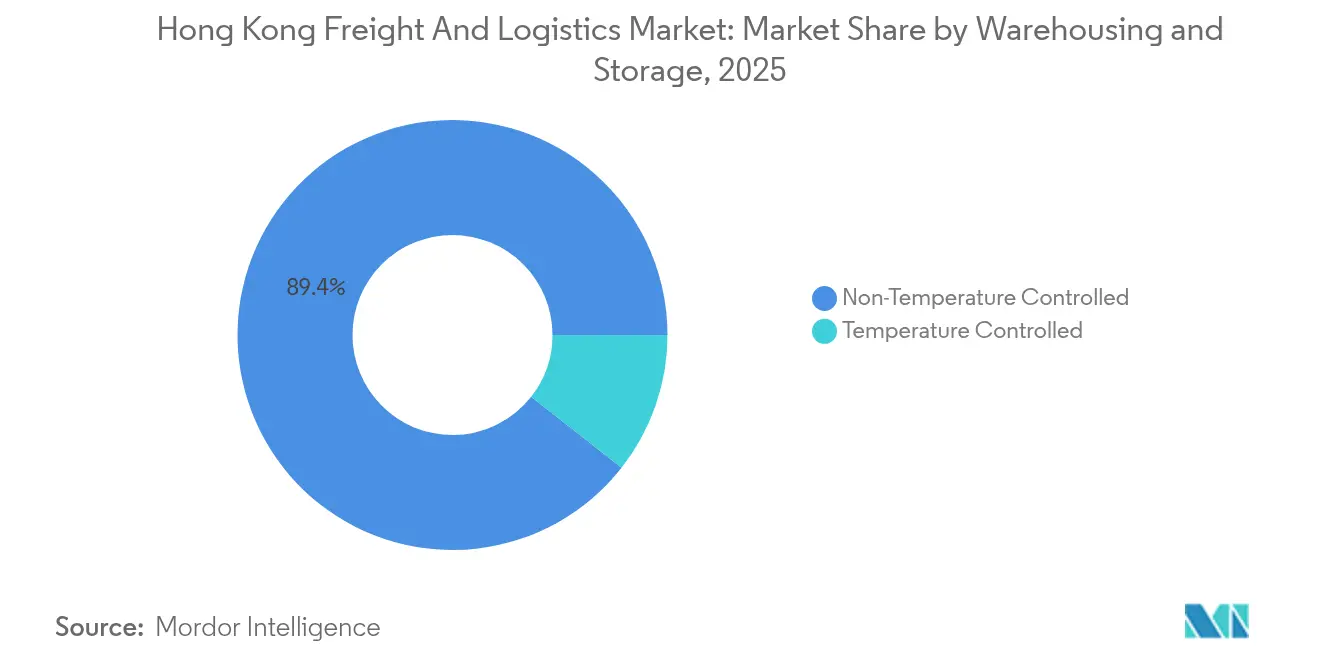

- By warehousing temperature control, ambient facilities represented 89.40% share in 2025; temperature-controlled space is growing at 4.33% CAGR through 2031.

- By freight forwarding mode, sea and inland waterways held 54.10% share in 2025 and are expected to grow at 4.21% CAGR to 2031.

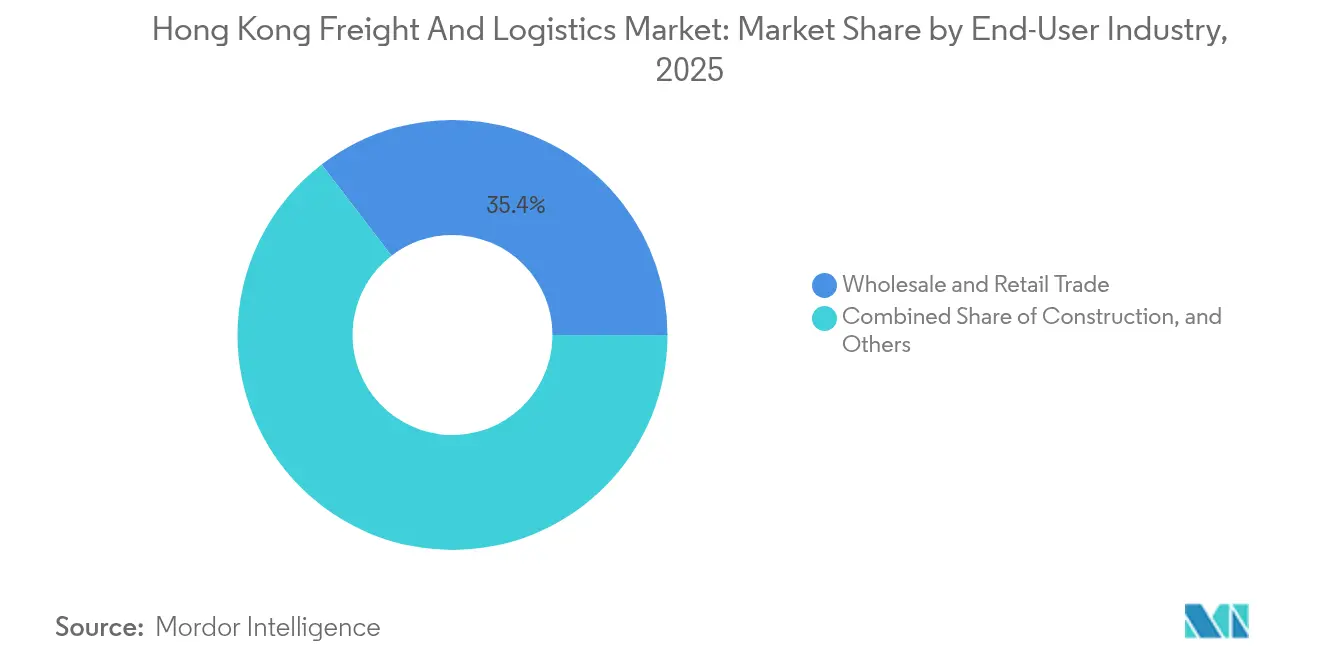

- By end-user industry, wholesale and retail trade led with 35.42% revenue share in 2025 and is also the fastest-growing segment, set for 4.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border e-commerce surge | +1.2% | Greater Bay Area and ASEAN | Medium term (2-4 years) |

| Smart port and HKIA 3RS investment | +0.8% | Hong Kong | Long term (≥ 4 years) |

| Cold-chain demand for pharma and F&B | +0.6% | Hong Kong, Macau, Pearl River Delta | Medium term (2-4 years) |

| Greater Bay Area integration and CEPA | +0.9% | Mainland China and Hong Kong | Long term (≥ 4 years) |

| Fintech hardware inflow | +0.4% | Hong Kong | Short term (≤ 2 years) |

| LME warehousing approval | +0.3% | Global metals trade via Hong Kong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Cross-Border E-Commerce Volumes

Greater Bay Area customs data show Shenzhen’s cross-border e-commerce value growing roughly 35-fold in five years, funneling high-margin volumes into Hong Kong’s air-cargo and express channels. Consumer penetration in local e-commerce reached 80.9% in 2023, reinforcing demand for same-day and next-day delivery. Operators such as HKTVmall opened fully automated warehouses to handle always-on order cycles, prompting courier firms to expand pickup density and invest in advanced sortation. Intensifying parcel flows lift CEP tonnage and support rising fulfillment center leasing, offsetting volume losses in traditional seaborne transshipment. However, service providers must re-optimize route planning to cope with peak-season volatility and rising return rates[1]“Half-Yearly Monetary and Financial Stability Report,” Hong Kong Monetary Authority, hkma.gov.hk .

Government Investment in Smart Port and HKIA 3RS

HKIA’s Three-Runway System commenced full operations in November 2024, lifting annual throughput capacity by 50% and reducing queuing delays. Complementary public funding of HKD 1 billion (USD 128.05 million) for the Hong Kong AI Research Institute channels research into autonomous yard vehicles, digital port community systems, and predictive cargo routing. DHL’s EUR 377 million (USD 416.07 million) Central Asia Hub expansion aligns private capital with public upgrades, delivering real-time cargo visibility and shorter dwell times. Policy support also extends to low-altitude economy test beds that accelerate drone delivery pilots. These developments collectively elevate Hong Kong’s competitiveness for time-critical shipments against Guangzhou or Shenzhen airports[2]“eCommerce – Hong Kong & Macau,” International Trade Administration, trade.gov .

Growing Cold-Chain Demand from Pharma and F&B

Temperature-controlled space posts the highest rental premiums as vaccine distribution, biologics trials, and specialty food imports grow. UPS allocated over USD 250 million for a Hong Kong cold-chain hub opening in 2028, targeting pharma clients that require GDP compliance. Warehouse operators install multi-chamber designs with redundancy, enabling 2-8 °C and -20 °C storage within single sites. Pharmaceutical makers leverage Hong Kong’s re-export gateway status to reach Southeast Asian clinics faster, while luxury food retailers lengthen shelf life of imported seafood and dairy. Rising energy bills push operators toward solar rooftops and high-efficiency refrigeration.

Integration with Greater Bay Area and CEPA Benefits

CEPA preferential rules of origin and streamlined customs procedures deepen cross-border trucking linkages connecting Hong Kong with Shenzhen, Guangzhou, and Dongguan. The five largest GBA cities generate 84% of regional GDP, underpinning steady lane demand for general cargo and finished electronics. RMB trade settlement handled by Hong Kong banks reached RMB 8.69 trillion (USD 1.22 trillion) in the first seven months of 2024, reinforcing the territory’s treasury-center role. Eased licensing helps Hong Kong freight forwarders secure mainland permits faster, lowering administrative costs and improving door-to-door visibility. Private fleets exploit the Hong Kong-Zhuhai-Macau Bridge to serve west-bank Pearl River Delta factories in a single shift[3]“Three-Runway System Operational,” Transport and Logistics Bureau, transport.gov.hk.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating fuel and electricity costs | -0.7% | Hong Kong | Short term (≤ 2 years) |

| Skilled-labor shortages | -0.5% | Hong Kong | Medium term (2-4 years) |

| Port-call bypass by carrier alliances | -1.1% | Hong Kong and South China | Long term (≥ 4 years) |

| Warehouse rent pressure from Cainiao supply | -0.3% | HKIA precinct | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Fuel and Electricity Costs Amid Carbon Measures

Marine bunker surcharges and peak-season trucking fuel premiums weigh on operator margins, with carriers quoting fees of USD 1,125-1,700 per FEU in January 2025. Hong Kong’s roadmap to carbon neutrality by 2050 layers costs for low-sulfur fuel and energy audits. Electricity tariffs remain high due to limited domestic generation, challenging operators of high-draw cold stores. Firms accelerate fleet renewal toward LNG trucks and explore power-purchase agreements to hedge price swings. Compliance with the IMO’s Carbon Intensity Indicator adds reporting complexity for ship agents.

Skilled-Labour Shortages in Warehousing and Trucking

An aging workforce and net natural population decline of 18,100 in 2024 shrink the pool of forklift drivers and cross-border truckers. Forecast shortfalls reach 180,000 workers by 2028, inflating overtime wage bills and straining service reliability. Government talent-list schemes attract foreign logistics professionals, yet visa processing nascently meets demand. Operators respond by installing automatic storage and retrieval systems and upskilling staff for maintenance roles. Collaboration with vocational institutes on cold-chain certifications eases compliance gaps but takes time to scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Retail Trade Dominance Across Growth Metrics

Wholesale and retail trade delivered 35.42% share in 2025 and is set to grow fastest at 4.08% CAGR, underpinned by tourism rebound and luxury brand restocking. Retailers demand omnichannel fulfillment, spurring dark-store conversions and last-mile collaborations with ride-hailing fleets. Manufacturing continues to rely on Hong Kong as a distribution switchboard for high-value electronics and apparel, though some volume diverts to bonded zones in Shenzhen.

Construction logistics benefit from major railway and land-reclamation projects that require heavy lift and oversized cargo coordination. Oil, gas, and mining movements center on drilling equipment and metal concentrates; prospects brighten with impending LME warehouse accreditation. Other sectors, including healthcare and professional services create niche demand for document management, sensitive data storage, and secure destruction.

By Logistics Function: Freight Transport Dominance Amid Express Growth

Freight transport controlled 58.45% of the Hong Kong freight and logistics market in 2025, reflecting entrenched road and maritime corridors connecting the city with Pearl River Delta factories. Courier, express, and parcel services are scaling fastest with a 4.44% CAGR to 2031, lifted by omnichannel retail and high import parcel ratios. The freight transport segment leverages the Hong Kong-Zhuhai-Macau Bridge for same-day trucking loops and remains the backbone for inbound components and outbound finished goods. Yet direct ocean services from Shenzhen challenge Hong Kong’s transshipment role, nudging carriers to offer bundled customs brokerage and bonded trucking.

Warehousing and storage deliver steady cash flows; ambient facilities occupy 89.40% of total capacity, while temperature-controlled space grows to meet vaccine and gourmet food inflows. Freight forwarding maintains relevance through complex routing solutions, with sea and inland waterways accounting for 54.10% of forwarding value. Other services such as supply-chain consulting and customs advisory gain share as shippers seek visibility and compliance expertise. Integration of digital freight platforms and EDI interfaces reduces paperwork and strengthens customer retention.

By CEP Destination: Domestic Strength with International Momentum

Domestic CEP services represented 65.25% of the Hong Kong freight and logistics market in 2025, anchored by dense urban delivery radii and high consumer expectations for intra-day fulfillment. Operators deploy micro-fulfillment centers inside industrial buildings to mitigate traffic delays. International CEP volumes accelerate at 4.62% CAGR, driven by cross-border marketplaces shipping into mainland China and Southeast Asia. SF Express’s 2024 Hong Kong IPO financed fleet expansion, and major players adopt digital customs clearance tools to cut last-leg latency.

Expanding duty-free order flows via CEPA reduce clearance costs, inviting SMEs to widen product catalogs. Service enhancements, such as guaranteed two-way returns and merchant analytics, differentiate premium international offerings. Regulatory alignment on HS code pre-lodgment encourages data-driven planning and helps carriers proactively resolve inspection holds.

By Warehousing Temperature Control: Ambient Dominance with Cold-Chain Expansion

Ambient inventory dominates with 89.40% share, storing apparel, electronics, and general merchandise. Nonetheless, temperature-controlled space grows at 4.33% CAGR as pharmaceutical firms and gourmet retailers escalate throughput. Cold-chain investments focus on modular racking, real-time sensor networks, and backup generators to meet stringent GDP protocols. UPS and DHL integrate cross-dock cold tunnels enabling unbroken temperature tracks from tarmac to chamber.

Oversupply in the ambient segment pressures effective rents, prompting conversions of older blocks into data centers or light assembly usage. Cold-chain operators sidestep rate erosion due to limited specialized stock and high fit-out costs. The Hong Kong freight and logistics market size attributable to cold-chain is expected to rise as regional vaccine trials and high-end food culture flourish.

By Freight Transport Mode: Road Leadership with Air Acceleration

Road shipments commanded 61.40% share in 2025, sustained by flexible cross-boundary trucking permits and bonded corridors linking Hong Kong with Shenzhen. Infrastructure upgrades enable 24-hour clearing at major land ports, shortening dwell time. Air freight, though smaller, is slated for a 4.55% CAGR, propelled by HKIA’s expanded slots and carrier fleet renewals. The Hong Kong freight and logistics market size for air cargo is expected to widen as fin-tech hardware and luxury items favor premium transit times. Maritime operators retain substantial volumes but confront margin pressure from direct calls at Nansha and Yantian.

Rail remains niche, serving select cold-chain and high-value electronics corridors through the West Kowloon link into mainland high-speed networks. Pipelines cater to fuel and chemical cargoes, with capacity expansion limited by land scarcity. Modal diversification strategies emphasize resilience, prompting 3PLs to offer integrated ocean-air solutions and cadence-based trucking runs.

By Freight Forwarding Mode: Maritime Leadership with Steady Growth

Sea and inland waterways captured 54.10% of forwarding revenue in 2025 and will remain front-runner, expanding at 4.21% CAGR to 2031. Forwarders navigate alliance reshuffles by securing space commitments across multiple carriers and leveraging digital rate management tools. Air forwarding retains a niche for time-critical shipments, with value-added services such as charter broking and temperature-controlled ULD leasing. Multimodal solutions gain traction to cushion rate swings and mitigate port congestion.

Kerry Logistics holds a top-15 global ocean forwarding rank, underscoring Hong Kong’s strategic role in maritime brokerage. The Hong Kong freight and logistics market share for forwarding remains split among incumbents with integrated warehousing and emerging digital brokers courting SMEs through self-service portals.

Geography Analysis

Hong Kong operates as the services nucleus of the USD 1.7-1.8 trillion Greater Bay Area economy, providing premium logistics, finance, and legal frameworks to manufacturing cities like Shenzhen, Dongguan, and Foshan. Cross-boundary bridges and rapid rail shorten transit cycles, enhancing just-in-time delivery for mainland factories. Despite losing a top-10 global port ranking, Hong Kong retains a competitive edge in regulatory rigor and duty-free re-exports. The city is forecast to surpass Switzerland as the world’s largest cross-border wealth center by 2026-27, bolstering demand for secure valuables transport.

Visitor arrivals of 29.5 million for January-August 2024, equal to 68% of 2019 levels, revive passenger belly-hold cargo capacity. Macau integration delivers incremental parcel flows since HKTVmall launched service to Macau in late 2022, signaling intraregional network synergies. Still, pressure from mainland ports forces Hong Kong to specialize in time-critical and value-added services instead of volume-driven transshipment. Government smart port roadmaps and AI institute funding intend to reinforce this premium positioning through digital twins and predictive yard planning.

Near-term rental and labor constraints mirror conditions in other mature Asia-Pacific cities yet remain more pronounced due to land scarcity. To cope, operators adopt vertical racking and stacker-crane systems to raise throughput. Financial incentives such as super-allowances for green equipment offset capex, ensuring Hong Kong sustains its role as a high-service gateway for the Greater Bay Area.

Regulatory Landscape

Hong Kong logistics operators operate under a compliance framework shaped by aviation security, trade facilitation digitization, and port and shipping rules. Air cargo security falls under the Civil Aviation Department (CAD) through the Aviation Security Ordinance, supported by schemes such as the Regulated Agent Regime (RAR), the Regulated Air Cargo Screening Facility (RACSF) scheme, and Known Consignor (KC) validation, which require documented security programmes and CAD inspections.

On the trade side, carrier manifest submission requirements apply across air, rail, ocean, and river movements under the Import and Export Ordinance (Cap 60), with electronic filing via EMAN. Hong Kong Customs and Excise Department initiatives also support transhipment activity, including the Free Trade Agreement Transhipment Facilitation Scheme, which was expanded effective 1 May 2026 to cover additional origin-destination combinations via Hong Kong. The Trade Single Window (TSW) program targets consolidation of 42 types of trade documents, with phase three (covering import/export declarations and cargo information) rolling out by batch starting in 2026, which elevates the need for systems integration among forwarders and brokers.

Value Chain Analysis

The Hong Kong freight and logistics value chain involves shippers (retail, electronics, pharma, and food importers/exporters), freight forwarders and 3PLs, carriers across air, sea, and road, terminal and airport cargo operators, customs brokers, and warehousing providers (ambient and temperature-controlled). Execution is centered on the airport cargo ecosystem around HKIA and the maritime gateway at Kwai Tsing, with cross-boundary trucking linking Hong Kong to Greater Bay Area production and consumption centers; digital community platforms are increasingly used to coordinate booking, documentation, and track-and-trace across these nodes.

Digital infrastructure and public programs are also changing how participants exchange data and manage handoffs. The Transport and Logistics Bureau (TLB) launched the Port Community System (PCS) in January 2026, managed by the Logistics and Supply Chain MultiTech R&D Centre (LSCM), to connect sea, land, and air information and support 24-hour visibility; the same policy push includes ESG data collection tools for logistics SMEs. On the port throughput side, Hong Kong handled 3.14 million TEUs in Q1 2026, down 7.0% year-on-year, highlighting the pressure to lift productivity per call, while longer-horizon capacity and land constraints are being addressed through planning for a modern logistics cluster in the Hung Shui Kiu/Ha Tsuen New Development Area after a study completed at the end of 2025.

Competitive Landscape

The Hong Kong freight and logistics market features moderate concentration, with ongoing consolidation moving the needle. DSV’s EUR 14.3 billion (USD 15.78 billion) takeover of DB Schenker forms the world’s largest integrated logistics group, heightening competitive intensity. CK Hutchison’s USD 17.77 billion sale of an 80% stake in Hutchison Ports redirects capital toward 5G and clean-energy ventures, leaving new port owners to optimize underused berths. Asia Airfreight Terminal and Cathay Cargo Terminal pioneer autonomous tractor rollouts, trimming labor hours and improving safety metrics. Cainiao’s RFID-equipped eHub sets a new yardstick for inventory traceability and forms the backbone for Alibaba-owned marketplace fulfillment.

Emerging players such as Globavend access public markets to scale cross-border parcel services, reflecting investor appetite for niche e-commerce logistics. Toll Group’s digital Quote & Book portal demonstrates incumbents’ pivot toward self-service shipping. Cold-chain specialists vie for pharma contracts, leveraging ISO 13485 certifications and redundant backup systems. Metals storage aspirants position facilities for LME accreditation, aiming to capture a fresh revenue stream from warrant fees and value-added sampling.

Legacy 3PLs maintain advantage through bonded warehouse licenses, deep compliance expertise, and multimodal connectivity. Yet capital-light tech entrants erode parts of the value chain by bundling instant rate quotes with embedded trade finance. Competitive intensity is further elevated by mainland firms launching Hong Kong subsidiaries to secure a CEPA service foothold.

Hong Kong Freight And Logistics Industry Leaders

Kerry Logistics Network

EV Cargo

Cargo Services Far East

DHL Logistics

Janco Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digitized trade and multimodal data sharing is a key whitespace area, especially for SMEs that still rely on fragmented documentation and manual exception handling across air, sea, and land legs. The government-led Port Community System (PCS) launched in January 2026 with 2,300 registered companies creates a baseline for platform-linked services such as standardized track-and-trace, smarter slot and yard coordination, and faster dispute resolution between forwarders, terminals, and truckers. This is reinforced by the Future Innovative Logistics Acceleration Scheme (FILAS) introduced in June 2026, which subsidizes SME adoption of logistics data platforms at a 2:1 ratio with a cap of HKD 2 million per enterprise.

Automation and cross-boundary integration also open commercialization pathways in port operations, air cargo, and cold-chain distribution. Hutchison Port Holdings Trust deployed six autonomous, AI-powered, 5G-connected trucks at Kwai Chung Terminal 4 in April 2026, pointing to demand for integrators that can retrofit yards with autonomous workflows, connectivity, and safety systems under local port operating rules. On the land-air interface, Greater Bay Area connectivity programs such as the HKIA Dongguan Logistics Park sea-air arrangement and work on the redeveloped Huanggang Port designed for 24-hour joint clearance support service bundles that combine cross-boundary trucking, pre-processing, and time-definite uplift via HKIA, particularly for e-commerce and high-value shipments.

Recent Industry Developments

- July 2026: Sin-Kung Logistics entered into an MOU with Airport Authority Hong Kong (AAHK) to pursue regional air cargo opportunities and strengthen cross-border logistics connectivity. The tie-up supports new service design around HKIA capacity and Greater Bay Area flows, creating competitive pressure on forwarders to deepen airport-linked partnerships and routings.

- May 2026: KLN Logistics Group Limited signed a strategic distributor contract with Del Monte Asia to oversee sales, trade marketing, and supply chain operations for the Hong Kong foodservice market. The award highlights demand for integrated distribution models that combine commercial execution with warehousing and last-mile control, supporting specialization in temperature-sensitive and high-service consumer supply chains.

- November 2024: SF Express completed a Hong Kong IPO to fund courier, express, and parcel (CEP) expansion. The capital raise strengthened network investment capacity in a market where CEP growth is tied to cross-border e-commerce and tighter delivery time windows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the total revenue earned from freight movement and related logistics services that support goods flows in Hong Kong, across domestic distribution and cross-border handling, reported in USD for the study period.

Scope exclusions: Passenger transport, pure postal services not linked to parcels, and in-house logistics costs that are not booked as third party revenue are excluded.

Segmentation Overview

- By Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Rail

- Road

- Sea and Inland Waterways

- Pipelines

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperatured Control

- Temperatured Control

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

- By End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model and to ensure inputs reflect Hong Kong operating realities. We mainly relied on public statistics and operational series that describe freight intensity, trade activity, and transport capacity before any pricing assumptions were applied.

Typical sources included government and official publications such as Hong Kong Census and Statistics Department releases, Hong Kong Trade and Industry Department trade statistics, Airport Authority Hong Kong cargo traffic updates, and Marine Department port and vessel movement data. We also used trade association publications and logistics journals to cross-check service mix and demand indicators. Company annual reports, exchange filings, investor decks, and reputable press were screened to understand service coverage and rate direction, and paid subscriptions were used selectively for company financials, shipment level trade signals, and freight rate context when public series were not granular enough for specific lanes. These examples are not exhaustive, and other sources were also used during the study for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions with people who see volumes and pricing on a recurring basis, including freight forwarders, carriers, warehouse operators, and logistics managers at importing and exporting firms. We also spoke with trade facing users across air, sea, and road oriented flows, so the mode mix, margin structure, and service attach rates could be adjusted when desk signals were noisy or incomplete.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | |

| Mid tier: 52% | Functional/Unit leaders: 37% | |

| Smaller Players: 16% | Managers: 47% |

Market-Sizing & Forecasting

Sizing starts with a top down build where Hong Kong trade and cargo activity is translated into a demand pool for logistics spending, then split across service lines like freight transport, forwarding, warehousing, and value added activities. Once the market total is formed, we corroborate it with selective bottom-up approximations, including sample provider revenue roll ups, lane based rate checks, and volume times average price calculations, and then adjust where gaps appear.

Key inputs used in the model include air cargo tonnage trends, seaborne container throughput, external merchandise trade values and re export intensity, warehouse space availability and typical occupancy patterns, and observed pricing direction for selected lanes and handling activities. Forecasting is run through scenario analysis supported by variable level expectations gathered from experts, and the path is kept consistent with the trade growth outlook, capacity additions, and shifts in service mix. Where provider data is missing, we handle gaps using service attach rates, utilization proxies, and peer benchmarks that are checked in interviews before being applied.

Data Validation & Update Cycle

Outputs are triangulated against independent signals, including cargo throughput series, trade values, and disclosed logistics revenue trends, and any large variance is traced back to the underlying driver assumptions. Outliers are reviewed in more than one step, where another analyst challenges the pricing, volume, and service mix logic before internal sign off.

The report is refreshed annually, and interim checks are triggered when material events occur, such as sharp trade swings, major capacity changes at air or port infrastructure, or regulatory shifts affecting cross border flows. Before delivery, a final pass is completed so the latest public updates and interview feedback are reflected in the numbers.

Mordor Intelligence's Hong Kong Freight Logistics Market Study Market Size Measured Against Other Published Estimates

Published market sizes for Hong Kong freight and logistics can look far apart even when they appear to cover the same topic, because the service boundary and the revenue counting rules are not always aligned. Differences in whether figures are reported as pure third party revenue, how cross border forwarding is treated, and how currency timing is handled are common reasons the totals do not match.

The key gap drivers in this market usually come from whether express and parcel activities are bundled with freight, whether warehousing is counted as a standalone revenue stream or only as an add on, and whether the model assumes aggressive or conservative price progression during trade upcycles. Some estimates also lean heavily on a single mode proxy, such as air cargo only, which can overstate downturns or understate recoveries when sea and road move differently.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 22.37 B (2025) | |

| Global Consultancy A | USD 24.37 B (2026) | Uses a later year and appears to bundle a wider set of value-added and express related services into the total, which can lift the number when e-commerce handling is strong. |

| Regional Consultancy B | USD 21.10 B (2025) | Leans more on trade value growth with conservative price assumptions, and it can undercount warehousing and forwarding fees when service attach rates are not validated by operator checks. |

The table shows a spread that is mainly explained by what is counted as logistics revenue and how pricing is carried forward year to year, and in Mordor Intelligence's model the total is limited to third party freight transport, forwarding, warehousing, and defined value-added logistics revenue earned for goods flows in Hong Kong. By tying the build to cargo and trade signals and then checking service mix and rate movement with operator inputs, we end up with a number that can be traced back to clear drivers and repeated consistently in future refreshes.

Key Questions Answered in the Report

How large is the Hong Kong freight and logistics market in 2026?

The market stands at USD 23.21 billion in 2026 and is forecast to grow to USD 27.95 billion by 2031 at a 3.78% CAGR.

Which logistics function leads in Hong Kong?

Freight transport leads with 58.45% share, anchored by extensive road and maritime corridors.

What segment is growing fastest?

Courier, express, and parcel services show the highest CAGR at 4.44% through 2031, fueled by cross-border e-commerce.

How is HKIA enhancing air-cargo capacity?

The Three-Runway System, operational since November 2024, lifts runway slots by 50% and supports larger freighter schedules.

Why is cold-chain logistics expanding?

Rising pharmaceutical trade and premium food demand push temperature-controlled warehousing to a 4.33% CAGR.

What challenges affect port activity?

Carrier alliances increasingly bypass Hong Kong, causing a 14.1% fall in 2023 container throughput and pressuring transshipment volumes.

Page last updated on: