Skills Intelligence And Taxonomy Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 5.67 Billion |

| Growth Rate (2026 - 2031) | 21.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skills Intelligence And Taxonomy Platform Market Analysis by Mordor Intelligence

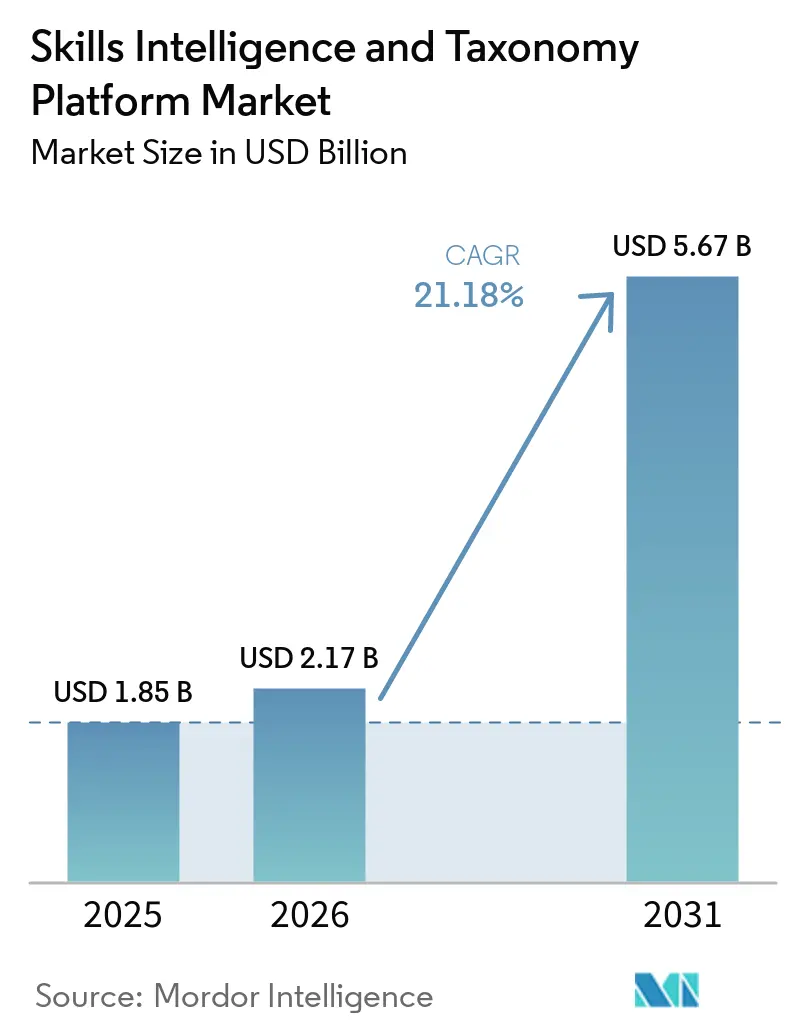

The skills intelligence and taxonomy platform market size was valued at USD 1.85 billion in 2025 and estimated to grow from USD 2.17 billion in 2026 to reach USD 5.67 billion by 2031, at a CAGR of 21.18% during the forecast period (2026-2031). This pace reflects a clear shift in enterprise spending toward structured workforce data that can support skills-based operating models, internal redeployment, and more consistent talent decisions. Demand is also rising because cloud-native artificial intelligence has reduced deployment friction, making these platforms easier to integrate with daily work systems and faster to operationalize across large organizations. Regulatory expectations around skills documentation, explainability, and workforce data quality are turning platform adoption into a risk management decision as much as a workforce modernization decision. Competitive pressure from HCM suite vendors is tightening pricing for basic features, while also pushing purpose-built providers to differentiate through deeper taxonomies, stronger inference quality, and better workflow integration. A further layer of demand is coming from agentic AI use cases, where enterprises need live, machine-readable skill graphs to support real-time task allocation across human workers and AI systems.

Key Report Takeaways

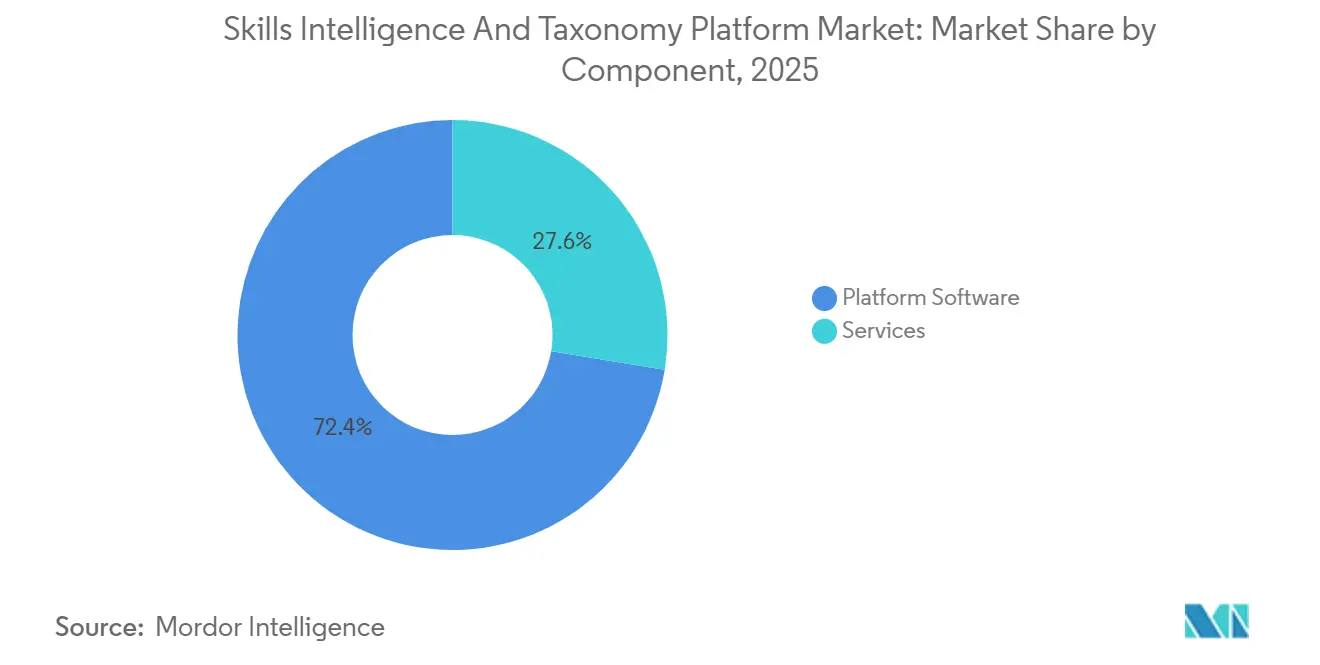

- By component, platform software led with 72.41% of 2025 revenue, while services are projected to expand at a 23.61% CAGR through 2031.

- By deployment model, cloud-based deployment held 68.92% of the 2025 skills intelligence and taxonomy platform market, and it is also the fastest-growing deployment model at a 24.83% CAGR through 2031.

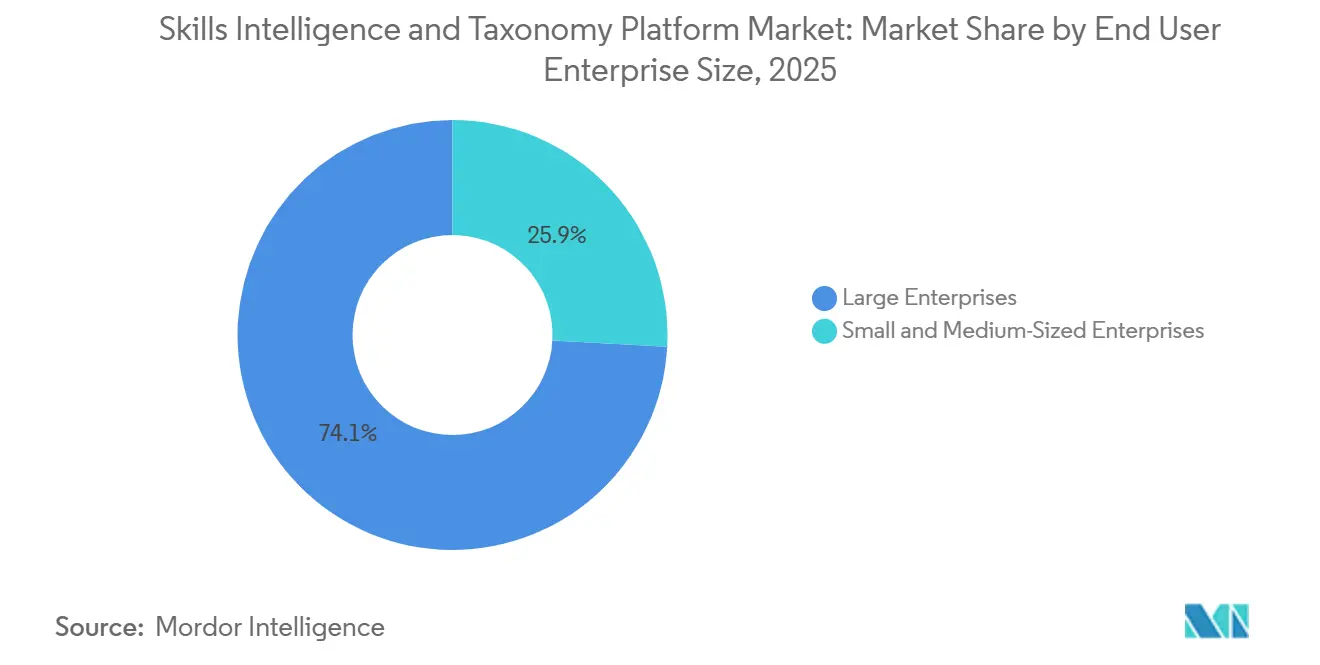

- By end-user enterprise size, large enterprises accounted for 74.13% of the 2025 skills intelligence and taxonomy platform market, while SMEs recorded the highest projected CAGR of 25.72% through 2031.

- By application, talent management and internal mobility commanded 29.34% of the 2025 market, while strategic workforce planning is projected to advance at a 26.41% CAGR for 2026-2031.

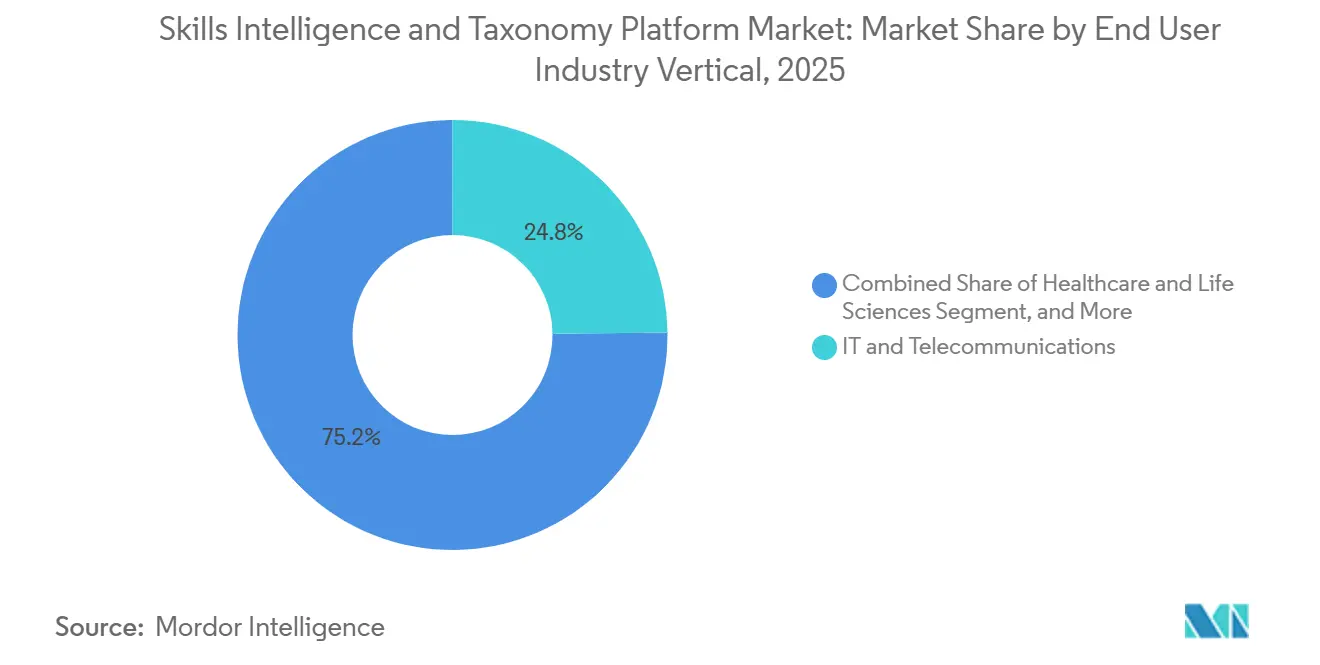

- By end-user industry vertical, information technology and telecommunications accounted for 24.82% of the 2025 market, while healthcare and life sciences are the fastest-growing verticals at a 27.12% CAGR through 2031.

- By geography, North America held 41.61% of the 2025 skills intelligence and taxonomy platform market, while Asia-Pacific is forecast to expand at a 28.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Skills Intelligence And Taxonomy Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift To Skills-Based Organization Design | +5.2% | Global | Long term (≥ 4 years) |

| Enterprise Focus On Internal Mobility And Retention | +4.3% | North America and Europe | Medium term (2-4 years) |

| Cloud-Native Artificial Intelligence Delivery Accelerating Time-To-Value | +3.8% | Global, with APAC core spill-over | Medium term (2-4 years) |

| Regulatory Pressure For Structured Workforce And Skills Disclosure | +2.6% | Europe, APAC | Short term (≤ 2 years) |

| Agentic Workflow Procurement Increasing Demand For Machine-Readable Skills Graphs | +2.1% | North America and Europe | Medium term (2-4 years) |

| Verifiable Credentials And Skills Wallets Improving Cross-Employer Skill Portability | +1.5% | Europe, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift To Skills-Based Organization Design Reshapes Talent Architecture

Organizations are moving away from fixed job descriptions and are building workforce models around skills that can be updated, compared, and redeployed across roles. The pressure is clear because 63% of employers identified skills gaps as the main barrier to transformation in the Future of Jobs Report 2025, which makes static role frameworks harder to defend in planning discussions.[1]World Economic Forum, “Future Of Jobs Report 2025,” World Economic Forum, weforum.org This shift raises demand for platforms that can maintain a common skills language across hiring, learning, mobility, and project staffing, rather than leaving each function to manage its own competency lists. The skills intelligence and taxonomy platform market is benefiting because a machine-readable taxonomy is becoming the operating layer that links workforce supply to business demand at enterprise scale. That need grows stronger as companies try to redeploy talent faster across teams, functions, and new work models without rebuilding role frameworks each time. The World Economic Forum’s 2025 description of skills intelligence as economic infrastructure captures why these platforms are moving into long-cycle enterprise budgets rather than short-term HR experimentation.[2]World Economic Forum, “Skills Intelligence, The New Economic Infrastructure,” World Economic Forum, weforum.org

Internal Mobility And Retention Investment Drives Platform Adoption

Internal mobility is becoming a financial decision, not just a talent practice, because enterprises want to fill more work with existing employees before turning to external hiring. Skills intelligence platforms support that shift by matching workers to roles, projects, and adjacent opportunities using verified or inferred capabilities instead of manager familiarity alone. A strong proof point came in April 2026, when 365Talents reported that SNCF saved USD 113 million in temporary labor costs through AI-driven skills matching.[3]365Talents, “Customer Success, SNCF, EUR 100 Million In Temporary Labor Savings,” 365Talents, 365talents.com LinkedIn’s 2026 Talent Velocity Report also showed that only 14% of organizations qualify as talent velocity leaders, suggesting that many employers still lack the infrastructure to move talent efficiently within the business. That gap is supporting platform demand because retention, redeployment, and workforce visibility are increasingly being funded together. As a result, buyers are treating skills systems as a way to lower hiring dependency and improve workforce stability, not only as a tool for HR process improvement.

Cloud-Native Artificial Intelligence Delivery Accelerates Time-To-Value

Cloud-native delivery is changing how these platforms are adopted, reducing setup friction and enabling skill data to be updated continuously from live enterprise systems. Microsoft’s March 2026 expansion of People Skills across Microsoft 365 E3 and E5 showed that skills inference is moving into collaboration software, where work activity already produces usable signals every day. That changes the value proposition because organizations can build richer skill profiles without depending only on self-declarations, surveys, or infrequent manager reviews. Cloud architecture also supports faster model updates, easier integration with adjacent software, and real-time querying by copilots and other AI tools that need current ontology data to function well. The commercial signal is also strong because TechWolf’s June 2024 Series B was co-led by SAP, Workday, and ServiceNow, showing that large enterprise software vendors see specialist taxonomy infrastructure as useful within their ecosystems. This is helping the market because buyers can adopt cloud-based skills systems with less concern that the model will sit outside core enterprise workflows.

Regulatory Pressure Turns Skills Data Into A Compliance Asset

Regulation is creating a separate demand stream because workforce skill records are becoming more important for auditability, explainability, and formal governance. The EU AI Act classified many workforce AI applications as high-risk systems, with AI literacy requirements beginning in February 2025 and broader enforcement starting in August 2026. In France, CNIL stepped up enforcement around automated HR decision-making under GDPR Article 22, which increases the need for traceable and explainable skills assessments instead of opaque or manual judgment calls. The European Commission also established the European Skills Intelligence Observatory in October 2025, reinforcing the role of structured skills data in labor market and economic policy. This matters because compliance-led spending tends to hold up better than discretionary HR spending during cost pressure. It also changes procurement logic, since buyers in Europe and parts of APAC can now justify these platforms as compliance infrastructure as much as workforce optimization software.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Employee Data Privacy And Artificial Intelligence Governance Burden | -1.8% | Europe, North America | Short term (= 2 years) |

| Integration Complexity Across Human Capital And Learning Systems | -1.4% | Global | Medium term (2-4 years) |

| Taxonomy Drift From Rapid Emergence Of Hybrid Human-Artificial Intelligence Roles | -0.9% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Embedded Skills Layers In Human Capital Suites Compressing Standalone Pricing Power | -0.7% | Global | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Employee Data Privacy And Artificial Intelligence Governance Burden Constrains Deployment Scale

Privacy obligations remain a real barrier because these platforms often infer employee skills from work behavior, collaboration patterns, and performance signals rather than relying only on declared profile data. That creates additional scrutiny under the EU AI Act and GDPR Article 22, especially when inferred skills influence mobility, hiring, or development decisions.[4]European Parliament And Council Of The European Union, “Regulation (EU) 2024/1689, Artificial Intelligence Act,” Official Journal Of The European Union, eur-lex.europa.eu A January 2026 Wharton and Accenture analysis also highlighted gaps between what workers say they can do and what employer AI systems infer or reward, raising fairness concerns that legal and HR teams cannot ignore. In practice, that means deployments often face longer reviews covering model documentation, consent workflows, data processing terms, and oversight responsibilities. The effect is most visible in regulated industries and in Europe, where risk teams can slow a rollout even after the business case has been accepted. This does not remove demand, but it does stretch procurement cycles and narrows early deployments to lower-risk use cases.

Integration Complexity Across Human Capital And Learning Systems Delays ROI Realization

Integration remains difficult because most enterprises are adding these platforms into HR environments that already include multiple systems for core HR, learning, recruiting, and performance management. Each of those systems may use different role structures, data models, permissions, and refresh schedules, which makes it harder to maintain a consistent skills graph over time. The HR Open Standards Consortium released the Trusted Career Profile specification in January 2026 to improve data portability, but enterprise adoption of new interoperability standards usually takes time after publication. Until that adoption broadens, buyers still face skill identifier mismatches, taxonomy translation problems, and delays in syncing skill updates across systems. These issues weaken user trust because recommendations are only as useful as the freshness and consistency of the underlying data. The commercial result is slower ROI realization, more limited first-phase deployments, and a longer path from signed contract to enterprise-wide usage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Software Anchors Revenue As Services Accelerate

Platform software held 72.41% of the skills intelligence and taxonomy platform market share in 2025, underscoring buyer preference for taxonomy engines, ontology management, and skills graph infrastructure. This dominance reflects the need for standardized skills language across hiring, learning, mobility, and workforce planning, with governed taxonomies and inference engines forming the backbone of durable organizational capability. Demand for platforms is also tied to continuously updated, machine-readable skill structures that support both human workflows and AI-assisted decision-making, making the software layer the starting point for most enterprise purchases, even when services later expand the deal scope.

Services, however, are projected to grow at a 23.61% CAGR from 2026 to 2031, highlighting the difficulty of operationalizing taxonomy systems inside complex organizations. Enterprises often require integration design, taxonomy curation, model training, and change management before they can trust outputs in real workflows. Gloat’s March 2026 launch of its Agentic HR Platform, with 2.4 million skill nodes and 18.7 million skill relationships, illustrates how ontology depth drives demand for expert configuration and governance support. Similarly, TechWolf’s June 2024 funding round, backed by SAP, Workday, and ServiceNow, reinforced confidence that specialist taxonomy infrastructure can coexist with large-suite ecosystems rather than being displaced. This dynamic supports a market structure in which software anchors revenue, while services grow faster as buyers move from pilot deployments to enterprise-wide programs.

By Deployment Model: Cloud Delivery Dominates As Hybrid Configurations Emerge

Cloud-based deployment held 68.92% of the skills intelligence and taxonomy platform market share in 2025, reflecting operational advantages such as faster updates, lower infrastructure burden, and stronger support for real-time data ingestion. Cloud architectures are particularly well-suited to skills platforms because their value depends on frequent refreshes from collaboration, learning, recruiting, and project data. This makes cloud delivery the most practical model for organizations seeking continuous inference rather than periodic workforce surveys. The ability to roll out quickly across geographies and business units also matters, as buyers increasingly demand visible value within current budget cycles, explaining why greenfield deployments now favor cloud over on-premises alternatives.

Cloud deployments are forecast to expand at a 24.83% CAGR through 2031, keeping this segment ahead of the broader market. Microsoft’s People Skills expansion in March 2026 demonstrated how skills intelligence is being embedded into daily work systems where cloud delivery is already the norm. At the same time, on-premises environments remain relevant in defense, government, and sensitive healthcare settings where data control is a board-level requirement. Hybrid models are emerging as a middle path, particularly in the banking, financial services, insurance, and energy sectors, where organizations want cloud inference without fully relinquishing control over employee records. Over time, the balance between passive work-signal capture and real-time ontology updates continues to favor the cloud, ensuring this deployment model maintains its lead even as hybrid demand persists in regulated or sovereignty-sensitive contexts.

By End User Enterprise Size: Large Enterprises Lead But SME Adoption Accelerates

Large enterprises held 74.13% of the 2025 market, reflecting the complexity of their role structures, the number of systems they need to connect, and the scale advantages they bring to model training. These organizations typically manage broader job architectures and more fragmented talent data, making the case for a unified skills graph easier to justify. In the skills intelligence and taxonomy platform market, large enterprises also have the budgets and governance capacity to support multi-phase deployments across regions and functions. Their demand is reinforced by the need to standardize skills and language across hiring, internal mobility, performance, and learning systems that were often implemented at different times. This is why the segment remained the revenue center in 2025, even as smaller organizations began entering the market more actively.

SMEs are projected to grow at a 25.72% CAGR through 2031, signaling that adoption is spreading beyond the largest and most resource-rich buyers. This shift reflects the rise of modular, API-ready offerings that reduce entry costs and shorten the path to an initial use case. SMEs can often move faster because they have fewer systems to reconcile and narrower role architectures to map at the outset. Vendors are also making the segment more accessible through pre-built templates and lighter implementation paths that ease setup burdens. LinkedIn’s 2026 Talent Velocity Report highlighted that only a small minority of organizations currently lead in talent architecture maturity, leaving broad whitespace across mid-sized employers seeking better internal visibility and mobility. As pricing models become more flexible and skill frameworks easier to configure, SMEs are expected to play a steadily larger role in the skills intelligence and taxonomy platform market over the forecast period.

By Application: Talent Management Anchors Demand While Workforce Planning Surges

Talent management and internal mobility accounted for 29.34% of the skills intelligence and taxonomy platform market size in 2025, confirming this as the most established commercial use case. Enterprises see immediate value in matching people to open roles, projects, and career paths, which provides clearer near-term payback than more strategic applications. Internal mobility also aligns directly with retention goals, workforce utilization, and reduced dependence on external recruiting, making it a natural entry point for adoption, especially in large organizations with talent marketplaces or structured career frameworks. The segment’s leading position in 2025 reflects the maturity of demand rather than a ceiling on future opportunity.

Strategic workforce planning is forecast to grow at a 26.41% CAGR from 2026 to 2031, making it the fastest-growing application within the market. Buyers increasingly want forward-looking modeling to estimate capability gaps, redeployment needs, and training priorities before business change exposes them. This shift elevates workforce planning to a board-level concern, as skills gaps remain the primary barrier to transformation for many employers. Learning and development continues to serve as an important middle layer, connecting assessed gaps to targeted content and credential pathways rather than broad catalog consumption. Recruitment, performance, succession, and analytics still generate meaningful demand pockets, but the strongest momentum is toward applications that let organizations model future talent risk rather than just report current conditions. This transition positions the skills, intelligence, and taxonomy platform market as a broader strategic enabler of workforce planning, not just a supporting HR tool.

By End User Industry Vertical: Technology Leads As Healthcare Accelerates

Information technology and telecommunications accounted for 24.82% of the skills intelligence and taxonomy platform market share in 2025, reflecting how quickly capability requirements shift across software, cloud, data, and cybersecurity roles. In these environments, job titles lose value quickly because tools, methods, and certifications evolve rapidly. As a result, technology-led organizations have become an early and reliable customer base, needing dynamic visibility into current and adjacent skills. These buyers also tend to have stronger digital foundations, making it easier to integrate work data, learning systems, and talent processes into a unified skills layer. That combination of rapid skill change and better data readiness explains why technology remained the largest vertical by revenue in 2025.

Healthcare and life sciences are expected to grow at a 27.12% CAGR through 2031, the fastest pace among verticals. Growth is driven by clinical competency documentation, licensing, accreditation, and patient safety requirements that demand structured records of workforce capabilities. In regulated settings, skills data becomes part of operating discipline and compliance readiness rather than just an efficiency tool. Banking, financial services, and insurance also remain strong adopters, as workforce risk, auditability, and specialized role requirements make skills visibility valuable beyond routine HR administration. Manufacturing and industrial operations are gaining relevance as automation increases demand for documented trade skills, safety certifications, and hybrid human-machine work patterns. The education and government sectors present mid-term opportunities, as public skills frameworks and national workforce programs encourage the use of standardized taxonomies. Together, these trends broaden the vertical base of the skills intelligence and taxonomy platform market beyond its earlier concentration in knowledge-worker industries.

Geography Analysis

North America held 41.61% of the skills intelligence and taxonomy platform market share in 2025, making it the largest region worldwide. The region benefits from a dense ecosystem of enterprise HR technology vendors, implementation partners, and early adopters of skills-based operating models. The United States remains the central demand engine because large employers in technology, financial services, and consulting face recurring pressure from fast-changing role requirements and internal mobility expectations. Canada is following a similar path through digital skills investment and enterprise modernization, while Mexico remains at an earlier stage, with adoption concentrated among multinational employers. In the skills, intelligence, and taxonomy platform market, North America continues to lead because commercial readiness, software ecosystem depth, and enterprise budgets are more closely aligned here than in any other region.

Asia-Pacific is the fastest-growing regional segment, with the market projected to rise at a 28.51% CAGR from 2026 to 2031. Growth in the region is supported by government-backed reskilling programs in Singapore, India, and South Korea, which are normalizing structured skills frameworks across both public and private workforce initiatives. Policy support helps create employer demand for standardized taxonomy tools instead of isolated internal competency models. Europe remains a major revenue contributor, but its demand pattern is shaped more heavily by regulation and compliance than by discretionary productivity spending. Regulatory activity has increased the importance of auditable, structured workforce data across the region, giving Europe a demand profile in which procurement is often triggered by governance and reporting needs as much as by talent-optimization goals.

South America remains an earlier-stage opportunity, with Brazil and Argentina as the main commercial entry points. Adoption is still led mainly by multinational subsidiaries extending global HR platforms into regional operations rather than by large volumes of locally originated procurement. The Middle East is developing faster, especially in Saudi Arabia and the UAE, where national workforce transformation programs are creating demand for structured skills mapping and localized taxonomy support. Africa is at the earliest stage, with South Africa, Nigeria, and Kenya showing initial momentum across financial services, telecommunications, and workforce development initiatives. Across these emerging regions, the market is being shaped more by policy-led workforce documentation and modernization agendas than by the enterprise-led efficiency logic that dominates in North America.

Competitive Landscape

The skills, intelligence, and taxonomy platform market is moderately fragmented, with pure-play specialists such as Eightfold AI, Gloat, TechWolf, and 365Talents competing alongside broader HCM suite vendors and labor market intelligence providers. No single company holds a controlling position, and the presence of more than 20 meaningful vendors indicates an active field where differentiation matters more than simple scale alone. This structure creates room for specialists who can deliver deeper ontology coverage, greater inference precision, or better workflow integration than broad-suite features can. It also means pricing power is uneven, because buyers can compare specialist capabilities with lighter embedded skills layers in larger platform suites. The result is a competitive environment where product depth and ecosystem fit often determine vendor success more than brand size by itself.

Strategic moves in 2025 and 2026 reveal two clear market patterns: deeper agentic AI integration and stronger ecosystem embedding. Gloat launched its Agentic HR Platform in March 2026, featuring a skills graph with 2.4 million skill nodes and 18.7 million skill relationships, positioning the platform as infrastructure for AI-led workforce task allocation. Eightfold AI followed in May 2026 with TalentForge, a suite trained on more than 1 billion career trajectories that supports dynamic taxonomy generation, talent matching, and AI-agent-ready APIs. Phenom’s February 2026 acquisition of Be Applied added AI hiring fairness and structured interviewing capability, strengthening its position with buyers focused on auditability and governance readiness. These moves show that the market is not only expanding but also redefining competitive advantage around explainability, workflow automation, and agent-ready skill infrastructure.

A partnership strategy is equally important because enterprise procurement increasingly favors vendors that can integrate with established software ecosystems. TechWolf’s June 2024 funding round from SAP, Workday, and ServiceNow clearly reflected this, as major incumbents backed specialist taxonomy infrastructure rather than replicating it internally. This suggests that ontology depth and inference quality are difficult to reproduce quickly within normal suite release cycles, leaving space for best-of-breed providers. At the same time, white-space opportunity remains strong in manufacturing and industrial settings, where many current platforms still require major customization to model trade skills, safety certifications, and physical competency benchmarks accurately. As agentic AI, interoperability, and embedded workflow support mature further, the market will likely remain fragmented, but competitive gaps will be defined more clearly by domain depth and platform integration strength.

Skills Intelligence And Taxonomy Platform Industry Leaders

Eightfold AI Inc.

Beamery Inc.

Degreed, Inc.

Phenom People, Inc.

Gloat Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launches TalentForge, a skills intelligence suite trained on more than 1 billion career trajectories, offering real-time talent matching, dynamic taxonomy generation, and AI-agent-ready skills APIs. The launch positions Eightfold as direct infrastructure for enterprises building agentic HR workflows and expands the platform's capability set beyond traditional talent matching.

- April 2026: Phenom acquired Be Applied, a UK-based AI hiring fairness and structured interviewing platform. The acquisition adds algorithmic bias mitigation and EU AI Act-compliant decision audit capabilities to Phenom's skills and talent experience platform, directly addressing a critical compliance requirement for European buyers operating under the Act's high-risk AI provisions.

- March 2026: Gloat launched its Agentic HR Platform, featuring a skills graph containing 2.4 million skill nodes and 18.7 million skill relationships. The platform is designed to serve as the skills intelligence substrate for AI agents managing real-time workforce task allocation and project staffing across large enterprise environments.

- March 2026: Degreed launched LENS 2026, an enhanced learning intelligence layer that connects skills gap assessments directly to curated content recommendations and third-party credentialing pathways. The update extends taxonomy coverage to emerging AI, sustainability, and hybrid human-AI collaboration skill domains.

Global Skills Intelligence And Taxonomy Platform Market Report Scope

The skills intelligence and taxonomy platform market is expanding as enterprises shift from static job descriptions to dynamic skills-based models. Demand is driven by internal mobility, compliance, and workforce planning needs, with cloud-first deployments and large enterprises leading adoption while SMEs and regulated sectors accelerate future growth.

The Skills Intelligence and Taxonomy Platform Market is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), End User Enterprise Size (Large Enterprises, and SMEs), Application (Talent Management and Internal Mobility, Strategic Workforce Planning, L and D, Recruitment and Talent Acquisition, Performance and Succession Management, and Skills Gap Analysis and Workforce Analytics), End User Industry Vertical (IT and Telecommunications, BFSI, Healthcare and Life Sciences, Manufacturing and Industrial Operations, Retail and E-commerce, Education, Government and Public Sector, Energy and Utilities, and Media and Entertainment), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts Are Provided in Terms of Value (USD).

| Platform Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Talent Management and Internal Mobility |

| Strategic Workforce Planning |

| Learning and Development (L&D) |

| Recruitment and Talent Acquisition |

| Performance and Succession Management |

| Skills Gap Analysis and Workforce Analytics |

| Information Technology (IT) and Telecommunications |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial Operations |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Energy and Utilities |

| Media and Entertainment |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Platform Software | |

| Services | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Application | Talent Management and Internal Mobility | |

| Strategic Workforce Planning | ||

| Learning and Development (L&D) | ||

| Recruitment and Talent Acquisition | ||

| Performance and Succession Management | ||

| Skills Gap Analysis and Workforce Analytics | ||

| By End User Industry Vertical | Information Technology (IT) and Telecommunications | |

| Banking, Financial Services, and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial Operations | ||

| Retail and E-commerce | ||

| Education | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Media and Entertainment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast market size for skills intelligence and taxonomy platforms?

The market was valued at USD 1.85 billion in 2025, is valued at USD 2.17 billion in 2026, and is projected to reach USD 5.67 billion by 2031 at a 21.18% CAGR.

What is driving adoption of skills intelligence and taxonomy platforms in large enterprises?

Large enterprises led with 74.13% of 2025 demand because they manage complex role structures, fragmented HR systems, and broad internal mobility needs that require a governed skills graph.

Which application area is growing the fastest through 2031?

Strategic workforce planning is the fastest-growing application, advancing at a 26.41% CAGR as employers seek forward-looking visibility into future capability gaps and redeployment needs.

Why is cloud deployment becoming the preferred model?

Cloud led with 68.92% of 2025 revenue and is growing at a 24.83% CAGR because it supports continuous model updates, passive work-signal capture, and faster integration with enterprise SaaS tools.

Which region offers the strongest growth opportunity over the forecast period?

Asia-Pacific is the fastest-growing regional opportunity at a 28.51% CAGR, supported by reskilling programs and broader institutional demand for standardized skills frameworks.

Which verticals are shaping product demand most strongly?

Information technology and telecommunications led with 24.82% of 2025 revenue, while healthcare and life sciences is growing the fastest at 27.12% CAGR because regulated competency documentation creates durable demand.

Page last updated on: