Career Pathing and Mobility Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

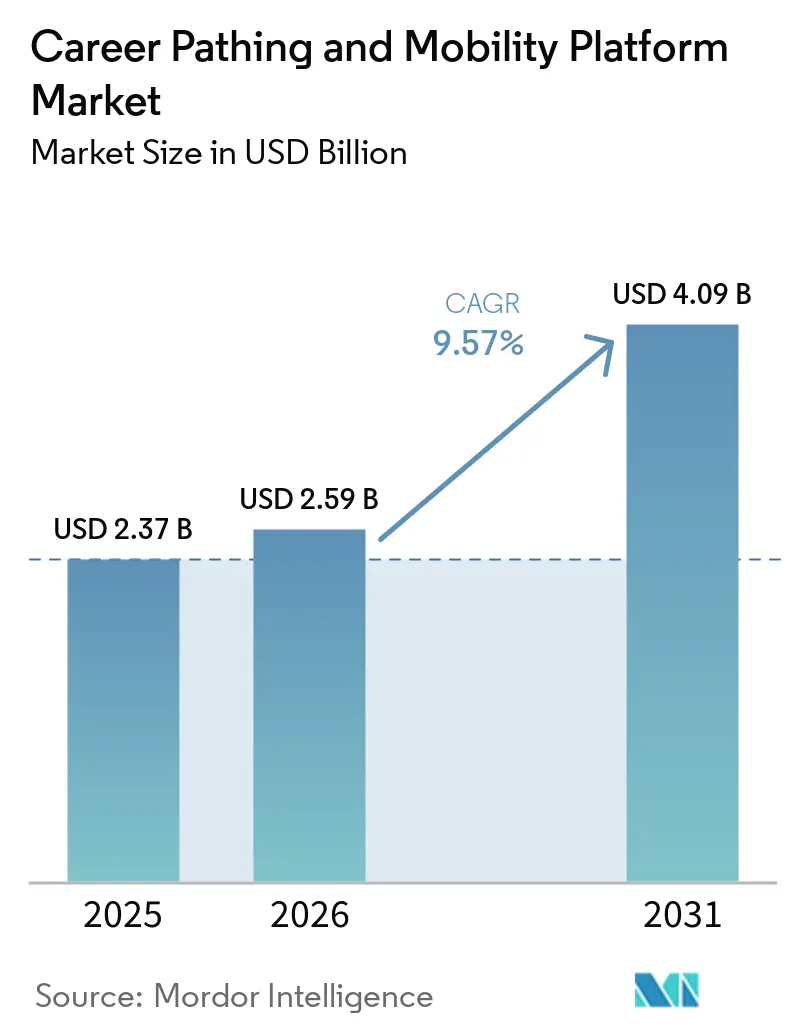

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 4.09 Billion |

| Growth Rate (2026 - 2031) | 9.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Career Pathing and Mobility Platform Market Analysis by Mordor Intelligence

The career pathing and mobility platform market size is expected to be USD 2.37 billion in 2025, USD 2.59 billion in 2026, and reach USD 4.09 billion by 2031, growing at a CAGR of 9.57% from 2026 to 2031. Widespread hiring freezes redirected budgets from external recruiting toward internal redeployment, spotlighting career-pathing platforms as a cost-containment and retention tool rather than a compliance checkbox. Organizations that once measured success in head-count reductions now treat employee skills as an appreciating asset, driving demand for systems that surface transferable capabilities in real time. Vendor roadmaps mirror this shift, embedding agentic artificial intelligence that automates role matching, competency gap analysis, and succession planning at scale. Regulatory pressure, notably the EU Pay Transparency Directive and state-level wage-range laws in the United States, further accelerates adoption by obligating employers to document objective progression pathways.

Key Report Takeaways

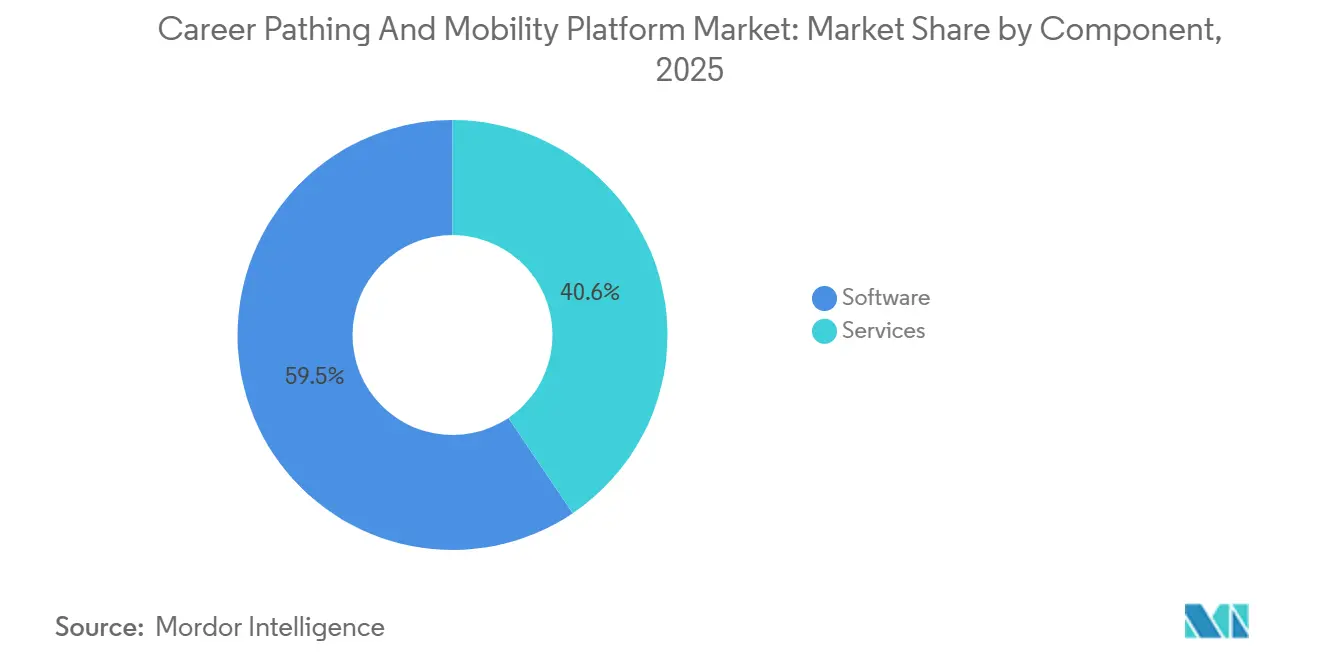

- By component, software captured 59.45% revenue share in 2025, while services are expanding at an 11.78% CAGR through 2031 and are on track to outpace software growth over the forecast horizon.

- By deployment mode, on-premises solutions held 67.49% of the career pathing and mobility platform market share in 2025, yet cloud offerings are advancing at a 12.04% CAGR through 2031 as multinational employers pursue unified talent visibility.

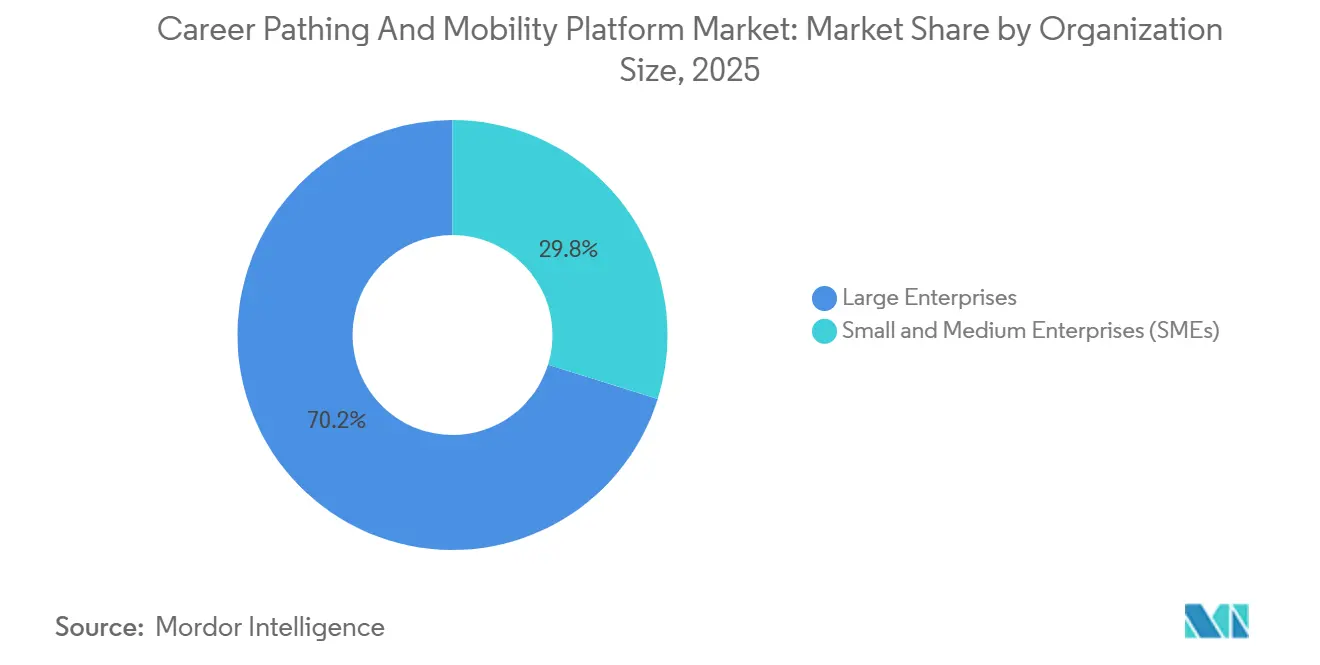

- By organization size, large enterprises accounted for 70.18% of 2025 spending, whereas small and medium enterprises are scaling investment at an 11.49% CAGR through 2031, benefiting from bundled career-pathing modules within broader human-capital-management suites.

- By industry vertical, information technology and telecommunications commanded 26.37% of 2025 revenue, but healthcare and life sciences are set to post the fastest growth at a 10.61% CAGR to 2031 in response to acute workforce shortages.

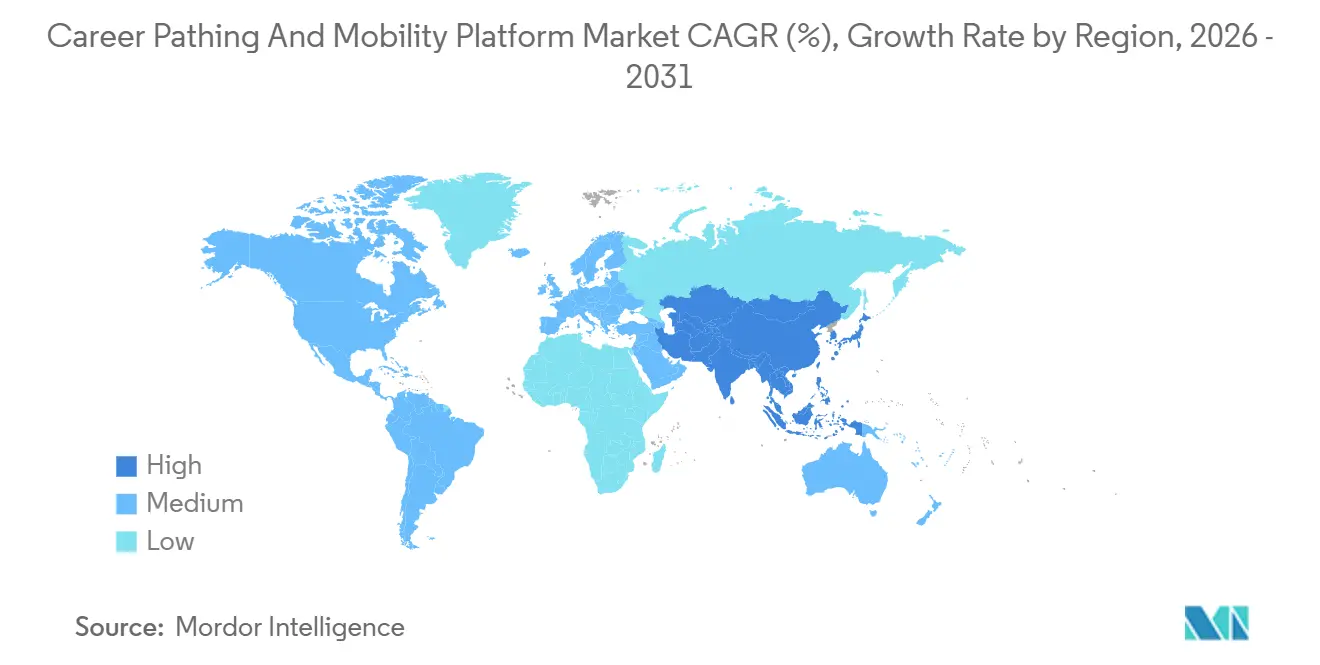

- By geography, North America led with 37.22% revenue share in 2025, while Asia-Pacific is projected to be the fastest growing region at a 10.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Career Pathing and Mobility Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration to skills‑based talent strategies | +2.8% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Growing adoption of AI‑driven talent intelligence platforms | +2.4% | North America, core growth in Asia‑Pacific | Short term (≤ 2 years) |

| Intensifying demand for internal mobility amid hiring freezes | +1.9% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Expansion of continuous learning ecosystem integrations | +1.3% | Global, strongest in IT and telecommunications | Medium term (2-4 years) |

| Increasing compliance pressures for pay and progression transparency | +0.9% | Europe and selected U.S. states | Long term (≥ 4 years) |

| Rise of hybrid work accelerating digital career‑coaching tools | +0.7% | Global, strongest in knowledge‑worker sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration to Skills-Based Talent Strategies

Enterprises are dismantling rigid job hierarchies in favor of granular skills taxonomies that match people to projects on demand. Talent teams now redeploy analysts into data-science sprints or shift supply-chain specialists toward sustainability work without waiting for formal promotions. LinkedIn reported that 72% of talent leaders rank skills-first hiring as top priority in 2025, and Accenture estimated 44% of banking roles require reskilling, signaling wide-ranging strategic urgency. Pay transparency regulations in Europe reinforce this shift by demanding auditable justification for wage differences, which skills-aligned frameworks deliver. As a result, platforms embedding dynamic skills graphs are becoming integral to workforce planning rather than optional plug-ins.

Growing Adoption of AI-Driven Talent Intelligence Platforms

Artificial intelligence has moved from bolt-on feature to design cornerstone for next-generation career-pathing systems. Recent launches such as SAP Career Development Agent and Oracle Career Advancement Command Center automate vacancy matching, development planning, and succession mapping, reducing manager workload while elevating match precision.[1]SAP, “SuccessFactors Career Development Agent Launch,” sap.com Phenom processes more than 1 billion talent interactions yearly, generating behavioral signals that trim time-to-fill by up to 40%. Regulatory bodies now scrutinize algorithmic decision-making, pushing vendors to embed explainability dashboards and human-in-the-loop override functions. Organizations that operationalize AI-driven insights report faster redeployment cycles and measurable retention gains.

Intensifying Demand for Internal Mobility Amid Hiring Freezes

Macroeconomic headwinds and capital-allocation discipline have led enterprises to pause external hiring even as critical roles remain vacant, forcing HR leaders to mine internal talent pools. 74% of respondents need more than a year to fill senior posts, yet only half can easily source global talent, underscoring supply-demand mismatch. Case studies from Hyatt and DHL show double-digit increases in internal moves and significant recruitment cost savings after platform deployment. Hospitals such as Parkview Health documented retention uplift from 87% to 91.3%, reinforcing mobility as a risk-mitigation lever in high-turnover settings.

Expansion of Continuous Learning Ecosystems Integrations

Static career maps are giving way to dynamic journeys that prescribe courses, credentials, and stretch assignments. Degreed’s launch of 150 industry pathways and Fuel50’s integration with Degreed Learn+ exemplify the convergence of learning and mobility, allowing completion data to update skills profiles automatically. Financial-services firms see particular value as half of roles face AI disruption by 2030, necessitating continuous upskilling. Vendors that offer bidirectional data flows create switching costs, raising customer lifetime value and throttling churn.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy concerns around employee profiling | -1.4% | Europe and North America | Short term (≤ 2 years) |

| Integration complexities with legacy HR tech stacks | -1.1% | Global, acute in large on‑premises environments | Medium term (2-4 years) |

| Limited analytics skills inside HR departments | -0.6% | Global, strongest in mid‑market and public-sector organizations | Long term (≥ 4 years) |

| Economic slowdowns curtailing HR technology budgets | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy Concerns Around Employee Profiling

Aggregating performance reviews, skills assessments, and behavioral signals enables granular segmentation but also triggers stringent GDPR and EU AI Act obligations. Cumulative GDPR fines surpassed EUR 4.2 billion, illustrating regulators’ willingness to levy sizable penalties. Vendors must invest in role-based access, explainability, and impact assessments, adding engineering overhead that can slow feature releases. Multinationals often apply European standards globally, amplifying compliance costs across non-EU operations.

Integration Complexities with Legacy HR Tech Stacks

Hundreds of enterprises still rely on Oracle PeopleSoft, SAP ECC, and ADP Workforce Now on-premises installations. Bridging these systems with modern cloud-native mobility platforms requires complex data-mapping, dual-running costs, and mitigation of payroll write-back risks. Extracting millions of historical records can span weeks, and full HCM transformations often run 12-24 months, stalling time-to-value. Vendors must therefore maintain coexistence strategies or risk displacement by point solutions that promise lighter-weight overlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum as Complexity Deepens

Services accounted for a smaller share than software at 40.55% of 2025 revenue, yet their 11.78% CAGR through 2031 outstrips software growth, underscoring a shift from license acquisition to value realization. Implementation projects increasingly involve mapping legacy job architectures to skills frameworks, configuring API pipelines, and training HR business partners to interpret algorithmic insights. Managed services resonate with mid-market buyers that lack dedicated HR technology teams, while large enterprises favor consulting engagements to customize workflows across multiple business units. Vendors owning robust services arms can capture a disproportionate share of customer lifetime value and hedge against price pressure on subscriptions.

Software subscriptions, although still dominant, face commoditization as core functionality converges across vendors. Differentiation now hinges on embedded AI copilots, ecosystem integrations, and regulatory compliance toolkits. Platforms that bundle proprietary skills graphs, real-time labor market intelligence, and in-product benchmarking command premium contract values even as per-user pricing compresses elsewhere. The widening services footprint therefore signals market maturation and increasing customer expectation for outcome-based partnerships.

By Deployment Mode: Cloud Accelerates Despite On-Premises Entrenchment

On-premises deployments retained 67.49% of the career pathing and mobility platform market size in 2025, reflecting sunk investments, data-sovereignty mandates, and customized integrations. Cloud solutions, however, are expanding at a 12.04% CAGR thanks to rapid time-to-value, elastic compute for AI workloads, and centralized compliance tooling.[2]ADP, “HR Trends for Small Businesses,” adp.comMultinationals with teams in 100-plus jurisdictions lean on global cloud backbones to unify skills taxonomies and analytics dashboards without regional data-center build-outs.

Hybrid coexistence models remain critical where sensitive employee data must reside on-premises while analytics leverage cloud processing. Oracle’s dual-stack strategy illustrates the pragmatic middle ground, enabling phased migrations that derisk change management. Over the forecast period, incremental cloud wins are expected to chip away at on-premises share, yet full displacement will be gated by industry-specific regulations and capital budgeting cycles.

By Organization Size: SME Uptake Climbs on Bundled Offerings

Large enterprises commanded more than two-thirds of 2025 spending, deploying sophisticated mobility ecosystems to mitigate succession risk and comply with transparency mandates. Yet small and medium enterprises are logging an 11.49% CAGR to 2031 as vendors wrap career-pathing modules into payroll, time, and benefits suites. Integrated packaging lowers entry barriers by removing the need for separate procurement processes and dedicated administrators.

SMEs chiefly seek to curb recruitment costs and retain top performers in tight labor markets, aligning with features such as AI-driven role recommendations and low-code workflow configurators. Conversely, global enterprises emphasize support for matrix reporting lines, regional compliance, and multi-language skills libraries. The bifurcation necessitates tiered product strategies that balance ease-of-use for SMEs with extensibility for Fortune 500 clients.

By Industry Vertical: Healthcare Emerges as the Fastest Grower

Information technology and telecommunications held 26.37% share in 2025, reflecting early adoption of API-first systems and data-driven HR cultures. Healthcare and life sciences, however, are projected to outpace all other verticals with a 10.61% CAGR through 2031 as hospitals confront nurse shortages and soaring turnover costs. Platforms that automate competency mapping and prescribe upskilling paths help providers redeploy staff to high-acuity units, directly alleviating staffing gaps.

Financial services prioritize reskilling amid AI-driven role evolution, while manufacturing wrestles with a projected 2.1 million unfilled jobs by 2030. Retailers use internal marketplaces to flex talent across seasonal peaks, and government agencies tackle looming retirement cliffs by pre-planning rotations. Vertical-specific content packs and regulatory templates therefore become decisive differentiators as vendors compete for specialized buyer personas.

Geography Analysis

North America retained 37.22% of 2025 revenue, buoyed by early adopter enterprises, mature vendor ecosystems, and state-mandated pay transparency that obliges documented progression frameworks. Consulting majors headquartered in the region embed career-pathing tools within digital workforce transformations, further amplifying software demand.

Asia-Pacific is primed for the fastest expansion at a 10.97% CAGR through 2031, catalyzed by China’s Greater Bay Area visa reforms, Singapore’s preferential tax zones, and rising cross-border assignments. Enterprises in the region favor platforms that can reconcile multi-jurisdiction labor rules and support rotational programs without permanent relocations. Local champions, notably in Japan, tailor workflows to seniority-based advancement norms, challenging global vendors to localize feature sets.

Europe’s market growth is framed by stringent GDPR and EU AI Act provisions that elevate compliance complexity.[3]European Commission, “Pay Transparency Directive,” ec.europa.euYet the same regulations create a protective moat for vendors able to offer turnkey audit trails, driving premium pricing. Middle Eastern adoption accelerates under national localization strategies such as Saudi Arabia’s Vision 2030, while South America and Africa remain early-stage, with deployments clustered in government modernization projects and multinational subsidiaries.

Competitive Landscape

The competitive field is moderately fragmented. HCM suite providers such as Workday, SAP, and Oracle are embedding agentic AI capabilities natively, protecting installed bases and creating high switching costs. Specialist vendors, including Gloat, Fuel50, and Eightfold AI, address white spaces in mid-market healthcare, manufacturing, and retail where legacy suites lack depth.

Recent consolidation, exemplified by Docebo’s acquisition of 365Talents and Phenom’s purchase of Included AI, signals an industry pivot toward unified talent-intelligence platforms. Strategic differentiation centers on real-time skills graphs, open-API ecosystems, and regulatory compliance safeguards.

Vendors that deliver explainable AI and role-based access controls gain an advantage in regions governed by the EU AI Act. Partnerships with learning-experience platforms and payroll providers broaden addressable markets, particularly among SMEs seeking single-stack HR solutions. Competitive intensity is expected to heighten as venture-backed entrants target vertical niches and as established suites double down on embedded AI roadmaps.

Career Pathing and Mobility Platform Industry Leaders

Workday, Inc.

SAP SE

Oracle Corporation

ADP, Inc.

Eightfold AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NextLadder Ventures launched a USD 1 billion NavTech AI fund targeting workforce analytics and career-pathing technologies.

- May 2026: Eightfold AI integrated with Oracle Fusion Cloud HCM to extend AI-driven talent matching across Oracle’s enterprise customer base.

- April 2026: Oracle released Fusion Agentic Applications for HR, featuring an AI-powered Career Advancement Command Center.

- April 2026: Humanly acquired Anthill, adding conversational AI to automate career coaching interactions.

Global Career Pathing and Mobility Platform Market Report Scope

The Career Pathing and Mobility Platform market assists employees in exploring internal career trajectories, aligning skills with opportunities, and managing role transitions. Leveraging skills data, learning suggestions, and AI-driven mobility insights, these tools foster internal talent development. Organizations utilize them to mitigate turnover, bolster succession planning, and enhance workforce agility. The market encompasses both standalone career mobility solutions and career modules integrated within talent management suites.

The Career Pathing and Mobility Platform Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Small and Medium Enterprises [SMEs], and Large Enterprises), Industry Vertical (BFSI, IT and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Government and Public Sector, Education, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Professional Services |

| Managed Services |

| Cloud-Based |

| On-Premises |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Government and Public Sector |

| Education |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Organization Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | BFSI | |

| IT and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Education | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current career pathing and mobility platform market size and projected growth?

The market stands at USD 2.59 billion in 2026 and is forecast to reach USD 4.09 billion by 2031, reflecting a 9.57% CAGR according to Mordor Intelligence.

Which component segment is growing the fastest?

Services are expanding at an 11.78% CAGR through 2031 as organizations seek implementation, integration, and managed support, per Mordor Intelligence data.

Why are healthcare organizations adopting these platforms rapidly?

Acute nurse shortages, high turnover costs, and mandated upskilling make structured internal mobility essential, driving a 10.61% CAGR in healthcare and life sciences.

How are regulations influencing platform design in Europe?

GDPR and the EU AI Act require transparency, human oversight, and impact assessments, prompting vendors to build explainable AI and robust access controls into their products.

What advantages do cloud deployments offer over on-premises systems?

Cloud platforms deliver quicker time-to-value, elastic compute for AI workloads, centralized compliance documentation, and lower capital outlays, fueling a 12.04% CAGR through 2031.

Page last updated on: