Market Overview

| Study Period | 2020 - 2031 |

|---|---|

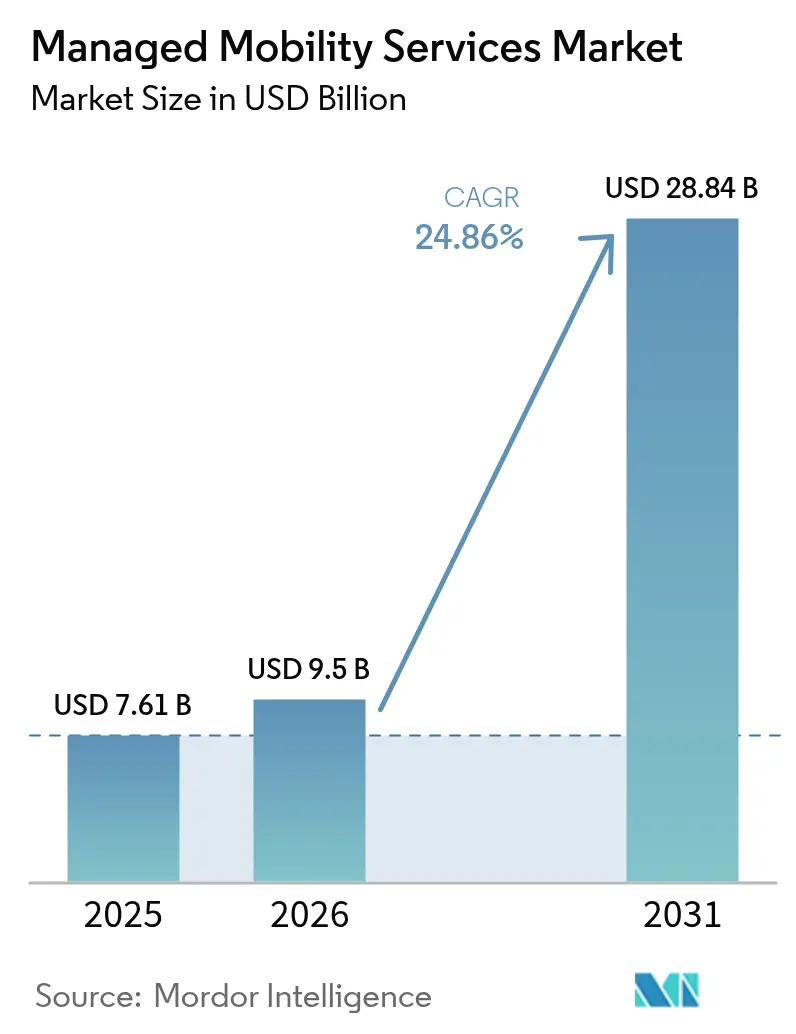

| Market Size (2026) | USD 9.5 Billion |

| Market Size (2031) | USD 28.84 Billion |

| Growth Rate (2026 - 2031) | 24.86% CAGR |

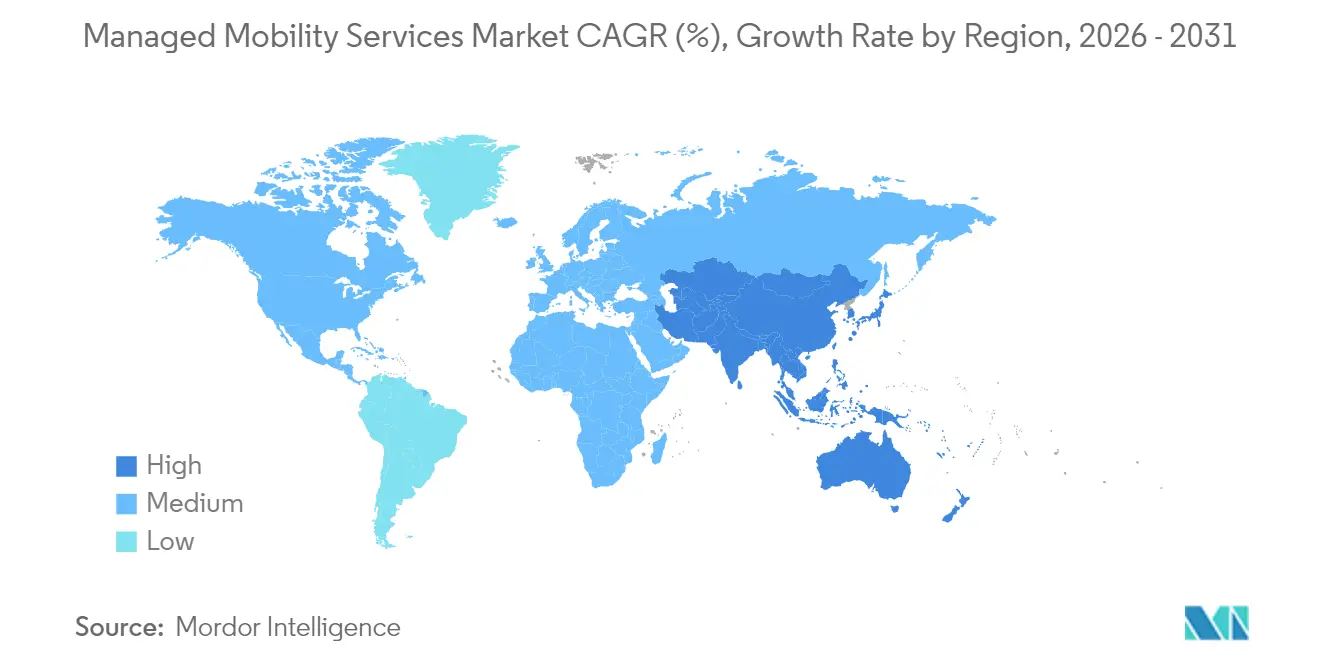

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Mobility Services Market Analysis by Mordor Intelligence

The managed mobility services market size is expected to grow from USD 7.61 billion in 2025 to USD 9.5 billion in 2026 and is forecast to reach USD 28.84 billion by 2031 at 24.86% CAGR over 2026-2031. Growth stems from organizations outsourcing complex mobility lifecycles as hybrid work becomes permanent, employee-owned devices multiply, and AI-enabled cloud platforms simplify endpoint orchestration. Accelerated bring-your-own-device adoption, rapid cloud migration, and unified security demands together fuel new service contracts while telecom operators, software providers, and niche vendors compete to deliver differentiated value propositions that cut support costs and sharpen workforce productivity. Intensifying demand for zero-touch onboarding through eSIM provisioning plus predictive support technologies further expands addressable revenue pools within the managed mobility services market.[1]Microsoft, “What’s New in Microsoft Intune,” microsoft.com

Key Report Takeaways

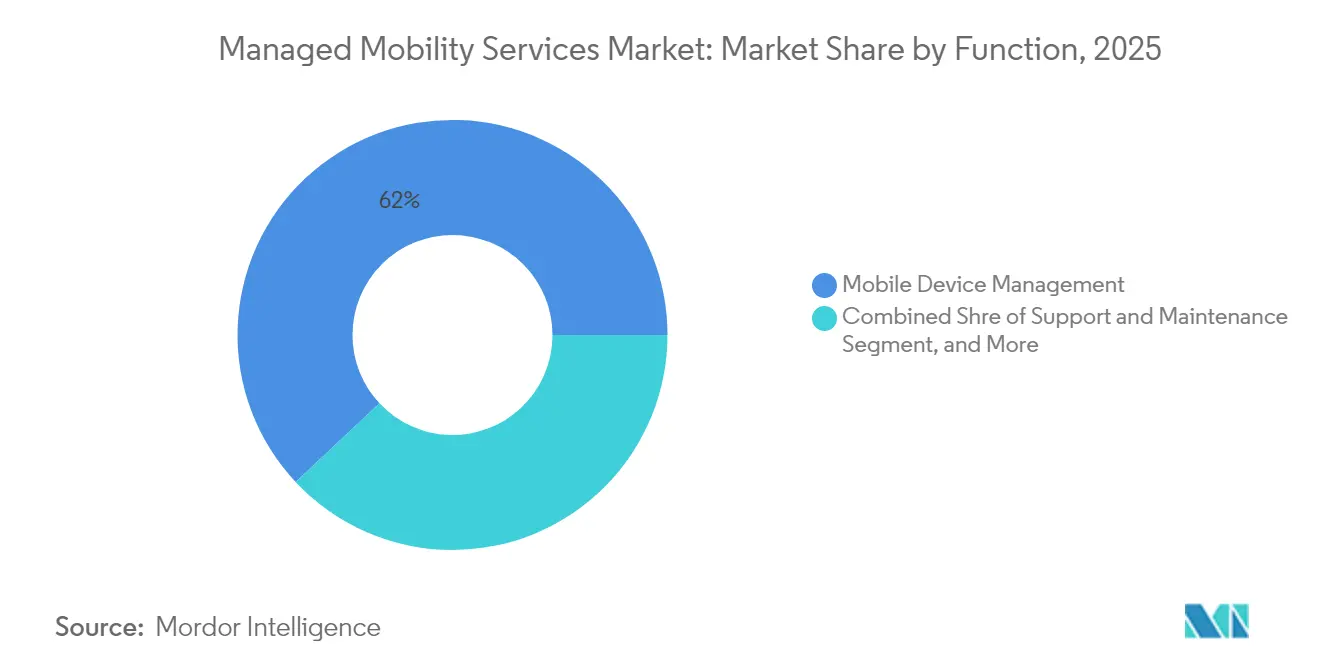

- By function, mobile device management led with 61.98% of managed mobility services market share in 2025 and mobile application management is on track to grow at a 26.64% CAGR to 2031.

- By deployment model, cloud-based services captured 68.15% of the managed mobility services market size in 2025 and are anticipated to expand at a 26.92% CAGR through 2031.

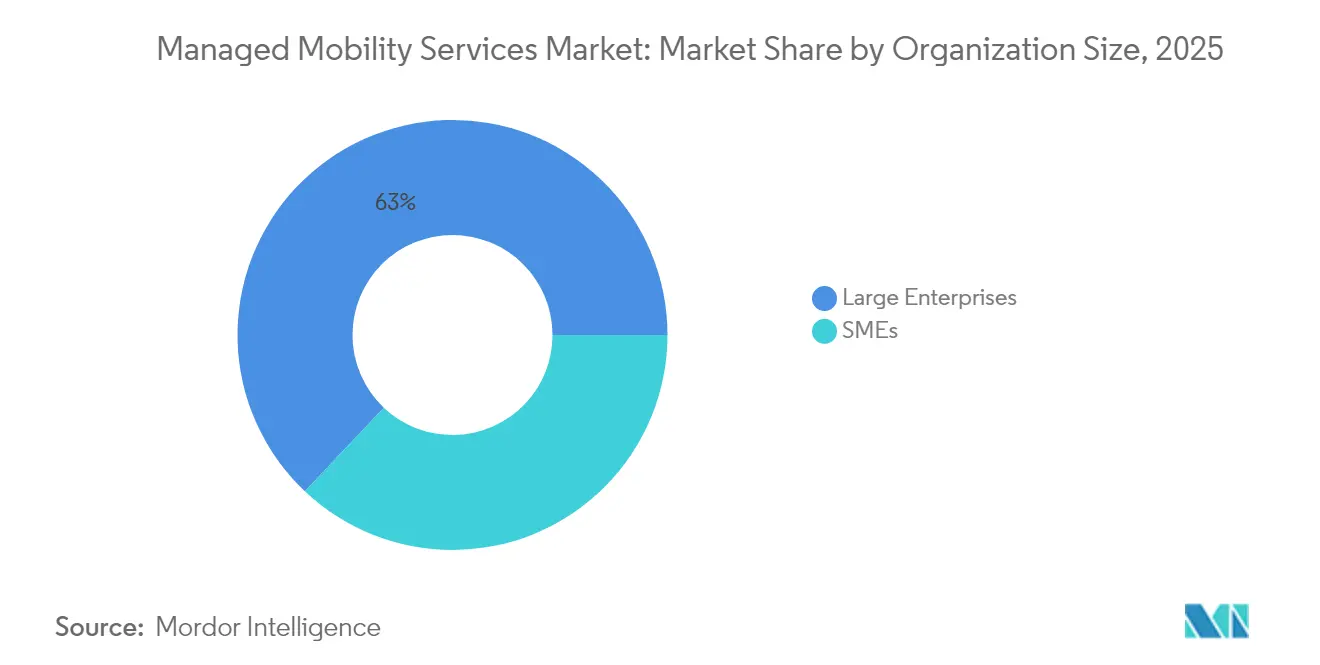

- By organization size, large enterprises accounted for 62.95% revenue share in 2025 in the managed mobility services market, whereas small and medium enterprises will post the fastest 26.7% CAGR through 2031.

- By end-user industry, IT and telecom retained the highest 28.55% share in 2025 in the managed mobility services market and healthcare is positioned for a 26.05% CAGR through 2031.

- By geography, North America held 39.35% share of the managed mobility services market size in 2025 while Asia-Pacific is projected to advance at a 26.21% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Managed Mobility Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BYOD proliferation and hybrid-work normalization | +6.2% | Global, with North America and Europe leading adoption | Short term (≤ 2 years) |

| Outsourcing of IT and mobility lifecycle to cut TCO | +5.8% | Global, with SME segment driving growth in APAC | Medium term (2-4 years) |

| Rapid cloud adoption enabling scalable MMS delivery | +4.9% | Global, with cloud-first markets leading | Short term (≤ 2 years) |

| Need for unified security and compliance across endpoints | +4.1% | North America and EU regulatory markets, expanding globally | Medium term (2-4 years) |

| eSIM/iSIM and remote SIM-OTA fueling zero-touch global fleets | +2.3% | APAC core, spill-over to global enterprise fleets | Long term (≥ 4 years) |

| AI-driven predictive support slashing device downtime | +1.8% | Advanced markets initially, scaling to emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BYOD proliferation and hybrid work normalization

Firms now manage unprecedented endpoint diversity because 80% of employees access corporate data from personal devices, a scenario that stretches internal IT teams beyond practical limits.[2]IBM Security, “MaaS360 Mobile Device Management,” ibm.com Cyber-risks rise when unmanaged smartphones and tablets handle sensitive files, so enterprises seek external specialists able to impose policy uniformity without limiting user freedom. Managed mobility services market vendors respond with containerization and real-time threat detection that secure data in motion and at rest. Demand rises fastest among knowledge-intensive industries where productivity gains offset device heterogeneity. Service providers that can blend security, user experience, and regulatory compliance stand to win large multiyear contracts as hybrid work policies solidify.

Outsourcing of IT and mobility lifecycle to cut TCO

Budget ownership has shifted from capital to operating expense, making predictable subscription models attractive. Comparative studies show per-device support costs drop 30% when lifecycle tasks move to a multi-tenant provider that leverages automation and scale. Outsourcing frees overstretched IT teams for strategic digital programs while giving executives uniform dashboards for usage, compliance, and spend. The managed mobility services market therefore grows rapidly among mid-market companies that lack mobility specialists. Vendors win deals when they can prove measurable savings, rapid onboarding, and SLA-based quality metrics that outclass in-house alternatives.

Rapid cloud adoption enabling scalable MMS delivery

Cloud-native platforms remove infrastructure barriers once inherent to on-premises mobility suites. Global policy engines, API-based integrations, and elastic compute resources allow providers to onboard thousands of devices in minutes while pushing updates without service windows. Real-time analytics and machine learning generate predictive insights that flag battery failures, malware attempts, or policy violations. These advantages help the managed mobility services market penetrate highly distributed organizations that need consistent experiences across geographies. Cloud dominance also encourages rapid feature co-innovation because modules can be rolled out incrementally instead of through large version upgrades.

Need for unified security and compliance across endpoints

Healthcare entities bound by HIPAA, banks governed by PCI DSS, and European firms subject to GDPR all seek unified solutions that streamline audit readiness.[3]Philips, “Clinical Mobility Solutions,” philips.com Managed mobility partners now embed compliance rule-sets directly into device management workflows, automating evidence collection and alerting staff when settings drift from baseline. Integration with threat intelligence feeds enables proactive containment, reducing breach dwell time. Vendor differentiation rests on domain expertise in sector-specific regulations and the ability to demonstrate continuous rather than point-in-time compliance. That requirement underpins steady recurring revenue in the managed mobility services market.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived loss of operational control and cost visibility | -2.8% | Global, particularly affecting large enterprises | Short term (≤ 2 years) |

| Integration complexity with legacy infrastructure | -2.1% | North America and Europe with established IT systems | Medium term (2-4 years) |

| Rising SLA penalties from customization and high-touch support | -1.6% | Global, affecting service provider margins | Medium term (2-4 years) |

| Shortage of skilled mobility professionals | -1.3% | Global, with acute shortages in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Perceived loss of operational control and cost visibility

Executives hesitate to hand key mobility functions to third parties when budget accountability and live performance data appear opaque. Concerns grow when variable fees, custom reporting surcharges, or vendor lock-in clauses come to light during contract negotiations. Providers now counter by exposing granular dashboards, flexible exit options, and benchmark pricing to rebuild trust. Transparent governance frameworks and co-managed models help sustain momentum in the managed mobility services market even among risk-averse organizations.

Integration complexity with legacy infrastructure

Multinational firms still rely on on-premises mail servers, proprietary ERPs, and outdated directory services that lack modern APIs. Connecting cloud-based mobility suites to these systems can trigger multi-phase migrations, unexpected downtime, and unforeseen license costs. Providers that invest in tooling, professional services, and reference architectures reduce friction, yet integration hurdles still prolong sales cycles and inflate total project spend. Where compliance prohibits extensive refactoring, some customers postpone full outsourcing, constraining near-term market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Device management dominance faces application challenge

Mobile device management delivered 61.98% of the managed mobility services market share in 2025 because enterprises initially prioritized uniform policy enforcement, asset tracking, and remote wipe capabilities across smartphones, tablets, and rugged endpoints. Comprehensive control over firmware updates and encryption status made the device layer an indispensable foundation for compliance audits and incident response. However, the segment’s expansion rate now lags more agile application-centric options as organizations refine security to the data layer.

Mobile application management is forecast to post a 26.64% CAGR, the strongest among functional categories, as containerization separates corporate and personal contexts on BYOD hardware without intrusive full-device controls. Healthcare providers adopt app-level management to safeguard patient records while permitting clinicians to use personal phones, and financial institutions deploy secure app wrappers for mobile banking advisors. The shift encourages service vendors to bundle device, app, and content modules so clients avoid multiple contracts. Such convergence keeps the managed mobility services market adaptable to evolving endpoint threats and workforce expectations.

By Deployment Model: Cloud supremacy accelerates

Cloud solutions held 68.15% of managed mobility services market size in 2025 and they will maintain momentum with a 26.92% CAGR as enterprises seek elastic capacity, uniform policy propagation, and rapid feature rollout. Multi-tenant architectures offer economies of scale for patch distribution, analytics processing, and compliance reporting that on-premises stacks cannot match. CIOs also value geographic redundancy delivered through hyperscale data centers that satisfy uptime commitments without capital expenditure.

On-premises deployments persist in defense, public sector, and heavily regulated utilities that require data residency or air-gapped operations. Even within those verticals, hybrid models emerge where core identity stores remain on site but device telemetry and AI analytics reside in the cloud. Service providers therefore invest in flexible architectures with connectors that move workloads seamlessly across environments. This approach keeps their addressable universe broad as sovereignty rules evolve, reinforcing the managed mobility services market as a pragmatic pathway to unified endpoint oversight.

By Organization Size: SME segment disrupts traditional patterns

Large enterprises controlled 62.95% of revenue in 2025 because their global device fleets and strict compliance mandates justify comprehensive outsourcing agreements that bundle 24 x 7 support, analytics, and governance reporting. Complex mobility estates spanning corporate-owned and BYOD assets demand deep integration skills and broad geographic reach, capabilities typically found among tier-one providers.

Small and medium enterprises will, however, record the highest 26.7% CAGR as low-code onboarding portals, pay-as-you-grow pricing, and automated policy sets erase earlier barriers. Cloud marketplaces now let an organization with fewer than 200 seats deploy full device, app, and identity control in hours. Providers that pre-package vertical templates for retail, professional services, or manufacturing stand out by reducing configuration complexity. As adoption broadens, SME demand fuels a vibrant long-tail ecosystem within the managed mobility services market, opening space for regional specialists and born-in-the-cloud startups.

By End-user Industry: Healthcare mobility transformation accelerates

IT and telecom companies captured 28.55% of managed mobility services market size in 2025 because their field engineers, salesforces, and customer-service agents rely on always-connected devices for critical workflows. High device turnover and stringent service-level expectations make external lifecycle management attractive. Telecom operators also bundle internal know-how into commercial offerings, creating virtuous cycles of scale and product improvement.

Healthcare is set for a 26.05% CAGR as hospitals digitize clinical workflows and enforce electronic health record security. Bedside devices, medication scanners, and telehealth tablets require continuous updates and HIPAA-aligned safeguards that internal biomedical teams seldom have bandwidth to manage. Managed services relieve resource strain while embedding audit trails and encryption defaults. Manufacturing, BFSI, retail, and government segments each add steady volumes, reflecting tailored compliance drivers such as PCI DSS, OSHA mandates, and citizen identity protection. The diversity of needs encourages solution modularity, sustaining multipronged expansion across the managed mobility services market.

Geography Analysis

North America retained 39.35% share in 2025 because early BYOD acceptance, mature cloud adoption, and stringent privacy rules together encouraged investment in full-featured managed programs. Enterprises routinely integrate mobile threat defense, secure connectivity, and analytics within unified contracts, raising average deal values. Public sector demand also rises as agencies modernize service delivery while satisfying FedRAMP and CJIS mandates, all of which magnify regional revenue pools for the managed mobility services market.

Asia-Pacific will advance at a 26.21% CAGR, the fastest worldwide, underpinned by industrial digitalization, government smart city agendas, and multifaceted e-commerce ecosystems. China’s domestic cloud champions bundle mobility services with 5G private networks, while India’s IT service integrators extend global best practices to local SMEs eager for remote support. ASEAN nations invest in workforce mobility to streamline tourism border checks, logistics corridors, and financial inclusion programs that rely on robust endpoint security. These varied deployments deepen regional expertise and attract fresh capital into the managed mobility services market.

Europe records steady growth due to GDPR enforcement, digital identity schemes, and demand for sovereignty-compliant clouds. Enterprises adjust procurement to favor providers that host telemetry within the bloc and can certify ISO 27001 compliance. Although budget cycles remain cautious, repeat contract renewals sustain predictable momentum. South America and the Middle East and Africa exhibit emerging demand as mobile broadband penetration climbs and multinational firms roll out standardized policies across affiliates. Capacity building by regional telecoms further enlarges the managed mobility services market footprint.

Competitive Landscape

The managed mobility services market remains moderately fragmented because telecom operators, global software houses, and pure-play mobility specialists each command pockets of influence without a single firm surpassing 15% revenue. Telecommunications incumbents leverage network assets and existing enterprise bill-of-materials to cross-sell lifecycle management packages, often bundling voice, data, and device financing into unified invoices. Software-centric players focus on platform extensibility, leaning on vast ISV communities to tailor workflows and analytics. Niche providers compete on deep vertical knowledge, for instance clinical mobility or rugged industrial device fleets, which larger peers sometimes overlook.

Strategic alliances escalate. Kyndryl partners with Microsoft to merge cloud scale and managed service expertise, allowing joint pursuit of multinational frameworks that integrate Intune with legacy on-premises identity stacks. Samsung SDS collaborates with chipset makers to optimize firmware for remote diagnostics, while Philips Healthcare aligns with hospital IT to certify medical-grade devices inside broader endpoint estates. Such partnerships convert technology synergies into market share wins by shortening deployment times and reducing integration risk.

Innovation remains the prime differentiator. AI-enabled predictive maintenance halves support tickets at several early adopters, prompting providers to embed machine learning in every incident management tier. Edge computing use cases such as offline compliance checks inside oil rigs or naval vessels create new premium service niches. Providers that translate technical advances into verifiable productivity and risk-reduction metrics secure multiyear renewals, raising switching costs and reinforcing competitive positioning across the managed mobility services market.

Managed Mobility Services Industry Leaders

Orange S.A.

AT&T Inc.

Fujitsu Limited

Kyndryl Holdings, Inc.

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Microsoft released Intune upgrades adding AI compliance monitoring, automated threat response, and deeper Microsoft 365 security integration.

- November 2024: Kyndryl expanded its Microsoft alliance to accelerate AI service delivery across managed mobility engagements.

- October 2024: Samsung SDS unveiled an integrated enterprise mobility suite featuring predictive support for multi-device environments.

- September 2024: Philips Healthcare launched clinical mobility solutions combining medical device integration and robust patient data safeguards.

Global Managed Mobility Services Market Report Scope

Managed mobility services (MMS) are defined as the procurement, deployment, and management of mobile devices and apps and PC software and services, connecting out-of-office workers to the enterprise environment. The options for allied services range from short-term post-go-live assistance to long-term application operations. Managed mobility services (MMS) market for the study defines the revenues generated from functions such as mobile device management, mobile application management, mobile security, and other functions that are being used in various end-user industries worldwide. The scope of the study is limited only to the services offered in the market for mobility management. The study also analyses the overall impact of COVID-19 on the ecosystem. The study includes qualitative coverage of the most adopted strategies and an analysis of the key base indicators in emerging markets.

The managed mobility services market is segmented by function (mobile device management, mobile application management, mobile security), deployment (cloud and on-premise), end-user industry (IT and telecom, BFSI, healthcare, manufacturing, retail, education), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Rest of Europe), Asia-Pacific (China, India, Japan, and the rest of Asia-Pacific), Latin America (Brazil, Argentina, Mexico, and the rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and the rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

By Function

| Mobile Device Management |

| Mobile Application Management |

| Mobile Security Management |

| Support and Maintenance |

By Deployment Model

| Cloud-based |

| On-premises |

By Organization Size

| Large Enterprises |

| Small and Medium-Sized Enterprises |

By End-user Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Manufacturing |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Function | Mobile Device Management | ||

| Mobile Application Management | |||

| Mobile Security Management | |||

| Support and Maintenance | |||

| By Deployment Model | Cloud-based | ||

| On-premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By End-user Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Education | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the managed mobility services market by 2031?

The market is projected to reach USD 28.84 billion by 2031, reflecting a 24.86% CAGR during 2026-2031.

Which function will expand the fastest over the forecast period?

Mobile application management is expected to grow at a 26.64% CAGR as enterprises shift to data-level controls.

Why are small and medium enterprises adopting managed mobility services quickly?

Cloud marketplaces, pay-as-you-grow pricing, and automated policy templates reduce complexity and support a 26.7% CAGR among SMEs.

Which region offers the highest growth potential for providers?

Asia-Pacific leads with a projected 26.21% CAGR driven by smart city initiatives and rapid smartphone penetration.

How do eSIM and remote SIM provisioning benefit global enterprises?

They enable zero-touch activation across borders, reducing logistics delays and roaming costs while simplifying fleet scaling

Page last updated on: