Germany Chemical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.01 Billion |

| Market Size (2026) | USD 19.75 Billion |

| Market Size (2031) | USD 23.64 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Chemical Logistics Market Analysis by Mordor Intelligence

The Germany chemical logistics market size is expected to increase from USD 19.01 billion in 2025 to USD 19.75 billion in 2026 and reach USD 23.64 billion by 2031, growing at a CAGR of 3.67% over 2026-2031.

Germany’s chemical park system also keeps the market structurally dense, as 41 member parks employ more than 260,000 workers and anchor a large share of the country’s chemical production. Competition is tightening in large contracts after Deutsche Bahn completed the sale of DB Schenker to DSV in April 2025, raising the scale threshold for multi-site contract logistics mandates in the German chemical logistics market. A longer-term opportunity is also emerging around hydrogen flows, as HOYER and TALKE both moved into early hydrogen logistics configurations, pointing to a new specialty transport layer within the Germany chemical logistics market.

Key Report Takeaways

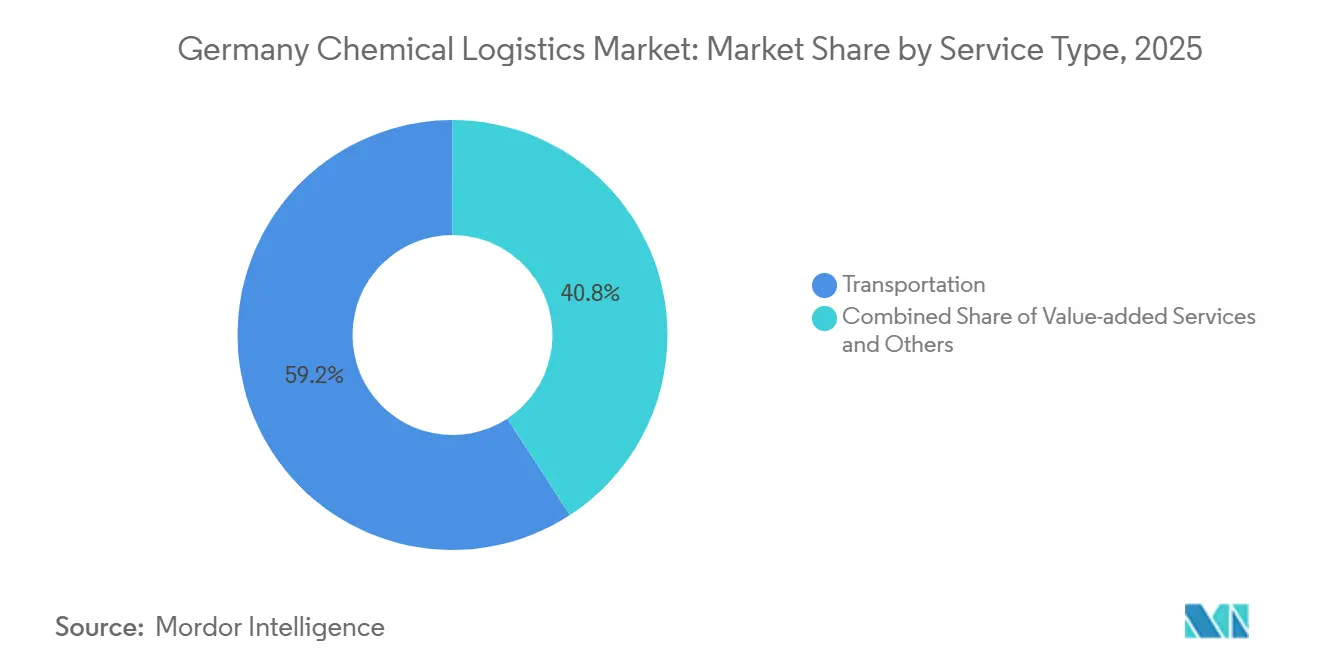

- By service type, transportation held 59.2% share of Germany chemical logistics market size in 2025, while value-added services are projected to grow at a 6.50% CAGR through 2031.

- By hazard class, hazardous chemicals accounted for 63% share of Germany chemical logistics market size in 2025, and are projected to grow at a CAGR of 5.67% through 2031.

- By temperature control, non-temperature-controlled logistics held 78.13% of Germany chemical logistics market share in 2025, while temperature-controlled logistics are forecast to expand at a 6.81% CAGR through 2031.

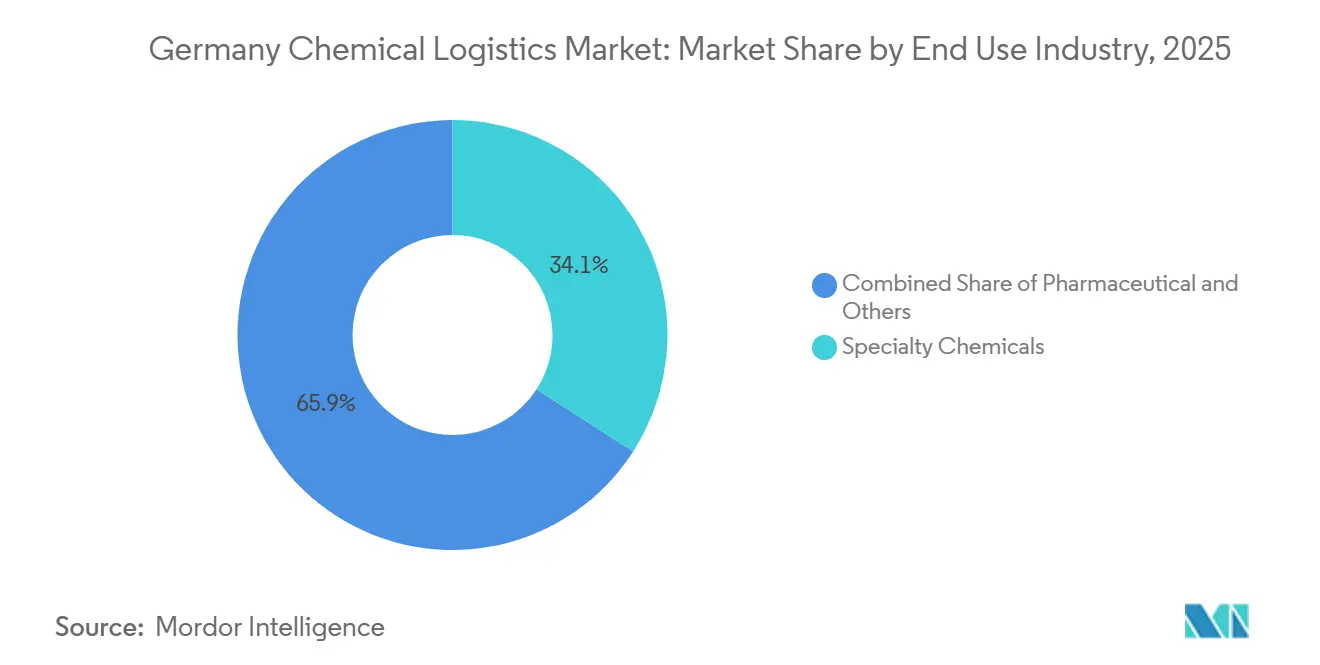

- By end-user industry, specialty chemicals accounted for 34.11% of Germany chemical logistics market size in 2025, while the pharmaceutical end-user is projected to grow at a 7.12% CAGR through 2031.

- By region, North Rhine-Westphalia held 41.92% share in 2025, while Bavaria recorded the highest projected CAGR at 5.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Chemical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Domestic Chemical Output Recovery | +0.5% | National, with concentrated upside in NRW and the Rhine-Ruhr cluster | Medium term (2-4 years) |

| EU-ADR Compliance Driving Specialist Demand | +0.6% | Nationwide, the highest compliance complexity is in NRW and Baden-Württemberg. | Short term (≤ 2 years) |

| Export-Oriented Supply-Chain Complexity | +0.7% | National, with export gateway benefits in Hamburg, Bremen, Rotterdam corridor | Medium term (2-4 years) |

| Growing Chemiepark-Based Integrated Logistics | +0.4% | NRW, Bavaria, Rhine-Main, Rhineland clusters | Long term (≥ 4 years) |

| Adoption of IoT Tanks and Digital Twins | +0.8% | National, with early adoption concentrated at large Chemiepark sites | Medium term (2-4 years) |

| Green-Hydrogen Corridor Build-Out | +0.3% | North Germany, Rhein-Neckar, expanding nationally post-2027 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Domestic Chemical Output Recovery: Fragile Uptick Creates Selective Logistics Demand

Germany’s chemical and pharmaceutical base entered 2026 from a weak 2025 operating position, because industry production fell 3.3%, sales declined 3%, and capacity utilization averaged 72.5%. That backdrop keeps recovery in the Germany chemical logistics market selective rather than broad-based, because even a modest pickup in output lifts tanker use, warehouse turns, and packaging activity without fully restoring bulk volumes. This gives multi-service operators a buffer, since pharma-linked flows can support network utilization while bulk producers continue to run at lower rates. It also means providers that add capacity too early in the Germany chemical logistics market may face weaker margins if restocking fades before a broader production recovery takes hold. Asset allocation is therefore moving toward mixed networks that can serve both core chemical volumes and smaller, more regulated shipments.

EU-ADR Compliance Driving Specialist Demand: Specialist Capability Remains a Clear Divider

Compliance remains a direct driver of demand in the Germany chemical logistics market, as hazardous-goods transport requires trained staff, certified processes, and storage assets designed for regulated materials. Operators that can combine road transport, tank handling, repacking, inspection, and documentation support are in a stronger position when shippers want fewer counterparties. Leschaco’s Bremen logistics center, commissioned in October 2025, added dedicated hazardous-goods infrastructure and classification-based storage capabilities, demonstrating how providers are investing in compliance-intensive demand. BASF’s dTEX deployment at Ludwigshafen also points in the same direction, because it nearly fully automated truck dispatch and strengthened the digital side of site access, movement control, and workflow execution[1]Source: Leschaco Group, “Leschaco Strengthens Dangerous Goods Logistics with New Multi-Purpose Facility in Bremen,” Leschaco News, leschaco.com. In practice, the Germany chemical logistics market is rewarding providers that treat compliance as an operating capability rather than a back-office burden. That gap is likely to widen as customers put more value on audit readiness and managed service support.

Growing Chemiepark-Based Integrated Logistics: Site Logistics Continues to Deepen Switching Costs

Chemiepark-linked operations remain a structural advantage in the Germany chemical logistics market, because shared utilities, site storage, and embedded distribution reduce handling risk and compress movement time. VCI’s chemical park network spans 41 member parks and supports more than 260,000 workers, which shows how much of the national production base remains tied to clustered industrial sites. TALKE’s footprint reinforces this pattern, because 9 of its 15 German sites are located in the Rhine-Ruhr cluster, where site logistics and trimodal access matter most[2]Source: TALKE Group, “Chemical Logistics in Europe, Locations,” TALKE, talke.com.This embedded position raises switching costs for customers, as changing a provider within a chemical park affects safety protocols, workflow integration, and on-site operational continuity. The Germany chemical logistics market therefore gives a durable advantage to operators that already control fence-line logistics at key chemical sites. That advantage should become more valuable as plant portfolios are reworked for energy transition, specialty output, and new feedstock flows.

Adoption of IoT Tanks and Digital Twins: Digital Control Is Moving Into Daily Operations

Digitalization is becoming a practical growth lever in the Germany chemical logistics market, as large sites are now using automation to reduce dwell time, improve slot utilization, and tighten truck dispatch. BASF completed the deployment of its dTEX system at Ludwigshafen in September 2025, and the company described the rollout as a near-complete digitalization and automation of truck dispatch at its largest integrated site. BASF also deployed an AI-supported digital twin for network planning with Google Cloud and prognostica GmbH, thereby shortening planning cycles and demonstrating how simulation can improve routing and supply decisions. These systems matter in the Germany chemical logistics market because they convert site data into faster dispatches, better equipment utilization, and stronger visibility across movements. They also raise customer expectations, especially for tank, rail, and yard operations, where timing errors quickly increase cost. At the same time, broader sensor and platform adoption make operational data security increasingly important for hazardous and temperature-sensitive chemical flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver Shortage and Rising Road Freight Rates | -0.4% | National, most acute in Eastern and Northern Germany | Short term (≤ 2 years) |

| Carbon-Pricing Linked Cost Escalation | -0.3% | National, with disproportionate impact on road-heavy chemical corridors | Medium term (2-4 years) |

| Scarcity of Temperature-Controlled Rail Tanks | -0.2% | National, especially the Rhine Valley and the North-South pharmaceutical corridors | Medium term (2-4 years) |

| Rhine Waterway Congestion and Lock Downtime | -0.3% | NRW, Baden-Württemberg, Rhineland, with spillover to Hamburg and ARA terminals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Driver Shortage and Rising Road Freight Rates: Road Capacity Remains the Main Short-Term Constraint

Road transport still accounts for a large share of chemical movement in the Germany chemical logistics market, so any shortage of qualified drivers quickly tightens available capacity. The pressure is greater in hazardous-goods transport because chemical shippers need drivers who can meet stricter handling and safety requirements than those in standard freight operations. This raises the value of route planning, yard automation, and network density, yet those tools only soften the constraint rather than remove it. It also increases the appeal of intermodal configurations, especially for operators that can connect road legs with rail or terminal-based consolidation. In the Germany chemical logistics market, providers with tank capacity, rail access, and disciplined scheduling are better placed to defend margins when road freight tightens. Shippers are therefore placing more emphasis on resilience and mode flexibility in logistics tenders.

Rhine Waterway Congestion and Lock Downtime: Corridor Dependence Adds Network Risk

The Rhine remains essential to the Germany chemical logistics market, especially for western clusters that depend on barge-linked inbound and outbound chemical flows. When waterway conditions weaken, the effect is not limited to inland shipping, as displaced volume quickly moves into rail and road networks already operating under pressure. This creates a broader problem for chemical parks, as inventory planning, feedstock timing, and outbound delivery become harder to stabilize simultaneously. BASF and Lineas’ dedicated rail shuttle between Ludwigshafen and Antwerp shows why rail-backed alternatives are becoming more important when Rhine exposure rises. The Germany chemical logistics market is therefore driving more investment toward multimodal terminals and corridor diversification rather than relying on a single dominant freight route. That shift supports resilient operators, but it also raises capital needs for shippers and logistics providers serving the Rhine belt.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Leads Revenue While Service Intensity Keeps Rising.

Transportation held 59.2% of the Germany chemical logistics market share in 2025, confirming that core movement activity still anchors revenue across tankers, rail wagons, barges, and contract haulage. Road transport remained the largest part of this function because Germany’s chemical production base is spread across clusters in North Rhine-Westphalia, Baden-Wurttemberg, and Bavaria, all of which depend on dense domestic freight links. Rail continued to strengthen its role in the Germany chemical logistics market as dedicated chemical shuttles moved closer to backbone status for large producers. BASF and Lineas marked the 1,000th round trip of their freight shuttle between Ludwigshafen and Antwerp in May 2025, underscoring that scheduled rail links are now central to selected cross-border chemical lanes[3]Source: BASF and Lineas, “Lineas and BASF Celebrate 1000th Freight Shuttle,” Lineas Newsroom, newsroom.lineas.net .

Value-added services are projected to grow at a 6.50% CAGR through 2031, making this the fastest-expanding logistics function in the Germany chemical logistics market. Demand is shifting toward in-warehouse blending, relabeling, re-drumming, inspection, and documentation support, as chemical producers seek to protect plant capital and outsource support work. DACHSER is commissioning a new hazardous materials warehouse in Rastatt in 2026, and the timing reflects expectations of stronger demand as chemical output gradually improves. Leschaco’s Bremen site adds the same message, because the facility combines dedicated hazardous storage with broader contract logistics capability for regulated chemical flows. As a result, the Germany chemical logistics market is placing greater value on warehouse capabilities that can absorb operational complexity rather than just storing product.

By Hazard Class: Hazardous Flows Continue to Define the Core of Chemical Logistics

Hazardous chemicals accounted for 63% of the Germany chemical logistics market size in 2025 and are expanding at a CAGR of 5.67% through 2031, underscoring the central role of ADR-ready transport, certified storage, and specialized tank assets. This part of the Germany chemical logistics market remains structurally important even when basic chemical output is soft, because many regulated substances still require dedicated transport and handling. Brenntag strengthened its central European footprint in Q2 2025 through the acquisition of GSZ Kaiserslautern, a hazardous substance storage facility in Germany, expanding its operational base for regulated materials. That move indicates that operators still see long-term value in certified hazardous infrastructure even during a weaker cycle.

The commercial logic inside this segment is shifting, because margin quality now depends less on pure volume and more on certification, audit readiness, and handling precision. In the Germany chemical logistics industry, certified operators can compete for long-term site and network contracts, while less specialized carriers are pushed toward more volatile spot work. The non-hazardous side faces more pricing pressure, since larger bulk flows can be routed through broader freight networks with fewer technical barriers. Hazardous logistics also gains support from adjacent categories such as lithium-ion battery handling, which fit well with existing dangerous-goods storage and distribution capability. This keeps the Germany chemical logistics market tilted toward providers that can combine equipment, training, warehousing, and compliance support in one operating model.

By Temperature Control: Ambient Volumes Dominate, but Controlled Handling Is Expanding Faster

Non-temperature-controlled logistics retained a 78.13% share of the Germany chemical logistics market share in 2025, because most bulk chemical movement in Germany still travels under ambient conditions across road, rail, and inland waterway networks. That base ensures the Germany chemical logistics market remains anchored in large-volume transport for standard industrial chemicals, polymers, solvents, and related flows. Even so, the strongest growth is moving into controlled handling where product integrity matters more than scale.

Temperature-controlled logistics is forecast to grow at a 6.81% CAGR through 2031 in the Germany chemical logistics market, supported by pharmaceutical, reagent, and specialty intermediate flows that require refrigerated or heated conditions. This is changing asset priorities toward insulated storage, monitored transport, and service models that can prove compliance at each step.

By End Use Industry: Specialty Chemicals Lead Revenue While Pharma Sets the Pace

Specialty chemicals accounted for 34.11% of of the Germany chemical logistics market size in 2025, making them the largest end-use segment in the Germany chemical logistics market. This segment depends on frequent, compliance-heavy deliveries rather than on very large shipment sizes, which align with Germany’s clustered production structure in Rhine-Neckar, Rhine-Main, and Bavaria. The Germany chemical logistics industry benefits from these flows because they support higher service content in transport, storage, and packaging.

Pharmaceutical end use is projected to grow at a 7.12% CAGR through 2031, and that outlook is consistent with VCI’s report that pharmaceutical production increased 4.5% in 2025 while the wider chemical base weakened. This divergence is important because it changes where providers place capital and management attention. Pharma-linked demand supports temperature-controlled movement, clean handling, traceability, and shorter response cycles, all of which raise the service profile of the Germany chemical logistics market.

Geography Analysis

North Rhine-Westphalia held 41.92% of the Germany chemical logistics market share in 2025, making it the clear regional leader. The state remains central to the Germany chemical logistics market because the Rhine-Ruhr cluster combines production, storage, terminals, and dense industrial demand in one corridor. TALKE’s network clearly shows concentration, as 9 of its 15 German sites are located in the Rhine-Ruhr region. The wider western corridor also benefits from BASF’s Ludwigshafen site, whose rail and container infrastructure influences freight patterns well beyond Rhineland-Palatinate. At the same time, NRW has greater exposure to Rhine-related disruptions, so operators there need greater modal flexibility than in many other parts of Germany.

Bavaria is projected to grow at a 5.05% CAGR through 2031, making it the fastest-growing regional segment in the Germany chemical logistics market. Growth is supported by pharmaceutical and specialty chemical production around Munich, Ingolstadt, and the wider ChemDelta Bavaria footprint. This raises demand for GMP-aligned storage, controlled handling, and higher-value contract logistics rather than only standard freight movement. DHL’s Florstadt pharmaceutical campus, while located in neighboring Hesse, is also relevant because it supports distribution into southern Germany and adds capacity close to the Bavarian demand base.

Baden-Wurttemberg and the rest of the states account for the remaining share of the Germany chemical logistics market. Baden-Wurttemberg is important because it connects German and Swiss specialty chemical production through the Rhine Valley and the Basel-Karlsruhe corridor. DHL’s new 26,600 m² Rheinbach logistics center, which is scheduled to go on stream in August 2026, will strengthen network flexibility for the wider Rhineland and airport-linked freight catchment[4]Source: DHL Group, “DHL Transforms DHL Health Logistics Campus in Florstadt Into a European Pharmaceutical Hub,” DHL Group Press, group.dhl.com. Northern states also contribute through port gateways and the early build-out of hydrogen and ammonia logistics routes, which adds a future growth layer to the Germany chemical logistics market.

Competitive Landscape

The Germany chemical logistics market has a moderately consolidated structure, with specialist operators and diversified global providers competing in parallel. HOYER Group, Bertschi AG, TALKE Group, Den Hartogh Logistics, and Leschaco hold strong positions in hazardous movement, tank operations, and site logistics. DSV, DHL Supply Chain, Kuehne+Nagel, CEVA Logistics, and GEODIS compete more broadly for contract logistics and 4PL work where chemical expertise is bundled with network scale. The most important structural move came in April 2025 when Deutsche Bahn completed the sale of DB Schenker to DSV for EUR 14.3 billion, which materially changed scale competition in the Germany chemical logistics market. This raises pressure on mid-sized operators to defend niches where certification, site integration, or tank specialization matter more than global volume.

Technology is becoming one of the clearest competitive filters in the Germany chemical logistics market. BASF’s dTEX rollout at Ludwigshafen raised the benchmark for digital dispatch, yard flow, and truck handling at integrated chemical sites. BASF’s use of an AI-supported digital twin for supply decisions also shows how customers are moving toward faster and more connected logistics planning. Providers that cannot offer control-tower visibility, shipment traceability, or data-backed exception handling are likely to face tougher contract renewals.

Low-emission logistics is emerging as another point of separation in the Germany chemical logistics market. HOYER signed a hydrogen logistics contract with H2 MOBILITY in July 2025, putting the company in an early operational role in hydrogen distribution. TALKE also invested in ADR-certified hydrogen trucks for deployment in 2026, while HOYER joined Germany’s Federal Transport Organization in February 2026, thereby widening its strategic relevance beyond commercial chemical work. Bertschi continued to invest in sustainable chemical logistics infrastructure in 2026, which supports its intermodal position and reinforces the shift toward lower-emission network design. Competition is therefore tightening at both ends of the Germany chemical logistics market, with scale, specialization, and operational transition becoming increasingly important.

Germany Chemical Logistics Industry Leaders

HOYER Group

Bertschi AG

TALKE Group

BASF SE

Brenntag SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Univar Solutions expanded its strategic partnership with Dow for the distribution of silicone additives across EMEA markets, including Germany.

- March 2026: Univar Solutions expanded its EMEA distribution partnership with SI Group for performance additives for plastics and adhesives, including German market coverage.

- March 2026: BASF SE and Schütz signed an agreement for the construction of a highly automated IBC production and storage facility at BASF's Ludwigshafen headquarters, with work scheduled to commence in Q3 2026.

- December 2025: Den Hartogh Logistics and Nissin Corporation established Den Hartogh Nissin Corporation as a joint venture in Tokyo, aiming to expand the ISO tank container business for the Japanese chemical market.

Germany Chemical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| Hazardous Chemicals |

| Non-hazardous Chemicals |

| Temperature-Controlled (Refrigerated/Heated) |

| Non-Temperature-Controlled |

| Pharmaceutical |

| Cosmetic |

| Oil and Gas |

| Specialty Chemicals |

| Other End-Users |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Hazard Class | Hazardous Chemicals | |

| Non-hazardous Chemicals | ||

| By Temperature Control | Temperature-Controlled (Refrigerated/Heated) | |

| Non-Temperature-Controlled | ||

| By End Use Industry | Pharmaceutical | |

| Cosmetic | ||

| Oil and Gas | ||

| Specialty Chemicals | ||

| Other End-Users | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States |

Key Questions Answered in the Report

What is the projected value of Germany chemical logistics by 2031?

The Germany chemical logistics market is forecast to reach USD 23.64 billion by 2031 from USD 19.75 billion in 2026, which reflects a 3.67% CAGR over 2026-2031.

Which logistics function currently contributes the most revenue in Germany?

Transportation is the largest function, with a 59.2% revenue share in 2025, because the market still depends heavily on road, rail, and bulk movement across dense chemical clusters.

Which segment is growing the fastest in this space?

Pharmaceutical end use is the fastest-growing end-use segment, with a 7.12% CAGR through 2031.

Why is North Rhine-Westphalia so important for chemical logistics in Germany?

North Rhine-Westphalia accounted for 41.92% of 2025 revenue because it combines the Rhine-Ruhr chemical cluster, a dense production infrastructure, major terminals, and strong site logistics activity.

How is pharmaceutical production influencing logistics demand in Germany?

Pharmaceutical production rose 4.5% in 2025 even as the broader chemical base weakened, which is shifting demand toward controlled storage, compliance-heavy transport, and higher-value logistics services.

What strategic change is reshaping competition among logistics providers?

The April 2025 completion of DSV’s acquisition of DB Schenker is raising the scale of competition in large contract logistics mandates, while specialists still defend niches in hazardous and tank-based operations.

Page last updated on: