Employee Experience Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.65 Billion |

| Market Size (2031) | USD 7.27 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employee Experience Platform Market Analysis by Mordor Intelligence

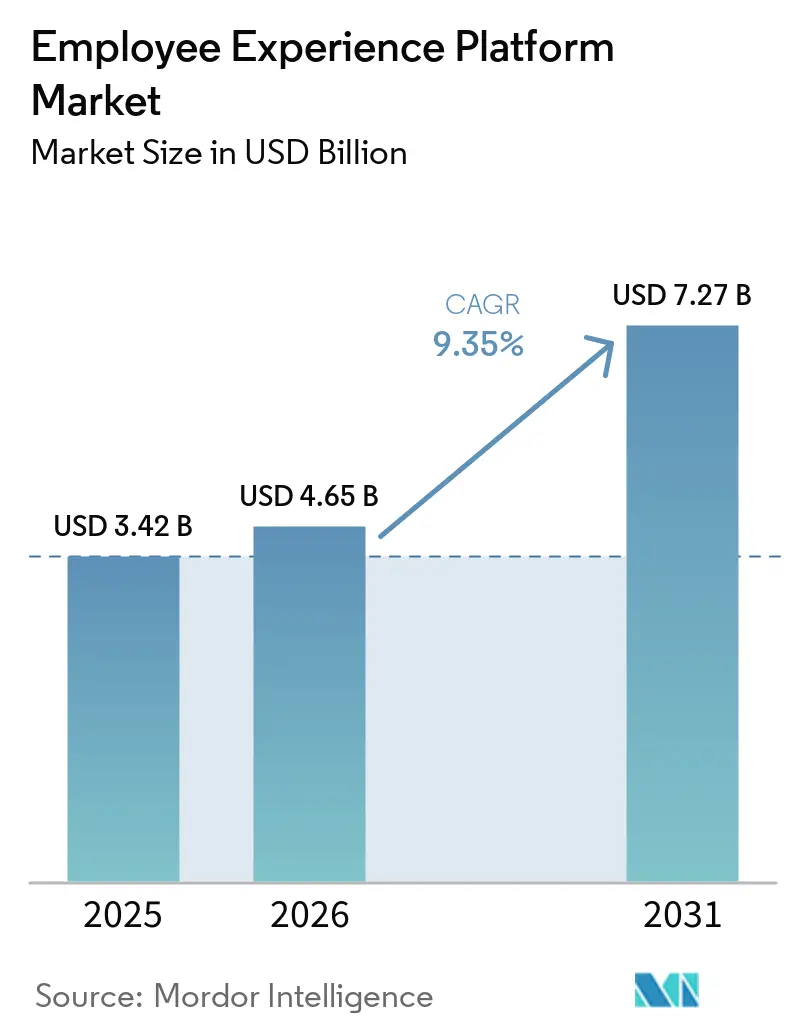

The employee experience platform market size is projected to be USD 3.42 billion in 2025, USD 4.65 billion in 2026, and reach USD 7.27 billion by 2031, growing at a CAGR of 9.35% from 2026 to 2031. The employee experience platform market is expanding as hybrid and distributed work are now part of the standard workforce design across sectors. Demand is also rising as agentic AI moves these platforms from passive feedback tools into active systems for self-service, communication, and workflow support. Organizations now treat workforce experience as a direct driver of retention, productivity, and compliance, elevating the category from an HR-led purchase to a broader leadership priority. Competition remains moderate to high because broad experience management vendors and specialist communication and engagement providers are all pushing deeper AI capabilities and stronger integration depth. The employee experience platform market is also gaining support from tighter talent conditions and higher expectations from multi-generational workforces, which are pushing buyers toward integrated platforms instead of isolated annual survey tools.

Key Report Takeaways

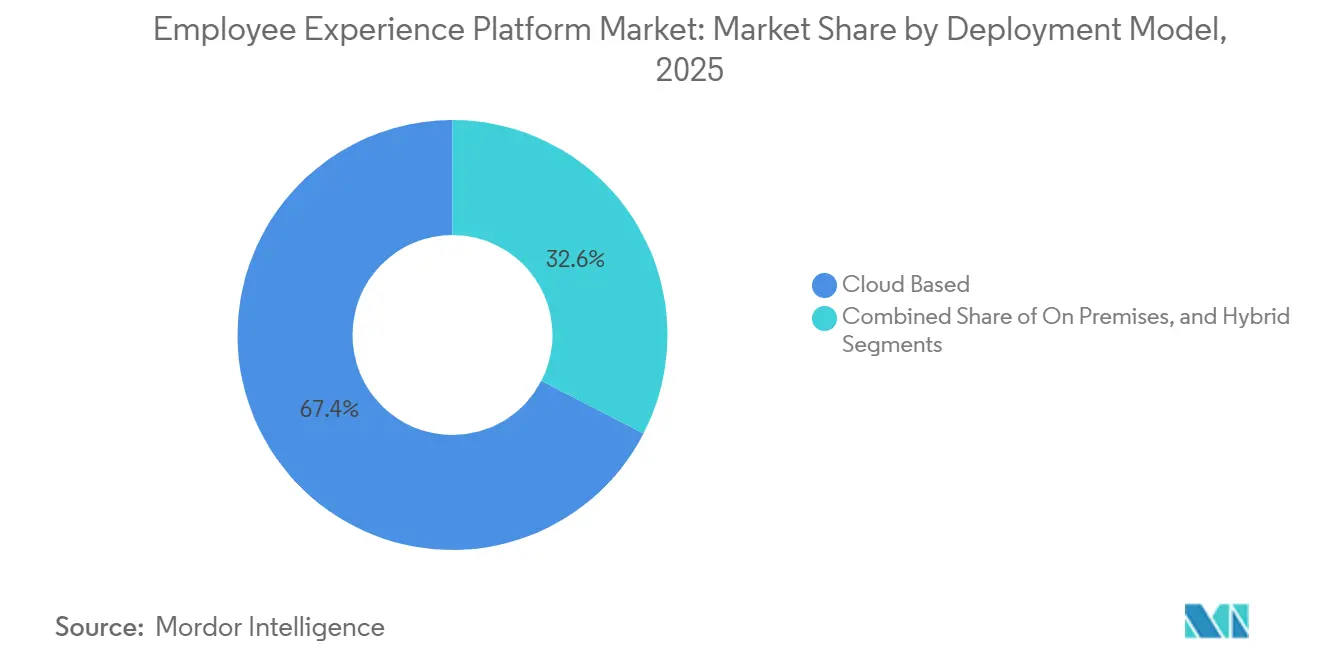

- By deployment model, cloud-based platforms held the largest share at 67.42% in employee experience platform market in 2025, while hybrid deployment is forecast to grow at a CAGR of 11.38% during 2026-2031.

- By end-user enterprise size, large enterprises commanded 62.19% of the market in 2025, while small and medium-sized enterprises were the fastest-growing cohort, with a CAGR of 12.74% during 2026-2031.

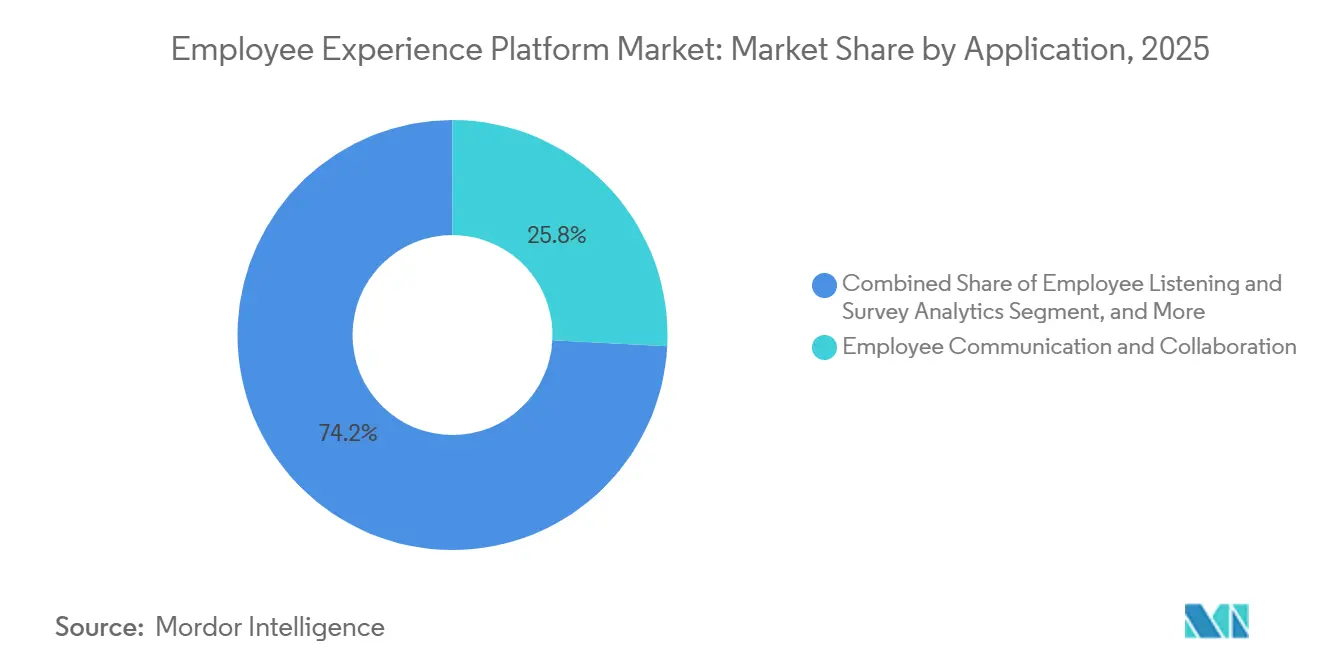

- By application, employee communication and collaboration retained the largest share at 25.83% in 2025, while employee listening and survey analytics is the fastest-growing application segment at a CAGR of 13.41% during 2026-2031.

- By end-user industry, the IT and telecom sector held the largest share at 22.67% in 2025, while healthcare and life sciences are the fastest-growing industry segments at a CAGR of 14.12% during 2026-2031.

- By geography, North America held the largest regional share at 36.91% in 2025, while Asia-Pacific is the fastest-growing regional market at a CAGR of 14.87% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employee Experience Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid and Distributed Work Normalization | +2.1% | Global, with concentrated impact in North America and Western Europe | Medium term (2-4 years) |

| AI-Powered Personalization and Employee Self-Service | +2.8% | Global, early-stage gains in North America and APAC, spill-over to MEA | Medium term (2-4 years) |

| Board-Level Focus on Retention and Productivity Metrics | +1.4% | North America and Europe, with emerging traction in APAC | Short term (= 2 years) |

| Frontline Workforce Digitization | +1.2% | APAC core, spill-over to MEA and South America, manufacturing-heavy markets | Medium term (2-4 years) |

| CSRD and ESRS S1 Workforce Disclosure Readiness | +0.8% | Europe primarily, with spill-over to non-EU multinationals operating in EU | Short term (= 2 years) |

| Skills Graphs and Internal Talent Mobility Orchestration | +0.7% | North America, Western Europe, technology-intensive APAC markets | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Hybrid And Distributed Work Normalization

Hybrid work has become a standard operating model across large employers, tying the employee experience platform market to workplace redesign rather than a short-lived adoption wave. A 2025 global study found that 88% of employers offered some form of hybrid work, while only 32% invested adequately in collaboration technology, leaving a clear gap for platform vendors to fill.[1]Cisco, “Navigating Hybrid Work Strategies in the Evolving Workplaces: Cisco Global Hybrid Work Study 2025,” Cisco, newsroom.cisco.com The same study showed that 90% of employees value collaboration tools and 77% view strict return-to-office mandates as a sign of low trust in remote productivity. This gap is pushing HR and IT teams to support shared platforms that improve communication, feedback, and access across locations. The employee experience platform market is also benefiting from retirement-driven labor pressure in Europe, where 12.9 million baby boomers in the DACH region are moving toward retirement through the mid-2030s, which raises the value of retention infrastructure. As a result, buyers are treating employee experience tools as part of workforce continuity planning, not just as engagement software.

AI-Powered Personalization And Employee Self-Service

AI personalization is moving platforms away from passive survey tools and toward active systems that route requests, recommend content, and resolve common HR tasks in real time. This shift matters because organizations now expect workplace tools to feel faster, more relevant, and easier to use across daily workflows. A platform example showed it handled more than 11.5 million interactions in 2024, resolving 94% of them within the system, and contributed USD 3.5 billion in productivity savings, demonstrating the scale of value that well-built self-service models can unlock.[2]Nickle LaMoreaux, “Entdecken Sie Die Zukunft Des Personalwesens, Indem Sie Ein KI-Zentriertes Unternehmen Werden,” IBM, ibm.com These results are shaping buyer expectations inside the employee experience platform market, especially where HR teams are under pressure to serve larger workforces without adding support headcount. They are also pushing vendors to connect personalization features with governance controls so that automation can scale without creating new risk. The result is a stronger demand for platforms that combine listening, workflow automation, and AI-assisted self-service into a single operating layer.

Board-Level Focus On Retention And Productivity Metrics

Employee experience budgets are now reviewed more often based on retention, productivity, and compliance outcomes than on standalone engagement goals. That shift has changed procurement inside the employee experience platform market, because CFO, HR, and IT teams now expect a clearer path from platform use to measurable business results. Buyers are placing more weight on action planning, manager enablement, and closed-loop follow-up than on survey collection alone. Vendors that connect listening data with workflow actions and performance signals are gaining an advantage in enterprise evaluations. This board-level attention is also reducing tolerance for slow implementations, which makes time-to-value a more important selling point. It is creating space for vendors to show early operational wins, even as larger retention and productivity gains take longer to measure.

Frontline Workforce Digitization

Frontline workforce digitization is expanding the employee experience platform market beyond office-based use cases and into manufacturing, retail, logistics, and field operations. Weavix reported in 2026 that 53% of frontline manufacturing workers lose at least 5% of their workday while waiting for critical information, which it linked to USD 15.4 billion in annual direct productivity loss in manufacturing.[3]Weavix, “Weavix Survey Finds Frontline Manufacturing Workers Are Ready for AI, But Stuck with Outdated Tools,” Weavix, weavix.com This gap explains why frontline communication is becoming a budget line item instead of an optional add-on. Employers are looking for tools built around shift notifications, multilingual messaging, QR-based onboarding, voice support, and offline access, because desk-centric designs do not fit operational settings. That need is strongest in Asia-Pacific and other manufacturing-heavy regions, where large workforces still have limited digital access at the point of work. Vendors that can serve both desk-based and deskless populations through a single platform are gaining a broader addressable base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cross-System Integration Complexity | -1.5% | EU and APAC core, spill-over to North America for multinational deployers | Medium term (2-4 years) |

| ROI Attribution and Change Fatigue | -1.0% | Global, concentrated in SME and mid-market segments | Short term (= 2 years) |

| EU AI Act and Works Council Limits on Monitoring Features | -0.7% | Europe primarily, affects non-EU vendors selling into EU markets | Short term (= 2 years) |

| Suite Bundling and Ecosystem Lock-In Pressure | -0.5% | Global, particularly where Microsoft or SAP ecosystems are dominant | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Cross-System Integration Complexity

Data privacy and integration complexity continue to slow the employee experience platform market, especially when platforms pull sentiment, behavioral, and performance data from many systems at once. Buyers in Europe are applying stricter review standards to AI-enabled listening and analytics features, which extends legal and technical validation before rollout. Integration work is also heavier than many buyers first expect, because HRIS, collaboration, payroll, performance, and security systems often store workforce data in different formats and under different permissions. This creates delays at the point where many projects move from pilot use into enterprise-wide deployment. The effect is strongest in organizations that operate across borders, where data residency, local hosting, and works council expectations all shape implementation design. Vendors that offer privacy-by-design controls and cleaner integration frameworks are better placed to convert this restraint into a procurement advantage.

ROI Attribution And Change Fatigue

ROI attribution remains a practical barrier because attrition, productivity, and engagement outcomes change for many reasons simultaneously. This makes it hard for buyers to isolate the financial impact of a single platform within a short budgeting window. The issue is more visible in mid-market companies, where each software purchase must compete against near-term cost controls and limited change capacity. Change fatigue adds to the challenge because each new listening, recognition, and AI module requires separate onboarding, manager training, and communication support. When value is expected in a few quarters but fuller benefits may take 18-24 months to emerge, buyers often delay, narrow, or phase deployments. Vendors that provide interim milestones, adoption dashboards, and clearer outcome measurement are more likely to protect renewals and expand accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Leads While Hybrid Gains Ground

Cloud-based platforms held 67.42% of the employee experience platform market share in 2025, which reflects the need to support distributed teams and continuous data exchange across modern HR systems. Cloud deployment aligns with the current direction of the employee experience platform market by enabling faster updates, easier integration, and broader access across locations. It also provides vendors with a stronger foundation for AI-enabled listening, workflow automation, and analytics features that depend on real-time data flow. That advantage is especially important for organizations that want communication, feedback, recognition, and support tools to operate through one connected architecture. On-premises deployments remain relevant, but they are increasingly tied to narrow cases where strict network isolation or highly specific internal controls outweigh the flexibility of cloud models.

Hybrid deployment is the fastest-growing model, with a 11.38% CAGR, indicating that buyers still want greater control over where sensitive workforce data is stored. The employee experience platform market for hybrid deployment is growing as regulated industries and large enterprises seek to balance data residency requirements with the need for cloud-based analytics. This is especially visible in European markets where local hosting preferences continue to shape procurement design. The direction of travel is still cloud-first, but it is cloud-first with stronger governance layers rather than cloud-only at any cost.

By End User Enterprise Size: Large Enterprises Hold The Spending Base While SMEs Expand Faster

Large enterprises captured 62.19% of the employee experience platform market in 2025, which reflects their need to manage large workforces across business units, geographies, and layered reporting structures. These organizations typically require deep integration with HRIS, learning, payroll, performance, and identity systems, which raises both the scope and cost of deployment. That complexity favors vendors with stronger implementation capacity, broader product suites, and clearer governance controls. It also explains why large enterprises remain the core revenue base of the employee experience platform market even as new buyers enter. In many cases, these organizations are not buying a single feature but a connected system that ties communication, listening, recognition, and manager workflows together.

Small and medium-sized enterprises are the fastest-growing cohort, with a CAGR of 12.74% through 2031, indicating that cost and setup barriers are easing. The employee experience platform market size for SMEs is growing as modular cloud-native products lower entry thresholds for companies with 100-2,000 employees. These buyers are responding to tighter labor competition and higher employee expectations, especially in sectors where smaller firms once depended on informal culture as their main retention tool. Vendors that can serve enterprise and mid-market needs with a single product architecture are in a stronger position to expand without building separate platforms.

By Application: Communication Holds The Revenue Base While Listening Analytics Accelerates

Employee communication and collaboration had the largest application share at 25.83% in 2025, as it serves as the base layer for most deployments in the employee experience platform market. Organizations often start with communication because it solves a daily operating need before they expand into listening, recognition, wellbeing, or performance-linked use cases. This gives communication tools a durable revenue position, particularly in hybrid and frontline settings where access, clarity, and reach are basic requirements. The segment also benefits from the fact that poor communication is easy to identify and easier to tie to missed operational outcomes than softer engagement measures. As a result, it continues to anchor spending even as the application mix becomes broader.

Employee listening and survey analytics is the fastest-growing application, with a 13.41% CAGR through 2031, as employers shift from annual feedback cycles to more continuous sensing models. The employee experience platform market for employee listening and survey analytics is growing as buyers seek faster theme detection, greater sentiment visibility, and earlier signals of attrition risk. Engagement and recognition tools remain important, but they are increasingly expected to connect with manager guidance and follow-up actions rather than stand alone. Product design is moving in the same direction, as shown by a 2026 release that embedded evidence-based AI review drafting and real-time coaching intelligence directly into manager workflows.[4]Amaury Sablon, “Evidence-Based AI Reviews, Coaching and Summarization in 1:1s, Compensation Enhancements, and More,” Lattice, lattice.com The wider application mix is therefore moving toward platforms where communication, listening, and workflow support share a single data model rather than being spread across separate systems.

By End-user Industry: IT And Telecom Leads Adoption While Healthcare And Life Sciences Grows Fastest

The IT and telecom vertical accounted for 22.67% of the employee experience platform market in 2025, reflecting early digital HR adoption and a long-standing focus on retention in highly competitive talent markets. This vertical has been quicker than most to connect employee listening, internal mobility, performance workflows, and communication within a single operating environment. Buyers in this group also tend to expect consumer-grade workplace tools, which has supported faster rollout of richer platform features. That makes IT and telecom the most mature use cases in the employee experience platform industry, with higher readiness for integrated, AI-assisted deployments. The segment remains important because its buying behavior often sets feature expectations for the wider employee experience platform market.

The healthcare and life sciences industry is the fastest-growing end-user industry, with a CAGR of 14.12% through 2031, because its workforce challenges are both operational and human. Frontline clinical teams often face communication gaps, high workload intensity, and high emotional strain, which increase the demand for platforms that support clearer communication and better follow-up. The sector is also under pressure to document workforce wellbeing and maintain stronger links between employee support and service quality. Retail, manufacturing, BFSI, government, and other industries continue to add demand, but healthcare and life sciences have a sharper growth path because the cost of poor workforce communication is especially evident in daily operations.

Geography Analysis

North America held 36.91% of the employee experience platform market share in 2025, making it the largest regional cluster. The region benefits from high enterprise software adoption, a mature HR technology base, and a dense concentration of vendors serving hybrid and knowledge-based workforces. The United States remained the main revenue center, while Canada and Mexico supported expansion as employers standardized platforms across North American operations. Demand in this part of the market is also moving from basic engagement surveys toward predictive attrition, AI-supported manager tools, and broader workforce analytics. Technology services, business services, and finance and insurance had among the highest hybrid adoption rates, supporting continued demand for platform-enabled employee communication and coordination.

Asia-Pacific is the fastest-growing region with a CAGR of 14.87% through 2031. Market size in Asia-Pacific is rising on the back of rapid enterprise digitization, mobile-first workforce strategies, and significant unmet demand among frontline workers in manufacturing, retail, and logistics. India’s large IT services base continues to support the adoption of engagement and performance tools, while China and South Korea are driving stronger interest in frontline communication platforms. This regional pattern provides the market with a broader growth base beyond office-led deployments.

Europe remained the second-largest regional cluster, supported by Germany, the United Kingdom, France, the Netherlands, and Spain. The region stands out because workforce experience, data governance, and reporting needs are becoming more closely linked in buying decisions. The ESRS S1 framework keeps workforce disclosures focused on working conditions, training, diversity, and well-being, which reinforces demand for systems that can collect and organize employee data more consistently. South America is still a developing market, with Brazil and Argentina showing stronger activity in financial and professional services. The Middle East is seeing more investment as workforce localization programs and large-employer projects increase the need for structured onboarding and communication, while Africa remains early-stage, with South Africa and Nigeria serving as the main entry points for cross-border employers.

Competitive Landscape

The employee experience platform market is moderately fragmented, with competition spread across full-suite experience management vendors, specialist communication and intranet providers, and point solutions in listening, recognition, and manager enablement. No single company holds a dominant position, and differentiation is increasingly tied to AI capability, integration depth, frontline reach, and compliance architecture. This mix keeps pricing pressure high in the mid-market while allowing stronger enterprise platforms to defend premium positioning through broader functionality and deeper services. It also means the market is in a consolidation phase rather than moving toward winner-take-all concentration. Buyers now compare vendors not only on feature depth, but also on whether one platform can serve desk-based and frontline populations through a common data structure.

Strategic moves in 2025 and 2026 show how vendors are expanding scope through M&A and product redesign. The LumApps-Beekeeper merger created a larger platform focused on both desk-based and frontline employees, and LumApps later added Comeen to extend further into workplace experience and building operations. Appspace strengthened its employee communications position through the acquisition of Igloo Software, which broadened its intranet and digital workplace capabilities. Perceptyx acquired Lyceum AI to connect employee experience listening more directly with learning and development, addressing a long-standing gap between sentiment measurement and skill-building action. These moves show that vendors are trying to own a broader operating layer rather than a single narrow use case.

Product strategy is also shifting toward AI-native design. Staffbase introduced an AI-native employee experience platform with hyper-personalized content, a native AI assistant, and prompt-based content creation, reflecting how communication-first vendors are moving closer to orchestration and automation roles. Medallia expanded its generative AI agenda in 2026 with tools such as Insights Assistant and Smart Topic Builder, while also broadening multilingual support for large global deployments. The market still has meaningful white space in frontline-heavy industrial settings, in SMEs across emerging economies, and in solutions that connect employee data with reporting and compliance needs. That leaves room for both large vendors and focused challengers to grow, provided they can show credible integration, clear governance, and faster time-to-value. The result is a market where competitive advantage comes less from owning a single feature and more from combining multiple workflows into a useful, trusted system.

Employee Experience Platform Industry Leaders

Qualtrics, LLC

Culture Amp Pty Ltd

LumApps SAS

Simpplr Inc.

Staffbase GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: LumApps acquired Comeen, integrating space management and workplace services into its AI-powered hub, expanding beyond communications into full-stack employee experience.

- March 2026: Qualtrics launched conversational feedback and predictive retention analytics, refreshing EX25 with “technology” and “AI adoption,” driving structured action-taking in enterprise deployments.

- March 2026: Perceptyx acquired Lyceum AI, linking employee listening with learning and development through conversational agent Ellie, unifying EX and L&D systems for Fortune 100 clients.

- March 2026: Lattice introduced AI review drafting, embedded coaching agents, and Workday integration, reducing performance cycle overhead while embedding intelligence directly into manager workflows.

Global Employee Experience Platform Market Report Scope

The employee experience platform market refers to digital solutions designed to enhance how employees interact, engage, and collaborate within organizations. These platforms integrate tools for communication, recognition, listening, and survey analytics, well-being support, and other applications that improve workforce satisfaction and productivity. Delivered through cloud, on-premises, or hybrid models, they serve both SMEs and large enterprises across industries such as BFSI, healthcare, IT and telecom, retail, manufacturing, government, and education. The primary goal is to strengthen employee engagement, streamline workflows, and foster a connected workplace culture.

The employee experience platform market is segmented by Deployment Model (Cloud-based, On-premises, and Hybrid), Enterprise Size (Small and Medium-sized Enterprises and Large Enterprises), Application (Employee Communication and Collaboration, Employee Engagement and Recognition, Employee Listening and Survey Analytics, Employee Wellbeing and Support, and Other Applications), End-user Industry (BFSI, Healthcare and Life Sciences, IT and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-based |

| On-premises |

| Hybrid |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| Employee Communication and Collaboration |

| Employee Engagement and Recognition |

| Employee Listening and Survey Analytics |

| Employee Wellbeing and Support |

| Other Applications |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By End User Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Application | Employee Communication and Collaboration | |

| Employee Engagement and Recognition | ||

| Employee Listening and Survey Analytics | ||

| Employee Wellbeing and Support | ||

| Other Applications | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the employee experience platform market and how fast is it growing through 2031?

The employee experience platform market stands at USD 4.65 billion in 2026 and is projected to reach USD 7.27 billion by 2031, growing at a CAGR of 9.35% during 2026-2031.

Which deployment model leads employee experience platform adoption?

Cloud-based deployment leads with 67.42% share in 2025 because it supports scalability, easier integration, and continuous data flow across dispersed workforces.

Why is hybrid deployment gaining more attention in employee experience platforms?

Hybrid deployment is growing at 11.38% CAGR through 2031 because buyers in regulated settings want stronger control over sensitive workforce data while still using cloud analytics and workflow tools.

Which application area is expanding the fastest in employee experience tools?

Employee listening and survey analytics is the fastest-growing application, with a 13.41% CAGR through 2031, as organizations move from annual surveys to continuous feedback and earlier risk detection.

Which industries are creating the strongest demand for employee experience platforms?

IT and telecom led with 22.67% share in 2025, while healthcare and life sciences is growing fastest at 14.12% CAGR because of frontline communication gaps, wellbeing demands, and workforce documentation needs.

Which region is showing the strongest future growth in employee experience platforms?

Asia-Pacific is the fastest-growing region at a 14.87% CAGR through 2031, driven by enterprise digitization, mobile-first workforce strategies, and a large underpenetrated frontline employee base.

Page last updated on: