China Container Shipping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 92.56 Billion |

| Market Size (2026) | USD 96.64 Billion |

| Market Size (2031) | USD 118.71 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Container Shipping Market Analysis by Mordor Intelligence

The China container shipping market size is projected to grow from USD 92.56 billion in 2025 to USD 96.64 billion in 2026, and reach USD 118.71 billion by 2031, growing at a CAGR of 4.20% from 2026 to 2031.

The China container shipping market is being supported by the continued pull of export manufacturing toward major coastal clusters, which keeps cargo moving through the country’s largest gateway ports and reinforces the role of deep-sea and feeder links within the same trade system. The China container shipping market is also benefiting from stronger cross-border e-commerce flows, expanding cold chain needs, and wider trade links across Asia, Africa, and other Belt and Road routes, which together are broadening cargo demand beyond older trade patterns. At the same time, the market is adjusting to heavier fleet additions, tighter environmental rules, and weaker rate discipline, which is pushing carriers to rely more on network control, cost efficiency, and targeted investment. These conditions are keeping the China container shipping market active, but they are also making execution quality, route mix, and vessel deployment more important than simple scale.

Key Report Takeaways

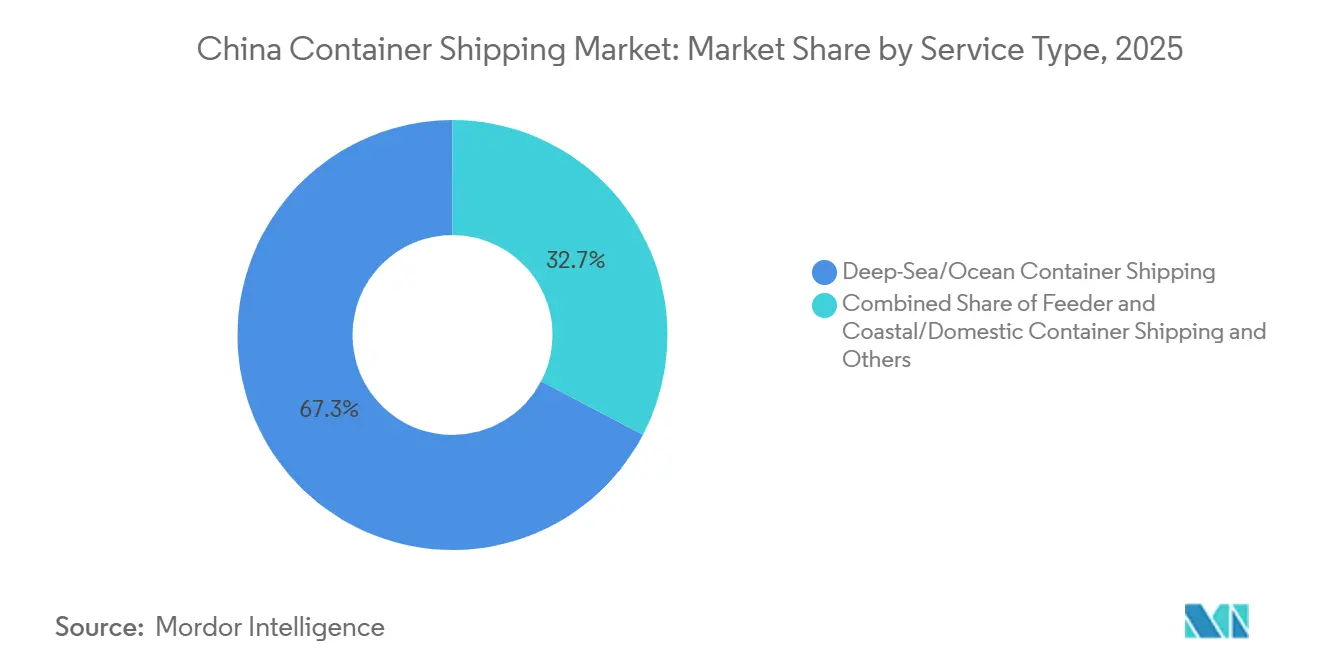

- By service type, deep-sea and ocean shipping led with a 67.33% of China container shipping market share in 2025, while feeder and coastal services are projected to grow at a 5.18% CAGR through 2031.

- By container type, dry containers held a 75.63% of China container shipping market size in 2025, while reefer containers are forecast to expand at a 7.80% CAGR through 2031.

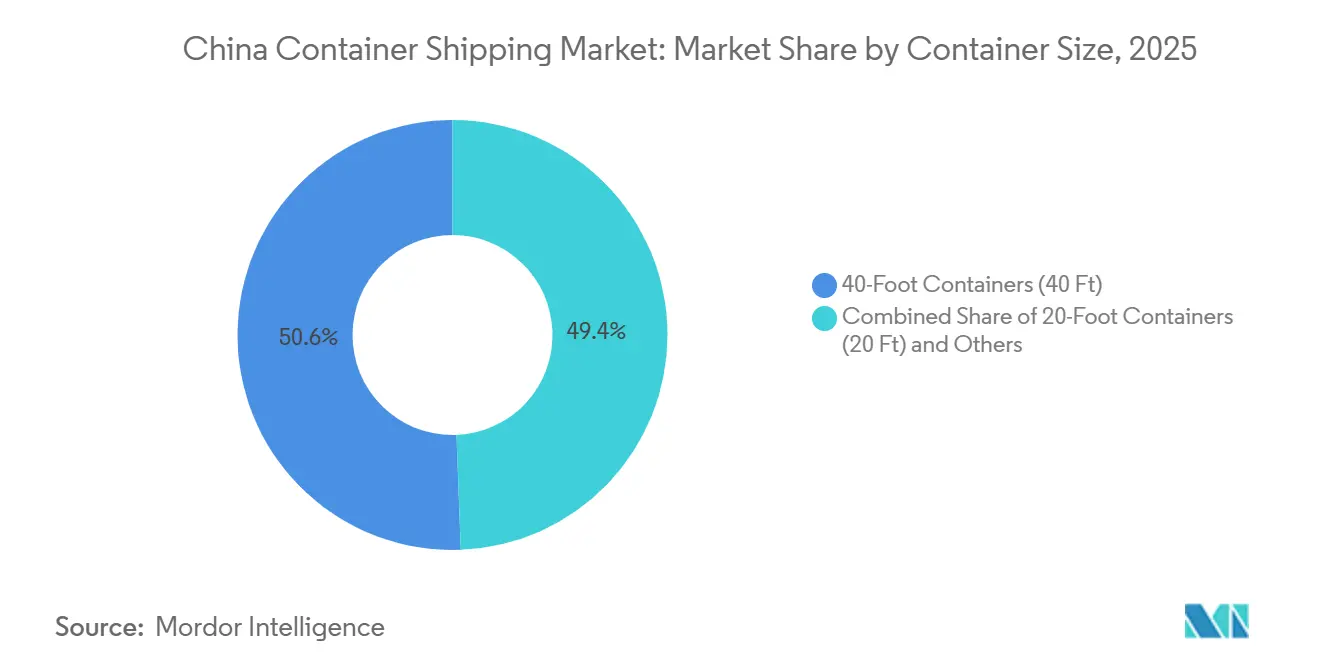

- By container size, 40-foot containers accounted for a 50.62% of China container shipping market share in 2025, while 20-foot containers are projected to grow at a 5.46% CAGR through 2031.

- By load type, FCL accounted for a 69.21% of China container shipping market size in 2025, while LCL is expected to advance at a 7.20% CAGR through 2031.

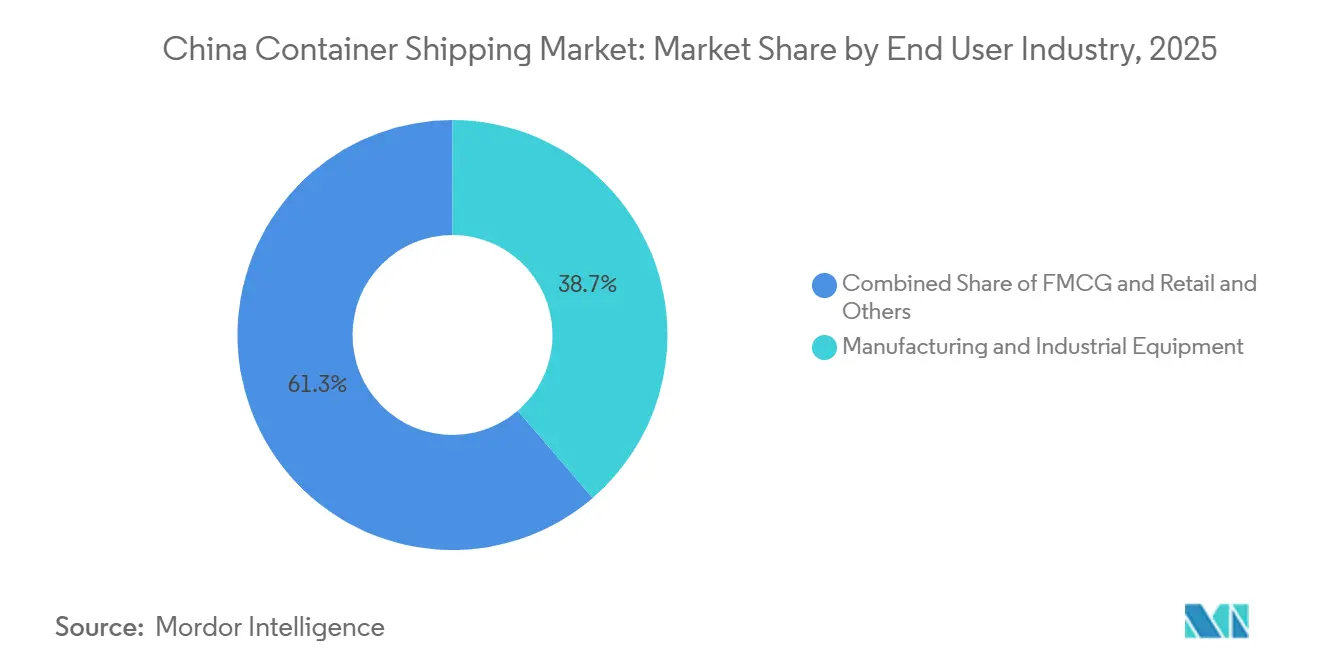

- By end-user industry, manufacturing and industrial equipment held a 38.70% of China container shipping market share in 2025, while FMCG and retail is projected to grow at a 6.52% CAGR through 2031.

- By geography, East China held 42.18% of China container shipping market size in 2025, while South China is projected to grow at a 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Container Shipping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Export Manufacturing Re-Allocation To Coastal Hubs | +1.1% | East China, South China, and North China, with spillover to Northeast China | Medium term (2-4 years) |

| Growth In E-Commerce Driven Short-Haul Domestic Movements | +0.8% | East China and South China, extending to Central China | Short term (≤ 2 years) |

| Network Upsizing To Improve Slot Utilization And Vessel Turnaround | +0.6% | National, with the strongest gains at East China and South China gateways | Medium term (2-4 years) |

| Higher Demand For Reefer Capacity From Food, Pharma, And Perishables | +1.0% | East China, South China, and RCEP-linked trade corridors | Short term (≤ 2 years) to Medium term (2-4 years) |

| Port Digitalization And Schedule Reliability Improvements | +0.5% | National, with early gains at Shanghai, Ningbo-Zhoushan, Guangzhou, and Tianjin | Long term (≥ 4 years) |

| Belt And Road-Linked Trade Diversification Supporting Carrier Volumes | +1.0% | Southeast Asia, the Middle East, Africa, and Latin America through the China gateways | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Export Manufacturing Re-Allocation To Coastal Hubs

The China container shipping market is seeing a stronger concentration of cargo around coastal production belts, especially in the Yangtze River Delta and the Pearl River Delta. This shift matters because it does more than lift volumes; it also changes how carriers deploy vessels, manage terminal calls, and plan feeder links from smaller coastal ports into the main gateway system. China’s port cargo throughput reached 2.87 billion tons in January and February 2026, while foreign trade container throughput increased by 13.7%, indicating that the main coastal gateways are still attracting more export traffic into their networks[1]Source: Ministry of Transport of China, “National Port Cargo and Container Throughput Statistics, January–February 2026,” Ministry of Transport of China, mot.gov.cn. Coastal port container throughput reached 27.2 million TEUs in March 2026, reinforcing the same direction of travel and supporting a denser concentration of linehaul volumes through the leading ports. In practical terms, larger carriers benefit from better scale at these hubs, while smaller operators find more room in feeder distribution and secondary routing around the same coastal system.

Growth In E-Commerce Driven Short-Haul Domestic Movements

The China container shipping market is gaining support from the spread of cross-border e-commerce, which is changing the shipment profile from larger consolidated orders to more frequent, smaller lots. China’s Ministry of Commerce stated that cross-border e-commerce import and export volume reached CNY 2.75 trillion (USD 406.9 billion) in 2025, up 69.7% from 2020[2]Source: Ministry of Commerce of China, “Cross-Border E-Commerce Import and Export Volume 2025,” Ministry of Commerce of China, english.mofcom.gov.cn. That growth is widening the role of LCL cargo, port-adjacent consolidation, and short-haul coastal services that connect inland exporters with gateway ports more often. It also reduces reliance on a narrow set of traditional long-haul lanes, as many of these sellers serve third-country demand rather than shipping only to the United States. As a result, the China container shipping market is drawing more volume from smaller exporters whose cargo patterns fit flexible coastal and feeder networks.

Network Upsizing To Improve Slot Utilization And Vessel Turnaround

The China container shipping market is also being influenced by network expansion and vessel upsizing across carrier fleets. These moves are not only adding capacity but also changing route design, alliance structure, and the balance between deep-sea services and regional loops. China released a plan in early 2026 to support leading logistics companies and strengthen supply chain services, providing policy support for the broader shift toward smarter, more efficient transport networks. The practical effect is that newer, more efficient vessels can take the largest long-haul positions. At the same time, older tonnage is pushed into feeder and intra-Asia trades, where cost pressure is often higher. This raises the competitive bar in the China container shipping market because carriers now need route fit and asset efficiency, not only fleet size.

Higher Demand For Reefer Capacity From Food, Pharma, And Perishables

The China container shipping market is seeing faster demand for reefer capacity than for standard dry cargo in several trade lanes. Food exports, pharmaceutical shipments, and other temperature-sensitive products are creating a more specialized demand base that depends on plug availability, terminal handling quality, and dependable transit performance. This trend is one reason reefer containers are projected to grow faster than the overall market through 2031. It also matters because reefer growth is harder to serve when vessel ordering is still weighted more toward large dry-container fleets than toward cold chain support assets. For carriers, this means that cargo quality, not only cargo volume, is becoming more important in the China container shipping market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Overcapacity Pressure In Regional Service Networks | -0.5% | Global, with a concentration on China-Europe and Transpacific lanes | Short term (≤ 2 years) to Medium term (2-4 years) |

| Freight Rate Volatility And Contract-Renewal Compression | -0.4% | Global, across China-origin deep-sea and short-sea lanes | Short term (≤ 2 years) |

| Port Congestion, Weather Disruption, And Inland Bottlenecks | -0.2% | East China, South China, and the Yangtze River inland corridor | Short term (≤ 2 years) |

| Stricter Emissions Compliance And Fuel Cost Pass-Through Risk | -0.3% | China-Europe and China-North America routes | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Overcapacity Pressure In Regional Service Networks

The China container shipping market is facing pressure from vessel supply growth that is outpacing the improvement in rate discipline. Even when carriers blank sailings or shift capacity between loops, the added tonnage still weighs on pricing across major China-origin lanes. This creates a difficult setting for operators that depend on freight rate recovery to protect margins. It also makes alliance design and service rationalization more important, as carriers need to keep ships full without further weakening rates. As a result, overcapacity remains one of the clearest checks on earnings quality in the China container shipping market.

Freight Rate Volatility And Contract-Renewal Compression

The China container shipping market is also grappling with volatile pricing amid several years of disruption to global shipping routes. Contract negotiations have become more difficult because shippers want greater visibility, while carriers still need flexibility to manage demand swings, route changes, and service costs. This tension is slowing the return to stable annual pricing patterns. It also limits how aggressively carriers can pass through higher costs when the supply side remains tight. In this setting, freight rate volatility keeps the China container shipping market active but less predictable from a revenue standpoint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Feeder Network Captures Coastal Trade Growth

Deep-sea and ocean shipping held 67.33% of the China container shipping market share in 2025, while feeder and coastal services are projected to grow at a 5.18% CAGR through 2031. The China container shipping market still leans heavily on deep-sea routes because the country remains a leading export base for manufactured goods moving on long-haul lanes. That position supports the large-scale role of gateway ports and the global alliances that anchor Asia-Europe and transpacific services. At the same time, the faster growth of feeder and coastal services shows that regional distribution is becoming more important within the same network.

The China container shipping market for feeder and coastal services is expanding as cargo increasingly requires short-haul movements between coastal hubs, inland connectors, and nearby regional destinations. Belt and Road traffic and broader intra-Asia trade are strengthening this pattern by moving more cargo through multi-stop routes rather than single, long-haul shipments. Smaller and mid-sized carriers are using this opening to position themselves around coastal loops and secondary port calls. Deep-sea operators still retain the largest revenue base, but they now depend more on integrated feeder support to maintain schedules and equipment flow. This means the service mix in the China container shipping industry is becoming more connected across vessel classes rather than more divided.

By Container Type: Reefer Growth Outpaces the Fleet Average

Dry containers accounted for 75.63% of the China container shipping market size in 2025, while reefer containers are projected to grow at a 7.80% CAGR through 2031. The large dry-container base reflects China’s broad trade in manufactured goods, electronics, machinery, and industrial cargo. That core remains important because it still carries most of the country’s containerized export volume. Even so, reefer demand is rising faster because food products, pharmaceuticals, and other perishable cargo require tighter temperature control and more specialized handling.

This shift changes more than the equipment mix. It also raises the importance of reefer plugs, terminal operating quality, and inland cold chain coordination. Carriers that can reliably support this cargo may achieve better cargo quality and stickier customer relationships than operators focused solely on standard dry freight. The result is that reefer growth is becoming a meaningful part of the China container shipping market, even though dry containers still account for the largest share. Over time, this should make service quality and cold chain capability a larger point of competition across the China container shipping market.

By Container Size: 20-Foot Units Gain on E-Commerce and BRI Commodity Trade

Forty-foot containers held a 50.62% of China container shipping market share in 2025, while 20-foot containers are projected to grow at a 5.46% CAGR through 2031. The large position of 40-foot units reflects the dominance of full loads tied to China’s main manufactured export flows. These units remain well-suited for high-volume cargo moving on major linehaul services out of the country’s largest ports. They therefore continue to anchor the standard cargo profile of the China container shipping market.

The faster growth of 20-foot units points to a different set of cargo needs. Commodity-oriented Belt and Road trade, smaller export consignments, and a wider use of feeder vessels are all supporting this segment. Twenty-foot units also fit shipment structures in which load density, route flexibility, or equipment-handling conditions matter more than maximum box volume. Specialized sizes still serve industrial and project cargo niches, but their role remains more stable than expansive. This leaves the China container shipping market with a container size mix that is still led by 40-foot units, while 20-foot units gain ground through route and cargo diversification.

By Load Type: LCL Demand Reshapes the Consolidation Market

FCL accounted for 69.21% of the China container shipping market size in 2025, while LCL is projected to expand at a 7.20% CAGR through 2031. FCL remains the dominant format because large manufacturing exporters still prefer direct and dedicated shipment structures when they can fill a full box. That preference supports efficient handling and lowers unit logistics costs for many established exporters. For that reason, FCL still accounts for the largest operating base in the China container shipping market.

LCL is growing faster because more exporters are entering overseas channels with shipment volumes that do not justify a full container. This changes the roles of consolidators, bonded warehouses, and port-adjacent logistics parks, as cargo preparation becomes more frequent and fragmented. It also enhances coordination between inland collection points and coastal departure ports. As a result, the China container shipping market is seeing more activity around consolidation quality and cargo handling speed, not only around vessel space. That shift gives LCL a larger strategic role than its current revenue share alone would suggest.

By End-User Industry: FMCG Emerges as the Growth Engine

Manufacturing and industrial equipment accounted for 38.7% of China container shipping market share in 2025, while FMCG and retail are projected to grow at a 6.52% CAGR through 2031. Manufacturing and automotive remain the largest end-user sectors because China continues to export large volumes of machinery, components, industrial products, and auto-related cargo. These shipments support steady FCL demand and keep the main deep-sea corridors well utilized. This base continues to define much of the core cargo structure within the China container shipping market.

FMCG and retail are growing faster because trade flows are widening toward consumer demand centers in Southeast Asia, Africa, and Latin America. That expansion supports both faster-moving retail goods and more frequent replenishment shipments. Healthcare and pharmaceuticals are also taking a larger role because they depend on reliable cold chain handling and stricter cargo condition control. Electronics and electrical equipment remain important for high-value shipments, while chemicals and raw materials provide a steadier but slower-moving volume base. Together, these patterns show that the China container shipping market is still led by industrial cargo, but future growth is spreading more evenly across consumer-facing segments.

Geography Analysis

East China held 42.18% of the China container shipping market share in 2025, making it the largest regional center in the country’s domestic container system. The region benefits from the concentration of Shanghai, Ningbo-Zhoushan, and other large gateway ports that handle export cargo at national scale. East China also has a stronger base of port automation and logistics coordination, which supports high-volume, time-sensitive freight along the same coastal corridor. Because of this, East China remains the main operating hub of the China container shipping market for both long-haul export services and domestic cargo relay.

South China is projected to grow at a 5.52% CAGR through 2031, which makes it the fastest-growing regional segment in the report. Guangzhou Nansha, Shenzhen Yantian, and Shekou continue to support the region’s role in electronics, apparel, and FMCG export flows. South China also has a strong position in intra-Asia and Belt and Road traffic, giving it a broader mix of regional and long-haul cargo exposure. This makes the South an important growth engine for the China container shipping market, even though East China still leads in absolute share[3]Source: Xinhua, “China’s Shipping Industry Propels Shift Toward Intelligence,” Xinhua, english.news.cn.

North China remains important for manufacturing and automotive cargo, with ports such as Tianjin and Qingdao serving as key hubs. The Northeast, Central, Southwest, and Northwest regions hold smaller shares, but they are becoming more relevant as inland logistics investment improves cargo access to coastal gateways. The Central region matters because Yangtze River ports facilitate the movement of containerized exports from inland provinces into the main maritime system. Southwest and Northwest China also benefit when inland hubs and intermodal links reduce the cost of reaching coastal ports. Taken together, these regions give the China container shipping market a broader domestic base, even though the largest concentration of volume still sits in the east and south.

Competitive Landscape

The China container shipping market is moderately consolidated at the global deep-sea level and more fragmented in feeder and intra-Asia services. Large international carriers and alliance-linked operators hold a strong position on long-haul routes because they can deploy larger vessels, operate wider schedules, and serve larger customer networks. At the same time, regional and domestic operators still compete across many shorter route pairs where local port coverage and frequency matter more than alliance scale. This creates a two-layer structure in the China container shipping market, with concentration in major east-west lanes and wider fragmentation in secondary and regional services.

One major strategic move came in February 2026, when Hapag-Lloyd signed an agreement to acquire ZIM for USD 4.2 billion, which would strengthen its position and expand its network reach if completed[4]Source: Hapag-Lloyd AG, “Hapag-Lloyd Signs Merger Agreement with ZIM,” Hapag-Lloyd AG, hapag-lloyd.com. Another important move came in March 2026, when Ocean Network Express entered into a strategic partnership with Dongwon Group at the Busan terminal to improve network reliability and support transshipment for Asian cargo flows. The market is also seeing carriers invest in cleaner fleets and more efficient route structures, indicating that competition is now closely tied to compliance readiness and service consistency. These moves indicate that the China container shipping market is being shaped by network control, reliability, and fleet quality rather than by simple capacity growth alone.

Technology is becoming a larger point of differentiation because weak rate conditions reduce the value of competing only on price. Carriers that can combine schedule discipline, digital visibility, and route flexibility are better placed to protect customer relationships when markets soften. There is also room in cold chain-enabled feeder services and in digital links between ports and inland logistics partners, where the field is still open enough for focused operators to build stronger positions. New environmental rules add another layer, as older fleets may face greater operating pressure than newer dual-fuel or more efficient vessels. For that reason, competitive strength in the China container shipping market now depends on how well each carrier aligns its fleet, routes, and service design with a less forgiving operating environment.

China Container Shipping Industry Leaders

COSCO Shipping Lines

Orient Overseas Container Line (OOCL)

Shanghai Pan Asia Shipping (SPA)

Sinotrans Container Lines

Ningbo Ocean Shipping Co., Ltd. (NBOSCO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: X-Press Feeders and Gold Star Line launched the South China Java X-Press (SCJX) service from Xiamen. The service connects Yantian, Xiamen, and Nansha with Jakarta and Surabaya using three vessels of about 2,800 TEU.

- March 2026: Ocean Network Express completed a long-term partnership with Dongwon Group, acquiring an indirect interest in Dongwon Global Terminal Busan. The investment gave ONE direct access to Busan terminal capacity and aimed to improve cargo-flow management, transshipment operations, and network reliability.

- February 2026: Hapag-Lloyd signed a merger agreement to acquire 100% of ZIM for USD 35 per share in cash, valuing the deal at about USD 4.2 billion. Subject to approvals and completion, the combination would strengthen Hapag-Lloyd’s global network, including Transpacific and intra-Asia services.

- June 2025: PIL, HMM, and X-Press Feeders launched the North China-Indonesia service, branded NCI by PIL and NIS by HMM. The service connected Tianjin, Qingdao, and Xiamen with Singapore, Jakarta, and Surabaya on a 35-day rotation using five vessels of 4,000-5,000 TEU.

China Container Shipping Market Report Scope

| Deep-Sea/Ocean Container Shipping |

| Short-Sea Container Shipping |

| Feeder and Coastal/Domestic Container Shipping |

| Dry Containers (General Purpose) |

| Reefer Containers |

| 20-foot Containers (20 ft) |

| 40-foot Containers (40 ft) |

| Other Specialized Sizes |

| Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) |

| FMCG and Retail |

| Manufacturing and Automotive |

| Healthcare and Pharmaceuticals |

| Electronics and Electrical Equipment |

| Industrial Chemicals and Raw Materials |

| Others |

| North |

| Northeast |

| East |

| Central |

| South |

| Southwest |

| Northwest |

| By Service Type | Deep-Sea/Ocean Container Shipping |

| Short-Sea Container Shipping | |

| Feeder and Coastal/Domestic Container Shipping | |

| By Container Type | Dry Containers (General Purpose) |

| Reefer Containers | |

| By Container Size | 20-foot Containers (20 ft) |

| 40-foot Containers (40 ft) | |

| Other Specialized Sizes | |

| By Load Type | Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) | |

| By End-User Industry | FMCG and Retail |

| Manufacturing and Automotive | |

| Healthcare and Pharmaceuticals | |

| Electronics and Electrical Equipment | |

| Industrial Chemicals and Raw Materials | |

| Others | |

| By Region | North |

| Northeast | |

| East | |

| Central | |

| South | |

| Southwest | |

| Northwest |

Key Questions Answered in the Report

What is the 2031 value forecast for container shipping in China?

The report projects that the China container shipping market will reach USD 118.71 billion by 2031, up from USD 96.64 billion in 2026, at a 4.20% CAGR.

Which service segment is growing the fastest in China?

Feeder and coastal services are the fastest-growing service type, with a projected 5.18% CAGR through 2031.

Which container type is expanding the quickest?

Reefer containers are forecast to grow at a 7.80% CAGR through 2031, ahead of the broader market, due to stronger demand from food, pharma, and perishables.

What keeps East China in the leading position?

East China held a 42.18% share in 2025 because it is home to major gateway ports, high export activity, and stronger automation and logistics coordination.

Why is LCL gaining importance in China’s shipping flows?

LCL is projected to grow at a 7.20% CAGR, driven by cross-border e-commerce, which is increasing the number of smaller exporters that do not ship full-container loads.

What are the main risks affecting carrier performance in China?

The main risks are overcapacity, freight rate volatility, weather, and inland bottlenecks, as well as stricter emissions compliance, which can raise operating costs and pressure margins.

Page last updated on: