Employment Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 50.75 Billion |

| Market Size (2031) | USD 109.29 Billion |

| Growth Rate (2026 - 2031) | 16.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employment Platform Market Analysis by Mordor Intelligence

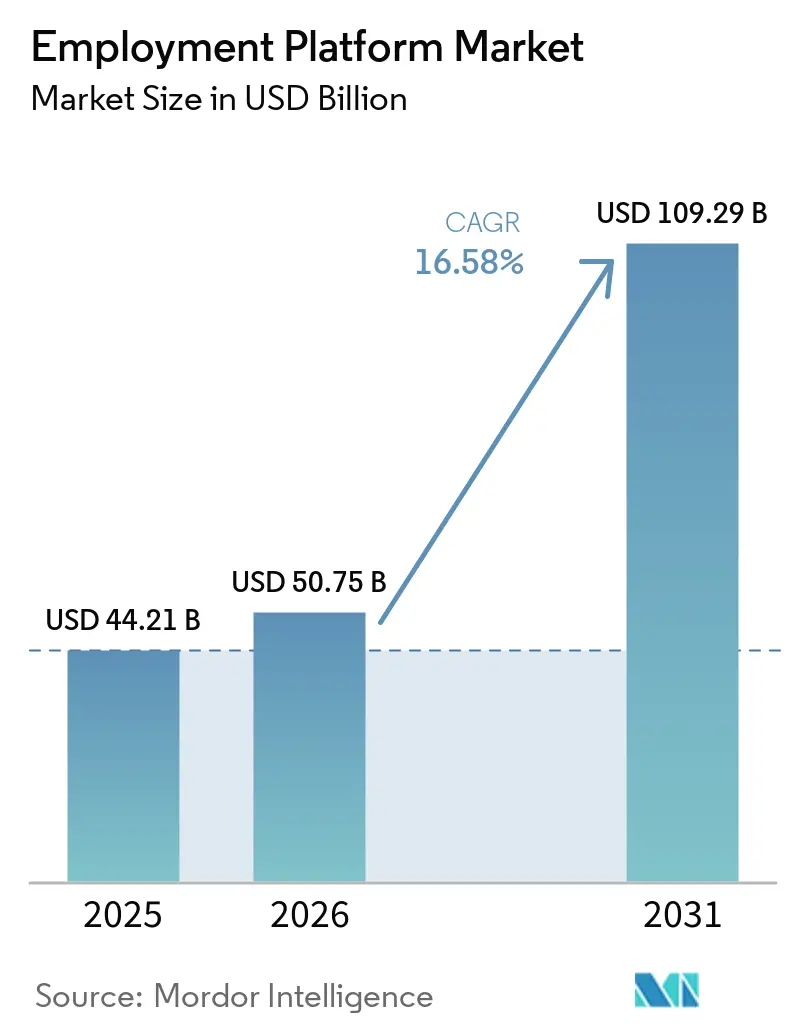

The employment platform market size is projected to be USD 44.21 billion in 2025, USD 50.75 billion in 2026, and reach USD 109.29 billion by 2031, growing at a CAGR of 16.58% from 2026 to 2031. This expansion reflected a broad shift in how employers sourced, screened, and hired workers, as manual and fragmented recruiting processes gave way to integrated digital systems. Recruiter urgency also remained high because competition for AI-skilled talent kept vacancy costs elevated and pushed employers toward tools that could shorten hiring cycles and improve candidate fit. The employment platform market was also being shaped by salary transparency rules, cross-border hiring needs, and skills-first frameworks, which expanded platform relevance beyond traditional job posting. Providers responded by investing in proprietary matching layers, deeper workflow coverage, and stronger employer tools that improved retention and pricing power. The result was a market where scale still mattered, but long-term advantage depended more on data depth, automation quality, and the ability to support employers across the full hiring process.

Key Report Takeaways

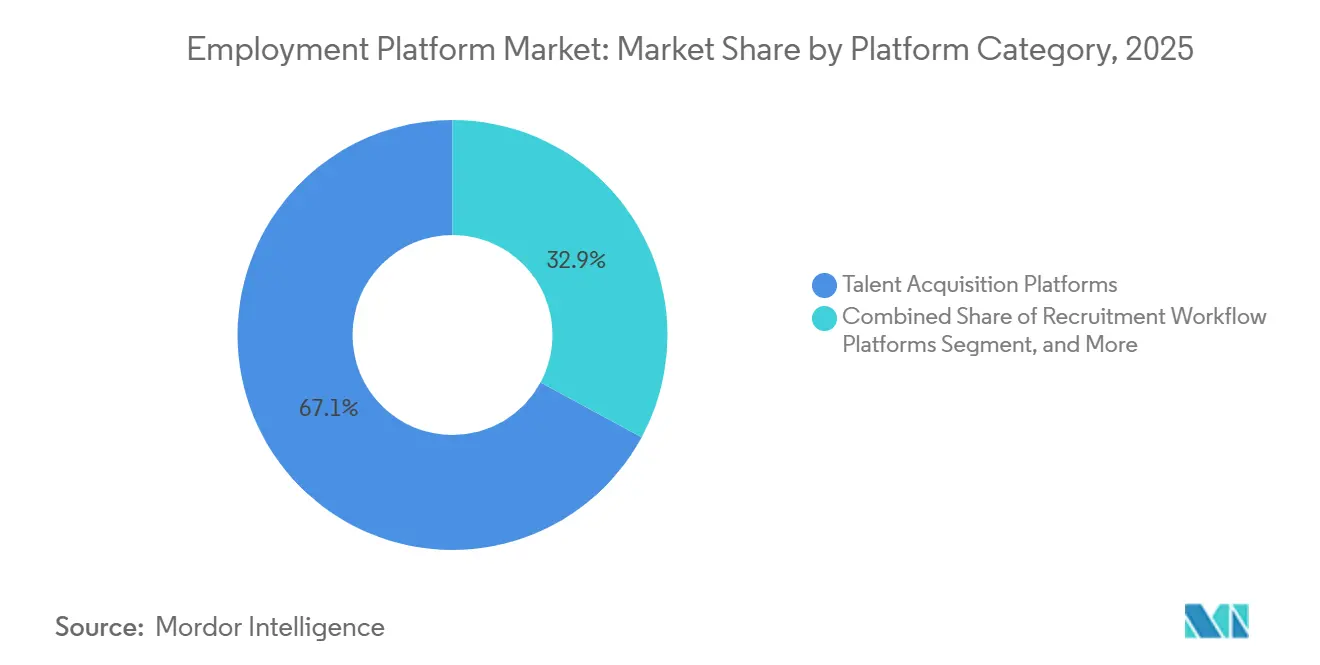

- By platform category, the employment platform market was led by talent acquisition platforms, which accounted for 67.12% of revenue in 2025, while recruitment workflow platforms are projected to expand at a 19.63% CAGR through 2031.

- By employment type, permanent employment held 62.47% share in 2025, while freelance and gig employment is projected to grow at a 21.28% CAGR through 2031.

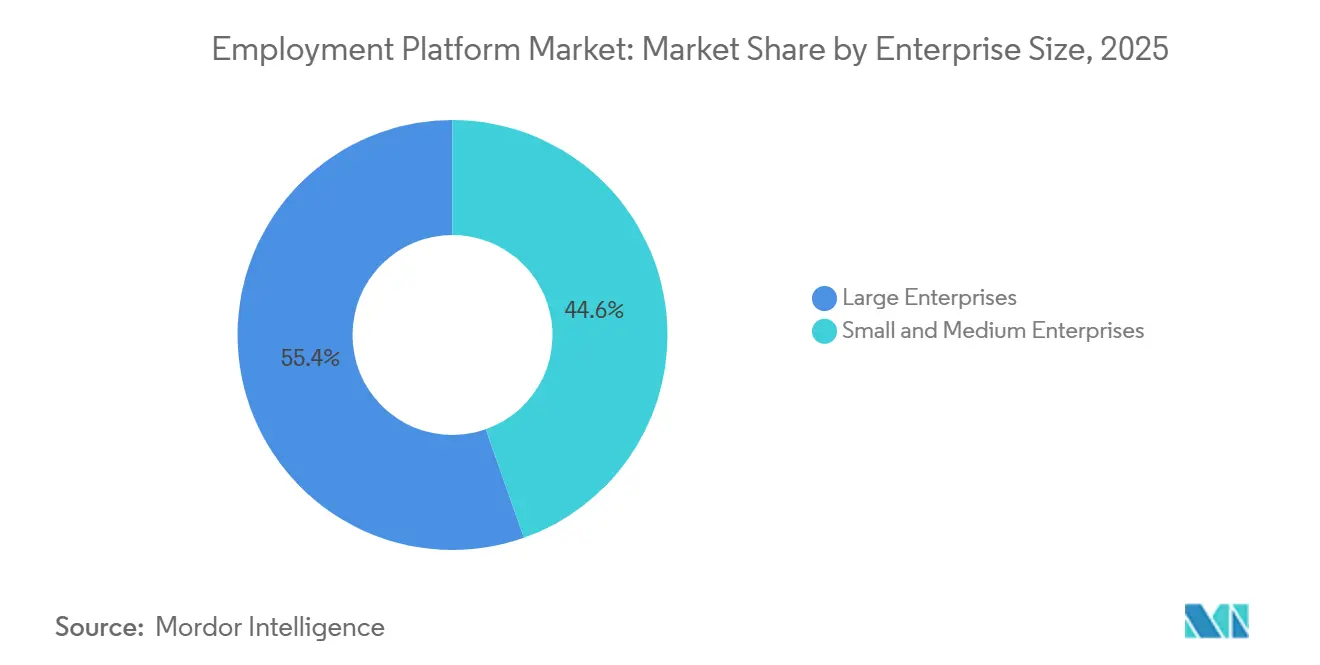

- By enterprise size, large enterprises accounted for 55.39% share of the employment platform market size in 2025, while small and medium enterprises are projected to expand at a 20.14% CAGR through 2031.

- By industry vertical, information technology and telecom accounted for 26.71% of the the employment platform market share in 2025, while healthcare and life sciences are projected to grow at a 22.36% CAGR through 2031.

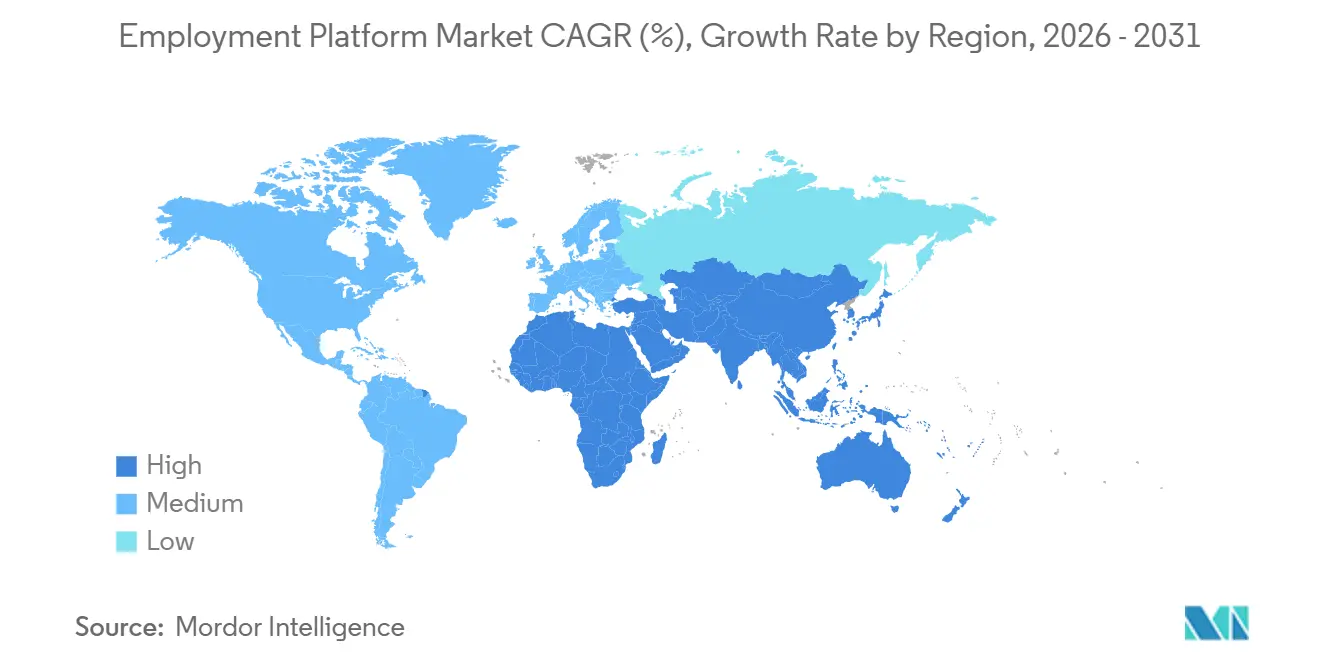

- By geography, North America accounted for 39.82% share of the employment platform market size in 2025, while Asia-Pacific is projected to record the fastest regional growth at a 23.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employment Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization Of Hiring Workflows | +4.1% | Global, with concentrated acceleration in North America, Western Europe, and APAC core | Short term (≤ 2 years) |

| Skills-First Hiring Adoption | +3.3% | North America and EU primary, spill-over to APAC and MEA | Medium term (2-4 years) |

| AI-Skills Scarcity And Recruiter Urgency | +2.6% | Global, with sharpest intensity in North America, UK, Germany, India, and Australia | Short term (≤ 2 years) |

| SME Adoption Of Subscription And Self-Serve Hiring Tools | +1.9% | Global, with early gains in US, India, and Southeast Asia | Medium term (2-4 years) |

| Salary Transparency Laws Expanding Apply Conversion | +1.2% | North America and EU, early gains in Australia and Canada | Medium term (2-4 years) |

| Cross-Border And Foreign-Talent Hiring Support Needs | +0.8% | Global, with concentrated demand in North America, EU, and GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitization of Hiring Workflows

Digitization of end-to-end hiring workflows remained the strongest structural demand driver for the employment platform market, as employers increasingly sought to consolidate sourcing, screening, scheduling, assessment, and onboarding within a single connected environment. The move away from standalone posting tools also changed how buyers evaluated vendors, since platforms were expected to improve process speed and candidate quality rather than simply expand application volume. Bullhorn reported in 2026 that only 10% of recruitment firms had AI embedded throughout their workflows, underscoring the significant automation runway still available across the addressable base.[1]Bullhorn, “2026 Recruitment Industry Trends Report,” Bullhorn, bullhorn.com As these workflows became more digital, platforms also accumulated richer match data, which over time improved recommendation quality and raised switching costs for employers already operating at scale. ZipRecruiter stated in May 2026 that its next-generation AI engine, deployed across the marketplace, drove a 37% increase in application volume for exposed job seekers, reinforcing the commercial case for continued workflow investment across the employment platform market.

Skills-First Hiring Adoption

Skills-first hiring created a clear shift in demand in the employment platform market, as employers increasingly sought tools to assess capability directly rather than rely solely on degrees, titles, or resume keywords. TestGorilla reported that 85% of employers globally used some form of skills-based assessment in 2025, up from 81% in 2024, indicating that this hiring model had moved from pilot to mainstream employer behavior.[2]TestGorilla, “The State of Skills-Based Hiring 2025,” TestGorilla, assets.ctfassets.net That shift favored platforms that could map candidate competencies to role needs in real time and support verification within the hiring workflow, rather than leaving employers to stitch together outside tools. OneTen and Ipsos found in 2025 that 86% of hiring managers supported skills-first approaches, but only 1 in 3 applied them consistently, underscoring the significant implementation headroom that still existed for vendors that could simplify execution. Providers that combined skills taxonomies, verification, screening logic, and internal mobility functions were therefore better placed to capture spending from employers whose stated intent was ahead of day-to-day practice.

AI-Skills Scarcity and Recruiter Urgency

Shortages of AI-capable professionals continued to increase recruiter urgency across the employment platform market, as employers grew less tolerant of long vacancy periods in software, cloud, data, and cybersecurity roles. Recruit Holdings stated in May 2026 that Indeed recorded a record number of users in March 2026 and that AI recommendations and tools accounted for 70% of applications, underscoring how central intelligent matching had become in mainstream recruitment behavior. Reporting on Korea's Ministry of Employment and Labor data, Asiae noted in March 2026 that 172,000 people found employment through the country's AI job matching service by the end of 2025, up 66% year on year.[3]Korean Ministry of Employment and Labor, “AI Job Matching Service Data,” Asiae, asiae.co.kr Kanzahun reported that revenue from AI-related roles on Boss Zhipin grew more than 100% in Q1 2026, while software engineer job postings rose 10.9% year on year from January through April 2026, underscoring that demand for AI talent on digital hiring platforms was still accelerating. This urgency supported higher-value premium placement, matching, and recruiter productivity features, allowing leading vendors to improve yield without depending only on growth in listing counts.

SME Adoption of Subscription And Self-Serve Hiring Tools

Small and medium enterprises became a more important source of expansion in the employment platform market because affordable subscription models lowered the threshold for using professional recruiting software. ManpowerGroup reported in Q3 2025 that 67% of organizations globally were already using AI in hiring, onboarding, or training, and that adoption reached 80% in Asia-Pacific, a region with high SME density and deepening platform use. Info Edge reported in May 2026 that Naukri.com had more than 55,000 billed customers in Q4 FY2026, and that over half of them were SMEs, confirming that smaller businesses were becoming a meaningful paid customer base rather than just a top-of-funnel audience. Vendors that offered modular pricing, transparent self-serve onboarding, and clear per-posting or subscription economics were converting these buyers faster than legacy enterprise sales models allowed. As that pattern widened across markets, recurring SME revenue began to complement the larger, but less frequent, spending cycles of large enterprise customers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy And Candidate Consent Compliance | -1.7% | EU primary, spill-over to North America, Australia, and India | Medium term (2-4 years) |

| Skills-First Hiring Execution Gaps Inside Employers | -1.1% | Global, with pronounced gaps in North America and APAC core | Medium term (2-4 years) |

| High-Risk AI Compliance Burden In Recruitment Workflows | -0.8% | EU and UK primary, APAC increasingly affected | Long term (≥ 4 years) |

| AI-Enabled Candidate Fraud And Identity Spoofing | -0.5% | Global, with highest incidence in remote-first hiring markets in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Candidate Consent Compliance

Data privacy and candidate consent requirements remained a material restraint on the employment platform market, as platforms handling applicant data across multiple jurisdictions had to build additional control layers into their core product architecture. European rules governing automated decision-making, transparency, and oversight in hiring systems increased the baseline compliance burden for vendors that relied on AI-driven screening and ranking tools. The user-provided draft also noted that non-compliance fines could start at EUR 10 million (USD 11.3 million) or 2% of annual global turnover, meaning compliance spending had become a minimum cost of participation for both smaller and larger providers. Platforms, therefore, had to fund consent withdrawal tools, access request exports, audit trails, and documentation layers that did not directly improve front-end hiring experience but were necessary for operating credibility. That shifted investment away from feature velocity and gave better-capitalized incumbents a structural edge in a market where regulatory readiness increasingly influenced enterprise buying decisions.[4]Regulation (EU) 2024/1689, “Artificial Intelligence Act,” EUR-Lex, eur-lex.europa.eu

Skills-First Hiring Execution Gaps Inside Employers

Employer-side execution gaps slowed monetization in the employment platform market, as many organizations still struggled to implement skills-first hiring consistently after publicly endorsing it. OneTen and Ipsos found in 2025 that 86% of hiring managers supported skills-first approaches, but only 1 in 3 used them consistently across teams, which limited the throughput available to advanced assessment and matching tools. When employers continued to default to resume-led and credential-led screening practices, the value case for premium skills modules weakened, and upsell conversion slowed. The friction was especially visible in fields such as financial services, law, and healthcare, where formal credentials remained deeply embedded in hiring culture and internal approval processes. Platform vendors, therefore, faced a change-management problem as much as a product problem, since stronger technology alone could not fully unlock demand until employer behavior changed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Category: Talent Acquisition Scale Anchors Revenue While Workflow Tools Drive Future Growth

Talent acquisition platforms held a 67.12% share in 2025 and accounted for the largest pool of demand in the employment platform market, supported by the scale of job boards, career portals, recruitment marketplaces, and professional networking platforms. These channels remained the volume backbone because they still delivered candidate reach that workflow tools could not match on a standalone basis. Their position was also reinforced by long-standing employer integrations and large candidate databases built over years of repeated hiring activity. Recruit Holdings confirmed in February 2026 that Indeed had integrated with ChatGPT, showing how a major incumbent was extending sourcing reach into AI-native discovery environments to defend share and keep candidate access broad.\

Recruitment workflow platforms are projected to expand at a 19.63% CAGR from 2026 to 2031, making them the fastest-growing part of the employment platform market by platform category. Applicant tracking systems remained the most common workflow layer, but competitive pressure increasingly shifted toward interviewing, candidate assessment, employer branding, and recruitment marketing tools. ZipRecruiter reported in May 2026 that its AI engine increased application volume by 37% for exposed job seekers, supporting employer demand for workflow products tied to measurable process outcomes rather than simple posting exposure. Upwork's 2025 acquisitions of Bubty B.V. and Ascen Inc. showed how platform providers were moving into enterprise contingent workforce management and broader hiring operations, adding workflow depth beyond marketplace matching alone.

By Employment Type: Permanent Roles Hold Scale While Gig Models Change Platform Economics

Permanent employment represented 62.47% of the employment platform market size in 2025, which reflected the higher value and frequency of full-time hiring across technology, finance, healthcare, and manufacturing. Employers continued to rely on these platforms for repeated headcount additions, especially in functions where vacancy costs were high and specialized skills were hard to secure quickly. Part-time employment platforms operated under a different model, with retail, hospitality, and logistics buyers placing greater weight on the speed of fill, location coverage, and repeat local hiring. Contract and temporary hiring also remained relevant as employers faced macroeconomic uncertainty and sought labor flexibility without making long-horizon workforce commitments.

Freelance and gig employment platforms are projected to grow at a 21.28% CAGR through 2031, making them the fastest-growing employment type in the employment platform market. Payoneer and Upwork extended their 15-year partnership in May 2026 and began exploring stablecoin-enabled payouts across Africa, Asia-Pacific, Europe, South America, and the Middle East, showing that freelance platforms were evolving into cross-border work and payment infrastructure rather than simple listing marketplaces. Fiverr reported in April 2026 that AI consulting categories and AI development services grew 118% year on year in Q1 2026, indicating that project-based hiring demand was concentrated in advanced digital work, where employers often preferred flexible engagement models. That pattern increasingly blurred the boundary between freelance marketplaces and enterprise talent sourcing, forcing traditional full-time hiring platforms to respond to competition from adjacent markets.

By Enterprise Size: Large Enterprises Lead Spend While SMEs Narrow The Gap

Large enterprises accounted for 55.39% of the employment platform market in 2025, as centralized HR teams, multi-market operations, and more stringent compliance requirements drove larger software subscriptions and higher premium posting budgets. These buyers typically favored integrated suites that combined sourcing, applicant tracking, interviewing, and analytics instead of isolated point solutions. Their preference for full-stack buying helped sustain longer contract terms and higher average revenue per account across the employment platform market. Large technology-intensive companies remained especially active users because they continued to fill specialized roles at a pace that required an always-on digital hiring infrastructure.

Small and medium enterprises are projected to grow at a 20.14% CAGR through 2031, reflecting how lower-cost SaaS models have widened access to recruiting capabilities that were previously concentrated in enterprise HR teams. Self-serve onboarding, modular packages, and subscription pricing made it easier for smaller firms to adopt formal hiring tools without long procurement cycles or dedicated implementation teams. ManpowerGroup reported in Q3 2025 that 67% of organizations used AI in hiring, onboarding, or training, and that usage reached 80% in Asia-Pacific, which supported the view that smaller business adoption was broadening in markets with dense SME populations. Info Edge stated in May 2026 that Naukri.com had more than 55,000 billed customers in Q4 FY2026, with more than half being SMEs, reinforcing the commercial depth of this customer segment in the employment platform market.

By Industry Vertical: Technology Leads Current Spend While Healthcare Builds The Fastest Momentum

Healthcare and life sciences are projected to grow at a 22.36% CAGR from 2026 to 2031, while information technology and telecom held 26.71% of the employment platform market share in 2025, which kept technology as the largest revenue center at the start of the forecast period. Healthcare demand was strengthened by structural shortages in nursing, physician, and related clinical roles, which pushed employers toward always-on sourcing systems rather than occasional campaigns. The sector also required licensure checks, privacy controls, and geographic compliance that generalist platforms often handled less effectively, leaving room for more specialized products. That combination of labor scarcity and workflow complexity made healthcare one of the clearest specialization opportunities inside the employment platform market.

Information technology and telecom remained the heaviest users of digital hiring infrastructure because employers in this vertical continued to recruit under tight time pressure for software, cloud, AI, and cybersecurity roles. KANZHUN reported that revenue from AI-related roles on BOSS Zhipin more than doubled in Q1 2026 and that software engineer postings rose 10.9% year on year from January through April 2026, which supported the view that technology hiring activity remained intense on major digital platforms. BFSI, identified in the user-provided draft as the second-largest vertical by platform spend, continued to value background verification and credential checks within workflow design, while retail and e-commerce prioritized high-volume, low-cost hiring tools for hourly labor. Industrial manufacturing and public sector demand also created space for platforms with stronger sourcing of skilled trades, multilingual capabilities, and structured compliance support.

Geography Analysis

North America held 39.82% of the employment platform market share in 2025, making it the largest regional revenue base. The region benefited from a mature digital hiring infrastructure in the United States and a high concentration of large employers in technology and financial services that maintained steady sourcing demand. A November 2025 NBER working paper found that pay transparency laws increased the share of job postings with disclosed salary ranges by 30 percentage points and raised wages by up to 3.6%, directly supporting platform conversion dynamics tied to clearer compensation disclosure. The Federal Reserve Bank of New York reported in October 2025 that more than two-thirds of US job postings included salary information, up sharply from 2018, showing how quickly employer posting behavior had shifted under layered state-level requirements. Canada and Mexico added to regional demand through multilingual sourcing needs in Canada and manufacturing-led hiring momentum in Mexico.

Europe remained a market where compliance readiness strongly influenced product selection and vendor trust. The EU AI Act classified recruitment AI as high-risk and brought transparency obligations into force from August 2, 2026, increasing implementation work while also creating an advantage for vendors able to demonstrate conformity sooner than peers. Germany, the UK, and France anchored regional demand, and post-Brexit cross-border complexity in the UK increased employer interest in platforms with employer-of-record and broader international hiring support. South America remained earlier stage, but Brazil and Argentina were moving faster on formal digital hiring and SME adoption of subscription tools, making the region a credible longer-run opportunity set.

Asia-Pacific is projected to expand at a 23.47% CAGR through 2031, giving the employment platform market its fastest regional growth profile. Growth in the region reflected the combination of large labor pools, fast-formalizing labor markets, and strong investment in AI-assisted matching systems. KANZHUN reported Q1 2026 revenue of CNY 2,068.8 million (USD 284 million) and more than 72 million monthly active users on BOSS Zhipin, showing the scale possible in China's digitally native hiring environment. Info Edge reported in May 2026 that Naukri.com hosted more than 115 million resumes and logged nearly 960,000 average daily resume searches in Q4 FY2026, reinforcing India's position as one of the highest-velocity hiring environments. South Korea's AI Jobs surpassed 8 million cumulative applications within its first year, while Saudi Arabia, Nigeria, and South Africa kept the Middle East and Africa important as earlier-stage but strategically relevant markets for mobile-first and white-collar platform growth.

Competitive Landscape

The employment platform market remained fragmented globally, but competition tightened in the premium tier where AI matching quality, proprietary candidate data, and workflow breadth mattered most. Large platforms benefited from strong network effects because they operated across job boards, professional communities, and workflow products simultaneously. Regional specialists also held defensible positions where local employer relationships, language fit, and regulatory familiarity were central to buyer trust. Recruit Holdings reported record-high Indeed user numbers in March 2026 and stated that AI recommendations and tools drove 70% of applications, demonstrating how deeply intelligent matching had already been embedded across leading operators. That combination of scale and data kept entry barriers meaningful even as new AI-native vendors entered the field.

Strategy patterns across the employment platform market centered on AI embedding, international hiring support, and expansion into broader workforce management. ZipRecruiter launched its ChatGPT app in March 2026 and rolled out an AI engine that lifted application volume by 37% for exposed job seekers, demonstrating how distribution and matching were both being redesigned for AI-native discovery. Upwork expanded beyond its core freelancer marketplace through its 2025 acquisitions of Bubty B.V. and Ascen Inc., while its May 2026 partnership extension with Payoneer pointed to deeper cross-border payout infrastructure and stronger enterprise service ambition. Fiverr reported 118% year-on-year growth in AI consulting and AI development services in Q1 2026, signaling that platform competition was moving toward AI-human hybrid work delivery rather than simple task listing volume. These moves showed that the strongest providers were trying to own more of the hiring, work delivery, and payment stack.

White-space opportunities remained strongest in skills verification, healthcare-specific compliance workflows, and cross-border hiring tools for SMEs that could not justify the costs of enterprise-grade employer-of-record services. Emerging AI sourcing agents also began to challenge traditional subscription models by identifying and contacting passive candidates beyond traditional job board flows. The employment platform industry, therefore, combined broad fragmentation with concentrated pockets of premium capability, where product integration and investment pace mattered more than simple geographic coverage. Providers that could connect sourcing, screening, compliance, payments, and branded candidate engagement were better positioned to widen their advantage as employer expectations continued to rise.

Employment Platform Industry Leaders

SEEK Limited

KANZHUN LIMITED

The Stepstone Group

ZipRecruiter, Inc.

Jobrapido S.r.l. Socio Unico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Payoneer and Upwork extended their 15-year strategic partnership, with Upwork joining as a Design Partner to explore stablecoin-enabled payouts across Africa, Asia-Pacific, Europe, South America, and the Middle East, addressing freelancer demand for faster, more flexible access to funds in emerging markets.

- May 2026: Indeed, operated by Recruit Holdings, launched "Job City by Indeed" on Roblox in partnership with Super League, an immersive game-based experience designed to help players build and assess in-demand workplace skills that can be showcased on their Indeed profiles, the initiative marks a new candidate acquisition channel targeting the Gen Z workforce pipeline.

- May 2026: KANZHUN Limited reported Q1 2026 revenues of CNY 2,068.8 million (approximately USD 284 million), up 7.6% year-on-year, with monthly active users exceeding 72 million. Revenue from AI-related roles on BOSS Zhipin grew over 100% year-on-year, reflecting the platform's accelerating monetization of AI-skills demand in China's labor market.

- May 2026: Info Edge (India) Limited reported Q4 FY2026 results for Naukri.com, with recruitment business billings reaching INR 811 crore (approximately USD 97 million) and operating margins of 58.5%, the platform hosted over 115 million resumes and logged approximately 960,000 average daily resume searches, with management highlighting increased AI deployment across matching and recommendation engines.

Global Employment Platform Market Report Scope

The employment platform market comprises digital solutions and services that enable organizations to manage recruitment, talent acquisition, and workforce engagement across employment types, including permanent, part-time, contract, temporary, and freelance or gig roles. These platforms encompass talent acquisition tools such as job boards, recruitment marketplaces, gig work platforms, and social recruiting networks, as well as recruitment workflow systems like applicant tracking, candidate assessment, and recruitment marketing solutions. Serving both large enterprises and small and medium-sized enterprises, they are deployed across industries including BFSI, healthcare and life sciences, information technology and telecom, retail and e-commerce, industrial manufacturing, government and public sector, and other end-user industries. The core purpose of this market is to streamline hiring processes, reduce recruitment costs, enhance candidate experience, and provide data-driven insights to improve workforce planning and talent management.

The employment platform market report is segmented by Platform Category (Talent Acquisition Platforms, [Job Boards and Career Portals, Recruitment Marketplaces and Talent Matching Platforms, Freelance and Gig Work Platforms, and Social and Professional Recruiting Platforms] and Recruitment Workflow Platforms [Applicant Tracking Systems, Interviewing and Candidate Assessment Platforms, and Recruitment Marketing and Employer Branding Platforms), Employment Type (Permanent Employment, Part-time Employment, Contract and Temporary Employment, and Freelance and Gig Employment), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Talent Acquisition Platforms | Job Boards and Career Portals |

| Recruitment Marketplaces and Talent Matching Platforms | |

| Freelance and Gig Work Platforms | |

| Social and Professional Recruiting Platforms | |

| Recruitment Workflow Platforms | Applicant Tracking Systems |

| Interviewing and Candidate Assessment Platforms | |

| Recruitment Marketing and Employer Branding Platforms |

| Permanent Employment |

| Part-time Employment |

| Contract and Temporary Employment |

| Freelance and Gig Employment |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Platform Category | Talent Acquisition Platforms | Job Boards and Career Portals |

| Recruitment Marketplaces and Talent Matching Platforms | ||

| Freelance and Gig Work Platforms | ||

| Social and Professional Recruiting Platforms | ||

| Recruitment Workflow Platforms | Applicant Tracking Systems | |

| Interviewing and Candidate Assessment Platforms | ||

| Recruitment Marketing and Employer Branding Platforms | ||

| By Employment Type | Permanent Employment | |

| Part-time Employment | ||

| Contract and Temporary Employment | ||

| Freelance and Gig Employment | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Industry Vertical | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the employment platform market in 2026 and what is the 2031 outlook?

The employment platform market stood at USD 50.75 billion in 2026 and is forecast to reach USD 109.29 billion by 2031, growing at a 16.58% CAGR over 2026-2031.

What is driving growth in employment platforms?

The main forces are digitization of hiring workflows, wider use of skills-based hiring, strong demand for AI-skilled talent, and faster adoption of subscription tools by SMEs.

Which platform category leads revenue and which one is growing fastest?

Talent acquisition platforms led with 67.12% share in 2025, while recruitment workflow platforms are projected to grow the fastest at a 19.63% CAGR through 2031.

Why are freelance and gig hiring platforms expanding faster than other employment types?

Freelance and gig platforms are projected to grow at 21.28% CAGR because employers increasingly use project-based hiring, cross-border talent access, and flexible payment models for AI and digital work.

Which region offers the strongest growth prospects through 2031?

Asia-Pacific is projected to grow the fastest at a 23.47% CAGR, supported by large labor pools, formalizing labor markets, and strong investment in AI matching tools.

How are AI and regulation changing competition among platform providers?

AI is pushing vendors to improve matching, workflow automation, and candidate discovery, while privacy and high-risk AI rules are raising compliance costs and favoring better-capitalized providers.

Page last updated on: